ABSTRACT

This paper proposes the strategy of container shipping industry in the foreseeable future. Container shipping presently encounters challenges such as excess container capacity, low-freight rate, high-fuel cost, and eco-efficient policy. In addition, the Fourth Industrial Revolution also affects the shipping industry via autonomous ship and reshoring phenomena. The hundreds of zettabytes big data enable deep-learning-based ship design as well as autonomous shipping; the various propulsion types become satisfied with the EEDI requirement; the small- and mid-sized containerships account for the significant portion of container fleets. By considering these key issues, the expectable changes are discussed for sustainable shipping.

Introduction

The sea is the world’s transportation route, and shipping accounts for more than 80% of international trade and 70% of its value. The worldwide seaborne trade volumes grew by approximately 1%; the merchant fleet growth has grown approximately 3% (United Nations, Citation2017). Because container shipping accounts for 15–20% every year, it is recognized as a significant industry (Lindstad, Asbjornslett, and Stromman Citation2016).

Standard containerization has led to innovative shifts in shipping and logistics (Cullinane and Khanna Citation2000). Currently, the metal box as a container is the product of various efforts by pioneers such as Malcom McLean, Seatrain, Alaska Steamship, and Matson Navigation. Four-corner fittings, twist-locks, cell guide, and hooking up the spreader by crane are key elements of the container system that enable innovation in logistics (Wijnolst and Wergeland Citation2009).

Since 2000, container shipping has been rapidly expanded by China’s economic growth. The increase of trade facilitated the expansion of the transportation capacity of containerships. The maximum capacity of a containership remained approximately 4,500 TEU for 10 years after 1984, but the proportion of containerships exceeding this size has increased from 9.6% in 1994 to 58.7% in 2000 (Cullinane and Khanna Citation2000). The maximum size has been steadily increasing from 15,500 TEU in 2006 to 18,000 TEU in 2015 and 22,000 TEU in 2018, and new categories such as post-panamax, neo-panamax, and ultra-large containerships have emerged (Tran and Haasis Citation2015).

The increase in containership capacity has led to the formation of an alliance between shipping companies. Because mega containerships caused high CAPEX (capital expenditure), shipping companies began to share business risks through shipping alliances (Cullinane and Khanna Citation2000). Such alliances bring three benefits: first, a cost reduction is obtained by joint service, the sharing and exchanging of shipping capacity, and joint investment in infrastructure; second, the expansion of service regions and the avoidance of surplus capacity can lead to transport competitiveness; third, alliance members can access the container market for a low cost and cooperate with partners to promptly respond to market changes (Ko et al. Citation2017). In 1997, the four strategic alliances, Sealand-Maersk Alliance, Tricon Alliance, Global Alliance, and Grand Alliance, accounted for 70% of the major trades between the East and West. Since April 2017, the three major alliances, 2M, Ocean Alliance, and The Alliance, have gained approximately 80% of the market share in container shipping. If the market changes in the future, the alliances will also be changed.

Container shipping encounters challenges such as excess containership capacity, low-freight rate, high-fuel cost, and implementation of environmental regulations. The slowdown in world trade growth led to a decline in container trade volume. Because the rate of increase of containership capacity became higher than that of container freight from 2009, it caused an imbalance of supply and demand in the container shipping market. In addition, because the proportion of over-8000 TEU-class containerships has been increased, mega containerships caused an excess of containership capacity and low-freight rate (Ko et al. Citation2017). Although the CCFI (China Containerized Freight Index) regained its uptrend after Q2 in 2016, high-fuel costs are still causing low profitability in the shipping sector. Meanwhile, the environmental regulations of the IMO (International Maritime Organization) have made significant changes in marine fuels, propulsion and auxiliary power supply (Faber et al. Citation2015).

The world’s current economic situation is changing the manufacturing and service regions of multinational companies (Brandon-Jones et al. Citation2017). Over the past few decades, most factory jobs have been relocated from high-cost to low-cost countries (Tate Citation2014). This phenomenon is called “offshoring” and is a popular strategy for improving the market competitiveness of Western manufacturers (Mauro et al. Citation2018). However, manufacturing companies have recently started to reconsider offshoring decisions and move business activities from high-cost locations to their homelands; this process is called “reshoring” (Brandon-Jones et al. Citation2017). In addition, the ICT (information and communication technology)-based Fourth Industrial Revolution has brought an improvement in productivity and sustainability in the manufacturing sector (Schwab Citation2016). This new paradigm may soon accelerate reshoring.

Ship oversupply, eco-friendly shipping, reshoring, and the Fourth Industrial Revolution seem to be causing significant changes in the shipping industry. These keywords are notable subjects in each discipline. However, there is a little investigation regarding the impact on container shipping in the macro view. Hence, this study investigates market changes with regard to autonomous ships, environmental regulation, and reshoring, and proposes a direction for development in container shipping. The remainder of this paper is organized as follows: Section 2 describes autonomous ships as well as the global trend towards their use; Section 3 explains the emission regulations and reduction strategy in the maritime sector; Section 4 analyzes the phenomenon of reshoring in the global market; Section 5 explores market changes and discusses a direction for development in container shipping; and Section 6 concludes this study.

Autonomous ship

The previous industrial revolutions changed the shipping industry notably. The introduction of steam engines was the basis for steamships with steel hull structures in the First Industrial Revolution. The Second Industrial Revolution brought the improvement of power efficiency through diesel engines, which are the most broadly used type of maritime propulsion machinery. The Third Industrial Revolution made the systematic shipping network, as well as satellite navigation via informatization.

Recently, the shipping industry has encountered changes brought by the Fourth Industrial Revolution. One such change is the paradigm shift of technological innovation by AI (artificial intelligence), robotics, the IoT (internet of things), and autonomous vehicles (Schwab Citation2016). Big data and the results of the Third Industrial Revolution have been combined with AI and the IoT technologies to enable smart shipping. Autonomous ships, e-Navigation, and smart ports are also representative innovations in the marine transportation sector.

Autonomous ships are the key elements of smart shipping. The definition of an autonomous ship is “next generation modular control systems and communications technology that will enable wireless monitoring and control functions both on and off board. These will include advanced decision support systems to provide a capability to operate ships remotely under semi or fully autonomous control” (Waterborne Citation2011). Autonomous ships have been variously referred to as unmanned ships, smart ships, remote control vessels, digital ships, and intelligent ships. However, the IMO has defined the ships as MASS (maritime autonomous surface ship) (International Maritime Organization Citation2018a). The concept of MASS may suggest an answer to the question that “can the ship navigate at sea for a lower cost?” In addition, it extensively relates to e-Navigation that integrates information on safety, security, and environmental protection while on a voyage (Burmeister et al. Citation2014). The 99th MSC (Maritime Safety Committee) dealt with MASSs and agreed to a schedule for developing regulatory scoping exercises and interim guidelines up to 2020 (International Maritime Organization Citation2018b). If the interim guidelines are implemented, technologically advanced countries such as Norway can permit the operation of MASSs.

The development of autonomous ships is aimed at economic, ecological, and social sustainability (Kretschmann, Burmeister, and Jahn Citation2017). The cost-effective and eco-friendly operation, productivity improvement, the optimization of logistics, the development of maritime infrastructures, and enhanced safety and security are expected to result. In particular, the electrification of propulsion systems has led to the reduction of crews. Because ship automation, at present, provides a sufficient environment for ship operation and control with 20 crew members, the number of crew members may be close to zero in the near future.

For the last decade, several projects of autonomous ships have launched: AAWA (Advanced Autonomous Waterborne Applications) by Rolls-Royce, the ReVolt project by DNV-GL, and MUNIN (Maritime Unmanned Navigation through Intelligence in Networks) by the EU (Kretschmann, Burmeister, and Jahn Citation2017). YARA and Kongsberg are cooperating to develop an autonomous feeder ship with a fully electric propulsion system (Rødseth Citation2017).

Environmental regulations

GHGs (greenhouse gases) and air pollutants remain challenges in terms of sustainable growth in the shipping industry. International shipping emitted an average of 210 million tons per year of CO2 from 2007 to 2012. It also caused 13% and 12% of the NOX and SOX, respectively, in global emissions (International Maritime Organization Citation2015). Containerships, bulk carriers, and tankers consume a large amount of hydrocarbon fuels, as they are major fleets. Containerships with a high proportion of hydrocarbon fuel consumption account for 24.25% of the CO2 from global shipping emissions.

The legislation of eco-friendly shipping has been implemented because of global warming and climate change. The IMO leads to the reduction of CO2, SOX, and NOX emissions by adopting the EEDI (energy efficiency design index) and ECAs (emission control area). In particular, the EEDI was re-emphasized as a mandatory requirement for newly built ships at the 72nd session of the MEPC (EC Citation2018); at that session, “the draft of the Initial IMO Strategy on Reduction of GHG Emissions from Ships” was adopted as Resolution MEPC.304(72) as the first step in the GHG reduction roadmap. The core contents are described in , including the vision, levels of ambition, and guiding principal (International Maritime Organization Citation2018c). In addition, the short-, mid-, and long-term measures with proceeding schedules and impacts on states were also discussed to achieve the initial strategy. In October 2018, follow-up actions were also considered at the 4th IMO ISWG (Intersessional Working Group)-GHG and 73rd MEPC sessions.

Table 1. Initial IMO strategy on the reduction of GHG emissions from ships.

The EEDI as an eco-efficiency policy in the marine transportation sector was introduced to improve the energy efficiency in a ship. The EEDI presents the ratio of economic benefits to environmental costs in ship operation; it calculates the CO2 emissions generated while a ship transports one ton of cargo for one nautical mile (Ahn et al. Citation2018). The attained EEDI values of all the merchant ships over 400 tons as gross tonnage must be less than each reference value. When deadweight is increased, the EEDI reference values become low; the values are also reduced by 10% for each phase (International Maritime Organization Citation2014). The time of implementation of each phase has been determined in the MEPC 74th session; here, the several issues of the shipping emission were discussed with regards to EEDI phase 3 and phase 4 requirements.

The shipping industry tries to satisfy the EEDI through the improvement of marine engines as well as through changes to marine fuels and propulsion types (DNV-GL Citation2015). There are many alternatives, such as a reduction of speed, trim optimization, hull cleaning, optimization of the propeller, alternative fuel, engine adjustment, on-board CCS (carbon capture and storage), and fuel cell propulsion (Ančić et al., Citation2015; Ahn et al. Citation2018; van den Akker, Citation2017). An alternative fuel is the most promising option. Because of the high HFO (heavy fuel oil) cost as well as the 2020 sulphur cap, LNG (liquefied natural gas) has become an alternative marine fuel. Passenger ships, gas carriers, and oil/chemical tankers have started to use the LNG and mega containerships have either an LNG-ready option or an LNG-fueled system to meet the demand for eco-friendly shipping (DNV-GL Citation2015).

Reshoring

Since NAFTA (North American Free Trade Agreement) in 1994, the manufacturing bases of labor-intensive industries from automobiles to washing machines moved to East Asian and Latin American countries. This phenomenon was called “offshoring”, in which manufacturing sites moved to overseas countries; this was a universal strategy for improving Western manufacturers’ competence for a long period. Although the distance between the manufacturer and the consumer was long, the manufacturer could have a competitive product with a low manufacturing cost (Mauro et al. Citation2018).

After the global financial crisis in 2008, offshoring was blamed for an increase in the unemployment rate and a decrease in the job openings in the United States (Cho et al. Citation2016). The Obama administration led to increased investment and value creation in the manufacturing industry starting in 2009. Meanwhile, the German government continuously facilitated domestic investment in the manufacturing sector; as a result of the policy, the growth rate of the German economy was recorded at 3.1%. This growth motivated other countries to encourage the domestic manufacturing industry. Since then, many manufacturing sites have returned to home countries or have moved to consuming countries. These processes are called “reshoring” and “on-shoring” and are new business strategies (Lee Citation2012).

The definition of reshoring is “the relocation back of value creation activities from offshore to the home country.” (Mauro et al. Citation2018). The major drivers of reshoring are the following challenges of offshoring:

Energy-supply risk,

Environmental and social sustainability,

Administrative costs,

Exchange rate fluctuation,

Supply chain risk,

High-fixed costs at local site (labor, real estate, intellectual property),

Lack of local infrastructure or skilled manpower,

Low production quality.

These environmental factors make manufacturing companies reconsider offshoring. The most prominent country participating in reshoring is the United States. The US government actively encourages incentives and tax benefits for home shoring and insourcing. In addition, the cost reduction of raw materials and the low cost of industrial electricity due to the shale gas supply support the reshoring phenomenon (Brandon-Jones et al. Citation2017).

The key technologies of the Fourth Industrial Revolution seem to accelerate the reshoring phenomena. One representative example is a smart factory built by the convergence of robotics, AI, the IoT, and blockchain. A smart factory does not require many low-cost laborers but rather only a few high-cost laborers. The skilled ICT persons, as high-cost laborers, can achieve high productivity and bring the cost down. Because developed countries have these ICTs, they can achieve higher efficiency in the manufacturing industry than in developing countries.

Strategy for container shipping

Ship automation is the foundation for autonomous containerships. Automation requires a large number of electrical and electronic elements for ship navigation, oceanic meteorology, telecommunication, traffic control, electronic nautical charts, and interconnected networks of on-board systems. A group of these electrical and electronic elements is called an ECU (electronic control unit). Along with the introduction of an electric propulsion system and advancement of operation and control, the ships will be more electrified and digitized than ships are currently. illustrates a vision of an autonomous containership that communicates with a satellite for navigation and collects shipping information via ECUs as well as electronic sensors. Shipping information, including weather conditions, service speed, ballast water level, fuel consumption, longitudinal strength of the hull, equipment conditions, and machinery vibration frequency, will gradually be generated from gigabytes to hundreds of zettabytes; this becomes big data that enables AI-based autonomous shipping. In addition, deep-learning-based ship design will be possible using big data.

Figure 1. Vision of an autonomous containership.

The emergence of autonomous containerships brings a change in the marine insurance business. Marine insurance is classified into H&M (hull and machinery) insurance and P&I (protection and indemnity) insurance. H&M premiums may rise, but P&I premiums may decline. The absence of a ship navigator may cause difficulty in responding to marine accidents. This means that the availability of other ships decreases and the risk of direct damage to the ship itself, which is the object of the insurance, increases. Because an autonomous containership has to be ready for a safe voyage, the H&M premium will rise. In contrast to the H&M insurance, shipping companies occupy the position of both insurer and insured in P&I insurance. The companies will demand various safety measures in an autonomous ship that can protect against damage from marine accidents. The measures can significantly reduce the frequency of an incident at sea; thus, the cost of risk management on indirect damage also decreases.

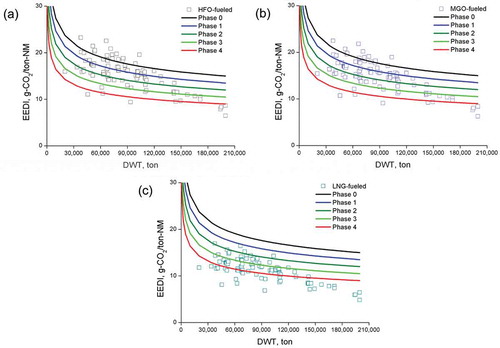

Future containerships will use different fuels based on their sizes. illustrates the EEDI values of the containerships that are in operation and owned by the top 10 container shipping companies. (A), (B), and (C) show the EEDI values of HFO-fueled engines, MGO (marine gas oil)-fueled engines, and LNG-fueled engines, respectively. Therein, it can be seen that fuel with a low carbon content satisfies EEDI requirements, which are gradually becoming stricter. Peculiarly, the mega containerships satisfy each EEDI phase even if they use HFO with high carbon content. This means that large-sized containerships have better energy efficiency than small-sized containerships. Therefore, ultra-large containerships over DWT 180,000 tons (approximately 16,000 TEU-class) are able to have HFO-fueled engines for mechanical propulsion. However, containerships under DWT 180,000 tons should have MGO- or LNG-fueled propulsion machinery to meet EEDI references. In particular, these ships must use LNG fuel in Phase 2 (2020–2024). Because LNG-fueled propulsion can comply with Phase 3 (2025–2039) and Phase 4 (after 2040), it is usable by all containerships. On the other hand, a carbon tax may burden shipping companies in terms of OPEX (operational expenditure), even though they satisfy the EEDI references; there is a need to develop a better more efficient marine engine than those presently available.

Figure 2. Attained and reference EEDI values for containerships.

Normally, container shipping is based on a regular route. A container liner is used for continuous and long-term transport because of the preplanned schedule and course. A major role of the containers is to transport complete products or half-finished goods. Container traffic has dramatically increased to transport these products because the economy of developing countries such as China has rapidly grown. This was the main cause of the emergence of mega containerships. However, because the rate of the increase of container capacity has become higher than that of container freight, a significant number of container liners are not fully loaded at sea. In addition, the container cargo volumes are slowing down due to the reshoring and on-shoring phenomena.

Economies of scale are a key precondition for the introduction of mega containerships. For the last several decades, the greater the use of the containership has been, the lesser the freight charge has become (Cullinane and Khanna Citation2000; van Hassel et al. Citation2016). There is no doubt about there are economies of scale for ocean-going large containerships (Tran et al., Citation2015). However, this is only valid for the freight charge while that containership is navigating at sea (van Hassel et al. Citation2016). Mega containerships cause the diseconomy of scale in terms of the efficient operation of container terminals (Notteboom et al. Citation2017) because the mega-ships need to stay in-port for a long time while loading and unloading a large amount of cargo. This means an increase in OPEX. In addition, the calling of mega-ships causes both rush and off-peak hours in ports (Tran and Haasis Citation2015); it leads to extra costs due to a delay in the use of cargo handling facilities. Additionally, as the capacity of a containership increases, the cost of in-land logistics becomes high (van Hassel et al. Citation2016). In summary, mega containerships always have the potential risk of the inefficiency of operation, over-tonnage, lower freight charges, and a decrease in profit (Tran and Haasis Citation2015).

The shipping alliances need a new strategy because of the slowdown of container transport and the diseconomy of mega-ships. The major three alliances by large shipping companies run a considerable number of containerships, from small feeders to ultra-large container ships. They have an unparalleled position in the transpacific, transatlantic, and Europe–Far East routes. However, they can encounter business risk due to the decrease of freight charges of 15,000 TEU-class mega containerships that account for 45% of all container fleets. Therefore, shipping companies need to prepare changes in shipping routes as well as logistic-chain planning. For example, it should be converted to satisfy the customer’s needs, from the low-speed operation of mega-sized ships to the high-speed operation of small- and mid-sized ships. The alliances should be transformed from the major company-centered organization into partnerships between small- and mid-sized regional companies.

Conclusions

This study proposed a sustainable strategy for container shipping in the near future. It is expected that the Fourth Industrial Revolution and environmental regulations will make container shipping become a smart industry beyond the capital- and labor-intensive businesses. Specifically, autonomous ships, eco-friendly shipping, and a reshoring phenomenon are the key phenomena that have brought about changes in container shipping. The shipping industry experiences unmanned maneuvering, near-zero GHG emission, and the high-speed small- and mid-sized ships in the near future. The scope of container shipping will be enlarged from cargo storage, loading and unloading, and transport to commercial trade, insurance, and idea-to-product. It is also possible that there will be specialized fleets to transport of post-Fordism products.

Big data from the operation of autonomous containerships will be the key element for deep-learning-based ship design. All the electronic sensors and ECUs gather the information on the shipping route, speed, and fuel consumption, and a shipowner will apply these databases to designing a new containership. This will maximize the ship owner’s profit while reducing costs. The quality of transport service will also become further improved.

The EEDI requirements have become stricter for eco-friendly shipping. Because of programs and timelines for meeting the IMO initial strategy, the energy-efficiency framework that is centered on EEDI and SEEMP (ship energy-efficiency management plan) needs to be improved. Considering the RSE (regulatory scoping exercise), the interim guidelines for autonomous ships and the GHG reduction strategy, container shipping seems to be the most affected sector. Containerships will use different fuels and propulsion machinery based on their sizes; the increase of small- and mid-sized containerships may lead to the growth of LNG consumption. The carbon taxation will be an enabler to make the shipping clean and the era of “beyond EEDI” needs to be considered.

Acknowledgments

This work is a result of the principal R&D program, “Preparation of R&D strategy for IMO core agenda and establishment of KRISO Global Cooperation System [PES3300]” which is supported by KRISO. The support is gratefully acknowledged.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Ahn, J., S. H. Park, S. Lee, Y. Noh, and D. Chang. 2018. “Molten Carbonate Fuel Cell (MCFC)-based Hybrid Propulsion Systems for a Liquefied Hydrogen Tanker.” International Journal of Hydrogen Energy 43: 7525–7537. doi:10.1016/j.ijhydene.2018.03.015.

- Ančić, I., and A. Šestan. 2015. “Influence of the Required EEDI Reduction Factor on the CO2 Emission from Bulk Carriers.” Energy Policy 84: 107–116. doi:10.1016/j.enpol.2015.04.031.

- Brandon-Jones, E., M. Dutordoir, J. Q. F. Neto, and B. Squire. 2017. “The Impact of Reshoring Decisions on Shareholder Wealth.” Journal of Operations Management 49–51: 31–36. doi:10.1016/j.jom.2016.12.002.

- Burmeister, H. C., W. Bruhn, Ø. J. Rødseth, and T. Porathe. 2014. “Autonomous Unmanned Merchant Vessel and Its Contribution Towards the e-Navigation Implementation: The MUNIN Perspective.” International Journal of e-Navigation and Maritime Economy 1: 1–13. doi:10.1016/j.enavi.2014.12.002.

- Cho, S. J., Y. S. Jang, H. S. Oh, J. H. Jeong, S. Hwang, and K. M. Kim. 2016. Global Manufacturing Network and Job Market Trends in East Asia (korean). Sejong: Korea Labor Institute.

- Cullinane, K., and M. Khanna. 2000. “Economies of Scale in Large Containerships: Optimal Size and Geographical Implications.” Journal of Transport Geography 8: 181–195. doi:10.1016/S0966-6923(00)00010-7.

- DNV-GL. 2015. Maritime in FOCUS – LNG as Ship Fuel, Latest Developments and Projects in the LNG Industry. Oslo: DNV-GL.

- European Commission. 2018. MEMO: 72nd session of the Marine Environment Protection Committee (MEPC 70) at the International Maritime Organization (IMO), Brussels.

- Faber, J., D. Nelissen, S. Ahdour, J. Harmsen, S. Toma, and L. Lebesque. 2015. Study on the Completion of an EU Framework on LNG-fuelled Ships and Its Relevant Fuel Provision Infrastructure. Brussels: European Commission.

- International Maritime Organization. 2014. Report of the Marine Environment Protection Committee on Its Sixty-Sixth Session, London.

- International Maritime Organization. 2015. Third IMO GHG Study 2014 Executive Summary. London: International Maritime Organization.

- International Maritime Organization. 2018a. “Regulatory Scoping Exercise for the Use of Maritime Autonomous Surface Ships (MASS).” Final Report: Analysis of Regulatory Barriers to the Use of Autonomous Ships, Submitted by Denmark.

- International Maritime Organization. 2018b. Report of the MSC on its 99th session, London.

- International Maritime Organization. 2018c. Resolution MEPC.304(72), Initial IMO Strategy on Reduction of GHG Emissions from Ships.

- Ko, B. W., J. W. Youn, S. H. Park, J. H. Kim, and Y. J. Choi. 2017. Study on Enhancing the Competitiveness of Container Shipping Industry through the Structural Improvements. Busan: Korea Maritime Institute.

- Kretschmann, L., H. C. Burmeister, and C. Jahn. 2017. “Analyzing the Economic Benefit of Unmanned Autonomous Ships: An Exploratory Cost-comparison between an Autonomous and a Conventional Bulk Carrier.” Research in Transportation Business & Management 25: 76–86. doi:10.1016/j.rtbm.2017.06.002.

- Lee, J. 2012. Revival of US Manufacturing Industry: On-shoring (korean). Seoul: Hyundai Research Institute.

- Lindstad, H., B. E. Asbjornslett, and A. H. Stromman. 2016. “Opportunities for Increased Profit and Reduced Cost and Emissions by Service Differentiation within Container Liner Shipping.” Maritime Policy & Management 43 (3): 280–294. doi:10.1080/03088839.2015.1038327.

- Mauro, C. D., L. Fratocchi, G. Orzes, and M. Sartor. 2018. “Offshoring and Backshoring: A Multiple Case Study Analysis.” Journal of Purchasing and Supply Management 24: 108–134. doi:10.1016/j.pursup.2017.07.003.

- Notteboom, T. E., F. Parola, G. Satta, and A. A. Pallis. 2017. “The Relationship between Port Choice and Terminal Involvement of Alliance Members in Container Shipping.” Journal of Transport Geography 64: 158–173. doi:10.1016/j.jtrangeo.2017.09.002.

- Rødseth, Ø. J. 2017. Introduction to Autonomous Ships in Trondheim. Trondheim: SINTEF Ocean AS.

- Schwab, K. 2016. The Fourth Industrial Revolution. New York: Crown Publishing Group.

- Tate, W. L. 2014. “Offshoring and Reshoring: U.S. Insights and Research Challenges.” Journal of Purchasing and Supply Management 20: 66–68. doi:10.1016/j.pursup.2014.01.007.

- Tran, N. K., and H. D. Haasis. 2015. “An Empirical Study of Fleet Expansion and Growth of Ship Size in Container Liner Shipping.” International Journal of Production Economics 159: 241–253. doi:10.1016/j.ijpe.2014.09.016.

- United Nations Conference on Trade and Development. 2017. Review of Maritime Transport, Geneva: United Nations Publication.

- van der Akker, J. T. 2017. Carbon Capture Onboard LNG-Fueled Vessels, A Feasibility Study. Delft: Delft University of Technology.

- van Hassel, E., H. Meersman, E. van de Voorde, and T. Vanelslander. 2016. “Impact of Scale Increase of Container Ships on the Generalised Chain Cost.” Maritime Policy & Management 43 (2): 192–208. doi:10.1080/03088839.2015.1132342.

- Waterborne, T. P., 2011. Waterborne implementation plan: Issue, Waterborne strategic research agenda, May.

- Wijnolst, N., and T. Wergeland. 2009. Shipping Innovation. Amsterdam: IOS Press BV.