?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study empirically analyzes how earnings management and board independence mediate the link between family ownership and environmental disclosures, using a sample of non-financial firms listed on the Indonesia Stock Exchange (IDX) for the fiscal years 2014 to 2017. Unsurprisingly, the main finding from multiple regression analyses suggests a positive association between family-controlled entities and environmental disclosure, but this relationship is statistically insignificant. Yet, intriguingly, the study finds that the association between family business entities and environmental disclosures is indirect through producing high-quality financial reports and appointing independent members to the board of directors. Our study contributes to Indonesian literature on the role of earnings management and independent boards in mediating the relationship between family firms and corporate environmental performance. Specifically, our results align with the agency theory suggesting that family owners and managers act in the best interests of the entire organization and its stakeholders, thus reporting higher-quality earnings. This study also contributes to the literature on corporate governance, highlighting the critical role of an independent board of directors as a supervisory mechanism. The study has practical implications that managers of Indonesian corporations should consider increasing the proportion of independent members on the board of directors to support the implementation of the company’s environmental strategy effectively. Likewise, the study offers insight to the policymakers in enhancing the oversight role of corporate boards in limiting earnings management practices and encouraging the communication of corporate environmental information. Finally, our study contributes to the global literature, which seeks to find positive implications for family business environmental performance.

1. Introduction

Many studies on environmental performance have been conducted using different predictors and samples of countries (Baboukardos, Citation2018; Qian et al., Citation2018; Welbeck et al., Citation2017), with some studies considering how environmental disclosures may showcase this performance (Delgado-Márquez et al., Citation2017; Lyon & Montgomery, Citation2015). The problem with this research is that inadequate or no work has been conducted on this aspect in the geographic area of Indonesia. Indonesia, a nation of around 270 million people, has an issue with excessive carbon emissions. Corporations in Indonesia are under intense pressure, from domestic and global communities, to cut carbon emissions (Rokhmawati, Citation2020). Indonesian regulators have established mechanisms to improve companies’ environmental performance to respond to internal pressure by introducing the Performance Rating Program in Environmental Management (PROPER) in 1995. The company’s environmental performance was assessed based on its air and water pollution control and waste management compliance. PROPER put pressures the industry to enhance ecological management performance through the community and the market. The company’s environmental performance level is ranked using five colors ranging from best to worst, with PROPER gold and green colors indicating excellent grades. As a corporation reaches gold or green levels, its sale value increases. However, a business that receives two straight black hues could face legal action or have its license suspended.

The further problem is that little work has been conducted on the link between family ownership and environmental performance and how earnings management and independent board of directors (commissioners)Footnote1 mediate these relationships. Claessens et al. (Citation2006) state that 73% of Indonesian business entities are family-owned, generating millions of jobs and thus playing a pivotal role in developing Indonesia’s economy. Claessens et al. (Citation2000) and Fisman (Citation2001) also note that of all East Asia, Indonesia has the highest ownership of family businesses with many entities politically connected in the knowledge that political connections add value to Indonesian firms. Many previous studies report that family-controlled firms show better environmental quality (e.g., Berrone et al., Citation2010; Brune et al., Citation2019; Zellweger et al., Citation2011).

Earnings management occurs due to the flexibility of generally accepted accounting principles (GAAP); thus, managers can have some discretions in reporting earnings figures (Prior et al., Citation2008). To put it another way, corporate managers will employ this opportunistic behavior to take intentional actions within the bounds of GAAP to attain the desired reported earnings (Davidson et al., Citation1987). This study assumes that accounting method selections and discretionary accruals are the best ways to represent opportunistic earnings management (McNichols & Wilson, Citation1988). Recently, many articles have been published on the relationship between family businesses and earnings management, with some mixed evidence. Findings reported in numerous studies (e.g., Ghaleb et al., Citation2020; Salehi et al., Citation2019; Setia-Atmaja et al., Citation2011) indicate that family-owned firms are associated with a lower level of earnings management. These findings imply that family firms are less likely to act opportunistically and, as a result, have higher earnings quality. On the other hand, a study by Ali et al. (Citation2007) reveals that family businesses are incentivized to engage in earnings management for long-term economic performance and tax purposes. Likewise, Prencipe and Bar-Yosef (Citation2011) document that managers in family firms practice earnings management upward to avoid debt covenant and leverage-related reasons. Furthermore, some researchers (e.g., Bozzolan et al., Citation2015; Gras-Gil et al., Citation2016; Palacios-Manzano et al., Citation2021) analyze the relationship between corporate earnings management practices and commitment to environmental performance. The results of their study indicate that socially committed firms practice fewer earnings management.

There are two views on the effectiveness of an independent board of directors in family firms. The supporters of board independence suggest that independent board members may effectively mitigate agency conflicts in family businesses (Anderson & Reeb, Citation2003) and, consequently, improve family business performance (Arosa et al., Citation2010; Bansal & Thenmozhi, Citation2021). The opponents of board independence argue that independent board members in family management could be ineffective (Chen & Jaggi, Citation2001; Martin-Reyna & Duran-Encalada, Citation2012) because they are appointed via friendship, personal relationships, or family ties (Songini et al., Citation2013). Regarding the relationship between board independence and environmental disclosure, many empirical studies document that more independent members on the board disclose more information for higher transparency and accountability (Agyei-Mensah, Citation2016). Fernandes et al. (Citation2018), Du et al. (Citation2020), and Shwairef et al. (Citation2021), for example, show that board independence is positively associated with environmental concerns. Additionally, previous studies (e.g., Dimitropoulos & Asteriou, Citation2010; Garcia-Meca & Sanchez-Ballesta, Citation2009; Lee, Citation2013; Prencipe & Bar-Yosef, Citation2011; Rajpal, Citation2012) investigate the relationship between board independence and earnings management behavior. Those studies clearly confirm that independent boards reduce earnings management practices.

In summary, the academic literature has indicated a direct relationship between (i) family ownership and environmental disclosure; (ii) family ownership and earnings management; (iii) earnings management and corporate environmental disclosure; (iv) family firms and independent board of commissioners; (v) independent board of commissioners and environmental disclosure; and (vi) board independence and level of earnings management. As a result, the overall relationship between family ownership and corporate environmental disclosure may be indirect through the presence of independent boards and the practices of earnings management. This study explores the mediating roles of board independence and earnings management on the link between family firms and corporate environmental disclosure, thus aiming to answer the research question of whether: The relationship between family business entities and environmental disclosure is indirect through the existence of an independent board of commissioners and the practices of earnings management.

The results from the regression analysis of 82 non-financial firms listed on the IDX for three fiscal years show that family-owned firms are positively associated with environmental disclosure, but it is statistically insignificant. However, our study finds that family ownership has a negative impact on earnings management behavior, implying that family businesses are less likely to engage in earnings management. Moreover, earnings management is negatively linked to corporate environmental disclosure. We also find that family owners prefer hiring independent boards of commissioners in their businesses. Additionally, this study reveals that independent commissioners are associated with better environmental performance and lower earnings management. In conclusion, the results of this study indicate the relationship between family ownership and corporate environmental performance is indirect through appointing independent members to the board and producing high-quality financial reports.

This study is essential because it investigates the relationship between family ownership and environmental performance and how it is affected by board composition and earnings management, which has not been examined. Furthermore, the Indonesian context of the research differs from the commonly studied using North American and Western European samples. Therefore, it can add further insights to the scholarly debate on how the practices of earnings management and board independence mediate the link between family ownership and environmental disclosures. The study is also critical because while Indonesia’s corporations have attempted to legitimize their activities through voluntary environmental disclosure, it is unclear how this objective is achieved (Cho & Patten, Citation2007). Additionally, our research contributes to the global literature that explores strategies for enhancing the environmental performance of family businesses.

The study is structured as follows. Section 2 presents a literature review accompanied by hypotheses development. The following section (Section 3) discusses the design of the research. Results and discussions are reported in Section 4. Finally, the conclusions, contributions, and limitations are presented in Section 6.

2. Literature review and hypotheses

This study proposes that Indonesian family businesses are associated with independent boards of commissioners and earnings management practices, each closely related to engagement with environmental disclosures. The impact of family ownership on earnings management behavior is indirect through the existence of board independence. Additionally, the effect of family ownership on environmental disclosure is indirect through the presence of board independence and earnings management practices. Four control variables (auditor type, financial leverage, return on assets, and firm’s size) are used in the regression analysis to control for cross-sectional influences (see Figure ).

Figure 1. Relationship between family ownership and environmental disclosure.

The study uses precepts of agency theory to argue that family businesses can either increase or moderate agency problems. Proponents of the exacerbated argument suggest that family-controlled entities experience more significant agency problems than nonfamily-owned entities. Family management is more prone to expropriate minority shareholders’ wealth for personal benefit. According to Claessens et al. (Citation2006), roughly 73% of Indonesian listed companies are owned by family members. Similarly, Fan and Wong (Citation2002) argue that family members or their business groups control most Indonesian companies, with many of the critical positions also holding a significant proportion of the firm’s equity. This phenomenon gives rise to a new agency conflict between controlling and minority shareholders, as family owners may utilize their controlled power to expropriate the earnings of minority shareholders (Salvato & Moores, Citation2010). However, Joni et al. (Citation2020) and Anderson and Reeb (Citation2003) point out that the agency issue in Indonesia differs significantly from most developing countries because family wealth is closely associated with business welfare. Thus, concentrated ownership in family firms reduces traditional cases of managerial expropriation. Following Anderson and Reeb (Citation2003) and Joni et al. (Citation2020), this study assumes that agency problems are less prevalent in Indonesian family firms.

2.1. Family ownership and earnings management

The optimistic view of family businesses asserts that families are better monitors of managers than other types of large shareholders; thus, family-controlled firms may have fewer agency problems than their counterparts (Anderson & Reeb, Citation2003; Bubolz, Citation2001; Davis et al., Citation1997). Demsetz and Lehn (Citation1985) argue that family businesses can mitigate the issues of managerial expropriation by placing relatives in senior positions to monitor and control the business. Relatives are more familiar with business activities because they are founding members or managing the business for a considerable time (DeAngelo & DeAngelo, Citation2000). Moreover, Andres (Citation2008) suggests that families invest their capital into the business; thus, they may have strong incentives to supervise management. This argument implies that family-controlled businesses are less likely to behave opportunistically and manage higher earnings. Many studies (Ferramosca & Ghio, Citation2018; Ghaleb et al., Citation2020; Salehi et al., Citation2019; Wang, Citation2006) document that managers of family firms are less aggressive in managing earnings due to their ability to monitor and have better knowledge of the firm’s business activities. With these arguments, the first hypothesis of this study is as follows:

H1

Family business entities manage fewer earnings management.

2.2. Family ownership and board independence

Peasnell et al. (Citation2000) demonstrated that independent board members improve the value of companies. However, the benefits of independent boards for family businesses are still being debated. Arcot and Bruno (Citation2018) argue that the governance of family firms is open to question. Songini et al. (Citation2013) claim that most independent board members in family businesses are chosen through family ties, friendship, and business or personal relationships. They also closely relate to controlling shareholders (Corbetta & Salvato, Citation2004). In addition, independent boards of family firms formally approve what the management has already decided, and they meet irregularly to solve problems (Sarbah et al., Citation2016). Thus, appointing independent members on the board in family management could be ineffective (Chen & Jaggi, Citation2001; Martin-Reyna & Duran-Encalada, Citation2012).

Nevertheless, some commentators argue that boards of family businesses are independent, transparent, and strategic, and reduce the risk of appropriation of private benefits, consequently decreasing agency costs (Bammens et al., Citation2011; Dyer, Citation1986; Sarbah et al., Citation2016). Thorning-Lund (Citation2012) also suggests that an independent board of commissioners may play a critical role in business development by delivering fresh perspectives, a strategic overview, and valuable networks for the family businesses. Therefore, independent commissioners of family firms effectively mitigate agency conflicts in family firms (Anderson & Reeb, Citation2003). Several studies (e.g., Arosa et al., Citation2010; Bansal & Thenmozhi, Citation2021) find that an independent board of commissioners improves family business performance. Based on these arguments, our second hypothesis is:

H2

Family business entities are more likely to appoint independent boards of commissioners.

2.3. Board independence and earnings management

Independent boards of directors are supposed to constrain the practices of earnings management. An ample body of research provides evidence that independent boards of directors reduce the practice of earnings management, particularly the reduction of financial statement fraud (Beasley, Citation1996). Klein (Citation2002), for example, shows that board independence mitigates earnings management behaviors. The existence of an independent board may also improve earnings informativeness, according to research by Moreover, Firth et al. (Citation2007) and Garcia-Meca and Sanchez-Ballesta (Citation2009). These findings are supported by Peasnell et al. (Citation2000) and Dechow et al. (Citation1996). They reveal that the more significant proportion of independent directors, the less likely the firm will violate the role. Similar conclusions are also documented in countries with different institutional environments, such as Greece (Dimitropoulos & Asteriou, Citation2010), India (Rajpal, Citation2012), and Taiwan (Lee, Citation2013). Additionally, in a study of family businesses, Prencipe and Bar-Yosef (Citation2011) argue that a higher proportion of independent members on a board will enable them to monitor and reduce the likelihood of earnings management by the family owners. Also, Chi et al. (Citation2015) report that independent directors negatively moderate the association between family-owned business and earnings management in Taiwan’s public-listed firms. As a result, this study tests the following hypothesis:

H3

The independent board of commissioners in family business entities is more likely to reduce earnings management.

2.4. Board independence and environmental disclosure

Boards with more independent members appear to focus on compliance with laws and regulations (Zahra & Stanton, Citation1988), ethical issues (Ibrahim & Angelidis, Citation1995), transparency, and social and environmental concerns (Kathy-Rao et al., Citation2012; Liu & Zang, Citation2017; Shwairef et al., Citation2021). Using a sample of 152 Brazilian firms, Fernandes et al. (Citation2018) point out that independent boards of directors have a significant positive relation to the level of environmental disclosure. Similarly, a high proportion of independent directors on board members is associated with greater ecological exposure in China (Du et al., Citation2020), Nigeria (Ofoegbu et al., Citation2018), and Iran (Alipour et al., Citation2019). These arguments lead us to state the prediction as follows:

H4

The independent board of commissioners is positively associated with a higher quality of environmental disclosure.

2.5. Earnings management and environmental disclosure

Some previous studies (e.g., Bozzolan et al., Citation2015; Choi et al., Citation2013; Gras-Gil et al., Citation2016; Palacios-Manzano et al., Citation2021) have addressed the relationship between corporate earnings management practices and commitment to corporate social responsibility. There are two perspectives regarding the relationship between earnings management and corporate social responsibility. Earnings management may be positively associated with environmental disclosure. The proponents of this view argue that corporate executives may strategically use corporate ecological information to disguise their opportunistic behavior (Choi et al., Citation2013; Prior et al., Citation2008). Prior et al. (Citation2008) affirm that entities with a high level of earnings management will be very proactive in boosting their public exposure via engaging in corporate environment activities. Likewise, Choi et al. (Citation2013) report that corporate managers who act in pursuit of personal benefits by altering earnings information can entrench themselves by conducting companies’ environmental activities. More specifically, in a study of the relationship between environmental disclosure and earnings management, Patten and Trompeter (Citation2003) find that the environmental disclosure variable is significantly and positively related to earnings management measures.

The second perspective assumes that earnings management and corporate disclosure are negatively related. The study of Chih et al. (Citation2008) suggests that socially responsible firms are less likely to manage reported earnings since they are more prone to act responsibly in presenting their financial statements. Similarly, Kim et al. (Citation2012) point out that firms spend their money and other resources on designing and implementing corporate social responsibility (CSR) programs to address the ethical interests of stakeholders. Those firms also deliver more transparent and reliable financial information to investors and are less likely to manage reported earnings figures. Empirical evidence from various industry sectors and around the globe (Bozzolan et al., Citation2015; Gras-Gil et al., Citation2016; Hong & Andersen, Citation2011; Kim et al., Citation2012) generally concludes that the more commitment of a firm to CSR the more likely they are to drive managers to produce high-quality financial reports. In addition, a study by Litt et al. (Citation2014) that specifically investigates the association between environmental disclosures and earnings management practices finds that firms with environmental initiatives exhibit lower earnings management. The authors reveal that earnings management practices negatively affect pollution prevention and climate protection. This argument leads to the following hypothesis:

H5

The extent of environmental disclosure is negatively related to the level of earnings management.

2.6. Family ownership and environmental disclosure

Chi et al. (Citation2015) point out that family management takes advantage of minority shareholders’ earnings by exploiting their highly concentrated ownership. However, the proponents of family firms argue that concentrated ownership lessens the typical issues of managerial expropriation in listed family firms due to their wealth is closely connected with business welfare (Anderson & Reeb, Citation2003). Family businesses are more inclined to put their relatives in key positions since they are more familiar with the company’s operations (Faccio et al., Citation2001) and possibly monitoring and controlling the business (Demsetz & Lehn, Citation1985). Additionally, families have particular concerns on the company’s survival since they have put a significant portion of their private resources into the firms (Prencipe & Bar-Yosef, Citation2011).

A number of studies document that family-controlled firms prioritize not only economic but also non-economic objectives (e.g., Andres, Citation2008) and argue that the primary goal of the family businesses is to preserve the family’s socio-emotional wealth (Berrone et al., Citation2012; Brune et al., Citation2019). For instance, Zellweger et al. (Citation2011) Iyer and Lulseged (Citation2013) all provide evidence that family business owners are more focused on ensuring a business’s survival and enhancing its efforts to practice corporate social responsibility. Similar to those studies, Berrone et al. (Citation2010) and Garcia-Sanchez et al. (Citation2014) report that family owners seek to demonstrate outstanding environmental quality to uphold the company’s reputation. Thus, the study tests the following hypothesis:

H6

Family business entities are positively associated with a higher quality of environmental disclosure.

2.7. Mediating effect of board independence on earnings management

Our H2 states that family ownership positively affects the independent board of commissioners. H3 suggests that independent boards of commissioners are more likely to reduce earnings management; thus, the relationship between family ownership and earnings management may be indirect through the presence of board independence. Therefore, the following hypothesis is proposed:

H7

The relationship between family business entities and earnings management is indirect through the presence of independent boards of commissioners.

2.8. Mediating effect of board independence and earnings management on environmental disclosure

The hypothesis H6 proposes a direct relationship between family ownerships and environmental disclosure. However, the association between family firms and corporate environmental disclosure possibly indirect. Our H2 suggests that family ownership relates to board independence; an independent board relates to environmental disclosure (H4). H1 states that family ownership is associated with earnings management, which in turn, earnings management relates to corporate environmental disclosure (H5). H3 suggests that board independence relates to the level of earnings management. These relationships indicate that the overall relationship between family ownership and corporate environmental disclosure may be indirect through (1) the presence of independent boards of commissioners and (2) the level of earnings management. Accordingly, the following hypothesis is proposed:

H8

The relationship between family business ownership and environmental disclosure is indirect through the presence of an independent board of commissioners and the level of earnings management.

3. Research method

3.1. Sample

The study’s sample includes the firms listed on the IDX that consistently joined the PROPER for 2014–2017. We determine our sample by looking at the public firms joining the PROPER in 2014. The baseline year of 2014 is selected because relatively few publicly listed firms joined this program before this financial year. Entities from the financial sector were eliminated because they have different regulatory regulations that could impact discretionary accruals (the proxy for earnings management, our moderating variable). In 2014, 92 non-financial firms joined PROPER. However, we cannot collect 10 annual reports from 2014 through 2017. Thus, our final useable sample is 82 firms or 328 observations (see Table ).

Table 1. The study’s sample

As shown in Table , the Basic industry and chemicals represent the most significant sample, with 104 observations (31.71%). It is followed by the Consumer goods industry 80 observations (24.39%). The smallest group is Property, real estate, and building construction entities and firms in the Infrastructure, utilities, and transportation classification (four observations, respectively).

3.2. Dependent variable

The dependent variable represents the level of environmental disclosure of the sample firms for 2014–2017 that the Indonesia Ministry of Environment ranks via the PROPER. The level of structuring a firm’s environmental performance is graded into five, from the worst to the best color categories (see Table ).

Table 2. Proper ranking criteria

In this study, the level of environmental disclosure is scored 1 to 5 for firms classified as black, red, blue, green, and gold, respectively.

3.3. Experimental variables

3.3.1. Independent variable

Family ownership datasets are primarily obtained from an article entitled “150 Richest Indonesian”, published in August 2012 by the Globe Asia Business Magazine (Globe Asia, Citation2012). Following Qosasi et al. (Citation2022), we updated this information in an article entitled “Family businesses maintaining relevance in the modern era,” published in the July 2019 edition of the Globe Asia Business Magazine (GlobeAsia, Citation2019). Furthermore, we traced our 82 sample firms to the websites of each group of companies, as in the article “family businesses maintaining relevance in the modern era”, to determine whether a company belongs to a family member.

3.3.2. Mediating variables

Board independence is represented by the ratio of independent boards of commissioners out of the total number of board members. We use a standard methodology by employing unexpected discretionary accruals as a proxy for earnings management. Similar to the extant literature on earnings management, our study focuses on the absolute value rather than the actual sign of discretionary accruals as a proxy for earnings management (Francis et al., Citation2016; Walker, Citation2004). Before predicting discretionary accruals, total accruals (TAcc) are calculated as:

Where:

TAccit is total accruals for firm i in year t. ∆CAssit is the change in current assets for firm i from year t-1 to t. ∆Cashit is the change in cash balance for firm i from year t-1 to t; ∆CLiait is the change in current liabilities for firm i from year t-1 to t; ∆LTdit is the change in long-term debt included in current liabilities for firm i from year t-1 to t; ∆ITxpit is the change in income tax payable for firm i from year t-1 to t; and DAit is depreciation & amortization expense for firm i in year t.

TAcc is then decomposed into normal accruals (NAcc), and discretionary accruals (DAcc) using the cross-sectional modified Jones (Citation1991) model defined formally as:

Where:

TAcc ik,t is total accruals for firm i in industry k in year t; TAssik,t-1 is total assets for firm i in industry k at the end of year t-1; ∆Revik,t is the change in net sales for firm i in industry k between years t-1 and t; ∆Recik,t is the change in accounts receivables for firm i in industry k between years t-1 and t; PPEik,t is gross property, plant and equipment for firm i in industry k in year t; αi, βi, γi is industry-specific estimated coefficients; εi is the error term.

NAcc is defined as the fitted values from EquationEquation 2(2)

(2) , while DAcc is the residual (TAcc- NAcc).

3.3.3. Control variables

We have selected four control variables based on a review of past studies. We include financial leverage (Lev) in the model to control entity risk impacts. Based on agency theory, entities with greater leverage levels have greater disclosure. Martinez-Ferrero et al. (Citation2020) and Ramon-Llorens et al. (Citation2020) document a positive association between financial leverage and corporate social responsibility disclosure. We also include firm performance (ROA) in the model, as profitable entities are more likely to increase disclosures to differentiate themselves from their counterparts (Clarkson et al., Citation2011). However, other studies fail to find a significant link between these two variables (Bammer & Pavelin, Citation2008; Zeng et al., Citation2012). Big4 audit firms are employed as another control variable. It is widely claimed that the Big4 auditors deliver higher audit quality than non-Big4 auditors. Big4 auditors may influence their clients to disclose more information to reduce the likelihood of possible litigation from omitting material information (Rover et al., Citation2016). Finally, this study adds firm’s size as another control variable. According to Hackston and Milne (Citation1996) the larger size of firms, the more activities they engage in and the greater the impact they have on the environment. Large organizations with a wide range of business activities have a better chance of putting a corporate social responsibility agenda into action (Mokhtar et al., Citation2016).

3.4. Empirical model equations

This study deploys the ordinary least squares and multiple regression to test the hypotheses and is defined as follows:

CED = indicator variable with the firm i scored one (1) if its environmental performance in fiscal year t is ranked black; two (2) for red; three (3) for blue; four (4) for green; and five (5) for gold; FamOwn = indicator variable scored one (1) if firm i is family-owned; otherwise scored zero (0); BOCInd = ratio of independent commissioners of firm i for year t to the total number of board members of firm i for year t; AbsDAC = non-directional value or absolute value of discretionary accruals of firm i for year t measured by Modified Jones (Citation1991) model; Big4 = indicator variable with the firm i scored one (1) if its auditor in fiscal year t is a Big4 audit firm; otherwise scored zero (0); Lev = ratio of total debt of firm i for year t to total assets of firm i for year t; ROA = ratio of net income of firm i for year t to total assets of firm i for year t. Size = the natural logarithm of total assets of firm i for year t. Year Fixed Effect, Industry Fixed Effect = the fixed effects for different years and industries.

4. Findings and discussions

4.1. Descriptive statistics

Descriptive statistics are presented in Tables . Table lists the study samples based on eight industry sectors, ownership structure, and corporate environmental disclosure rank.

Table 3. Number and %tage of family and non-family firms by industry sector and CED level

Table 4. Descriptive statistics (n = 328)

Table 5. Correlation matrix

Table presents the five levels of environmental disclosure (from the lowest to the highest): black, red, blue, green, and gold. Firms in the blue category represent the largest (240 observations or 73.17%) of the sample. The blue category is dominated by firms in the “Basic industry and chemicals” sector (81 observations or 33,75%). Companies in the gold level represent the lowest sample (11 observations or 3.35%). The gold ranking is achieved by companies in the industrial group of “Mining” and “Basic industry and chemicals”; both represent nine and two observations, respectively. Interestingly, according to Indonesian Law No. 32/2009 on environmental protection and management, three sectors are classified as polluted including firms in the “Mining” and “Basic industry and chemicals”. Moreover, Table reports that seven out of 11 observations rank as “gold” level environmental disclosure are family-controlled firms. Contradictory, “black” rank environmental disclosure is dominated by non-family firms (14 out of 15 observations). Critically, this evidence indicates that family-owned firms lead in disclosing environmental information.

Table reports the descriptive statistics for the study’s variables, with Panel A depicting the continuous variables and Panel B showing the dummy regression variables.

Table , Panel A shows that the ratio of independent commissioners has an average of 39.99% with a median of 33.33%. The Financial Services Authority Regulation No. 33/POJK.04/2014 states that the board of commissioners shall have at least two members, and 30% of them should be independent. The average discretionary accruals of the total assets are −0.0610, ranging from −0.7041 to 0.9036. The distribution of discretionary accruals indicates a wide range of variation. Nonetheless, the total number of companies with positive and negative discretionary accruals is relatively equal (169 and 159 companies, respectively). Panel A of Table reports that the median AbsDAC (0.0674) is significantly lower than its mean (1.332), indicating that the dataset is positively skewed. Thus, we transform the data of AbsDAC into the squared root. The sample firms’ average total debt to total assets ratio (Lev) is 46.37%, with a median of 47.50%. Table presents that the average return on assets (ROA) is 0.0634. The median (0.0378) is significantly lower than the mean figure (0.0634), indicating a small number of substantial profit firms in our sample. There are also wide ranges in the sample’s minimum and maximum figures of the ROA (ranging from −0.2094 to 0.7146). Such figures specify that the data on ROA is skewed to the left. Thus, this study transforms the data of ROA into the natural logarithm in an analysis of the variable. The average firm size as measured by total assets is 18,144,657 million Indonesian rupiah (IDR) with a median of IDR5.315.049 million. The median figure is significantly lower than the mean value indicates that only a few of the sample firms have very large capitalizations. The data also indicate that total assets are skewed, as there is a wide range in the minimum and maximum figures of total assets. Consistent with the approach used in other studies, this study transforms total assets into the natural logarithm when measuring size of firm.

Panel B of Table reports that an individual or family members own 38.27% of the sample firms. About 63.11% of the sample observations use the service of Big4 auditors. Ali and Aulia (Citation2015) reveal that Indonesia’s audit market share of the Big4 accounting firms has gradually decreased since 2010. This phenomenon may have arisen from second-tier global audit firms (e.g., Moore Stephens International, BDO International Limited, and BKR International) affiliated with domestic firms. Still, Big4 audit firms provide extensive audit services on the IDX with a 71.54% market share.

4.2. Correlations

Table presents a correlation matrix between the dependent, independent, mediating, and control variables.

In general, the correlation results support the study hypotheses. The correlation coefficients of the associations between (1) family ownership and earnings management (H1, r = −0.115, p = 0.05); (2) family ownership and board independence (H2, r = 0.155, p = 0.01); (3) board independence and earnings management (H3, r = −0.131, p = 0.005); board independence and corporate environmental disclosure (H4, r = 0.325, p = 0.001); and earnings management and corporate environmental disclosure (H5, r = −0.217, p = 0.01) are all significant and in the predicted direction. Thus, these results indicate the acceptance of all the direct and indirect relationships, as hypothesized, with corporate environmental disclosure.

As reported in Table , the magnitudes of the correlations between the independent and mediating variables are relatively small. As such, the multicollinearity problem does not occur in the regression models. Concerning correlations between independent, mediating, and control variables and among control variables themselves, the highest correlation is between Lev and ROA, with a coefficient of −0.402 (p < 0.01) and is below the critical limit of 0.80 (Cooper & Schindler, Citation2003). Hence, a multicollinearity problem does not appear to arise from using these variables.

4.3. Regression results

We conduct simple and multiple regressions to analyze this hypotheses relationship using SPSS 22. The results of regression for testing the hypotheses are tabulated in Table .

Table 6. Regression results

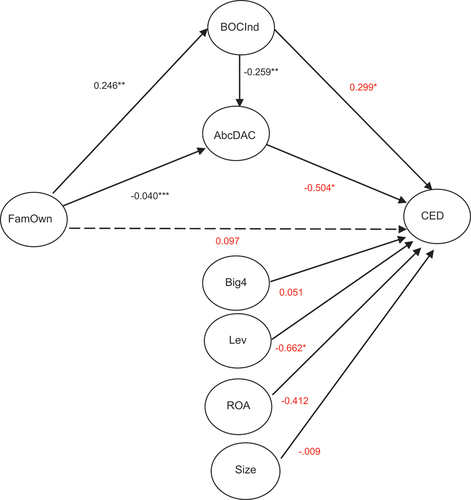

Panels A and B of Table report results from simple regressions based on equation models 1 and 2, respectively. Panel C presents the findings of all independent, mediating, and control variables used in the multiple regression based on equation model 3. Regression model estimates reported in Table , Panels A to C, are all statistically significant (F-statistic, p < 0.01) with the explanatory power of 8.4% (Panel A), 8.8% (Panel B), and 25.0% (Panel C). The lower explanatory power in Panels A and B is due to simple regression results (based on equation models 1 and 2) with only one and two predictors, respectively. The model’s explanatory power increased to 25.0% (which is fairly typical in social field research) when we included four control variables in the model (based on equation model 3). The fact that all variance inflation factor (VIF) values are less than 10 is evidence that multicollinearity is not a concern in the model estimations. The details of the hypothesis testing results are presented in Figure .

Figure 2. Regression results with path coefficients.

5. Discussions

The regression results reported in Table and Figure are all statistically significant and in the predicted direction. Therefore, they provide support for H1 to H5. For H1, family ownership has a negative and significant effect on the level of earnings management (β = −0.040, p < 0.10). This result suggests family firms are less likely to engage in earnings management practices. This result is consistent with prior studies (Ferramosca & Ghio, Citation2018; Ghaleb et al., Citation2020; Salehi et al., Citation2019; Wang, Citation2006), which document that family firms demonstrate better earnings quality than non-family firms. Our findings support agency theory, which posits that family managers’ interests align with that of corporations and other shareholders (Anderson & Reeb, Citation2003). Family owners and managers often act in the organization’s and its shareholders’ best interest (Davids et al., Citation1997). They commonly have a deep emotional attachment due to their satisfaction (Bubolz, Citation2001). Furthermore, Wang (Citation2006) notes that founding families have incentives to report higher-quality earnings to protect the family’s reputation and improve the long-term firm’s performance.

For H2, family business entities are more likely to appoint independent boards of commissioners (β = 0.246, p < 0.05). The positive and significant relationship between family ownership and board independence supports previous findings. Earlier studies suggest that independent boards increase a firm’s value (Peasnell et al., Citation2000), reduce agency issues (Anderson & Reeb, Citation2003), and improve the performance of family businesses (Arosa et al., Citation2010; Bansal & Thenmozhi, Citation2021). Yet, the findings of our study contradict the nation that independent boards in family businesses are ineffective. Independent members on the board of directors in family firms are selected through their ties to the family, friendship, or close business relationship with controlling shareholders (Corbetta & Salvato, Citation2004; Songini et al., Citation2013).

The coefficient on BOCInd is negatively associated with AbsDAC (β = −0.259, p < 0.05), indicating that an independent board of commissioners is more likely to limit earnings management. H3 is therefore supported. The results confirm much prior research showing that independent members of commissioners reduce the practices of earnings management, which improve the quality of reported earnings (e.g., Dimitropoulos & Asteriou, Citation2010; Firth et al., Citation2007; Garcia-Meca & Sanchez-Ballesta, Citation2009; Klein, Citation2002; Rajpal, Citation2012). Using a sample of Taiwan-listed companies, Chi et al. (Citation2015) additionally report that independent directors negatively influence the link between family-controlled firms and earnings management behavior.

Table , Panel C provides evidence that board independence is positively associated with environmental disclosure (β = 0.299, p < 0.01), supporting hypothesis H4. Again, this outcome is consistent with research done in the past using a sample of companies from Brazil, China, Nigeria, and Iran (Alipour et al., Citation2019; Du et al., Citation2020; Fernandes et al., Citation2018; Ofoegbu et al., Citation2018). They undoubtedly demonstrate the link between an independent board of commissioners and a higher level of environmental disclosure.

Finally, the regression result in Table , Panel C reveals that earnings management is negatively associated with environmental disclosure (β = −0.504, p < 0.01), supporting our hypothesis H5. Our findings support the idea that socially responsible firms are less likely to manage earnings figures because they are more prone to act appropriately and ethically when presenting their financial information (e.g., Bozzolan et al., Citation2015; Chih et al., Citation2008; Gras-Gil et al., Citation2016; Kim et al., Citation2012). In conclusion, based on these results, hypotheses H1 to H5 are supported. However, the regression results in Table , Panel C indicate that the association between family ownership and environmental disclosure is statistically insignificant (β = −0.097, p > 0.10); thus H6 is not supported. Certainly, this result suggests the presence of mediating effects.

Regarding the control variables, this study finds that financial leverage (Lev) presents a negative and significant sign (at p < 0.01). The significant negative association between a firm’s financial leverage and environmental performance (CED) is contrary to previous studies, for example, Martinez-Ferrero et al. (Citation2020) and Ramon-Llorens et al. (Citation2020). The control variables of a firm’s performance (ROA), big international audit firms (Big4), and firm’s size have no significant relationships with CED. The study fails to support that those three variables are associated with environmental disclosure.

According to H7, the relationship between family ownership and earnings management is indirect through the presence of board independence. From H8, the relationship between family ownership and corporate environmental disclosure is indirect through the existence of board independence and the level of earnings management. For testing the intervening influences of board independence and earnings management, it is necessary to ascertain the indirect impacts that can be calculated from the path coefficients in Figure as follows: family ownership—board independence—earnings management = 0.246 × −0.259= −0.064. This indirect effect of 0.064 is above the meaningful threshold of an absolute amount of 0.05 (Pedhazur, Citation1982). Accordingly, H7 is supported. A similar analysis is undertaken for hypothesis H8. Based on the coefficients presented in Figure , the indirect impacts are calculated and reported in Table .

Table 7. Indirect effects of board independence and earnings management

The results show that the indirect impact through board independence (BOCInd) is 0.074, and the indirect effect through earnings management (AbsDAC) is 0.052. These figures are considered meaningful because they are above the threshold of 0.05. Thus, H8 is supported.

5.1. Endogeneity tests

This study performs further robust analysis to check the potential effect of endogeneity. Abdallah et al. (Citation2015) argue that an important concern in corporate governance research is the endogeneity problem among the dependent and explanatory variables. Following Baatwah et al. (Citation2022) and Rezaee et al. (Citation2021), this study employs the Heckman two‐stage least squares (2SLS) approach to ensure that our results are not driven by endogeneity. Adopting 2SLS will address endogeneity issues that could arise from simultaneous-equation bias and correlated omitted variable bias (Larcker & Rusticus, Citation2010).

In the first stage, we run a probit model using a dichotomous variable of FamOwn, BOCInd, AbsDAC as dependent variables and regress on all the control variables and year and industry fixed effects as predictors. BOCInd is a dummy variable that takes a value of 1 if a firm has a BOCInd value greater than the median BOCInd value and 0 otherwise. AbsDAC is a dummy variable that takes a value of 1 if a firm has an AbsDAC value greater than the median AbsDAC value and 0 otherwise. Estimated parameters from the probit regression are used to obtain Inverse Mills Ratio (IMR) for each FamOwn, BOCInd, and AbsDAC. In the second stage, we extracted the IMR and added it to the main models as an independent variable along with other explanatory variables. The results of the second stage (see Table ), after controlling for endogeneity because of self-selection bias, are quantitatively similar to our original findings.

Table 8. Regression results (endogeneity)

6. Conclusions, contributions, and limitations

This study investigates the mediating role of board independence and earnings management in the relationship between family business entities and environmental disclosure. Specifically, the study focuses on whether “the effect of family business entities on environmental disclosure is indirect through the existence of an independent board of commissioners and the practices of earnings management.”

This study indicates that family business entities are positively associated with environmental disclosure, but it is statistically insignificant. However, our results reveal that family business entities negatively affect earnings management behavior. The results imply that family-controlled firms engage less in earnings management and, thus, report a higher quality of earnings. Our result also reveals a positive and significant association between family business entities and independent boards of commissioners, suggesting that family owners prefer a higher ratio of independent commissioners in their firms. This result implies that the family executives’ interests align with the organization’s goals and objectives. Family business owners and managers welcome independent members in the boardroom as they become an essential control mechanism.

The effectiveness of independent boards of commissioners in monitoring managerial activities has been examined in past studies. In line with many previous studies, this study reports evidence that independent boards of commissioners reduce earnings management practices. It means that independent commissioners provide effective monitoring of earnings management behaviors. Again, our results confirm many earlier studies’ findings that independent board members are positively associated with improved environmental performance. The results suggest that independent board members prefer to disclose more information for higher transparency and accountability. In other words, independent members on the board provide an effective mechanism for aligning the interests of stakeholders and showing a greater tendency for information transparency. Finally, our finding supports the claim that entities with strong environmental values are more prone to disclose their financial information adequately. Specifically, we find that the earnings management measure is negatively and significantly associated with environmental disclosure.

This study fails to find a significant relationship between family ownership and environmental disclosure. However, our results indicate that the association between family business entities and environmental disclosure is indirect through appointing independent members to the board and producing high-quality financial reports. The finding leads us to draw the following inferences. First, the existence of listed family business entities is advantageous, as it appears to enhance earnings quality leading to being responsible for and disclosing more environmental issues. Second, appointing independent members into the boardroom seems to provide transparent processes, good governance, and an empowering atmosphere in family businesses, resulting in better environmental performance. Third, our results indicate that independent commissioners effectively monitor earnings management practices in family business entities. This finding suggests that strengthening the board of commissioners by appointing more independent members is a positive step toward improving earnings quality and environmental performance. Generally, our results are consistent with the Indonesian family business survey conducted by PricewaterhouseCoopers in 2018. The survey report that family-controlled firms (1) prefer to hire professional expertise from outside the family and (2) are less likely to allow next-generation family members to work in the business and take up corporate governance roles.

This study offers the following contributions. First, it delivers in-depth research of family business entities in a different context from previous studies where most are based in developed markets. Second, given the limited number of family business studies about Indonesia, this study provides a real contribution to Indonesian literature. Specifically, the Indonesian capital market is characterized by bigger family businesses with a high ownership concentration in the hands of a few shareholders. Moreover, this study contributes to the global literature, which seeks ways to find positive implications for family business environmental performance.

The implications for family business theory and practice are rather than a direct association between family businesses and environmental performance. There appears to be a more nuanced indirect association through the appointment of independent members on the board and the production of high-quality financial reports. The literature benefits from this novel finding because it shows how potential stories may become apparent when thinking outside the box. Our results align with the agency theory and the literature on corporate governance that highlight the critical role of an independent board of directors as a supervisory mechanism. The findings of this study hold significant practical implications for managers of Indonesian corporations. It is recommended that they increase the proportion of independent members on the board of directors to effectively support the implementation of the company’s environmental strategy. Additionally, this study provides valuable insights for policymakers to strengthen the oversight role of corporate boards in curbing earnings management practices and promoting the dissemination of corporate environmental information.

Limitations of the study need to be acknowledged. First, our study is limited to the Indonesian case, constraining our results’ generalization. Therefore, future studies may consider the study of the link between family businesses and environmental disclosures in other jurisdictions. Second, our sample only includes publicly traded companies. Future research may investigate the earnings management and the environmental disclosure practice of family firms that are not publicly traded. Another avenue for future research is comparing data sets before and during the pandemic.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Agus Joko Pramono

Agus Joko Pramono (first author) is the Vice-Chairman of the Audit Board of the Republic of Indonesia. He has participated in numerous international workshops and courses and has contributed as a speaker in international forums, such as the United Nations meetings and the INTOSAI Congress. He is also a Vice-Chairman of the Independent Audit Advisory Committee of the United Nations, and a board member of INTOSAI Development Initiative. He holds a doctoral degree from Padjadjaran University, Indonesia.

Rusmin Rusmin

Rusmin Rusmin (co-author) is a faculty member at Universitas Teknologi Yogyakarta. Rusmin completed his auditing and financial accounting doctorate at Curtin University, Australia. He has published research papers in journals such as the Managerial Auditing Journal, the International Journal of Public Administration, the International Journal of Accounting and Information Management, the International Journal of Accounting, Auditing, and Performance Evaluation, the Asia Review of Accounting, and the Cogent Economics and Finance. His primary interests are auditing, corporate governance, earnings management, and environmental management.

Emita W. Astami

Emita Wahyu Astami (corresponding author) holds a Ph.D. in Accounting from Curtin University, Australia, and has been on the faculty at Universitas Teknologi Yogyakarta. She has conducted research in the areas of corporate governance, financial reporting, and financial and environmental disclosures. She has published research papers in journals such as the International Journal of Accounting, Asian Review of Accounting, International Journal of Accounting and Information Management, Australasian Accounting Business and Finance Journal, and Cogent Economics and Finance.

Alistair Brown

Alistair Brown (co-author) teaches and researches at the School of Accounting, Economics & Finance at Curtin University, Western Australia. His Web of Science Researcher ID is U-4009-2018, and his Scopus ID is 0000-0002-4529-9099.

Notes

1. Since Indonesia has a two-tiered structure, this study interchanges the terms “board of directors” and “board of commissioners”.

References

- Abdallah, W., Goergen, M., & O’Sullivan, N. (2015). Endogeneity: How failure to correct for it can cause wrong inferences and some remedies. British Journal of Management, 26(4), 791–23. https://doi.org/10.1111/1467-8551.12113

- Agyei-Mensah, B. K. (2016). Internal control information disclosure and corporate governance: Evidence from an emerging market. Corporate Governance, 16(1), 79–95. https://doi.org/10.1108/CG-10-2015-0136

- Ali, S., & Aulia, M. R. P. (2015). Audit firm size, auditor industry specialization and audit quality: An empirical study of Indonesian state-owned enterprises. Research Journal of Finance & Accounting, 6(22), 1–14.

- Alipour, M., Ghanbari, M., Jamshidinavid, B., & Taherabadi, A. (2019). Does board independence moderate the relationship between environmental disclosure quality and performance? Evidence from static and dynamic panel data corporate governance. The International Journal of Business in Society, 19(3), 580–610. https://doi.org/10.1108/CG-06-2018-0196

- Ali, C., Y, T., & Radhakrishnan, S. (2007). Corporate disclosures by family firms. Journal of Accounting and Economics, 44(1–2), 238–286. https://doi.org/10.1016/j.jacceco.2007.1001.1006

- Anderson, R. C., & Reeb, D. M. (2003). Founding family ownership and firm performance: Evidence from the S&P 500. The Journal of Finance, 61(3), 1301–1328. https://doi.org/10.1111/1540-6261.00567

- Andres, C. (2008). Large shareholders and firm performance-an empirical examination of founding-family ownership. Journal of Corporate Finance, 14(4), 431–445. https://doi.org/10.1016/j.jcorpfin.2008.05.003

- Arcot, S., & Bruno, V. (2018). Corporate governance and ownership: Evidence from a non-mandatory regulation. Journal of Law, Finance, and Accounting, 3(1), 59–84. https://doi.org/10.1561/108.00000023

- Arosa, B., Iturralde, T., & Maseda, A. (2010). Ownership structure and firm performance in non-listed firms: Evidence from Spain. Journal of Family Business Strategy, 1(2), 88–96. https://doi.org/10.1016/j.jfbs.2010.1003.1001

- Baatwah, S., Almoataz, E., Omer, W., & Aljaaidi, K. (2022). Does KAM disclosure make a difference in emerging markets? An investigation into audit fees and report lag. International Journal of Emerging Markets, ahead-of-print(ahead-of-print). https://do.org/10.1108.ijo.em.1110.2021.1606

- Baboukardos, D. (2018). The valuation relevance of environmental performance revisited: The moderating role of environmental provisions. The British Accounting Review, 50(1), 32–47. https://doi.org/10.1016/j.bar.2017.1009.1002

- Bammens, Y., Voordockers, W., & Van Girls, A. (2011). Boards of directors in family businesses: A literature review and research agenda. International Journal of Management, 13(2), 134–152. https://doi.org/10.1111/j.1468-2370.2010.00289.x

- Bammer, S., & Pavelin, S. (2008). Factors influencing the quality of corporate environmental disclosure business Strategy and the Environment. Business Strategy and the Environment, 17(2), 120–136. https://doi.org/10.1002/bse.1506

- Bansal, S., & Thenmozhi, M. (2021). Does CEO duality affect board independence? The moderating impact of founder ownership and family blockholding. IIMB Management Review, 33(3), 225–238. https://doi.org/10.1016/j.iimb.2021.09.004

- Beasley, M. S. (1996). An empirical analysis of the relation between the board of director composition and financial statement fraud. The Accounting Review, 71(4), 443–465. https://www.jstor.org/stable/248566

- Berrone, P., Cruz, C., & Gómez-Mejía, L. R. (2012). Socioemotional wealth in family firms: Theoretical dimensions, assessment approaches, and agenda for future research. Family Business Review, 25(3), 258–279. https://doi.org/10.1177/0894486511435355

- Berrone, P., Cruz, C., Gómez-Mejía, L. R., & Larraza-Kintana, M. (2010). Socioemotional wealth and corporate responses to institutional pressures: Do family-controlled firms pollute less? Administrative Science Quarterly, 55(1), 82–113. https://doi.org/10.2189/asqu.2010.2155.2181.2182

- Bozzolan, S., Fabrizi, M., Mallin, C. A., & Michelon, G. (2015). Corporate social responsibility and earnings quality: International evidence. The International Journal of Accounting, 50(4), 361–396. https://doi.org/10.1016/j.intacc.2015.10.003

- Brune, A., Thomsen, M., & Watrin, C. (2019). Family firms heterogeneity and tax avoidance: The role of the founder. Family Business Review, 32(3), 296–317. https://doi.org/10.1177/0894486519831467

- Bubolz, M. (2001). Family as a source, user and builder of social capital. Journal of Socio-Economics, 30(4), 129–131. https://doi.org/10.1016/S1053-5357(00)00091-3

- Chen, C. J., & Jaggi, B. (2001). Association between independent non-executive directors, family control and financial disclosures in Hong Kong. Journal of Accounting and Public Policy, 19(4), 285–310. https://doi.org/10.1016/S0278-4254(00)00015-6

- Chih, H. L., Shen, C. H., & Kang, F. C. (2008). Corporate social responsibility, investor protection, and earnings management: Some international evidence. Journal of Business Ethics, 79(1–2), 179–198. https://doi.org/10.1007/s10551-10007-19383-10557

- Chi, C. W., Hung, K., Cheng, H. W., & Lieu, P. T. (2015). Family firms and earnings management in Taiwan: Influence of corporate governance. International Review of Economics and Finance, 36, 88–98. https://doi.org/10.1016/j.iref.2014.11.009

- Choi, B. B., Lee, D., & Park, Y. (2013). Corporate social responsibility, corporate governance and earnings quality: Evidence from Korea. Corporate Governance an International Review, 21(5), 447–467. https://doi.org/10.1111/corg.12033

- Choi, B. B., Lee, D., & Praros, J. (2013). An analysis of Australian company carbon emission disclosures. Pacific Accounting Review, 25(1), 58–79. https://doi.org/10.1108/01140581311318968

- Cho, C. H., & Patten, D. M. (2007). The role of environmental disclosures as tools of legitimacy: A research note. Accounting, Organizations & Society, 32(7–8), 639–647. https://doi.org/10.1016/j.aos.2006.09.009

- Claessens, S., Djankov, S., & Lang, L. H. P. (2000). The separation of ownership and control in East Asian corporations. Journal of Financial Economics, 58(1–2), 81–112. https://doi.org/10.1016/S0304-1405X(1000)00067-00062

- Claessens, S., Fan, J. P. H., & Lang, L. H. P. (2006). The benefits and costs of group affiliation: Evidence from East Asia. Emerging Markets Review, 7(1), 1–26. https://doi.org/10.1016/j.ememar.2005.08.001

- Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2011). Does it really pay to be green? Determinants and consequences of proactive environmental strategies. Journal of Accounting and Public Policy, 30(2), 122–144. https://doi.org/10.1016/j.jaccpubpol.2010.09.013

- Cooper, D. R., & Schindler, P. S. (2003). Business research methods (8th ed.). McGraw-Hill.

- Corbetta, G., & Salvato, C. (2004). Self-serving or self-actualizing? Models of man and agency costs in different types of family firms: A commentary on “comparing the agency costs of family and non-family firms: Conceptual issues and exploratory evidence”. Entrepreneurship Theory and Practice, 28(4), 355–362. https://doi.org/10.1111/j.1540-6520.2004.00050.x

- Davidson, S., Schindler, J. S., & Weil, R. L. (1987). Accounting: The language of business. Thomas Horton and Daughter.

- Davids, J. H., Schoorman, F. D., & Donaldson, L. (1997). Toward a stewardship theory of management. Academy of Management Review, 22(1), 20–47. https://doi.org/10.2307/259223

- Davis, J. H., Schoorman, F. D., & Donaldson, L. (1997). Toward a stewardship theory of management. Academy of Management Review, 22(1), 20–47. https://doi.org/10.2307/259223

- DeAngelo, H., & DeAngelo, L. (2000). Controlling stockholders and the disciplinary role of corporate payout policy: A study of the times mirror company. Journal of Financial Economics, 56(2), 153–207. https://doi.org/10.1016/S0304-1405X(1000)00039-00038

- Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1996). Causes and consequences of earnings manipulation: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research, 13(1), 1–36. https://doi.org/10.1111/j.1911-3846.1996.tb00489.x

- Delgado-Márquez, B. L., Pedauga, L. E., & Cordón-Pozo, E. (2017). Industries regulation and firm environmental disclosure: A stakeholders perspective on the importance of legitimation and international activities. Organization & Environment, 30(2), 103–121. https://doi.org/10.1177/1086026615622028

- Demsetz, H., & Lehn, K. (1985). The structure of corporate ownership: Causes and consequences. Journal of Political Economy, 93(6), 1155–1177. https://doi.org/10.1086/261354

- Dimitropoulos, E., & Asteriou, D. (2010). The effect of board composition on the informativeness and quality of annual earnings: Empirical evidence from Greece. Research in International Business and Finance, 24(2), 190–205. https://doi.org/10.1016/j.ribaf.2009.12.001

- Du, X., Yin, J., Zhang, Y., & Du, Y. (2020). The globalised board of directors and corporate environmental performance: Evidence from China. China Journal of Accounting Studies, 8(4), 495–527. https://doi.org/10.1080/21697213.2021.1966175

- Dyer, W. G. J. (1986). Culture change in family firms: Anticipating and managing business and family transitions. Jossey-Bass.

- Faccio, M., Lang, L. H. P., & Young, L. (2001). Dividends and expropriation. American Economic Review, 91(1), 54–78. https://doi.org/10.1257/aer.1291.1251.1254

- Fan, J. P. H., & Wong, T. J. (2002). Corporate ownership structure and the informativeness of accounting earnings in East Asia. Journal of Accounting and Economics, 33(3), 401–425. https://doi.org/10.1016/S0165-4101(1002)00047-00042

- Fernandes, S. M., Bornia, A. C., & Nakamura, L. R. (2018). The influence of boards of directors on environmental disclosure. Management Decision, 57(9), 2358–2382. https://doi.org/10.1108/MD-2311-2017-1084

- Ferramosca, S., & Ghio, A. (2018). Earnings management in family firms. In Accounting choices in family firms. In contributions to management science (p. pp). Springer. https://doi.org/10.1007/978-3-319-73588-7

- Firth, M., Fung, P. M. Y., & Rui, O. M. (2007). Ownership, two-tier board structure, and the informativeness of earnings – evidence from China. Journal of Accounting and Public Policy, 26(4), 463–496. https://doi.org/10.1016/j.jaccpubpol.2007.1005.1004

- Fisman, R. (2001). Estimating the value of political connections. American Economic Association, 91(4), 1095–1102. https://doi.org/10.1257/aer.91.4.1095

- Francis, B., Hasan, I., & Li, L. (2016). A cross-countries study of legal-system strength and real earnings management. Journal of Accounting and Public Policy, 35(5), 417–512. https://doi.org/10.1016/j.jaccpubpol.2016.1006.1004

- Garcia-Meca, E., & Sanchez-Ballesta, J. P. (2009). Corporate governance and earnings management: A meta-analysis. Corporate Governance-An International Review, 17(5), 594–610. https://doi.org/10.1111/j.1467-8683.2009.00753.x

- Garcia-Sanchez, I.-M., Cuadrado-Ballesteros, B., & Sepulveda, C. (2014). Does media pressure moderate CSR disclosures by external directors? Management Decision, 52(6), 1014–1045. https://doi.org/10.1108/MD-09-2013-0446

- Ghaleb, B. A. A., Kamardin, H., & Tabash, M. I. (2020). Family ownership concentration and real earnings management: Empirical evidence from an emerging market. Cogent Economics & Finance, 8(1), 1–17. https://doi.org/10.1080/23322039.2020.1751488

- Globe Asia. (2012). 150 richest Indonesian (August ed.). BeritaSatu Media Holdings.

- GlobeAsia. (2019). Family businesses: Maintaining relevance in the modern era (July ed.). BeritaSatu Media Holdings, Jakarta.

- Gras-Gil, E., Manzano, M. P., & Fernandez, J. H. (2016). Investigating the relationship between corporate social responsibility and earnings management: Evidence from Spain. Business Research Quarterly, 19(4), 289–299. https://doi.org/10.1016/j.brq.2016.02.002

- Hackston, D., & Milne, M. J. (1996). Some determinants of social and environmental disclosures in New Zealand companies. Accounting Auditing & Accountability Journal, 9(1), 77–108. https://doi.org/10.1108/09513579610109987

- Hong, Y., & Andersen, M. L. (2011). The relationship between corporate social responsibility and earnings management: An exploratory study. Journal of Business Ethics, 104(4), 461–471. https://doi.org/10.1007/s10551-10011-10921-y

- Ibrahim, N., & Angelidis, J. (1995). The corporate social responsiveness orientation of board members: Are there differences between inside and outside directors? Journal of Business Ethics, 14(5), 405–410. https://doi.org/10.1007/BF00872102

- Iyer, V., & Lulseged, A. (2013). Does family status impact US firms’ sustainability reporting? Sustainability Accounting, Management and Policy Journal, 4(2), 163–189. https://doi.org/10.1108/SAMPJ-Nov-2011-0032

- Jones, J. J. (1991). Earnings management during import relief investigations. Journal of Accounting Research, 29(2), 193–228. https://doi.org/10.2307/2491047

- Joni, J., Ahmed, K., & Hamilton, J. (2020). Politically connected boards, family and business group affiliations, and cost of capital: Evidence from Indonesia. The British Accounting Review, 52(3), 100878. https://doi.org/10.1016/j.bar.2019.100878

- Kathy-Rao, K., Tilt, C. A., & Lester, L. H. (2012). Corporate governance and environmental reporting: An Australian study. Corporate Governance the International Journal of Business in Society, 12(2), 143–163. https://doi.org/10.1108/14720701211214052

- Kim, Y., Park, M. S., & Wier, B. (2012). Is earnings quality associated with corporate social responsibility? The Accounting Review, 87(3), 761–796. https://doi.org/10.2308/accr-10209

- Klein, A. (2002). Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics, 33(3), 375–400. https://doi.org/10.1016/S0165-4101(02)00059-9

- Larcker, D. F., & Rusticus, T. O. (2010). On the use of instrumental variables in accounting research. Journal of Accounting and Economics, 49(3), 186–205. https://doi.org/10.1016/j.jacceco.2009.11.004

- Lee, Y. (2013). Can independent directors improve the quality of earnings? Evidence from Taiwan. Advances in Management and Applied Economics, 3(3), 163–197.

- Litt, B., Sharma, D., & Sharma, V. (2014). Environmental initiatives and earnings management. Managerial Auditing Journal, 29(1), 76–106. https://doi.org/10.1108/MAJ-05-2013-0867

- Liu, X., & Zang, C. (2017). Corporate governance, social responsibility information disclosure, and enterprise value in China. Journal of Cleaner Production, 142, 1075–1084. https://doi.org/10.1016/j.jclepro.2016.09.102

- Lyon, T. P., & Montgomery, A. W. (2015). The means and end of greenwash. Organization & Environment, 28(2), 223–249. https://doi.org/10.1177/1086026615575332

- Martinez-Ferrero, J., Lozano, M. B., & Vivas, M. (2020). The impact of board cultural diversity on a firm’s commitment toward the sustainability issues of emerging countries: The mediating effect of a CSR committee. Corporate Social Responsibility and Environmental Management, 28(2), 675–685. https://doi.org/10.1002/csr.2080

- Martin-Reyna, J. M. S., & Duran-Encalada, J. A. (2012). The relationship among family business, corporate governance and firm performance: Evidence from the Mexican stock exchange. Journal of Family Business Strategy, 3(2), 106–117. https://doi.org/10.1016/j.jfbs.2012.03.001

- McNichols, M., & Wilson, P. (1988). Evidence of earnings management from the provision for bad debts. Journal of Accounting Research, 26(Supplement), 1–31. https://doi.org/10.2307/2491176

- Mokhtar, N., Jusoh, R., & Zulkifli, N. (2016). Corporate characteristics and environmental management accounting (EMA) implementation: Evidence from Malaysian public listed companies (PLCs). Journal of Cleaner Production, 136, 111–122. https://doi.org/10.1016/j.jclepro.2016.01.085

- Ofoegbu, G. N., Odoemelam, N., & Okafor, R. G. (2018). Corporate board characteristics and environmental disclosure quantity: Evidence from South Africa (integrated reporting) and Nigeria (traditional reporting. Journal Cogent Business & Management, 5(1), 1–27. https://doi.org/10.1080/23311975.2018.1551510

- Palacios-Manzano, M., Gras-Gil, E., & Santos-Jaen, J. M. (2021). Corporate social responsibility and its effect on earnings management: An empirical research on Spanish firms. Total Quality Management & Business Excellence, 32(7–8), 921–937. https://doi.org/10.1080/14783363.2019.1652586

- Patten, D. M., & Trompeter, G. (2003). Corporate responses to political costs: An examination of the relation between environmental disclosure and earnings management. Journal of Accounting and Public Policy, 22(1), 3–94. https://doi.org/10.1016/S0278-4254(1002)00087-X

- Peasnell, K. V., Pope, P. F., & Young, S. (2000). Accrual management to meet earnings targets: U.K. evidence pre-and post-cadbury. The British Accounting Review, 32(4), 415–445. https://doi.org/10.1006/bare.2000.0134

- Pedhazur, E. (1982). Multiple regression in behavioral research. Holt, Rinhart & Winston.

- Prencipe, A., & Bar-Yosef, S. (2011). Corporate governance and earning management in family-controlled companies. Journal of Accounting, Auditing & Finance, 26(2), 119–227. https://doi.org/10.1177/0148558X11401212

- Prior, D., Surroca, J., & Tribo, J. A. (2008). Are socially responsible managers really ethical? Exploring the relationship between earnings management and corporate social responsibilit. Corporate Governance, 16(3), 160–177. https://doi.org/10.1111/j.1467-8683.2008.00678.x

- Qian, W., Horisch, J., & Schaltegger, A. (2018). Environmental management accounting and its effects on carbon management and disclosure quality. Journal of Cleaner Production, 174, 1608–1619. https://doi.org/10.1016/j.jclepro.2017.11.092

- Qosasi, A., Susanto, H., Rusmin, R., Astami, E. W., & Brown, A. (2022). An alignment effect of concentrated and family ownership on carbon emission performance: The case of Indonesia. Cogent Economics & Finance, 10(1), 1–21. https://doi.org/10.1080/23322039.2022.2140906

- Rajpal, H. (2012). Independent directors and earnings management: Evidence from India. International Journal of Accounting and Financial Management Research, 2(4), 9–24.

- Ramon-Llorens, M. C., Garcia-Meca, E., & Pucheta-Martinez, M. C. (2020). Female directors on boards. The impact of faultlines on CSR reporting. Sustainability Accounting, Management and Policy Journal, 12(1), 156–183. https://doi.org/10.1108/SAMPJ-07-2019-0273

- Rezaee, Z., Alipour, M., Faraji, O., Ghanbari, M., & Jamshidinavid, B. (2021). Environmental disclosure quality and risk: The moderating effect of corporate governance sustainability Accounting. Management and Policy Journal, 12(4), 733–766. https://doi.org/10.1108/SAMPJ-10-2018-0269

- Rokhmawati, A. (2020). The nexus between type of energy consumed, CO2, emissions, and carbon-related costs. International Journal of Energy Economics & Policy, 10(4), 172–183. https://doi.org/10.32479/ijeep.9246

- Rover, S., Dal-Ri Murcia, F., & de Souza Murcia, F. C. (2016). The determinants of social and environmental disclosure practices: The Brazilian case. Environmental Quality Management, Fall, 25(1), 5–24. https://doi.org/10.1002/tqem.21406

- Salehi, M., Hoshmand, M., & Ranjbar, R. H. (2019). The effect of earnings management on the reputation of family and non-family firms. Journal of Family Business Management, 10(2), 128–143. https://doi.org/10.1108/JFBM-12-2018-0060

- Salvato, C., & Moores, K. (2010). Research on accounting in family firms: Past accomplishments and future challenges. Family Business Review, 23(3), 193–215. https://doi.org/10.1177/0894486510375069

- Sarbah, A., Quaye, I., & Affum-Osei, E. (2016). Corporate governance in family businesses: The role of the non-executive and independent directors. Journal of Business and Management, 4(1), 14–35. https://doi.org/10.4236/ojbm.2016.41003

- Setia-Atmaja, L., Haman, J., & Tanewski, G. (2011). The role of board independence in mitigating agency problem II in Australian family firms. The British Accounting Review, 43(3), 230–246. https://doi.org/10.1016/j.bar.2011.1006.1006

- Shwairef, A., Amran, A., Iranmanish, M., & Ahmad, N. H. (2021). The mediating effect of strategic posture on corporate governance and environmental reporting. Review of Managerial Science, 15(2), 349–378. https://doi.org/10.1007/s11846-11019-00343-11846

- Songini, I., Gnan, L., & Malmi, T. (2013). The role and impact of accounting in family business: Past research and future challenges. Journal of Family Business Strategy, 4(2), 71–83. https://doi.org/10.1016/j.jfbs.2013.1004.1002

- Thorning-Lund, S. (2012). Keeping it in the family? How independent directors add value to family businesses. Odgers Berndtson.

- Walker, R. G. (2004). Gaps in guidelines on audit committee. ABACUS, 40(2), 157–192. https://doi.org/10.1111/j.1467-6281.2004.00156.x

- Wang, D. (2006). Founding family ownership and earnings quality. Journal of Accounting Research, 44(3), 619–656. https://doi.org/10.1111/j.1475-679X.2006.00213.x

- Welbeck, E. E., Owusu, G. M. Y., Bekoe, R. A., & Kusi, J. A. (2017). Determinants of environmental disclosures of listed firms in Ghana. International Journal of Corporate Social Responsibility, 2(1), 1–12. https://doi.org/10.1186/s40991-017-0023-y

- Zahra, S., & Stanton, W. (1988). The implication of board of directors’ composition for corporate strategy and performance. International Journal of Management, 5, 261–272.

- Zellweger, T. M., Nason, R. S., Nordqvist, M., & Brush, C. G. (2011). Why do family firms strive for non-financial goals? An organizational identity perspective. Entrepreneurship Theory and Practice, 37(2), 229–248. https://doi.org/10.1111/j.1540-6520.2011.00466.x