Abstract

Purpose

The novel study describes the behXavioural phenomena of family firm types and explores the relationship between the family firm types of control diversity and Research and Development (R&D) investments. Acquiring controlling rights is a psychological phenomenon for family firm owners. The moderating effect of CEO compensations on R&D investments is investigated.

Methodology

We collected data of listed A-share family firms in China from 2011 to 2020 in the China Stock Market and Accounting Research database. We used Tobit regression for data analysis.

Results/Finding

The study concludes that lone-controller family firms (LCFFs) are less willing to invest in R&D and multi-controller family firms (MCFFs) have positive behaviour towards R&D. The moderating role of CEO compensation deviates the willingness and behaviour to invest in R&D.

Conclusion/Originality

To the best of our knowledge, this study is the first to outline the paradoxical empirical evidence on family firms and R&D investments by analysing control diversity and how the moderating role of CEO compensation nexus can alter willingness towards R&D. The study is a novel attempt following De Massis et al’s framework to test the willingness and ability of LCFFs and MCFFs. Previous studies based on agency theory have tacitly assumed that ability and willingness exist in family-controlled firms. However, this study challenges this implicit assumption.

Introduction

Family firms have the attention of scholars as potential Research and Development (R&D) investments, eg,Citation1–3 due to significance of R&D, economic growth, and the ubiquity form of controlling family firms, eg.Citation2,Citation4 R&D investment is recognized as a rudimentary driver of small and medium-sized (SME) firm performance.Citation5 As a major element of innovation, R&D expenditure supports economic growth, value, and profitability of firms, eg.Citation6 From 1964 to 1991, the willingness of family firms to invest in R&D innovation was minimal, eg.Citation7 This legacy continues, as the nature of family firms tend to adopt a conservative policy with respect to growth strategies,Citation8 limiting growth rates by avoiding debt.Citation9

The tendency started with the founder, and founding family firms tended to use less debt.Citation10 Later, Morck and YeungCitation11 revealed that succession-controlled family firms invest less in R&D than the non-succession controlled family firms, regardless of the variation of age and size of the same industry. The explanation of these results could be the importance of survival as well as family employment rather than to maximize profits or market return.Citation12 However, the firm’s market share and growth rate influenced change for family firms to use debtCitation13 to support R&D expenses. Owing to the strong support of the theoretical reasoning, scholars agree that the control mechanism of family firms is different from non-family firms, due to the nature of the organizational goals, exposure to risks, and investment prospect, eg.Citation14,Citation15 Acquiring controlling rights is a psychological phenomenon for family firm owners.Citation12 Additionally, according to the upper echelons theory, stock ownership is a characteristic of “executive compensation” that is said to accentuate the effect of owners psychological phenomena on their ability to make and implement strategic decisions.Citation16 However, within the control mechanism, how family members with controlling rights affect the decision on R&D lacks research for family businesses. To fill this gap, this study categorizes Chinese family firms with respect to control diversity.

Family firms are heterogeneous and possess multiple behaviours towards R&D investments,Citation17 which depend on the ability and willingness of controllers.Citation1 We argue that a lone-controller family firm, where no other family member participates in the decision process, allows freedom from compromise with multiple controllers or family members for the controller in R&D decisions. Additionally, LCFFs may not face the behavioural agency issues. Individuals are more concerned with losses as compared to gains.Citation18,Citation19 Some researchers indicate that family owners have socio-emotional wealth, while other researchers, eg, Zellweger and AstrachanCitation20 suggest they have emotional value to do the same. Gómez-Mejía et al empirically indicated that the yearning to preserve socio-emotional wealth can strengthenCitation21 the risk of compensation reduction for family leaders.Citation22 The priority of maintaining family control, even when this upsurges business risk,Citation7 is a propensity to avoid diversification that may reduce business risk and increase control risk.Citation23

According to Tsao et al,Citation24 the sensitivity of R&D investments with respect to CEO compensation is larger in the family firms compared to non-family firms, and some CEOs are paid more than the R&D investment level. However, CEO compensation is a dearth contextual factor in family business governance literature, while extant research shows the relationship between executive incentives and risks.Citation25–27 Examining the compensation effect of executives between family firms owners and R&D is important, because many scholars explored how managerial incentives alter the myopic aversion of family and non-family firms, eg.Citation28,Citation29 Research on the effect of the managerial compensation configuration within Chinese family firms is lacking. This study explores the different types of family firms and their effect on R&D with the moderating role of CEO compensation. Compensation is a major factor for motivation, which can alter output and investment preferences. The executives’ compensation moderates between family firms and downside risk,Citation30 sold relationship found between managerial incentives and risk preferences behaviour by executive management, eg.Citation25,Citation26 Family firms have significant difference in single- and dual-class companies with respect to executive compensation.Citation31,Citation32

This study aims to investigate the relationship between the family firm’s control diversity and R&D investments and how CEO compensation moderates R&D investments for these firms by applyingCitation1 an ability and willingness framework. Specifically, we examined how the LCFFs (without other family members), MCFFs (with multiple family members), and CEO compensation alter R&D investment of family firms in the emerging economy. Ability is the family’s freedom of choice to assign, allocate, purchase, or sell the firm’s economic resources.Citation1 It includes choosing the firm’s goals and decisions relating to strategy, structure, and tactics.Citation33,Citation34 Willingness is the involved family’s favourable disposition to be involved in distinguishing behaviour.Citation1 It incorporates the goals, targets, and motivations that stimulate the firm’s behaviour in directions different to non-family engaged firms.

This study makes three important contributions to the literature on family firm governance, specifically in the areas of control diversity and the moderating role of CEO compensation in R&D investments. First, by using De Massis et al’sCitation1 ability and willingness framework, we extend the research in the emerging markets by dividing the control diversity as lone-controller family firms and multi-controller family firms as the control mechanism of family firms for the first time. The study differentiates the behaviour of LCFFs and MCFFs towards risk preference. We observed that the LCFFs have negative effect, while MCFFs have positive effect, on R&D investment. Second, we demonstrated that CEO compensation modifies R&D investment behaviour for both types of family firms in the emerging markets and showed that executive compensation may alter the motivation level towards risk preference. A good compensation package motivates executives.Citation35 The prior study explored that if the compensation structure of CEOs is based on the R&D investments, it helps in value-enhancing.Citation24 Motivation of executives add firm value.Citation36 Third, prior research, trusting on the agency theory,Citation37–39 assumed that family firms have both ability and willingness. However, we negate this implicit assumption and argue that all family firms have ability, but willingness depends on the controller’s behaviour, attitude, and financial and non-financial objectives. Additionally, we explored that the LCFFs have greater R&D investments than multi-controller family firms.

The rest of the paper is structured as follows. Hypothesis Development provides a literature review and theoretical framework. Sample and Data contain the data, and Results delineates the identification plan and provides summary statistics. Discussion and Conclusion shows the empirical results of the study and a collection of robustness checks. Finally, Conclusion presents the summary and concludes the study and future recommendations.

Theoretical Framework

Behavioural Agency Model

The executive’s or controller’s shortcomings of risk preference and risk-taking behaviour are addressed in the behavioural agency model (BAM).Citation18 The BAM advocates that executive’s behavioural preferences are formed by outlining the problem and loss aversion. The BAM is an important framework that explains mechanisms that link executive behaviour, incentives, risk preference, and the type of high-performance outcomes.Citation40 Scholars argue that behavioural agency theory is a good platform for theorizing executive compensation and is a better framework for correcting recommendations about executive compensation strategies. Moreover, behavioural agency theory enhances the theory of agent behaviour. According to Wiseman and Gomez-Mejia,Citation18 BAM indicates that senior executives are primarily loss averse and secondarily risk averse.

While CEO compensation is part of motivation, and the motivation impacts firm value and risk preference, when considering BAM, scholars argue that to measure the optimal performance of competent executives, the executives must be properly motivated.Citation41 BAM supports an observing cost and incentive alignment,Citation42,Citation43 and behavioural agency theory considers motivation of duties and performance, arguing that when firm executives have motivation to perform their best and implement available strategies effectively, shareholders interest and their agents are aligned.Citation40 According to Camerer et al,Citation44 behavioural agency theory has four constructs that are the main factors affecting the behaviour: (1) loss aversion and reference dependence; (2) preferences relating to risky and uncertain outcomes; (3) temporal discounting; and (4) fairness and inequity aversion.

If executives believe that their skills, efforts, and abilities on the job are rewarded (tangibly or intangibly) fairly and sufficiently according to productivity, they will be happy and will be motivated to perform duties in an excellent way to add value.Citation36 Conversely, if the relationship between input and output are unbalanced, then executives are demotivated.Citation40

Hypothesis Development

Family Firm’s Control Diversity and R&D Investment

A family firm’s R&D expenditure differs concerning firm ownership and management.Citation45 If family ownership is less than 30%, R&D is less when compared with firms with family ownership greater than 30%.Citation46 This indicates that the relationship between R&D investment and family ownership is nonlinear. However, separating ownership and control may instigate a manager’s opportunistic behaviours in R&D investments,Citation47 which means that the lone controller minimizes the manager’s opportunistic behaviours. According to recent agency theory research, individual shareholders can have a variety of motives and desires. As a result, some research on the relationship between innovation funding and corporate governance have inconclusive findings.Citation48

Numerous researches examined the founders’ and their families’ impact on R&D investment decisions.Citation38,Citation39,Citation49,Citation50 According to prior research, families are distinct from other investors in that their undiversified equity and human capital can promote risk aversion, resulting in decreased R&D investment.Citation51 Other research indicates that family-owned businesses are less likely to invest in innovation than other types of businesses.Citation52

Additionally, a family could have capital-rationed financing considerations in order to preserve the firm’s controlling rights. This constraint also contributes to the pressure to cut R&D spending.Citation49 Additionally, some studies indicate that publicly traded companies face pressure from external investors to maximise short-term profits, which may result in R&D under investment.Citation49,Citation53,Citation54 However, family firms seek to safeguard family’s capital in order to transfer the company on to their descendants and future generations, and are thus believed to have less agency tension between owners and managers than other types of firms.

According to behavioural agency theory, firms that tend to be risk averse and are motivated to secure jobs, family, security, and social welfare may be inclined to minimize R&D investment; as such investments reduce firm profitability. Additionally, the higher failure rates of R&D investments may lead to lone controllers preferring short-term profitability and avoiding long-term R&D investments. However, when the family’s control or future progress is at risk, family firms can change behaviours.Citation13,Citation55,Citation56 Studies highlight these contradictory research outcomes, calling for further research to enhance the understanding of family firm risk preferences.

Agency costs are an important issue for R&D investments. Interestingly, the agency costs are zero when the firm is managed by family owners as the firm’s benefit equals the owner’s benefits.Citation57 Moreover, the benefits of alignment of interests between family owners and family management lower agency costs.Citation47,Citation58 Alignment of interests between lenders and family owners leads to lower agency costs.Citation59 However, according to Chrisman and Patel,Citation50 this idea of zero or minimal agency costs prevails in the family firms due to the expectations that lead to the altruistic behaviours within family members. The family association produces a moral obligation to help family members regardless of cultural variation.Citation60 According to Becker,Citation61 altruism by one family member will motivate a self-centred family member to act for the sake of the family. It further indicates that the close family members choose actions that maximize family income, leading to better financial performance when compared to non-family firms. Additionally, when ownership is intended to transfer to the next generation, family firms tend to invest in R&D for the long term.Citation62 Additionally, a higher degree of trustworthiness in family firms may result in investing more in R&D Dyer Jr and Whetten.Citation63 The transfer of ownership and control of the firm to the next generation leads to long-term alignment of financial goals and the intact legacy of family values. Therefore, the following hypotheses are proposed:

H1: Lone-controller family firms, without other family member involvement, have a negative relationship with R&D.

H2: Multi-controller family firms, with family member involvement, have a positive relationship with R&D.

CEO Compensation, Family Firms Control Diversity, and R&D Investment

A firm’s risk preference may be altered by executive compensations and incentives. According to Alessandri et al,Citation30 providing larger stock ownership to managers induces greater risks in the long run for non-family firms rather than family firms. Conversely, larger cash incentives to executives reduce family firm’s risk in the short term compared to their counterparts. Additionally, diverse forms of executive compensations inspire diverse time latitudes, eg.Citation28,Citation29,Citation64 Executive compensation and incentives may diversely affect the degree of myopic loss aversion and a firm’s risk preferences. Therefore, executives compensations and incentives can impact risk preferences based on a firm’s investment time latitude.Citation30 The empirical research on this topic reveals a significant relationship with compensation and innovation. According to Ryan and Wiggins,Citation65 R&D is favourably associated to equity-based pay. Coles et alCitation66 discovered a positive relationship between incentives from the convexity of performance-linked remuneration and R&D spending.

Chinese family firms have three types of CEOs: CEOs from family who are controllers; CEOs from outside the family who are not controllers; and CEOs from family who are not controllers.Citation67,Citation68 Family firms choose the CEO type based on qualification and compensation package.Citation60,Citation69 Family CEOs possess non-financial objectives that may affect willingness for R&D investment. Agency theory advocates the likely encounter of interest between family firm owners and professional CEOs.

Considering the lone controller short-term profit maximization arguments, the myopic short-term R&D investment tendency of family firms can be mitigated by the CEO compensations.Citation70 Lone controller family firms possess more power to make investment decisions and enjoy supreme authority to exploit the firm’s policy and strategy but are focused on the firm’s short-term profit maximization to mitigate family members’ financial and societal needs.Citation71 These firms possess a limited resources pool of the owning familyCitation72 and altruism towards members of the owning family. However, family firms realize that investment in R&D is essential. As such, family firms formulate CEO compensation to motivate CEO’s approval of R&D investments, which advocates that lone controller family firms moderate the relationship between CEO compensation and R&D investments. Conversely, multi-controller family firms may consider that their joint decision is enough for the success and growth of the business and that CEO compensation may not be an influence on the firm’s R&D investments. Therefore, the following hypotheses are proposed:

H3: The moderating role of CEO compensations in lone controller family firms has a positive impact on R&D investments.

H4: The moderating role of CEO compensations in multiple-controller family firms has a negative impact on R&D investments.

Methodology

Sample and Data

This study is focused on different types of family firms, uses data collected from the China Stock Market and Accounting Research Database (CSMAR), specifically data of A-share firms listed on the Shenzhen Stock Exchange or Shanghai Stock Exchange. CSMAR is a wide-ranging and appropriate database for publicly listed Chinese firms.Citation73 We excluded all State-Owned (SOEs) firms and firms having missing values of revenues, total assets, or total liabilities. For the analysis, we used panel data from 2011 to 2020. We used winsor2 technique at 1st and 99th percentile to remove extreme values.Citation73,Citation74 To remove bias from the results, we excluded firms from lone-controller family firms where the CEO and controller was the same person. In the empirical model, we diminished possible biases for omitted variables and endogeneity by applying two actions. First, we controlled the year and industry effect by creating dummies of both. Second, we took one-year lag on all independent variables. The final analysis yielded a final sample of 1943 firms.

Variables

Family Firms

This study follows the categorization of the family business provided by the China Stock Market and Accounting Research Database (CSMAR) database. Three forms of family-controlled firms exist, and we explore two forms and use the third for reference. First, a family business where only one family member controls the business and where other family members have no control rights is called a lone-controller family firm (LCFFs). Many studies consider this type of family firm for research.Citation37–39 Second, a business in which other family members have control rights is known as a multi-controller family firm (MCFFs). Apart from the controller, at least one family member holds, manages, and controls the business of the listed company or the supervisory shareholder company. CSMAR also defines a family member according to the control rights. LCFFs can change status to MCFF at any time during the business cycle. LCFF companies are known as non-board family (NBF) firm, where no other family member has a controlling role.Citation75 According to Claessens et al,Citation76 the sole regulator is the main owner with more than half of the company’s voting rights. Third, the real controller is a group of independent people outside the family.

R&D Investment

R&D investment is a dependent variable measured by annual expenditure divided by total sales at the end of the year.Citation77–82 Additionally, we calculated the ratio of R&D expenditure and total assets at the end of the year.Citation24,Citation83,Citation84

CEO Compensation

CEO compensation means the total remuneration received by a CEO in a year, excluding bonuses. As the distribution of pay is highly skewed, the logarithmic transformation is taken.Citation85

Control Variables

Variables were established to control firm-specific characteristics which follows previous research.Citation17,Citation39,Citation86–90 Accordingly, we included variables to control for the following: leverage, measured as total debt scaled by total assets; CEO tenure (CEO_tenure); CEO overconfidence (overconfidence=1, otherwise 0); independent director ratio (Ind_director_ratio), measured as board size divided by independent directors on the board; number of board meetings each year (NOB_meetings); if the board chair is a family member (Is_chair_family); age of the firm (Firm_age); firm size (Size); firm’s returns on equity (ROE); size of the board (Board size); and institutional shareholding; Patent application is measured by taking the natural logarithm of total counts of patent application; Family CEO is the CEO of family member then the value assigned is 1 otherwise 0; The percentage of stock owned by individual investors or large-block shareholders (Ultimate ownership).

Econometric Model

We developed a baseline econometric model to measure the impact of family firm types on R&D investment by controlling year- and industry-fixed effects.

where R&Dit investment is the dependent variable. FFTi is type of family firm (lone-controller family firms and multi-controller family firms). Controlit are firm-level control variables. Yrt is year-fixed effects, indi is industry-fixed effects, and are standard errors.

Further, to investigate the moderating impact of CEO compensation on the relationship between firm type and R&D investment, we extend the baseline model as

where CEO_PAYit is CEO compensation, and CEO_PAYit *FFTi is the interaction term of CEO compensation with firm type. Other variables are the same as for Model (1).

Furthermore, we apply Tobit regression to test the robustness and present the model as

Results

We applied a mean comparison test on the data set to determine if the firm types have similar or different means. The t-statistics values and their significance levels are reported in . On average, the numbers of multi-controller family firms were higher than the other two types of firms. Most variables have a t-test score indicating significance. The R&D investment has lower mean value in multi-controller family firms as compared to the lone controller family firms. CEO pay has fewer variances of mean values between lone controller family firms and multi-controller family firms.

Table 1 Mean Comparison Test

indicates that the proportion of firms studied were 32% LCFF and 61% MCFF. Results in report descriptive statistics and indicate that Chinese family firm’s invest 1.18% of the total sales in R&D. In the fast-growing Chinese economy, some family firms invest a maximum in innovation, up to 40% of the total sales for R&D. This indicates that family firms boost the Chinese economy through innovation.Citation91 After taking the log, the average CEO pay is 12.51.

Table 2 Descriptive Statistics

The results in show that the lone-controller family firms R&D investment ratio (1.14%) is higher than the multi-controller family firms (0.86%) this difference is statistically significant. The regression outcomes indicate that an increase of lone-controller family firms decreases R&D investment by 0.0334%.

Table 3 LCFF & MCFF Descriptive analysis

We ran the pair-wise correlation to remove the multi-collinearity effect. shows the R&D investment significantly positively correlates with LCFFs; therefore, MCFFs are significantly negatively correlated. The moderating variable CEO pay has significant positive associations with R&D investment. shows the value of variance inflation factors (VIF). All values are less than 2, meaning there is no multi-collinearity.Citation92–94

Table 4 Pearson’s Pairwise Correlation Matrix

We report regression outcomes in , which indicates that H1 and H2 showed significant results. LCFFs behave negatively towards R&D investment and MCFFs showed positive behaviour towards R&D investment. It means that, the MCFFs have more willingness towards R&D investment. presents the regression consequence of family firm types R&D investment with the moderating role of CEO compensation. CEO compensation altered willingness towards R&D investment of LCFFs. With the moderating effect of CEO compensation, LCFFs are more willing to invest in long-term risky projects. MCFFs have a significant negative effect on R&D with the moderating role of CEO compensation, which supports hypothesis H4. With the moderation of CEO compensation, willingness changed from positive to negative for R&D investment, supporting studies that indicate CEO compensations are sensitive in family firms, especially towards R&D investment.Citation24

Table 5 Regression Results Without Moderation

Table 6 Regression Results with Moderation

Robustness

In , we applied the Tobit regression model for the main results and also applied the pooled OLS regression model for robustness. We found qualitatively similar outcomes. We again checked the robustness of the regression results which are presented in . We changed the R&D scale from the sale to assets and reran our main models. We found a qualitatively similar outcome.

Table 7 Robust Regression Results Without Moderating Variables and R&D Scale Change Sale to Assets

With the moderating role of CEO compensation, LCFFs have a positive effect on R&D. However, MCFFs behave negatively towards R&D investment. For the purpose of robustness, we reran our results with a pooled OLS regression model, and the last two columns of present the outcomes. also presents the robust results, in first two columns, we changed the R&D scale from the sale to assets and reran our main models. We found qualitatively similar outcome. In the last two columns of , we changed the moderating variable, CEO compensation, to the top five executives’ pay and checked the robustness. The results are qualitatively similar.

Table 8 Robust Regression Results with Moderating Variables

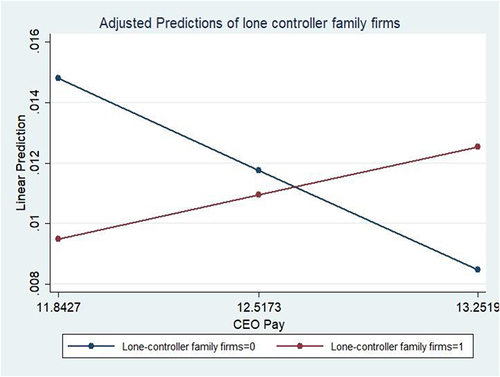

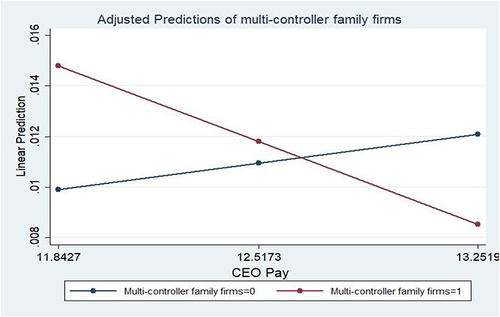

Graphical Explanation of Moderating Effect

present the moderating role of CEO compensation. reports the moderating role of CEO compensation between LCFFs and R&D investment. The red line growing up means that LCFFs behave positively towards R&D investment with the moderating effect of CEO compensation and the blue line shows that other types of family firms have negative behaviours to R&D. reports the moderating role of CEO compensations between MCFFs and R&D. The red line going down means the behaviour of MCFFs has been moderated negatively by CEO compensations towards R&D investment. The blue line indicates that other types of family firms have positive behaviours toward R&D.

Figure 1 Moderating effect of CEO pay on LCFF-R&D investment.

Figure 2 Moderating effect of CEO pay on MCFF-R&D investment.

Discussion

Our hypothesis H1 showed significant results. LCFFs behave negatively towards R&D investment. LCFFs showed less willingness to invest in R&D. The behavioural agency theory suggested, family firms tend to be risk averse and are interested to secure jobs and family security, may be inclined to minimize R&D investment, as such investments reduce firm profitability. Moreover, the more decline rates of R&D investments may lead to lone controllers choosing short-term profitability and evading long-term R&D investments. However, when the family’s control or future progress is at risk, family firms can change behaviours.Citation13,Citation55,Citation56 May be the lone controller do not have professional qualification.Citation95 As a result, LCFFs did not invest in high-risk projects due to information asymmetry. This study demonstrates that in LCFFs the controller did not trust other family members and made decisions solely. They are willing to invest in short-term, not long-term (riskier), projects. The high ownership concentration offers decision power (ability) and incentives (willingness) on the basis of the broader prospect. According to Zulfiqar and HussainCitation94 shareholders can exercise their statutory rights in strategic decision-making of a company due to ownership structure concentration. In family firm research, this is the one contribution of this study. Family owners are able to encourage more effective R&D investment than non-family owners because they stay with the company for a longer period of time and are therefore more committed to their employees and organisation.Citation96 Lone controller family firms (LCFF) are more willing to invest in long-term projects and multi-controller family firms (MCFF) show less willingness to invest in the risky projects.Citation95 Our results show that LCFFs and MCFFs rights intend to protect their socio-emotional wealth and engage in non-economic activities. Family owner (CEO) is more willing to invest in long-term projects.

indicates that MCFFs invest in long-term projects. When multiple family members are the controllers, they are more willing to invest in R&D. In this way, hypothesis H2 contradicts the behavioural agency theory, because the behavioural phenomena argued that the family firms are risk-averse and avoid investing in long-term risky projects. This is the contribution of the study. Previous studies used the agency theory and considered ability and willingness in family firms.Citation38,Citation39,Citation97,Citation98 We demonstrated that family firms have only ability, and willingness depends on behaviour, attitude, and objectives (financial or non-financial). Additionally, family firms have non-economic objectives to protect socio-emotional wealth and make family-oriented decisions accordingly.Citation99,Citation100 Therefore, willingness predicts the behaviour of family firm controllers. Unlike other studies, we followed the “ability and willingness” framework of De Massis et alCitation1 on different types of Chinese family firms (see Appendix-A). To explore the differentiated effects of ability and willingness of firms, many scholars have adopted the framework of De Massis et al. This method explains that all the firms have the ability, but the willingness to do may vary due to different firm characteristics. The sign of regression output shows the willingness of the firm (see Appendix-B). This similar approach has been adopted by many studies such as those of Bozec and Di Vito and Debellis et al.Citation17,Citation101

Considering hypothesis H2, family firms have non-financial incentivesCitation102 when they have ability (discretion power), and the agency theory does not consider this critical limitation. When the short-term and accrual-basis earnings declined and debt violates contract, family firms use non-financial incentives to protect family and firms’ reputations. Family firm controllers avoid myopic R&D investment and invest in the long-term projects to care for minority shareholders.Citation103 Moreover, when the family firm objectives lead to long-term goals, strategic time horizons lengthen and controllers become less risk-averse and increase investment in R&D.Citation50 Furthermore, the study demonstrates that Chinese family-controlled businesses are heterogeneous with regard to risky investment.Citation95 In this situation, controllers set goals that consider next generations.

Family firms are heterogeneous.Citation38,Citation104,Citation105 The heterogeneity of family firms can be better understood through their governance mechanism. Many scholars have stated that the major source of heterogeneity in family firms lies in the nature of family involvement in governance, ownership and management. Miller etalCitation38,Citation104,Citation105 also stated that family firms are not homogenous. Anderson and ReebCitation106 stated that family firm heterogeneity depends upon the combination of family and non-family members in the management. These scholars also suggested that family firm performance also largely depends on whether the CEO of the firm is a family member or non-family. As evident from previous discussion that governance is one of the fundamental sources of family firm heterogeneity, ChrismanCitation107 further stated that governance in a family firm either originates from inside or outside the organization through formal and informal mechanisms.

Here, no other family member controls the activities; therefore, LCFFs can take R&D investment decision without any hindrance. LCFFs may have longer-term decision-making than the multi-controller family firms (MCFFs) and non-family-controlled firms. Previous study evidenced that lone-founder-controlled family firms have positively influenced the R&D investment willingness.Citation108 Businesses analyse and predict the risk rate before investment in R&D and should have patience and could bear uncertainty.Citation109

The results in show that the lone-controller family firms R&D investment ratio (1.14%) is higher than the multi-controller family firms (0.86%) this difference is statistically significant. LCFF are investing a larger percentage of their budget for innovation input as compared to multi-controller family firms. Surprisingly, the regression outcomes indicate that an increase of lone-controller family firms decreases R&D investment by 0.0334%. This decrease in investment is may be due to the lack of professional qualification or an unprofessional team of the lone controller.

However, MCFFs have less budget than LCFFs. This means that the MCFFs make important decisions by consensus. Therefore, we predict that controllers make investment decisions in long-term risky projects based on professional qualifications and experience as well as analytical judgments of the market information.

CEO compensation renewed willingness towards R&D investment of LCFFs. With the moderating effect of CEO compensation, LCFFs are more willing to invest in long term risky projects. A CEO, whether or not a member of the family with professionalism and acquired compensation, might act for the welfare of the family firm reputation and for minority shareholders. Usually, good compensation packages are used for the motivation of executives.Citation35 The prior study explored that if the compensation structure of CEOs is based on the R&D investments, it helps in value-enhancingCitation22,Citation24 discovered that the positive influence of R&D investment on the proportion of CEO compensation is attributed to a long-term earning in family-controlled firm.

MCFFs have a statistically significant negative impact on R&D, with CEO remuneration acting as a moderating, which supports hypothesis H4. The moderation of CEO remuneration resulted in a shift from a positive to a negative attitude towards R&D investment, corroborating research that has found that CEO compensation in family businesses, particularly in relation to R&D investment, is sensitive.Citation24 Our hypothesis supports the behavioural agency theory with the moderating role of CEO compensations that outline how family firms are risk-averse and do not want to invest in long-term risky projects. As there are three types of CEO in family firms, they should have different behaviours, attitudes, and willingness towards R&D investment. Prior studies established that CEO compensations are 13% lower in MCFFs and 56% higher when the CEO is the lone controller.Citation110 To protect the SEW may affect the R&D investment.Citation111 The relationship between family businesses and innovation is negatively moderated by CEO pay, which must be seriously handled to decrease agency costs.Citation112

Sometimes the undiversified nature of family ownership may motivate family owners to maintain control and pay less to CEOs. As a result, CEOs do not have the motivation to invest in long-term risky projects. Many large shareholders are family owners who hold an undiversified investment portfolio and attempt to carry the risk themselves.Citation24

Conclusion

Using data for 2011–2020 compiled by the Chinese Stock Market & Accounting Research (CSMAR) database, this study investigated the behavioural phenomena of family firms on R&D investment and explored that family firms are heterogeneous. To the best of our knowledge, this is the first study to categorize family firms with unique ownership characteristics between lone-controller family firms and multi-controller family firms. We described our findings using the particularistic behaviour model of family firms.Citation1 We proved that family firms’ types behave differently regarding R&D investment. According to our findings, family businesses should maintain their investment in R&D in order to increase their firm’s higher value. We investigated the R&D investment behaviour of lone controller family firms and multi-controller family firms, with CEO compensation playing a moderating role. This study adds to the research evidence on the family business and governance by providing a comprehensive understanding of family firm control types as well as CEO compensation influence on R&D investments in the emerging economies.

We concluded that LCFFs without family members (H1) are less willing to invest in R&D and multi-controller family firms with family members (H2) have a positive behaviour toward R&D investment. The moderating role of CEO compensation deviates the willingness and behaviour to invest in R&D. Different CEO types have different behaviours. We concluded that, with the moderating role of CEO compensation, LCFFs have positive behaviour towards R&D investment and MCFFs have negative behaviour.

Practical Implications

This study has several practical implications. This study has important implication for firm owners/controllers as it demonstrates that controlling rights are very crucial for determining the R&D investment behaviour of LCFFs and MCFFs. The findings suggest that the family control firms engage in protecting socio-emotional wealth, which decrease the willingness to invest in R&D. Nevertheless, for Chinese MCFFs, hypothesis H2 contradicts the behavioural agency theory, even when these firms suffer unusual conditions. Moreover, LCFFs with the moderating role of CEO compensations contradicts the behavioural agency theory.

Family firms are predominant worldwide, and several countries’ economic growth depends on them. This study shows that setting CEO compensations packages is important for performance and continuous innovation of firms. This study will help investors in knowing which type of family firms are willing to invest in R&D. Innovation in family firms plays a vital role in economic growth. The only way for family firms to enhance value is by investing in R&D.

Limitations and Future Recommendations

This work has few limitations that offer future research opportunities. Firstly, this study has focused on Chinese family firms only. Secondly, the family firms can be categorized on the basis of different characteristics, whereas in the current study, family firm types have been considered on the basis of controlling rights. With respect to controlling rights, family firms are categorized into three categories. However, the researcher has considered only two types due to the study objectives and requirements. In this study we have used data from 2011–2020 due to non-availability of data for the latest years. Furthermore, researchers are also encouraged to compare the results of the current study with non-family firms and state-owned firms.

Data Sharing Statement

The data presented in this study are available on request from the corresponding author.

Ethical Approval

This article does not require approval from an Institutional Review Board or Ethics Committee. In this study we have used secondary data. It is publicly available on CSMAR, through a paid source. This article does not include any studies with human and animal participants performed by any of the authors.

Informed Consent

This article does not contain any studies with human participants performed by any of the authors.

Author Contributions

All authors made a significant contribution to the work reported, whether that is in the conception, study design, execution, acquisition of data, analysis, and interpretation, or in all these areas; took part in drafting, revising, or critically reviewing the article; gave final approval of the version to be published; have agreed on the journal to which the article has been submitted; and agree to be accountable for all aspects of the work.

Disclosure

The authors declare no conflicts of interest in this work.

References

- De Massis A, Kotlar J, Chua JH, Chrisman JJ. Ability and willingness as sufficiency conditions for family‐oriented particularistic behavior: implications for theory and empirical studies. J Small Bus Manage. 2014;52(2):344–364.

- Chrisman JJ, Chua JH, De Massis A, et al. The ability and willingness paradox in family firm innovation. J Prod Innov Manage. 2015;32(3):310–318. doi:10.1111/jpim.12207

- Rau SB, Werner A, Schell S. Psychological ownership as a driving factor of innovation in older family firms. J Fam Bus Strat. 2018;10:100246.

- Amit R, Ding Y, Villalonga B, Hua Z. The role of institutional development in the prevalence and value of family firms. In: Finance and Corporate Governance Conference; 2010.

- Booltink LW, Saka-Helmhout A. The effects of R&D intensity and internationalization on the performance of non-high-tech SMEs. Int Small Bus J. 2018;36(1):81–103. doi:10.1177/0266242617707566

- Di Vito J, Laurin C, Bozec Y. R&D activity in Canada: does corporate ownership structure matter? Can J Administr Sci. 2010;27(2):107–121. doi:10.1002/cjas.152

- Gómez-Mejía LR, Haynes KT, Núñez-Nickel M, et al. Socioemotional wealth and business risks in family-controlled firms: evidence from Spanish olive oil mills. Adm Sci Q. 2007;52(1):106–137. doi:10.2189/asqu.52.1.106

- Daily CM, Dollinger MJ. Family firms are different. Rev Bus. 1991;13(1–2):3–6.

- Górriz CG, Fumás VS. Ownership structure and firm performance: some empirical evidence from Spain. Manage Decis Econ. 1996;17(6):575–586. doi:10.1002/(SICI)1099-1468(199611)17:6<575::AID-MDE778>3.0.CO;2-N

- Mishra CS, McConaughy DL. Founding family control and capital structure: the risk of loss of control and the aversion to debt. Entrepreneursh Theory Pract. 1999;23(4):53–64. doi:10.1177/104225879902300404

- Morck R, Yeung B. Agency problems in large family business groups. Entrepreneursh Theory Pract. 2003;27(4):367–382. doi:10.1111/1540-8520.t01-1-00015

- Athanassiou N, Crittenden WF, Kelly LM, et al. Founder centrality effects on the Mexican family firm’s top management group: firm culture, strategic vision and goals, and firm performance. J World Bus. 2002;37(2):139–150. doi:10.1016/S1090-9516(02)00073-1

- Schulze WS, Lubatkin MH, Dino RN. Exploring the agency consequences of ownership dispersion among the directors of private family firms. Acad Manage J. 2003;46(2):179–194. doi:10.2307/30040613

- Chrisman JJ, Chua JH, Pearson AW, et al. Family involvement, family influence, and family–centered non–economic goals in small firms. Entrepreneursh Theory Pract. 2012;36(2):267–293. doi:10.1111/j.1540-6520.2010.00407.x

- Zellweger TM, Nason RS, Nordqvist M. From longevity of firms to transgenerational entrepreneurship of families: introducing family entrepreneurial orientation. Fam Bus Rev. 2012;25(2):136–155. doi:10.1177/0894486511423531

- Hambrick DC. Upper Echelons Theory: An Update. Briarcliff Manor, NY: Academy of Management; 2007:334–343.

- Bozec Y, Di Vito J. Founder-controlled firms and R&D investments: new evidence from Canada. Fam Bus Rev. 2019;32(1):76–96. doi:10.1177/0894486518793237

- Wiseman RM, Gomez-Mejia LR. A behavioral agency model of managerial risk taking. Acad Manage Rev. 1998;23(1):133–153. doi:10.2307/259103

- Benartzi S, Thaler RH. Myopic loss aversion and the equity premium puzzle. Q J Econ. 1995;110(1):73–92. doi:10.2307/2118511

- Zellweger TM, Astrachan JH. On the emotional value of owning a firm. Fam Bus Rev. 2008;21(4):347–363. doi:10.1177/08944865080210040106

- Gomez-Mejia LR, Nunez-Nickel M, Gutierrez I. The role of family ties in agency contracts. Acad Manage J. 2001;44(1):81–95. doi:10.2307/3069338

- Gomez-Mejia LR, Larraza-Kintana M, Makri M. The determinants of executive compensation in family-controlled public corporations. Acad Manage J. 2003;46(2):226–237. doi:10.2307/30040616

- Gomez‐Mejia LR, Makri M, Kintana ML. Diversification decisions in family‐controlled firms. J Manage Stud. 2010;47(2):223–252. doi:10.1111/j.1467-6486.2009.00889.x

- Tsao S-M, Lin C-H, Chen VY. Family ownership as a moderator between R&D investments and CEO compensation. J Bus Res. 2015;68(3):599–606. doi:10.1016/j.jbusres.2014.09.001

- Beatty RP, Zajac EJ. Managerial incentives, monitoring, and risk bearing: a study of executive compensation, ownership, and board structure in initial public offerings. Adm Sci Q. 1994;39:313–335. doi:10.2307/2393238

- Larraza‐Kintana M, Wiseman RM, Gomez-Mejia LR, et al. Disentangling compensation and employment risks using the behavioral agency model. Strat Manage J. 2007;28(10):1001–1019. doi:10.1002/smj.624

- Sanders WG, Hambrick DC. Swinging for the fences: the effects of CEO stock options on company risk taking and performance. Acad Manage J. 2007;50(5):1055–1078. doi:10.5465/amj.2007.27156438

- Alessandri TM, Tong TW, Reuer JJ. Firm heterogeneity in growth option value: the role of managerial incentives. Strat Manage J. 2012;33(13):1557–1566. doi:10.1002/smj.1992

- Carpenter MA, Sanders WG. The effects of top management team pay and firm internationalization on MNC performance. J Manage. 2004;30(4):509–528. doi:10.1016/j.jm.2004.02.001

- Alessandri TM, Mammen J, Eddleston K. Managerial incentives, myopic loss aversion, and firm risk: a comparison of family and non-family firms. J Bus Res. 2018;91:19–27. doi:10.1016/j.jbusres.2018.05.030

- Amoako-Adu B, Baulkaran V, Smith BF. Executive compensation in firms with concentrated control: the impact of dual class structure and family management. J Corporate Finance. 2011;17(5):1580–1594. doi:10.1016/j.jcorpfin.2011.09.003

- Cheung Y-L, Stouraitis A, Wong AW. Ownership concentration and executive compensation in closely held firms: evidence from Hong Kong. J Empirical Finance. 2005;12(4):511–532. doi:10.1016/j.jempfin.2004.10.001

- Hambrick DC, Finkelstein S. Managerial Discretion: A Bridge Between Polar Views of Organizational Outcomes. Research in organizational behavior; 1987.

- Morck R, Shleifer A, Vishny RW. Management ownership and market valuation: an empirical analysis. J Financ Econ. 1988;20:293–315. doi:10.1016/0304-405X(88)90048-7

- Amore MD, Failla V. Pay dispersion and executive behaviour: evidence from innovation. Br J Manage. 2018;31:487–504.

- Adams JS. Inequity in Social Exchange, in Advances in Experimental Social Psychology. Elsevier; 1965:267–299.

- Miller D, Le Breton‐Miller I, Lester RH. Family ownership and acquisition behavior in publicly‐traded companies. Strat Manage J. 2010;31(2):201–223.

- Miller D, Le Breton‐Miller I, Lester RH. Family and lone founder ownership and strategic behaviour: social context, identity, and institutional logics. J Manage Stud. 2011;48(1):1–25. doi:10.1111/j.1467-6486.2009.00896.x

- Block JH. R&D investments in family and founder firms: an agency perspective. J Bus Vent. 2012;27(2):248–265. doi:10.1016/j.jbusvent.2010.09.003

- Pepper A, Gore J. Behavioral agency theory: new foundations for theorizing about executive compensation. J Manage. 2015;41(4):1045–1068. doi:10.1177/0149206312461054

- Pratt JW, Zeckhauser R. Principals and agents: the structure of business. 1991.

- Beatty RP, Zajac EJ. Top management incentives, monitoring, and risk-bearing: a study of executive compensation, ownership, and board structure in initial public offerings. In: Academy of Management Proceedings. Briarcliff Manor, NY: Academy of Management; 1990:10510.

- Zajac EJ, Westphal JD. The costs and benefits of managerial incentives and monitoring in large US corporations: when is more not better? Strat Manage J. 1994;15(S1):121–142. doi:10.1002/smj.4250150909

- Camerer CF, Loewenstein G, Rabin M. Advances in Behavioral Economics. Princeton university press; 2004.

- Claessens S, Djankov S, Fan JPH, et al. Disentangling the incentive and entrenchment effects of large shareholdings. J Finance. 2002;57(6):2741–2771. doi:10.1111/1540-6261.00511

- Block J. Long-Term Orientation of Family Firms: An Investigation of R&D Investments, Downsizing Practices, and Executive Pay. Springer Science & Business Media; 2009.

- Jensen MC, Meckling WH. Theory of the firm: managerial behavior, agency costs and ownership structure. J Financ Econ. 1976;3(4):305–360. doi:10.1016/0304-405X(76)90026-X

- Brickley JA, Lease RC, Smith C. Ownership structure and voting on antitakeover amendments. J Financ Econ. 1988;20(1–2):267–291. doi:10.1016/0304-405X(88)90047-5

- Munari F, Oriani R, Sobrero M. The effects of owner identity and external governance systems on R&D investments: a study of Western European firms. Res Policy. 2010;39(8):1093–1104. doi:10.1016/j.respol.2010.05.004

- Chrisman JJ, Patel PC. Variations in R&D investments of family and nonfamily firms: behavioral agency and myopic loss aversion perspectives. Acad Manage J. 2012;55(4):976–997. doi:10.5465/amj.2011.0211

- Shleifer A, Vishny RW. A survey of corporate governance. J Finance. 1997;52(2):737–783. doi:10.1111/j.1540-6261.1997.tb04820.x

- Ashwin A, Krishnan RT, George R. Family firms in India: family involvement, innovation and agency and stewardship behaviors. Asia Pacific J Manage. 2015;32(4):869–900. doi:10.1007/s10490-015-9440-1

- Kim J-B, Krinsky I, Lee J. Institutional holdings and trading volume reactions to quarterly earnings announcements. J Account Audit Finance. 1997;12(1):1–14. doi:10.1177/0148558X9701200101

- Laverty KJ. Economic “short-termism”: the debate, the unresolved issues, and the implications for management practice and research. Acad Manage Rev. 1996;21(3):825–860.

- Sirmon DG, Arregle J, Hitt MA, et al. The role of family influence in firms’ strategic responses to threat of imitation. Entrepreneursh Theory Pract. 2008;32(6):979–998. doi:10.1111/j.1540-6520.2008.00267.x

- Gedajlovic E, Carney M, Chrisman JJ, et al. The adolescence of family firm research: taking stock and planning for the future. J Manage. 2012;38(4):1010–1037. doi:10.1177/0149206311429990

- Ang JS, Cole RA, Lin JW. Agency costs and ownership structure. J Finance. 2000;55(1):81–106. doi:10.1111/0022-1082.00201

- Fama EF, Jensen MC. Agency problems and residual claims. J Law Econ. 1983;26(2):327–349. doi:10.1086/467038

- Anderson RC, Mansi SA, Reeb DM. Founding family ownership and the agency cost of debt. J Financ Econ. 2003;68(2):263–285. doi:10.1016/S0304-405X(03)00067-9

- Stewart A. Help one another, use one another: toward an anthropology of family business. Entrepreneursh Theory Pract. 2003;27(4):383–396. doi:10.1111/1540-8520.00016

- Becker GS. Altruism, egoism, and genetic fitness: economics and sociobiology. J Econ Lit. 1976;14(3):817–826.

- Berghoff H. The end of family business? The Mittelstand and German capitalism in transition, 1949–2000. Bus Hist Rev. 2006;80(2):263–295. doi:10.1017/S0007680500035492

- Dyer WG, Whetten DA. Family firms and social responsibility: preliminary evidence from the S&P 500. Entrepreneursh Theory Pract. 2006;30(6):785–802. doi:10.1111/j.1540-6520.2006.00151.x

- Sanders WG. Behavioral responses of CEOs to stock ownership and stock option pay. Acad Manage J. 2001;44(3):477–492. doi:10.2307/3069365

- Ryan HE, Wiggins RA. The interactions between R&D investment decisions and compensation policy. Financial Manage. 2002;31:5–29. doi:10.2307/3666319

- Coles JL, Daniel ND, Naveen L. Managerial incentives and risk-taking. J Financ Econ. 2006;79(2):431–468. doi:10.1016/j.jfineco.2004.09.004

- Ghafoor S, Wang M, Chen S, Zhang R, Zulfiqar M. Behavioural investigation of the impact of different types of CEOs on innovation in family firms: moderating role of ownership divergence between cash flow rights and voting rights. Econ Res. 2021;2021:1–24.

- Zulfiqar M, Zhang R, Khan N, et al. Behavior towards R&D investment of family firms CEOs: the role of psychological attribute. Psychol Res Behav Manag. 2021;14:595. doi:10.2147/PRBM.S306443

- Le Breton‐Miller I, Miller D. Socioemotional wealth across the family firm life cycle: a commentary on “family business survival and the role of boards”. Entrepreneursh Theory Pract. 2013;37(6):1391–1397. doi:10.1111/etap.12072

- Block JH. How to pay nonfamily managers in large family firms: a principal agent model. Fam Bus Rev. 2011;24(1):9–27. doi:10.1177/0894486510394359

- Carney M. Corporate governance and competitive advantage in family–controlled firms. Entrepreneursh Theory Pract. 2005;29(3):249–265. doi:10.1111/j.1540-6520.2005.00081.x

- Bennedsen M, Nielsen KM, Perez-Gonzalez F, et al. Inside the family firm: the role of families in succession decisions and performance. Q J Econ. 2007;122(2):647–691. doi:10.1162/qjec.122.2.647

- Carney M, Zhao J, Zhu L. Lean innovation: family firm succession and patenting strategy in a dynamic institutional landscape. J Fam Bus Strat. 2019;10:100247. doi:10.1016/j.jfbs.2018.03.002

- Kale JR, Shahrur H. Corporate capital structure and the characteristics of suppliers and customers. J Financ Econ. 2007;83(2):321–365. doi:10.1016/j.jfineco.2005.12.007

- Martínez B, Requejo I. Does the type of family control affect the relationship between ownership structure and firm value? Int Rev Finance. 2017;17(1):135–146. doi:10.1111/irfi.12093

- Claessens S, Djankov S, Lang LH. The separation of ownership and control in East Asian corporations. J Financ Econ. 2000;58(1–2):81–112. doi:10.1016/S0304-405X(00)00067-2

- Alam MS, Atif M, Chien-Chi C, et al. Does corporate R&D investment affect firm environmental performance? Evidence from G-6 countries. Energy Econ. 2019;78:401–411. doi:10.1016/j.eneco.2018.11.031

- Honoré F, Munari F, de La Potterie BP. Corporate governance practices and companies’ R&D intensity: evidence from European countries. Res Policy. 2015;44(2):533–543. doi:10.1016/j.respol.2014.10.016

- Chen C-J, Lin B-W, Lin Y-H, et al. Ownership structure, independent board members and innovation performance: a contingency perspective. J Bus Res. 2016;69(9):3371–3379. doi:10.1016/j.jbusres.2016.02.007

- Wang Y, Wei Y, Song FM. Uncertainty and corporate R&D investment: evidence from Chinese listed firms. Int Rev Econ Finance. 2017;47:176–200. doi:10.1016/j.iref.2016.10.004

- Diéguez-Soto J, Manzaneque M, González-García V, et al. A study of the moderating influence of R&D intensity on the family management-firm performance relationship: evidence from Spanish private manufacturing firms. Bus Res Quart. 2019;22(2):105–118. doi:10.1016/j.brq.2018.08.007

- Xiang D, Chen J, Tripe D, et al. Family firms, sustainable innovation and financing cost: evidence from Chinese hi-tech small and medium-sized enterprises. Technol Forecast Soc Change. 2019;144:499–511. doi:10.1016/j.techfore.2018.02.021

- Tyler BB, Caner T. New product introductions below aspirations, slack and R&D alliances: a behavioral perspective. Strat Manage J. 2016;37(5):896–910. doi:10.1002/smj.2367

- Jiang F, Jiang Z, Kim KA, et al. Family-firm risk-taking: does religion matter? J Corporate Finance. 2015;33:260–278. doi:10.1016/j.jcorpfin.2015.01.007

- Song W-L, Wan K-M. Does CEO compensation reflect managerial ability or managerial power? Evidence from the compensation of powerful CEOs. J Corporate Finance. 2019;56:1–14. doi:10.1016/j.jcorpfin.2018.11.009

- Czarnitzki D, Kraft K, Thorwarth S. The knowledge production of ‘R’and ‘D’. Econ Lett. 2009;105(1):141–143. doi:10.1016/j.econlet.2009.06.020

- Feng X, Rui OM, Chen D, Lee J. How does quality of government moderate the influence of family firm governance on the R&D Intensity? The empirical research on Chinese listed family firms. The Empirical Research on Chinese Listed Family Firms (April 19, 2016). 2016.

- Bianchini S, Krafft J, Quatraro F, Ravix J. Corporate Governance, Innovation and Firm Age: Insights and New Evidence. University of Turin; 2015.

- Lim EN. The role of reference point in CEO restricted stock and its impact on R&D intensity in high‐technology firms. Strat Manage J. 2015;36(6):872–889. doi:10.1002/smj.2252

- Heyden ML, Reimer M, Van Doorn S. Innovating beyond the horizon: CEO career horizon, top management composition, and R&D intensity. Hum Resour Manage. 2017;56(2):205–224. doi:10.1002/hrm.21730

- Cao J, Cumming D, Wang X. One-child policy and family firms in China. J Corporate Finance. 2015;33:317–329. doi:10.1016/j.jcorpfin.2015.01.005

- Claver E, Rienda L, Quer D. Family firms’ international commitment: the influence of family-related factors. Fam Bus Rev. 2009;22(2):125–135. doi:10.1177/0894486508330054

- Nieto MJ, Santamaria L, Fernandez Z. Understanding the innovation behavior of family firms. J Small Bus Manage. 2015;53(2):382–399. doi:10.1111/jsbm.12075

- Chu W. Family ownership and firm performance: influence of family management, family control, and firm size. Asia Pacific J Manage. 2011;28(4):833–851. doi:10.1007/s10490-009-9180-1

- Zulfiqar M, Huo W, Wu S, et al. Behavioural psychology of unique family firms toward R&D investment in the digital era: the role of ownership discrepancy. Front Psychol. 2022;13. doi:10.3389/fpsyg.2022.928447

- Chen VY, Tsao S-M, Chen G-Z. Founding family ownership and innovation. Asia-Pacific J Account Econ. 2013;20(4):429–456. doi:10.1080/16081625.2012.762971

- Prencipe A, Markarian G, Pozza L. Earnings management in family firms: evidence from R&D cost capitalization in Italy. Fam Bus Rev. 2008;21(1):71–88. doi:10.1111/j.1741-6248.2007.00112.x

- Choi YR, Zahra SA, Yoshikawa T, et al. Family ownership and R&D investment: the role of growth opportunities and business group membership. J Bus Res. 2015;68(5):1053–1061. doi:10.1016/j.jbusres.2014.10.007

- Randolph RV, Alexander BN, Debicki BJ, et al. Untangling non-economic objectives in family & non-family SMEs: a goal systems approach. J Bus Res. 2019;98:317–327. doi:10.1016/j.jbusres.2019.02.017

- De Massis A, Ding S, Kotlar J, et al. Family involvement and R&D expenses in the context of weak property rights protection: an examination of non-state-owned listed companies in China. Eur J Finance. 2018;24(16):1506–1527. doi:10.1080/1351847X.2016.1200994

- Debellis F, De Massis A, Petruzzelli AM, Frattini F, Del Giudice M. Strategic agility and international joint ventures: the willingness-ability paradox of family firms. J Int Manage. 2020;2020:100739.

- Prencipe A, Bar-Yosef S, Dekker HC. Accounting research in family firms: theoretical and empirical challenges. Eur Account Rev. 2014;23(3):361–385. doi:10.1080/09638180.2014.895621

- Tsao S-M, Chang Y-W, Koh K. Founding family ownership and myopic R&D investment behavior. J Account Audit Finance. 2019;34(3):361–384. doi:10.1177/0148558X17704084

- Daspit JJ, Chrisman JJ, Sharma P, Pearson AW, Mahto RV. Governance as a Source of Family Firm Heterogeneity. Elsevier; 2018.

- Fang HC, Siau KL, Memili E, et al. Cognitive antecedents of family business bias in investment decisions: a commentary on “Risky decisions and the family firm bias: an experimental study based on prospect theory”. Entrepreneursh Theory Pract. 2019;43(2):409–416. doi:10.1177/1042258718796073

- Anderson RC, Reeb DM. Founding‐family ownership and firm performance: evidence from the S&P 500. J Finance. 2003;58(3):1301–1328. doi:10.1111/1540-6261.00567

- Chrisman JJ, Chua JH, Le Breton-Miller I, et al. Governance mechanisms and family firms. Entrepreneursh Theory Pract. 2017;42(2):171–186. doi:10.1177/1042258717748650

- Bozec Y, Di Vito J. Founder-controlled firms and R&D investments: new evidence from Canada. Fam Bus Rev. 2018;2018:894486518793237.

- Le Breton‐Miller I, Miller D. To grow or to harvest? Governance, strategy and performance in family and lone founder firms. J Strat Manage. 2008;1:41–56. doi:10.1108/17554250810909419

- Combs JG, Penney CR, Crook TR, et al. The impact of family representation on CEO compensation. Entrepreneursh Theory Pract. 2010;34(6):1125–1144. doi:10.1111/j.1540-6520.2010.00417.x

- Diéguez-Soto J, Manzaneque M, Rojo-Ramírez AA. Technological innovation inputs, outputs, and performance: the moderating role of family involvement in management. Fam Bus Rev. 2016;29(3):327–346. doi:10.1177/0894486516646917

- Zulfiqar M, Hussain K, Yousaf MU, et al. Moderating role of CEO compensation in lean innovation strategies of Chinese listed family firms. Corporate Govern. 2020;20(5):887–902. doi:10.1108/CG-03-2019-0092