Abstract

With near-zero policy rates becoming the norm in many advanced economies, the focus on long-term bond yields has strengthened considerably. The unconventional monetary policy decision by the Bank of Japan (BOJ) in September 2016 to explicitly target the ten-year Japanese government bond (JGB) yield institutionalized this process—by effectively creating a new monetary policy focal point. In this article, we study the importance of such focal points. Empirically, we also investigate how JGB benchmark maturities ranging from one to thirty years has affected other benchmark maturities over time. We find that the ten-year bond, indeed, became more influential in 2016. However, the effect was surprisingly short-lived. The results suggest that once financial market participants anchored their expectations of the ten-year JGB yield to the new BOJ target, the attention merely shifted towards even longer maturities. Contrary to the logic of the monetary transmission mechanism, we also find the short end of the yield curve has been an absorber, rather than transmitter, of influence during the last decades.

Central banks often adopt anchors and targets to steer the expectations of market participants and the wider public. Indeed, anchors, targets, benchmarks, pegs, focal points etc., are very common and extremely helpful for coordination processes towards some kind of goal—a crucial aspect of many economic activities. In a classic example, Thomas Schelling (Citation1960) illustrates this by posing the question: “If you are to meet a stranger in New York City, but you cannot communicate with the person, then when and where will you choose to meet?” The most common answer is “noon at Grand Central Terminal.” Game theorists, in particular, have found this example intriguing, as the meeting point and time could be conceptualized as a kind of equilibrium for a voluntary exchange or a monetary transaction. However, anchors, targets, benchmarks, pegs, and focal points typically have deep sociological, institutional, and political underpinnings. Some evolve and become formalized via habits and conventions, whereas others are constructs solidifying relationships of power (Stenfors Citation2018; Stenfors and Lindo Citation2018).

Fixed Exchange Rate Regimes

As an annex of the state and leader of the club of banks, the central bank has significant power to choose a particular monetary focal point and coordinate others’ behavior towards it. However, it is by no means absolute. Throughout modern history, numerous central banks have tried to maintain a fixed exchange rate regime—a monetary policy focal point in the form of a specific exchange rate or a reasonably narrow range within which this exchange rate is allowed to fluctuate without central bank intervention. Importantly, regardless of whether a currency is perceived to be over or undervalued, a fixed exchange rate regime involves trying to maintain trust in the central bank’s ability and commitment to its chosen focal point indefinitely. For instance, when market speculators (unsuccessfully) tested the long-lasting Danish krone peg against the euro at 7.46 in February 2015, Denmark’s central bank Governor Lars Rohde stated that he would do “whatever it takes” and that the central bank could “go on forever” to defend the peg—in other words to forcefully keep the focal point unchanged at 7.46 (Milne Citation2015). However, Denmark belongs to a group of exceptions, and the lifetime of most exchange rate pegs have tended to be relatively short.

Inflation Targeting

Since the 1990s, there has been a systematic trend to abandon such fixed exchange rates in favor of floating exchange rates, price stability, and inflation targeting. Instead, monetary policy targets in the form of economic indicators such as inflation have become common. Inflation per se cannot come under the attack by speculators—regardless of how inflation is defined (e.g. CPI or CPIF), the nominal target of the inflation rate (e.g. 2 or 2–3%) or the horizon for when this target is supposed to be met (e.g., two or three years). Inflation targeting, therefore, eliminates an almost inevitable battle between the central bank and financial market participants to preserve or break a specific focal point.

However, this does not mean that the central bank has given up all its power. It simply means that the focal point obtained a more indirect characteristic. According to the logic of the monetary transmission mechanism, the official interest rate set by the central bank filters through to the rest of the economy via medium- and long-term interest rates. Further, following the expectations hypothesis of the term structure of interest rates, bond yields of different maturities are closely correlated. Chotibhak Jotikasthira, Anh Le, and Christian Lundblad (Citation2015) find that co-movements among bond yields can be derived from other the central bank policy rate (the “policy channel”) or term premia (the “risk compensation channel”). Historically, central banks have been content to exercise influence over short-term maturities. Indeed, during the early years of inflation targeting, they were reluctant to tamper with the market forces that ultimately had the final say in the level of long-term yields. Instead, the difficulty in steering long-term interest rates (and hence the inflation rate) started to become addressed through a trend towards greater transparency. Market uncertainty could be minimized by publicly announcing monetary policy meeting schedules, voting results, and minutes.

Unconventional Monetary Policy

Nonetheless, the usage of more direct and formal focal points became much more explicit with the launch of so-called “forward guidance” (Stenfors Citation2014). With this, market participants were presented with a blueprint for how the central bank would behave under various scenarios in the future. To paraphrase Thomas Schelling, market participants were not explicitly told to meet at noon at Grand Central Terminal. Still, they were given clues as to where others might be likely to encounter if an event were to happen. By openly disclosing the central bank’s view of the possible interest rate path in the future and the circumstances when this scenario might change, a string of focal points could be sprinkled along the yield curve towards which market participants could then anchor their expectations. The focal points were not randomly chosen but rather followed conventional benchmark maturities such as six months, one year, two years, etc.

With the advent of the Great Recession, the deployment of forward guidance, coupled with a battery of other unconventional monetary policies, increased considerably. Then, following the Eurozone sovereign debt crisis, the European Central Bank (ECB) Governor Mario Draghi made one of the boldest moves in this famous “whatever it takes” speech on July 26, 2012 (ECB Citation2012). The speech, which came to substantially lower bond yields across the Eurozone, was interpreted as if the ECB were prepared to go any length, or at least much further than previously envisaged, to save the euro. However, despite having a huge impact on financial markets in general and European government bond yields in particular, the speech did not alter any existing focal points as such. Instead, it signaled a warning to market participants not to be led astray by economic commentators and speculators who had become tempted to anchor their expectations to the demise of the Eurozone project.

Yield Curve Control

Since near-zero policy rates have become the norm in many advanced economies following the Great Recession, the focus of attention to long-term bond yields has strengthened considerably. The COVID-19 pandemic has provided further impetus, as governments have become faced with higher levels of debt that will need to be managed in the future. The logical next step from a string of focal points based upon expectations and promises that are open to interpretation is a firm target of a specific yield for a particular maturity along the yield curve spectrum.

Although it had been adopted in the past (in the United States during and in the immediate aftermath of WWII), Japan became a pioneer with yield curve control in the modern era. The unconventional monetary policy decision by the Bank of Japan (BOJ) on September 21, 2016 to explicitly target the ten-year Japanese government bond (JGB) yield at around 0% effectively institutionalized a new yield curve anchor—a role historically only played by the short-term policy rate (Bank of Japan Citation2016).

From a theoretical perspective, introducing a completely new focal point is important by serving as a reminder of the debate during the first half of the twentieth century concerning the role of expectations in monetary policy. The fact that interest rates have been low in Japan for a very long time has prompted comparisons to the writings by John Maynard Keynes (1935) on the “liquidity trap.” Furthermore, the idea that the central bank could determine the current, future, and possibly even the expected future interest rate goes back to the contributions by Ralph George Hawtrey (Citation1923 and Citation1938) and John Richard Hicks (Citation1977). Put together, they pose a crucial question: “Can, and shall, the state systematically intervene to determine the long-term interest rate?”

From a simple theoretical and practical point of view, the Japanese reform is significant because it questions whether the logic of the first steps of the monetary transmission mechanism is fit for purpose. If the central bank suddenly tells market participants to get accustomed to a ten-year yield of 0% and then uses its power to stand by its commitment, why would the market need to second-guess and constantly generate new expectations of future interest rates?

The Case of Japan

From a focal point of view, this prompts two questions. First, suppose the ten-year benchmark maturity has been selected as “the chosen one” among several alternatives. In that case, its importance should, to some degree, have been at the expense of other “competing” nodes along the yield curve—most notably the five-year and fifteen-year maturities. Second, and more fundamentally, the change ought to have been followed by a weaker influence from the short end of the yield curve. After all, the yield curve control policy was adopted after a period of realization that the official central bank interest rate had become insufficient as a means to steer behavior further out along the yield curve.

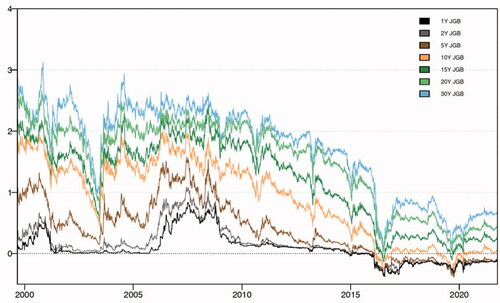

We explore these two questions by investigating how the transmission mechanism among benchmark JGBs have changed over time. Empirically, we do so by employing a framework that combines a time-varying parameter vector autoregressive (TVP-VAR) model with the dynamic connectedness approach. A technical exposition of the relatively widely adopted methodology is beyond the scope of this article. For details, see Francis Diebold and Kamil Yilmaz (Citation2014) and Ioannis Chatziantoniou, David Gabauer, and Alexis Stenfors (Citation2020, Citation2021a, and Citation2021b). We include seven key benchmark maturities in our study, namely one-, two-, five-, ten-, fifteen-, twenty- and thirty-year JGBs. depicts the development of these bonds from September 2, 1999 to October 4, 2021.

Figure 1. Japanese Government Bond Yields

As can be seen, short-term interest rates have been very low since the Japanese Banking Crisis during the 1990s. Moreover, the yield curve has been positive (i.e., upward-sloping) more or less throughout the period, but has gradually become flatter. The figure also shows that JGBs of different benchmark maturities appear to be closely correlated. The strength of the correlation seems to depend on the closeness of the maturities in question.

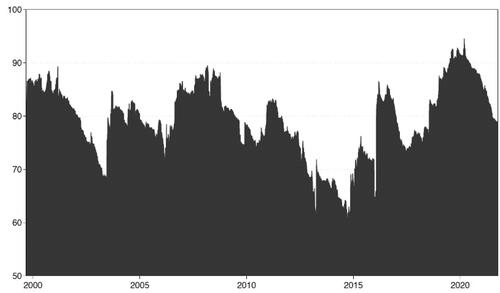

Next, let us study the dynamic connectedness of the network of benchmarks JGBs. A high connectedness index indicates strong co-movements among the “benchmark nodes” across the yield curve. A low index, by contrast, suggests that a change in one series (e.g., the five-year bond yield) has little impact on the other series.

As can be seen from , the index has ranged between 60% and 90% during the period studied—confirming the observation that the universe of JGBs is a highly connected system. Notable peaks include the Dot-com bubble in 2000, the Great Recession in 2007–2009, the introduction of yield curve control in 2016, and the start of the COVID-19 pandemic in 2020. This seesaw pattern is consistent with the literature that generally shows that connectedness (and herd behavior) tends to peak around episodes of stress and crises and decline during the early phases of significant policy changes (see, for instance, Chatziantoniou, Gabauer, and Stenfors Citation2020, Citation2021a, and Citation2021b).

Figure 2. Dynamic Total Connectedness

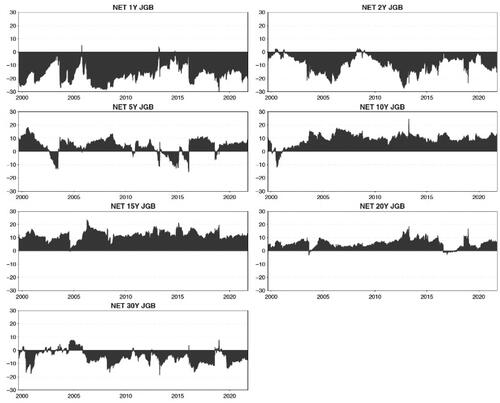

However, whereas the overall connectedness across the Japanese yield curve is interesting, the crucial question is whether and how the ten-year bond has changed since it achieved a new formal focal point status in September 2016. In addition, has there been a sudden or gradual reduction in the role of the one-year bond as a representative of the shorter-end of the yield curve? To answer these questions, let us study whether the individual bonds have influenced, or been influenced by, the other benchmark bond within this network from 1999 to 2021.

shows the “net total directional connectedness” among the JGB maturities within this network—ranging from the one-year to the thirty-year bond. A dark area significantly and consistently above [below] zero implies that the bond yield of a specific maturity transmits [receives] strong shocks or influences to [from] the others.

Figure 3. Net Total Directional Connectedness

Two observations are notable. First, the ten-year and fifteen-year (and to a lesser degree twenty-year) bonds have acted as transmitters of shocks during the last two decades. The ten-year bond also shows a “hump” around the introduction of yield curve control in 2016—confirming the notion that the ten-year focal point obtained an elevated status among the long-benchmark bonds. Indeed, shows that ever since the policy change, the BOJ has managed to keep the ten-year bond yield very close to 0%. Interestingly, however, shows that the effect was surprisingly short-lived. The results suggest that once financial market participants anchored their expectations of the ten-year JGB yield to the new BOJ target, the attention merely shifted towards even longer maturities (fifteen-year and beyond). Second, as can be seen, the dark area has almost exclusively been negative for the one-year JGB yield. Indeed, it is crystal clear that the shortest bond, more or less throughout the last two decades, has been influenced by longer-term bonds—and not vice versa. It is also notable that the two-year bond appears to have received influence from, rather than transmitted impact to, other benchmark bonds.

Concluding Remarks

In this article, we have investigated how the transmission mechanism among Japanese government bonds has changed over time. From a focal point of view, two key findings stand out. First, the short end of the yield curve has been a consistent receiver of influence from longer maturities. Second, the “shock” to the universe of benchmark maturities following the introduction of yield curve control was very short-lived. Once financial market participants anchored their expectations of the ten-year JGB yield to the new BOJ target, the attention merely shifted towards even longer maturities (fifteen-year and beyond). The observations seem to contradict the logic of the monetary transmission mechanism. Moreover, the establishment of a new focal point in the form of yield curve control appears to be surprisingly feasible and less dramatic than observers might like to think.

However, the findings do not necessarily need to be paradoxical. Japan has had near-zero and stable policy interest rates for several decades, and this typical focal point became inadequate to address the challenges a long time ago. It is only logical that the attention to the short end of the yield curve has become more muted. This is consistent with short-term bonds having been receivers of shocks from nodes further out along the yield curve. Indeed, ever since the Japanese banking crisis during the 1990s, the Bank of Japan has gone to extraordinary lengths in terms of monetary policy—ultimately intending to revive the sluggish economy and achieve a moderate and stable inflation rate. The radical policies have ranged from zero interest rate policy and quantitative easing to yield curve control. Whereas zero (or even negative) interest rates and quantitative easing have since become standard in many other advanced economies, yield curve control has not yet been widely adopted elsewhere.

However, on March 19, 2020, the Reserve Bank of Australia announced introducing a yield curve control policy in response to the COVID-19 outbreak (Reserve Bank of Australia Citation2020). A target for the yield on three-year Australian government bonds was set at around 0.25%, which would be achieved by purchasing bonds in the secondary market. Such interventions would, in addition, “address market dislocations.” Although this policy might become short-lived and temporary, it demonstrates the role of BOJ as a pioneer in adding radical, crisis-driven, and extraordinary monetary policy into the mainstream central banking toolbox. Whether the Keynes-inspired BOJ Governor Haruhiko Kuroda’s thought process will spread around the world remains to be seen (Kuroda Citation2017). Regardless, it serves as an important reminder that even in the era of “independent central banking,” the central bank remains an annex to the state.

Additional information

Notes on contributors

Alexis Stenfors

Alexis Stenfors is Reader in Economics and Finance at the University of Portsmouth (UK). Ioannis Chatziantoniou is Associate Professor of Empirical Finance at the Department of Accounting and Finance, Laboratory of Accounting and Financial Management – LAFIM, Hellenic Mediterranean University, Heraklion (Greece). David Gabauer is Senior Data Scientist at Software Competence Center Hagenberg (Austria). David Gabauer would like to acknowledge that this research has been partly funded by BMK, BMDW, Austria and the Province of Upper Austria in the frame of the COMET Program managed by FFG, Austria.

Ioannis Chatziantoniou

Alexis Stenfors is Reader in Economics and Finance at the University of Portsmouth (UK). Ioannis Chatziantoniou is Associate Professor of Empirical Finance at the Department of Accounting and Finance, Laboratory of Accounting and Financial Management – LAFIM, Hellenic Mediterranean University, Heraklion (Greece). David Gabauer is Senior Data Scientist at Software Competence Center Hagenberg (Austria). David Gabauer would like to acknowledge that this research has been partly funded by BMK, BMDW, Austria and the Province of Upper Austria in the frame of the COMET Program managed by FFG, Austria.

David Gabauer

Alexis Stenfors is Reader in Economics and Finance at the University of Portsmouth (UK). Ioannis Chatziantoniou is Associate Professor of Empirical Finance at the Department of Accounting and Finance, Laboratory of Accounting and Financial Management – LAFIM, Hellenic Mediterranean University, Heraklion (Greece). David Gabauer is Senior Data Scientist at Software Competence Center Hagenberg (Austria). David Gabauer would like to acknowledge that this research has been partly funded by BMK, BMDW, Austria and the Province of Upper Austria in the frame of the COMET Program managed by FFG, Austria.

References

- Bank of Japan (BOJ). 2016. “New Framework for Strengthening Monetary Easing: ‘Quantitative and Qualitative Monetary Easing with Yield Curve Control.’” September 21, 2016. Tokyo, Japan. Available at: https://www.boj.or.jp/en/announcements/release_2016/k160921a.pdf. Accessed October 6, 2021.

- Chatziantoniou, Ioannis, David Gabauer, and Alexis Stenfors. 2020. “From CIP-Deviations to a Market for Risk Premia: A Dynamic Investigation of Cross-Currency Basis Swaps.” Journal of International Financial Markets, Institutions and Money 69 (November): 101245.

- Chatziantoniou, Ioannis, David Gabauer, and Alexis Stenfors. 2021a “Interest Rate Swaps and the Transmission Mechanism of Monetary Policy: A Quantile Connectedness Approach.” Economics Letters 204 (July): 109891.

- Chatziantoniou, Ioannis, David Gabauer, and Alexis Stenfors. 2021b. “Independent Policy, Dependent Outcomes: A Game of Cross-Country Dominoes across European Yield Curves.” Working Papers in Economics & Finance 2021-06, University of Portsmouth, Portsmouth Business School, Economics and Finance Subject Group.

- Diebold, Francis. X., and Yılmaz, Kamil. 2014. “On the Network Topology of Variance Decompositions: Measuring the Connectedness of Financial Firms.” Journal of Econometrics 182 (1): 119–134.

- European Central Bank (ECB). 2012. “Speech by Mario Draghi, President of the European Central Bank at the Global Investment Conference in London, July 26, 2012.” Frankfurt, Germany: ECB. Available at: https://www.ecb.europa.eu/press/key/date/2012/html/sp120726.en.html. Accessed November 4, 2021.

- Hawtrey, Ralph George. 1923. Monetary Reconstruction. London: Longmans, Green and Co. Ltd.

- Hawtrey, Ralph George. 1938. A Century of Bank Rate. London: Longmans, Green and Co. Ltd.

- Hicks, John Richard. 1977. Economic Perspectives: Further Essays on Money and Growth. Oxford: Clarendon Press.

- Jotikasthira, Chotibhak, Anh Le, and Christian Lundblad. 2015. “Why do Term Structures in Different Currencies Co-Move?” Journal of Financial Economics 115 (1): 58–83.

- Keynes, John Maynard. 1936. The General Theory of Interest, Employment and Money. London: Macmillan.

- Kuroda, Haruhiko. 2017. “The Role of Expectations in Monetary Policy: Evolution of Theories and the Bank of Japan’s Experience.” Speech at the University of Oxford, June 8, 2017. Available at: www.bis.org/review/r170612d.pdf. Accessed June 10, 2021.

- Milne, Richard. 2015. “Danish Central Bank Fiercely Defends Currency Peg.” Financial Times, February 6, 2015. Available at www.ft.com/content/d3c385f6-adc6-11e4-919e-00144feab7de. Accessed October 6, 2021.

- Reserve Bank of Australia (RBA). 2020. “Statement by Philip Lowe, Governor: Monetary Policy Decision.” Number 2020-80, March 19, 2020. Available at: www.rba.gov.au/media-releases/2020/mr-20-08.html. Accessed October 7, 2021.

- Schelling, Thomas. 1960. The Strategy of Conflict. Cambridge, MA: Harvard University Press.

- Stenfors, Alexis. 2014. “LIBOR Deception and Central Bank Forward (Mis-)Guidance: Evidence from Norway during 2007–2011.” Journal of International Financial Markets, Institutions and Money 32 (C): 452–472.

- Stenfors, Alexis. 2018. “Bid-Ask Spread Determination in the FX Swap Market: Competition, Collusion or a Convention?” Journal of International Financial Markets, Institutions and Money 54 (May): 78–97.

- Stenfors, Alexis, and Duncan Lindo. 2018 “LIBOR 1986–2021: The Making and Unmaking of ‘The World’s Most Important Price.’” Distinktion: Journal of Social Theory 19 (2): 170–192.