?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study analyses the importance of lean supply chain strategy (SCS) and agile SCS in Indonesia’s bottled water industries, influencing the financial performance through mediating variables. Using the resource-based view (RBV) theory and relational view to investigate these relations, a series of hypotheses are developed, considering strategic supplier integration (SSI), strategic customer integration (SCI) as a mediator variable. The study analyses structural equation modeling (SEM) derived by observed data from 139 firms in Indonesia. The research analyzes how lean SCS and agility SCS on financial performance is affected by SSI and SCI. The paper supports the literature on lean SCS and agile SCS by theoretically elucidating and empirically revealing how SSI and SCI collaborating affect a positive relationship between lean SCS & agile SCS and financial performance.

PUBLIC INTEREST STATEMENT

The supply chain strategy policy in the bottled drinking water industry is needed in the face of business uncertainty, especially in raw materials management. For this reason, choosing the right supply chain strategy can increase the company’s competitive advantage. This article shows that strategic collaboration with suppliers and consumers can be a bridge for implementing lean and agile supply chain strategies in improving financial performance.

1. Introduction

Supply linkages exist through various terrestrial regions, which influence the vulnerability of domestic industries to operational risk and encounter more significant necessity uncertainty. For instance, the need for bottled drinking in Indonesia indicates great unpredictability due to several reasons such as climate, special occasions, and lifestyle customers. Furthermore, the bottled drinking firm is immense, complex, and affected by the monetary, community, and fiscal concerns. The drinking water industries must prioritize managing market dynamics to diminish the instability supply chain from the downstream and upstream (Giri & Bardhan, Citation2014). Its industry adopts supply chain strategies that are lean strategy and agile strategy. The lean approach eliminates waste and costs that incorporate comprehensively all operations that impact the goods and services offered to consumers, whether they are carried out by the business or by external suppliers, from the product creation to the product life span (Monczka et al., Citation1995). Externally, the JIT and Vendor-Management-Inventory (VMI) practices combine suppliers to decrease inventory costs by determining the quantity of each delivery of raw materials (Gharaei, Hoseini Shekarabi et al., Citation2019a). They also include supplier machinery operators to increase the product’s consistency, resulting in the significant development of the cup, bottle, or gallon. In contrast to what consumers prefer, the firm must produce a flexible supply chain, i.e., quickly adapt to changes in the market and limited product life spans (Blome et al., Citation2013; Gligor et al., Citation2015). The agile supply chain strategy (SCS) is necessary for the quick launch of new products to respond to adapting consumer demands (Qi et al., Citation2011) and for an efficient response to adjustments in volume and speed delivery requirements (Yusuf et al., Citation2004).

Furthermore, drinking supply chains become more exposed while a disruption arises because of the supply chain aspects (Tse, Zhang, et al., Citation2016). Manufacturers encounter the trial of establishing complicated sourcing processes capable of accommodating both suppliers’ and consumers’ needs. Bottled drinking firms in Indonesia face obstacles in performing resources because most of their material is composed of plastic pellets whose cost depends on unstable exchange rates and crude oil tariff (Sugeng et al., Citation2010). The excellent price’s influence would be more high-priced because of the factors of upstream disturbance risk (Ellis et al., Citation2010). The plain packaging expenditures mainly engage the fabrication expenses. The distinctiveness of the drinking market causes significant defiance for downstream parties by increasing unpredictable necessity.

Moreover, information and rumors associated with price spears can induce consumer need then substantially affect the quantity to fill inventory requisites through the supply chain (Chen et al., Citation2000), then diminishing consumer satisfaction. While there is a distraction in the necessity, the existing estimation plan turns ambiguous, and the primary industry could not be responsive to market situations (Germain et al., Citation2008). As an outcome of deficiency to accomplish consumer necessity, the company might bear a slump in sales ending in financial performance decreases due to surplus stock being endured (Sarkar & Giri, Citation2020). By the intensifying importance of supply chain management (SCM), SCSs should engage in vital functions in leveraging companies’ performance. The SCSs operate as a logical link between the company’s higher strategy and supply chain operations from a strategic SCM perspective (Perez-Franco et al., Citation2016).

Furthermore, developing intelligent supply chain strategies have many obstacles to enhance firm performance depended on the business environment. For instance, the execution of lean supply chain strategy (SCS) does not influence to increase the company’s performance because there is a lack of training, machine operator competence, and limited resources (Bevilacqua et al., Citation2017; Dobrzykowski et al., Citation2016). However, in stable demand, many empirical studies revealed which lean SCS enhances business performance by reducing waste and inventory cost (Antony et al., Citation2012; Chavez et al., Citation2015; Nawanir et al., Citation2013; Prajogo et al., Citation2016). Besides, the implementation of agile SCS has a failure to increase its performance because there are diseconomies of scale and cost leadership in the production process (Gligor et al., Citation2015; Um, Citation2017). Conversely, in volatile demand, many empirical findings indicated that agile SCS accelerated business performance by the speedy and effective response of supply chain to fulfill consumer requirements (Alzoubi & Yanamandra, Citation2020; Chan et al., Citation2017; Eckstein et al., Citation2015; Martinez-Sanchez & Lahoz-Leo, Citation2018; Tse et al., Citation2016). In conclusion, these endeavors fulfill the research gaps by exploring the effect of lean SCS and agile SCS on the financial performance of drinking firms in Indonesia.

To address these gaps, drawing from the theory of relational view (Dyer & Singh, Citation1998) and the theory of resource-based view (Barney, Citation1991), we create and empirically confirm a framework propositioning that two supply chain practices, namely strategic supplier integration (SSI) and strategic customer integration (SCI), respectively mediate the relationship between two SCSs, namely lean and agile, and financial performance. Intensifying efficacious SCS integrates operational activities and strategic policies among externally spread corporates (Narasimhan et al., Citation2010; Ralston et al., Citation2015). The maintenance of supply chain ties needs to be involved by firm business practices with precision knowledge sharing, solid alliances, and corporate collaboration (Leuschner et al., Citation2013). Evolving within this context, SSI is a mechanism for acquiring and sharing strategic knowledge and information within and outside the manufacturing industry through supply chain connections and their consumers (Swink et al., Citation2007).

A study’s theoretical contribution is and broadens supply chain literature to include a concept-wide viewpoint. It takes strategic supplier integration and strategic customer integration’s two supply chain practices as mediators for lean SCS and agile SCS to improve their financial performance. A linked contribution is to develop a better understanding of how competitive advantage can be achieved to benefit from inter-company integration to acquire valuable resources that are not owned internally by synergizing between the relational view perspective and the resource-based perspective. Our findings show practitioners how important it is to follow supply chain practices that enhance the supply chain strategy. The findings also show that before a supply chain strategy is deployed within the firm, the supply chain capabilities are considered.

2. Literature review

2.1. Theory of resource based view (RBV)

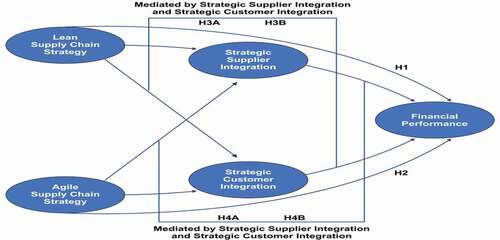

The resource-based view implies that businesses sustain their strategies and benefit from strategic capital (Barney, Citation1991). Based on the above idea that activities or practices permit implementing a policy, we view supply chain strategies as tools for improving financial performance efficiency. The supply chain strategy is to increase consumer responsiveness in the focal company’s supply chain (Melnyk et al., Citation2010). An SCS explains how an organization can benefit from competitive benefits, such as cost efficiency, response time, and flexible supply chain capabilities (Qi et al., Citation2011). SCSs are categorized into two general groups before literature: lean and agile (Fisher, Citation1997; Yusuf et al., Citation2004). While a lean SCS simplifies the entire supply chain effectively, agile SCS concentrates on reconfiguring a supply chain for unsure and competitive conditions (Ben et al., Citation1999). In drawing upon the RBV, this study identifies lean SCS and agile SCS as resources and examines their impacts on the financial performance depicted in

Figure 1. Conceptual model

2.2. Theory of relational view (RV)

The relational view theory states that competitive advantage can come from external resources such as integration between companies not to be imitated by other competitors (Dyer & Singh, Citation1998; Lavie, Citation2006)). Integration between other companies can create mutually beneficial conditions between the two parties. The supply chain’s applicability will increase due to particular assets, skills, and complex information to replicate. When the bottled-drinking industry develops the knowledge acquisition process jointly with suppliers, it is likely to achieve relational performance gains. The joint acquisition of knowledge between buyers and suppliers is a complex manufacturing knowledge by suppliers where buyers focus on direct participation in the production schedule process. Direct participation relates to buyers involved in efforts to acquire supplier knowledge by exchanging knowledge information and joint participation. The exchange of information can be illustrated when bottled water producers have PPIC (production planning inventory controlling) staff to coordinate the delivery of the supply chain for supporting raw materials in a just-in-time and responsive manner according to consumers’ needs. In portraying upon the RV, this research recognizes SSI and SCI as external resources that mediate the relationship between lean SCS and agile SCS on the financial performance depicted in .

2.3. Relationship between lean SCS and financial performance

To minimize total cost and increase product quality and lower delivery time, the Lean supply chain follows different management strategies such as JIT, Kanba, and TQM (Ardalan & Diaz, Citation2012). In a stable market environment, the lean SCS (Supply Chain Strategy) model is better for greater and consistent demand, whereas for a volatile market, it is inefficient (Katayama & Bennett, Citation1999). Bortolotti et al. (Citation2015) argue that the practice of implementing lean through TQM (Total Quality Management) indirectly affects production cost performance. There is less need for raw material supplies to protect the production system from external variants and reduce rework (Sim & Curatola, Citation1999; Yin et al., Citation2016).

Implementing lean SCS improves financial performance for the better because of reducing the cost of storing raw materials because carrying out production activities is efficient (Shah et al., Citation2020). The inventory level is by planning production needs, thereby increasing cash flow to become more liquid because the turnover of finished product expenditures is balanced with the amount of productivity produced (Shashi et al., Citation2019). For example, bottled drinking water industries’ supply chain tries to reduce the cost of excessive inventory storage by implementing just-in-time inventory management. The efficiency of inventory storage costs and the purchase of raw materials for production to be more controllable effect the production plan has been scheduled monthly by maintaining the ideal strategy through Joint Economic Lot-sizing (Gharaei, Hoseini Shekarabi et al., Citation2020a). Besides, manufacturers can save cash flow because raw materials will be carried out quickly (Sarkar & Giri, Citation2020). The turnover of finished product inventory becomes smoother, which directly increases sales turnover (Nawanir et al., Citation2016; Prajogo et al., Citation2016). Therefore we posit the following hypothesis:

: The influence of Lean SCS on financial performance is a positive significant.

2.4. Relationship between Agile SCS and financial performance

Agile SCS (Supply Chain Strategy) has two objectives: to provide timely access to market situation knowledge affected by seasonal variation, consumer expectations, and competitive measures to satisfy changing customer demands by introducing new products (Lee, Citation2004; Whitten et al., Citation2012). Besides, these goods’ rapid design and distribution include facilitating cooperation and collaboration with stakeholders, such as schedule sharing, loading times, and inventory through sustainable mobility way out (Awasthi & Omrani, Citation2019; Swafford et al., Citation2006).

Agile SCS emphasizes a dynamic supply chain that can engage and respond rapidly to dynamic changes in a particular context and an intense supply chain (Qrunfleh & Tarafdar, Citation2014). Thus, the supply chain can offer different quantities of goods and satisfy various requirements of markets that indirectly increase the business’s financial performance (Chan et al., Citation2017). For example, the supply chain from bottled water manufacturers focuses on the existence of a high buffer stock when facing a surge in demand from consumers and the support of responsive and flexible supplier performance. The high certainty of the availability of finished products so that customer needs can be fulfilled by establishing the overall ideal replenishments (Gharaei, Hoseini Shekarabi et al., Citation2019b). Besides, the supply chain can change at any time following requests from customers, such as requests to suppliers in the form of 600 ml packaging bottles that can be exchanged for 1500 ml packaging bottles because there is a change in significant consumers’ orders. The availability of high buffer stock in production support materials has a positive effect on bottled drinking water producers when there is a significant increase in demand from a dynamic market that can still meet the needs of consumers (Eckstein et al., Citation2015). Therefore we posit the following hypothesis:

: The influence of Agile SCS on financial performance is a positive significant.

2.5. Mediation effect of SSI, and SCI on the relationship between Lean SCS and financial performance

The lean SCS diffuses its impact on financial performance through the SSI (strategic supplier integration) in several practices. First, manufacturers who execute lean SCS must maintain good relationships with their suppliers to ensure raw materials’ availability. The implementation of supply chain integration runs well that focuses on the lean supply chain to develop and access supply chain partners’ resources to build long-term relationships with suppliers based on faith (Qrunfleh & Tarafdar, Citation2013). They indirectly help reduce the level of finished goods inventory storage and save production costs, thus enabling the company to realize the benefits of lean SCS (McIvor, Citation2001). Thus, the successful implementation of the lean supply chain tends to produce cooperative and integrated supplier relationships at a high level in exchanging information between producers and their suppliers (Choi & Wu, Citation2009). Second, the firm has a partnership with strategic suppliers who have a close relationship by integrating the process of taking raw materials for production with their suppliers in improving operational performance in factories (Cheng et al., Citation2016). Support firms take initiatives such as ideas exchange, identifying potential business prospects, increasing know-how of natural products, and sustainable development practices with their suppliers (Saeed et al., Citation2011). With closer relationships and a more comprehensive range of interactions from suppliers, focused manufacturers can be more flexible and innovative in the face of changing competitive pressures and opportunities (Rabbani et al., Citation2019). For example, bottled drinking water manufacturers face demand during the rainy season, where the demand for products tends to be stable. The producer’s supply chain must adjust to the production planning schedule of the leading supplier so that it can reduce the rejection of excessive inventory storage due to the slow turnover of finished goods in the producer warehouse (Rabbani et al., Citation2020). With the application of just-in-time inventory management by manufacturers, it is necessary to synchronize fast information exchange and strong relationships with major suppliers, such as supplying raw materials for cups, cartons, or bottles (Giri & Masanta, Citation2020). The schedule for delivery of raw materials from suppliers can be well planned accordingly with the bottle-drinking industry’s wishes (Yusuf et al., Citation2004).

Third, an enhanced integration process and information sharing among supply chain partners, including trust, partnership, and collaboration, can reduce uncertainty from internal and external business factors such as engine trouble at the factory. They further reduce waste and increase operational efficiency by considering the availability of maintenance time to minimize downtime cost, indirectly improving its financial performance (Duan et al., Citation2018; Huo et al., Citation2016; Wiengarten et al., Citation2016). The firm has a partnership with strategic suppliers who have a close relationship by integrating the process of taking raw materials for production with their suppliers in improving operational performance in factories (Cheng et al., Citation2016). For example, bottled drinking industries often find it difficult to obtain raw materials for production such as cups or bottles when the US Dollar exchange rate is strengthening significantly. The price of crude oil has increased sharply, which affects the price of plastic ore material, where the purchase order (PO) from the manufacturer will change according to the prevailing market price. The exchange of information linked to fabrication preparing schedules and the accessibility of raw sources by the manufacturer will help the supplier provide additional PO quotas for more extensive production auxiliary materials or hedging with price contracts valid for 3 (three) months. In this regard, they can minimize the expense of supporting raw sources, which indirectly results in economic fabrication costs. The accessibility of finished products is sustainable and increases sales turnover. The integration and exchange of knowledge with supply chain allies in establishing faith and strong support can lower the unpredictability of dynamic circumstances and continuously reduce the total inventory cost (Hoseini Shekarabi et al., Citation2019). It improves the quality of production operations, indirectly improves the company’s financial performance, such as cost-effectiveness; sales growth (Huo et al., Citation2016; Ketchen & Hult, Citation2007). Therefore we posit the following hypothesis:

: SSI mediates the relation between the lean SCS and financial performance.

SCI helps businesses responsibly look for information on significant consumers’ expectations and demands (Vickery et al., Citation2003). Consumer data enables manufacturers to coordinate their activity to satisfy customer requirements because strategically integrating with customers’ needs more than multi-level process or operational tasks (Ralston et al., Citation2015). Mutually respectful customer interactions and mutual customer satisfaction knowledge around the organization make strategic customer integration more relevant (Flynn et al., Citation2010), so manufacturers of lean SCS implementation can build custom integration capabilities in good working order (Qi et al., Citation2017). For example, bottled drinking manufactures face demand during the rainy season, where the demand for products is relatively stable. Thus, the producer’s supply chain must adjust the expenditure of finished products to the customers so that there is no accumulation of finished products, which causes the producer’s warehouse to become full quickly with considering sustainable shipping scheduling (Sayyadi & Awasthi, Citation2018). Therefore, with strong integration with the main customers, manufacturers can entrust the finished products or products to their main customers’ warehouses (Restuputri et al., Citation2020). This implementation of lean SCS can predict the demand for finished products from major customers because there is an exchange of inventory information (Huo et al., Citation2016).

Strategic policies between manufacturers and customers are in the form of collaboration on storage, distributing, purchasing, production scheduling, and transporting, also, to solve problems linked to product quality to increase sales turnover and efficiency of storage costs for finished goods (Ku et al., Citation2015; Payne & Frow, Citation2005; Sayyadi & Awasthi, Citation2020; Wong et al., Citation2011). For example, bottled drinking water manufacturers produce glass and bottle products in a volume of 2000 cartons per day during the rainy season. The finished products stored in the producer’s warehouse will continue to increase if the sales department experiences decreased product absorption in the market every day. For this reason, the turnover of finished product expenditures slows down, and the producer must find a rental warehouse so that it can store finished product inventories. Related to this, the consignment of finished products in customer warehouses can increase sales on an ongoing basis to minimize warehouse rental costs and the level of accessibility of finished products at a safe level and retain existing market portion by other competitors (Hoseini Shekarabi et al., Citation2019; Kazemi et al., Citation2018). Solid collaboration among customers and producers supports benefits to improve the value of information related to product necessity and production preparation time, ensures damage arising from inventory storage in consumer warehouses, and makes it more responsive to customer needs (He et al., Citation2014; Ralston et al., Citation2015). Therefore we posit the following hypothesis:

: SCI mediates the relation between the lean SCS and financial performance.

2.6. Mediation impact of SSI, and SCI on the relationship between Agile SCS and financial performance

The agile SCS allows companies that concentrate on evolving consumer needs to improve response and adaptability while adding value to consumers by reducing waste in the supply chain (Roh et al., Citation2014). Stavrulaki and Davis (Citation2010) stated that agile SCS should emphasize flexible logistics processes. Manufacturers must explore various supplier options and logistics networks to ensure rapid response to customized demand and supply chain disruption due to uncertainty. Relationships with strategic suppliers through knowledge sharing and strong commitment are an integral part of SCS (Zhao et al., Citation2011). For example, bottled drinking water manufacturers face demand in summer conditions where product demand has significantly increased when compared to typical situations. For this reason, flexible and responsive supplier performance is needed in supporting the supply chain for bottled water producers so that the supplier’s production schedule planning can change and follow the demand from the producer. Illustrating manufacturer has purchasing order for a type of 600 ml bottle outside of the set schedule. In contrast, the supplier has prepared a product with a 1500 ml bottle type for the manufacture. Based on this situation, the supplier must respond to requests and flexibly replace shipments with 600 ml bottles so that the joint problem resolution can be accommodated by both parties properly. For this reason, a frequency of information exchange with significant suppliers is needed in response to information about delivery waiting times quickly (Lai et al., Citation2012; Tarafdar & Qrunfleh, Citation2017).

Implementing a solid SSI increases the cost ability, efficiency, and distribution speed to producers in achieving better financial performance (Ariadi et al., Citation2020; Cheng et al., Citation2016; Huo et al., Citation2016; Subburaj et al., Citation2020; Wiengarten et al., Citation2016). It is due to a synchronized schedule in real-time for raw material collection between the producer and the supplier by facilitating virtual collaboration (Hao et al., Citation2018). The purchase order for auxiliary materials from the price and volume of the material can be hedged. For example, when raw materials’ price has increased, the producer still gets the same volume and price as the old contract from the supplier. The operational costs of purchasing raw materials do not increase. Therefore we posit the following hypothesis:

: SSI mediates the relation between the agile SCS and financial performance.

Agile SCS recognizes that the supply chain is fast to adapt to short-run changes that meet consumer needs and enable businesses to address market uncertainty. The supply chain needs to maintain an increased capacity buffer stock for responding to the dynamic market (Qi et al., Citation2009). Businesses need to be aware of emerging challenges and respond to them appropriately and responsively. Companies that implement agile SCS will always prioritize their customers’ desires so that they are always optimal in terms of service, which leads to the achievement of a sustainable competitive advantage (Tarafdar & Qrunfleh, Citation2017). For example, bottled drinking water manufacturers face high demand in the summer season compared to normal conditions. Flexible and responsive supplier performance is needed to support the supply chain for firms to meet consumers’ demands. It can be illustrated when a firm receives 600 ml bottles with a volume outside the contract agreed with consumers, while manufacturers only have limited production raw materials. Based on this situation, their supply chains must be supported by flexible and responsive supplier performance to send more raw materials than the previous normal situation.

SCI includes customers collaborating with manufacturing firms to coordinate stock levels, forecast production, demand estimates, monitor orders, and provide goods through the vendor-managed inventory with consignment stock agreement (Gharaei, Karimi., et al., Citation2019a; Wong et al., Citation2011). From the following factors, the significant influence of customer integration can be clarified on improving financial results. Customers can deliver businesses with strategic insights into consumer demands and potential opportunities that enable customers to meet their needs more effectively and effectively (Wong et al., Citation2011). By integrating customers, firms can penetrate deep into consumer activities to understand their goods, cultures, markets, and industries to meet customer requirements and demands accordingly (Dubey et al., Citation2015). The close partnership between the customer and the manufacturer allows for an improvement in the precision of product request details, thereby reducing the manufacturer’s product design and preparation time, reducing inventory cost storage, and responding more effectively to consumer needs (Ariadi et al., Citation2020; He et al., Citation2014; Tsao, Citation2015). Therefore we posit the following hypothesis:

: SCI mediates the relation between the agile SCS and financial performance.

3. Methodology

3.1. Sample and data collection

Data were gathered by a database of the Indonesian Association for Bottled Water Industry. The analytical unit is at the company level. The buying, manufacturing, and supply chain functions were chosen as senior executives (directors, vice presidents, and managers). In a randomly selected manufacturing industry sample in Indonesia, we have used a list of 212 executives who have more than 100 employees and 1 USD million in annual sales revenue. The size restrictions’ objective was to adjust for small companies’ unlikely acquisition or usage in their supply chains of sophisticated information systems. The data has been obtained via e-mail. One hundred thirty-nine completed surveys, representing 65.6 percent, were retrieved compared to other previous supply chain management studies (Li et al., Citation2006). below lists the sample profiles of the respondents.

Table 1. The Respondent Profiles

3.2. Measurement items

This research built and adopted buildings tailored to the established literature. The researchers defined five variables based on the literature review (lean SCS, agile SCS, SSI, and SCI) supporting financial performance. For example, respondents were enquired to affirm the significance of lean SCS and agile SCS to increase their financial performance, applying a five-point scale, “Strongly disagree” (1) and “strongly agree” (5).

Lean SCS was determined by eight items that our supply chain reduces any wastes; selects supplier based on cost; selects supplier based on quality; has to maintain a long relationship of suppliers; has to maintain a rigid relationship of suppliers; supplies predictable products; has the small number of suppliers; implements just in time for inventory (Qi et al., Citation2017). Agile SCS was measured by eight items which our supply chain provides the customer with customized products; selects supplier based on flexibility; selects supplier based on responsiveness; has to maintain a short relationship of suppliers; has to maintain a flexible relationship of suppliers; supplies predictable products; has a large number of suppliers; has a higher capacity buffer for inventory (Qrunfleh & Tarafdar, Citation2013). SSI was determined by six items which we collect supplier feedbacks for quality improvement; share information related to inventory with suppliers; solve problems jointly with our suppliers; develop the joint product with suppliers; share information related to production schedule with suppliers; implement vendor management inventory in suppliers’ warehouse (Tarafdar & Qrunfleh, Citation2017; Wong et al., Citation2011). SCI was determined by six items which we collect customer feedbacks for quality improvement; share information related to inventory with customers; solve problems jointly with our customers; develop the joint product with customers; share information related to production schedule with customers; implement consignment management inventory in customers’ warehouse (Tarafdar & Qrunfleh, Citation2017; Wiengarten et al., Citation2016). Financial performance was determined by five items which are Return on Investment (ROI), Return on Asset (ROA), production cost, Return on Sales (ROS), and growth of market share in the last three years (Chan et al., Citation2017).

4. Data analysis and results

To identify the direct and indirect effect of lean SCS and agile SCS on financial performance with the mediating effect of SSI and SCI in Indonesia’s bottled water industry. A statistical SmartPLS software, PLS-SEM (Partial Least Square-Structural Equation Modelling) method, was applied to evaluate the overall measurement model.

4.1. Measurement model

Convergent validity and discriminant validity have been tested. Convergent validity is the extent to which the objects that calculate a sole building agree. Evaluating convergent validity by testing substantial factor loads exceeding 0.7, composite reliabilities exceeding 0.8, and the average extracted variance (AVE) should be more than 0.5 for all constructs (Fornell & Larcker, Citation1981). All factor charges in our model are more significant than 0.7, and measuring objects are removed if their factor loads are less than 0.70. The outcomes display which our model fulfills the criterion of convergent validity. With Cronbach α, we tested the internal reliability of scales. indicates the loading factor, Average Variance Extracted (AVE), composite reliability, and rho_A of all constructions.

Table 2. Convergent validity

This newly recommended approach was additionally applied to test the discriminant validity in the method of the Heterotrait-Monotrait ratio of correlations, and the outcomes are displayed in . If the HTMT is lesser than the value of 0.90 (Gold et al., Citation2001), a discriminant validity analysis is confirmed shown in . All constructions in the measurement model also were determined to be sufficiently discriminatory. The estimation model takes into account the relationship between the variables and their items. The measuring of the goodness-of-fit model was shown to be acceptable (Standardized Root Mean Square Residual [SRMR] = 0.071, and Normal Fit Index [NFI] = 0.928) and confirmed the proposed model because of SRMR value <0.08 and NFI value >0.9 (Henseler et al., Citation2015). Finally, we posit how the framework fits well with the data and is therefore sufficient to test the study’s hypothesis.

Table 3. Discriminant validity

4.2. Hypothesis examining

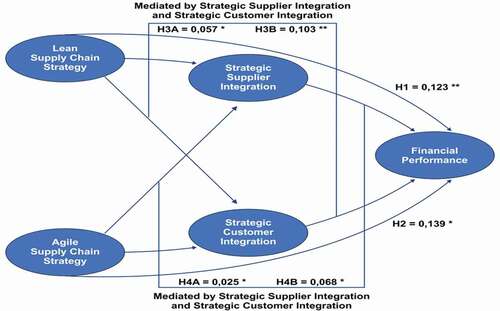

The research assesses the variables’ structural relationships by analyzing the various mediatory impacts through a path analysis. Path analyses were employed to evaluate hypotheses in the research model using the Smart-PLS program. The outcome displayed in portrays standardized path coefficients of the research model. and define that the path coefficients from lean SCS to Financial Performance were positive and significant (ß = 0.123; p-value < 0.05), whereas the path coefficients from agile SCS to Financial Performance were also positive and significant (ß = 0.139; p < 0.01). Thus, H1 and H2 are supported. Additionally, The indirect relationship of lean SCS on Financial Performance through Strategic Supplier Integration, and Strategic Customer Integration as mediator was also positive and significant respectively (ß = 0.057, p < 0.05; ß = 0.103, p < 0.05), that and

are supported. Thus, the indirect effects of agile SCS on Financial Performance through Strategic Supplier Integration, and Strategic Customer Integration as mediator was also positive and significant (ß = 0.025, p < 0.05; ß = 0.068, p < 0.05), that state

and

are supported. Given the above, we can conclude which SSI and SCI partially mediates the relationship between lean SCS & agile SCS and financial performance.

Figure 2. Results of path analysis (*p value < 0,01; **p value < 0,05)

Table 4. Hypotheses testing

value, presented in , shows that the lean SCS, agile SCS, SSI, and SCI account for 71,4 percent of the Financial Performance variance.

5. Discussion

The outcomes of the present research determine that the lean SCS (Supply Chain Strategy) significantly influences the financial performance of the bottled drinking firm in Indonesia, which confirms the findings of Nawanir et al. (Citation2016), Prajogo et al. (Citation2016), and Shashi et al. (Citation2019). It focuses on reducing waste or time in the production process and minimizing raw material inventories with the just-in-time concept. Implementing lean SCS improves financial performance for the better due to a decrease in the cost of storing raw materials and a more efficient implementation time of production activities, and increasing inventory levels by planning production requirements. Cash flow becomes liquid because the turnover of finished product expenditures is offset by generated productivity (Shashi et al., Citation2019).

Furthermore, the agile SCS significantly impacts the financial performance of the bottled drinking firm in Indonesia, which confirms the findings of Chan et al. (Citation2017), Eckstein et al. (Citation2015), Tse et al. (Citation2016), Martinez-Sanchez and Lahoz-Leo (Citation2018), and Wahyuni et al. (Citation2020). The execution of agile SCS improves the better because of the high buffer stock in auxiliary production materials. So it has a positive effect on bottled water manufacturers when there is a significant increase in demand from a dynamic market that can still meet consumers’ needs. Besides, the agile supply chain supporting customized products based on the personalized customer can increase the growth of new shares where manufacturers can provide private label products for the hotel and restaurant segments. The sales turnover of the product continues to increase apart from regular products.

We find that the lean SCS has a close and strong relationship with major suppliers so that collaboration and coordination with suppliers can run well. For this reason, the successful implementation of the supply chain in a lean-oriented manner creates cooperative supplier relationships and a high level of information exchange between the two parties (Choi & Wu, Citation2009; Qrunfleh & Tarafdar, Citation2013). Manufacturers who implement high integration with suppliers prioritize information sharing related to production schedule planning and raw materials’ availability. So the significant suppliers can distribute auxiliary materials on time according to the needs of the manufactures. Strategic supplier integration helps firms develop production plans, providing raw materials and on-time delivery (Flynn et al., Citation2010). Firms can be assisted by reducing the cost of storing raw materials in warehouses because of a strong relationship with suppliers. The availability of production raw materials ensure to the demand from customers, the achievement of financial performance can run optimally because of continuous product sales and consistent growth of new market share every month, which impacts the increase in the company’s net profit (Zhao et al., Citation2015; Chen et al., Citation2018; Ariadi et al., Citation2020; Subburaj et al., Citation2020). That is, strategic supplier integration partially mediates the relationship between lean SCS and financial performance.

Furthermore, another finding is that lean SCS has impacted strategic customer integration, which influences financial performance. The implementation of lean SCS focuses on regular production demand and production costs using low-cost raw materials. It has standard quality, such as cup packaging that is not easily broken even though the weight is relatively standard. The harmonious relationship between significant customers and manufacturers can improve demand information and production planning time. A decrease in finished stocks’ inventory to increase customer service satisfaction remains optimal (Huo et al., Citation2016). By solid integration with the main customers, manufacturers can entrust the products to the customers’ warehouse. The products consignment in customers’ warehouses can increase sales on an ongoing basis to minimize manufacturers’ warehouse of rental costs and the level of accessibility of finished goods at a safe inventory and retain existing market segment from other competitors (Gharaei, Karimi et al., Citation2019a). The solid alliance among customers and industries grants benefits to improve the quality of information related to product necessity and production preparation time, ensures damage arising from inventory storage in consumer warehouses, and becomes more responsive to meeting consumer demands (He et al., Citation2014; Ralston et al., Citation2015). Therefore, producers respond to customer demand requirements accurately and quickly, improve service levels of delivery of finished products on schedule, and reduce their stock storage costs, thereby increasing sustainable product sales and company profitability (Swink et al., Citation2007; Chen et al. al., Citation2018; Subburaj et al., Citation2020; Ariadi et al., Citation2020). That is, strategic customer integration partially mediates the relationship between lean SCS and financial performance.

Our finding shows that an agile SCS has impacted strategic supplier integration, which increases financial performance. Manufactures are to integrate with their primary suppliers so that any design changes in cup or cardboard packaging products ordered from consumers can be responded to quickly by the supplier. They identify new market opportunities and develop more excellent knowledge about the raw materials of products from suppliers (Saeed et al., Citation2011) so that they can be more flexible and innovative in facing changing competitive pressures and opportunities. Major suppliers’ orientation is involved in every production activity (design, engineering, procurement, delivery, and recycling). It helps industries develop input related to product design and raw materials’ availability (Vickery et al., Citation2010). Sharing information about the availability of supporting raw materials from manufactures toward major suppliers provides certainty of information about the waiting time for the delivery of raw materials (Lai et al., Citation2012), so there is efficiency in the cost of purchasing and storing raw materials. Firms that implement high integration with suppliers prioritize information sharing related to production schedule planning so that the leading suppliers can distribute auxiliary materials on time according to their needs (Flynn et al., Citation2010). Thus, a strong relationship with major suppliers reduces the cost of storing raw materials in warehouses that ensure the availability of production raw materials according to manufacturers’ demand (Zhao et al., Citation2015; Chen et al., Citation2018; Ariadi et al., Citation2020). That is, strategic supplier integration partially mediates the relationship between agile SCS and financial performance.

Furthermore, another finding shows that an agile SCS has impacted strategic customer integration, affecting financial performance. Intense interaction with critical customers allows manufacturers to consider the needs of their consumers and predict how they will evolve. A supply chain that has responsive and flexible performance is needed to handle varies when the market is dynamic by collecting customer specifications effectively and retorting to amends in customer demand such as product design (Ralston et al., Citation2015). The creation of a close relationship with customers increases the exchange of information so that producers can determine and fulfill needs according to customers’ preferences (Droge et al., Citation2012). Besides, the guarantee of return (exchange) of damaged products from manufacturers and receiving input from customers regarding the design and quality of product packaging is a form of joint problem solving with consumers who will purchase orders for products. Firms receive suggestions and feedback about packaging design so that they can build long-term and strategic relationships with consumers (X. A. Koufteros et al., Citation2010; X. Koufteros et al., Citation2005). Therefore, manufacturers respond to customer demand needs accurately and quickly, resulting in increased service delivery of finished products on schedule, and reduced stock storage costs from manufacturers, which will directly increase sustainable product sales and company profitability (Swink et al., Citation2007; Chen et al., Citation2018; Subburaj et al., Citation2020; Ariadi et al., Citation2020). That is, SCI partially mediates the relationship between agile SCS and financial performance.

6. Theoretical and managerial implications

Theoretically, this research collaborates the synergy between the theory of resource-based view and relational view for relationship lean SCS (Supply Chain Strategy), and agile SCS to enhance financial performance through SSI and SCI in bottled water industry Indonesia. The SSI and SCI are arranged as mediators. These represent the new model that fulfills the research gap between lean SCS and agile SCS on financial performance. The perspective RV theory that manufacturers achieve relational performance through partnerships with strategic suppliers such as certainty of production schedules and delivery of raw materials. While partnerships with strategic consumers such as sales projections and delivery of finished products become more sustainable, the cash flow is more liquid to affect financial performance.

From a practical point of view, the findings have significant repercussions for managers. First, an agile SCS is more effectively applied to enhance financial performance when compared to a lean supply chain strategy. Due to the very tight competition situation in the bottled water industries, the market tends to seasonal variation. Thus, manufactures try to respond to customer demands quickly, such as changes in packaging design and customization of packaging products according to the personalized customers, and support for buffer inventory is relatively high. Second, implementing lean SCS has a more substantial effect on SSI and SCI than an agile SCS. The lean SCS collects auxiliary raw materials from the leading supplier with a minimum volume of the purchase order (PO) on a large scale and releases the finished product to the leading distributor according to the monthly cooperation agreement contract.

In contrast, the agile supply chain focuses on supporting raw materials with flexible PO and issuance of finished products according to the needs of customized customers, such as private label products sold in hotels or minimarkets. The lean SCS can improve financial performance more optimally through an integrated approach to customers. The manufacturer’s sales marketing will regularly place the product stocks into the customers’ warehouse every week or day to optimize production results’ absorption. These paths offer managers instructions to perform financial performance.

7. Conclusions and limitations

This study’s findings have delivered some significantly helpful shreds of evidence of the role of lean SCS and agile SCS to increase financial performance in the bottled water firms in Indonesia. The agile SCS is more effective in dynamic conditions than the lean SCS in stable conditions because of seasonal variation. Then, the research proposes that SSI and SCI mediate the link between lean SCS & agile SCS and financial performance. However, mediating SSI and SCI effectively impacts lean SCS to financial performance rather than from agile SCS to financial performance. The firm’s approach is more inclined towards strategic customer integration because collaboration and coordination policies are easy to implement regarding the delivery and supply of products to customer warehouses compared to strategic supplier integration. There are standard operating procedures from the supplier so that the coordination policy process becomes more complicated, especially concerning the payment.

There are limitations in this analysis that suggest some future study advice. This analysis applies a cross-sectional design, which will allow a longitudinal study to be used for subsequent research to examine further the impacts of lean SCS and agile SCS on SSI and SCI that also enhances financial performance. Finally, this research is only carried out by a single industry, and it is pretty advantageous to gather data from other industries to deliver more confirmation of outcomes.

Additional information

Funding

Notes on contributors

Gede Ariadi

Gede Ariadi is a PhD student of management department at Brawijaya University, Indonesia. His research interests include supply chain management, operational management, manufacturing flexibility and vocational industry.

Surachman is Professor of Management at Brawijaya University, Indonesia. His research interests include supply chain management, operational management, production planning, total quality control and total quality management.

Sumiati is Associate Professor of Management at Brawijaya University, Indonesia. His research interests include financial management, operational management, and flexibility management.

Fatchur Rohman is Associate Professor of Management at Brawijaya University, Indonesia. His research interests include operational management, marketing, and flexibility management.

References

- Alzoubi, H., & Yanamandra, R. (2020). Investigating the mediating role of information sharing strategy on agile supply chain. Uncertain Supply Chain Management, 8(2), 273–18. https://doi.org/https://doi.org/10.5267/j.uscm.2019.12.004

- Antony, J., Agus, A., & Hajinoor, M. S. (2012). Lean production supply chain management as driver towards enhancing product quality and business performance. International Journal of Quality & Reliability Management., 29(1), 92-121. https://doi.org/https://doi.org/10.1108/02656711211190891

- Ardalan, A., & Diaz, R. (2012). NERJIT: Using net requirement data in Kanban‐controlled jumbled‐flow shops. Production and Operations Management, 21(3), 606–618. https://doi.org/https://doi.org/10.1111/j.1937-5956.2011.01268.x

- Ariadi, G., Surachman, Sumiati, Rohman, F., Surachman, S., & Sumiati, S. (2020). The effect of strategic external integration on financial performance with mediating role of manufacturing flexibility : Evidence from bottled drinking industry in Indonesia. Management Science Letters, 10(15), 3495–3506. https://doi.org/https://doi.org/10.5267/j.msl.2020.6.045

- Awasthi, A., & Omrani, H. (2019). A goal-oriented approach based on fuzzy axiomatic design for sustainable mobility project selection. International Journal of Systems Science: Operations and Logistics, 6(1), 86–98. https://doi.org/https://doi.org/10.1080/23302674.2018.1435834

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/https://doi.org/10.1177/014920639101700108

- Ben, N. J., Naim, M. M., & Berry, D. (1999). Leagility: Integrating the lean and agile manufacturing paradigms in the total supply chain. International Journal of Production Economics, 62(1–2), 107–118. https://doi.org/https://doi.org/10.1016/S0925-5273(98)00223-0

- Bevilacqua, M., Ciarapica, F. E., & De Sanctis, I. (2017). Lean practices implementation and their relationships with operational responsiveness and company performance: An Italian study. International Journal of Production Research, 55(3), 769–794. https://doi.org/https://doi.org/10.1080/00207543.2016.1211346

- Blome, C., Schoenherr, T., & Rexhausen, D. (2013). Antecedents and enablers of supply chain agility and its effect on performance: A dynamic capabilities perspective. International Journal of Production Research, 51(4), 1295–1318. https://doi.org/https://doi.org/10.1080/00207543.2012.728011

- Bortolotti, T., Danese, P., Flynn, B. B., & Romano, P. (2015). Leveraging fitness and lean bundles to build the cumulative performance sand cone model. International Journal of Production Economics, 162, 227–241. https://doi.org/https://doi.org/10.1016/j.ijpe.2014.09.014

- Chan, A. T. L., Ngai, E. W. T., & Moon, K. K. L. (2017). The effects of strategic and manufacturing flexibilities and supply chain agility on firm performance in the fashion industry. European Journal of Operational Research, 259(4), 486–499. https://doi.org/https://doi.org/10.1016/j.ejor.2016.11.006

- Chavez, R., Yu, W., Jacobs, M., Fynes, B., Wiengarten, F., & Lecuna, A. (2015). Internal lean practices and performance: The role of technological turbulence. International Journal of Production Economics, 160, 157–171. https://doi.org/https://doi.org/10.1016/j.ijpe.2014.10.005

- Chen, F., Drezner, Z., Ryan, J. K., & Simchi-Levi, D. (2000). Quantifying the bullwhip effect in a simple supply chain: The impact of forecasting, lead times, and information. Management Science, 46(3), 436–443. https://doi.org/https://doi.org/10.1287/mnsc.46.3.436.12069

- Chen, M., Liu, H., Wei, S., & Gu, J. (2018). Top managers' managerial ties, supply chain integration, and firm performance in China: A social capital perspective. Industrial Marketing Management, 74, 205–214.

- Cheng, Y., Chaudhuri, A., & Farooq, S. (2016). Interplant coordination, supply chain integration, and operational performance of a plant in a manufacturing network: A mediation analysis. Supply Chain Management: An International Journal, 21(5), 550–568. https://doi.org/https://doi.org/10.1108/SCM-10-2015-0391

- Choi, T. Y., & Wu, Z. (2009). Taking the leap from dyads to triads: Buyer–supplier relationships in supply networks. Journal of Purchasing and Supply Management, 15(4), 263–266. https://doi.org/https://doi.org/10.1016/j.pursup.2009.08.003

- Dobrzykowski, D. D., McFadden, K. L., & Vonderembse, M. A. (2016). Examining pathways to safety and financial performance in hospitals: A study of lean in professional service operations. Journal of Operations Management, 42, 39–51. https://doi.org/http://dx.doi.org/10.1016/j.jom.2016.03.001

- Droge, C., Vickery, S. K., & Jacobs, M. A. (2012). Does supply chain integration mediate the relationships between product/process strategy and service performance? An empirical study. International Journal of Production Economics, 137(2), 250–262. https://doi.org/https://doi.org/10.1016/j.ijpe.2012.02.005

- Duan, C., Deng, C., Gharaei, A., Wu, J., & Wang, B. (2018). Selective maintenance scheduling under stochastic maintenance quality with multiple maintenance actions. International Journal of Production Research, 56(23), 7160–7178. https://doi.org/https://doi.org/10.1080/00207543.2018.1436789

- Dubey, R., Gunasekaran, A., Sushil, & Singh, T. (2015). Building theory of sustainable manufacturing using total interpretive structural modelling. International Journal of Systems Science: Operations and Logistics, 2(4), 231–247. https://doi.org/https://doi.org/10.1080/23302674.2015.1025890

- Dyer, J. H., & Singh, H. (1998). The relational view: Cooperative strategy and sources of interorganizational competitive advantage. Academy of Management Review, 23(4), 660–679. https://doi.org/https://doi.org/10.5465/amr.1998.1255632

- Eckstein, D., Goellner, M., Blome, C., & Henke, M. (2015). The performance impact of supply chain agility and supply chain adaptability: The moderating effect of product complexity. International Journal of Production Research, 53(10), 3028–3046. https://doi.org/https://doi.org/10.1080/00207543.2014.970707

- Ellis, S. C., Henry, R. M., & Shockley, J. (2010). Buyer perceptions of supply disruption risk: A behavioral view and empirical assessment. Journal of Operations Management, 28(1), 34–46. https://doi.org/https://doi.org/10.1016/j.jom.2009.07.002

- Fisher, M. L. (1997). What is the right supply chain for your product? Harvard Business Review, 75, 105–117. https://www.hbsp.harvard.edu/product/97205-PDF-ENG

- Flynn, B. B., Huo, B., & Zhao, X. (2010). The impact of supply chain integration on performance: A contingency and configuration approach. Journal of Operations Management, 28(1), 58–71. https://doi.org/https://doi.org/10.1016/j.jom.2009.06.001

- Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Sage Publications Sage CA.

- Germain, R., Claycomb, C., & Dröge, C. (2008). Supply chain variability, organizational structure, and performance: The moderating effect of demand unpredictability. Journal of Operations Management, 26(5), 557–570. https://doi.org/https://doi.org/10.1016/j.jom.2007.10.002

- Gharaei, A., Hoseini Shekarabi, S. A., & Karimi, M. (2020a). Modelling and optimal lot-sizing of the replenishments in constrained, multi-product and bi-objective EPQ models with defective products: Generalised cross decomposition. International Journal of Systems Science: Operations and Logistics, 7(3), 262–274. https://doi.org/https://doi.org/10.1080/23302674.2019

- Gharaei, A., Hoseini Shekarabi, S. A., Karimi, M., Pourjavad, E., & Amjadian, A. (2019a). An integrated stochastic EPQ model under quality and green policies: Generalised cross decomposition under the separability approach. International Journal of Systems Science: Operations and Logistics, 1–13. https://doi.org/https://doi.org/10.1080/23302674.2019

- Gharaei, A., Karimi, M., & Hoseini Shekarabi, S. A. (2019b). An integrated multi-product, multi-buyer supply chain under penalty, green, and quality control polices and a vendor managed inventory with consignment stock agreement: The outer approximation with equality relaxation and augmented penalty algorithm. Applied Mathematical Modelling, 69, 223–254. https://doi.org/https://doi.org/10.1016/j.apm.2018.11.035

- Gharaei, A., Karimi, M., & Hoseini Shekarabi, S. A. (2020). Joint economic lot-sizing in multi-product multi-level integrated supply chains: Generalized benders decomposition. International Journal of Systems Science: Operations and Logistics, 7(4), 309–325. https://doi.org/https://doi.org/10.1080/23302674.2019.1585595

- Giri, B. C., & Bardhan, S. (2014). Coordinating a supply chain with backup supplier through buyback contract under supply disruption and uncertain demand. International Journal of Systems Science: Operations and Logistics, 1(4), 193–204. https://doi.org/https://doi.org/10.1080/23302674.2014.951714

- Giri, B. C., & Masanta, M. (2020). Developing a closed-loop supply chain model with price and quality dependent demand and learning in production in a stochastic environment. International Journal of Systems Science: Operations & Logistics, 7(2), 147–163. https://doi.org/https://doi.org/10.1080/23302674.2018.1542042

- Gligor, D. M., Esmark, C. L., & Holcomb, M. C. (2015). Performance outcomes of supply chain agility: When should you be agile? Journal of Operations Management, 33, 71–82. https://doi.org/https://doi.org/10.1016/j.jom.2014.10.008

- Gold, A. H., Malhotra, A., & Segars, A. H. (2001). Knowledge management: An organizational capabilities perspective. Journal of Management Information Systems, 18(1), 185–214. https://doi.org/https://doi.org/10.1080/07421222.2001.11045669

- Hao, Y., Helo, P., & Shamsuzzoha, A. (2018). Virtual factory system design and implementation: Integrated sustainable manufacturing. International Journal of Systems Science: Operations and Logistics, 5(2), 116–132. https://doi.org/https://doi.org/10.1080/23302674.2016.1242819

- He, Y., Keung Lai, K., Sun, H., & Chen, Y. (2014). The impact of supplier integration on customer integration and new product performance: The mediating role of manufacturing flexibility under trust theory. International Journal of Production Economics, 147(PART B), 260–270. https://doi.org/https://doi.org/10.1016/j.ijpe.2013.04.044

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/https://doi.org/10.1007/s11747-014-0403-8

- Hoseini Shekarabi, S. A., Gharaei, A., & Karimi, M. (2019). Modelling and optimal lot-sizing of integrated multi-level multi-wholesaler supply chains under the shortage and limited warehouse space: Generalised outer approximation. International Journal of Systems Science: Operations and Logistics, 6(3), 237–257. https://doi.org/https://doi.org/10.1080/23302674.2018.1435835

- Huo, B., Han, Z., & Prajogo, D. (2016). Antecedents and consequences of supply chain information integration: A resource-based view. Supply Chain Management: An International Journal, 21(6), 661–677. https://doi.org/https://doi.org/10.1108/SCM-08-2015-0336

- Katayama, H., & Bennett, D. (1999). Agility, adaptability and leanness: A comparison of concepts and a study of practice. International Journal of Production Economics, 60, 43–51. https://doi.org/https://doi.org/10.1016/S0925-5273(98)00129-7

- Kazemi, N., Abdul-Rashid, S. H., Ghazilla, R. A. R., Shekarian, E., & Zanoni, S. (2018). Economic order quantity models for items with imperfect quality and emission considerations. International Journal of Systems Science: Operations and Logistics, 5(2), 99–115. https://doi.org/https://doi.org/10.1080/23302674.2016.1240254

- Ketchen, D. J., & Hult, G. T. M. (2007). Bridging organization theory and supply chain management: The case of best value supply chains. Journal of Operations Management, 25(2), 573–580. https://doi.org/https://doi.org/10.1016/j.jom.2006.05.010

- Koufteros, X., Vonderembse, M., & Jayaram, J. (2005). Internal and external integration for product development: The contingency effects of uncertainty, equivocality, and platform strategy. Decision Sciences, 36(1), 97–133. https://doi.org/https://doi.org/10.1111/j.1540-5915.2005.00067.x

- Koufteros, X. A., Rawski, G. E., & Rupak, R. (2010). Organizational integration for product development: The effects on glitches, on-time execution of engineering change orders, and market success. Decision Sciences, 41(1), 49–80. https://doi.org/https://doi.org/10.1111/j.1540-5915.2009.00259.x

- Ku, E. C. S., Wu, W.-C., & Chen, Y. J. (2015). customer orientation, and operational performance : The effect of flexibility. Information Systems and E-Business Management, 14(1). https://doi.org/https://doi.org/10.1007/s10257-015-0289-0

- Lai, F., Zhang, M., Lee, D. M. S., & Zhao, X. (2012). The impact of supply chain integration on mass customization capability: An extended resource-based view. IEEE Transactions on Engineering Management, 59(3), 443–456. https://doi.org/https://doi.org/10.1109/TEM.2012.2189009

- Lavie, D. (2006). The competitive advantage of interconnected firms: An extension of the resource-based view. Academy of Management Review, 31(3), 638–658. https://doi.org/https://doi.org/10.5465/amr.2006.21318922

- Lee, H. L. (2004). The triple-A supply chain. Harvard Business Review, 82(10), 102–113. http://www.scap.pk/article/SupplyChaindd.pdf

- Leuschner, R., Rogers, D. S., & Charvet, F. F. (2013). A meta-analysis of supply chain integration and firm performance. Journal of Supply Chain Management, 49(2), 34–57. https://doi.org/https://doi.org/10.1111/jscm.12013

- Li, S., Ragu-Nathan, B., Ragu-Nathan, T. S., & Rao, S. S. (2006). The impact of supply chain management practices on competitive advantage and organizational performance. Omega, 34(2), 107–124. https://doi.org/https://doi.org/10.1016/j.omega.2004.08.002

- Martinez-Sanchez, A., & Lahoz-Leo, F. (2018). Supply chain agility: A mediator for absorptive capacity. Baltic Journal of Management, 13(2), 264–278. https://doi.org/https://doi.org/10.1108/BJM-10-2017-0304

- McIvor, R. (2001). Lean supply: The design and cost reduction dimensions. European Journal of Purchasing & Supply Management, 7(4), 227–242. https://doi.org/https://doi.org/10.1016/S0969-7012(01)00004-1

- Melnyk, S. A., Hanson, J. D., & Calantone, R. J. (2010). Hitting the target … but missing the point: Resolving the paradox of strategic transition. Long Range Planning, 43(4), 555–574. https://doi.org/https://doi.org/10.1016/j.lrp.2009.11.004

- Monczka, R. M., Callahan, T. J., & Nichols, E. L. (1995). Predictors of relationships among buying and supplying firms. International Journal of Physical Distribution & Logistics Management, 25(10), 45–59. https://doi.org/https://doi.org/10.1108/09600039510101799

- Narasimhan, R., Swink, M., & Viswanathan, S. (2010). On decisions for integration implementation: An examination of complementarities between product‐Process technology integration and supply chain integration. Decision Sciences, 41(2), 355–372. https://doi.org/https://doi.org/10.1111/j.1540-5915.2010.00267.x

- Nawanir, G., Lim, K. T., & Othman, S. N. (2016). Lean manufacturing practices in Indonesian manufacturing firms: Are there business performance effects? International Journal of Lean Six Sigma, 7(2), 149–170. https://doi.org/https://doi.org/10.1108/IJLSS-06-2014-0013

- Nawanir, G., Teong, L. K., & Othman, S. N. (2013). Impact of lean practices on operations performance and business performance: Some evidence from Indonesian manufacturing companies. Journal of Manufacturing Technology Management, 24(7), 1019–1050. https://doi.org/https://doi.org/10.1108/JMTM-03-2012-0027

- Payne, A., & Frow, P. (2005). A strategic framework for customer relationship management. Journal of Marketing, 69(4), 167–176. https://doi.org/https://doi.org/10.1509/jmkg.2005.69.4.167

- Perez-Franco, R., Phadnis, S., Caplice, C., & Sheffi, Y. (2016). Rethinking supply chain strategy as a conceptual system. International Journal of Production Economics, 182, 384–396. https://doi.org/https://doi.org/10.1016/j.ijpe.2016.09.012

- Prajogo, D., Oke, A., & Olhager, J. (2016). Supply chain processes: Linking supply logistics integration, supply performance, lean processes and competitive performance. International Journal of Operations & Production Management, 36(2), 220–238. https://doi.org/https://doi.org/10.1108/IJOPM-03-2014-0129

- Qi, Y., Boyer, K. K., & Zhao, X. (2009). Supply chain strategy, product characteristics, and performance impact: Evidence from Chinese manufacturers. Decision Sciences, 40(4), 667–695. https://doi.org/https://doi.org/10.1111/j.1540-5915.2009.00246.x

- Qi, Y., Huo, B., Wang, Z., & Yan, H. (2017). The impact of operations and supply chain strategies on integration and performance. Intern. Journal of Production Economics, 185, 162–174. https://doi.org/https://doi.org/10.1016/j.ijpe.2016.12.028

- Qi, Y., Zhao, X., & Sheu, C. (2011). The impact of competitive strategy and supply chain strategy on business performance: The role of environmental uncertainty. Decision Sciences, 42(2), 371–389. https://doi.org/https://doi.org/10.1111/j.1540-5915.2011.00315.x

- Qrunfleh, S., & Tarafdar, M. (2013). Lean and agile supply chain strategies and supply chain responsiveness : The role of strategic supplier partnership and postponement. Supply Chain Management: An International Journal, 6(18), 571–582. https://doi.org/https://doi.org/10.1108/SCM-01-2013-0015

- Qrunfleh, S., & Tarafdar, M. (2014). Supply chain information systems strategy: Impacts on supply chain performance and firm performance. International Journal of Production Economics, 147(PART B), 340–350. https://doi.org/https://doi.org/10.1016/j.ijpe.2012.09.018

- Rabbani, M., Foroozesh, N., Mousavi, S. M., & Farrokhi-Asl, H. (2019). Sustainable supplier selection by a new decision model based on interval-valued fuzzy sets and possibilistic statistical reference point systems under uncertainty. International Journal of Systems Science: Operations and Logistics, 6(2), 162–178. https://doi.org/https://doi.org/10.1080/23302674.2017.1376232

- Rabbani, M., Hosseini-Mokhallesun, S. A. A., Ordibazar, A. H., & Farrokhi-Asl, H. (2020). A hybrid robust possibilistic approach for a sustainable supply chain location-allocation network design. International Journal of Systems Science: Operations and Logistics, 7(1), 60–75. https://doi.org/https://doi.org/10.1080/23302674.2018.1506061

- Ralston, P. M., Blackhurst, J., Cantor, D. E., & Crum, M. R. (2015). A structure–conduct–performance perspective of how strategic supply chain integration affects firm performance. Journal of Supply Chain Management, 51(2), 47–64. https://doi.org/https://doi.org/10.1111/jscm.12064

- Restuputri, D. P., Masudin, I., Sari, C. P., & Tan, A. W. K. (2020). Customers perception on logistics service quality using Kansei engineering: Empirical evidence from indonesian logistics providers. Cogent Business and Management, 7(1), 1751021. https://doi.org/https://doi.org/10.1080/23311975.2020.1751021

- Roh, J., Hong, P., & Min, H. (2014). Implementation of a responsive supply chain strategy in global complexity: The case of manufacturing firms. International Journal of Production Economics, 147(PART B), 198–210. https://doi.org/https://doi.org/10.1016/j.ijpe.2013.04.013

- Saeed, K. A., Malhotra, M. K., & Grover, V. (2011). Interorganizational system characteristics and supply chain integration: An empirical assessment. Decision Sciences, 42(1), 7–42. https://doi.org/https://doi.org/10.1111/j.1540-5915.2010.00300.x

- Sarkar, S., & Giri, B. C. (2020). Stochastic supply chain model with imperfect production and controllable defective rate. International Journal of Systems Science: Operations and Logistics, 7(2), 133–146. https://doi.org/https://doi.org/10.1080/23302674.2018.1536231

- Sayyadi, R., & Awasthi, A. (2018). A simulation-based optimisation approach for identifying key determinants for sustainable transportation planning. International Journal of Systems Science: Operations and Logistics, 5(2), 161–174. https://doi.org/https://doi.org/10.1080/23302674.2016.1244301

- Sayyadi, R., & Awasthi, A. (2020). An integrated approach based on system dynamics and ANP for evaluating sustainable transportation policies. International Journal of Systems Science: Operations and Logistics, 7(2), 182–191. https://doi.org/https://doi.org/10.1080/23302674.2018.1554168

- Shah, N. H., Chaudhari, U., & Cárdenas-Barrón, L. E. (2020). Integrating credit and replenishment policies for deteriorating items under quadratic demand in a three echelon supply chain. International Journal of Systems Science: Operations and Logistics, 7(1), 34–45. https://doi.org/https://doi.org/10.1080/23302674.2018.1487606

- Shashi, Centobelli, P., Cerchione, R., & Singh, R. (2019). The impact of leanness and innovativeness on environmental and financial performance: Insights from Indian SMEs. International Journal of Production Economics, 212(December2017), 111–124. https://doi.org/https://doi.org/10.1016/j.ijpe.2019.02.011

- Sim, K. L., & Curatola, A. P. (1999). Time‐based competition. International Journal of Quality & Reliability Management,16(7), 659-674.. https://doi.org/https://doi.org/10.1108/02656719910268215

- Stavrulaki, E., & Davis, M. (2010). Aligning products with supply chain processes and strategy. The International Journal of Logistics Management, 21(1), 127–151. https://doi.org/https://doi.org/10.1108/09574091011042214

- Subburaj, A., Sriram, V. P., & Mehrolia, S. (2020). Effects of supply chain integration on firm’s performance: A study on micro, small and medium enterprises in India. Uncertain Supply Chain Management, 8(1), 231–240. https://doi.org/https://doi.org/10.5267/j.uscm.2019.7.001

- Sugeng, S., Nugroho, M. N., Ibrahim, I., & Yanfitri, Y. (2010). Effects of foreign exchange supply and demand dynamics to Rupiah Exchange Rate and Economic Performance. Buletin Ekonomi Moneter Dan Perbankan, 12(3), 289–328. https://doi.org/https://doi.org/10.21098/bemp.v12i3.374

- Swafford, P. M., Ghosh, S., & Murthy, N. (2006). The antecedents of supply chain agility of a firm: Scale development and model testing. Journal of Operations Management, 24(2), 170–188. https://doi.org/https://doi.org/10.1016/j.jom.2005.05.002

- Swink, M., Narasimhan, R., & Wang, C. (2007). Managing beyond the factory walls: Effects of four types of strategic integration on manufacturing plant performance. Journal of Operations Management, 25(1), 148–164. https://doi.org/https://doi.org/10.1016/j.jom.2006.02.006

- Tarafdar, M., & Qrunfleh, S. (2017). Agile supply chain strategy and supply chain performance: Complementary roles of supply chain practices and information systems capability for agility. International Journal OfProduction Research, 55(4), 925–938. https://doi.org/https://doi.org/10.1080/00207543.2016.1203079

- Tsao, Y. C. (2015). Design of a carbon-efficient supply-chain network under trade credits. International Journal of Systems Science: Operations and Logistics, 2(3), 177–186. https://doi.org/https://doi.org/10.1080/23302674.2015.1024187

- Tse, Y. K., Zhang, M., Akhtar, P., & MacBryde, J. (2016). Embracing supply chain agility: An investigation in the electronics industry. Supply Chain Management: An International Journal, 21(1), 140–156. https://doi.org/https://doi.org/10.1108/SCM-06-2015-0237

- Um, J. (2017). The impact of supply chain agility on business performance in a high level customization environment. Operations Management Research, 10(1–2), 10–19. https://doi.org/https://doi.org/10.1007/s12063-016-0120-1

- Vickery, S. K., Droge, C., Setia, P., & Sambamurthy, V. (2010). Supply chain information technologies and organisational initiatives: Complementary versus independent effects on agility and firm performance. International Journal of Production Research, 48(23), 7025–7042. https://doi.org/https://doi.org/10.1080/00207540903348353

- Vickery, S. K., Jayaram, J., Droge, C., & Calantone, R. (2003). The effects of an integrative supply chain strategy on customer service and financial performance: An analysis of direct versus indirect relationships. Journal of Operations Management, 21(5), 523–539. https://doi.org/https://doi.org/10.1016/j.jom.2003.02.002

- Wahyuni, D., Sudira, P., Agustini, K., & Ariadi, G. (2020). The effect of external learning on vocational high school performance with mediating role of in- structional agility and product innovation efficacy in Indonesia. Management Science Letters, 10(16), 3931–3940. https://doi.org/https://doi.org/10.5267/j.msl.2020.7.017

- Whitten, G. D., Green, K. W., & Zelbst, P. J. (2012). Triple‐A supply chain performance. International Journal of Operations & Production Management., 32(1), 28-48. https://doi.org/https://doi.org/10.1108/01443571211195727

- Wiengarten, F., Humphreys, P., Gimenez, C., & McIvor, R. (2016). Risk, risk management practices, and the success of supply chain integration. International Journal of Production Economics, 171(3), 361–370. https://doi.org/https://doi.org/10.1016/j.ijpe.2015.03.020

- Wong, C. Y., Boon-Itt, S., & Wong, C. W. Y. (2011). The contingency effects of environmental uncertainty on the relationship between supply chain integration and operational performance. Journal of Operations Management, 29(6), 604–615. https://doi.org/https://doi.org/10.1016/j.jom.2011.01.003

- Yin, S., Nishi, T., & Zhang, G. (2016). A game theoretic model for coordination of single manufacturer and multiple suppliers with quality variations under uncertain demands. International Journal of Systems Science: Operations and Logistics, 3(2), 79–91. https://doi.org/https://doi.org/10.1080/23302674.2015.1050079

- Yusuf, Y. Y., Gunasekaran, A., Adeleye, E. O., & Sivayoganathan, K. (2004). Agile supply chain capabilities: Determinants of competitive objectives. European Journal of Operational Research, 159(2), 379–392. https://doi.org/https://doi.org/10.1016/j.ejor.2003.08.022

- Zhao, G., Feng, T., & Wang, D. (2015). Is more supply chain integration always beneficial to financial performance?. Industrial Marketing Management, 45, 162–172.

- Zhao, X., Huo, B., Selen, W., & Yeung, J. H. Y. (2011). The impact of internal integration and relationship commitment on external integration. Journal of Operations Management, 29(1–2), 17–32. https://doi.org/https://doi.org/10.1016/j.jom.2010.04.004