Abstract

Engaging in exploration and exploitation is essential to business survival and performance. While firms manage exploration and exploitation alliances for the long‐term, how prepared are they for sudden shocks in the short‐term? We address this question in the context of a unique and opportune natural experiment associated with the 2008 financial crisis. Our analysis of 155 new biopharmaceutical ventures over a seven‐year period suggests that exploration alliances—with a long‐term orientation—make a firm more vulnerable to external shocks. In contrast, exploitation alliances as well as a balance between exploration and exploitation alliances—which underlie short‐term performance—enable the firm to sustain external shocks.

Introduction

The global financial crisis of 2008 contains a stark contrast between its sudden, unexpected onset and its obviousness in retrospect, laid out in numerous analyses highlighting its inevitability. This contrast has been popularized by the notion of Black Swans, that is, unanticipatable events with extreme impact that are relatively easy to explain retrospectively (Taleb Citation2007). Such events expose a significant rift between theory and practice of business and management. On the one hand, they are normally treated as unusual events, buried in the extreme but very thin tails of a presumed normal distribution of environmental shocks. Indeed, as important and consequential such events may be, they should be weighed down by a rational decision‐maker given the assumed rarity of their occurrence. As such, their expected impact is, in theory, minuscule and thus relatively safe to ignore by a rational decision‐maker. On the other hand, in practice, their actual impact is significant, with long‐term reverberations. Moreover, recent writings suggest that economic crises occur much more frequently than a normal probability distribution would suggest (Krugman Citation2008; Taleb Citation2007).

Survival over the long term is a fundamental goal for firms; it looms large in the evolution and change in business environments that challenge firms to adapt (Levinthal Citation1994). However, given that the short term of focus of many venture capital (VC) backed firms, exit via flotation and/or friendly mergers and acquisitions (M&A) based on superior short‐term performance may also represent an attractive option. In view of this, the literature has emphasized the importance of engaging in both exploration and exploitation activities as a means of balancing short‐term performance and long‐term survival (March Citation1991). This represents a particular challenge for new high‐technology ventures that often lack the resources to develop new products and thus keep up with the pace of change (Venkataraman et al. Citation1990). For such ventures, strategic alliances represent an important mechanism for ensuring innovative output (Baum, Calabrese, and Silverman Citation2000; Deeds and Hill Citation1996). In line with the exploration‐exploitation dilemma, some alliances aim to exploit existing capabilities, while others aim to explore new opportunities (Koza and Lewin Citation1998; Lee et al. Citation2012). Both types of alliances play a vital role in sustaining a system of new product development, particularly for smaller firms (Rothaermel and Deeds Citation2004). However, given the different nature of these alliances, the question arises of whether and how they matter for firm survival in the face of an external economic shock.

In this paper, we address this question in the context of a unique and opportune natural experiment associated with the global financial crisis of 2008, deemed by many the worst since the Great Depression of the 1930s. A survey of firms conducted in 2006, with no anticipation of what was to come, aimed to examine factors that contributed to firms' long‐term prospects. After the crisis, in 2012, this became an opportunity to assess the survival of these firms following this extraordinary and unanticipated short‐term shock. We distinguish alliances on the basis of their exploration versus exploitation focus, with the former focusing on longer‐term prospects and the latter on more immediate product commercialization outcomes. Our analysis of the survival of 155 new ventures in the biotechnology and pharmaceutical industries over the 2006–2012 period shows that ventures that failed had tended to have a higher number of exploration alliances and a lower number of exploitation alliances.

Our work raises important theoretical and managerial questions. First, while current theory on firms' adaptation to environmental changes (business turnaround) is concerned predominantly with the perils of long‐term survival and the exploratory behavior necessary to overcome it (Bourgeois Citation1981; Cyert and March Citation1963; Lavie, Kang, and Rosenkopf Citation2011), our work suggests that short‐term disruptions should constitute a more prominent angle in our theories. Second, our work enhances the understanding of the performance consequences of strategic behaviors in recession conditions, where market selection pressures are less forgiving than those in buoyant conditions. Our findings demonstrate that there are distinct resource considerations for the short term that can help contribute to the firm's survival in the wake of short‐term shocks. Finally, while prior work on the balance of exploration and exploitation in alliance formation emphasizes its importance on the basis of ensuring long‐term survival, our work suggests that short‐term survival is an equally vital consideration. Additionally, emphasis on long‐term strategy of biopharmaceutical firms overlooks a more VC driven strategy that may encourage early acquisition of the firm in the form of trade sale.

Theory and Hypothesis

Exploration, Exploitation, and Strategic Alliances

March (Citation1991) links adaptations at firm level to changes occurring at the level of the organizational population through a model of exploration and exploitation in organizational learning. He described exploration as “experimentation with new alternatives” having returns that “are uncertain, distant, and often negative,” and exploitation as “the refinement and extension of existing competencies, technologies, and paradigms” exhibiting returns that “are positive, proximate, and predictable” (p. 85). However, refining exploitation more rapidly than exploration may exhaust a firm's opportunities and render its competencies obsolete (March Citation1991). The survival of the firm thus depends on its ability to “engage in enough exploitation to ensure the organization's current viability and engage in enough exploration to ensure its future viability” (Levinthal and March Citation1993, 105). These two activities are difficult to balance since exploration of new alternatives slows down the process of exploiting existing ones; and improvement in competence at existing procedures makes experimentation with others less attractive (Levitt and March Citation1988).

Exploration–exploitation choices are readily applicable to strategic alliances, defined as voluntarily initiated inter‐firm cooperative agreements that involve contributions by partners reflected in exchange, sharing or co‐development of capital, technology, knowledge, or other firm‐specific assets (Gulati Citation1995). A firm's choice of the type of alliances to enter can be distinguished by its motivation to either explore for new opportunities or exploit existing capabilities (Koza and Lewin Citation1998). From this viewpoint, exploration alliances are established with the motivation to discover something new and they focus on the “R” in the research and development process. They support technological or product innovation with an emphasis on generating new knowledge and social capital, which allows the firm to acquire new capabilities, therefore enhance its future viability (Koza and Lewin Citation1998; Levinthal and March Citation1993; Mowery, Oxley, and Silverman Citation1996). Alternatively, exploitation alliances focus on the “D” in the research and development process and are established with the goal to join existing competencies across organizational boundaries to generate synergies, which are then shared across the partners. They support product commercialization with a strong focus on leveraging existing knowledge and relationships (Deeds and Rothaermel Citation2003), which allows a firm to achieve short‐term efficiency by generating immediate benefits, therefore improving its current viability.

Exploration and exploitation alliances are particularly prevalent in the biotechnology industry (George et al. Citation2001) and play a crucial role in the process of developing new products (Deeds and Hill Citation1996; Dowling and Helm Citation2006; Gerwin Citation2004; Gilsing and Nooteboomb Citation2006). It is very unlikely for a new venture to possess the necessary resources and capabilities to develop products entirely on their own (Amir‐Aslani and Negassi Citation2006; Azzone and Dalla Pozza Citation2003; Tucker, Friar, and Simpson Citation2012), due mainly to their liability of newness and relatively small size (Aldrich and Auster Citation1986; Stinchcombe Citation1965).

Engagement in both types of alliance activities also allows start‐up biopharmaceutical firms to overcome such liabilities by tapping into partners' resource networks and making extensive use of their manufacturing facilities, distribution channels and customer bases (Fosfuri and Tribo Citation2006; Miller Citation2004; Rothaermel and Deeds Citation2006). In return, large incumbent firms can gain access to start‐ups' technologies and make use of their external knowledge and expertise (Diestre and Rajagopalan Citation2012; Gilsing and Nooteboomb Citation2006; Rothaermel and Deeds Citation2004). More importantly, exploration and exploitation alliances can provide the funding for a start‐up to develop its drug to the stage at which an established company deems it worthwhile to acquire it even though a commercial drug has yet to be generated (Diestre and Rajagopalan Citation2012; McNamara and Baden‐Fuller Citation2007). For most young biopharmaceutical companies, such alliances represent their major source of funding in addition to equity investments prior to a positive exit such as IPOs (Lazonick and Tulum Citation2011; Niosi Citation2003).

In the case of the global financial crisis and tightening resources, access to other sources of funding such as VC becomes ever harder, specifically as the VC sector is increasingly reluctant to gamble on drug development projects in the hostile financial climate (Baum and Silverman Citation2004; Dimov and De Clercq Citation2006; Lazonick and Tulum Citation2011). The situation deteriorates due to the high risk, capital‐intensive nature of the biopharmaceutical sector. To survive under such scenarios, start‐up biopharmaceutical firms often lack the resources necessary to contend with major environmental shifts (Roijakkers and Hagedoorn Citation2006), despite of their strategic flexibility (Raynor and Leroux Citation2004), Thus, exploitation and exploitation alliances may provide an attractive option to contend with unexpected hostile external shocks, as such alliances provide start‐up biopharmaceutical firms with funding or income as well as direct resource access from alliance partners, which can be used to buffer the negative impact of sudden hostile shocks (Hoang and Rothaermel Citation2010; Meyer Citation1982).

Maintaining a balance between exploration and exploitation is vital for a new venture's survival and prosperity: firms that engage in exploration to the exclusion of exploitation suffer the costs of experimentation without gaining the benefits associated with exploiting extant opportunities, and may end up with undeveloped ideas and missed opportunities (March Citation1991). Equally, firms that exploit to the exclusion of exploration become trapped in suboptimal equilibrium which makes adaptation difficult as current opportunities become exhausted and existing competences obsolete (Levinthal and March Citation1993). In terms of strategic alliances, new ventures that focus excessively on exploration alliances forgo the opportunities that cannot be efficiently tapped by its internal organization as a result of limited market access. Likewise, a new venture that relies excessively on exploitation alliances may fail to internalize external knowledge that cannot be developed internally (Hagedoorn Citation1993; Mowery, Oxley, and Silverman Citation1996; Rothaermel Citation2001). Hence, an alliance portfolio that excessively emphasizes exploration or exploitation is sub‐optimal (Hoffmann Citation2007; Lavie, Kang, and Rosenkopf Citation2011). The two types of alliance complement one another along the firm's value chain (Rothaermel and Deeds Citation2004).

External Shocks

External shocks and their impact on firms have drawn the attention of organization and innovation scholars. Shepherd, Douglas, and Shanley (Citation2000) define shocks as an exogenous event that alters the overall degree of novelty at a point in time; by contrast, Venkataraman and Van de Ven (Citation1998) view an external shock as a low probability but high consequence event with an adverse economic impact. The occurrence of an external shock is therefore difficult to predict and its impact on firms is disruptive and potentially inimical. External shocks present both danger and opportunities (Starbuck, Greve, and Hedberg Citation1978). An external shock has direct influence on the potential customers, immediately inhibits a new venture's potential sales and ways of exit. On the other hand, however, new opportunities may be concomitantly created as the external environment redefines attractive market positions (Meyer, Brooks, and Goes Citation1990).

External shocks dramatically alter the competitive and operating conditions of an environment (Sine and David Citation2004). Due to their liabilities of newness and relatively small size (Aldrich and Auster Citation1986; Stinchcombe Citation1965), new ventures are particularly vulnerable to hostile external shocks, that is, those shocks that shrink the economic opportunities for the population of ventures within an economic niche (Venkataraman and Van de Ven Citation1998). As discussed already, alliances extend a new venture's boundary so it can engage in value chain activities that are otherwise unavailable given its limited internal resources and market opportunities (Gulati Citation1995; Lavie and Rosenkopf Citation2011). The resource dependency and information process theories suggest that the key theoretical motivation for alliances under increasing environmental uncertainty is to access partners' resources and ensure necessary knowledge flows to reduce such uncertainty (Combs and Ketchen Citation1999; Pfeffer and Salancik Citation1978). Therefore, in the face of external shocks, the nature of the venture's strategic alliances can be of pivotal importance for whether a new venture can withstand such shocks.

On the other hand, alliances increase a new venture's exposure to uncertainty arising from a partner's future behavior. It may be challenging to accommodate each partner's internal threat rigidity and failing to do so may hinder the joint response to increasing environmental threats (Marino et al. Citation2002). In addition, over‐relying on partners may lead to power imbalance, in particular when a new venture collaborates with large established firms. It is more likely that the stronger partners will wield more power which increases their potential for opportunism. These relational risks are rather predictable and can be minimized as alliance relationships develop. Moreover, it is very unlikely that such risks will have an immediate life‐threatening effect on each partner. In contrast to relational risks, external shocks are unpredictable, when they coexist, uncertainty at the macro level overrides risks at the micro level, as environmental shocks are fatal to the vast majority of firms (Shepherd, Douglas, and Shanley Citation2000). Thus it is reasonable to assume that under sudden hostile shocks, firms' needs to secure necessary resources and information flows will outweigh the fear of relational uncertainty and will encourage their increasing external focus and alliance activities (Marino et al. Citation2008). Empirical studies show that emerging market firms increasingly engage in partnership activities with a purpose to cope with uncertainty resulting from major economic changes (Hitt et al. Citation2004; Peng and Heath Citation1996). However, it is likely that external shocks may amplify a new venture's relational risks if the firm is overly dependent on one or a set of partners, who fail due to external shocks.

Hypotheses

Prior studies suggest that firms tend to invest more in exploration activities under perceived gradual shifts in the macro environment, as it increases the rate of innovation required for longer‐term survival (Lant and Mezias Citation1992). However, focus on exploration alliances can be detrimental to a new venture's survival in the wake of unexpected external shocks such as a financial crisis (Jansen, Van Den Bosch, and Volberda Citation2006; Shepherd, Douglas, and Shanley Citation2000). Because exploration alliances entail gradual and continuous investments with a long payoff horizon and uncertain outcomes (i.e., scientific breakthroughs), they are particularly vulnerable to the liquidity constraints following a financial crisis as such constraints threaten the firm's continued commitment to the alliances. After a negative shock, the level of resource munificence is generally lower and a firm's ability to reduce uncertainty in production and market is significantly restricted (Shepherd, Douglas, and Shanley Citation2000). In addition, to the extent that a crisis disrupts the current order in the industry, the long‐term prospects of an exploration alliance may be undermined by the degrading of the new knowledge it generates (Kim and Rhee Citation2009; Levinthal and Posen Citation2009; Madrid‐Guijarro, García‐Pérez‐de‐Lema, and Van Auken Citation2013). It is likely that more advanced knowledge may come out before such new knowledge has been applied in a specific product prototype and finally commercialized in the marketplace.

To deal with such situations, firms may adopt retrenchment strategies, such as terminating R&D projects, significant cut down of R&D budgets and delay of new product development. However, a new product may miss the right timing for its specific market and fail to be commercialized eventually. Exploration alliances formed with the purpose of developing such products may collapse due to being unable to meet their anticipated goals (Mohr and Spekman Citation1994; Saxton Citation1997). The cost of engaging in undermined exploration alliances and failing is not recoupable, and may be greater than the cost of not pursuing such activities under unexpected external shocks, specifically when the failure of such alliances carries debt obligations beyond the firms' short term debt paying ability. As a result, new ventures that are counterparties to such alliances may be deprived of critical funds that sustain their ongoing operations. In addition, the benefits of exploration alliances such as learning and knowledge accumulation, are less imminent to a new venture in the face of a sudden hostile shock than instant profits, which have immediate value to its continuous survival in the short‐term.

H1: Exploration alliances increase new ventures' likelihood of failure following a hostile external shock.

Exploitation alliances focus on the downstream activities of the value chain (clinical trials, FDA regulatory process, and marketing and sales) with a strong market orientation (Kohli and Jaworski Citation1990; Narver and Slater Citation1990). Investment in exploitation alliances can make a new venture more resilient to immediate changes in the business environment. Because firms with an emphasis on marketing as opposed to other business functions are more sensitive to the impact of external shocks that may potentially jeopardize business survival, and this enables them to make timely internal adjustments to counteract reduction in demand (Pearce and Michael Citation1997).

Sudden hostile shocks imply looming loss and a loss of control over operational decisions and outcomes. From a threat‐rigidity perspective (Sitkin and Pablo Citation1992; Staw, Sandelands, and Dutton Citation1981), exploitation alliances allow new ventures to engage in risk‐averse activities by focusing on tried and tested competencies with more predictable outcomes that limit potential loss (Voss, Sirdeshmukh, and Voss Citation2008). External shocks can create opportunities for new ventures with a strong orientation on product commercialization in their alliance portfolios, as the turmoil can make customers dissatisfied and more willing to switch suppliers. This can lower the level of market uncertainty (e.g., the market entry barriers) for a new venture and thus dampen its liability of newness (Stinchcombe Citation1965). In addition to adaptability to changes and provision of new opportunities, new ventures salvage their past investments by exploiting existing knowledge and leveraging past experience via exploitation alliances. From a resource‐based perspective, financial returns achieved through exploitation alliances, though not sustainable in the long run, provide immediately available resources that would allow firms to act faster in response to unexpected external shocks in the short term (Bourgeois Citation1981; Hambrick and D'Aveni Citation1988). Thus, the ability to tap into a firm's available resources is crucial not only to cushion the sudden impact of a shock but also to quickly capture the newly created opportunities by the shock (Cyert and March Citation1963).

H2: Exploitation alliances reduce new ventures' likelihood of failure following a hostile external shock.

H1 and H2 naturally raise the question of what happens when firms engage in both exploration and exploitation. A balance between exploration and exploitation alliances may also allow a new venture to adapt external shocks through exploiting existing assets and positions in a profit producing way and simultaneously to explore new technologies and markets. The balance enables the new venture to enjoy synergies by leveraging value chain complementarities across its partners (Lavie and Rosenkopf Citation2011). For example, a new venture can commercialize products by exploiting some of its partner's market access and production facilities based on knowledge acquired from some of its other partners. From a resilience perspective, a new venture becomes more robust through the accumulation of resources generated via exploitation alliances, which can be used immediately to absorb stress caused by sudden hostile shocks; equally, exploration alliances enhance the new venture's capability to bounce back from these shocks by transforming itself (Moberg and Folke Citation1999). Although achieving such a balance is difficult due to trade‐offs in resource allocation and internal conflicts associated with the use of inconsistent organizational routines (Lavie, Kang, and Rosenkopf Citation2011), these difficulties may be less applicable to new ventures. Given its limited internal resources and reliance on internal value chain activities, a new venture may depend on alliance partners for both exploratory R&D activities and exploitative marketing or production activities and become more vested in its alliances (Rothaermel and Deeds Citation2004). In addition, a new venture enjoys sufficient strategic flexibility and is more responsive and agile when attempting to balance its exploration and exploitation efforts, due to its flat organizational structure. Accordingly, a new venture would face limited inertial pressures when employing different procedures or adjusting its routines when engaging in R&D versus marketing or production alliances. Its partnering routines therefore become sufficiently flexible to enable it to effectively balance exploration and exploitation in alliances with less friction.

Engagement with exploration alliances increases a new venture's ability to detect tremors and prepare for external shocks (Meyer Citation1982). It allows the new venture to capitalize on the emerging opportunities for organizational learning created by the external shocks, and implement unrelated changes (such as the termination of the bad relationships), which makes the firm more resilient to external shocks. However, exploration alliances also represent a source of risk to the venture during external shocks, as the costs of undertaking such activities can be greater than the profit they generate. Concurrent engagement with exploitation alliances can generate immediate income or slack resources that can be used to buffer visceral components, safeguard brittle linkages, and conserve scarce resources which temporally insulates a new venture from external shocks and fuels adaptive responses to them (Cyert and March Citation1963; Meyer Citation1982).

Overall, in facing an external shock a firm engaging in both exploration and exploitation alliances would experience the pros and cons of each. Given the individual arguments giving rise to H1 and H2, there is no basis for arguing a priori for a particular direction of the combined effect of engaging in exploration and exploitation alliances. As a result, we propose the following set of competing hypotheses:

H3a: The balance between exploration and exploitation alliances reduces new ventures' likelihood of failure following a hostile external shock.

H3b: The balance between exploration and exploitation alliances increases new ventures' likelihood of failure following a hostile external shock.

Data and Methods

Original Sample and Data Collection

We focus on the biopharmaceutical sector in particular, as past studies have emphasized the importance of inter‐firm collaboration in new product development, and the particularly costly and risky nature of this process in biopharmaceutical firms (Ernst and Young Citation2006; Pisano Citation1990). The objective of our original data collection was to obtain information on the absorptive capacity, open innovation activities and growth of representative groups of biopharmaceutical firms from the U.S. and three major European economies (i.e., France, Germany, and the United Kingdom). Separate exercises were undertaken to define target populations for the company survey in Europe and the United States. In the United States, we obtained information on firms in the broader biotechnology sector from the Bioscan industry directoryFootnote13 (see also Deeds and Hill Citation1996; Rothaermel and Deeds Citation2004; Zollo, Reuer, and Singh Citation2002). For the European economies the target group was based on the data provided by http://Biotechnology-Europe.comFootnote14 which is the most comprehensive list of firms in the European biotechnology industry.

Once a comprehensive list of biotechnology firms had been identified we reviewed each firm's product profile and verified their inclusion in our final list of biopharmaceutical firms. We also excluded service firms (e.g., consultancies, technology transfer organizations, incubator centers, investors in biotechnology companies) at this point as well as organizations that were active in the bio‐pharmaceutical sector but which were not formal legal entities. This resulted in a U.S. target group of 999 biopharmaceutical firms, and a European target group of 1,099 firms (343 English companies, 247 French companies, and 509 German companies).

Once the target groups of biopharmaceutical firms had been identified each company was approached by telephone to confirm contact details, explain the purpose of this research, and encourage their participation in the study. Survey design was informed by inductive interviews with six R&D managers from five English biopharmaceutical firms. These interviews, which lasted 40–90 minutes each, helped to clarify key concepts and verify the transparency of metrics for absorptive capacity, open innovation, etc. Further verification of the questionnaire design was provided by a pilot postal survey covering 75 Irish biopharmaceutical companies to pretest the initial design for the English language questionnaire. Following some minor changes to the English language questionnaire, French and German versions were developed. In each case questionnaires were cross‐translated by two different translators and any differences in meaning were resolved.

The main survey was administered to the final target list of 2,173 U.S. and European biopharmaceutical firms between June and October 2006. An initial mail shot including freepost response envelopes, was followed‐up after two weeks by telephone and a further mailing. Finally, we obtained useful responses from 349 biopharmaceutical firms, an overall response rate of 16.1 percent. Individual country response rates were: United States, 14.4 percent, Europe, 17.5 percent (United Kingdom, 23.9 percent, France, 14.2 percent, Germany, 14.0 percent, and Ireland, 22.7 percent). The average respondent firm had 47 employees, with U.S. firms being larger (average 65 employees) than those in the European Union countries (35 employees).

The Natural Experiment Afforded by the global financial crisis of 2008

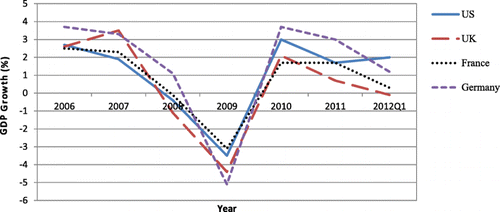

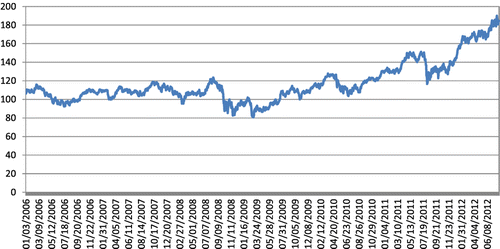

As a hostile exogenous shock that is widely acknowledged as the worst since the Great Depression of the 1930s (Haidar Citation2012; Reuters Citation2008), the 2008 global financial crisis provides an ideal natural experiment to examine our research questions (Chakrabarti, Singh, and Mahmood Citation2007; Wan and Yiu Citation2009). Brewing for a while, the crisis started to show its effects in the middle of 2007 and into 2008. As shown in Figure 1, the GDP growth of the four study countries dropped significantly and plunged to the historically lowest points in the first quarter of 2008. Though a sharper rise was seen in the following period, cresting around mid‐2009, the growth rates of all four economies slowly declined again soon afterward. This trend is closely mirrored by the stock value of the global biotechnology industry: for example, a significant drop in the NASDQ Biotechnology Index can be clearly identified between September 2008 and March 2009 (Figure 2).

Figure 1. GDP Growth between 2006 and 2012 Q1 by Country [Color figure can be viewed at http://wileyonlinelibrary.com]

Source: World Bank.

Figure 2. NASDAQ Biotechnology Index (NBI) [Color figure can be viewed at http://wileyonlinelibrary.com]

Source: NASDAQ.

The 2007–2008 financial crisis played a significant role in the failure of major businesses, decline in consumer wealth estimated in trillions of U.S. dollars, and a downturn in economic activity leading to the 2008–2012 global recession and contributing to the European sovereign debt crisis (Baily and Elliott Citation2009; Williams Citation2012). The resulting “credit crunch” significantly slowed VC fundraising for technology‐based start‐ups such as new biopharmaceutical ventures since 2007 (British Venture Capital Association [BVCA] Citation2009; National Venture Capital Association [NVCA] 2009; World Bank Citation2009), as investors became more cautious in committing money to VC funds. The following recession impacted sales growth for many start‐ups, the timeline to profitability, and hence amount of funding required. In the meantime, the economic downturn provided cost effective opportunities to invest in new or disruptive technologies spinning out from the science base. The booming clean energy investment and associated high level of investor enthusiasm for the sector provide some evidence to support this proposition (Makower, Pernick, and Wilder Citation2007).

We examine only the period of the global financial crisis in this study for several reasons. First, the global financial crisis created a series of subsequent shocks such as the follow on economic crisis, as well as changes in government spending, regulations, and financial availability, etc. We separate them from the financial crisis itself, as the effects of these subsequent shocks are dramatic and still ongoing at the time of our study. Second, capital‐raised declined sharply during the crisis period as a result of a sharp rise in the equity risk premium (the risk premium of equities over bonds), causing the cost of capital to rise and private investment to fall. Biotechnology companies in the United States and Europe raised US$16 billion in 2008, a 46 percent decline from 2007. IPO funding fell 95 percent to US$116 million (Ernst and Young Citation2009). This systemic and protracted funding drought placed the business model that fueled biotech growth for the past three decades under unprecedented strain. To survive in this environment, firms may need to restructure operations and use deals creatively, as well as bring the creativity that has long been the industry's hallmark to establishing more durable models for funding innovation, for example, via more creative development partnerships.

We focus on new ventures within our original sample, defined as those less than ten years old at the time of the crisis (Certo, Daily, and Dalton Citation2001; Covin and Slevin Citation1990; Shepherd Citation1999; Sigmund, Semrau, and Wegner Citation2015). We consider this as appropriate in the context of our study as it usually takes at least ten years for a biopharmaceutical company to bring a new drug from discovery to FDA approval—a time horizon that captures the transition from a new venture to an established business. This yielded a final sample of 155 new ventures out of a list of 349 biopharmaceutical firms included in the original sample. We collected further information on their latest survival status in 2012 from FAMEFootnote15 (for the United Kingdom) and Thomson ONEFootnote16 (for France and Germany) using the company name identifiers. For respondent firms that could not be identified in these two databases, we collected the survival information from their official websites and/or industry newspapers such as Healthcare Industry TodayFootnote17 and BioPortfolio.Footnote18 These data sources also helped us gather the latest information, for the firms that did survive the crisis, on their product portfolio, in particular the number of new product(s) on the market. Table summarizes the observations and key variables in each of the three countries and the overall sample. In terms of the nonresponse bias, no significant differences are found between respondent and nonrespondent firms on firm size (p = 0.35) and age (p = 0.67).

Table 1. Basic Descriptives of the Sample Firms

Survival Time

We study the survival time from initial establishment until failure. The event of interest is firm exit by bankrupcy or liquidation (coded as 1). Exit by M&A is a competing event (coded as 2). From an investor and entrepreneur's viewpoint, being acquired and/or merged is often viewed as success rather than failure given that a business is sold at or above its market value, because successful sale of the business allows investors and entrepreneurs to harvest from their investment. Specifically, during the period of the crisis, when world stock markets have been depressed, trade sales are usually considered as more desirable exit routes than flotations (Storey and Greene Citation2010). This has led to acceleration of consolidation of the global biotechnology industry (Ernst and Young 2009). As firms are at risk of failing all the time, to examine the net effect of the global financial crisis on firm survival, we split each firm's observation spell into three, with the dividing lines representing the onset and end of the global financial crisis respectively. In this specification, the second observation spell, during of the crisis, represents the heightened hazard of failure triggered by the external economic shock. The first and last observation spells capture firm survivability before and after the crisis. Since the exact dates of exit were not precisely recorded in the database but the months were, we chose the month of exit as our time variable.

We used September 2008 as the onset of the global financial crisis for the purpose of this study, as according to the World Bank and NASDAQ official statistics, this was the time when the GDP growth of all our four study countries plunged into the undergrowth (Figure 1) and the market value of the global biotechnology industry begun to collapse below the historically lowest point since 2006 (Figure 2). Equally, June 2009 was considered as the end of most severe period of the crisis (Hulbert Citation2010), as GDP growth for the four countries in ours study climbed to its highest level since the onset of the crisis at this point (Figure 1), after which the growth of the market value of the global biotechnology industry took off (Figure 2). Unless firms failed before September 2008,Footnote19 the first spells were right censored and the actual outcomes were shown in the second spells, which capture whether the firms in the study survived the global financial crisis. The last spells comprise those firms survived beyond the financial crisis. This organization of the data yielded a total of 430 observations (12 firms failed before September 2008 + 143 firms × 2 periods + 132 firms).

Model Specification

We estimate the hazard rate using a competing risk model (CRM) (Han and Hausman Citation1990), as two types of exit forms are examined in this study, namely firm failure (bankruptcy or liquidation) and M&A. The model is based on Fine and Gray's proportional hazard model and thus does not require any restrictive assumptions regarding the baseline hazard, such as a Weibull or lognormal specification. This allows us to account for the mode of exit in terms of bankruptcy or liquidation and M&A. The two outcomes are treated as independent so that the probability of the occurrence of one is assumed not to depend on the probability of the occurrence of another.Footnote20 Thus, the discrete time formulation of the hazard of exit type j for firm i at duration t is denoted as

and can be given by a complementary log logistic function as follows:

1

where j = 1 or 2, depending on the type of exit (bankruptcy or liquidation versus M&A); i = 1, …, n; t = 1, …, T.

is the baseline hazard function relating to the hazard rate

at the tth interval with the spell duration (Jenkins Citation2007). It is assumed to take the proportional form as

, where

is the baseline function,

is a vector of the regression parameters and

is a vector of covariates for firm (i). The vector

in our empirical model includes a range of time varying explanatory variables relating to the factors affecting firm survival, that is, number of exploration or exploitation alliances, and the global financial crisis. It also includes control variables relating to the firm characteristics (such as age and R&D intensity) and strategic focus. These explanatory variables are effectively measured with a six‐year lag with respect to the dependent variable, since they were collected in the initial survey in 2006 and firm survival status is updated in 2012. Each of the factors associated with firm survival is explained in more detail as follows.

Measures

Exploration and Exploitation Alliances

We measure exploration and exploitation alliances in which a biopharmaceutical firm engages along its value chain (Deeds and Hill Citation1996; Xia and Roper Citation2008). Exploration alliances are a count variable of research based partnerships which focus on upstream activities in a biopharmaceutical firm's value chain, that is, basic research, drug discovery, preclinical development. Exploitation alliances are a count variable of marketing based partnerships that focus on downstream activities, that is, clinical trials, FDA regulatory process, marketing, and sales. In industries like the biopharmaceuticals, alliance activities are widely observed (George et al. Citation2001), and are seen as playing an important role in contributing to the survivability of new ventures (Dowling and Helm Citation2006; Gilsing and Nooteboomb Citation2006).

Balance Between Exploraton and Exploitation Alliances

We measure the balance between exploraton and exploitation alliances by adopting the approach to measuring firm ambidexterity of exploratory and exploitative innovation, that is, as a multidimensional construct comprising the non‐substitutable combination of exploration and exploitation alliances (Gibson and Birkinshaw Citation2004; Jansen, Simsek, and Cao Citation2012). In practice, firm ambidexterity is operationalized as the multiplicative interaction of exploration and exploitation activities (Cao, Gedajlovic, and Zhang Citation2009; Gibson and Birkinshaw Citation2004; He and Wong Citation2004; Lavie, Kang, and Rosenkopf Citation2011), as high levels of exploration and exploitation complement and augment the performance enhancing effect of each other (Cao, Gedajlovic, and Zhang Citation2009; Jansen, Simsek, and Cao Citation2012). To address the facts that the simple multiplicative term is very sensitive to the total number of alliances and that it fails to account for the balance itself (e.g., 2 × 8 gives the same multiplicative score as 4 × 4), we divide the multiplicative term by the square of the average number of exploration/exploitation alliances. The intuition for this is that for a given total number of alliances, the multiplicative score is highest when the numbers of exploration and exploitation alliances are equal. Our measure thus ranges between 0 and 1 and represents the raw multiplicative score as a proportion of its maximum for the given number of alliances. In the earlier examples, for alliance numbers of 2 and 8, the balance measure yields a value of 0.64 (i.e., 2 × 8/52), while for alliance numbers of 4 and 4, the balance measure yields a value of 1. We note, however, that using the simple multiplicative term yields results consistent with those reported below.

Global Financial Crisis. To capture the impact of the global financial crisis on the likelihood of firm survival, we included a crisis dummy variable reflecting the period during the global financial crisis between September 2008 and June 2009 (1 respresents the survival period between September 2008 and June 2009 and 0 otherwise).

Control variables

In addition to the main variables of interest, we control for a number of other possible effects as captured by various relevant firm characteristics such as age, size, R&D intensity, location, strategic focus, and funding profile. We control for firm age (measured in years), as new ventures typically suffer from the liabilities of newness and the risks of failure are higher for young firms than older firms (Stinchcombe Citation1965). Competing arguments based on a liability of adolescence, however, suggest that the risk of failure is relatively low for very young firms due to support by external constituents and initial endowments. But when these initial resources become depleted, the failure hazard shoots up and then declines following the liabilities of newness pattern (Bruderl and Schussler Citation1990).

We measure size by a firm's number of full‐time employees. According to Penrose's theory of growth (Citation1959), if a firm grows too fast by size, the entrepreneur or the management team of the firm may not be able to respond quickly enough and make necessary changes to the organization and management structure. The resulting mismatch between firm size and management structure may put the firm at risk of going bankrupt and lead to firm exit (Churchill and Lewis Citation1983).

R&D intensity is measured by the average percentage of R&D investment to total turnover for each firm during the last three years at the time of the survey (Deeds Citation2001; Fontana and Nesta Citation2009). Firms investing in R&D activities are more likely to generate new knowledge stocks and improved productivity growth which will increase the market value of the firm, and consequently the likelihood of survival (Hall Citation1987). In knowledge‐intensive industries such as biopharmaceuticals, a significant strategic commitment to R&D appears to be critical to the firm's ability to develop competencies required to survive and succeed (Deeds Citation2001). However, over‐capitalizing in R&D activities (above the optimal level of R&D) is risky to a firm's continuous survival, as it increases uncertainty. Higher uncertainty generates a temporary slowdown and bounceback as firms postpone activity and wait for uncertainty to resolve (Bloom et al., Citation2007). This significantly reduces a firm's responsiveness of R&D to changes in business conditions, such as major economic shocks. New establishments generally operate below the optimal level of R&D with no access to large R&D facilities (e.g., large R&D laboratories) unless through external partners such as large corporates and public research institutions (Mahmood and Mitchell, Citation2004). In addition, it is very unlikely for a start‐up biopharmaceutical firms to attract massive initial VC investment in basic R&D without staging, due to the high attrition rate and prolonged process of biopharmaceutical product development.

Next, as there may be significant institutional or environmental effects we use a dummy variable to control for European Union–United States differences (0 = United States, 1 = European Union) (Rothaermel and Deeds Citation2006). We also control for new ventures access to VC funding, which may make a critical difference to their engagement with exploration or exploitation alliance activities. Firms backed by VC are more likely to capitalize on exploitation alliance activity and survive better, because they can call upon sufficient resources to pursue exploration activity (Niosi Citation2003). The variable takes a value of 1 if a new venture receives external funding from venture capitalists, and 0 otherwise. Finally, the strategic focus of biopharmaceutical firm represents an important factor for their survival and growth (i.e., Deeds and Hill Citation1996; George et al. Citation2001; Maurer and Ebera Citation2006). We measure this firm characteristic by two indicator variables, reflecting, respectively, whether a firm focuses on preclinical development and marketing and sales.

Since our survey firms are relatively small companies in an emerging sector, there were no consistent secondary data sources that could provide an objective corroboration of some of the individual responses. Nevertheless, we sought to minimize common method bias by guaranteeing response anonymity, counterbalancing the question order and structuring the questionnaire to seperate the measurements of predictor and criterion variables (Podsakoff et al. Citation2003). In addition, we conducted a Harman's single‐factor test of all variables in this study. Exploratory factor analysis shows a result of seven factors with eigenvalues greater than one with the first factor accounting for only 12 percent of the total variance. Independent and dependent variables of each of our equations clearly loaded on different factors. These results indicate that common method bias is not substantially present in our data.

Results

Tables and report the descriptive statistics and correlations for the variables used in our analysis. Table reports the results from CRM of firm failure. Model 1 includes the control variables as well as the main effects for the crisis and the numbers of exploration and exploitation alliances. In Model 2, we add the interaction effects of the alliance variables with the crisis dummy. These interaction effects represent the effects of exploration and exploitation alliances on firm failure after the onset of the financial crisis. In Models 3 and 4, we include the effect of balance between exploration and exploitation alliances and then its interaction with the crisis dummy, to test H3a and H3b.

Table 2. Basic Descriptives by Exit Type

Table 3. Correlation Matrix (N = 155)

Table 4. Competing Risk Regression of New Venture Failure

In terms of main effects of the alliance variables, in Model 1 we find the effect for crisis to be positive and marginally significant (β = 0.328, p < .10), indicating—as one would expect—that the risk of failure increases after the onset of the crisis. The effect of the number of exploration alliances is positive and marginally significant (β = 0.041, p < .10), while the effect of exploitation alliances is negative and marginally significant (β = −0.043, p < .10). These results suggest that engagement in exploration alliances has a negative impact on firm survival, whereas engagement in exploitation alliances has a positive impact. In Model 3, the main effect for balance between exploration and exploitation alliances on the likelihood of failure is negative and marginally significant (β = −0.464, p < .01), suggesting that this balance has a positive impact on survival.

The interaction effects of the numbers of exploration and exploitation alliances and the balance between them with the crisis dummy enhance the just described main effects in each case. In Model 2, the interaction between the number of exploration alliances and the crisis dummy is positive and marginally significant (β = 0.002, p < .10). It suggests that engaging in exploration alliances leads to even higher likelihood of failure after the onset of the crisis. This result provides some support for H1. The interaction between the number of exploitation alliances and the crisis dummy is negative and significant (β = −0.972, p < .05). It suggests that engaging in exploitation alliances leads to much lower likelihood of failure after the onset of the crisis. This result supports H2. Finally, in Model 4, the interaction effect of the balance between exploration and exploitation alliances and the crisis dummy is negative and significant (β = −2.241, p < .01). It suggests that maintaining a balance between the two types of alliance leads to lower likelihood of failure after the onset of the crisis. This result provides some support for H3a. Thus, H3b is rejected.

Robustness Checks

To verify the robustness of our results, we performed several additional analysis. First as we focus on two types of exit, failure (bankruptcy or liquidation) and M&A, which can be treated as categorical outcomes, we re‐estimated the previously examined relationships using an alternative multinominal logistic regression without separating the net effect of the global financial crisis. The results suggest very similar patterns to the CRM in Table .

Second, an M&A can be a successful exit if it is valued well for the acquired company. However, it can also be an indication of firm failure if the M&A is hostile or extremely low‐valued, and the acquired company has to sell with little bargaining power. To rule out this type of M&A from our analysis, we have checked the M&A profiles of our respondent firms by looking for information on their valuations from various secondary sources, such as company websites, industry reports, business news and commentary. Our finding confirms that all the 19 M&A deals included in our estimation are successful exits.

Third, to test whether the two forms of exit examined in this study can be treated as independent event, we estimated the hazard of each form of exit using a Cox proportionate model, and performed a Hausman test of the differences between these two outcomes. The results confirm the significant differences between exit by bankruptcy or liquidation (failure) and M&A.

Fourth, we performed a robustness check on the consistency between our sample firms' engagement with both types of alliances and their overall explorative and/or exploitative strategy.Footnote21 The results show that our sample firms, engagement with exploration alliances is highly correlated with their overall focus on the explorative dimension (β = 0.787, p < .01); likewise these firms' engagement with exploitation alliances is highly correlated with an overall focus on the exploitative dimension (β = 0.706, p < .01). As an extension of this analysis, we have included a variable capturing the ratio of exploration to exploitation alliances in our estimation of new venture failure. The result confirms that the share of effort toward exploratory activity in a new venture's alliance portfolio is a significant predictor of its failure under external shocks.Footnote22

Fifth, to test the sensitivity of our results to the choice of period for the global financial crisis, we conducted further analysis of our sample firms' likelihood of failure during the years within and following the crisis. The results obtained in each year are consistent with our current results.

Finally, it is important to recognize that firms with more exploitation alliance activities at the time of our initial survey in 2006 would naturally expect to be more advanced in their innovation. They are more likely to have products nearer to market, which will make it easier for such firms to obtain funding and therefore increase their likelihood of survive during external shocks. To test this potential effect, we included a count variable capturing a firm's number of products at late stage development in our estimation. The results confirm that the possession of products nearer to market does not have a significant effect on our sample firms' likelihood of failure during the global financial crisis.

Discussion

Our aim in this paper has been to gain some understanding of how alliance behavior relates to new venture survival under extraordinary and unanticipated short‐term shocks. We did so in the context of the global financial crisis of 2008, which afforded a natural experiment for the paper. The empirical results suggest that exploration alliances, that is, those focused on longer‐term product development, make firms more vulnerable to external shocks in the short term. In contrast, exploitation alliances, that is, those aimed at leveraging existing knowledge and competencies, enable firms to withstand such shocks and thus ensure their short‐term survival. Similarly, balancing both types of activities also enhances the likelihood of new venture survival in the short term. A number of implications are identified as follows.

First, our study provides new insights into the relationship between exploration alliances and firms' performance outcomes. Previous research has shown that firms using exploration alliances to identify market opportunities have higher performance, and this relationship is stronger both in unstable external environments and for smaller start‐up firms (Marino et al. Citation2008; Sarkar, Echambadi, and Harrison Citation2001). Our finding of a negative relationship between exploration alliances and firm survival suggests that engaging in exploration alliances jeopardizes a new venture's survival under sudden hostile external shocks such as the global financial crisis. In other words, exploring new products contributes to the biopharmaceutical firm's future success, however, at the expense of its current viability. Moreover, we explicitly focus on an unexpected external shock in this study. Such shocks are rarely considered in theoretical accounts of firm survival and absent in the empirical literature as they are, by definition, unusual and unexpected. Successful strategy adaptation assumes knowing what the future business environment will look like, however, the unpredictable and instant nature of such shocks makes it hard to envisage and prevent firms from making prompt adjustments. But to the extent that they are more prevalent—as recent work suggests (Krugman Citation2008; Taleb Citation2007)—our work suggests that long‐term, risky endeavors such as exploration alliances should be complemented by initiatives to maintain firm viability in the short‐term.

Second, our study articulates the role of exploitation alliances as a compelling strategy for enduring survival. Previous studies suggest that exploitation alliances prevent firms from discovering new opportunities and reduce their future viability in the buoyant conditions (Koza and Lewin Citation1998; March Citation1991). However, the short‐term performance benefits of such alliances have been largely overlooked, given that there is a wide variety of situations in which exploitation alliances can provide firms with distinctive resources considerations in the short term such as under the recession conditions, where market selection pressures are less forgiving than those in buoyant conditions. Our study extends this line of research by uncovering the exceptional short‐term performance implications of exploitation alliances that can help contribute to the firm's survival in the wake of short‐term shocks (Barker and Duhaime Citation1997; Robbins and Pearce Citation1992). More specifically, we shed light on this critical research gap by providing the rationale with empirical evidence for a positive relationship between exploitation alliances and firm survival under external shocks. Our finding suggests that engagement with exploitation alliances enhances a start‐up biopharmaceutical firm's chance of survival under sudden hostile external shocks. When faced with a sudden shock, entrepreneurs must react quickly and decisively to ensure a firm's continued viability because implementing small, incremental changes, even in large numbers, often will not produce changes necessary to adjust to new environmental realities (Romanelli and Tushman Citation1985).

Moreover, our study highlights differences in the extent to which each type of alliance affects firm survival under external shocks. Specifically, in its absolute magnitude, the effect of exploitation alliances on new venture failure following the external shock is much greater than that of exploration alliances (−1.02 versus 0.02). This suggests that short‐term shocks catalyze the value of exploitation alliances as a buffer for survival. In contrast, the increased likelihood of failure associated with exploration alliances, though relatively small in magnitude, is much less sensitive to the short‐term shock. This suggests that in the aftermath of an external shock, survival is all down to whether a firm can latch on to the positive effect of exploitation alliances. Revenues generated through exploitation alliances can help new ventures to acquire valuable resources at bargain prices during the recession (Wan and Yiu Citation2009), without being limited by the accompanying funding drought, and the high interest rates charged by most fund providers to compensate for greater uncertainty (Storey and Greene Citation2010). This enables these firms to capture the emerging opportunities created by external shocks faster and more aggressively (Hambrick and D'Aveni Citation1988; Wan and Yiu Citation2009).

Finally, our study contributes to a growing understanding of alliance ambidexterity and the conditions for such strategies to flourish. In line with the previous research on alliance ambidexterity (Cao, Gedajlovic, and Zhang Citation2009; He and Wong Citation2004; Hill and Birkenshaw Citation2014), our finding confirms that maintaining a balance between exploration and exploitation alliance activities is of pivotal importance to a new venture's survival. The dangers that external shocks present are usually overlooked in the light of the possible opportunities they create. Prior work on the balance between exploration and exploitation in alliance formation emphasizes its importance on the basis of ensuring long‐term survival (Gupta, Smith, and Shalley Citation2006; Hill and Birkenshaw Citation2014; Lavie, Kang, and Rosenkopf Citation2011). Our study complements this body of research by underscoring the merits of balancing exploration and exploitation alliance activities in contributing to firms' short‐term survival under sudden hostile shocks. Previous literature on firm performance draws a clear line between strategies that are beneficial to long‐term performance and those contribute to short‐term viability (Levinthal and March Citation1993; March Citation1991). Given that the long‐term performance contributions of balancing exploration and exploitation alliances are well documented (Hill and Birkenshaw Citation2014; Lavie and Rosenkopf Citation2011), we are able to demonstrate that there are strategies that can help not only sustain the firm's performance growth but also contribute to its survival in the wake of short‐term shocks.

However, our analysis further suggests that overdependence on either type of alliance activity under external shocks may lead a new venture to lose either its continued viability or emerging opportunities that could potentially contribute to its future viability. As evidenced by our robustness check, alliance portfolio with a stronger orientation on exploration activity makes a new venture more vulnerable to short‐term shocks. Balancing exploration and exploitation within the alliance portfolio therefore helps a new venture effectively tackle both sides of an external shock and enhances its chance of survival. From an organizational learning perspective, to identify opportunities emerged from external shocks with the potential for exploitation, a new venture needs to possess sufficient absorptive capacity to identify and evaluate new opportunities. The foundations for these activities reside in the existing knowledge and competence bases which can be built through its exploration alliance activity (Hill and Birkenshaw Citation2014). Likewise, a number of studies show that the slack resources generated through engaging in exploitation alliance activity can provide crucial resources for new ventures to better capture emerging opportunities more aggressively in an external shock (Cheng and Kesner Citation1997; Hambrick and D'Aveni Citation1988; Wan and Yiu Citation2009).

Reflecting further on our results opens up research possibilities that we have not been able to explore in our data. The first research possibility relates to the new venture's exposure to uncertainty arising from a partner's future behavior. It may be challenging to accommodate each partner's internal threat rigidity and failing to do so may hinder their joint response to increasing environmental threats (Marino et al. Citation2002). Over‐relying on partners may lead to power imbalance, in particular when a new venture collaborates with large established firms. It is likely that external shocks may amplify a new venture's relational risks if the firm is overly dependent on one or a set of partners, who fail due to external shocks. Second, from the viewpoint of relational capital, in the event of a crisis and tightening resources, it is questionable whether another firm is really likely to make available its limited number of resources to a partner firm “instantly.” These issues raise an interesting direction for future research to study alliance behaviors under external shocks while controlling for relational dependence, power, and duration of the relationship up to the point of crisis.

Limitations

Our study is, however, subject to a number of limitations. First due to the limitation of our data, we can only study exploration and exploitation within the function domain of alliance formation. We are also unable to identify the length of each individual alliance, as it is possible that some of the alliances are entered in the final stage when the survey was conducted and resolve before the external shock. Future studies should test the robustness of our findings across different domains of alliance formation, such as the structure and attribute domains while controlling for the length of each alliance.

Similarly, we measure alliance activity by counting exploration and exploitation alliances, given the difficulties of measuring the value of alliance activity. So many alliance benefits are indirect, what matters most may not be the balance between direct alliance input and output but the impact of the alliance on the competitive standing of each partner and the strategic options made available or foreclose (Doz and Hamel Citation1998). Therefore, some alliance value can be measured directly, but other benefits may go into partners' ledgers in a furtive manner. These may be intangible and difficult to link with the activities of the alliance, but they are real nevertheless (Doz and Hamel Citation1998). Future research should attempt to go beyond simple count measures to develop alliance activity measures that reflect its quality and value more accurately. More in‐depth understanding of value creation and value appropriation in strategic alliances is critical for developing measures for the value of alliance activities.

Second, our analysis is based on the biopharmaceutical sector, a sector that is often regarded as having distinct characteristics. In particular, our definition of new ventures as firms less than ten years old—may not be compatitable with new ventures in industries where the new product development and/or approval window is relatively short, such as the software industry. Therefore, before attempting wider generalization, other studies could usefully be undertaken in an attempt to generalize our results to other industries, such as the telecommunication and semiconductor industries. Finally, further exploration of the positive impact of exploitation alliances on firm survival is clearly needed, as our study provides little insight into the behavioral processes underlying this effect under external shocks. This will also help entrepreneurs enhance their strategic planning to prevent failure in the event of sudden hostile external shocks.

Conclusions

In conclusion, this study represents a step in the direction of acknowledging “business as usual” not as tucked away from the improbable extremities of a normal distribution but as subject to sizeable probability of short‐term shocks. The natural experiment afforded by the global financial crisis of 2008 enabled us to examine how the strategic choices of firms in 2006—unsuspecting of what was to come—had significant consequences, both positive and negative, for firm survival in the wake of the crisis. It suggests that theory and the body of evidence on the performance consequences of strategic behaviors should be sensitive to the unknown but real dangers of the short‐term. In specific, when prompt adaptation becomes unviable due to the unknown and instant nature of such shocks, it is likely that businesses may fail before even realizing their arrival and/or possible impact. To fully capture the opportunity and avoid the dangers external shocks present, the occurrence of such events should be controlled in the evaluation of the effectiveness of certain strategies before making a strategic choice. Our findings suggest that exploration alliances with a long‐term orientation make firms more vulnerable to external shocks, whereas exploitation alliances as well as a balance between exploration and exploitation alliances—which underlie short‐term performance—enable these firms to sustain external shocks.

Additional information

Notes on contributors

Tianjiao Xia

Tianjiao Xia is Lecturer at the School of Business and Economics, Loughborough University.

Dimo Dimov

Dimo Dimov is a professor at School of Management, University of Bath.

Notes

13. BioWorld, Atlanta, Georgia.

14. Biotechnology World, Warsaw, Poland.

15. Bureau Van Duk, Brussels.

16. Thomson Reuters. New York.

17. IPD Group, Washington, D.C.

18. Bioportfolio, Dorset, UK.

19. In our case, we found 12 such firms that failed between January 2006 and September 2008.

20. To test whether these two exit types can be treated as independent, we performed a Hausman test and a Wald‐test of equality for all parameters. The results from both tests confirmed the significant differences between these two forms of exit.

21. We operationalized firms' overall focus on the explorative and exploitative dimensions in terms of two dummy variables (1 stands for a focus on explorative or exploitative dimension, 0 otherwise). In the original survey, we ruled out those firms whose overall focus was neither explorative nor exploitative dimensions.

22. The results are available upon request.

References

- Aldrich, H., and E. Auster (1986). “Even Dwarfs Started Small: Liabilities of Age and Size and Their Strategic Implications,” in Research in Organizational Behavior, Vol. 8. Eds. B. Staw and L. Cummings. Greenwich, CT: JAI Press, 165–198.

- Amir‐aslani, A., and S. Negassi (2006). “Is Technology Integration the Solution to Biotechnology's Low Research and Development Productivity?,” Technovation 26, 573–582.

- Azzone, G., and I. Dalla pozza (2003). “An Integrated Strategy for Launching a New Product in the Biotech Industry,” Management Decision 41, 832–843.

- Baily, M., and D. Elliott (2009). “The U.S. Financial and Economic Crisis: Where Does It Stand and Where Do We Go from Here?” [Electronic Version]. Business and Public Policy, http://www.brookings.edu/papers/2009/0615_economic_crisis_baily_elliott.aspx

- Barker, V. III, and I. Duhaime (1997). “Strategic Change in the Turnaround Process: Theory and Empirical Evidence,” Strategic Management Journal 18, 13–38.

- Baum, J., T. Calabrese, and B. Silverman (2000). “Don't Go It Alone: Alliance Network Composition and Startups' Performance in Canadian Biotechnology,” Strategic Management Journal 21, 267–294.

- Baum, J. A. C., and B. S. Silverman (2004). “Picking Winners or Building Them? Alliance, Intellectual, and Human Capital as Selection Criteria in Venture Financing and Performance of Biotechnology Startups,” Journal of Business Venturing 19, 411–436.

- Bloom, N., S. Bond, and J. Van reenen (2007). “Uncertainty and Investment Dynamics,” Review of Economic Studies 74, 391–415.

- Bourgeois, L. (1981). “On the Measurement of Organizational Slack,” Academy of Management Review 6, 29–39.

- British Venture Capital Association (2009). BVCA Private Equity and Venture Capital Report on Investment Activity 2009. London: The British Private Equity and Venture Capital Association.

- Bruderl, J., and R. Schussler (1990). “Organizational Mortality: The Liability of Newness and Adolescence,” Administrative Science Quarterly 35, 530–547.

- Cao, Q., E. Gedajlovic, and H. Zhang (2009). “Unpacking Organizational Ambidexterity: Dimensions, Contingencies, and Synergistic Effects,” Organization Science 20, 781–796.

- Certo, S., C. Daily, and D. Dalton (2001). “Signaling Firm Value through Board Structure: An Investigation of Initial Public Offerings,” Entrepreneurship Theory and Practice 26, 33–50.

- Chakrabarti, A., K. Singh, and I. Mahmood (2007). “Diversification and Performance: Evidence from East Asian Firms,” Strategic Management Journal 28, 101–120.

- Cheng, J., and I. Kesner (1997). “Organizational Slack and Response to Environmental Shifts: The Impact of Resource Allocation Patterns,” Journal of Management 23, 1–18.

- Churchill, N. C., and V. L. Lewis (1983). “Growing Concerns,” Harvard Business Review 61, 30–50.

- Combs, J., and D. Ketchen (1999). “Explaining Interfirm Cooperation and Performance: Toward a Reconciliation of Predictions from the Resource‐Based View and Organizational Economics,” Strategic Management Journal 20, 867–888.

- Covin, J., and D. Slevin (1990). “New Venture Strategic Posture, Structure, and Performance: An Industry Life Cycle Analysis,” Journal of Business Venturing 5, 123–135.

- Cyert, R. M., and J. G. March (1963). A Behavioral Theory of the Firm. Englewood Cliffs, NJ: Prentice Hall.

- Deeds, D. L. (2001). “The Role of R&D Intensity, Technical Development and Absorptive Capacity in Creating Entrepreneurial Wealth in High Technology Start‐Ups,” Journal of Engineering and Technology Management 18, 29–47.

- Deeds, D. L., and C. W. L. Hill (1996). “Strategic Alliances and the Rate of New Product Development: An Empirical Study of Entrepreneurial Biotechnology Firms,” Journal of Business Venturing 11, 41–55.

- Deeds, D. L., and F. T. Rothaermel (2003). “Honeymoons and Liabilities: The Relationship between Age and Performance in Research and Development Alliances,” Journal of Product and Innovation Management 20, 468–484.

- Diestre, L., and N. Rajagopalan (2012). “Are All Sharks Dangerous? New Biotechnology Ventures and Partner Selection in R&D Alliances,” Strategic Management Journal 33, 1115–1134.

- Dimov, D. P., and D. De Clercq (2006). “Venture Capital Investment Strategy and Portfolio Failure Rate: A Longitudinal Study,” Entrepreneurship Theory and Practice 30, 207–223.

- Dowling, M., and R. Helm (2006). “Product Development Success through Cooperation: A Study of Entrepreneurial Firms,” Technovation 26, 483–488.

- Doz, Y., and G. Hamel (1998). Alliance Advantage: The Art of Creating Value through Partnering. Boston, MA: Harvard Business School Press.

- Ernst & Young (2006). Beyond Borders ‐ Global Biotechnology Report 2006. Palo Alto, CA: Ernst & Young LLPo, Document Number.

- Ernst & Young (2009). Beyond Borders ‐ Global Biotechnology Report 2009. Palo Alto, CA: Ernst & Young LLP.

- Fontana, R., and L. Nesta (2009). “Product Innovation and Survival in a High‐Tech Industry,” Review of Industrial Organization 34, 287–306.

- Fosfuri, A., and J. A. Tribo (2006). “Exploring the Antecedents of Potential Absorptive Capacity and Its Impact on Innovation Performance,” Omega 36, 173–187.

- George, G., S. A. Zahra, K. K. Wheatley, and R. Khan (2001). “The Effects of Alliance Portfolio Characteristics and Absorptive Capacity on Performance: A Study of Biotechnology Firms,” Journal of High Technology Management Research 12, 205–226.

- Gerwin, D. (2004). “Coordinating New Product Development in Strategic Alliances,” The Academy of Management Review 29, 241–258.

- Gibson, C. B., and J. Birkinshaw (2004). “The Antecedents, Consequences and Mediating Role of Organizational Ambidexterity,” Academy of Management Journal 47, 209–226.

- Gilsing, V., and B. Nooteboomb (2006). “Exploration and Exploitation in Innovation Systems: The Case of Pharmaceutical Biotechnology,” Research Policy 35, 1–23.

- Gulati, R. (1995). “Does Familiarity Breed Trust? the Implications of Repeated Ties for Contractual Choices,” Academy of Management Journal 35, 85–112.

- Gupta, A. K., K. G. Smith, and C. E. Shalley (2006). “The Interplay between Exploration and Exploitation,” Academy of Management Journal 4, 693–706.

- Hagedoorn, J. (1993). “Understanding the Rationale of Strategic Technology Partnering: Inter‐Organizational Modes of Cooperation and Sectoral Differences,” Strategic Management Journal 14, 371–385.

- Haidar, J. (2012). “Sovereign Credit Risk in the Eurozone,” World Economics 13, 123–136.

- Hall, B. (1987). “The Relationship between Firm Size and Firm Growth in the US Manufacturing Sector,” Journal of Industrial Economics 36, 583–606.

- Hambrick, D., and R. D'aveni (1988). “Large Corporate Failures as Downward Spirals,” Administrative Science Quarterly 33, 1–23.

- Han, A., and J. Hausman (1990). “Flexible Parametric Estimation of Duration and Competing Risk Models,” Journal of Applied Econometrics 5, 1–28.

- He, Z. L., and P. K. Wong (2004). “Exploration Vs. Exploita Tion: An Empirical Test of the Ambidexterity Hypothesis,” Organization Science 15, 481–494.

- Hoffmann, W. (2007). “Strategies for Managing a Portfolio of Alliances,” Strategic Management Journal 28, 827–856.

- Hill, S. A., and J. Birkenshaw (2014). “Ambidexterity and Survival in Corporate Venture Units,” Journal of Management 40, 1899–1931.

- Hitt, M. A., D. Ahlstrom, M. T. Dacin, E. Levitas, and L. Syobodina (2004). “The Institutional Effects on Strategic Alliance Partner Selection in Transition Economies: China Vs Russia,” Organization Science 15, 173–185.

- Hoang, H., and F. T. Rothaermel (2010). “Leveraging Internal and External Experience: Exploration, Exploitation, and R&D Project Performance,” Strategic Management Journal 31, 734–758.

- Hulbert, M. (2010). It's Dippy to Fret about a Double‐Dip Recession. Cambridge, MA: The National Bureau of Economic Research (NBER).

- Jansen, J., F. Van Den bosch, and H. Volberda (2006). “Exploratory Innovation, Exploitative Innovation, and Performance: Effects of Organizational Antecedents and Environmental Moderators,” Management Science 52, 1661–1674.

- Jansen, J., Z. Simsek, and Q. Cao (2012). “Ambidexterity and Performance in Multiunit Contexts: Cross‐Level Moderating Effects of Structural and Resource Attributes,” Strategic Management Journal 33, 1286–1303.

- Jenkins, S. P. (1995). “Easy Estimation Methods for Discrete‐Time Duration Models,” Oxford Bulletin of Economics and Statistics 57, 129–138.

- Kim, T., and M. Rhee (2009). “Exploration and Exploitation: Internal Variety and Environmental Dynamism,” Strategic Organization 7, 11–41.

- Kohli, A., and B. Jaworski (1990). “Market Orientation: The Construct, Research Propositions, and Managerial Implications,” Journal of Marketing 54, 1–18.

- Koza, M., and A. Lewin (1998). “The Co‐Evolution of Strategic Alliances,” Organization Science 9, 255–264.

- Krugman, P. (2008). The Return of Depression Economics and the Crisis of 2008. New York: W.W. Norton.

- Lant, T., and S. Mezias (1992). “An Organizational Learning Model of Convergence and Reorientation,” Organization Science 3, 47–71.

- Lavie, D., J. Kang, and L. Rosenkopf (2011). “Balance within and across Domains: The Performance Implications of Exploration and Exploitation in Alliances,” Organization Science 22, 1517–1538.

- Lavie, D., and L. Rosenkopf (2011). “Balancing Exploration and Exploitation in Alliance Formation,” Academy of Management Journal 49, 797–818.

- Lazonick, W., and Ö. Tulum (2011). “U.S. Biopharmaceutical Finance and the Sustainability of the U.S. Biotech Business Model,” Research Policy 40, 1170–1187.

- Lee, H., D. Kelley, J. Lee, and S. Lee (2012). “SME Survival: The Impact of Internationalization, Technology Resources, and Alliances,” Journal of Small Business Management 50(1), 1–19.

- Levinthal, D. (1994). “Surviving Schumpeterian Environments: An Evolutionary Perspective,” in Evolutionary Dynamics of Organizations. Eds. J. Baum and J. Singh. New York: Oxford University Press, 167–178.

- Levinthal, D., and J. March (1993). “The Myopia of Learning,” Strategic Management Journal 14, 95–112.