ABSTRACT

This paper examines the transformative potential of inward investment on cluster development. It undertakes this through the lens of the evolving semiconductor cluster in South Wales (UK) and within a context whereby the semiconductor industry is under pressure with government interventions to improve prospects being implemented at a time of increasing global tension in the industry. The paper reveals the potential of inward investors as agents of regional economic change and cluster development. It shows that the emerging South Wales cluster distinguishes itself in terms of investment motivation, commodities and services produced. These factors result in growing embeddedness in relation to elements such as joint research with higher education and intra-firm collaboration to develop new products and processes. The paper concludes that investments based on risky and fast-changing technologies in industries such as the semiconductor sector necessarily create challenges for policy makers. These are best managed by placing greater emphasis on developing the conditions to satisfy the needs of such knowledge-intensive industries in relation to labour market conditions, factor conditions and market access.

1. Introduction

The significance of the semiconductor industry has been underlined in recent years by attempts of national governments to support firms in the industry, to strengthen the security of value chains in the sector and to protect intellectual property and research (Huggins et al. Citation2023). The US Chips Act of 2022 (US Department of State Citation2022) has become an intervention benchmark with similar interventions occurring in China, Korea, Taiwan and the European Union (European Commission Citation2022). The UK has also moved to support the semiconductor industry, with the aims contained in the UK National Semiconductor Strategy (DSIT Citation2023). Part of the UK strategy is the encouragement of identified UK clusters of semiconductor activity, and planned interventions are associated with improving both capacity and capability in a sector that has been seriously weakened (Johnston and Huggins Citation2022). One identified ‘shining light’ in the UK strategy has been the compound semiconductor cluster in South Wales (DSIT Citation2023).

Foreign direct investment (FDI) has formed a foundational part of this compound semiconductor cluster in South Wales but with limited understanding of its role. A better understanding of this developmental role is at the heart of this paper. The developmental role of past rounds of Welsh inward investment has been contested and with questions on its role in transforming the regional developmental trajectory (McNabb and Munday Citation2017; Welsh Government Citation2009). Wales is cited as an example of where historical positive public policy action in respect of attracting new investment capital has been valued in helping the local economy overcome shocks, but has arguably been less effective to transform the economy away from a low productivity trajectory since the 1960s (Kapitsinis, Munday, and Roberts Citation2021).

The paper examines the evolving compound semiconductor (CS) cluster in South Wales in order to analyse the potential role of inward investors as agents of regional economic change. This analysis indicates that a characteristic of the cluster is the use of local knowledge, expertise and assets across the compound semiconductor space, in terms of research collaboration and specialist facilities, in close conjunction with FDI.

The paper contributes to the literature on regional development in more disadvantaged local economies by indicating the transformative role of inward investment in fostering clusters of knowledge-intensive industry as well as the role of agency and network dynamics associated with such development. While revealing a new approach to inward investment, and regional transformation potential, the case also reveals the role of a ‘triple helix’ approach to regional economic development policy, whereby firms of different sizes, are linked to local R&D institutions, and then to associated government and public agencies in a configuration that works to improve prospects for local productivity growth (see Johnston and Huggins Citation2022; Leydesdorff Citation2000).

The second section reviews the literature on the role of inward investment in the regional economy, its role in cluster development, and its potentially transformative capability. This indicates the potential importance of knowledge spillovers resulting from selected forms of inward investment and reveals Wales to be a useful lens through which to examine questions on the transformative role or otherwise of inward investment. The third section provides background on the development of the UK semiconductor sector and highlights recent events of relevance to Wales. The fourth section discusses the method of collecting the data to inform the paper. The fifth section analyses the emerging semiconductor cluster in Wales and seeks to identify characteristics of inward investment into the sector that signal a more transformative regional development role. The final section discusses the meaning of the findings and concludes with implications for regional economic development policy.

2. Transforming regions with inward investment

2.1 Revisiting the costs and benefits of inward investment

Inward investment is often considered a factor promoting host location economic growth because it is associated with technological improvement and new capital formation. Several conduits have been identified through which inward investment affects economic growth, including human capital formation, better integration into the global economy, increased competition and business development and restructuring (Forte and Moura Citation2013).

The effects of inward investment are, however, contested. Inward investment may have negative impacts in terms of the employment of unskilled labour and lead to a lower regional skills equilibrium (Bailey and Driffield Citation2007; Firn Citation1975). Moreover, the transformative potential of inward investment may be lessened in cases where externally owned plants do not embed themselves into the local economy and community and could relocate more easily when the political or socio-economic environment changes (Fuller and Phelps Citation2018; McAleese and Counahan Citation1979; Wei Citation2015).

One evidence of lower levels of regional embeddedness of inward investment capital can be seen in a production-only, as opposed to a knowledge focus of manufacturing activity, with more ‘routine’ business activities allocated by foreign firms to the region in question (Huggins and Izushi Citation2007). Typically, the commodities produced are towards the end of the product life cycle and with limited opportunities for innovation in production. Consequently, this activity rarely involves fundamental R&D or extensive collaboration with the university sector or other research institutions.

Such a lack of embeddedness results in lower levels of skills/knowledge-intensive R&D and engineering activity at the regional level, contributing to a low skills equilibrium in the host economy (Welsh Government Citation2009). External control may also pose additional constraints linked to non-local procurement patterns with reduced regional expenditure multiplier effects (Fuller and Phelps Citation2018).

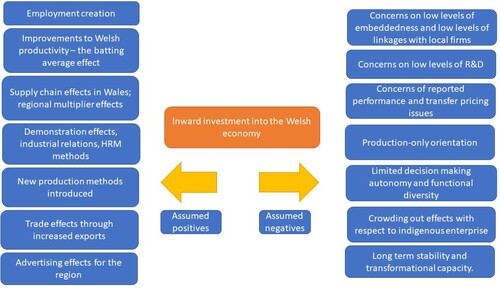

In the case of Wales, pertinent to this paper, it was identified as one of the most successful UK regions in attracting inward investment in the 1980s and 1990s. Key location determinants included grants and subsidies, infrastructure access to EU markets and relatively low unit labour costs (Hill and Munday Citation1992). The location marketing effort was led strongly by the Welsh Development Agency that sought to streamline regional marketing and present a ‘Team Wales’ approach to inward investment attraction. Between 1984 and 2007 it is estimated that inward investment into Wales resulted in approximately £13.5bn of investment and close to 100,000 planned new jobs (Welsh Government Citation2009). summarizes the findings from a review of the literature on inward investment in Wales (derived from Welsh Government Citation2009). On the left of the figure are a series of factors that were drawn out of the regional literature as potential positives of inward investment. On the right is a summary of the concerns that have been raised.

Figure 1. Reported strength and weaknesses of inward investment for Wales.

Critically, specific characteristics of inward investment impact the propensity for knowledge spillovers. This poses challenges for the host economy as it is precisely this channel that is considered the most important effect of inward investment, with the potential to change the relative competitive position of local and foreign firms (Perri and Andersson Citation2014; Perri and Peruffo Citation2016). The potential for knowledge spillovers connects to the characteristics of the inward investment itself. For example, the lack of a local core of decision-making in large firms has been a common theme in the regional economic development literature since the seminal work of Firn (Citation1975), who showed that regions where firms are largely externally controlled and owned could lose out to other regions and with external ownership linked more to ‘management’ as opposed to ‘entrepreneurship’ activity. A corollary is that businesses investing overseas have historically tended to maintain their high-technology and knowledge-intensive resources within their home location.

A difficulty in much of this literature, however, has been establishing the nature of a counterfactual i.e. what would have occurred without the exogenous investment. Inward investment has been shown to have had some positive impacts on the Welsh economy, creating employment, providing some well-paid jobs and enhancing economic stability (McNabb and Munday Citation2017). However, Wales has maintained its position somewhere close to the bottom of the UK regional productivity rankings, and with relatively poor productivity growth (Kapitsinis, Munday, and Roberts Citation2021). Policymakers have suggested the inward investment strategies should then be steered more towards inward investors who bring HQ-type and higher order management and research functions to Welsh industry.

Given this, the question we consider is how far activity in the emerging compound semiconductor (CS) cluster marks a different pattern from what has gone before, not least in terms of the establishment of a strong network involving inward investors, higher education institutions and public sector (including actors such as Welsh Government and Cardiff Capital Region) as well as what this means in terms of policy development towards inward investment.

2.2 Transforming the local economy: FDI in clusters and innovation

In light of the above, the influence of inward investment on a local economy relies on both the knowledge intensity of the investment and local characteristics. However, there has also been interest in the specific role of foreign capital in strengthening industrial clusters (Ryan et al. Citation2021; Ryan and Giblin Citation2012) and regional innovation systems of which clusters are a part (Cooke Citation1996, Citation2012). For example, foreign subsidiaries upscale a cluster, while inward investment in a cluster can facilitate the internationalization of local companies, and the presence of multinationals in a cluster may enhance the interconnectivity among different clusters (Hervás-Oliver, Albors-Garrigós, and Dalmau-Porta Citation2008).

A cluster may also benefit from inward investment through the encouragement of local entrepreneurship (Ryan et al. Citation2021; Thompson and Zang Citation2022). New ventures established by former workers from multinationals can result in technological heterogeneity, which could be crucial for the resilience of a regional cluster (Ryan et al. Citation2021). In general, therefore, the characteristics of FDI with higher value-added activities may lead to stronger positive effects on the development and dynamics of a cluster.

Linked to impacts on clusters of interrelated industry and institutional activity is the prospect for inward investment to affect host innovation systems (Cooke Citation2012; Rodríguez-Pose and Crescenzi Citation2008), thereby influencing regional development paths (Huggins and Thompson Citation2023; Thompson and Zang Citation2022). Regional innovation systems might be described as organizationally thin or thick, with thin systems being identified with, for example, ‘branch plant’ economies (Cooke Citation1996; Tödtling and Trippl Citation2005). Alternatively, in organizationally thick regional innovation systems, development paths might be linked to indigenous spin-offs from knowledge institutions working with the local industry base, with this resulting in more likelihood of extant regional industries diversifying into new areas (Chaminade et al. Citation2019).

In particular, where inward investor products are mature or at the end of their life cycle there may be more limited scope for knowledge spillovers into the local economy, innovative spin-offs or new entrepreneurial behaviour development (Chaminade et al. Citation2019). There is also a profit contingency as surpluses from more mature goods might simply be returned to head offices elsewhere, as opposed to being reinvested in local operations, which again places limits on what can be achieved in regional subsidiaries (Munday, Peel, and Taylor Citation2005).

The above illustrates a potential fundamental developmental problem whereby inward investors may act as potential corporate bed blockers, surviving over a long period and soaking up regional factors in a limited range of functions (McNabb and Munday Citation2017). With the headquarters (HQ) located out of the region, the entrepreneurial capacity of the territorial economy declines, alongside its ability to innovate. This creates challenges for future policy initiatives towards inward investment.

2.3 Inward investment policy, agency and the triple helix

Inward investment policy of ‘old’ followed a series of well-rehearsed rules, encompassing the provision of pragmatic attractions such as financial incentives, ample land availability and a sound infrastructure with competitively priced labour (Lall Citation1995). As the knowledge economy is prioritizing the nurturing of skills and talent (Brown, Hesketh, and Williams Citation2004), it is also changing how economies attract the types of overseas investments creating high value-added. Global competition for such investment is increasing, requiring shifts in policy and strategy (Huggins et al. Citation2023). Economies that have traditionally attracted high shares of such investment may need to think more innovatively about how they attract and embed knowledge-based external capital. It is important to understand the different approaches required to attract and embed knowledge-based investment compared with more traditional sectors of activity.

Traditional areas of inward investment, such as textiles, medium manufacturing and basic consumer electronics have declined within most OECD nations and are being replaced by knowledge-based activities such as financial services and pharmaceuticals (Crescenzi, Di Cataldo, and Giua Citation2021). Also, the size of initial inward investments in developed economies has fallen in recent years, with a switch toward attracting smaller and growing knowledge-intensive businesses, as mainstream and large-scale manufacturing operations relocate to developing nations in Eastern Europe and Asia, particularly in the 2000s (Kapitsinis Citation2017).

Given the above, there is a requirement for disadvantaged regional economies to formulate investment conditions both for retaining home-grown companies and for encouraging inward investors to choose their nation or region as a home for knowledge-intensive industries. Under the new environment, the primary goal and means of inward investment attraction is based more on the creation of knowledge spillovers, such as the transfer of new skills, science and management techniques (Baltagi, Egger, and Kesina Citation2015; Thompson and Zang Citation2022). Viewed by the host economy, such spillovers may stimulate emerging cluster development, encouraging local competition and innovation.

More generally, when knowledge is the key competitive component of investment attraction, land or plant-based policy incentives become less relevant, replaced by opportunities for networking and technology transfer (Kowalski, Rabaioli, and Vallejo Citation2017). Chiefly, this might come in the form of fostering local and global relationships and networks between indigenous businesses and inward investors. An existing concentration of well-qualified workers is a crucial cog in the building of successful knowledge-based inward investment policies. Therefore, if the correct mix of skills is present, a knowledge-based company is more likely to gravitate toward a particular region whether or not there are subsidies on offer.

By attracting knowledge workers, firms and investors may follow, allowing further start-up investment to be available and allowing cluster development to occur (Huggins and Izushi Citation2007). Indeed, inward investment interventions are likely to benefit from being grounded in a triple helix approach to cluster and innovation system development. Such an approach seeks to connect domestic and foreign firms with R&D capacity in higher education institutions and relevant government and public agencies (Ranga and Etzkowitz Citation2013). In this case, higher levels of regional innovation and productivity growth are likely to require higher levels of networked behaviour between industry, government and higher education. In this respect, Harris (Citation2021) shows that literature seeking to explain cluster evolution requires more actor-centric approaches, and reveals that a better understanding of the combination of shared goals, behaviours and relationships between cluster participants (cluster institutional configurations) can provide a way of understanding how actors drive cluster evolution (p. 437). For example, shared goals of an institutional configuration in terms of seeking to make a cluster internationally competitive, might be linked with cluster outcomes in terms of stronger relationships with extra-local research organizations, which could be particularly important in the growth phase of the cluster.

If a triple helix approach is to actually promote innovation and economic development there is clearly a requirement for actors to possess and utilize a significant degree of agency in order to catalyse change (Grillitsch and Sotarauta Citation2020). Indeed, Harris (Citation2021) highlights how actors, for example, can work to change existing patterns of shared goals and behaviours of cluster actors, and argues that Silicon Valley is a case whereby an integrated firm and government institutional configuration leads to cluster evolution. Agency may come from individual actors, such as the inward investors themselves – so-called firm-level agency – or from the triple helix cluster itself – so-called system-level agency (Benner Citation2024; Leydesdorff Citation2000). It is this system-level agency whereby the discourse stemming from networks dynamics may result in heightened embeddedness and new regional development narratives (Beer, Barnes, and Horne Citation2023; Huggins and Thompson Citation2023).

In this sense, Wales is a useful lens for exploring the transformative role of inward investment, and the importance of a triple helix approach, and agents within it, to transforming regional prospects. It is an economy where many of its business head offices are located outside the region or the UK, with prior work suggesting this impacts the quality of underlying business activity and skills (Phelps Citation2016; Welsh Government Citation2009). Indeed: ‘One of the most defining characteristics of the Welsh economy when looked at in an evolutionary perspective is its enduring dependence on external and often cost-sensitive investment’ (Bristow and Healy Citation2015, 248).

3. The semiconductor industry in the UK

Owen (Citation2022) in a review of the historical development of the UK semiconductor industry concludes that there has been limited UK Government interest in the sector. As far back as the 1980s the UK industry had lost competitiveness with US firms, neglecting investment in high-volume memory devices and micro-processors with activity concentrated in semiconductors for telecommunications and defense. Owen (Citation2022) concludes that by the 2000s domestic firms had largely moved away from ‘mainstream’ semiconductor production, but with smaller-scale fabrication plants serving a few niche markets, and with the UK having strengths in other parts of the semiconductor industry.

A House of Commons (2022) review also highlighted a long-run lack of investment into the development of UK semiconductor facilities for 20–30 years, while showing that this same lack of patchy investment has: ‘Led to a distinct semiconductor ecosystem in the UK, with specialised “clusters” forming around fabs providing jobs, spin-offs, and links with academia' (p. 13). The review estimated that the UK semiconductor industry was focused on 25 manufacturing sites, with facilities processing wafers ranging from a few hundred to several thousand per month and covering compound epitaxy (growing crystals on wafers) and legacy silicon production to thin film fabrication (producing flexible semiconductor devices) (DSIT Citation2023). These devices and components target markets such as sensors, photonics, battery technology and communications. Moreover, there are over 100 semiconductor design and IP houses in the UK (Global Counsel and Imagination Citation2022).

UK Government interest in the semiconductor sector has turned a corner. A ‘side-effect’ of Covid-19 was to highlight the importance of the semiconductor industry, and with the pandemic revealing the dependence of Europe and the US on complex and sometime risky geographically distant supply chains (Huggins et al. Citation2023). Alongside are concerns around ‘digital sovereignty’ in key technologies, with this leading to UK Government interventions in 2022 in the case of the sale of the Wales-based Newport Wafer Fab to Chinese group Nexperia, and concerns about the Nvidia purchase of UK chip designer ARM from Japanese group Softbank. Pressure in 2021–2022 grew for a comprehensive UK strategy to encourage the sector, paralleling developments in other nations. For example, declining US semiconductor manufacturing activity was a key context for the development of the US CHIPS Act in 2022, which provided significant inward investment grants, tax credits and financial support for semiconductor design. Taiwan, South Korea and the European Union have linked initiatives as does China (Miller Citation2022).

The UK National Semiconductor Strategy (DSIT Citation2023) seeks to target resources on R&D, design, intellectual property and then identified national strengths in compound semiconductors and related materials. The plan commits £1bn to the UK industry, starting with £200 m for the period 2023–2025 (DSIT Citation2023). This funding will seek to improve and strengthen access to facilities and infrastructure by delivering a National Semiconductor Infrastructure Initiative and a specialist incubator pilot pertaining to semiconductor start-ups. These funds also aim to boost commercial innovation within UK SMEs and improve their attractiveness for domestic and global investors. Moreover, the UK government commits to strengthen international collaborations with countries such as the US, South Korea and Japan, seeking to develop skills and improve capacity and the resilience of the industry supply chain.

As indicated above, the strategy has come after a period whereby the domestic semiconductor sector has been viewed as weakened by a long-run lack of investment, restricted international collaboration, and extensive supply shortages (House of Commons Citation2022; Johnston and Huggins Citation2022; Citation2023). Moreover, resources available to strengthen the sector have been limited due to the 2022–2023 cost of living crisis, and limits on public spending following the interventions needed to deal with the Covid-19 pandemic.

Among proposals to improve the semiconductor industry is support for existing clusters of semiconductor activity in South Wales as well as Bristol, Cambridge, the North-East, Northern Ireland and Scotland (DSIT Citation2023). Critical is the South Wales cluster focused on emerging compound semiconductor technologies, an area of significant global growth. These technologies are forecast to underpin products linked to commodities needed in relation to progress towards net zero (see House of Commons Citation2022).

The UK Semiconductor Strategy (DSIT Citation2023) indicates that the emerging South Wales cluster constitutes the first compound semiconductor cluster globally. However, little is known about this emergence, particularly the potentially ‘transformative’ role of FDI in facilitating the development of this cluster.

4. Data and methods

The following analysis was informed by a series of data sources based on a triangulation of information gathered via an on-going case study analysis of an initiative to develop a compound semiconductor in South Wales that is termed CSconnected.Footnote1 This initiative seeks to build on regional strengths in advanced semiconductor materials and manufacturing. An element of the CSconnected work was the development of an annual survey of the firms and publicly funded institutions that form part of the CS cluster in Wales. This annual survey (for this paper materials derived from surveys covering cluster activity for 2020 and 2021) collected information with respect to business activity, employment, earnings, capital and operational spending. While some of the investments in the CS cluster have gone through different ownerships, activity has been maintained in Wales with limited instances of disinvestment.

In the case of business spending/linkages, the survey collected information in terms of the main categories of commodity spending as well as the destination of spending, i.e. in terms of proportions spent in Wales, rest of the UK and rest of the world. The collation of local spending data allowed the team to examine the extent of multiplier impacts back into the regional economy. Survey information was complemented, for analytical purposes, with data from company accounts.

The survey round for 2020 provided information for six out of seven of the principal private and public sector organizations involved in the CS cluster, and the 2021 survey covered eight out of nine organizations (i.e. with a new cluster entrant in 2021). The survey information allowed an analysis of the productivity, R&D spending, relative earnings and overseas trade propensity of the private sector employers in the cluster. For the 2021 survey round, the survey material was also complemented with a series of seven high-level interviews with private and public sector funded parts of the cluster. These interviews and site visits occurred between August-December 2021 and the interviewees comprised senior directors in cluster firms and the associated institutions. These interviews sought to gain more detailed information with respect to selected survey questions, particularly for products and services developed and innovative activity by cluster members. In other words, the role of the interviews was to ensure the veracity of the findings from the survey and also to provide some qualitative depth to understanding the process of change and the nature of the agency of this change. Finally, information on CS cluster activity was gained from attendance at regular meetings of the chief technical officers’ group of the collaborating manufacturing firms and organizations that were part of the CSconnected initiative funded by the UK government (via the UKRI ‘Strength in Places’ programme).

5. The Welsh compound semiconductor cluster: transformative potential?

The question first addressed here is: how far does the CS cluster differ in terms of ‘fit’ to the regional inward investment context outlined earlier? The CS cluster has features placing it in the knowledge-based category of Welsh inward investment stock, with it being potentially better placed than past investment in terms of generating local economic transformation, particularly because it forms a critical part of a network of private sector businesses, higher education and other research institutions and the public sector in Wales.

To begin with, provides a summary checklist of the expected effects of inward investment following from along with a brief appreciation based on our interviews and survey returns on how the CS cluster measures up. In what follows, we address ‘effects’ themes in terms of investment motivation, production activity and embeddedness, linking through to the transformation themes discussed in the review.

Table 1. Summary of CS cluster local economic effects.

5.1 Motivations for investment?

First, it was found that issues of factor costs and EU market access are largely secondary, and with markets served global in nature. While production costs in Wales for CS cluster firms are lower than in some competitor locations such as Singapore and Silicon Valley, supply side issues proved to be more fundamental to firms, with these issues pertaining to knowledge, technology, skills and institutional support. For example, important here are organizations such as the Compound Semiconductor Catapult which works to accelerate the adoption of compound semiconductor applications and with its Newport Innovation Centre being able to assist industry in engaging with new technology.

The CS cluster has also gained support from the Cardiff Capital Region City Deal. This is an agreement between the UK Government, the Welsh Government and ten local authorities covering the city region. The aim is to build a more connected, competitive and resilient community and region. Cardiff Capital Region has sought to support the CS cluster investing in a Compound Semiconductor Centre along with IQE plc, one of the private sector investors in the cluster.

The representative of one firm in the cluster argued that their location decision was primarily affected by the presence of key technology partners and whether or not there was a technology match. At the time of their location decision, another cluster member had useful linkages to a series of UK universities, while they also had pre-existing linkages with a second cluster member in terms of specialized chemical processes.

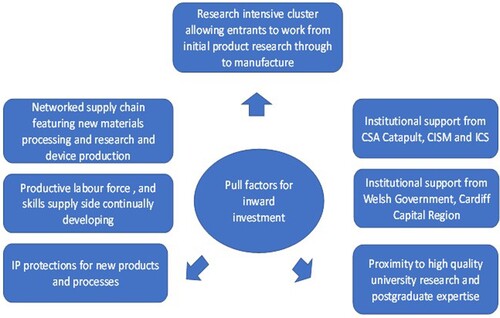

Continued inward investment into the CS cluster reflected a willingness to use Wales’ knowledge, expertise and assets across the CS space in terms of research collaboration and specialist facilities such as the Institute for Compound Semiconductors, Centre for Integrated Semiconductor Materials (CISM, Swansea University) and Compound Semiconductor Centre (Cardiff University). Access to higher education also supported recruitment for the CS cluster firms. It is estimated by the Higher Education Statistics Agency, that Welsh universities in 2021/22 produced around 11,000 graduates in subjects commonly used by the CS cluster firms each year. In consequence, recent trends in inward investment into the CS cluster revealed an element of technology and knowledge-sourcing investment making full use of the local cluster conditions as summarized by .

Figure 2. Pull factors for new inward investment in the CS cluster.

In summary, inward investment led to a more global market orientation, with a heightened focus on supply side issues, strategic collaborations, technology partnerships and the conscious utilization of local knowledge and talent. This transformation reflects a more adaptive approach to capitalize on the changing dynamics of the semiconductor industry.

5.2. What is produced?

As indicated earlier, much of Welsh inward investment after the 1980s has been connected to more mature products that were developed and researched elsewhere. In part, this regional manufacturing orientation worked to reduce R&D in the local economy, and with this being a factor that has been flagged up in research that has sought to explain Wales’ poor productivity growth record (Henley Citation2021).

Activity in the CS cluster appears quite different. The product set of the CS cluster is diverse in terms of production of chips, design, tooling, coatings on wafers, research, technical solutions and consultancy. The commodities vary in terms of their technological maturity, but with the overall market growing fast, compound semiconductors are increasingly adopted by diverse industries such as automotive, telecommunications and robotics (Huggins et al. Citation2023).

Critically, outputs in the CS sector are IP heavy, meaning that in addition to final goods and services the CS businesses in Wales produce intermediate knowledge and research outputs. For inward investors into the cluster there is therefore the opportunity to research and innovate, collaborate with one another on research funding for new products and services and collaborate with the university sector for testing and pure research. This is a key element of the triple helix approach and seems to strongly link to transformative potential. For example, currently, within the cluster, research is being undertaken into innovative new materials (such as Gallium Oxide) that are more cost effective than silicon, provide improved energy efficiency, and when applied to devices permit faster communication speeds. This means that there are products, services and technical solutions being jointly developed in Wales for international customers. A good example here is the case of one member of the CS cluster that produces advanced wafer products. Their underlying innovation created new export opportunities and importantly the advances made involved other firms within the CS cluster.

Indirect evidence for the knowledge and skills intensity of production can be found in the high salaries being offered in the CS cluster. This reflects the employment of operations staff but also highly qualified engineers and research personnel.

The survey revealed that the CS cluster paid an average gross wage of approximately £52,000 (annual average pay in Wales in 2021 for all full-time workers was around £32,700). Consequently, gross value added per employee in the CS cluster (estimated £121,000 in 2021) was well above the Welsh average.

Other indirect evidence is reflected in the wide constituency from which CS cluster members draw skills. For example, in the case of one inward investor, the local research and engineering team had developed to over 30 staff, with their Welsh site being the largest in Europe. The skills used by this investor are reflected in average salaries that topped £80,000 in 2021. The workforce derived from a constituency that included Hong Kong, Scotland and Italy and embraced postgraduate skills in material science, micro-electronics and chemistry. Indeed, for one inward investor the presence of the cluster of interrelated CS activity was critical when seeking to attract new talent as they believed that there was: ‘Enough going on here to get people’s interest’. Moreover, four manufacturing members of the CS cluster in Wales had 20% of their 1,300 workers involved in R&D activity, in 2021.

In summary, inward investment has markedly transformed the Compound Semiconductor (CS) cluster in Wales. Unlike past trends, the CS sector encompasses diverse activities, fostering intellectual property-heavy outputs. Cluster members benefit from collaborative research, innovation and triple helix partnerships, contributing to high salaries and a dynamic, knowledge-intensive environment, setting the CS cluster apart from historical Welsh investment patterns.

5.3 Embeddedness

For the CS cluster businesses, opportunities to purchase goods and services locally in Wales are currently limited. Indeed, our survey of the CS cluster suggests that local economic impact comes as much through the spending of employee wages and salaries as it does through spending with local producers of goods and services. This would be expected in the context of a small open regional economy such as Wales. That said, it is interesting to note that one of the larger cluster firms reports developing linkages in Wales and the South West of England in terms of specialized metal fabrication, machining and electronic components. Moreover, some of their suppliers had invested heavily in new clean room facilities, cleaning capability, and were employing manufacturing and design engineers to assist in developing the partnership links.

The CS cluster appeared to score more strongly on other facets of embeddedness with each of the cluster’s manufacturing firms maintaining a rich functional diversity in terms of staffing with limited resemblance to the production-only branch plant model more common in the 1980s and 1990s. Some of the cluster firms have HQ-type functions alongside production functions. This means that investment decisions with ramifications for the region are taken locally. A good example here is one investor that announced in 2021 it was seeking to develop a new R&D and manufacturing HQ site allowing for greater expansion. Importantly, there is evidence that decisions made in Wales shape the wider global operations of the cluster firms. For example, in the case of one firm all major policy and technological decisions are made from the Wales HQ in shaping the development and operations of their other plants in North America and Asia.

In terms of coupling with public and higher education institutions and other manufacturers, the development of the CS cluster speaks to these elements of embeddedness. For example, since 2018 there has been an increase in strategic coupling in Wales between the CS manufacturers, particularly in relation to research collaboration and joint research bids. A good case is whereby the manufacturing elements of the cluster joined with Cardiff and Swansea Universities, and public sector partners to successfully bid in 2020 for public sector funding to support cluster development. Another example was industry support for the development of a Compound Semiconductor Centre at Cardiff University.Footnote3

Businesses’ willingness to work together with universities and regional government to overcome challenges facing the whole sector is crucial here. For example, CS cluster firms have collaborated to develop elements of the UK supply chain related to innovations in material and ‘trench’ devices. These devices help in conducting electrical current from one semiconductor surface to another which improves the capability and efficiency of the devices. Such innovation is part of a process that seeks to develop a UK manufacturing capability in this technology. It is a consortium led by one cluster member that has worked to introduce new trench technologies to the UK. Other local members of the consortium include Swansea University and the Compound Semiconductor Centre. The Welsh partners seek to deliver industrial processes for trench etching, which significantly supports new supply chain development and the development of new human skills in an area where the UK economy has started to fall behind.

Similarly, there is evidence of evolving linkages between the CS cluster firms and higher education, and local and regional government in terms of skills provision, location marketing, research infrastructure and support for new inward investors. One example is the development of the Centre for Integrated Semiconductor Manufacturing (CISM) at Swansea University, which seeks to undertake research around compound semiconductor materials and processes and develop human capital to benefit the regional industry. The Centre is developing the capacity to offer research services to inward investors, but also the opportunity to link cluster firms to research undertaken by academic staff. Local collaborative partners in the venture include two cluster members, with other businesses and institutions in the process of joining at the time of writing. Critical here is that CISM builds upon a process whereby local research teams can use exactly the same equipment used or manufactured locally to test out new ideas. The cluster manufacturing partners had a role in planning a building that will support primary research leading to new opportunities for the same manufacturers.

In summary, inward investment has helped transform the cluster in terms of local economic impact as well as showcasing functional diversity and localized decision-making, with major global decisions increasingly being made in Wales. Collaborations with universities and public sector partners result in successful joint bids, supporting research and cluster development.

6. Discussion and conclusion

This paper reveals that Wales provides a useful example of positive public policy action in respect of attracting new investment capital. It also provides new evidence of the effectiveness of a triple helix approach to cluster and innovation system development that seeks to network private sector inward investors, with research institutions and public sector agencies. This investment has supported an increase in regional adaptive capacity and has begun to transform the economy away from what has been a low productivity trajectory.

While inward investment embeddedness has often been understood in terms of local buyer-supplier linkages and the presence of a local decision-making nexus, the example analysed shows that it is important to examine the evolution of inward investment and the strategic coupling between firms and institutions that moves beyond just purchasing and sales links.

The evolving CS cluster case provides evidence of the presence of these facets of emerging embeddedness, which are considered critical in growing the transformative potential of inward investment. highlights a range of key differences between the CS cluster approach to inward investment and the more traditional approach to such investment in relation to dimensions concerning investment motivations and product-set and procurement, as well as decision-making and skills, innovation and entrepreneurship, and employment impacts. These distinctions point to a more regionally transformative impact of the new approach.

Table 2. Comparing the new ‘transformative’ and traditional approaches to inward investment in supporting regional economic development.

In the past, many triple helix models have possessed actors from each of these sectors, but in regions such as Wales they have often lacked agency and were relatively disconnected (Grillitsch and Sotarauta Citation2020; Harris Citation2021; Leydesdorff Citation2000). However, in the analysed approach the model is fostering a collaborative ecosystem emphasizing strategic embeddedness and innovation to drive economic transformation. In particular, system-level agency across the cluster is emerging and providing the basis for the cluster’s increased embeddedness and growing economic performance (Benner Citation2024).

The paper provides a policy challenge. Prior research on Wales has suggested that foreign capital ownership and external control of businesses is likely to make the economy more resilient to the effects of shocks. This might be good news for policy makers seeking stability over the economic cycle. However, the inward investment history of Wales has seen a growing dependence on external capital creating a lock-in to a given development path (Huggins and Thompson Citation2023). This implies more stable employment but coupled with the maintenance of a low skills and innovation equilibrium, without transformation or upgrade of the developmental trajectory.

In this context, the compound semiconductor case is interesting since it provides evidence of national research funders, government, higher education and manufacturing companies engaging together with the dual challenges of marketing the location, but more importantly developing the strategic networks and coupling that can strengthen cluster appeal (Fuller and Phelps Citation2018). Moreover, following Harris (Citation2021) there is evidence here as to how actors have shared goals within an institutional configuration of firms, colleges and government, which has the objective of making inward investment in the cluster more internationally competitive. Indeed, this paper suggests that the cluster activity has been present for some time, but with limited external intervention to bring functions together as a means of location marketing and economic transformation.

Encouragement for research collaboration between manufacturers and higher education has been crucial, alongside the development of the education supply side, and coordination of activity benefitting the cluster in terms of its promotion internationally. An important feature of this more transformative model, therefore, is the capacity of the private sector players to make decisions in the local context, and then the presence of higher order and HQ functions. While this links to old debates in the regional economic development literature it seems central in this case.

Clearly, development conditions have to be created in such a way that high technology businesses bring in higher order functions to the region in question. This cluster of transformative activity in Wales is still evolving, with emerging challenges including the development of more technology linkages and cooperation between the manufacturing and institutional players in the cluster. In improving long run regional transformative capacity, the ownership of firms is expected to be important in the process of building and sustaining resilience. Wales has few large or medium sized, headquartered firms in high technology areas (Kapitsinis, Munday, and Roberts Citation2019). In terms of the CS cluster, therefore, future research might address how far further evolution will result in locally based and owned suppliers to the sector moving to higher levels of technology activity as a result of their cluster collaborations. Furthermore, research should monitor whether or not the higher education/manufacturing sector ties will lead to spin-off businesses in high technology areas.

In conclusion, this case demonstrates a policy/public resources issue when entering strategic interventions in the field of high-technology. The compound semiconductor sector is based on risky and fast changing technologies. The IP intensity and importance of R&D in the sector shows that new discovery/developments can quickly change the rules of the game. This creates a challenge for policy makers in that account must be taken of technology trends and underlying risks. This case also suggests a need for developing the conditions satisfying the requirements of knowledge intensive manufacturing vis-à-vis labour market conditions, factor and market access. This type of reorientation could limit the welfare losses that occur when regional policy resources and incentives are used to attract investors for short term gain, but actually work to obscure where the best locations for mobile capital might be.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 The research method underpinning this paper was reviewed by the Research Ethics Committee of the Lead Author Institution (Cardiff Business School). 21st May 2021. Reference SREC 2021061. The annual survey developed and resulting findings were approved by the Chief Technical Officers group of CSconnected.

2 ‘The business survey data supporting this study is not available because it contains commercially sensitive information on the firms involved. The aggregated findings from the business survey in terms of the contribution of the CS cluster to the Welsh economy in 2021 are reported in CSConnected and Welsh Economy Research Unit (Citation2022)'.

References

- Bailey, D., and N. Driffield. 2007. “Industrial Policy, FDI and Employment: Still Missing a Strategy.” Journal of Industry, Competition and Trade 7: 189–211. doi:10.1007/s10842-006-7185-8

- Baltagi, H., H. Egger, and M. Kesina. 2015. “Sources of Productivity Spillovers: Panel Data Evidence from China.” Journal of Productivity Analysis 43 (3): 389–402. doi:10.1007/s11123-014-0393-z.

- Beer, A., T. Barnes, and S. Horne. 2023. “Place-based Industrial Strategy and Economic Trajectory: Advancing Agency-Based Approaches.” Regional Studies 57 (6): 984–997. doi:10.1080/00343404.2021.1947485

- Benner, M. 2024. “System-level Agency and its Many Shades: Path Development in a Multidimensional Innovation System.” Regional Studies 58 (1): 238–251. doi:10.1080/00343404.2023.2179614

- Bristow, G., and A. Healy. 2015. “Crisis Response, Choice and Resilience: Insights from Complexity Thinking.” Cambridge Journal of Regions, Economy and Society 8: 241–256. doi:10.1093/cjres/rsv002

- Brown, P., A. Hesketh, and S. Williams. 2004. The Mismanagement of Talent: Employability and Jobs in the Knowledge Economy. Oxford: Oxford University Press.

- Chaminade, C., M. Bellandi, M. Plechero, and E. Santini. 2019. “Understanding Processes of Path Renewal and Creation in Thick Specialized Regional Innovation Systems. Evidence from two Textile Districts in Italy and Sweden.” European Planning Studies 27 (10): 1978–1994. doi:10.1080/09654313.2019.1610727

- Cooke, P. 1996. “The New Wave of Regional Innovation Networks: Analysis, Characteristics and Strategy.” Small Business Economics 8 (2): 159–171. doi:10.1007/BF00394424

- Cooke, P. 2012. “MNCs, Clusters and Varieties of Innovative Impulse.” In Innovation and Institutional Embeddedness of Multinational Companies, edited by Martin Heidenreich, 105–139. Cheltenham: Edward Elgar.

- Crescenzi, R., M. Di Cataldo, and M. Giua. 2021. “FDI Inflows in Europe: Does Investment Promotion Work?” Journal of International Economics 132: 103497. doi:10.1016/j.jinteco.2021.103497

- CS Connected and Welsh Economy Research Unit. 2022. Annual Report: Compound Semiconductor Cluster in South Wales. Cardiff: CS Connected. https://csconnected.com/media/ryunhxaa/csconnected-annual-report-cardiff-university-business-school.pdf

- DSIT. 2023. Department for Science, Innovation and Technology, National Semiconductor Strategy. https://www.gov.uk/government/publications/national-semiconductor-strategy

- European Commission. 2022. European Chips Act. https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/europe-fit-digital-age/european-chips-act_en

- Firn, R. 1975. “External Control and Regional Development: The Case of Scotland.” Environment and Planning A 7 (4): 393–414. doi:10.1068/a070393

- Forte, R., and R. Moura. 2013. “The Effects of Foreign Direct Investment on the Host Country’s Economic Growth: Theory and Empirical Evidence.” The Singapore Economic Review 58 (3): 1350017. doi:10.1142/S0217590813500173

- Fuller, C., and A. Phelps. 2018. “Revisiting the Multinational Enterprise in Global Production Networks.” Journal of Economic Geography 18 (1): 139–161. doi:10.1093/jeg/lbx024

- Global Counsel and Imagination. 2022. The Future of the UK’s Semiconductor Strategy an Alternative to Onshoring: Strategic Interdependency. https://6008785.fs1.hubspotusercontent-na1.net/hubfs/6008785/GC_Imagination_18_new%20colour.pdf

- Grillitsch, M., and M. Sotarauta. 2020. “Trinity of Change Agency, Regional Development Paths and Opportunity Spaces.” Progress in Human Geography 44 (4): 704–723. doi:10.1177/0309132519853870

- Harris, J. 2021. “Rethinking Cluster Evolution: Actors, Institutional Configurations, and new Path Development.” Progress in Human Geography 45 (3): 436–454. doi:10.1177/0309132520926587

- Henley, A. 2021. Wales’ Productivity Challenge: Exploring the Issues. Productivity Insights Paper No. 007, The Productivity Institute.

- Hervás-Oliver, J., J. Albors-Garrigós, and J. Dalmau-Porta. 2008. “External Ties and the Reduction of Knowledge Asymmetries among Clusters Within Global Value Chains: The Case of the Ceramic Tile District of Castellon.” European Planning Studies 16: 507–520. doi:10.1080/09654310801983308

- Hill, S., and M. Munday. 1992. “The UK Regional Distribution of Foreign Direct Investment: Analysis and Determinants.” Regional Studies 26 (6): 535–544. doi:10.1080/00343409212331347181

- House of Commons. 2022. The Semiconductor Industry in the UK. https://committees.parliament.uk/publications/31752/documents/178214/default/

- Huggins, R., and H. Izushi. 2007. Competing for Knowledge: Creating, Connecting, and Growing. London: Routledge.

- Huggins, R., A. Johnston, M. Munday, and C. Xu. 2023. “Competition, Open Innovation and Growth Challenges in the Semiconductor Industry: The Case of Europe's Clusters.” Science and Public Policy 50 (3): 531–547. doi:10.1093/scipol/scad005.

- Huggins, R., and P. Thompson. 2023. “Human Agency, Network Dynamics and Regional Development: The Behavioural Principles of new Path Creation.” Regional Studies 57 (8): 1469–1481. doi:10.1080/00343404.2022.2060958.

- Johnston, A., and R. Huggins. 2022. Computer Chips: While US and EU Invest to Challenge Asia, the UK Industry is in Mortal Danger. https://theconversation.com/computer-chips-while-us-and-eu-invest-to-challenge-asia-the-uk-industry-is-in-mortal-danger-188604

- Johnston, A., and R. Huggins. 2023. “Euro Commentary - Europe’s Semiconductor Industry at a Crossroads: Industrial Policy and Regional Clusters.” European Urban and Regional Studies 30 (3): 207–213. doi:10.1177/09697764231165199.

- Kapitsinis, N. 2017. “Firm Relocation in Times of Economic Crisis: Evidence from Greek Small and Medium Enterprises’ Movement to Bulgaria, 2007-2014.” European Planning Studies 25 (4): 703–725. doi:10.1080/09654313.2017.1288703

- Kapitsinis, N., M. Munday, and A. Roberts. 2019. Medium-Sized Businesses and Welsh Business Structure. Economic Intelligence Wales Report. https://orca.cardiff.ac.uk/id/eprint/130021/1/EIW%20Quarterly%20Bespoke%20report%20English.pdf

- Kapitsinis, N., M. Munday, and A. Roberts. 2021. “Exploring a low SME Equity Equilibrium in Wales.” European Planning Studies 29 (10): 1777–1797. doi:10.1080/09654313.2021.1882945

- Kowalski, P., D. Rabaioli, and S. Vallejo. 2017. International Technology Transfer Measures in an Interconnected World: Lessons and Policy Implications. OECD Trade Policy Papers, No. 206, OECD, Paris.

- Lall, S. 1995. “Employment and Foreign Investment: Policy Options for Developing Countries.” International Labor Review 134: 521. doi:10.1787/1816687

- Leydesdorff, L. 2000. “The Triple Helix: An Evolutionary Model of Innovations.” Research Policy 29 (2): 243–255. doi:10.1016/S0048-7333(99)00063-3

- McAleese, D., and M. Counahan. 1979. “Stickers or Snatchers? Employment in Multinational Corporations During the Recession.” Oxford Bulletin of Economics and Statistics 41: 345–358. doi:10.1111/j.1468-0084.1979.mp41004007.x

- McNabb, R., and M. Munday. 2017. “The Stability of the Foreign Manufacturing Sector: Evidence and Analysis for Wales 1966-2003.” European Urban and Regional Studies 24 (1): 50–68. doi:10.1177/0969776415593615

- Miller, C. 2022. Chip War: The Fight for the World’s Most Critical Technology. New York: Scribner.

- Munday, M., M. Peel, and K. Taylor. 2005. “The Performance of the Foreign-Owned Sector of UK Manufacturing: Some Evidence and Implications for UK Inward Investment Policy.” Fiscal Studies 24 (4): 501–521. doi:10.1111/j.1475-5890.2003.tb00093.x

- Owen, G. 2022. Semiconductors in the UK. Searching for a Strategy. London: Policy Exchange.

- Perri, A., and U. Andersson. 2014. “Knowledge Outflows from Foreign Subsidiaries and the Tension Between Knowledge Creation and Knowledge Protection: Evidence from the Semiconductor Industry.” International Business Review 23 (1): 63–75. doi:10.1016/j.ibusrev.2013.08.007

- Perri, A., and E. Peruffo. 2016. “Knowledge Spillovers from FDI: A Critical Review from the International Business Perspective.” International Journal of Management Reviews 18 (1): 3–27. doi:10.1111/ijmr.12054

- Phelps, N. 2016. “Branch Plant Economy.” In International Encyclopaedia of Geography: People, the Earth, Environment and Technology, edited by D. Richardson, N. Castree, M. Goodchild, A. Koyobashi, W. Liu, R. Marston, and K. Falconer Al-Hindi, 1–17. Chichester: Wiley-Blackwell.

- Ranga, M., and H. Etzkowitz. 2013. “Triple Helix Systems: An Analytical Framework for Innovation Policy and Practice in the Knowledge Society.” Industry and Higher Education 27 (4): 237–262. doi:10.5367/ihe.2013.0165

- Rodríguez-Pose, A., and R. Crescenzi. 2008. “Research and Development, Spillovers, Innovation Systems, and the Genesis of Regional Growth in Europe.” Regional Studies 42 (1): 51–67. doi:10.1080/00343400701654186

- Ryan, P., and M. Giblin. 2012. “High-tech Clusters, Innovation Capabilities and Technological Entrepreneurship: Evidence from Ireland.” World Economy 35: 1322–1339. doi:10.1111/j.1467-9701.2012.01486.x

- Ryan, P., M. Giblin, G. Buciuni, and D. Kogler. 2021. “The Role of MNEs in the Genesis and Growth of a Resilient Entrepreneurial Ecosystem.” Entrepreneurship & Regional Development 33: 36–53. doi:10.1080/08985626.2020.1734260

- Thompson, P., and W. Zang. 2022. “A Matter of Life and Death? Knowledge Intensity of FDI Activities and Domestic Enterprise.” Papers in Regional Science 101 (5): 1157–1179. doi:10.1111/pirs.12699

- Tödtling, F., and M. Trippl. 2005. “One Size Fits all? Towards a Differentiated Regional Innovation Policy Approach.” Research Policy 34: 1203–1219. doi:10.1016/j.respol.2005.01.018

- US Department of State. 2022. The CHIPS and Science Act. For Summary see https://www.whitehouse.gov/briefing-room/statements-releases/2022/08/09/fact-sheet-chips-and-science-act-will-lower-costs-create-jobs-strengthen-supply-chains-and-counter-china/

- Wei, Y. 2015. “Network Linkages and Local Embeddedness of Foreign Ventures in China: The Case of Suzhou Municipality.” Regional Studies 49: 287–299. doi:10.1080/00343404.2013.770139

- Welsh Government. 2009. “Foreign Direct Investment: Review of Determinants and Impact.” Report for Welsh Assembly Government by Welsh Economy Research Unit, Cardiff Business School.