Abstract

Purpose

The rational strategic behavior of humanity to prioritize their self motives may lead to unethical conduct, with a potential financial consequence. Thus, this study investigates how the love of money and locus of control can affect the unethical behavior and performance of small and medium economic actors in the Indonesian context.

Participants and Methods

This article examines the responses from 530 small entrepreneurs as part of the hypotheses in behavioral strategy by employing covariance-based structural-equation modeling (CB-SEM). This quantitative approach is conducted following the acceptance of the data quality requirements.

Results

The findings confirm most hypotheses, leaving one insignificant nexus of locus of control and SME performance. This finding also illuminates the intangible behavior in shaping the SMEs’ strategic performance. Some indirect relationships are also provided.

Conclusion

This study substantiated the notion that the strategic aspect of SMEs’ business relies on the behavioral construction of the actors. How entrepreneurs view their source of action internally or externally is critical in shaping how they view money achievement. A strong tendency to love money too much leads them to be more unethical and ends up in a deteriorating sign of financial performance. However, being unethical justifies the potentiality of increased income streams. This specific finding of strategic behavior corresponds to the how “unregulated morality” creates a freedom in doing business.

Introduction

Small and medium enterprises (SMEs) are the backbone of the Indonesian economy, as 50 million citizens depend on it.Citation1 They account for 99.8% of employment and 95% of business entities in Indonesia,Citation2 thus, securing a 60% contribution to the Indonesian economy.Citation3 This fact reiterates the need to support the SMEs’ performance through governmental aid, external funding, or even management training and reformation. This study aims to highlight the importance of SMEs’ reformation in the form of behavioral aspects. This focus is evident as the SMEs issues like existential funding, government support, the market access have been widely discussed.Citation2,Citation3 Powell et alCitation4 urge the importance of aligning the social and cognitive conversation to firms’ strategic actions. He points it as the most discussion in strategic absorption is on the business success recipes.Citation5 This relatively late development is strange as rational motive is the underlining element in strategic formulation and decision-making.Citation6

Investigating economic actors’ behavior can contribute to knowledge expansion as it creates the foundational reasonings upon executing a task in market uncertainty,Citation7 eg, entrepreneurial orientation, market orientation,Citation8 or the potentiality of financial behavior.Citation9 How they manage their financial assets is subject to complex decision-making as part of their self-interests to rationally focus on their own needs. Adam Smith has long observed this selfish strategic behavior and even got moral support in his theory of moral sentiment.Citation10 Furthermore, the seminal work of Kahneman and Tversky has noted how this rationality may create risky behavior upon making a judgment.Citation11,Citation12 As rational behaviors are subject to potential biases,Citation13 SME entrepreneurs may be entitled to a prerequisite strategic condition that may affect the ideal behavior upon dealing with money.

The expected behavior when dealing with money supposedly presents a higher ethical ground; however, the money-achieving motives may erode this ideal condition. Tang has consistently discussed this issue, pointing to the presence of the love of money (LOM) and its repercussive effects across genders.Citation14–17 The impact on financial performance is also expected to be constructed from the locus of control (LOC) as to how humans consider their actions in retrospect to the internal or external factors that may lead to organizational effectiveness.Citation18,Citation19 Several studies have highlighted this positive relationship that solid inner beliefs of the entrepreneurs’ actions are substantial in securing strong performance.Citation20,Citation21 While the investigations of LOC, LOM, and unethical perceptions have been sufficiently discussed,Citation22 the mediation effects in the context of entrepreneurs are still elusive. Furthermore, how entrepreneurs may jeopardize their money ethics in pursuing income streams lead to potentially neglected ethical issues.Citation23–25

This study is expected to contribute to the neglected investigation of how entrepreneurs’ money ethics may correspond to how they may secure positive outcomes. As to the authors’ knowledge, the article of SusantoCitation26 discussing innovative work behavior is the closest work linking these constructs. The strategic behavior of perceiving money and how the behavioral management of it in the SMEs’ contexts may serve as the early investigation in entrepreneurial research and the connection toward strategic behavioral management. Thus, this study advances the conversation by presenting the analyses of ethical-behavioral strategies for securing organizational performance in Indonesian SMEs.

Behavioral Strategy

The development of strategic management is pushed within the boundary of actors’ behavioral decisions and actions. The famous John Nash’s game theory (1950) presents humans’ strategic decision-making to make rational movements are foundational with extensive applications.Citation27 As strategic decisions are related to human behavior, selecting one strategy over another and pushing the edge of victory are constructed in human minds.Citation28 This path is where the trajectory of firm strategy and psychology converged. Behavioral strategy is the merging of cognitive and social psychology and strategic management. It discusses how human cognition, emotion, and behavior make realistic predictions in the organization and push the conversation in strategy theory, academic research, and practices.Citation4 The initial construction of strategy theory comes from the ramifications that strategy is a thought process in actors’ minds. On the other hand, it is the application of various organizational strategies.Citation29 The strategic field will significantly improve by considering the organization’s microfoundations, namely the motivational aspect, by considering goal-framing theory based on cognitive theory, behavioral economics, and social psychology.Citation30,Citation31

Behavioral biases are other endeavors in psychology that are meaningful for strategic management conversations. It addresses the nature of humans to make biases upon deciding, deviating from the rationality path.Citation32,Citation33 The study results show that these biases may harm organizational performance, for example, when the source of strategic information comes from peers.Citation34 The study found that organizational performance results from various predictors, one of which is the behavioral aspect of employees.Citation35 Socio-emotional factors are critical in making a strategic shift from one decision to another, provided the business performance results are considered.Citation36 Because the rationality process encourages humans to maximize the benefits of their efforts, the potentiality of future research endeavors is imminent. Another study on the theme of dynamic capabilities emphasizes that sensing, seizing, and transforming abilities need to mobilize and exploit the emotional and cognitive capabilities in the process to secure substantial output.Citation37 Controlling humans in various organizational positions will give rise to multiple conditions inherent in the social-emotional aspects of the actors.Citation38,Citation39 Recent updates on the strategic behavior conversation in entrepreneurship have taken on the improvisational behavior during the crisis to safeguard positive performance when the market competition is intense.Citation40 Based on the description above, this paper departs from the study of behavioral strategy in studying psychological variables and their ability to influence organizational performance in the context of SMEs.

The Locus of Control

Locus of Control (LOC) is a psychological condition Rotter first mentioned in 1966. He defines it as a person’s perspective regarding events, whether or not they can control the outcomes of such appearance.Citation41 The LOC is divided into internal and external drivers, where inner subjective beliefs polish an individual’s internal agenda, and external factors shape the judgment of a particular decision.Citation42 When individuals make up their mind that things happen because of their presence, they have a solid internal LOC. Conversely, if they believe that luck, coincidence, or fate as the reasons for everything means a strong presence of external LOC.Citation43

LOC has been often associated with attitudes.Citation44,Citation45 This study also expands the conversation by investigating the relationships between LOC and the attitude toward economic gains, specifically the love of money. This conversation was investigated in 1992 by Tang et al;Citation14 however, the connection between these two did not capture the most attention. In strategic behavior, these two constructs are some stimuli that make up human minds to conduct action and, thus, need further clarification on the effect or directions.

Previous research has discussed the relationship between LOC and individual ethical perceptions. Individuals with a firm grasp over their internal locus of control are more ethical.Citation17 Business people in the United States and Taiwan have different moral perceptions when they get external stimuli to get more money in the form of bribery. The results of cross-cultural studies prove that business people in Taiwan are more open to the issue of giving facilitation money to speed up their business results than those from the USA.Citation46 LOC is also proven to encourage the increasing ethical tendency of managers to become whistleblowers of harmful practices within the company.Citation47

The relationship between LOC and business performance outcome still needs further expansions for their minimum conversation. One study has seen that external LOC is negatively associated with performance, while the internal is positive.Citation48 The effect of LOC toward performance is mainly mediated by strategic decision,Citation49 changes in attitudes,Citation44,Citation45 or the increasing market and entrepreneurial orientation.Citation21 The LOC has also negatively influenced attitude formation regarding immigrants in Canada, the United States, and the United Kingdom.Citation50 Another study points out that LOC cannot moderate the relationships between burnout and performance among business leaders.Citation51 This study believes that LOC can add a positive contribution to the strategic behavior conversation, and thus:

H1: The locus of control increases the money-loving stance of SMEs entrepreneurs

H2: The locus of control is positively related to the unethical perception

H3: The locus of control is associated with the increase in the SME performance

The Love of Money

Love of money (LOM) or love of money is a concept first formulated by Tang, which measures the subjective role of cash in one’s life.Citation14 LOM serves as an individual’s behavior, expectations, and aspirations for using funds in their presentation of good, respect, achievement, power, budget, and evil.Citation52 Tang & ChiuCitation53 hypothesized that a love of money would substantially increase greed, concluding that money-loving is evil, but the money itself is not. Love for money is often negatively connoted and is considered taboo in several religious teaching and beliefs. Understanding someone’s love for money is necessary because capital can foster positive and negative behavior. Tang and ChiuCitation53 show that a high passion for income will result in a person becoming greedy and less able to work well with their peers. Tang & LiuCitation54 reported that money ethics, or the love of one’s money, has a significant and direct influence on unethical behavior. People with high money ethics (love of money) who place great importance on capital will be less ethical and sensitive than people with low money ethics. A study of employees in Hong Kong proved that a love of money made them uncomfortable at work compared to those who did not particularly like money. The constant awareness of the income source will persist in individuals with good ethics towards money.Citation53 However, the love of money cannot always be viewed negatively. The study results by Liu and Tang indicate that love of money can encourage increased employee motivation and job satisfaction.Citation55 These positive attitudes may be the source of positive performance.

Adam SmithCitation56 has long viewed that self-interest motives are what drive the market. His proposition is consistent with the rationality theory of humankind that seeking a continuous income stream is the rational choice to survive.Citation57 Thus, it is logical to assume that those with substantive love of money would drive to work hardCitation55 to secure better economic returns. Moreover, people would strategically and rationally strive to obtain more money as it leads to better performance for their business performance. This effort would make them love the cash even more as they appreciate the sacrifice to obtain it. Putting money as the gold performance standard has also been a modern world customary.Citation58 This conversation is built upon the minimum research discussing the role of love of money on business performance and paves the way for potential investigation as in the followings:

H4: The love of money propels the unethical perception

H5: The love of money created a better performance for SMEs

Unethical Perception

Business activities cannot be separated from ethical aspects. Business ethics are ways to conduct business activities that cover all aspects of individuals, companies, industries, and society. This definition includes how to do morally good business by changing the world’s view of business ethics to improve the world’s economic order. Business without ethics causes the rulers and business people to become uncontrollable and justifies any means to achieve their goals.

Ethical perception presents as an endogenous variable of this research. Conroy and EmersonCitation59 argued that ethics is a good and bad value system for humans and society. The limits of normative values in interactions with society and their environment can then be ethical values. Donaldson & DunfeeCitation60 divides the theory of business ethics into two forms: the normative and empirical sides. Normative issues are studied by researchers with a deep understanding of philosophical issues.

On the other hand, the empiricist chooses a practical approach with straightforward applications in various parts of the business, such as finance and marketing. The constant marketing of ethics has been criticized by TrevinoCitation61 as it cannot explain and predict decision-making processes. How it may lead to better performance is also debated.

Several studies have highlighted the role of ethics in better performance.Citation62,Citation63 However, the magnitude of its effect is often not presented. Hair et alCitation64 have advocated the presentation of effect size to analyze whether a strategic business decision can be made or just neglect it for a minimum relevance. Thus, this study aims to present it to investigate this relationship with a twist on whether being unethical is suitable for performance. This formulation is plausible as being unethical may allow the business actors to do whatever is necessary to secure their internal motives. Thus, breaking off the chain may lead to:

H6: Unethical perception increases organizational performance.

Materials and Methods

Design

This research extracted psychological response data from small and medium enterprise (SME) entrepreneurs in Makassar City and conducted a quantitative analysis. This response will provide an overview of how ethical phenomena among members are related to their work. This study follows convenient sampling by calculating the minimum sample size and conducting a study field. Researchers employ several enumerators to collect data from the entrepreneurs by visiting them and directly recording the data on their cellphones through a google form. The coded responses are tabulated and analyzed through several statistical tests, ie, normality measurement, convergent validity test, confirmatory factor analysis (CFA), and structural equation modeling (SEM), for the path model.

In particular, the data were analyzed in two steps; firstly, the quality assessment to present the validity and reliability tests regarding the behavioral perceptions of Small and Medium Enterprises in Indonesia. Hair et alCitation65 suggest the quality tests for CB-SEM analysis to include the information of convergent validity, discriminant validity, and multicollinearity, in addition to the mandatory goodness-of-fit analysis. Thus, this study maximizes the Smartpls software for the validity and reliability criteria analysis, along with the Lisrel 10.2. Secondly, inferential statistics following the principles of parametric testing and data normality. The analysis employs Lisrel 10.2 software for path constructions in the covariance-based structural equation modeling. This process will provide the answers to the presented hypotheses. This study uses google form media, where respondents fill the data on their cellular device to facilitate a more straightforward presentation and faster response rates.

Measure

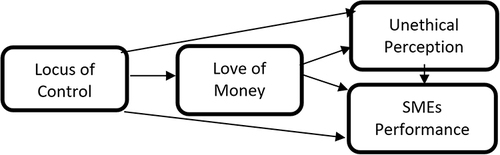

This study compiled a questionnaire that was targeted to be a medium to obtain relevant information from SME actors. The questionnaire contains closed statements manifesting the latent variables that are the object of investigation, namely love of money, locus of control, unethical perception, and financial performance, which form the conceptual model shown in . The statement is assessed using a 5-point Likert scale (see Appendix 1). Love of money is measured based on the money ethic scale developed by Tang.Citation14 His initial study revealed the Cronbach’s alpha in the second order constructs as Good (α 0.81), Evil (α 0.69), Achievement (α 0.70), respect (self-esteem) (α 0.68), Budget (α 0.72), and Freedom (power) (α 0.71). Locus of Control as a mapping of external/internal information in investment decisions is measured based on the work locus of control scale from Spector.Citation66 The unethical perception that reflects how individuals respond to various unethical actions/violations is adapted from the capacity of relativism and idealism by the construction of Forsyth.Citation67 This study also estimates the perceptions of SME owners regarding their financial performance without taking financial data that might be considered sensitive.Citation68 This perception aims to reduce the managerial resistance to sharing strategic information. All instruments were translated or adapted from the original language in their respective research essays into Indonesian to get an accurate response (the descriptive result in ). The research instruments are then presented to the Ethical Commission for clearance in a study involving human subjects.

Table 1 Descriptive Measure

Figure 1 Conceptual framework.

This study will test the validity and reliability of the indicators proposed in the confirmatory factor analysis (CFA) analysis, loading factor, and the average variance extractor (AVE) (see Appendix 1 for the questionnaire statements). The results of the validation and reliability are shown in .

Table 2 The Outer Model Quality

This study examines four variables which are the main objects of study, namely LOC, LOM, Unethical Perception, and finally, the SMEs’ Performance. The descriptive test in provides information about the distribution of data, both mean, standardized deviation, and correlation among each variable. This study proposes 17 indicators derived from various previous theories. The final investigated scales are available in the Appendix 1. The indicators are subject to a confirmatory factor analysis test, and two correlated error covariances within the same variable are constructed to reach a better fit model. The items align with the sampling procedure, as discussed in the sampling technique.

Sample

The population in this study was 16,492 SME entrepreneurs registered in the Ministry of Cooperatives and Small and Medium Enterprises in Makassar City. The authors characterized the sample with the characteristics of having an annual asset turnover of at least IDR. 15,000,000 (+ USD 1000), and the business has been around for five years. This study uses nonprobability convenience sampling, where every SME who coincidentally meets the researcher and fulfills the specified data terms can become the study’s participants.

This study then takes the ethically-approved questionnaire to the field research. The author visits the SMEs in the local hubs scattered across Makassar, Indonesia. These entrepreneurial centers host many tenants, thus, simplifying the data collection procedure. The author ensures the entrepreneurs that the study would not collect confidential data, allowing for a high response rate by using a snowballing recommendation from the entrepreneurs to their peers. This gentle approach leads to 530 usable responses. There are no missing data as the author employs the online survey in Google forms with a mandatory setting to fill all questions. The 530 coded data are sufficient by the majority of sampling requirements, eg, the ten-time rules,Citation65 the 100–150 the minimum threshold for SEM analysis;Citation69,Citation70 the five times number of indicators;Citation71,Citation72 or the Yamane or Roscoe sampling formulas.Citation73,Citation74 Out of 37 initial items, 20 indicators become the object of investigation following the CFA, validity, and reliability tests presented for hypothesis inquiries.

Results

This study investigates the appropriateness of the instruments proposed in two major groups, namely the outer-model test, to obtain information about the suitability of the data used. The first test performed was data normality based on Kolmogorov–Smirnov’s test through SPSS software and resulted in an insignificant p-value, indicating no non-normality problem.

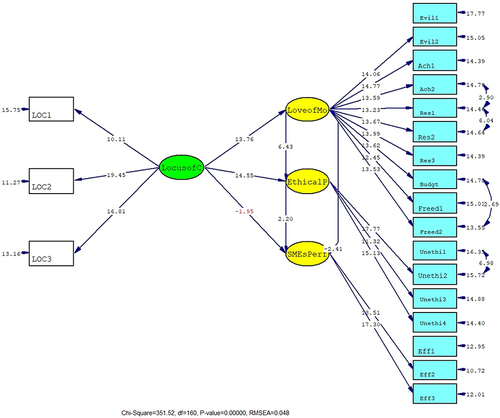

This study explored the proposed quality indicators using Confirmatory Factor Analysis (CFA) based on Covariance-based Structural Equation Modeling with Lisrel software. The results of the CFA study indicate that the final model consisting of 17 items has a stable and highly dependable model quality, as recorded in the goodness of fit results. With some improvements (two correlated standard-error within the same variable), the final model is shown to have the important indicators to be χ2 = 360 (p = 0.000); df = 160; RMSEA = 0.0475; RMR = 0.0360; GFI = 0.936. Those absolute fit indexes reveal the close fit of the investigated model, despite the chi-square (χ2) and the degree of freedom (df) not meeting the cut-off value for a high χ2 and df. These two measures are sensitive to sample numbers with higher data would certainly decrease those two fitness measures; however, other absolute indexes like RMSEA, RMR, and GFI still support the data fitness. Thus, this study then investigates the convergent validity and reliability tests and discovers the support for the data, as revealed in .

This study employs the Smartpls 3 output to investigate the quality presentation of the outer model. All loading outputs are substantial enough above 0.5. Hair et alCitation64 stated that its expected value is above 0.7, but it is not the final criterion, as other measures have to be considered. Removing indicators is unnecessary if it cannot increase the value of Cronbach’s alpha or Average Variance Extractor (AVE). As all Composite Reliability (CR) values above 0.7 are sufficient, this study proceeds with other criteria. Unethical perception appears as the variable with the lowest data quality but is still suitable because the CR is adequate. Overall loading values, alpha, rho_a, CR, and AVE provide support for the quality of the outer model. The model also does not show symptoms of multicollinearity, with a Variance Inflation Factor (VIF) value above 0.2 and below 3. VIF values below three also indicate the absence of common method bias.Citation75 This study also tested discriminant validity using the Heterotrait-monotrait test (HTMT), as in .

Table 3 The HTMT Test of Discriminant Validity

After all the instruments in this study meet the data quality rules, from validity and reliability to the outer model formulation, hypothesis testing can be carried out. and present the summarized inferential statistics to prove the nomological validity of the proposed model in path analysis.

Table 4 The Relationships Summary

Figure 2 The path revelation.

After all the instruments used in the study meet the data quality rules, from validity and reliability to the outer model formulation, hypothesis testing can be carried out. presents the summarized findings of inferential statistics to prove the nomological validity of the proposed model, and illustrates Lisrel’s statistical presentation in path analysis.

The study finds some notable and exciting findings in the hypothesis inquiries test in CB-SEM. All significant relationships are present at the confidence level of 99%, with a t-value higher than 2.58. LOC is strongly and positively related to LOM and ethical stance, but not toward entrepreneurial financial performance. The LOM is statistically significant in the increase of unethical perception but reveals an adverse impact on performance. Being unethical also leads to better performance. All indirect relationships are found to be statistically significant. The discussion is as follows.

Discussion

This study found that the results supported the H1 hypothesis: the higher the perception of personal locus of control (LOC), the higher the love for money (LOM). Locus of control appears as a motivational driver that shapes individual attitudes.Citation76 It is not surprising that one’s perception of self-enrichment in the context of materialism is formed from how one’s self-control is constructed. An initial investigation of TangCitation15 shows that the locus of control includes the elements of the love of money, such as importance, achievement, respect, and freedom. This finding is an extension of Tang’s study in 1992, which rarely gets further investigations. Furthermore, the effect size of the relationship is relatively large, indicating the robust prediction of locus of control toward love of money.

This finding implies that small entrepreneurs reconstruct their moral behavior mainly from external sources, either religion, environment, peer pressure, or social customaries.Citation23 These external encouragements create the foundation for the increasing love of money following their economic motives to increase income. The entrepreneurs’ tendency to love money too much can be associated with greed, as the liberal view of wealth has created the foundation of the ideal-life imagination of being rich. The social customs amplifying respect for those wealthy figures become the foundation for the external locus of control construction. Conversely, another study reveals that individuals with robust internal control will have a more apathetic attitude toward money,Citation77 making them wiser in their economic journey. The construction of these relationships indicates that the external locus of control can have an evident effect on the money-loving perceptions, potentially serving as the basis for increasing unethical conduct among entrepreneurs.

This study advances the conversation by investigating how the entrepreneurial actors’ locus of control may become the foundation of their unethical perceptions in doing business. This analysis clarifies the causative effect, confirming the preposition of hypothesis 2 that locus of control in shaping individual perceptions is a strong predictor of SMEs’ unethical perceptions in Indonesia. Previous studies reveal that the relationship between these two behaviors is complex. A study found that only women showed the symptoms between locus of control and ethics;Citation78 however, other research rejected this claim by reporting the no-gender dichotomy in the relationship.Citation79 One investigationCitation46 pointed to indirect demographic/geographic factors influencing the relationship between these constructs, as evident in the Taiwanese and USA business people.

Conversely, a local study in Indonesia found a non-existing effect in the relationships,Citation80 hence against the result of this study. However, most investigations support the role of locus of control in the ethical construction of small entrepreneurs.Citation81,Citation82 The diversity of research reports indicates that further investigations have to sufficiently admit the variation across human behavior not to be taken lightly.

As this study constructs the locus of control as confidence regarding one’s behavior, the SME actors increase their unethical perception. This finding is different, as most study point to the positive causation between locus of control and ethics. Thus, this research report provides evidence that as entrepreneurs believe that life is beyond their control, they will focus on maximization of the controllable results in economic gains. This self-interest motive is evident as they concentrate on what is at hand, supporting the basic construction of rational behavior in financial gains/losses.Citation11,Citation57

This research formulation presents the case of locus of control and its effect on financial performance among SMEs in Indonesia. This study discovered a non-significant relationship and thus rejected hypothesis 3. This finding indicates that the entrepreneurs’ belief regarding their life course will not result in better SME performance. This result contributes to the minimum conversation regarding these two behavioral constructs. Previous studies mainly discuss the locus of control and financial performance. Some reports reveal that Internal business self-control can create better outcomes than those with a greater tendency toward externalities.Citation18,Citation83 This result is plausible as external influences like the strategic activities of peers can be a supporting factor or constraint on individual performance.Citation45

While the fight over the internal or external locus of control capacity in pushing for better behavior continues, the strategic management agenda is trying to reconcile these two notions. The efforts are evident by, eg, the dynamic capability theoryCitation84–86 or strategic entrepreneurship,Citation87–89 which focuses on internal/external adaptive capabilities in producing sustainable advantages. SMEs’ actors must have substantial control over various resources to orchestrate the desirable financial income. Entrepreneurs are expected to maintain positive strategic behavior; however, social connectedness may present positive or negative consequences. Economic activities may lead to a strong focus on money-seeking motives, leading to the presence of a love of money.

This study reinforces the investigation by testing the economic motive in the form of the love of money and unethical perception. The finding confirms the relationship in hypothesis 4, which found a positive association between LOM and unethical perception. This finding corresponds with the mainstream research that generally reports an association between these two psychological conditions.Citation25,Citation54,Citation90 This result confirms that excessive love of money, with its various expressions,Citation91 has great potential to encourage individuals to behave unethically. The strong urge to enrich oneself may enhance selfish decisionsCitation92 in different strategic choices.Citation93 Moreover, the SMEs’ business landscape can encourage creating an atmosphere of intense competition and promote unethical attitudes.Citation94 While a loving money attitude positively increases the unethical stance, it may not end well for securing a good performance.

This study also tests whether the economic outcome of being a money lover is evident. This investigation advances the study of behavioral strategy by observing whether one perception is related to financial performance. This study confirms the formulation of hypothesis 5 but with a negative causality. This result means that as the SMEs’ entrepreneurs increase their love of money, it decreases their economic gain. It can be understood that the formulation of the relationship between these two variables is still hypothetical and exploratory, where the discussion of previous research is still very minimal, if not existing. The closest previous investigation is regarding the love of money and innovative behavior, which results in a positive and significant association.Citation26 Psychological studies also provide information that those with a great passion for money have a greater tendency to take risks, as a high-risk profile is associated with the opportunity to get a more beneficial result.Citation95 This study’s unique finding is that the potential tendency to enjoy the obtained income irresponsibly may lead SME entrepreneurs to use their money irresponsibly, thus jeopardizing their business performance. This observation needs further clarification in future studies as the research investigation is still anew. While loving money can be unethical, ethics and business performance research have been well established.

This study also examines the relationship between unethical perceptions and SME performance, confirming hypothesis 6 in a positive direction. This finding contradicts mainstream research in business ethics that supports the role of ethics in shaping positive organizational performance.Citation62,Citation63,Citation96 However, this study reinforces the rational behavioral strategic motives of doing business to secure maximum gains for their self-interests, as Adam Smith’s revelation.Citation56,Citation57 Thus, being unethical may open the windows of opportunity constrained by moral factors. No wonder these advanced chances may yield a positive result toward economic gains, eg, decreasing the quality of the products without consumers’ consent.

This research investigation has been controversial, but the academic field of business ethics has continuously strived to prove its importance. This is evident by the majority of research reports;Citation62,Citation63,Citation97 however, some academics have pointed toward the little effect of ethical investment in the market for securing substantial economic gain.Citation98,Citation99 Another academician has disputed the role of ethics in the stakeholder theory for its inability to promote better organizational performance.Citation100 Another finding reports that being ethical is less effective for small firm income but favorable for the large ones.Citation101 Conclusively, this study’s finding has added further conversation to the debates by acknowledging the self-interest motives of humanity.

This study also examines several indirect relationships between all existing variables without formulating specific hypotheses. There is an indirect effect between locus of control on the love of money and unethical perception with a reasonably substantial effect size. Locus of control is related to SMEs’ performance, mediated by the love of money and crooked perception. Unethical perception creates an indirect relationship between love of money and SME performance. There is still much controversy surrounding this study, and the relationship between business ethics commitment and financial performance remains ambiguous.Citation102 If substantial positive relationships can be formed, this will help market the ethical stance in doing business.Citation61 These mixed results on indirect relationships suggest complex relationships in the theoretical or measurement building, thus, requiring further investigation.

Conclusion

Small business entrepreneurs are subject to many internal and external inputs affecting their performance. This study advances the discussions in behavioral strategy by highlighting how locus of control, love of money, and unethical perception shape the performance of small and medium enterprises. The structural model reveals significant support for the proposed hypothesis but the locus of control relationship and SME performance. All indirect relationships are discovered to be significantly existing. This study implies that entrepreneurs must manage their control over external information and their inherent motive in doing business, as increased money-loving may deteriorate business performance. While our finding is controversial as being unethical is suitable for the economic outcome, doing business ethically is still highly expected for the sake of the community.

This study admittedly comes with several weaknesses. Further data distribution from different geographics and nationalities may present a more straightforward message. Some investigated relationships are still in the initial states; thus, they require other pieces of evidence in future studies. Further investigations would benefit from advancing the weakness and studying other behavioral aspects that might impact the strategy formulation within firms, like notable biases such as herding, overconfidence, or illusion of control. These endeavors we leave to future aspiring researchers.

Ethics Statement

This study obtained the data from Indonesian SME entrepreneurs by revealing their behavioral motives under some business ethics contexts. The participants are initially provided with the Letter of Research Conduct attached in the Google Form. The respondents agreed to participate in filling the questionnaires with recorded consent through online questionnaires. The survey does not record confidential information that may be used for inappropriate measures. The research is also conducted under the supervision of the ethical committee in the Management Department, Faculty of Islamic Economics and Business, Universitas Islam Negeri Alauddin Makassar, Indonesia.

Disclosure

The author reports no conflicts of interest in this work.

References

- Batunanggar S. Fintech development and Asian Development Bank Institute. 2019.

- Maksum IR, Sri Rahayu AY, Kusumawardhani D. A social enterprise approach to empowering micro, small and medium enterprises (SMEs) in Indonesia. J Open Innov Technol Mark Complex. 2020;6(3). doi:10.3390/JOITMC6030050

- Surya B, Menne F, Sabhan H, Suriani S, Abubakar H, Idris M. Economic growth, increasing productivity of SMEs, and open innovation. J Open Innov. 2021;7:20. doi:10.3390/joitmc7010020

- Powell TC, Lovallo D, Fox CR. Behavioral strategy4643. Strateg Manag J. 2011;32:1369–1386. doi:10.1002/smj.968

- Powell TC. Strategy as diligence: putting behavioral strategy into practice. Calif Manage Rev. 2017;59:162–190. doi:10.1177/0008125617707975

- Levinthal DA. A behavioral approach to strategy-what’s the alternative? Strateg Manag J. 2011;32:1517–1523. doi:10.1002/smj.963

- Vaitoonkiat E, Charoensukmongkol P. Stakeholder orientation’s contribution to firm performance: the moderating effect of perceived market uncertainty. Manag Res Rev. 2020;43(7):863–883. doi:10.1108/MRR-07-2019-0296

- Vaitoonkiat E, Charoensukmongkol P. Interaction effect of entrepreneurial orientation and stakeholder orientation on the business performance of firms in the steel fabrication industry in Thailand. J Entrep Emerg Econ. 2020;12(4). doi:10.1108/JEEE-05-2019-0072

- Parmitasari RDA, Syariati A. Chain reaction of behavioral bias and risky investment decision in Indonesian nascent investors. Risks. 2022;10(8):145. doi:10.3390/risks10080145

- Smith A. The theory of moral sentiments. In: The Two Narratives of Political Economy. Penguin; 2011. doi10.1002/9781118011690.ch10

- Kahneman D, Tversky A. Prospect theory: an analysis of decision under risk Daniel. Econometrica. 1979;47:263. doi:10.1017/CBO9781107415324.004

- Sarapultsev A, Sarapultsev P. Novelty, stress, and biological roots in human market behavior. Behav Sci. 2014;4(1):53–69. doi:10.3390/bs4010053

- Kumar S, Goyal N. Behavioural biases in investment decision making – a systematic literature review. Qual Res Financ Mark. 2015;7:88–108. doi:10.1108/QRFM-07-2014-0022

- Tang TLP. The meaning of money revisited: the development of the money ethic scale. J Organ Behav. 1992;13:197–202. doi:10.1002/job.4030130209

- Tang TL. The meaning of money: extension and exploration of the money ethic scale in a sample of university students in Taiwan. J Organ Behav. 1993;14:93–99. doi:10.1002/job.4030140109

- Tang TLP, Kim JK, Tang DSH. Does attitude toward money moderate the relationship between intrinsic job satisfaction and voluntary turnover? Hum Relations. 2000. doi:10.1177/a010560

- Khanifah K, Isgiyarta J, Lestari I, Udin U. The effect of gender, locus of control, love of money, and economic status on students’ ethical perception. Int J High Educ. 2019;8(5). doi:10.5430/ijhe.v8n5p168

- Brownell P. Budgeting, locus of control and organizational effectiveness. Account Rev. 1981. doi:10.1017/CBO9781107415324.004

- Li M, Tan M, Wang S, Li J, Zhang G, Zhong Y. The effect of preceding self-control on green consumption behavior: the moderating role of moral elevation. Psychol Res Behav Manag. 2021;14:2169–2180. doi:10.2147/PRBM.S341786

- Ramadhan AY, Asandimitra N. Determinants of financial management behavior of millennial generation in surabaya. J Minds Manaj Ide Dan Inspirasi. 2019;6(2):129. doi:10.24252/minds.v6i2.9506

- Di Zhang D, Bruning E. Personal characteristics and strategic orientation: entrepreneurs in Canadian manufacturing companies. Int J Entrep Behav Res. 2011;17:82–103. doi:10.1108/13552551111107525

- Lim VKG, Teo TSH, Loo GL. Sex, financial hardship and locus of control: an empirical study of attitudes towards money among Singaporean Chinese. Pers Individ Dif. 2003;34(3):411–429. doi:10.1016/S0191-8869(02)00063-6

- Forte A. Locus of control and the moral reasoning of managers. J Business Ethics. 2005;58:65–77. doi:10.1007/s10551-005-1387-6

- Chang HH, Vitell SJ, Lu LC. Consumers’ perceptions regarding questionable consumption practices in China: the impacts of personality. Asia Pacific J Mark Logist. 2019;31(3):592–608. doi:10.1108/APJML-08-2017-0168

- Alwi Z, Parmitasari RDA, Syariati A, Binti Sidik R. Hadith corresponding thoughts on the ethical interacting behavior of young entrepreneurs in Indonesia. J Asian Financ Econ Bus. 2021. doi:10.13106/jafeb.2021.vol8.no3.0331

- Susanto E. Does love of money matter for innovative work behavior in public sector organizations? Evidence from Indonesia. Int J Public Sect Manag. 2020;34:71–85. doi:10.1108/IJPSM-01-2020-0028

- Sterman JD, Henderson R, Beinhocker ED, Newman LI. Getting big too fast: strategic dynamics with increasing returns and bounded rationality. Manage Sci. 2007;53:683–696. doi:10.1287/mnsc.1060.0673

- Simon HA. Theories of Bounded Rationality. Palgrave Macmillan; 1972.

- Gavetti G, Rivkin JW. On the origin of strategy: action and cognition over time. Organ Sci. 2007;18:420–439. doi:10.1287/orsc.1070.0282

- Foss NJ, Lindenberg S. Microfoundations for strategy: a goal-framing perspective on the drivers of value creation. Acad Manag Perspect. 2013;27:85–102. doi:10.5465/amp.2012.0103

- Teece DJ. A capability theory of the firm: an economics and (Strategic) management perspective. New Zeal Econ Pap. 2019;53(1):1–43. doi:10.1080/00779954.2017.1371208

- Zahera SA, Bansal R. Do investors exhibit behavioral biases in investment decision making? A systematic review. Qual Res Financ Mark. 2018;10:210–251. doi:10.1108/QRFM-04-2017-0028

- Rzepczynski MS, Fridson MS. Beyond greed and fear: understanding behavioral finance and the psychology of investing (a review). Financ Anal J. 2000;56:112–113. doi:10.2469/faj.v56.n6.2407

- Reitzig M, Sorenson O. Biases in the selection stage of bottom-up strategy formulation. Strateg Manag J. 2013;34:782–799. doi:10.1002/smj.2047

- Olson EM, Slater SF, Hult GTM. The importance of structure and process to strategy implementation. Bus Horiz. 2005;48:47–54. doi:10.1016/j.bushor.2004.10.002

- Patel PC, Chrisman JJ. Risk abatement as a strategy for R&D investments in family firms. Strateg Manag J. 2014;35:617–627. doi:10.1002/smj.2119

- Hodgkinson GP, Healey MP. Psychological foundations of dynamic capabilities: reflexion and reflection in strategic management. Strateg Manag J. 2011;32(13):1500–1516. doi:10.1002/smj.964

- Huy QN. How middle managers’ group-focus emotions and social identities influence strategy implementation. Strateg Manag J. 2011;32:1387–1410. doi:10.1002/smj.961

- Reitzig M, Maciejovsky B. Corporate hierarchy and vertical information flow inside the firm - A behavioral view. Strateg Manag J. 2015;36:1979–1999. doi:10.1002/smj.2334

- Charoensukmongkol P. Does entrepreneurs’ improvisational behavior improve firm performance in time of crisis? Manag Res Rev. 2021. doi:10.1108/MRR-12-2020-0738

- Rotter JB. Generalized expectancies for internal versus external control of reinforcement. Psychol Monogr. 1966;80:1–28. doi:10.1037/h0092976

- Caliendo M, Cobb-Clark DA, Uhlendorff A. Locus of control and job search strategies. Rev Econ Stat. 2015;97:88–103. doi:10.1162/REST_a_00459

- Golding J, Gregory S, Iles-Caven Y, Nowicki S. The antecedents of women’s external locus of control: associations with characteristics of their parents and their early childhood. Heliyon. 2017;3:e00236. doi:10.1016/j.heliyon.2017.e00236

- Kesavayuth D, Ko KM, Zikos V. Locus of control and financial risk attitudes. Econ Model. 2018;72:122–131. doi:10.1016/j.econmod.2018.01.010

- Lee-Kelley L. Locus of control and attitudes to working in virtual teams. Int J Proj Manag. 2006;24:234–243. doi:10.1016/j.ijproman.2006.01.003

- Cherry J. The impact of normative influence and locus of control on ethical judgments and intentions: a cross-cultural comparison. J Bus Ethics. 2006;68:113–132. doi:10.1007/s10551-006-9043-3

- Chiu RK. Ethical judgment and whistleblowing intention: examining the moderating role of locus of control. J Business Ethics. 2003;43:65–74. doi:10.1023/A:1022911215204

- Howell JM, Avolio BJ. Transformational leadership, transactional leadership, locus of control, and support for innovation: key predictors of consolidated-business-unit performance. J Appl Psychol. 1993;78(6):891–902. doi:10.1037/0021-9010.78.6.891

- Wangrow DB, Kolev K, Hughes-Morgan M. Not all responses are the same: how CEO cognitions impact strategy when performance falls below aspirations. J Gen Manag. 2019. doi:10.1177/0306307018798143

- Harell A, Soroka S, Iyengar S. Locus of control and anti-immigrant sentiment in Canada, the United States, and the United Kingdom. Polit Psychol. 2017;38:245–260. doi:10.1111/pops.12338

- Sirén C, Patel PC, Örtqvist D, Wincent J. CEO burnout, managerial discretion, and firm performance: the role of CEO locus of control, structural power, and organizational factors. Long Range Plann. 2018;51:953–971. doi:10.1016/j.lrp.2018.05.002

- Tang TLP, Chen YJ. Intelligence vs. wisdom: the love of money, machiavellianism, and unethical behavior across college major and gender. J Bus Ethics. 2008;82:1–26. doi:10.1007/s10551-007-9559-1

- Tang TLP, Chiu RK. Income, money ethic, pay satisfaction, commitment, and unethical behavior: is the love of money the root of evil for Hong Kong employees? J Bus Ethics. 2003;46:13–30. doi:10.1023/A:1024731611490

- Tang TLP, Liu H. Love of money and unethical behavior intention: does an Authentic Supervisor’s Personal Integrity and Character (ASPIRE) make a difference? J Bus Ethics. 2012;107:295–312. doi:10.1007/s10551-011-1040-5

- Liu BC, Tang TLP. Does the love of money moderate the relationship between public service motivation and job satisfaction? The case of Chinese professionals in the public sector. Public Adm Rev. 2011;71:718–727. doi:10.1111/j.1540-6210.2011.02411.x

- Smith A. An Inquiry into the Wealth of Nations. London: Strahan and Cadell; 1776.

- Kumar S, Goyal N. Evidence on rationality and behavioural biases in investment decision making. Qual Res Financ Mark. 2016;8:270–287. doi:10.1108/QRFM-05-2016-0016

- Kurniansyah F, Saraswati E, Rahman AF. Corporate governance, profitability, media exposure, and firm value: the mediation role of environmental disclosure. J Minds Manaj Ide Dan Inspirasi. 2021;8(1):69. doi:10.24252/minds.v8i1.20823

- Conroy SJ, Emerson TLN. Business ethics and religion: religiosity as a predictor of ethical awareness among students. J Bus Ethics. 2004;50:383–396. doi:10.1023/B:BUSI.0000025040.41263.09

- Donaldson T, Dunfee TW. Toward a unified conception of business ethics: integrative. Acad Manag Acad Manag Rev. 1994;19:252. doi:10.2307/258705

- Trevino LK. Ethical decision making in organizations: a person-situation interactionist model. Acad Manag Rev. 1986;11:601. doi:10.5465/amr.1986.4306235

- Stanwick PA, Stanwick SD. The relationship between corporate social performance, and organizational size, financial performance, and environmental performance: an empirical examination. J Bus Ethics. 1998;17:195–204. doi:10.1023/A:1005784421547

- McMurrian RC, Matulich E. Building customer value and profitability with business ethics. J Bus Econ Res. 2016. doi:10.19030/jber.v14i3.9748

- Hair JF, Hult GTM, Ringle CM, Sarstedt M. Partial Least Squares Structural Equation Modeling (PLS-SEM). Sage Publ; 2014. doi:10.1108/EBR-10-2013-0128

- Hair J, Black W, Babin B, Anderson R. Multivariate data analysis: a global perspective. In: Multivariate Data Analysis: A Global Perspective. Vol. 7th. Springer; 2010.

- Spector PE. Development of the work locus of control scale. J Occup Psychol. 1988;61:335–340. doi:10.1111/j.2044-8325.1988.tb00470.x

- Forsyth DR. A taxonomy of ethical ideologies. J Pers Soc Psychol. 1980;39:175–184. doi:10.1037/0022-3514.39.1.175

- Tavitiyaman P, Qu H, Zhang HQ. The impact of industry force factors on resource competitive strategies and hotel performance. Int J Hosp Manag. 2011;30(3):648–657. doi:10.1016/j.ijhm.2010.11.010

- Anderson JC, Gerbing DW. Structural equation modelling by Anderson and Gerbing 1988. Psychol Bull. 1998. doi:10.1037/0033-2909.103.3.411

- Tabachnick BG, Fidell LS. Using Multivariate Statistics. 3rd ed. New York: Harper Collins; 1996.

- Bentler PM, Chou CP. Practical issues in structural modeling. Sociol Methods Res. 1987;16:78–117. doi:10.1177/0049124187016001004

- Bastardoz N, Antonakis J. Sample size requirement for unbiased estimation of structural equation models: a Monte Carlo study. Acad Manag Proc. 2014;2014:13405. doi:10.5465/ambpp.2014.13405abstract

- Yamane T. Statistics, an Introductory Analysis, 1967. New York Harper Row CO USA; 1967.

- Roscoe JT. Fundamental research statistics for the behavioural sciences (2nd edition). 1975.

- Podsakoff PM, MacKenzie SB, Lee JY, Podsakoff NP. Common method biases in behavioral research: a critical review of the literature and recommended remedies. J Appl Psychol. 2003;88(5):879–903. doi:10.1037/0021-9010.88.5.879

- Coovert MD, Goldstein M. Locus of control as a predictor of users’ attitude toward computers. Psychol Rep. 1980;47:1167–1173. doi:10.2466/pr0.1980.47.3f.1167

- Tang TLP, Tillery KR, Lazarevski B, Luna-Arocas R. The love of money and work-related attitudes: money profiles in Macedonia. J Manag Psychol. 2004. doi:10.1108/02683940410543614

- Kleiber DA, Crandall R. Leisure and work ethics and locus of control. Leis Sci. 1981;4:477–485. doi:10.1080/01490408109512982

- Jones GE, Kavanagh MJ. An experimental examination of the effects of individual and situational factors on unethical behavioral intentions in the workplace. J Bus Ethics. 1996;15:511–523. doi:10.1007/BF00381927

- Kusvanti H, Suhendro S, Dewi RR. Individual factors that influence the ethical behavior of accounting student. eBA J Econ Business Account. 2019;5:1–10. doi:10.32492/eba.v5i1.705

- Valentine SR, Hanson SK, Fleischman GM. The presence of ethics codes and employees’ internal locus of control, social aversion/ malevolence, and ethical judgment of incivility: a study of smaller organizations. J Bus Ethics. 2019;160:657–674. doi:10.1007/s10551-018-3880-8

- Reiss MC, Mitra K. The effects of individual difference factors on the acceptability of ethical and unethical workplace behaviors. J Bus Ethics. 1998;17:1581–1593. doi:10.1023/A:1005742408725

- Boone C, Van Olffen W, Van Witteloostuijn A. Team locus-of-control composition, leadership structure, information acquisition, and financial performance: a business simulation study. Acad Manag J. 2005;48:889–909. doi:10.5465/AMJ.2005.18803929

- Teece DJ, Pisano G, Shuen A. Dynamic capabilities and strategic management. Strateg Manag J. 1997;18(7):509–533. doi:10.1002/(SICI)1097-0266(199708)18:7<509::AID-SMJ882>3.0.CO;2-Z

- Teece DJ. Explicating dynamic capabilities: the nature and microfoundations of (sustainable) enterprise performance. Strateg Manag J. 2007;28:1319–1350. doi:10.1002/smj.640

- Amar MY, Syariati A, Ridwan R, Parmitasari RDA. Indonesian hotels’ dynamic capability under the risks of covid-19. Risks. 2021;9(11):194. doi:10.3390/risks9110194

- Amar MY, Syariati A, Rahim FR. Enhancing hotel industry performance through service based resources and strategic entrepreneurship (case study at hotel industries in Indonesia). Acad Entrep J. 2019;25(3):1–10.

- Hitt M, Ireland R, Sirmon D, Trahms C. Strategic entrepreneurship: creating value for individuals, organizations, and society. Acad Manag Perspect. 2011. doi:10.5465/AMP.2011.61020802

- Syariati A, Amar MY, Syariati NE. The strategic choices in achieving tourism’s competitiveness and performance among hotels in Indonesia. Geoj Tour Geosites. 2021;38(4). doi:10.30892/gtg.38429-763

- Singhapakdi A, Vitell SJ, Lee DJ, Nisius AM, Yu GB. The influence of love of money and religiosity on ethical decision-making in marketing. J Bus Ethics. 2013;114:183–191. doi:10.1007/s10551-012-1334-2

- Tang TLP, Sutarso T, Ansari MA, et al. Monetary intelligence and behavioral economics: the Enron effect—love of money, corporate ethical values, Corruption Perceptions Index (CPI), and dishonesty across 31 geopolitical entities. J Bus Ethics. 2018;148(4):919–937. doi:10.1007/s10551-015-2942-4

- Luna-Arocas R, Tang TLP. The love of money, satisfaction, and the protestant work ethic: money profiles among university professors in the USA and Spain. J Bus Ethics. 2004;50:329–354. doi:10.1023/B:BUSI.0000025081.51622.2f

- Tremellen K, Everingham S. For love or money? Australian attitudes to financially compensated (commercial) surrogacy. Aust NZ J Obstet Gynaecol. 2016;56:558–563. doi:10.1111/ajo.12559

- Tang TLP, Sutarso T. Falling or not falling into temptation? Multiple faces of temptation, monetary intelligence, and unethical intentions across gender. J Bus Ethics. 2013;116:529–552. doi:10.1007/s10551-012-1475-3

- Jia S, Zhang W, Li P, Feng T, Li H. Attitude toward money modulates outcome processing: an ERP study. Soc Neurosci. 2013;8:43–51. doi:10.1080/17470919.2012.713316

- Harrison JS, Wicks AC. Stakeholder theory, value, and firm performance. Bus Ethics Q. 2013;23(1):97–124. doi:10.5840/beq20132314

- Mohammad J, Quoquab F, Idris F, Al-Jabari M, Hussin N, Wishah R. The relationship between Islamic work ethic and workplace outcome: a partial least squares approach. Pers Rev. 2018;47(7):1286–1308. doi:10.1108/PR-05-2017-0138

- Abdelsalam O, Duygun M, Matallín-Sáez JC, Tortosa-Ausina E. Do ethics imply persistence? The case of Islamic and socially responsible funds. J Bank Financ. 2014;40:182–194. doi:10.1016/j.jbankfin.2013.11.027

- Dawkins C, Fraas JW. Coming clean: the impact of environmental performance and visibility on corporate climate change disclosure. J Bus Ethics. 2011;100(2):303–322. doi:10.1007/s10551-010-0681-0

- Sternberg E. The defects of stakeholder theory. Corp Gov an Int Rev. 1997;5(1):3–10. doi:10.1111/1467-8683.00034

- Longenecker JG, Moore CW, Petty JW, Palich LE, McKinney JA. Ethical attitudes in small businesses and large corporations: theory and empirical findings from a tracking study spanning three decades. J Small Bus Manag. 2006;44:167–183. doi:10.1111/j.1540-627X.2006.00162.x

- Sumampouw OO. The use of small capital selling snacks as a business opportunity in the Langowan shopping complex. Asia Pacific J Manag Educ. 2021;4(1):1–8. doi:10.32535/apjme.v4i1.1047