?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Forestry and forest industry sectors have vital roles for many regional economies. Consequently, it is important to understand how the introduction of the iron and steel industry (ISI) as a new large consumer of woody materials may affect existing feedstock markets. The use of metallurgical coal can partially or fully be substituted by refined biomass. To analyze the potential consequences of a new woody consumer on regional markets, three regions in northern Sweden and Finland are used as a case. A regional partial equilibrium model is developed, the Norrbotten County Forest Sector Model (NCFSM), and applied on three different scenarios. The purpose of the study is to analyze the intra- and inter-regional effects increased competition for woody materials may have on regional markets and on the economic well-being of the regions. The result suggest that the total welfare effect is relatively small, however, some regional welfare distributional effects are observed. Additionally, the price of roundwood will only be moderately affected if the ISI sector switch from fossil fuels to refined woody biomass. However, secondary woody materials, i.e. by-products and harvesting residues, will experience larger price shifts.

Introduction

In 2016, the Swedish iron and steel industry (ISI) sector released 6 million tonnes of CO2-equivalent emissions, or 36% of the total industry emissions. This makes it the largest industrial emitter of greenhouse gases (GHGs) is Sweden (SEPA Citation2017a). As such, the sector will need to find ways to improve its overall abatement and lower fossil based emissions of GHGs, especially with the introduction of more ambitious environmental and climate policy goals (SEPA Citation2017b). A possible way of achieving this is to substitute the use of fossil fuels, e.g. metallurgical coal, in the blast furnace with refined woody biomass (e.g. Mandova et al. Citation2018). Wang et al. (Citation2015) estimate that substituting coal with charcoal can reduce on-site emissions by 17–28%. For Sweden’s largest steel mill, located in the northern part of the country, this reduction corresponds to a potential saving of 1.14 million tonnes of fossil based CO2 (Wang et al. Citation2015). However, a switch from fossil fuels to refined woody materials will introduce the ISI sector as a major actor on regional feedstock markets.

Woody biomass is sold on established feedstock markets, which are regional in character due to the low value-to-weight of the material (e.g. Olofsson and Lundmark Citation2018). Long-range hauling of the harvested woody material is, for the most part, not economically viable. Therefore, the introduction of a new large wood consumer will primarily have an impact on the regional level by increasing competition for woody materials and raise local feedstock prices. This will not only affect the forest owners and the existing forest industries but also the viability of the ISI sector to substitute to charcoal. Since the forest industry has an important role on many regional economies (e.g. Ejdemo et al. Citation2014; Korhonen Citation2015) it becomes important to understand how it is affected by a transition toward a green ISI sector.

The purpose of the study is to analyze the intra- and inter-regional effects increased competition for woody materials may have on regional markets and on the regional economic well-being (i.e. welfare). While there are numerous studies analyzing the feasibility of the ISI sector substituting fossil fuels with woody biomass (e.g. Wang et al. Citation2015), the economic implications of such a development is, to the author’s best knowledge, still missing. This article studies the impact of one ISI mill implementing the use of refined woody biomass as an auxiliary fuel source, and how this development may affect existing forest industries and the regional woody feedstock supply. To achieve this, four research questions are asked: (i) how does the price of hot metalFootnote1 affect optimal allocation of the woody feedstock; (ii) what are the market effects of a partial transition from fossil fuels to refined woody biomass in the ISI sector; (iii) what are the market effects of an increased roundwood supply; and (iv), what are the overall regional implications of this market development. To analyze the potential consequences of this development on regional markets, three regions in northern Sweden and Finland are used as a case. These regions are modeled in a regional partial equilibrium (PE) model, the Norrbotten County Forest Sector Model (NCFSM) (Olofsson Citation2018).

PE models in a Swedish context

PE models in a forest and forestry setting, generally referred to as a Forest Sector Model (FSM), have become a commonly used tools over the past two decades (e.g. Toppinen and Kuuluvainen Citation2010; Latta et al. Citation2013). The strength of this modeling approach is that it produces informative and comparable results, highlighting the effects from specific schemes on a subset of the economy (Northway et al. Citation2013). In many regards, Kallio et al. (Citation1987) and the Global Trade Model (GTM) is considered the genesis of modern FSM studies (Buongiorno Citation1996; Latta et al. Citation2013; Northway et al. Citation2013).

Regional FSMs have been applied in e.g. a Norwegian (Bolkesjø Citation2005; Trømborg et al. Citation2007, Citation2013), French (Lecocq et al. Citation2011; Caurla et al. Citation2015) and Finnish (Kallio et al. Citation2008; Kangas et al. Citation2011) setting. These models have been used to analyze a wide array of research topics, such as: (i) assessing different policy schemes for further development of the bioheat sector (Trømborg et al. Citation2007; Lecocq et al. Citation2011), (ii) effects of increased production of second-generation biofuels (Kangas et al. Citation2011; Trømborg et al. Citation2013), and (iii) the market implications of increased forest conservation (Bolkesjø et al. Citation2005; Kallio et al. Citation2008). In a Swedish context, Lestander (Citation2011) developed the Swedish Forest Sector Trade Model (SFSTM), which was later expanded upon by Carlsson (Citation2012) in SFSTM II. Both analyzed the effect of increased competition of forest fuels. This was done in a spatial setting by dividing Sweden into four aggregated regions, and one region for foreign trade. While Lestander argues that the SFSTM was underdeveloped, primarily due to data limitations, Carlsson found the second iteration of the SFSTM to be robust. Carlsson (Citation2012) analyzed the effect of different bioenergy targets and how an increased demand for forest-based biofuels would affect the forestry and forest industry sectors. Increasing bioenergy production with between 5 and 30 TWh annually was found to cost between 30 and 620 million SEK. Carlsson also assessed the effects of a trade restriction on woody biomass and found that it would increase cost five-fold in the high production scenario. This result suggests that Sweden is dependent on wood imports in order to achieve its bioenergy policy targets. Olsson and Lundmark (Citation2014) analyzed the degree of feedstock competition between forest industry sectors and the heating sector. Sweden was treated as one aggregated region, with four industries, three woody feedstocks, and six outputs. The result indicates that feedstock markets will only be moderately affected by changing market conditions. Mustapha (Citation2016) used a more detailed spatial/geographic modeling approach in developing the Nordic Forest Sector Model (NFSM). The model incorporates the forest sectors of Norway, Sweden, Finland and Denmark on a regional level. The exception is Denmark, which remained as one geographical entity, and the same is true for the rest of the world. The primary objective of the NFSM is to analyze the role bioenergy plays in future energy systems. In Mustapha et al. (Citation2017) the NFSM was used to study the (economically) optimal allocation of biofuel production. The result indicates that allocation is depending on: (a) the degree of substitutability between different primary woody inputs a specific biofuel technology allows, (b) accessibility to local heat markets as a secondary market, and (c), the cost of labor. However, access to the woody feedstock is shown to be the main determinant for the allocation of biofuel production.

The studies above demonstrate the importance of the spatial dimension on the results. Due to the availability and reliability of the data, the NCFSM uses a spatial dimension which is a combination of county and aggregated counties.

The iron and steel industry

With ever more stringent climate policy targets from national governments, the ISI sector have been searching for alternatives to metallurgical coal and coke, to improve general energy efficiency and lower fossil fuel emissions (Larsson et al. Citation2014; Mandova et al. Citation2018).

The largest crude steel mill in Sweden (SSAB Luleå), with a capacity of 2.55 million tonnes (Mton) of hot metal per year, is located in Norrbotten County. This mill produces steel slabs from iron ore pellets and annually consumes between 0.31 and 0.368 Mton of coal and 0.73 Mton of coke (Wang et al. Citation2015). In 2008, this single mill emitted 3.7 Mton of CO2, corresponding to 59% of the Swedish ISI sector’s total CO2-emissions (Wang et al. Citation2015).

There are however more environmentally friendly production technologies that can be implemented in the steel-making process. Amongst these are technologies using woody biomass as the primary feedstock to produce green alternatives that can be used as a substitute to conventional fossil fuels (Suopajärvi and Fabritius Citation2013; Larsson et al. Citation2014; Mandova et al. Citation2018).Footnote2 However, the hesitation to implement green technologies is partially due to the large costs and uncertainties these can entail, but also by the technological lock-in’s and large costs that have already been incurred by investing in fossil fuels (Wang et al. Citation2015).

The introduction of pulverized coal injection (PCI) has resulted in that the use of refined woody biomass has become a viable alternative to fossil fuels (Larsson et al. Citation2014; Wang et al. Citation2015). PCI is a production process that allows an auxiliary fuel, in this case pulverized coal, to be blown into the blast furnace as a way of introducing additional carbon, thus speeding up the process, and reducing the amount of coke needed (Wei et al. Citation2013). The use of coal can partly or fully be substituted with charcoal, i.e. refined woody biomass (Wei et al. Citation2013; Wang et al. Citation2015). Consequently, PCI offers an relatively easy and efficient way to reduce fossil emissions, and is the only viable way to replace large quantities of fossil fuels that does not entail large investments in existing facilities (Wang et al. Citation2015). There are additional production technologies that can be implemented to reduce dependency on fossil fuels (e.g. Johansson Citation2016; Suopajärvi et al. Citation2017; Nwachukwu et al. Citation2018). Furthermore, other bio-based products (e.g. wood pellets, bio-oil, and torrefied fuels) can also be used as an auxiliary fuel in a blast furnace injection system. However, charcoal is the best performing biofuel (Suopajärvi et al. Citation2017), and can potentially offer CO2 savings of 4.3–4.9 times that of torrefied materials or wood pellets (Wang et al. Citation2015). As a consequence, charcoal is the only injection fuel that is considered in this article.

There are a number of ways to enrich woody biomass into charcoal (e.g. Child Citation2014; Mousa et al. Citation2014). However, Sweden currently lacks a domestic charcoal production on an industrial scale (Wei et al. Citation2013), though there are plans of building large-scale plants, using slow pyrolysis and torrefaction to enrich the woody biomass, some 90 and 270 kilometers from the steel mill in Luleå (Mefos Citation2017). In the article, the enrichment of the woody material to charcoal is assumed to take place through a slow pyrolysis process with a mass conversion ratio of 35%, and this industry sector is only located in Norrbotten County.

Materials and methods

Model outline

Since the primary region of interest is Norrbotten County, the model is named the Norrbotten County Forest Sector Model (NCFSM). The NCFSM is a regional PE model, built upon the modeling approach of SFSTM II by Carlsson (Citation2012), whom in turn based his model on the works of Kallio et al. (Citation1987) and Bolkesjø (Citation2004). All markets in the NCFSM are assumed to be operating under perfect competition.

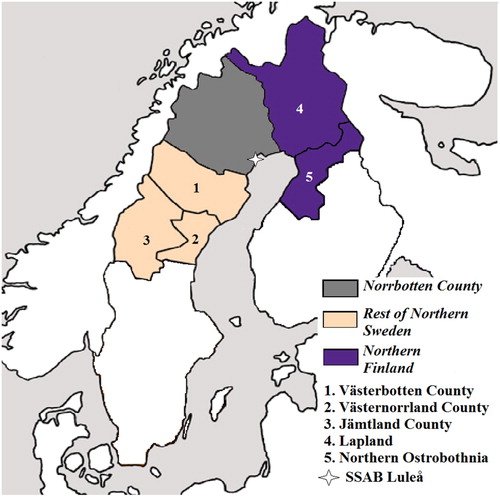

shows the three geographical regions of the NCFSM: Norrbotten County (NB); Rest of northern Sweden (RoNS), made up by the counties of Västerbotten, Västernorrland and Jämtland; and Northern Finland (NF), which includes the administrative regions of Lapland and Northern Ostrobothnia. These regions make up approximately 40–50% of each country’s total land area, but only 9–11% of the total population. It is assumed that all transportation between regions take place by road. Since long-range hauling of the harvested woody material often is not economically viable, the model includes the three regions between which trade is deemed feasible. All other woody feedstock markets are assumed to be inaccessible.

Figure 1. Regional areas included in the NCFSM.

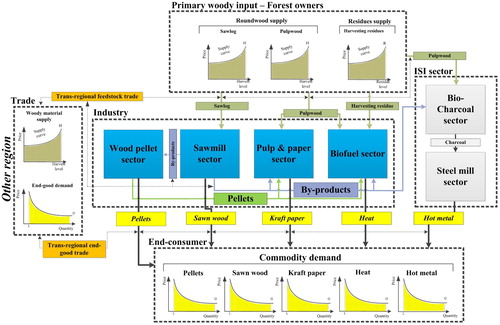

is a graphical representation of the NCFSM, composed of the four existing forest industries, i.e. sawmill, pulp and paper mill, wood pellets and bioenergyFootnote3 sectors, in addition to the steel mill and bio-charcoal sectors (in defined as the combined ISI sector). In the model, the steel mill and bio-charcoal sectors are restricted to Norrbotten County. This entails that steel mills located elsewhere are not included in the model since they are assumed to only consume fossil fuels and therefore outside the scope of this article. This constraint is motivated by limitations in reliable data, and the comprehension that the use of charcoal in a blast furnace is still an emerging technology and is therefore likely to be implemented at one mill initially rather than across the whole sector at once. Similarly, bio-charcoal sectors located outside of Norrbotten County are not considered.

Figure 2. NCFSM flow chart.

In the model, each sector produce one specific end-good, but its production can be split into a number of different activities, each using a different production technology. The end-goods are: sawn wood from the sawmill; kraft paper from the pulp and paper mill; pellets from the wood pellet industry; heat from the bioenergy industry; and hot metal from the steel mill. Charcoal from the bio-charcoal sector is only used as an intermediate good by the steel mill and is therefore not sold on end-good markets.

The NCFSM contains two roundwood types, sawlogs and pulpwood, which are supplied to the market by the forest owner. In addition to roundwood, left-overs from the felling site, e.g. stumps, tree tops, branches, can also be collected and sold by the forest owner. Left-over materials are defined as the all-encompassing commodity harvesting residues. Besides harvested woody materials, the model also includes three woody by-products: woodchips, sawdust and bark. These are supplied by the sawmill sector and can be used as a primary woody feedstock by other industries.

Nine commodities are assumed tradable between regions: sawlogs, pulpwood, woodchips, sawdust, bark, sawn wood, kraft paper, pellets, and hot metal; while three commodities are assumed non-tradable: heat, charcoal and harvesting residues. Heat is limited by the length of DH networks, which are often limited to the urban nucleus, while charcoal is as an intermediate good that is only used by the steel mill. Harvesting residues are assumed to be non-tradable primarily due to its low value-to-weight ratio, and empirically, the commodity is not extensively traded between the two Swedish regions (Asmoarp and Davidsson Citation2016).

Model specification

The NCFSM is a static, one-period, optimization model, where the objective function is to maximize the general economic state (i.e. welfare) for all regions, given a number of constraints. On competitive markets, this is equivalent to maximizing the sum of the consumer and producer surplus, minus the total cost of inter-regional trade (cf. EquationEquation 1(1)

(1) ). i is a set over the different regions, and l is the lower integral value for the end-goods. For a more detailed description of the NCFSM, see Olofsson (Citation2018). The model is expressed as:

(1)

(1) s.t.

(2)

(2)

(3)

(3)

(4)

(4)

(5)

(5)

(6)

(6)

(7)

(7)

(8)

(8)

The first element in EquationEquation (1(1)

(1) ) is the consumer surplus from the end-goods (o), the second element is the producer surplus from the different types of roundwood (RW), the third element is the producer surplus from harvesting residues (HR), and the final element corresponds to the cost of inter-regional trading, where IM and EX denotes importer and exporter, respectively.Footnote4 EquationEquation (2

(2)

(2) ) state that consumption at equilibrium must equal regional production after trade is taken into account. This entails that all produced goods will be consumed. EquationEquation (3

(3)

(3) ) guarantees that roundwood demand is satisfied through regional roundwood harvest or trade. EquationEquation (4

(4)

(4) ) ensures that harvesting residue demand is satisfied by regional supply. EquationEquation (5

(5)

(5) ) states that demand for a by-product is less or equal to supply, thus allowing for a surplus in supply but not in demand. EquationEquation (6

(6)

(6) ) restricts any non-tradable goods of being sold to another region. EquationEquation (7

(7)

(7) ) states that all hot metal production must be satisfied through the use of charcoal as an auxiliary fuel. And finally, the expressions in EquationEquation (8

(8)

(8) ) state that there exist an upper limit (constraint) for: end-good demand, roundwood harvest, collection of harvesting residues, and an upper capacity level for each activity.

From the marginal of the balance constraints (Equations (Equation2(2)

(2) )–(Equation7

(7)

(7) )) it is possible to obtain a theoretical, non-monetary, market price (i.e. the shadow price) for each commodities and region (Hazell and Norton Citation1986). However, the shadow price in itself cannot be used to gain any insight. Rather the variable of interest is the change in shadow price between different scenario simulations, which can provide a useful measure for how markets are impacted by shifting market conditions.

Model implementation

The model is constructed using General Algebraic Model System (GAMS) software and the optimization is solved using the CONOPT solver.

Data

Data for the reference values are collected from: (a) online open sources (e.g. Swedish Energy Markets Inspectorate, EI Citation2017), (b) official national statistics (e.g. Swedish Statistical Yearbook of Forestry, SFA Citation2014), and (c) through personal correspondence with forest industries. Regional forest industries are identified with information from Swedish Forest Industries Federation (SFIF Citation2017), and the Finnish Forest Industries (FFI Citation2017), EI (Citation2017), Natural Resources Institute Finland (LUKE Citation2017), Bioenergi (Citation2017), and Selkimäki and Röser (Citation2009). Forest industries located in Norrbotten County are asked to provide information regarding their demand of woody materials, current production levels and their production capacity (see Appendix 2 for the included forest industries in Norrbotten County). However, when this information is not made available, open source data is used.

The model is built upon the assumption that industries use a Leontief production function (similar to e.g. Kallio et al. Citation1987). This entails that industry sectors cannot substitute between different commodities to produce a given output. A way to incorporate some production flexibility is to allow for a number of different activities to produce the same end-good. However, each sub-activity still has strict input requirements to produce a given output.

All prices are given in Swedish Kronor (SEK), the woody feedstock is in cubic meter solid volume excluding bark (m3fub) or cubic meter solid (m3f), while end-goods are in: cubic meter (m3) for sawn wood; tonnes for kraft paper, charcoal and hot metal; gigawatt hour (GWh) for heat; and cubic meter solid (m3f) for pellets.Footnote5 For a more detailed examination of model data and the input-output coefficients, see Olofsson (Citation2018).

Core model assumptions

All sectors are assumed to have a fixed capital stock. Additionally, the sunk cost of building and developing a regional bio-charcoal industry is not taken into account in the model.

A lower production constraint is introduced for the bioenergy sector located in Norrbotten County and in Rest of northern Sweden. The bioenergy sector in Norrbotten County must produce a minimum of 117 GWh of heat from pulpwood, and an additional 92 GWh from harvesting residues. These production estimates are obtained through personal correspondence with individual DH utilities and cross-referenced with values from EI (Citation2017). Meanwhile, the bioenergy sector in the Rest of northern Sweden must produce a minimum of 102 GWh from pellets. Pellets is also added as an input feedstock for the pulp and paper sector in the Rest of northern Sweden, since the regional sector is a large consumer of the feedstock (Bioenergi Citation2017). These production levels are based on observed data for each activity and region, and are used to reflect the inability of the regional sector to adjust its woody demand, i.e. they are assumed to be locked into certain feedstocks.

The model does not take into account the cost of intra-regional transportation, which is assumed to be internalized by the forest industry and end-good consumer. A transportation cost is only added when woody materials and end-goods are traded between different regions. However, for the pulp and paper sector in Norrbotten County to reach its observed production quantity of 1.36 Mton of kraft paper an additional 0.323 million m3f of woodchips are required from other regions. This is primarily a consequence of data limitation, since according to the model, there is a large excess demand in by-products from the forest industries in Norrbotten County, and a large supply surplus in the Rest of northern Sweden. Therefore, inter-regional trade in woody by-products is restricted to 0.4 million m3f per commodity and region to avoid over-excessive trade, which may produce unrealistic outcomes.

Baseline calibration

An initial baseline scenario run is compared to observed quantities (). The result indicates that all regional end-consumer demand is satisfied through regional production or trade, with the exception of the pulp and paper sector, which produce 2.23 Mton less than observed quantities. The result also indicates that an additional 3 million m3fub sawlogs and 3.55 million m3fub pulpwood are left standing, compared to observed harvest levels of roundwood (

). A majority of the trees are located in the Rest of northern Sweden. The primary reason for why the pulp and paper sector is unable to produce more kraft paper is a shortage in woodchip supply. Therefore, the pulp and paper sector is split into two activities: PP1 that use a combination of woodchips and pulpwood, and PP2 that only use pulpwood. However, the pulp and paper sector in Norrbotten County is assumed to only have access to the PP1-activity. The primary reason for this restriction is that firm-level data is used to estimate the input-output coefficient for the pulp and paper sector in Norrbotten County. For the other regions, coefficients are obtained from Metla (Citation2014) and SFA (Citation2014); while woodchip demand in PP1 is collected from Carlsson (Citation2012) and subtracted from the regional sector’s roundwood demand. By splitting the pulp and paper sector into two activities an additional 0.871 Mton of kraft paper is produced across all regions, and all available pulpwood is harvested.

The activities included are: sawmill, pulp and paper 1 (PP1), pulp and paper 2 (PP2), bioenergy from pulpwood, bioenergy from harvesting residues, bioenergy from woodchips, bioenergy from sawdust, bioenergy from bark, bioenergy from pellets, and wood pellet. To this, the ISI sector is added, divided into three activities: the steel mill, bio-charcoal from pulpwood, and bio-charcoal from sawdust.

Scenario description

To assess the regional implications of a transition toward a green ISI sector, the research questions presented in the introduction are used as the basis for three different scenario runs. The scenarios evaluated are:

The impact hot metal price has on optimal allocation of woody materials

The market effects of a partial transition to charcoal

The market effects of increased roundwood supply

The initial scenario is motivated by the recognition that hot metal is an intermediate good in the steel-making process, and as a consequence there is no observed market price for the good. Subsequently a price interval for the end-good is assumed, and the model is run over three price level to analyze its effect. The second scenario is motivated by the realization that production of charcoal in Sweden, and its use in the ISI sector, is in its infancy. Consequently, the introduction of charcoal as an auxiliary fuel in the ISI sector will most likely be in parallel with the use of conventional metallurgical coal. In the final scenario, the potential roundwood supply is doubled to that of observed harvesting levels. Increasing roundwood supply is a way to ease the effects of increased woody competition. However, this is not the same as doubling the amount of roundwood harvested, rather allowing forest owner to potentially supply up to double the amount.

Results

The price of hot metal

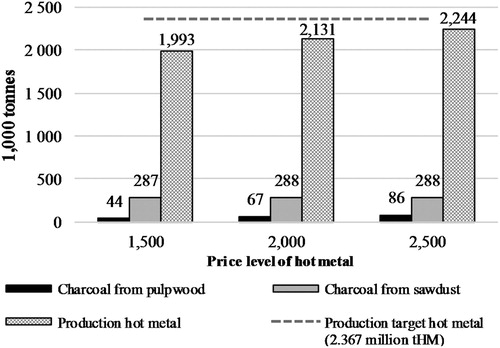

Hot metal is an intermediate good in the steel-making process and lacks an observable market price. After consulting with industry representatives, a price interval of 1500–2500 SEK/tonne hot metal (tHM) is selected. Production target for the steel mill sector is 2.367 million tHM, i.e. observed production quantity, thus requiring 0.394 Mton of charcoal (Wang et al. Citation2015). The end-good price is an essential part in solving of the optimization problem. It is one of the deciding factors in how the model prioritized the allocation of the woody feedstock to maximize overall welfare (cf. EquationEquation (1(1)

(1) )).

The results in show that the steel mill sector has to lower production by approximately 5–15%, depending on the price level of hot metal, compared to the observed production level; or alternatively, that the steel industry can only satisfy 85–95% of its auxiliary fuel demand by substituting to charcoal.Footnote6 That is, at a hot metal price of 1500 SEK/tHM, the result indicates that the ISI sector will produce 1.993 Mton hot metal, compared to 2.244 Mton if the price is increased to 2500 SEK/tHM. As shown in , a majority of the charcoal produced will use sawdust as its woody feedstock, but as the price of hot metal increases, more pulpwood will be allocated to the charcoal production.

Figure 3. ISI production at different price-levels for hot metal.

Compared to the baseline, production of kraft paper in Northern Finland will decrease by 5–10%, depending on the price level of hot metal. This reduction corresponds to a decrease in total kraft paper consumption of approximately 0.5–1.5%, in all regions. The introduction of the ISI sector on woody feedstock markets will, regardless of the price of hot metal, result in reduced production for the wood pellet and bioenergy sectors. The wood pellet sector in Norrbotten County will cease all production, and total pellet production will decrease by 65% across all regions, while total end-good consumption of pellets will decrease by 70%, compared to the baseline. The bioenergy sector in Norrbotten County and Northern Finland will lower wood-based production of heat (5% and 7%, respectively) due to increased feedstock competition from the ISI sector.

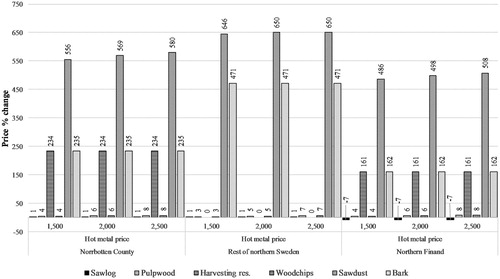

shows how feedstock prices will be affected by the introduction of a new wood consumer. Roundwood prices are only marginally affected by this development, where sawlog prices in Northern Finland will decrease by 7% as sawn wood production moves elsewhere, while pulpwood prices will increase by 3–8%, depending on the price of hot metal and region. As indicated by the results in , the largest percentage changes are observed on the market for secondary woody materials (i.e. by-products and harvesting residues). The price of sawdust will increase between 486% and 650% (depending on the price of hot metal and region) as the bio-charcoal sector shifts the market’s aggregated demand curve; while the bioenergy sector will experience surging prices for harvesting residues (161–234%) and bark (162–471%).

Figure 4. Regional price development for woody materials at different hot metal prices.

The suggested price development for sawdust and bark will result in the commodities being price above pulpwood, while the same is true for harvesting residues in Norrbotten County.Footnote7 An increase of 471% would result in bark becoming the most expensive woody feedstock. A market outcome where secondary woody materials are priced above pulpwood is arguably not realistic. At a certain price level, market actors will substitute the more expensive commodities with another woody feedstock and the price of that commodity will experience a price increase. Furthermore, since woodchips, sawdust and bark are by-products from sawmilling, the production of by-products is not governed by its own-price; nor is the sawmill sector, as depicted in the NCFSM, able to take advantage of this price development since its already operating close to capacity in most regions.

Partial transition to charcoal

Under the assumption that the ISI sector, at an initial transitional stage, only wish to substitute part of its auxiliary fuel demand with woody biomass, production of hot metal is set equal to 10%, 25% and 50% of observed consumption levels. That is, a partial restriction is introduced for hot metal in the first expression of EquationEquation (8(8)

(8) ), which restricts end-good demand, and it is assumed that the remaining hot metal quantities (i.e. 90%, 75% and 50%) are produced using other means, e.g. fossil fuels. However, since fossil fuels are not included as feedstock alternatives (see Equation (7)), fossil based production of hot metal is not explicitly modeled in the NCFSM. There are numerous reasons why the ISI sector would choose to only substitute part of its auxiliary fuel demand with charcoal, e.g. supply security, long-term supply contracts for fossil fuels, etc. However, since charcoal is an untested feedstock for the Swedish ISI sector, it will in all likelihood, initially be used in parallel with conventional metallurgical coal. As noted above, hot metal lacks an observable market price since it is an intermediate good in the steel-making process. However, at these lower production quantities the hot metal price does not affect model results; and the hot metal price is therefore set to 2000 SEK/tHM.

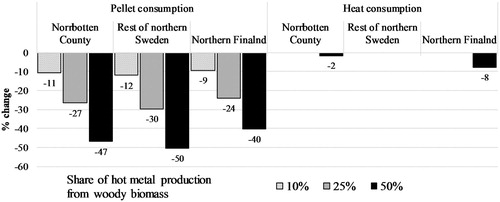

The results show that at lower production levels of hot metal, the bio-charcoal sector will only produce charcoal from sawdust. Only when hot metal production exceeds 75% of observed production will the bio-charcoal sector start using pulpwood. Consequently, the price of pulpwood is not affected at these initial transitionary production levels of hot metal, and the same is true for production of kraft paper and sawn wood. However, production and consumption of pellets will be affected. Total production of pellets will on average decrease by 9–45% compared to observed production levels, and all pellet production in Norrbotten County will cease when the ISI sector substitutes 25% of its auxiliary fuel demand with woody biomass. As shown in , the decline in pellet production will also reduce end-good consumption, which will fall by 9–50% compared to the baseline. In addition to affecting the wood pellet sector and end-good consumption of pellets, increased competition for the woody feedstock will also affect the bioenergy sector’s ability to produce heat. As shown in , when the ISI sector substitutes 50% of its auxiliary fuel demand with woody biomass, heat production in Norrbotten County and Northern Finland will decline by 2% and 8%, respectively. Thus suggesting that the bioenergy sector will be price out of the woody feedstock when the ISI sector increases its demand for woody biomass.

Figure 5. Changes to end-good consumption at partial transition to charcoal.

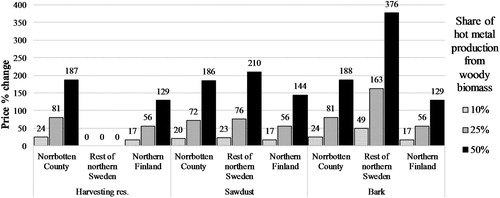

shows the price development of the woody feedstock at different production levels of hot metal. Similarly to the price development observed in , increased competition for the woody feedstock will primarily have an effect on secondary woody materials. However, only harvesting residues, sawdust and bark are affected at lower production levels of hot metal. Harvesting residues will increase by 14–187%, sawdust by 20–210%, and bark by 17–376%. At a 25% transition level, the observed price changes will lead to bark being priced above pulpwood in the Rest of northern Sweden; and at a 50% transition level, bark will be priced above pulpwood in all regions. For other secondary woody materials, the observed price change will not lead to feedstock prices exceeding the pulpwood level.

Figure 6. Regional price development for woody materials at partial transition to charcoal.

Increased roundwood supply

A way to ease the effect of increased woody competition is to increase supply of roundwood. In the following scenario, the harvesting constraint parameter () is increased to 2. However, this is not the same as doubling the amount of harvested roundwood but rather allowing forest owner to potentially supply up to double the amount. The hot metal price is set equal to 2000 SEK/tHM and the ISI sector is trying to produce 2.367 million tHM using charcoal as its only auxiliary fuel.

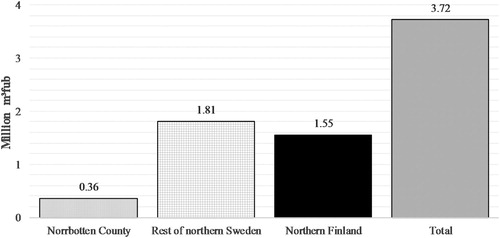

The result in indicates that increasing the harvesting constraint parameter will increase pulpwood supply with 3.72 million m3fub across all regions, while the supply of sawlogs will remain relatively unchanged (reduce by 4000 m3fub). A majority of the additional roundwood will be harvest in the rest of northern Sweden and Northern Finland. The pulp and paper sectors in these two regions are not operating at capacity and can therefore increase production, while the pulp and paper sector in Norrbotten County is already operating at full capacity. The increase in pulpwood supply will result in a 14% increase in total kraft paper consumption, compared to the baseline. Increasing roundwood harvest will also allow the ISI sector to operate at capacity, and 44% of the auxiliary fuel demand will come from pulpwood charcoal, compared to between 13% and 23% in . Compared to the baseline, consumption of pellets will decrease by approximately 52% across all regions. However, this reduction in pellets consumption is 18 percentage points less than the equivalent run in the Price of hot metal scenario.

Figure 7. Changes in regional harvest rate from increased potential roundwood supply.

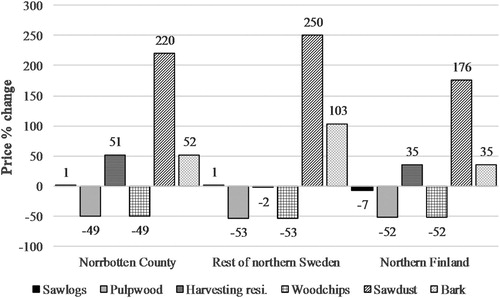

As the size of the harvesting constraint parameter increases, the pulpwood supply curve will shift outwards, leading to a reduction in the feedstock price. This development is shown in , where prices for pulpwood and woodchips decrease by 49–53%. Overall competition for sawdust will increase by the introduction of the ISI sector, leading to a price increase of 176–250%. However, compared to the price development observed in , the sawdust price is (on average) 357 percentage points lower in ; a consequence of increased pulpwood availability. Overall, the suggested price movements observed in will not lead to feedstock prices exceeding the initial reference price of pulpwood, the exceptions being sawdust and bark in the Rest of northern Sweden. However, after taking into account the suggested reduction to pulpwood prices, sawdust and bark will be priced above pulpwood in all regions. A similar price development is observed for harvesting residues in Norrbotten County. Such a market outcome is unlikely, since there are incentives for market actors to substitute expensive commodities with cheaper woody alternatives.Footnote8

Figure 8. Regional price development from increased roundwood supply.

Discussion

The total welfare effect of increased feedstock competition is relatively small, ranging from between −0.01% and +0.02%, compared to the baseline. Thus suggesting that increased competition will, from a purely welfare perspective, not have any significant impact on the three regions. Any reduction in welfare caused by declining heat and pellet production is alleviated by the ISI sector. The industry sectors will face rising feedstock prices, though this is balanced out by increased revenue for forest owners. However, examining welfare effects in specific regions indicates that the consumer surplus in Norrbotten County will increase by 6–10%, while the consumer surplus in Northern Finland will experience a marginal reduction. As such, the result suggests that there may be some regional welfare redistribution effects from increased feedstock competition, but this is negated by an increase in the cost of trading, since forest owners in Norrbotten County are not able to meet regional woody demand. However, it is important to remember that there are numerous effects that are not taken into account. For instance, the model does not consider how increased feedstock prices affect profitability, were the long-run effects of increased competition may be falling profits. Such a development may in the end cause the closure of individual mills. Additionally, the model does not consider the local implications from a reduction in end-good production, the costs associated with the closure of mills, or the bio-charcoal sector’s start-up cost.

The overall results can be interpreted as indicating:

the importance of inter-regional trade for optimal allocation of woody materials;

the difficulty of the ISI sector utilizing woody biomass to produce green steel;

the problem of increasing demand for a finite resource that is already used to produce carbon-neutral goods.

The result indicates that the three regions are highly interconnected. The introduction of a new wood consumer in one region will have clear spillover effects on neighboring regions by increasing feedstock competition and raising woody prices. As a consequence, inter-regional trade is crucial for optimal allocation of the woody feedstock when competition and demand increases. This result is similar to Carlsson (Citation2012) and implicitly entails that any trade obstructing policy (e.g. an additional tax on heavy trucks (Swedish Riksdag Citation2015)) will have a negative impact on welfare; while increased investment in infrastructure, improved trans-national cooperation, and general improvements in the trade structure will help to facilitate the transition toward a green ISI sector.

The result also indicates that the largest price change will be experienced on the market for secondary woody materials, which may potentially be priced above pulpwood. This outcome is highly unlikely since consumers will substitute the woody commodity with another feedstock under such a circumstance. Thus, rather than an explicit price increase of up to 650%, the results can be interpreted as indicating a potential conflict of interest from increasing demand for a finite resource that is already used. Where the introduction of the ISI sector may necessitate a shift in how woody feedstock markets in general, and by-product markets in particular, operate. Alternatively, the results can be interpreted as an indication of the improbability of the ISI sector substituting fossil fuels for biofuels, since such a development would cause feedstock prices to spiral, thereby making the switch less likely. The primary reasons for why the ISI sector would consider substituting metallurgical coal for charcoal is arguably the green credentials of the latter and the low cost of the woody feedstock. However, woody biomass is sold on established feedstock markets. This entails that if the ISI sector enters the marketplace, the status quo will be disturbed and prices will change. Thereby potentially rendering the ISI sector’s decision to start substituting fossil fuels with charcoal unprofitable.

A potential way of countering the feedstock price changes indicated by the results is to increase the harvesting rate of roundwood. However, forest owners in the model are not able to fully respond to the increased roundwood demand since the harvesting constraint parameter () limits the amount of roundwood that can be harvested, see EquationEquation (8

(8)

(8) ). The same is true for the supply of harvesting residues. If harvesting rates increase, the competition effect will be alleviated to a degree and price changes will not be as severe as they otherwise would. A similar development can be observed on by-product markets, were the sawmill sector is unable to increase supply since it is operating at, or close to, capacity in most regions. The sawmill sector is thus unable to fully take advantage or respond to the large price increase in woody by-products.

It is estimated that the use of charcoal by the steel industry in Norrbotten County can result in an annual total saving of approximately 1.04–1.14 Mton of CO2 (Wang et al. Citation2015). However, the model result suggests that the use of refined woody biomass in the blast furnace will cause production of pellets and heat to decrease. Such an outcome may in worst case cause end-consumers and DH utilities to increase their use of fossil fuels to satisfy the energy demand. The largest drop in heat and pellets consumption corresponded to 295 GWh of heat and 1933 GWh of pellets. Replacing the total energy content with fuel oil (EO1) will result in the emission of approximately 0.718 Mton of CO2.Footnote9 The total annual CO2-saving is then between 0.32 and 0.42 Mton. However, it is worth noting that no conversion or transmission losses are accounted for in the model. The decrease in total bioenergy production may therefore be underestimated, since more woody materials are required at all production level. While it may be unlikely that end-consumers and DH utilities replace the energy content of woody biomass with fuel oil, the example highlights the intrinsic conflict present when analyzing this type of problem, i.e. the increased use of a finite feedstock that is already utilized. The result suggests that if the ISI sector starts using refined woody biomass, other sectors that are producing carbon-neutral sources of energy will have to adjust to the changing market condition and lower its production. This entails that the total abatement of CO2-emissions will not correspond to the saving of one actor but rather the sum total of the whole system. A green steel industry will potentially come at the expense of increased emissions elsewhere, meaning that society is not necessarily made better off by the change, and will only lead to rising feedstock prices.

Conclusion

It can be argued that society at large is facing a proverbial fork in the road. Either (a) increase the utilization rate of woody materials, and continue the transition toward a bioeconomy; or (b) uphold the status quo and safeguard the interests of the existing forest industries and the biodiversity of forestlands. The primary concern facing communities in northern Sweden and Finland is arguably the effects increased competition may have on local DH utilities and their ability to maintain heat production. Due to the harsh and cold climate in these regions, DH utilities provide a critical societal good. It can be argued that the reliability of the system is one of its strongest sale points, the other being its green credentials, part of which is based on the use of woody biomass. A reduction in supply of woody materials can potentially cause reliability issues, forcing the sector to change which commodities they use to produce heat, thereby undermining the system. This development may also have an effect on the price of heat, since a rise in input prices will be passed on to the end-consumer.

Regarding future research, a possible way to alleviate some of the short-comings observed in the model is to develop a dynamic model that allows for capital investment and takes into consideration the annual growth rate of the timber stock (see e.g. Bolkesjø et al. Citation2005). These developments would allow forest owners to increase the harvesting rate of roundwood and harvesting residues as demand and prices increase; and the sawmill sector to increase its capacity to take advantage of the new demand structure. The NCFSM can also be expanded both geographically and sectorally. The number of included regions can be expanded, and the geographical detail can be increased. The latter is most easily done by having all regions on a county level, i.e. the lowest geographical resolution for which there exist reliable and accessible data. The number of wood consuming sectors can also be increased, and other potential wood consumer can be added to the model; and the number of end-goods being produced can easily be expanded and depicted in greater detail. It is also worth highlighting that while the NCFSM explores regional effects in northern Sweden and Finland, the model’s core specifications are applicable to other geographical regions.

Acknowledgements

The authors would like to thank Robert Lundmark, Ismail Ouraich, Elisabeth Wetterlund, Chuan Wang, and Chinedu Nwachukwu for their input and comments.

ORCID

Elias Olofsson http://orcid.org/0000-0001-7303-7769

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes

1. Hot metal is the molten iron that is being produced in a blast furnace; and to avoid confusion or the misuse of steel industry terminology, it is assumed to be the primary production good of the ISI sector. Further refurbishment of the good is outside of the scope of the model.

2. It is worth noting that the total amount of CO2 emitted in the steel-making process will not necessarily be reduced by using biomass instead of fossil fuels. Rather the amount of CO2 emitted when using woody biomass will, in a best case scenario, correspond to that being consumed during the growth of the woody material. In such a case, the feedstock will be carbon-neutral.

3. The bioenergy sector is defined as the aggregated district heating (DH) industry of a region. However, for Northern Finland the industry sector is made up by local combined heating and power (CHP) plants, but it is assumed to only produce heat. Only production originating from woody fuels are considered; all other fuel sources are outside of the model. DH utilities integrated in other industries are not considered.

4. See Appendix 1 for model notations.

5. m3fub measuring unit corresponding to cubic meter solid volume excluding bark, and is a commonly used unit in the Swedish forest industry. The alternative notation of m3f is used to notate the solid volume for commodities that are not bark clad, e.g., pellets or by-products.

6. The remaining fuel demand must in such a case be satisfied through other means, e.g., fossil fuels. However, fossil fuels are not explicitly included as a feedstock alternative in the NCFSM.

7. See Appendix 3 for estimated feedstock prices.

8. It is important to keep in mind that the results of the model is contingent on a number of assumptions. For a general sensitivity analysis of the NCFSM, see Olofsson E. 2018. An introduction to the Norrbotten County Forest Sector Model – Technical report for a regional partial equilibrium model for a general sensitivity analysis of the NCFSM.

9. The author's own calculation.

References

- Asmoarp V, Davidsson A. 2016. Skogsbrukets transporter 2014 [Forestry transports 2014]. Skogforsk; [cited 2017 Nov]. Available from: https://www.skogforsk.se/kunskap/kunskapsbanken/2016/skogsbrukets-transporter-2014/.

- Bioenergi. 2017. Pellets i Sverige [Pellets in Sweden]; [cited 2017 Dec]. https://bioenergitidningen.se/e-tidning-kartor/pelletskartan.

- Bolkesjø TF. 2004. Modeling supply, demand and trade in the Norwegian forest sector. Ǻs: Agricultural University of Norway.

- Bolkesjø TF. 2005. Projecting Pulpwood Prices under Different Assumptions on Future Capacities in the Pulp and Paper Industry. Silva Fennica. 39(1):103–116.

- Bolkesjø TF, Trømborg E, Solberg B. 2005. Increasing forest conservation in Norway: consequences for timber and forest products market. Environ Resour Econ. 41:95–115. doi: 10.1007/s10640-004-8248-0

- Buongiorno J. 1996. Forest sector modeling: a synthesis of econometrics, mathematical programming, and system dynamics methods. Int J Forecast. 12(3):329–343. doi: 10.1016/0169-2070(96)00668-1

- Carlsson M. 2012. Bioenergy from the Swedish forest sector. Uppsala: Swedish University of Agricultural Sciences.

- Caurla S, Garcia S, Niedzwiedz A. 2015. Store or export? An economic evaluation of financial compensation to forest sector after windstorm. The case of Hurricane Klaus. Forest Policy Econ. 61(Supplement C):30–38. doi: 10.1016/j.forpol.2015.06.005

- Child M. 2014. Industrial-scale hydrothermal carbonization of waste sludge materials for fuel production. Lappeenranta: Lappeenranta University of Technology.

- EI. 2017. Fjärrvärmekollen [District heating auditing]. Swedish Energy Markets Inspectorate; [cited 2018 May]. Available from: http://ei.se/sv/start-fjarrvarmekollen/.

- Ejdemo T, Söderholm P, Ylinenpää H. 2014. Norrbottens roll i samhällsekonomin – En kritisk granskning av indikatorer samt några lärdomar för framtiden [Norrbotten County's role in the economy]. Länsstyrelsen i Norrbotten.

- FFI. 2017. Statistics. Finnish Forest Industries; [cited 2018 May]. Available from: https://www.forestindustries.fi.

- Hazell PBR, Norton RD. 1986. Mathematical programming for economic analysis in agriculture. New York (NY): Macmillan. rBiological Resource Management.

- Johansson MT. 2016. Effects on global CO2 emissions when substituting LPG with bio-SNG as fuel in steel industry reheating furnaces – the impact of different perspectives on CO2 assessment. Energy Efficiency. 9(6):1437–1445. doi: 10.1007/s12053-016-9432-0

- JTI. 2013. Exempel på bränsledata för olika bränslen [Fuel data for different fuels]. Swedish Institute of Agricultural and Environmental Engineering; [cited 2017 Nov]. Available from: http://www.bioenergiportalen.se/?p=1590.

- Kallio AM, Dykstra DP, Binkley CS. 1987. The global forest sector: an analytical perspective. Chichester (UK): John Wiley & Sons. IIASA.

- Kallio AM, Hänninen R, Vainikainen N, Luque S. 2008. Biodiversity value and the optimal location of forest conservation sites in Southern Finland. Ecological Economics (67): 232–243.

- Kangas H-L, Lintunen J, Pohjola J, Hetemäki L, Uusivuori J. 2011. Investments into forest biorefineries under different price and policy structures. Energy Econ. 33:1165–1176. doi: 10.1016/j.eneco.2011.04.008

- Korhonen K-M. 2015. Introduction to the forestry in lapland; [cited 2017 Oct]. Available from: http://www.metsa.fi/documents/10739/4144441/Introduction+to+the+Forestry+in+Lapland100615.pdf/4f64cf6e-b751-4ebc-bf5b-8f4a2d21ac9c.

- Larsson M, Anheden M, Uhlir L. 2014. Roadmap 2015 to 2025 Biofuels for low-carbon steel industry. Gothenburg. Research Institutes of Sweden.

- Latta GS, Sjølie HK, Solberg B. 2013. A review of recent developments and applications of partial equilibrium models of the forest sector. J Forest Econ. 19(4):350–360. doi: 10.1016/j.jfe.2013.06.006

- Lecocq F, Caurla S, Delacote P, Barkaoui A, Sauquet A. 2011. Paying for forest carbon or stimulating fuelwood demand? Insights from the French forest sector model. J Forest Econ. 17(2):157–168. doi: 10.1016/j.jfe.2011.02.011

- Lestander D. 2011. Competition for forest fuels in Sweden – exploring the possibilities of modeling forest fuel markets in a regional partial equilibrium framework. Uppsala: Swedish University of Agricultural Sciences.

- LUKE. 2017. Statistics database. Natural Resources Institute Finland ; [cited 2017 Nov]. Available from: http://statdb.luke.fi/PXWeb/pxweb/en/LUKE/?rxid=aefb4d14-6df8-4981-a304-01c37a46d087.

- Mandova H, Leduc S, Wang C, Wetterlund E, Patrizio P, Gale W, Kraxner F. 2018. Possibilities for CO2 emission reduction using biomass in European integrated steel plants. Biomass Bioenergy. 115:231–243. doi: 10.1016/j.biombioe.2018.04.021

- Mefos S, editor. 2017. Grön Masugn – Fokus biomassa [Green blast furnace – focus biomass] Grön Masugn workshop; Luleå.

- Metla. 2014. Statistical Yearbook of Forestry. Vantaa. Finnish Forest Reseach Institute.

- Mousa E, Wang C, Riesbeck J, Larsson M. 2014. Biomass applications in iron and steel industry: an overview of challenges and opportunities. Renew Sust Energy Rev. 65:1247–1266. doi: 10.1016/j.rser.2016.07.061

- Mustapha W. 2016. The Nordic forest sector model (NFSM): data and Model Structure. INA fagrapport 38.

- Mustapha W, Trømborg E, Bolkesjø TF. 2017. Forest-based biofuel production in the Nordic countries: modelling of optimal allocation. Forest Policy Econ.

- Northway S, Bull GQ, Nelson JD. 2013. Forest sector partial equilibrium models: processing components. Forest Sci. 59(2):151–156. doi: 10.5849/forsci.11-156

- Novator. 2006. Fakta om biobränsle [Fact about biofuels]; [cited 2017 Oct]. Available from: http://www.novator.se/bioenergy/facts/fakta-1.html.

- Nwachukwu C, Toffolo A, Wang C, Grip C-E, Wetterlund E. 2018. Systems analysis of sawmill by-products gasification towards a bio-based steel production. International Conference on Efficiency, Cost, Optimization, Simulation, and Environmental impact of Energy Systems Guimaraes, Portugal.

- Olofsson E. 2018. An introduction to the Norrbotten County forest sector model – technical report for a regional partial equilibrium model.

- Olofsson E, Lundmark R. 2018. Competition in the forest sector: an extensive review. Swedish Association for Energy Economics (SAEE) conference 2016, Luleå, Augt 23–24 2016.

- Olsson A, Lundmark R. 2014. Modelling the competition for forest resources: The case of Sweden. J Energy Nat Resour. 3(2):11–19. doi: 10.11648/j.jenr.20140302.11

- Riksdag S. 2015. Avståndsbaserad vägslitageskatt för tunga lastbilar [Distance based road wear tax for heavy trucks]; [cited 2017 Dec]. Available from: https://www.riksdagen.se/sv/dokument-lagar/dokument/kommittedirektiv/avstandsbaserad-vagslitageskatt-for-tunga_H3B147.

- Selkimäki M, Röser D. 2009. Pellet logistics and transportationof raw materials in Finland. PELLETime. Vantaa. Metla.

- SEPA. 2017a. Utsläpp av växthusgaser från industri [Emissions of greenhouse gases from industry]. Swedish Environmental Protection Agency ; [cited 2017 Nov 29]. Available from: http://www.naturvardsverket.se/Sa-mar-miljon/Statistik-A-O/Vaxthusgaser-utslapp-fran-industrin.

- SEPA. 2017b. Sverige halvvägs till klimatetappmålet för år 2030 [Sweden halfway to the climate target for the year 2030]. Swedish Environmental Protection Agency – Naturvårdsverket ; [cited 2017 Dec 12]. Available from: https://www.miljomal.se/Aktuellt/Alla-nyheter/Sverige-halvvags-till-klimatetappmalet-for-ar-2030/.

- SFA. 2014. Skogsstatistisk årsbok 2014 – Swedish statistical yearbook of forestry. Swedish Forest Agency.

- SFIF. 2017. Member-map. Swedish Forest Industries Federation; [cited 2018 May]. Available from: http://www.forestindustries.se/about-us/our-members/member-map/.

- Suopajärvi H, Fabritius T. 2013. Towards more sustainable ironmaking – an analysis of energy wood availability in Finland and the economics of charcoal production. Sustainability. 5:1188–1207. doi: 10.3390/su5031188

- Suopajärvi H, Kemppainen A, Haapakangas J, Fabritius T. 2017. Extensive review of the opportunities to use biomass-based fuels in iron and steelmaking processes. J Clean Prod. 148(Supplement C):709–734. doi: 10.1016/j.jclepro.2017.02.029

- Toppinen A, Kuuluvainen J. 2010. Forest sector modelling in Europe – the state of the art and future research directions. Forest Policy Econ. 12(1):2–8. doi: 10.1016/j.forpol.2009.09.017

- Trømborg E, Bolkesjø TF, Solberg B. 2007. Impacts of policy means for increased use of forest-based bioenergy in Norway – a spatial partial equilibrium analysis. Energy Policy. 35(12):5980–5990. doi: 10.1016/j.enpol.2007.08.004

- Trømborg E, Bolkesjø TF, Solberg B. 2013. Second-generation biofuels: impacts on bioheat production and forest products markets. Int J Energy Sect Manag. 7(3):383–402. English. doi: 10.1108/IJESM-03-2013-0001

- Wang C, Mellin P, Lövgren J, Nilsson L, Yang W, Salman H, Hultgren A, Larsson M. 2015. Biomass as blast furnace injectant – Considering availability, pretreatment and deployment in the Swedish steel industry. Energy Convers Manag. 102:217–226. doi: 10.1016/j.enconman.2015.04.013

- Wei W, Mellin P, Yang W, Wang C, Hultgren A, Salman H. 2013. Utilization of biomass for blast furnace in Sweden: biomass availability and upgrading technologies. Stockholm. Report I:1. 978-91-7501-989-5.

Appendices

Appendix 1. Model notations

Table A1. Sets notations.

Table A2. Parameter notations.

Table A3. Variable notations.

Appendix 2. Forest industry Norrbotten County

Table A4. Forest industries and steel mill in Norrbotten County.

Appendix 3. Estimated feedstock prices

The suggested percentage change in feedstock price (, and ) are in the following section converted into SEK/m3fub or SEK/m3f. The reference price of secondary woody materials was collected from SFA (Citation2014) and converted from SEK/MWh into SEK/m3f using estimated energy content and bulk density data from Novator (Citation2006); JTI (Citation2013); SFA (Citation2014). See Olofsson (Citation2018) for additional information regarding the estimated energy content of the woody feedstock.