Abstract

The difference in purchase behavior between male and female consumers is a well-established narrative because of the considerable differences in their buying preferences and decision-making approaches. Women buyer market for financial products is an untapped yet promising segment, however, beyond certain generic assumptions, very little is known about the consumer behavior patterns, satisfaction, and positive word of mouth (WOM) of women customers related to financial products. Targeting a serving woman as a financial service customer necessitates an understanding of the factors contributing to satisfaction level leading to the positive WOM of female customers. Therefore, this paper is an effort to explore the role of the responsiveness component of service quality and sincerity dimension of brand personality on WOM via customer satisfaction. Using the partial least square method in structural equation modeling (PLS-SEM) on 183 working women respondents in India, the research results highlighted some interesting findings. Results revealed that brand sincerity directly impacts the WOM of the women customers where achieving satisfaction is not necessary; however, the responsiveness of a financial product does not directly lead to a positive WOM, rather through satisfaction. The research is novel in empirically testing and comparing the role of brand sincerity and responsiveness in generating satisfaction and positive WOM. This study provides insights for the financial product designers and marketers intending to target women-customers, by focusing on the specific consumer behavioral dimensions leading to satisfaction and positive WOM to ensure the product success.

PUBLIC INTEREST STATEMENT

Women customers of financial products are an untapped yet promising segment. Targeting a serving woman necessitates the need to understand various factors contributing to satisfaction levels leading to the positive word of mouth (WOM). Therefore, this study postulates the impact of brand sincerity and responsiveness in establishing a direct or indirect word of mouth with mediating impact of customer satisfaction. Using a sample of 183 working women respondents in India, the research results highlighted some interesting findings: brand sincerity was found to have a direct impact on the WOM of the women customers where achieving satisfaction was not validated for a positive WOM generation. However, the responsiveness of a financial brand was found not directly leading to a positive WOM, rather the presence of satisfaction was deemed necessary towards establishing a positive WOM. This study provides valuable insights for the financial product designers and marketers intending to target women customers by focusing on the specific consumer behavioral dimensions leading to satisfaction and positive WOM.

1. Introduction

The financial sector is one of those sectors where drastic changes have been reported overthe last couple of decades. Factors like technological advancements, digitalization, local and international regulations, and globalization have made it a highly competitive sector (Alt et al., Citation2018; Weqar et al., Citation2020). Consumer behavior in the financial sector has been reported to be an area where the major shift has happened and price sensitivity (Liu & Lee, Citation2016) and customer loyalty have increased over time (Kasasbeh et al., Citation2017; Lymperopoulos & Chaniotakis, Citation2008). It has been debated that customer satisfaction determines the future course of action of the customers (Eren, Citation2021); therefore, institutions specifically focus on formulating strategies to retain customers by enhancing customer satisfaction (Ramanathan et al., Citation2018).

Apart from customer satisfaction, WOM is also considered a powerful tool through which the customers express their views and about a product or service (Chang & Chieng, Citation2006). WOM plays a significant role in attracting or repelling potential customers (Bruwer & Buller, Citation2012; Wang & Yang, Citation2011). There is abundant literature available on the importance of WOM; where various variables have been studied to have a positive impact on WOM in the financial sector (Oraedu et al., Citation2020; Salehnia et al., Citation2014, April). Customer satisfaction itself is reported to have an impact on positive WOM (Anderson, Citation1998). However, ensuring customer satisfaction and ensuring customers’ positive WOM and is a complex path, there are multiple routes and variable tested to be involved in various forms where multidimensional research is available on identifying the elements contributing towards customer satisfaction and positive WOM for financial services (Anderson, Citation1998; Ashtiani & Iranmanesh, Citation2012; Bolia et al., Citation2016, Citation2020; Salehnia et al., Citation2014, April). Brand personality and service quality are two of the key concepts which are reported to be critical while deciding customer satisfaction, retention, and WOM (Chaniotakis & Lymperopoulos, Citation2009; Narteh, Citation2018; Shanka, Citation2012). Service quality and brand personality have been highlighted as essential contributors towards customer satisfaction in the financial sector thus playing a major role in establishing a competitive advantage (Almossawi, Citation2001; Ozbekler & Ozturkoglu, Citation2020; Rezaei et al., Citation2016). Additionally, research also suggests the service quality and brand personality impact the WOM of the products of institutions positively (Chaniotakis & Lymperopoulos, Citation2009; Mukerjee, Citation2018; Siddiqi, Citation2011). The impact of service quality and brand personality has also been researched for impacting positively on customer services, and WOM has also been reported to have increased significantly because of increased customer satisfaction (Mohtasham et al., Citation2017; Mukerjee, Citation2018; Sivadas & Jindal, Citation2017).

Service quality (ServQual) has become an important concept since it was first introduced by (Parasuraman et al., Citation1988). Service quality refers to the customers’ assessment of the perceived quality of service delivered by the businesses in comparison with the preconceived customer expectations (Lai & Hitchcock, Citation2016). The assessment helps businesses plan, manage and improve the quality of their services. In the case of purely service-oriented businesses like financial institutions, the importance of perception of service quality is even more significant (Lebdaoui & Chetioui, Citation2020). Various researchers have researched the ServQual model in various contexts and sectors generally and in financial sectors particularly (Allred & Addams, Citation2000; Arasli et al., Citation2005; Boyd et al., Citation1994; Chaniotakis & Lymperopoulos, Citation2009; Gounaris et al., Citation2003; Ramanathan et al., Citation2018; Shi & Shang, 2020; Sohn & Tadisina, Citation2008). The original ServQual model addresses various service dimensions that includes reliability, assurance, tangibles, empathy and responsiveness (Parasuraman et al., Citation1988). Various researchers have identified positive linkages between various dimensions of service quality, customer satisfaction, and WOM (Alrwashdeh et al., Citation2020; Mukerjee, Citation2018; Pranoto et al., Citation2020). Each of these dimensions is important and has a precise role to play in deciding the customer satisfaction and WOM; therefore, an in-depth analysis of the impact of each of the dimensions separately provides explicit insight into their effect on customers. Responsiveness is one of the dimensions that has been studied to have a positive impact on customer satisfaction and WOM (Brown & Beltramini, Citation1989; Grandey et al., Citation2011; Smart & Martin, Citation1992). This research paper specifically studies the responsiveness dimension of ServQual and its impact on WOM.

Similarly, another area that has been researched to have a deeper impact on consumer behavior is brand personality. Brand personality is a concept that helps the organizations identify the perception of the consumer about the brand image of their products, services, or overall mission that helps a company or organization shape the way people feel about its product, service, or mission (Aaker, Citation1997; Beldona & Wysong, Citation2007). An organization’s brand personality emotionally elicits the consumers towards the product and services and generates satisfaction and loyalty (Magin et al., Citation2003; O’Neill & Carlbäck, Citation2011). Brand personalities of various products and services can be differentiated based on various factors such as excitement, sincerity, ruggedness, competence and sophistication (Aaker, Citation1997). Each of the factors has a unique role in defining the personality of the products or services and having an impact on customer satisfaction and the WOM of the customer (Hultman et al., Citation2015; Mandal et al., Citation2021). Some of the factors have been studied by various researchers both collectively as to establish an overall picture of the financial brands or separately to identify the specific role each factor plays in defining the personality of products or services; where each dimension has been reported to have a different magnitude impact (Hultman et al., Citation2015; Ismail & Spinelli, Citation2012; Madrigal & Boush, Citation2008; So et al., Citation2017; Taheri et al., Citation2018). The literature suggests that sincerity is the strongest and most influential dimension of brand personality (Folse et al., Citation2012; Sung & Kim, Citation2010). Although the sincerity dimension has specifically been researched in various sectors (Braunstein & Ross, Citation2010; Demirel & Erdogmus, Citation2016; Perepelkin & Zhang 2014); however, to the best of our knowledge, it has not been researched concerning financial services. Therefore, it is important to understand the impact sincerity dimension specifically in the context of financial services. Hence, this study specifically considers the sincerity dimension of brand personality and its role in building customer satisfaction and WOM for customers in financial institutions.

Financial services have become more customized according to the specific needs of the various market segments (Germain, Citation2000). One of the underserved segments of the financial sector is the female customers, where the financial sector has been predominantly focusing on men as its prime customers (Driva et al., Citation2016; Feldman, 2002; Women in Financial Services, Citation2020). Although, as buyers, women have reported having an influential role to play; however, the focus on meeting their specific needs has not been addressed much (Feldman, 2002; Women in Financial Services, Citation2020). It has been observed that females in emerging economies are becoming financially independent, well-informed, and educated, thus their decisions and choices should also specifically be focused (Bucher-Koenen et al.,Citation2017; Driva et al., Citation2016). As per statistics, in the financial sector, the purchase behavior of women is an important factor to consider which can promise a potential revenue of 700 USD billion; this is an opportunity which, at present, is majorly overlooked (Feldman, 2002; Women in Financial Services, Citation2020). Furthermore, the financial market appears to operate gender-neutral, rather biased towards meeting male customers’ choices and needs. It can safely be said that the gender segmentation based on the biological sex generally, and meeting the needs of female customers particularly, is a blind spot in the financial sector which needs practitioners’ attention (Feldman, 2002; Kofman & Payne, Citation2020). Therefore, this study hypothesizes that female customers will speak positively about the product if they experience responsiveness and sincerity in financial services. The purpose of this research paper is to identify the relationship between brand responsiveness and brand sincerity in the WOM of female customers of the financial products while considering the satisfaction of female customers playing to be a mediating role.

2. Literature review and hypotheses development

2.1. Service quality and customer satisfaction

There is overwhelming literature support available concerning service quality and customer satisfaction of financial services (Al-Salem & Mostafa, Citation2019; Avkiran, Citation1994; Bakar et al., Citation2019; Bolton & Drew, Citation1991; Cadotte et al., Citation1987; Devesh, Citation2019; Levesque & McDougall, Citation1996; Pakurár et al., Citation2019; Suciptawati et al., Citation2019; Vencataya et al., Citation2019). It has been frequently debated that customer satisfaction is increased because of high perceived service quality (Gounaris et al., Citation2003; Parasuraman et al., Citation1988), which defines the strong relationship between the two. Moreover, the literature also debates that the two concepts are conceptually distinct from each other, however, at the same time are closely related; where in the case of higher service quality, customer satisfaction also increases (Devesh, Citation2019; Pakurár et al., Citation2019; Parasuraman et al., Citation1988). Following the same direction, numerous studies have identified and tested the significant positive relationship between the two, specifically in the financial institutions (Bakar et al., Citation2019; Razak et al., Citation2007; Sulistiyawan et al., Citation2019). It is therefore suggested by many that to enhance customer satisfaction, the financial institutions should focus on providing better service quality (Devesh, Citation2019; Sivesan, Citation2019). Targeting service quality will not only provide long-term benefits to the business but will also provide a competitive advantage (Wang et al., Citation2003). Within financial institutions, different types of institutions are researched to establish the service quality and satisfying relationships. Sivesan (Citation2019) investigated the relationship between the two in the specific context of insurance companies. There have been numerous studies conducted on the service quality and customer satisfaction of banking customers, proving it to be a strong relation (Devesh, Citation2019; Endara et al., Citation2019; Li et al., Citation2021; Pakurár et al., Citation2019; Razak et al., Citation2007). Ramanathan et al. (Citation2018) compared the customers of leasing contracts in public and private sectors and suggested responsiveness and assurance be the most important dimensions ensuring an indirect relationship with customer satisfaction. Moreover, even within the banking sector, product-specific research like sharia banking service has been tested; there also the relationship between the two has even proven to be highly significant (Bakar et al., Citation2019; Suciptawati et al., Citation2019). Likewise, the service quality and satisfaction are reported to be harmonious in online and e-banking segments too (Shankar & Jebarajakirthy, Citation2019; Shared, Citation2019).

2.2. Service quality and WOM

The financial service institutions are one of those sectors where WOM is reported to have a tremendous potential to reach out to customers (Choudhury, Citation2014). Various factors including customer satisfaction and service quality have been researched to identify their relationship with WOM (Alrwashdeh et al., Citation2020; Anderson, Citation1998; Ashtiani & Iranmanesh, Citation2012; Choudhury, Citation2014; Salehnia et al., 2014; Rajaobelina et al., Citation2021). Literature suggests that WOM is a two-tiered phenomenon; in the presence of superior quality service it ensures the positive WOM from the customers; however, in the case of low service quality, research suggests, it is likely that customers will engage in negative word of mouth (Chaniotakis & Lymperopoulos, Citation2009). This means that if an institution fails to meet the service quality expectations of the customers, it is more prone to negative WOM as compared to those with superior quality offerings ; in both cases, service quality proves a relationship with the WOM. There are numerous researches on financial institutions, debating on the role of service quality in creating positive WOM, reducing the customers’ complaints, and strengthening the customer relations (Choudhury, Citation2014; Wangenheim & Bayón, Citation2004; Yavas et al., Citation2004). Apart from research in the financial sector, the service quality and WOM studies have also shown positive correlations in other sectors. Alexandris et al. (Citation2002) conducted research on the hotel industry studying the relationship between service quality and WOM; their results suggested a positive relationship between the two; however, the tangible dimension was the only dimension where the positive correlation was not established. Similarly, a study conducted by Amin and Nasharuddin (Citation2013) concluded that higher service delivery in hospitals leads to customer satisfaction and positive behavioral intentions including WOM. In addition, the relationship between the duo has also been reported to be significantly positive in the education industry (Smith & Ennew, Citation2001). The literature also advocates the correlation of service quality with various behavioral factors including WOM; directly or with the mediating intervention of customer satisfaction (Caruana, Citation2002; Chaniotakis & Lymperopoulos, Citation2009; Cronin et al., Citation2000; Cronin & Taylor, Citation1992; Santika et al., Citation2020). It has also been supported in the literature that service quality and customer services in various arrangements endorse the positive WOM (Lovelock et al., Citation1996).

2.3. Responsiveness in service quality

Responsiveness in service refers to the disposition to serve the customers promptly. It refers to the organization’s attentiveness and speediness while handling customers’ queries, being available, handling customer calls, requests, issues, and complaints (Ahearne et al., Citation2007). The organization’s timely response and flexibility determine the responsiveness in service. Responsiveness is an acknowledged service concept in the financial industry. Various researchers have highlighted that since the competition has soared because of the influence of technological changes, it has become extremely important for institutions to adopt agility and responsiveness (Islam et al., Citation2020; Malhotra & Mukherjee, Citation2004; Mariappan, Citation2006; Zhu et al., Citation2002). Responsiveness in the financial sector has been tested in various forms in the literature. Crosby et al. (Citation1990) suggested that in life insurance services, the repeated contact and salespersons’ expression of inclination to offer help to customers is pivotal in establishing a customer relationship. It has also been emphasized that financial institutions like banks are using information technology to offer consistently quick and timely responses to the customers’ requests, which leads to enhanced customer satisfaction (Iberahim et al., Citation2016). Likewise, a study by Chompis et al. (Citation2012) stressed that responsiveness in financial services builds trust in customers, which, as a result, contributes towards establishing customer satisfaction. In other sectors also, research testifies that responsiveness is one of the most significant service factors that lead to customer satisfaction substantially (Andaleeb & Conway, Citation2006). Literature suggests that responsive companies not only delight the customers but also persuade customers to buy back (Smart & Martin, Citation1992). Similarly, researchers have established a very strong direct relationship between responsiveness and customer satisfaction (Agnihotri et al., Citation2016; Shanka, Citation2012). Furthermore, literature also suggests that if a customer feels unwelcomed, gets disenchanted and will shift to some other business whenever possible (Keaveney, Citation1995). Likewise, the responsiveness path has also been studied at a deeper level, where, it has been reported that the satisfied employees of organizations will be more responsive towards customers, which in turn will positively impact customer satisfaction (Grandey et al., Citation2011; Hong et al., Citation2013). Similarly, Bitner et al. (Citation1990) advocates that employees’ voluntary positive and welcoming response including offering service more than asked and giving special attention to customers leaves a positive memory, whereas employees’ unsolicited response such as rudeness, irritation results in dissatisfactory experience. Besides, the literature also suggests that the customers’ eWOM response is stimulated by the online responsiveness in the service sector, where customers are well prepared for expressing their positive experience or otherwise (Choi et al., Citation2018; Sheng, Citation2019). In this context, the speed of response is a critical factor that encourages customers to leave written feedback and comments (Sheng, Citation2019). Additionally, the literature also refers that responsiveness has an indirect relationship with WOM (WOM), where customer satisfaction mediates the relationship between the two (Chaniotakis & Lymperopoulos, Citation2009). Another reported outcome of responsiveness is time-saving, the prompt service and quick response by the employee save time. Time costs are charged to organizations who lack responsiveness which has a significant impact on customers’ perceived value (Leclerc et al., Citation1995; Naylor & Frank, Citation2000), congruently, absence of responsiveness also triggers various psychological costs including anxiety, boredom, irritation, and stress that adversely impacts customer satisfaction and repurchase decision (Carmon et al., Citation1995; Kumar et al., Citation1997). Henceforth, literature verifies responsiveness to be a critical dimension in service quality (Berry et al., Citation2002; Theoharakis & Hooley, Citation2003).

Although the relationship between service quality, customer satisfaction, and WOM has been researched in abundance; however, works of the literature suggest that there is still a huge research gap, where each dimension of service quality should be hypothesized to have an impact on various arrangements of the relationship between customer satisfaction and WOM (Chaniotakis & Lymperopoulos, Citation2009; Choudhury, Citation2014; Schlesinger et al., Citation2021). Therefore, this study is an effort to hypothesize the dimension (responsiveness) specific relationship of service quality with customer satisfaction and WOM. Henceforth, based on the literature support on responsiveness, customer service, and WOM following hypotheses are developed.

H1: Responsiveness has a significant impact on Customer Satisfaction

H2: Responsiveness has a significant impact on WOM

H3: Customer Satisfaction mediated the relationship between Responsiveness and WOM

2.4. Brand personality and customer satisfaction

Brand personality and customer satisfaction had been widely documented in various studies, where a positively perceived brand personality has been reported as a consistent and significant contributor towards customer satisfaction (Achouri & Bouslama, Citation2010; Hultman et al., Citation2015; Kim & Lee, Citation2008; Kwong & Candinegara, Citation2014; Memon, Citation2021; Su & Tong, Citation2016). Literature advocates that brand personality is a powerful marketing tool through which businesses can attain their satisfaction objectives (Hans & Anamaria, Citation2001). Various studies have also predicted for brand personality to have a relationship with customer loyalty (Ekinci et al., Citation2007; Perepelkin & Zhang, 2014). Researchers have also predicted brand personality to have a strong association with human personality while establishing customer satisfaction towards a brand (Park & Lee, Citation2005). Similarly, in a study conducted by Kim (Citation2013) brand personality was found to be critical in establishing customer satisfaction and brand equity, where brand personality was a means of creating differentiation in the coffee market. Moreover, numerous studies have researched the relationship between self-image, brand personability, and customer satisfaction; where post-purchase behaviors have been the focus of most of these studies (Graeff, Citation1996; Sirgy, Citation1982). Similarly, the congruence of self-image on satisfaction has been a topic of debate in many pieces of research, and a significant positive correlation has been reported (Chon, Citation1990; Jamal & Goode, Citation2001; Smith, Citation2020). Brand personality in the financial sector has not been a much-researched area. Very few studies are available where these two concepts are researched specifically in the financial services context. Shetty and Rodrigues (Citation2017) conducted a study to explore the brand personality effect on post-purchase evaluation and customer satisfaction in the banking sector; data analysis of 500 banking customers resulted in proving a significant positive relationship between brand personality, satisfaction, and brand loyalty. Similarly, another study was conducted by Ong et al. (Citation2017), discusses the e brands or virtual brand personalities in congruence with customer satisfaction in the online banking environment; their research proposes a significant positive relationship between some dimensions of brand personality and customer satisfaction and loyalty. They further highlight that although the sincerity dimension seems to be relevant in an online environment, the data result for sincerity was insignificant in their study; however, they urged to study all the dimensions in detail and in different contexts to uncover the impact of brand personality in creating customers’ satisfaction and loyalty (Ong et al., Citation2017).

2.5. Brand personality and WOM

Word of mouth (WOM) has been widely advocated to play a significant role in influencing customer’s post-purchase behavior and choices (Hennig-Thurau et al., Citation2003; Kim et al., Citation2011). WOM has been reported to be the most influential form of all other types of communication (Herr et al., Citation1991). Research supports that even in case the details of the offer are available to customers, the positive attitude towards brands is often established based on positive WOM (Mangold et al., Citation1999). The brand personality triggers the customers’ positive feelings towards the brand (Orth et al., Citation2010), thus ensures positive WOM (Mandal et al., Citation2021). The relationship between brand personality and WOM has been hypothesized with various dimensions of brand personality, individually or in groups. For example, Meiske and Balqiah (Citation2019) hypothesized the impact of 5 dimensions of brand personality on brand love, brand loyalty, and WOM in the online retailer context; the researchers analyzed the data from 398 respondents and concluded that three of the brand personalities including, sincerity, sophistication, and competence to have a positive impact on brand loyalty and WOM with the mediating impact of brand love. Similarly, Ismail and Spinelli (Citation2012) and Anggraeni (Citation2015), studied the relationship between the excitement dimension of brand personality, brand love, brand image, and WOM, and concluded that the excitement dimension of brand personality is having a positive impact on WOM. Likewise, Polyorat (Citation2011), researched three dimensions of brand personality to validate the relationship with WOM having a mediating effect on brand identification; the resulting research concluded that sincerity and competence dimensions were strongly associated with WOM through the mediating effect of brand identity. Furthermore, the concept of brand personality has been researched in congruence with human personalities; research conducted by Liao et al., (Citation2015), studies the impact of customers’ personality on WOM by mediating the impact of brand personality. The research suggested that brand personality, as a mediator has a significant impact on WOM; therefore, the brand personalities should carefully be analyzed and understood in detail (Liao et al., Citation2015). Although brand personality and WOM congruence are a fairly popular research topic; however, as per our best knowledge, there is a huge research gap in terms of testing the relationship of this duo in the financial services industry.

2.6. Sincerity in brand personality

The sincerity of a brand refers to the quality of being honest, down-to-earth, cheerful, genuine, and wholesome (Aaker, Citation1997). Sincerity ensures a warm-fuzzies relationship with customers, offering caregiving, honor, trust, and belief. Sincerity has been referred to as one of the success factors needed in salespeople (Perepelkin & Di Zhang, Citation2014). Sincerity in brands is often related to high morals and values (Maehle et al., Citation2011). Research also states that while choosing a service provider, customers not only look for quality but also integrity (Lynch, Citation1993). Various researchers have specifically worked on the sincerity dimension of brand personality in various ways, and reported it to be one of the strongest and most cited dimensions of brand personality (Folse et al., Citation2012; Hoeffler & Keller, Citation2002; Sung & Kim, Citation2010). A few researchers have tested the sincerity dimension in the context of sports brands and proven it to be impacting significantly on the outcomes (Braunstein & Ross, Citation2010; Demirel & Erdogmus, Citation2016). Likewise, literature claims that brands with sincerity and excitement personality dimensions can earn the limelight because they are prominent in the market (Aaker et al., Citation2004; Ching, Citation2009). Sincerity is a topic of research in multiple industries. Some researches have tested the impact of severity on the pharmaceutical industry and emphasized that besides quality, conveying sincerity to establish a rapport with customers is equally important, where sincerity has been reported to significantly mediate the relationship between service quality and customer trust (Perepelkin & Zhang, 2014). Similarly, sincerity has also been a popular area of research in the social media/online business domain, where it has been projected that the social media influencers having high perceived sincerity are reported to build highly positive relations as compared to influencers having low perceived sincerity (Lee & Eastin, Citation2020). Moreover, another popular area where brand sincerity has been reported to have a positive relationship with is corporate social responsibility; where it has been reported that the organizations’ involvement in various CSR initiatives translates into a sincere brand personality (Hoeffler & Keller, Citation2002; Mandal et al., Citation2021; Ragas & Roberts, Citation2009). Brand sincerity is also reported to have a strong impact on customer trust (Perepelkin & Zhang, 2014) and has been tested positively to be a strong mediator between service quality and customer Trust (Perepelkin & Zhang, 2014). This means that the organizations working on service quality to develop customer trust must carefully plan the brand’s sincerity to be successful. Similarly, literature also supports the relationship of brand personality with WOM with the mediating effect of brand identification (Polyorat, Citation2011). In research conducted in the universities, it has been advocated that out of all the dimensions of brand personality, sincerity and competence are the two dimensions that congruence strongly with the WOM, and where brand identification strongly mediated the relationship (Polyorat, Citation2011).

Although brand sincerity has been a popular research topic in various fields; however, to the best of our knowledge, it has not been researched concerning financial services. Therefore, this study specifically focuses on analyzing the impact of sincerity on customer satisfaction and WOM. Similarly, research also suggested the mediating role of a variable in between the relationship of brand personality and WOM (Polyorat, Citation2011); customer satisfaction being a strong aspirant (Achouri & Bouslama, Citation2010; Hultman et al., Citation2015; Kim & Lee, Citation2008; Kwong & Candinegara, Citation2014; Su & Tong, Citation2016). Henceforward, based on the literature review on brand personality, sincerity, customer services, and WOM, the following hypotheses are developed leading to the conceptual model ().

Figure 1. Conceptual model

H4: Sincerity has a significant impact on Customer Satisfaction

H5: Sincerity has a significant impact on WOM

H6: Customer Satisfaction mediated the relationship between Sincerity and WOM

3. Research methodology

Research is an impartial, structured, and sequential method of investigation, directed towards a distinct implicit or explicit objective. This might lead to confirmation of existing propositions or arrival of new philosophies and models (Chawla & Sodhi, Citation2011; Kothari, Citation2004). Research is the original input to the existing stock of knowledge making for its progression. The central premise of this study revolves around the role of women in the decision-making about financial products.

3.1. Research instrument design

Based on a literature review and the conceptual framework with sincere and responsive brands compelling women to talk positively about financial brands, a research questionnaire was designed using existing scales. Validated measures from published literature were used for all variables and the questionnaire was circulated among respondents to test the model as well as the stated hypothesis. Sincerity finds itself among one of the strongest personality constructs to attract customers towards financial brands. Sincerity was explained by eleven items in the brand personality scale (Aaker, Citation1997) and the items were used to measure this variable in the model. Parasuraman et al. (Citation1988) measured responsiveness with four items as a variable in the ServQual scale and the items were used to measure this variable in the model. To measure customer satisfaction of a 3 item and 10-point American Customer Satisfaction Index (ACSI) (Fornell et al., Citation1996). Harrison-Walker (Citation2001) developed and empirically validated a 6-item Scale to measure WOM communication and was found suitable for financial brands in this study.

3.2. Sample and data collection

The respondents chosen for the study had an average age of 28.67 years, a minimum of 21 years, and a maximum of 53 years with maximum respondents belonging to 24 years age group. The sample constituted of all females having educational qualifications of graduation and above and the majority worked for the private sector (78%). The questionnaire was floated to respondents who had bought any financial product in the recent past. The questionnaire was self-administered as well as sent to the prospective respondents through a web-based form, and we used 183 valid responses for analysis using the partial least-squares method for structural equation modeling. Purposive sampling was used, and the sample was chosen on a judgmental basis as all respondents were adults, either had been working executives or earning members or had bought some financial products in the past.

4. Analysis and results

The final data has been pulled into PLS-SEM 3 for doing the final analysis. The accuracy of raw data has been generated through PLS-SEM 3. This software has been widely adopted for statistical analysis (Sarstedt, Citation2008; Urbach & Ahlemann, Citation2010; Vinzi et al., Citation2010). While testing established relationships with normal data researchers suggested the use of the partial least square method in structural equation modeling (PLS-SEM) if there is a limitation in the number of data points collected (Hair Jr et al., Citation2016).

4.1. Reliability & convergent validity

The outer model was assessed first by values of composite reliability (to assess internal consistency), outer loadings (to assess indicator reliability), and average variance extracted (AVE) (to assess convergent validity). Composite reliability is an appropriate measure of internal consistency reliability because it accounts for the different outer loadings of the indicator variables, whereas Cronbach’s alpha assumes all indicators to be equally reliable (Hair et al., Citation2013). Items SN3 (The brand was like a small-town brand) & SN10 (The brand was sentimental) were dropped after the first iteration as the outer loading values were less than 0.60 as desired. The values of Cronbach’s alpha and composite reliability () were found to be greater than the prescribed value of 0.60 (Hair et al., Citation2013) and the values of AVE were found to be greater than 0.50 (Hair et al., Citation2013). The average variance extracted (AVE) is the summary indicator of convergence. AVE values of greater than 0.5 are considered adequate indicating good convergence (Hair et al., Citation2013; Malhotra & Dash, Citation2011).

Table 1. Reliability & convergent validity

(CS–Customer satisfaction; WOM–Word of Mouth; RES–Responsiveness; SN–Sincerity)

4.2 Discriminant validity

As per the Fornell–Larcker Criterion (Ab Hamid et al., Citation2017), discriminant validity denotes the degree to which the concept is dissimilar from one another empirically. The discriminant validity can be assessed using the cross-loading of the indicators. By observing at the cross-loadings, factor loading indicators on the given construct must be higher than all loading of other constructs with the condition that the cut-off value of factor loading is higher than 0.70. Discriminant validity has been addressed successfully in this model ().

Table 2. Discriminant validity

4.3 Model assessment & hypothesis testing

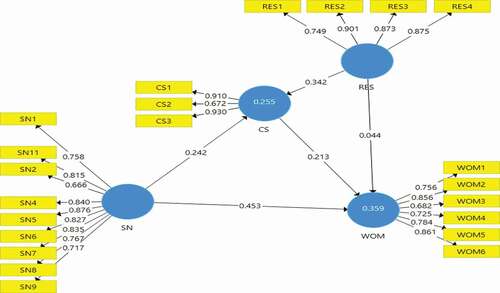

The inner model (structural model) was assessed to test the relationship between the endogenous and exogenous variables. The path coefficients were obtained by applying a non-parametric, bootstrapping routine (Vinzi et al., Citation2010), with 183 cases and 5000 samples for the non-return model (two-tailed; 0.05 significance level). In the model, the endogenous variables (customer satisfaction & WOM) had R2 values of 0.255, and 0.359, respectively, suggesting sufficient predictive accuracy of the structural model ().

Figure 2. Structural equation model

The model fit statistic NFI was observed (0.768) is found to be closer to the desired value of 0.90 & above; however, an important statistic SRMR (0.076) was found to be well within the desired limits of less than 0.08 (Hair Jr et al., 2016). The model seems acceptable based on these statistics.

The hypothesis testing () results conclude that sincere brands are always leading to higher customer satisfaction as well as positive WOM while being a responsive brand results in higher customer satisfaction but not a positive WOM, rather no WOM unless the customer gets satisfied. The model also indicates that in the context of financial brands, customer satisfaction might not lead to WOM unless the brands are sincere, while responsiveness seems to be assumed expectation from the sellers.

Table 3. Path Coefficients and hypothesis testing (Direct Effects)

Table 4. Path coefficients and hypothesis testing (In-Direct Effects/Mediation Effects)

4.4. Common method bias

Probability of common method bias is prevalent in survey-based studies; hence, it becomes imperative to address the same. The common method bias was addressed through two methods- process-based and statistical investigation (Podsakoff et al., Citation2003; Viswanathan & Kayande, Citation2012). The respondents were informed about the purpose and nature of the study. The respondents were also assured about the confidentiality of the responses. There was no compulsion for any respondent to fill out the forms. Some questions were reverse coded on the Likert scale to check uninterested responses. The data collection was done in person by the author as well through social networking sites by connecting with prospective respondents personally; hence, the procedural integrity was not compromised. The study used a full collinearity test in SMART PLS to address common method bias. The occurrence of a VIF (variance inflation factor) greater than 3.3 is proposed as an indication of pathological collinearity, and also as an indication that the model may be contaminated by common method bias. Therefore, if all (factor level) VIFs resulting from a full collinearity test are equal to or less than 3.3, the model can be considered free of common method bias (Kock, Citation2015). The results of the full collinearity test () confirm that the data is not contaminated by common method bias as all Inner VIF values are below 3.3.

Table 5. Full collinearity VIFs

(CS- Customer satisfaction; WOM - Word of Mouth; RES - Responsiveness; SN - Sincerity)

5. Discussion

A seller’s ultimate dream is to maximize WOM for stronger brand equity leading to higher valuations, increased customer base, and higher margins. Customers who feel proud to speak about a brand are willing to pay a premium too for the offerings (Casidy & Wymer, Citation2016). Generating WOM requires many factors and sincerity in all the moment of truths and quick response to the customers’ queries. The research suggested that those unhappy customers who are attended to customers quickly are more prone to convey a positive WOM. Securing a major market share might not result in a strong and preferred brand as the reason might be lower prices or some compelling unavoidable conditions for customers to buy that brand. However, once they get better options, they might dump the brand. Hypothesis 1 stated that responsiveness has a significant impact on customer satisfaction and was supported by the results (β = 0.342, p = .000) which supported the premise that suggested that the repeated contact and salespersons’ expression of inclination to offer help to customers are pivotal in establishing a satisfied customer relationship (Crosby et al., Citation1990). It has also been argued that although high service quality is associated with customer satisfaction, it gets dulled by category attitudes in the financial sector due to disruptive events, however, a responsive attitude helps in bridging the discontent (Farrag et al., Citation2020). The results are also aligned with the proposition that the use of technology to offer consistent and timely responses to customers has enhanced customer satisfaction (Iberahim et al., Citation2016; Islam et al., Citation2020). Hypothesis 2 stated that responsive brands significantly impacted WOM which was not supported in the results (β = 0.044, p = .563) and confirmed the proposition that customers want to experience the journey before speaking good words about a brand (Chaniotakis & Lymperopoulos, Citation2009; Choi et al., Citation2018; Sheng, Citation2019). Researchers in past suggested that convenience during the entire consumer journey plays an important role in customer word of mouth (Ahmadi, Citation2019; Moyes et al., Citation2016), hence in addition to being responsive to the customers, the marketers should plan the service support to ensure convenience to the customers, thereby negating the hypothesis that just being responsive towards customers might significantly impact word of mouth. The customer might be delighted by the quick and timely response by the service providers, however, to speak words of praise, customers need to be satisfied with the products and the entire customer journey, and the results of the study supported hypothesis 3 which stated that customer satisfaction mediated the relationship between responsiveness and WOM (β = 0.073, p = .017), thus, vindicating the past research which suggested customer satisfaction as a moderator in influencing word of mouth (De Matos et al., Citation2009). Hypothesis 4 stated that sincerity has a significant impact on customer satisfaction and was well supported by the results (β = 0.242, p = .003) and confirmed the premise that customers not only look for the quality of products but also integrity (Lynch, 1992). Past research proposed a strong brand-customer relationship as customers are confident about the offerings of the brand, hence indulge in WOM without waiting for the satisfaction, thereby supporting the results of hypothesis 5 (β = 0.453, p = .000) which stated that sincerity has a significant impact on WOM (Braunstein & Ross, Citation2010; Demirel & Erdogmus, Citation2016). Past research also revealed that negative brand ratings affected the word of mouth negatively (Hickman & Ward, Citation2013). The study strongly proposed that sincere brands do not need to wait for satisfying customers before seeking a word of mouth and praise from their customers (β = 0.052, p = .062), also resisting negative information, willingness to pay a premium, and active engagement (Bairrada et al., Citation2019), thereby not supporting the propositions that mediation of customer satisfaction will add to resulting positive WOM (Kim & Lee, Citation2008; Kwong & Candinegara, Citation2014) as stated in hypothesis 6 (Customer Satisfaction mediated the relationship between Sincerity and WOM).

6. Theoretical and managerial implications

A preferred brand needs to create a favorable impression in the minds of women customers (Bakewell & Mitchell, Citation2003). Customers are delighted in today’s scenarios when they encounter a sincere seller who is interested in customers’ welfare along with persuading for the purchase of the products. The financial sector in the world has been marred by false commitments and frauds which have created a wrong impression among the customers about the benefits of financial products and the paucity of sincere efforts for solving a customer’s requirement has been overlooked. However, the growing competition has forced financial brands to ensure processes that enthuse trust and faith among prospective and existing customers with a special focus on women customers. The study reveals that sincere brands are always loved by customers, especially women customers. However, the brands need to be responsive and that seems to be the hygiene factor expected by women customers responsible for generating satisfaction because of which women customers will be involved in a positive WOM. This study contributes significantly towards emphasis on hygiene factors which cannot be overlooked while designing strategies specially for women customers and what women customers would value while influencing a purchase decision or making a purchase decision that was missing greatly in the previous studies (Barr, Citation2002; Bucher‐Koenen et al., Citation2017; Kofman & Payne, Citation2020; Shetty & Rodrigues, Citation2017; Yavas et al., Citation2004; Zhu et al., Citation2002).

The findings of this research meaningfully contribute to the field of consumer behavior and gender differences based on male and female. The women customers in the financial industry are an understated market segment, this study provides an understanding of factors responsible for women customers’ positive word of mouth and satisfaction thus will be enriching the literature of the financial sector’s consumer behavior. The research results provide valuable insights for the marketers and designers of financial products to offer customized strategies for women customers. The results provide practical insights to the managers and marketers of the financial brands by suggesting that the women customers’ positive word of mouth can indirectly be achieved by targeting customer satisfaction through the responsive dimension of brand personality; however, the sincerity component of service quality can directly be targeted to generate positive word of mouth for financial brands (Braunstein & Ross, Citation2010; Demirel & Erdogmus, Citation2016; Perepelkin & Zhang, 2014).

7. Limitations and areas of future research

While the study tried to study the word-of-mouth behavior of female customers of financial brands, the valid responses were largely from females who were employed in the private sector. A subsequent study with self-employed women might uncover different aspects and different expectations. It would be interesting to understand the similarities or differences in the attitudes of salaried and self-employed women customers. The sampling techniques used were purposive and judgmental sampling to ensure valid feedback, which could be challenged, and an appropriate sampling technique could be arrayed to see if there are any differences in the population and responses. This study deployed the validated measures for seeking responses from female customers, which could have been a limiting factor in analyzing the contemporary ideas and trends. Qualitative research deploying focus group discussions could be stimulating, thereby resulting in redesigning of the measures. Future researchers could very well aim to deploy measures to understand what type of brands in the goods category women customers love to talk about.

Additional information

Funding

Notes on contributors

Brajesh Bolia

Brajesh Bolia is an Associate Professor with K J Somaiya Institute of Management, India with over 23 years of experience in industry and academia. He teaches the courses - Sales and Distribution Management & Business to Business Marketing. Prof Bolia has delivered management development programs for over 200 h to over 2000 participants of several reputed organizations in India. He has research interests in consumer behavior and sales & customer interface. He has completed his PhD in management with a focus on cognitive dissonance and its marketing implications in the financial services sector.

References

- Aaker, J., Fournier, S., & Brasel, S. A. (2004). When good brands do bad. Journal of Consumer Research, 31(1), 1–22. https://doi.org/https://doi.org/10.1086/383419

- Aaker, J. L. (1997). Dimensions of brand personality. Journal of Marketing Research, 34(3), 347–356. https://doi.org/https://doi.org/10.1177/002224379703400304

- Ab Hamid, M. R., Sami, W., & Sidek, M. M. (2017, September). Discriminant validity assessment: Use of Fornell & Larcker criterion versus HTMT criterion. In Journal of Physics: Conference Series (Vol. 890, p. 012163). IOP Publishing.

- Achouri, M. A., & Bouslama, N. (2010). The effect of the congruence between brand personality and self-image on consumers’ satisfaction and loyalty: A conceptual framework. IBIMA Business Review.

- Agnihotri, R., Dingus, R., Hu, M. Y., & Krush, M. T. (2016). Social media: Influencing customer satisfaction in B2B sales. Industrial Marketing Management, 53, 172–180. https://doi.org/https://doi.org/10.1016/j.indmarman.2015.09.003

- Ahearne, M., Jelinek, R., & Jones, E. (2007). Examining the effect of salesperson service behavior in a competitive context. Journal of the Academy of Marketing Science, 35(4), 603–616. https://doi.org/https://doi.org/10.1007/s11747-006-0013-1

- Ahmadi, A. (2019). Thai Airways: Key influencing factors on customers’ word of mouth. International Journal of Quality & Reliability Management, 36(1), 40–57. https://doi.org/https://doi.org/10.1108/IJQRM-02-2018-0024

- Alexandris, K., Dimitriadis, N., & Markata, D. (2002). Can perceptions of service quality predict behavioral intentions? An exploratory study in the hotel sector in Greece. Managing Service Quality: An International Journal, 12(4), 224–231. https://doi.org/https://doi.org/10.1108/09604520210434839

- Allred, A. T., & Addams, H. L. (2000). Service quality at banks and credit unions: What do their customers say? Managing Service Quality: An International Journal, 18(4), 200–207.

- Almossawi, M. (2001). Bank selection criteria employed by college students in Bahrain: An empirical analysis. The International Journal of Bank Marketing, 19(3), 115–125. https://doi.org/https://doi.org/10.1108/02652320110388540

- Alrwashdeh, M., Jahmani, A., Ibrahim, B., & Aljuhmani, H. Y. (2020). Data to model the effects of perceived telecommunication service quality and value on the degree of user satisfaction and e-WOM among telecommunications users in North Cyprus. Data in Brief, 28, 104981. https://doi.org/https://doi.org/10.1016/j.dib.2019.104981

- Al-Salem, F., & Mostafa, M. M. (2019). Clustering Kuwaiti consumer attitudes towards sharia-compliant financial products. International Journal of Bank Marketing, 37(1), 142–155. https://doi.org/https://doi.org/10.1108/IJBM-09-2017-0198

- Alt, R., Beck, R., & Smits, M. T. (2018). FinTech and the transformation of the financial industry. Electronic Markets, 28(3), 235–243. https://doi.org/https://doi.org/10.1007/s12525-018-0310-9

- Amin, M., & Nasharuddin, S. Z. (2013). Hospital service quality and its effects on patient satisfaction and behavioural intention. Clinical Governance: An International Journal, 18(3), 238–254. https://doi.org/https://doi.org/10.1108/CGIJ-05-2012-0016

- Andaleeb, S. S., & Conway, C. (2006). Customer satisfaction in the restaurant industry: An examination of the transaction‐specific model. Journal of Services Marketing, 20(1), 3–11. https://doi.org/https://doi.org/10.1108/08876040610646536

- Anderson, E. W. (1998). Customer satisfaction and WOM. Journal of Service Research, 1(1), 5–17. https://doi.org/https://doi.org/10.1177/109467059800100102

- Anggraeni, A. (2015). Effects of brand love, personality and image on word of mouth; the case of local fashion brands among young consumers. Procedia-Social and Behavioral Sciences, 211, 442–447. https://doi.org/https://doi.org/10.1016/j.sbspro.2015.11.058

- Arasli, H., Mehtap‐Smadi, S., & Katircioglu, S. T. (2005). Customer service quality in the Greek Cypriot banking industry. Managing Service Quality: An International Journal, 15(1), 41–56. https://doi.org/https://doi.org/10.1108/09604520510575254

- Ashtiani, P. G., & Iranmanesh, A. (2012). New approach to study of factors affecting adoption of electronic banking services with emphasis on the role of positive WOM. African Journal of Business Management, 6(11), 4328–4335.

- Avkiran, N. K. (1994). Developing an instrument to measure customer service quality in branch banking. International Journal of Bank Marketing, 12(6), 10–18. https://doi.org/https://doi.org/10.1108/02652329410063223

- Bairrada, C. M., Coelho, A., & Lizanets, V. (2019). The impact of brand personality on consumer behavior: The role of brand love. Journal of Fashion Marketing and Management: An International Journal, 23(1), 30–47. https://doi.org/https://doi.org/10.1108/JFMM-07-2018-0091

- Bakar, A. N. A., Hussin, M. Y. M., Latip, N. A. M., & Mahmood, A. (2019). Customers satisfaction and service quality of Islamic Banks in Perak, Malaysia. International Journal of Academic Research in Business and Social Sciences, 9(9), 1283–1297. https://doi.org/https://doi.org/10.6007/IJARBSS/v9-i9/6461

- Bakewell, C., & Mitchell, V. W. (2003). Generation Y female consumer decision‐making styles. International Journal of Retail & Distribution Management, 31(2), 95–106. https://doi.org/https://doi.org/10.1108/09590550310461994

- Barr, T. F. (2002). EVEolution: The Eight truths of marketing to women. Journal of Consumer Marketing, 19(1), 74–82.

- Beldona, S., & Wysong, S. (2007). Putting the “brand” back into store brands: An exploratory examination of store brands and brand personality. Journal of Product & Brand Management, 16(4), 226–235. https://doi.org/https://doi.org/10.1108/10610420710763912

- Berry, L. L., Seiders, K., & Grewal, D. (2002). Understanding service convenience. Journal of Marketing, 66(3), 1–17. https://doi.org/https://doi.org/10.1509/jmkg.66.3.1.18505

- Bitner, M. J., Booms, B. H., & Tetreault, M. S. (1990). The service encounter: Diagnosing favorable and unfavorable incidents. Journal of Marketing, 54(1), 71–84. https://doi.org/https://doi.org/10.1177/002224299005400105

- Bolia, B., Jha, S., & Jha, M. K. (2016). Cognitive dissonance: A review of causes and marketing implications. Researchers World, 7(2), 63–76.

- Bolia, B., Jha, S., & Jha, M. K. (2020). Understanding cognitive dissonance of Indian customers for financial products: A Multi-Dimensional scale development approach. Indian Journal of Finance and Banking, 4(1), 20–32. https://doi.org/https://doi.org/10.46281/ijfb.v4i1.500

- Bolton, R. N., & Drew, J. H. (1991). A multistage model of customers’ assessments of service quality and value. Journal of Consumer Research, 17(4), 375–384. https://doi.org/https://doi.org/10.1086/208564

- Boyd, W. L., Leonard, M., & White, C. (1994). Customer preferences for financial services: An analysis. International Journal of Bank Marketing, 12(1), 9–15. https://doi.org/https://doi.org/10.1108/02652329410049562

- Braunstein, J. R., & Ross, S. D. (2010). Brand personality in sport: Dimension analysis and general scale development. Sport Marketing Quarterly, 19(1), 8–16.

- Brown, S. P., & Beltramini, R. F. (1989). Consumer complaining and WOM activities: Field evidence. ACR North American Advances, 16, 9–16.

- Bruwer, J., & Buller, C. (2012). Country‐of‐origin (COO) brand preferences and associated knowledge levels of Japanese wine consumers. Journal of Product & Brand Management, 25(1), 307–316. https://doi.org/https://doi.org/10.1108/10610421211253605

- Bucher‐Koenen, T., Lusardi, A., Alessie, R., & Van Rooij, M. (2017). How financially literate are women? An overview and new insights. Journal of Consumer Affairs, 51(2), 255–283. https://doi.org/https://doi.org/10.1111/joca.12121

- Cadotte, E. R., Woodruff, R. B., & Jenkins, R. L. (1987). Expectations and norms in models of consumer satisfaction. Journal of Marketing Research, 24(3), 305–314. https://doi.org/https://doi.org/10.1177/002224378702400307

- Carmon, Z., Shanthikumar, J. G., & Carmon, T. F. (1995). A psychological perspective on service segmentation models: The significance of accounting for consumers’ perceptions of waiting and service. Management Science, 41(11), 1806–1815. https://doi.org/https://doi.org/10.1287/mnsc.41.11.1806

- Caruana, A. (2002). Service loyalty: The effects of service quality and the mediating role of customer satisfaction. European Journal of Marketing, 36(7/8), 811–828. https://doi.org/https://doi.org/10.1108/03090560210430818

- Casidy, R., & Wymer, W. (2016). A risk worth taking: Perceived risk as moderator of satisfaction, loyalty, and willingness-to-pay premium price. Journal of Retailing and Consumer Services, 32, 189–197. https://doi.org/https://doi.org/10.1016/j.jretconser.2016.06.014

- Chang, P. L., & Chieng, M. H. (2006). Building consumer–brand relationship: A cross‐cultural experiential view. Psychology & Marketing, 23(11), 927–959. https://doi.org/https://doi.org/10.1002/mar.20140

- Chaniotakis, I. E., & Lymperopoulos, C. (2009). Service quality effect on satisfaction and WOM in the health care industry. Managing Service Quality: An International Journal, 19(2), 229–242. https://doi.org/https://doi.org/10.1108/09604520910943206

- Chawla, D., & Sodhi, N. (2011). Research methodology: Concepts and cases. Vikas Publishing House.

- Ching, K. M. (2009). Sincerity and Excitement: when should be emphasized in the Chinese context? Evidence from Chinese medicine industry (Doctoral dissertation, Hong Kong Baptist University Hong Kong).

- Choi, Y., Thoeni, A., & Kroff, M. W. (2018). Brand actions on social media: Direct effects on electronic WOM (eWOM) and moderating effects of brand loyalty and social media usage intensity. Journal of Relationship Marketing, 17(1), 52–70. https://doi.org/https://doi.org/10.1080/15332667.2018.1440140

- Chompis, E., Horn, H. J., Bons, R. W., & Feldberg, F. (2012, June). Social media in B2B financial services: A matter of trust and responsiveness? In Bled eConference (p. 3).

- Chon, K. S. (1990). Consumer satisfaction and dissatisfaction in tourism as related to destination image perception [ Doctoral dissertation], Virginia Tech.

- Choudhury, K. (2014). Service quality and WOM: A study of the banking sector. International Journal of Bank Marketing, 32(7), 612–627. https://doi.org/https://doi.org/10.1108/IJBM-12-2012-0122

- Cronin, J. J., Jr, Brady, M. K., & Hult, G. T. M. (2000). Assessing the effects of quality, value, and customer satisfaction on consumer behavioral intentions in service environments. Journal of Retailing, 76(2), 193–218. https://doi.org/https://doi.org/10.1016/S0022-4359(00)00028-2

- Cronin, J. J., Jr, & Taylor, S. A. (1992). Measuring service quality: A reexamination and extension. Journal of Marketing, 56(3), 55–68. https://doi.org/https://doi.org/10.1177/002224299205600304

- Crosby, L. A., Evans, K. R., & Cowles, D. (1990). Relationship quality in services selling: An interpersonal influence perspective. Journal of Marketing, 54(3), 68–81. https://doi.org/https://doi.org/10.1177/002224299005400306

- De Matos, C. A., Rossi, C. A. V., Veiga, R. T., & Vieira, V. A. (2009). Consumer reaction to service failure and recovery: The moderating role of attitude toward complaining. Journal of Services Marketing, 23(7), 462–475. https://doi.org/https://doi.org/10.1108/08876040910995257

- Demirel, A., & Erdogmus, I. (2016). The impacts of fans’ sincerity perceptions and social media usage on attitude toward sponsor. Sport, Business and Management: An International Journal, 6(1), 36–54. https://doi.org/https://doi.org/10.1108/SBM-07-2014-0036

- Devesh, S. (2019). Service quality dimensions and customer satisfaction: Empirical evidence from retail banking sector in Oman. Total Quality Management & Business Excellence, 30(15–16), 1616–1629. https://doi.org/https://doi.org/10.1080/14783363.2017.1393330

- Driva, A., Lührmann, M., & Winter, J. (2016). Gender differences and stereotypes in financial literacy: Off to an early start. Economics Letters, 146, 143–146. https://doi.org/https://doi.org/10.1016/j.econlet.2016.07.029

- Ekinci, Y., Sirakaya-Turk, E., & Baloglu, S. (2007). Host image and destination personality. Tourism Analysis, 12(5–6), 433–446. https://doi.org/https://doi.org/10.3727/108354207783227885

- Endara, Y. M., Ali, A. B., & Ab Yajid, M. S. (2019). The influence of culture on service quality leading to customer satisfaction and moderation role of type of bank. Journal of Islamic Accounting and Business Research, 10(1), 134–154. https://doi.org/https://doi.org/10.1108/JIABR-12-2015-0060

- Eren, B. A. (2021). Determinants of customer satisfaction in chatbot use: Evidence from a banking application in Turkey. International Journal of Bank Marketing, 39(2), 294–311. https://doi.org/https://doi.org/10.1108/IJBM-02-2020-0056

- Farrag, D. A. R., Murphy, W. H., & Hassan, M. (2020). Influence of category attitudes on the relationship between SERVQUAL and satisfaction in Islamic banks; the role of disruptive societal-level events. Journal of Islamic Marketing, ahead-of-print(ahead–of–print), ahead-of-print. https://doi.org/https://doi.org/10.1108/JIMA-08-2020-0228

- Folse, J. A. G., Netemeyer, R. G., & Burton, S. (2012). Spokescharacters. Journal of Advertising, 41(1), 17–32. https://doi.org/https://doi.org/10.2753/JOA0091-3367410102

- Fornell, C., Johnson, M. D., Anderson, E. W., Cha, J., & Bryant, B. E. (1996). The American customer satisfaction index: Nature, purpose, and findings. Journal of Marketing, 60(4), 7–18. https://doi.org/https://doi.org/10.1177/002224299606000403

- Germain, R. (2000). Were banks marketing themselves well from a segmentation perspective before the emergence of scientific inquiry on services marketing? Journal of Services Marketing, 14(1), 44–60. https://doi.org/https://doi.org/10.1108/08876040010309202

- Gounaris, S. P., Stathakopoulos, V., & Athanassopoulos, A. D. (2003). Antecedents to perceived service quality: An exploratory study in the banking industry. International Journal of Bank Marketing, 21(4), 168–190. https://doi.org/https://doi.org/10.1108/02652320310479178

- Graeff, T. R. (1996). Using promotional messages to manage the effects of brand and self‐image on brand evaluations. Journal of Consumer Marketing, 13(3), 4–18. https://doi.org/https://doi.org/10.1108/07363769610118921

- Grandey, A. A., Goldberg, L., & Pugh, S. D. (2011, January). Employee satisfaction, responsiveness, and customer satisfaction: Linkages and boundary conditions. In Academy of Management Proceedings (Vol. 2011, pp. 1–6). Briarcliff Manor, NY 10510: Academy of Management.

- Hair, J., Black, W., Babin, B., & Anderson, R. (2013). Multivariate data analysis ((7th ed.). Prentice Hall, Inc..

- Hair, J. F., Jr, Hult, G. T. M., Ringle, C., & Sarstedt, M. (2016). A primer on partial least squares structural equation modeling (PLS-SEM). Sage publications.

- Hans, O., & Anamaria, T. (2001). Brand personality creation through advertising (No. 015). . Research Memorandum 015, Maastricht University, Maastricht Research School of Economics of Technology and Organization (METEOR).

- Harrison-Walker, L. J. (2001). The measurement of word-of-mouth communication and an investigation of service quality and customer commitment as potential antecedents. Journal of Service Research, 4(1), 60–75. https://doi.org/https://doi.org/10.1177/109467050141006

- Hennig-Thurau, T., Walsh, G., & Walsh, G. (2003). Electronic word-of-mouth: Motives for and consequences of reading customer articulations on the Internet. International Journal of Electronic Commerce, 8(2), 51–74. https://doi.org/https://doi.org/10.1080/10864415.2003.11044293

- Herr, P. M., Kardes, F. R., & Kim, J. (1991). Effects of word-of-mouth and product-attribute information on persuasion: An accessibility-diagnosticity perspective. Journal of Consumer Research, 17(4), 454–462. https://doi.org/https://doi.org/10.1086/208570

- Hickman, T. M., & Ward, J. C. (2013). Implications of brand communities for rival brands: Negative brand ratings, negative stereotyping of their consumers and negative word-of-mouth. Journal of Brand Management, 20(6), 501–517. https://doi.org/https://doi.org/10.1057/bm.2012.57

- Hoeffler, S., & Keller, K. L. (2002). Building brand equity through corporate societal marketing. Journal of Public Policy & Marketing, 21(1), 78–89. https://doi.org/https://doi.org/10.1509/jppm.21.1.78.17600

- Hong, Y., Liao, H., Hu, J., & Jiang, K. (2013). Missing link in the service profit chain: A meta-analytic review of the antecedents, consequences, and moderators of service climate. Journal of Applied Psychology, 98(2), 237. https://doi.org/https://doi.org/10.1037/a0031666

- Hultman, M., Skarmeas, D., Oghazi, P., & Beheshti, H. M. (2015). Achieving tourist loyalty through destination personality, satisfaction, and identification. Journal of Business Research, 68(11), 2227–2231. https://doi.org/https://doi.org/10.1016/j.jbusres.2015.06.002

- Iberahim, H., Taufik, N. K., Adzmir, A. S., & Saharuddin, H. (2016). Customer satisfaction on reliability and responsiveness of self service technology for retail banking services. Procedia Economics and Finance, 37, 13–20. https://doi.org/https://doi.org/10.1016/S2212-5671(16)30086-7

- Islam, R., Ahmed, S., Rahman, M., & Al Asheq, A. (2020). Determinants of service quality and its effect on customer satisfaction and loyalty: An empirical study of private banking sector. The TQM Journal, ahead-of-print(ahead–of–print). https://doi.org/https://doi.org/10.1108/TQM-05-2020-0119

- Ismail, A. R., & Spinelli, G. (2012). Effects of brand love, personality and image on WOM. Journal of Fashion Marketing and Management: An International Journal, 16(4), 386–398. https://doi.org/https://doi.org/10.1108/13612021211265791

- Jamal, A., & Goode, M. M. (2001). Consumers and brands: A study of the impact of self‐image congruence on brand preference and satisfaction. Marketing Intelligence & Planning, 19(7), 482–492. https://doi.org/https://doi.org/10.1108/02634500110408286

- Kasasbeh, E. A., Harada, Y., & Noor, I. M. (2017). Factors influencing competitive advantage in banking sector: A systematic literature review. Research Journal of Business Management, 11(2), 67–73. https://doi.org/https://doi.org/10.3923/rjbm.2017.67.73

- Keaveney, S. M. (1995). Customer switching behavior in service industries: An exploratory study. Journal of Marketing, 59(2), 71–82. https://doi.org/https://doi.org/10.1177/002224299505900206

- Kim, D., Magnini, V. P., & Singal, M. (2011). The effects of customers’ perceptions of brand personality in casual theme restaurants. International Journal of Hospitality Management, 30(2), 448–458. https://doi.org/https://doi.org/10.1016/j.ijhm.2010.09.008

- Kim, K. H. (2013). The effect of take-out coffee shop brand personality on customer satisfaction and brand loyalty. Journal of the Korean Society of Food Culture, 28(5), 473–479. https://doi.org/https://doi.org/10.7318/KJFC/2013.28.5.473

- Kim, Y. E., & Lee, J. W. (2008). Relationship between brand personality, customer satisfaction, and brand loyalty, and its application to branding strategy. Journal of Customer Satisfaction Management, 10(2), 137–152.

- Kock, N. (2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration (Ijec), 11(4), 1–10.

- Kofman, P., & Payne, C. (2020). Digital financial inclusion of women: An ethical appraisal. In Handbook on ethics in finance (pp. 1–25). https://doi.org/https://doi.org/10.1007/2F978-3-030-29371-0_34

- Kothari, C. R. (2004). Research methodology: Methods and techniques. New Age International.

- Kumar, P., Kalwani, M. U., & Dada, M. (1997). The impact of waiting time guarantees on customers’ waiting experiences. Marketing Science, 16(4), 295–314. https://doi.org/https://doi.org/10.1287/mksc.16.4.295

- Kwong, M. Z., & Candinegara, I. (2014). Relationship between brand experience, brand personality, consumer satisfaction, and consumer loyalty of DSSMF brand. iBuss Management, 2(2), 89–98.

- Lai, I. K. W., & Hitchcock, M. (2016). A comparison of service quality attributes for stand-alone and resort-based luxury hotels in Macau: 3-Dimensional importance-performance analysis. Tourism Management, 55, 139–159. https://doi.org/https://doi.org/10.1016/j.tourman.2016.01.007

- Lebdaoui, H., & Chetioui, Y. (2020). CRM, service quality and organizational performance in the banking industry a comparative study of conventional and Islamic banks. International Journal of Bank Marketing, 38(5), 1081–1106. https://doi.org/https://doi.org/10.1108/IJBM-09-2019-0344

- Leclerc, F., Schmitt, B. H., & Dube, L. (1995). Waiting time and decision making: Is time like money? Journal of Consumer Research, 22(1), 110–119. https://doi.org/https://doi.org/10.1086/209439

- Lee, J. A., & Eastin, M. S. (2020). I like what she’s# endorsing: The impact of female social media influencers’ perceived sincerity, consumer envy, and product type. Journal of Interactive Advertising, 20(1), 76–91. https://doi.org/https://doi.org/10.1080/15252019.2020.1737849

- Levesque, T., & McDougall, G. H. (1996). Determinants of customer satisfaction in retail banking. International Journal of Bank Marketing, 14(7), 12–20. https://doi.org/https://doi.org/10.1108/02652329610151340

- Li, F., Lu, H., Hou, M., Cui, K., & Darbandi, M. (2021). Customer satisfaction with bank services: The role of cloud services, security, e-learning and service quality. Technology in Society, 64, 101487. https://doi.org/https://doi.org/10.1016/j.techsoc.2020.101487

- Liao, S. H., Chung, Y. C., & Lin, K. Y. (2015). A clash of personality? The relationship among consumer personality, brand personality and word-of-mouth with social-cognitive perspective: Generation as the moderator. International Journal of Services Technology and Management, 21(1–3), 111–126. https://doi.org/https://doi.org/10.1504/IJSTM.2015.071096

- Liu, C. H. S., & Lee, T. (2016). Service quality and price perception of service: Influence on word-of-mouth and revisit intention. Journal of Air Transport Management, 52, 42–54. https://doi.org/https://doi.org/10.1016/j.jairtraman.2015.12.007

- Lovelock, C., Vandermerwe, S., & Lewis, B. (1996). Service marketing: A European perspective. Prenice Hall.

- Lymperopoulos, C., & Chaniotakis, I. E. (2008). Price satisfaction and personnel efficiency as antecedents of overall satisfaction from consumer credit products and positive WOM. Journal of Financial Services Marketing, 13(1), 63–71. https://doi.org/https://doi.org/10.1057/fsm.2008.6

- Lynch, J. (1993). Hear it from the heart. Managing Service Quality: An International Journal, 3(1), 379–383. https://doi.org/https://doi.org/10.1108/EUM0000000003151

- Madrigal, R., & Boush, D. M. (2008). Social responsibility as a unique dimension of brand personality and consumers’ willingness to reward. Psychology & Marketing, 25(6), 538–564. https://doi.org/https://doi.org/10.1002/mar.20224

- Maehle, N., Otnes, C., & Supphellen, M. (2011). Consumers’ perceptions of the dimensions of brand personality. Journal of Consumer Behaviour, 10(5), 290–303. https://doi.org/https://doi.org/10.1002/cb.355

- Magin, S., Algesheimer, R., Huber, F., & Herrmann, A. (2003). The impact of brand personality and customer satisfaction on customer’s loyalty: Theoretical approach and findings of a causal analytical study in the sector of Internet service providers. Electronic Markets, 13(4), 294–308. https://doi.org/https://doi.org/10.1080/1019678032000135572

- Malhotra, N., & Mukherjee, A. (2004). The relative influence of organisational commitment and job satisfaction on service quality of customer‐contact employees in banking call centres. Journal of Services Marketing, 18(3), 162–174. https://doi.org/https://doi.org/10.1108/08876040410536477

- Malhotra, N. K., & Dash, S. (2011). Marketing research: an applied orientation (6th ed. ed.). Pearson Education.

- Mandal, S., Sahay, A., Terron, A., & Mahto, K. (2021). How implicit self-theories and dual-brand personalities enhance word-of-mouth. European Journal of Marketing, 55(5), 1489-1515. https://doi.org/https://doi.org/10.1108/EJM-07-2019-0591

- Mangold, W. G., Miller, F., & Brockway, G. R. (1999). Word‐of‐mouth communication in the service marketplace. Journal of Services Marketing, 13(1), 73–83. https://doi.org/https://doi.org/10.1108/08876049910256186

- Mariappan, V. (2006). Changing the way of banking in India. Vinimaya, 26(2), 26–34.

- Meiske, T., & Balqiah, E. (2019). How to build WOM: The role brand personality, brand love and brand loyalty. In SU-AFBE 2018: Proceedings of the 1st Sampoerna University-AFBE International Conference, SU-AFBE 2018, 6-7 December 2018, Jakarta Indonesia (p. 421-526). European Alliance for Innovation. https://doi.org/https://doi.org/10.4108/eai.6-12-2018.2286284

- Memon, M. S. (2021). Measuring the effect of brand personality on brand loyalty: Mediating role of customer satisfaction. Psychology and Education Journal, 58(1), 2386–2397. https://doi.org/https://doi.org/10.17762/pae.v58i1.1114

- Mohtasham, S. S., Sarollahi, S. K., & Hamirazavi, D. (2017). The effect of service quality and innovation on WOM marketing success. Eurasian Business Review, 7(2), 229–245. https://doi.org/https://doi.org/10.1007/s40821-017-0080-x

- Moyes, D., Cano-Kourouklis, M., & Scott, J. (2016). Testing the three Rs model of service quality. The TQM Journal, 28(3), 455–466. https://doi.org/https://doi.org/10.1108/TQM-02-2015-0026

- Mukerjee, K. (2018). The impact of brand experience, service quality and perceived value on WOM of retail bank customers: Investigating the mediating effect of loyalty. Journal of Financial Services Marketing, 23(1), 12–24. https://doi.org/https://doi.org/10.1057/s41264-018-0039-8

- Narteh, B. (2018). Brand equity and financial performance. Marketing Intelligence & Planning, 36(3), 381–395. https://doi.org/https://doi.org/10.1108/MIP-05-2017-0098

- Naylor, G., & Frank, K. E. (2000). The impact of retail sales force responsiveness on consumers’ perceptions of value. Journal of Services Marketing, 14(4), 310–322. https://doi.org/https://doi.org/10.1108/08876040010334529

- O’Neill, J. W., & Carlbäck, M. (2011). Do brands matter? A comparison of branded and independent hotels’ performance during a full economic cycle. International Journal of Hospitality Management, 30(3), 515–521. https://doi.org/https://doi.org/10.1016/j.ijhm.2010.08.003

- Ong, K. S., Nguyen, B., & Alwi, S. F. S. (2017). Consumer-based virtual brand personality (CBVBP), customer satisfaction and brand loyalty in the online banking industry. International Journal of Bank Marketing, 35(3), 370–390. https://doi.org/https://doi.org/10.1108/IJBM-04-2016-0054

- Oraedu, C., Izogo, E. E., Nnabuko, J., & Ogba, I. E. (2020). Understanding electronic and face-to-face word-of-mouth influencers: An emerging market perspective. Management Research Review, 44(1), 112–132. https://doi.org/https://doi.org/10.1108/MRR-02-2020-0066

- Orth, U. R., Limon, Y., & Rose, G. (2010). Store-evoked affect, personalities, and consumer emotional attachments to brands. Journal of Business Research, 63(11), 1202–1208. https://doi.org/https://doi.org/10.1016/j.jbusres.2009.10.018

- Ozbekler, T. M., & Ozturkoglu, Y. (2020). Analysing the importance of sustainability‐oriented service quality in competition environment. Business Strategy and the Environment, 29(3), 1504–1516. https://doi.org/https://doi.org/10.1002/bse.2449

- Pakurár, M., Haddad, H., Nagy, J., Popp, J., & Oláh, J. (2019). The service quality dimensions that affect customer satisfaction in the Jordanian banking sector. Sustainability, 11(4), 1113. https://doi.org/https://doi.org/10.3390/su11041113

- Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). Servqual: A multiple-item scale for measuring consumer perc. Journal of Retailing, 64(1), 12–40.

- Park, S. Y., & Lee, E. M. (2005). Congruence between brand personality and self-image, and the mediating roles of satisfaction and consumer-brand relationship on brand loyalty. ACR Asia-Pacific Advances, 6, 39–45.

- Perepelkin, J., & Di Zhang, D. (2014). Quality alone is not enough to be trustworthy. International Journal of Pharmaceutical and Healthcare Marketing, 8(2), 226–242. https://doi.org/https://doi.org/10.1108/IJPHM-02-2013-0006

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879–903. https://doi.org/https://doi.org/10.1037/0021-9010.88.5.879