Abstract

Despite recent clarifications by central banks that it is indeed commercial banks that are the main creators of the money supply, money creation processes remain as confusing and opaque as ever to many. This article develops a simplified macro-visual diagram of today’s money system based on the increasingly accepted “credit theory” of money creation. It aims to explain not only how money is created and which institutions have the authority to create it; it also aims to discuss the implications of this understanding of money creation for wider issues, such as political sovereignty, inequality, and socio-economic development. Ultimately, it aims to provide a pedagogical resource upon which both technical and normative discussions about our current money system among academics, activists, and students can be based.

JEL CODES:

The need for money education

After years of post-2008 scrutiny on money and banking, in March 2014, a Bank of England paper (McLeay, Radia, and Thomas Citation2014) was released entitled “Money Creation in the Modern Economy.” The paper described the process through which, in coordination with the national central bank, “the majority of money in the modern economy is created by commercial banks making loans” (14). This detailed and clearly written report confirmed years of assertions by money analysts and reformers who had been regularly dismissed as “cranks” for claiming that, contrary to the common view (that banks were simply “intermediaries” who lent out preexisting customer deposits), rather, it was the banks themselves that created new money through the act of lending (Ingham, Coutts, and Konzelmann Citation2016, 1247). It also clarified the position that, beyond their role as creators of the legal monetary framework, governments themselves play no role in money creation and are themselves effectively “borrowers” of private-sector-created moneyFootnote1 (Sgambati Citation2016; Mellor Citation2019).

While the Bank of England’s clarification was shortly followed by those from other important central banking authorities, such as the Bank for International Settlements,Footnote2 the few polls to have been conducted in recent years on the subject reveal that the overall public understanding of money and banks (in the United Kingdom [UK] and elsewhere) remains very low. A studyFootnote3 conducted by the University of Zurich in 2014 about the level of knowledge in the general population about the financial system, for example, found that only 13 percent knew that private commercial banks provide the majority of the money in circulation; 73 percent mistakenly believed money is created by the state or by the Swiss National Bank. This ignorance extends to politicians, with a 2014 surveyFootnote4 by the money reform group, Positive Money, finding that only 15 percent of UK Members of Parliament (MPs) realized that private banks create the money supply. Overall, conversations today continue to be driven by “folk” metaphors that frame money as a scarce commodity that can somehow become exhausted (Braun Citation2016; Mellor Citation2019). Because of this, most citizens are unable to begin to offer informed rebuttals to orthodox claims by politicians who recycle metaphors of “scarcity” to explain why, for example, poverty and homelessness are unfortunate—but unavoidable—things that we just have to live with (Mellor Citation2019; Kelton Citation2020a). Moreover, most people are aware of a growing amount of private indebtedness across society but don’t have a clear idea of where this money came from and who exactly it is owed to (Montgomerie Citation2019). The ongoing “mystery” surrounding money and banks—combined with growing inequality in many societies—meanwhile risks fueling misinformation and dangerous conspiracies (Lockwood Citation2021).

This lack of public understanding about money and banks is also reflected in the relative lack of explicit attention that money—as a social and political object of study—receives in general across the social sciences, even within economics (Mirowski Citation2013; Goodwin Citation2014; Morgan Citation2015). As reform group Rethinking Economics argued in a 2019 letter addressed to University Economics Departments:

Banks and their role in the creation of money are integral to our modern, financialized economies. Yet, the teaching economics students receive doesn’t give them the full picture. As those with the power to influence the next generation of economists, it is essential that you review the teaching of the role of banks in economics courses and bring it in line with up-to-date research. Our economics graduates need to understand how banks function in the real-world in order to avoid past crises and to create better economies in the future.

Where money creation is covered within orthodox economics teaching, it still tends to be based on increasingly discredited theories, such as the basic reserve-constrained base-multiplier (i.e., the money multiplier) and the quantity theory of money (Di Muzio and Noble Citation2017). This is because, as Neveu (Citation2020, 298) comments, the “status quo bias” within the economics discipline itself “presents a strong roadblock to textbook authors and publishers.” However, this bias is undermining the credibility of economics teaching, particularly in the light of both the post-2008 actions by central banks and advances in the collective understanding of how money creation actually occurs. Indeed, the money multiplier and the quantity theory of money now appear dramatically at odds with the recent clarification of commercial bank-led credit creation (Ryan-Collins et al. Citation2012). Overall, the predication of economics teaching on outdated or vague understandings of money creation is preventing today’s students from being able to engage properly with a range of pressing economic, social, political, and environmental challenges that are intimately connected to questions of money, finance, and banking (Di Muzio and Noble Citation2017).

Despite the ongoing silence in relation to money across much of society and academia, the overall attention on both the technical and political dimensions of money has expanded since 2008 within the more specialist literatures. Scholarship in critical finance and accounting studies has, for example, explained the highly complex and idiosyncratic processes through which commercial banks create the money supply and governments borrow money (e.g., Ryan-Collins et al. Citation2012; Werner Citation2014a, Citation2014b, Citation2016). This work has offered considerably clearer explanations and visualizations of the money creation process than previously existed, where the visual explanations relied on algebra and, as such, remained inaccessible for many noneconomists (e.g., Gamble Citation1991; Thornton, Ekelund, and DeLorme Citation1991; Lai, Chang, and Kao Citation2004). It has joined emerging work within the economics pedagogy itself, which has offered clearer explanations of money creation processes based on more up-to-date understandings (e.g., Pitrou Citation2019; Guse and Brasfield Citation2020; Neveu Citation2020). Political economy and economic sociology scholarship have meanwhile drawn attention to the historical evolution of monetary institutions and the questions of politics and power that underlie all systems of money governance (e.g., Weber Citation2018; Koddenbrock Citation2019; Feinig Citation2020). Along with advocacy groups such as Positive Money, this scholarship has opened a broader conversation about the normative dimensions of the current money system and about proposals for re-engineering it to better support financial stability and socio-economic needs.

Although these recent developments are welcome, this article argues that two gaps still need to be addressed to make the topic even more accessible to a non-specialist audience. The first is a clear, visual, integrative overview of the entire money system that illustrates the money creation process according to the increasingly accepted “credit theory” of money. So far, a few excellent visualizations have been provided of specific components or processes within the money system (see especially Ryan-Collins et al. [Citation2012] and Positive Money [n.d.]Footnote5); but a macro-visual model that clarifies the overall institutional picture accompanied by clear, simple explanations does not so far exist—not least within a single journal article. Such visual conceptualizations can be critical in facilitating better understandings of financial processes and practices that are particularly complex and unintuitive (Boehnert Citation2018; Shanks Citation2020). The second gap is a generalized disconnect between the technical and the sociological literature. The more technical literature (e.g., Ryan-Collins et al. Citation2012) provides unprecedentedly clear explanations of the operation of the money system but tends not to engage with broader normative debates about the system it is describing. Thus, in this more technical writing, it is not always clear what the relevance of today’s particular money system is for the very latest debates across the social sciences. Conversely, while providing this historical and political contextualization, the more sociological writing (e.g., Sgambati Citation2016; Koddenbrock Citation2019; Ingham Citation2020) tends not to provide the same complementary visual presentations as the more technical literature.

This article is therefore an attempt to address these gaps. To do this, it centers its analysis on an original visual figure that represents the whole money system. This figure attempts to explain how money comes into existence and which institutions have the authority to create it. The figure provides a basis for discussion of the implications of the current system for broader concerns about legitimacy and democracy. The article proceeds as follows. The next section introduces the set of theoretical debates that circumscribe this article, especially debates about where money comes from and who has the authority to create it. These debates relate to folk, neoclassical, and state-centered theories of money creation, as well as to emerging scholarship around the increasingly accepted “credit theory” of money creation. The following section introduces and explains fully the money system figure that has been developed as a visual conceptualization based on the credit theory of money creation. The next section reflects on the implications of the expositions of the money creation process and the broader money governance system for a range of contemporary macroeconomic debates before the article concludes.

Theories of money’s origins and originators: Folk, orthodox, state, and hybrid

There is considerable literature on money, especially within economics and economic sociology. This literature is diverse, analyzing issues such as what money is (i.e., whether it is a commodity or social relation, or both) (e.g., Ingham Citation2004; Sgambati Citation2016); what historical role money has played within the development of capitalism (e.g., Klein Citation2020; Koddenbrock Citation2019); how the socio-cultural context shapes how money emerges (e.g., Zelizer Citation1997; Graeber Citation2012; Mellor Citation2019); and what causes inflation (Wallace Citation2014). Although touching on these debates, this present article is speaking to a much narrower range of questions, namely: where does money come from?; which institutions can create it?; and what system of governance oversees its creation? This section will therefore discuss four main schools of thought relating to money creation and how they are generally applied within contemporary debates.

“Folk” tales

For some, the level of public confusion about money and its origins is related to the fact that the dominant public understanding is still based on what Braun (Citation2016, 1064) characterizes as a “folk” tale. While this tale contains an element of truth about historical banking processes,Footnote6 it clearly does not reflect the contemporary reality of money creation as outlined in the Bank of England’s 2014 document and elsewhere. At the heart of this folk tale is the idea of money as a scarce commodity that is linked to—or represented by—a precious metal, typically gold (Mellor Citation2019). How this money came into existence (or who issues it) is typically only vaguely articulated within this folk tale; but there is a general assumption that it is the government (or some other public authority) that creates the money that subsequently circulates within the economy and makes its way into the banks (Fessler, Silgoner, and Weber Citation2020; Kraemer et al. Citation2020).

Within this story, the money that has been deposited into banks can then be lent out to those who require it for consumption or investment, including even the government itself (Quinn Citation1994, Citation1995; Sgambati Citation2016). Banks are then effectively framed as mere “intermediaries” between borrowers and lenders, as opposed to being creators of money themselves (Ingham Citation2004). At this point, an additional element is typically added to the folk tale to explain the role of banks in regulating the money supply: the concept of a “fractional reserve” system. According to this system, banks lend out the majority of their customers’ deposits, leading to an expansion in the money supply. Banks are able to do this because—so the story goes—they have realized that most customers only ever come to claim a small amount of their money at a time for day-to-day expenditure. As well as expanding the money supply via the fractional reserve system, banks are understood to be able to make extra profits for themselves on the interest earned from lending out these otherwise “idle” savings (Quinn Citation1994). But while banks’ do indeed play a central role in expanding the money supply, the process through which they do this is completely mischaracterized within this “folk” tale, as will be explored in detail in subsequent sections of this article.

Neoclassical orthodoxy

Where more sophisticated understandings of today’s money creation process emerge, such as in discussions of business or finance, they tend to be based on what is taught within standard neoclassical economics (Di Muzio and Noble Citation2017). The main principle here is the “money multiplier” model of credit creation, which is outlined in Mankiw’s popular textbook, Macroeconomics (Citation2009), and which is taught in the vast majority of introductory courses on Economics (Ryan-Collins et al. Citation2012; Werner Citation2014a, Citation2014b). According to this model, banks first try to attract savers’ deposits, as per the “folk” story. The central bank then determines exactly what proportion of total customer deposits must be retained by commercial banks, and what proportion of deposits can be lent back out by the bank. This proportional figure is known as a “reserve requirement” and is typically around 10 percentFootnote7 (Ryan-Collins et al. Citation2012). If the reserve requirement is low, this means that banks can lend out the majority of their customers’ deposits. Conversely, if the reserve requirement is high, banks can lend out a smaller proportion of savers’ deposits. The central bank can, in this way—so the theory goes—regulate the amount of new credit that is created by regulating the amount of deposits that the banks are required to hold (Epstein Citation2006; Goodhart, Bartsch, and Ashworth Citation2016). As Neveu (Citation2020) observes, more advanced textbooks introduce the idea of interest being paid on central bank reserves to further explain how central banks influence banks’ loan-making activities.

This neoclassical rendering offers a more nuanced explanation of money creation than the folk story, especially in its involvement of central banks in the process. However, the neoclassical story still replicates core components—and omissions—of the folk story (e.g., Pearlman and Rebelein Citation2013). Most concernedly, it appears dramatically at odds with the recent developments in understanding of credit creation, such as those confirmed by the Bank of England and other central banks. Indeed, a key component of this neoclassical story of money creation is the fact that there must first be customer deposits before new loans can be created derived from those deposits (and based on the central bank’s reserve requirement) (Werner Citation2014a). It also asserts that banks are essentially just “intermediaries” between savers and borrowers (Ingham Citation2004). But if that is true, where did the money that customers are able to deposit in the bank to initiate the loan-making process originally come from? Did banks also create those initial deposits themselves, as proponents of the Banking School had argued for 200 years? (Huber Citation2016) Did the central bank or government create that money on behalf of the banks (as many members of the public still assume)? Or does the original source of money lie elsewhere? Because of its inability to address these questions, Di Muzio and Noble (Citation2017, 85) argue that the money multiplier “cannot explain the expansion of the money supply by logic, simple math and by basic bank accounting practices.”

State-based money theories

A different group of thinkers, emboldened by the ellipsis in the neoclassical explanation about money’s origins, propose an alternative understanding. Indeed, the theory of Chartalism, developed by the German theorist Georg Knapp in the 19th century, argues that the source of money is not the market (and banks) but rather the state or sovereign (Ingham Citation2004; Wray Citation2014; Huber Citation2016). Knapp argued that, historically, the state or sovereign was the institution to originally createFootnote8 money (in their mints) and then spend that money into the economy to pay for goods and services that it needed (e.g., supplies to fund wars or paying salaries to troops). This state or sovereign would then sustain demand for that currency by mandating that people pay taxes in it (Huber Citation2016). Those trying to create and circulate their own currencies without permission would be punished as it undermined the sovereign’s authority and monopoly control over money (Dodd Citation2016). Thus, money was a political contract between citizens and the state, as well as being a commodity that could be used to purchase goods and services within the market (Huber Citation2016). Chartalists also emphasize that modern money is ultimately a fiat creation, i.e., a form of money not backed by anything other than state authority; this contrasts with folk and (some) neoclassical stories that see money as ultimately backed by (and connected to) a physical commodity, such as gold (Sieroń Citation2019).

But while Chartalists’ “state theory” of money is somewhat supported by historical evidence, recent clarifications that it is indeed banks, and not governments, that are the main creators of new money clearly pose a challenge to the Chartalist story (Palley Citation2019). Governments/Sovereigns did once—and could again—become creators of the money supply, but the reality in many countries today is that it is now illegal for governments to either create and spend their own money or to borrow directly from their own central bank (a process termed “monetary financing”) (Huber Citation2016). Within the Eurozone, for example, Article 123 of the Maastricht Treaty prohibits member states from engaging in the monetary financing of governments by their central banks (Ryan-Collins et al. Citation2012), and IMF loans to countries generally explicitly prohibitFootnote9 borrowing countries from engaging in monetary financing (Ryan-Collins 2017). Some neo-Chartalists maintain that, because the state technically makes payments of reserves from its own central bank reserve account before receiving taxes from the public, this proves that states do indeed “create” money (e.g., Kelton Citation2020a). For others, though, this merely illustrates the idiosyncratic nature of the central bank reserve circuit, which allows those institutions with reserve accounts at the central bank to go into “overdraft” ahead of later settling their outstanding reserve balances (Huber Citation2014).

The growing consensus around money creation as a public-private “deal”

Amidst the polarized debates of “market” and “state”-centered theories of money creation, others have favored a hybrid characterization of today’s money governance system—as neither entirely “of the market” nor “of the state” but rather as a public-private “deal” between states and banks (Koddenbrock Citation2019). This interpretation incorporates ideas from both the “credit theory” of money (which was essentially the theory of commercial bank-driven money creation clarifiedFootnote10 by the Bank of England) and Chartalism. Overall, it sees money creation as a cooperative process between states and banks, as per the neoclassical rendering (Huber Citation2016; Ingham Citation2020). It also similarly casts commercial banks as the institutions that intermediate between the government and institutional investors when governments borrow money from institutional investors in exchange for the government’s own bonds (Ryan-Collins et al. Citation2012; Huber Citation2016). However, it ultimately casts commercial banks as the institutions that create the new money that appears (and subsequently circulates) within peoples’ bank accounts in the economyFootnote11 (Werner Citation2014a, Citation2016; Huber Citation2016). In this rendering, commercial banks then have the upper hand by virtue of the fact that they first decide if they are going to extend credit to a new “borrower” and only afterwards seek central bank reserves to back or “cover” the transaction (Huber Citation2016; Ingham Citation2020). Thus, as Ryan-Collins et al. (Citation2012, 122) argue:

banks do not need to wait for a customer to deposit money before they can make a new loan to someone else. In fact, it is exactly the opposite: the making of a loan creates a new deposit in the borrower’s account.

Werner (Citation2014a) has since run what he claims was the first “empirical test” of the credit theory of money creation, demonstrating that when banks create deposits on making a new loan, no transfers are made from other accounts at the bank when the loan is made: it is brand new money that is being created in the customer’s account at the same time as the bank creates a new asset for itself. Combined with the Bank of England’s own clarification of the process of money creation, this evidence presents a strong rebuttal to the orthodox story of money creation, as featured in Mankiw (Citation2009) and many other introductory textbooks. Thus, from this perspective, the process of deposit-taking is effectively independent of the loan-making process (Di Muzio and Noble Citation2017).

An empirical examination of modern money creation

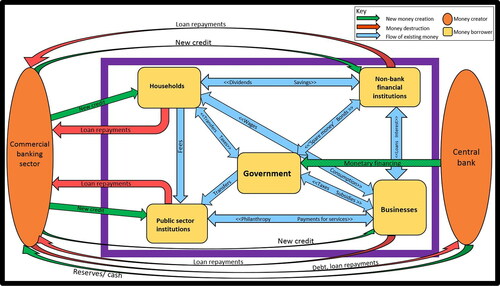

This section is based primarily on , which is an attempt to visually represent the “credit theory” of money creation that is becoming increasingly accepted as the most accurate characterization of the money creation process. The figure is the product of a comprehensive analysis of technical documents and sociological writings on money and attempts to integrate these into one figure. The development of this figure, alongside the explanation of the processes at work, is aligned with broader efforts to use metaphors, diagrams, and visual frames in order to re-frame the way we understand the world of money and finance (Shanks Citation2020). As Raworth (Citation2017, 21) states: if “we want to write a new economic story, we must draw new pictures that leave the old ones lying in the pages of last century’s textbooks.” The analysis is based on the current UK monetary system, which has remained largely unchanged since its establishment in 1694 with the founding of the Bank of England (Desan Citation2017). However, the focus on the UK should not be seen as provincial; although there are terminological differences between the UK’s money system and those of other countries’, the overall “monetary design” across nations today is remarkably uniform (Koddenbrock Citation2019). For example, while in the United States (U.S.), the national central bank (the Federal Reserve) is not a public but rather a privately owned entity operating according to a public mandate, the United States’ overall “monetary design” is, like the UK’s (and like that of many other countries’), characterized by a set of fairly standardized institutions. These include a network of commercial banks that create the money supply; a government with nonexistent money creation powers; and a national monetary governance system that entails ongoing coordination between public and private agencies (Feinig Citation2020). Another important reason for recognizing the transferability of insights about the UK’s system is the fact that the Bank of England’s 2014 clarification of the correctness of the “credit theory” of money creation is something that has multiple historical precedents. Indeed, as early as 1961, the Federal Reserve Bank of Chicago itself confirmed that “The actual process of money creation takes place primarily in banks” (Federal Reserve Citation1992, 3).

Figure 1. An Institutional Representation of the Money Creation Process.

Source: Author.

Within , there are several key features that need explaining. The figure is bounded by a black box, which could be considered as representing the boundary of the whole national economy. The purple box represents a legal-institutional boundary between those institutions that can and those that cannot create new money. Within the purple box, existing money circulates among users, but new money cannot be created. It is only outside the purple boundary that new money can be created by the two orange ovals: the commercial banks and the central bank. Every arrow in represents a different flow of money. Green arrows represent “newly created” money entering the economy via the commercial banks and central bank. Red arrows represent money “leaving” the economy as loan repayments by debtors. Blue arrows represent flows or transfers of money that have originally been “borrowed into existence” by a debtor but which thereafter circulates among entities within the economy simply as “money.” While orange ovals represent institutions that can create new money, yellow squares represent institutions that cannot create new money. They must borrow from others—either from other yellow squares within the purple square (which would be existing money, represented by blue arrows) or else by borrowing new money into existence from commercial banks (represented by the green arrows entering the purple box). The subsequent parts of this section are split into two: the first part explains the nature of the flows of money; and the second part explains the role of the different actors and institutions within the figure.

Money entering, leaving, and circulating within the economy

New money being created and entering the economy

The green arrows in represent new money being created.Footnote12 As can be seen, it is only commercial banks and the central bank that can create new money. However, it is only via the commercial banks as bankmoneyFootnote13 that new money can actually enter the economy in the form of deposits into the bank accounts of actors and institutions. Money created by the central bank cannot be received directly by any actor or institution within the economy, even the government. Money created by the central bank takes the form of “reserves” and must first enter commercial banks’ own reserve accounts before it can play any role in the money creation process (as will be explained).

The new bankmoney created by commercial banks enters a customer’s account when the customer takes out a loan. Effectively, customers “borrow new money into existence” when they take out a mortgage, business, personal, or other loans. As Huber (Citation2016, 62) summarizes: “by proactively extending credits into current accounts, thus creating bankmoney by primary credit, the banking sector determines the entire stock of money in public and interbank circulation.” By creating new deposits in customers’ bank accounts for them to spend within the economy in this way, banks enable consumption by the customer, who becomes a debtor to the bank for the amount of the loan. For Werner (Citation2014b), banks’ ability to create credit money is a consequence of them being exempt from the “client money rules.” The client money rules prevent nonbank organizations from creating new bankmoney, because nonbank organizations (for example, stockbrokers, solicitors, and accountants) are required to keep clients’ money separate from the nonbank organization’s assets and liabilities on their balance sheet.

By creating new bankmoney in this way, commercial banks are responsible for creating around 97 percent of all bank deposits in existence within the economy (Ryan-Collins et al. Citation2012). The remaining 3 percent comprises physical cash that the central bank first prints and mints before then selling to the commercial banks for distribution to customers.Footnote14 New bankmoney (i.e., deposits in customers’ accounts) can also be created by commercial banks when they “purchase assets” (such as securities) from the nonbank sector (Huber Citation2016). The bank receives these securities (which they then put on their own balance sheet as an “asset”), and in return, it creates new bankmoney deposits in the bank account of the nonbank business.

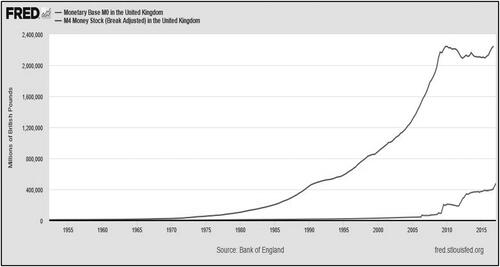

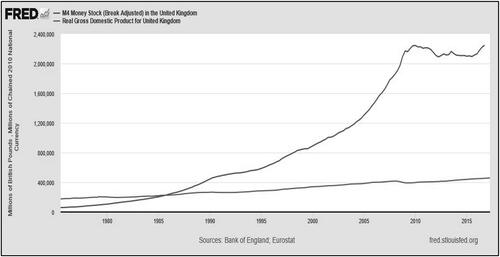

Creating new bankmoney (or credit) in this way is profitable for the bank, as the amount being returned to it is always greater than the amount it originally created. For example, for an average mortgage loan in the UK of £227,000, with an interest rate of 4.33 percent over 25 years, the customer will pay back £381,018 to the bank over the loan period. This means that the bank can claim £151,018 in profit for itself (the original £227,000 principal created is destroyed on repayment). Creating credit in this way has also become increasingly easy for commercial banks over the past few decades for several reasons. One is the de-linking of global currencies from any real commodity, such as gold, which ended in 1971 (Cohen Citation2018). This removed any obligation for banks or states to keep the money supply within any real material limits (Mellor Citation2019). A second reason is the financial deregulation since the 1970s, which relaxed rules on credit creation —in terms of both the amount that could be created relative to reserves and the geographic range within which institutions could create and lend money (Christophers Citation2013; Ryan-Collins et al. Citation2012). As a result of these two factors, the amount of new bankmoney created (what is technically referred to as M4 in the UK) increased from around £150 billion in 1963 to £2.8 trillion in 2020, as illustrated by (Bank of England Citation2021).

Figure 2. UK Money Supply, 1950–2021: Broad Money (M4) and Base Money (M0).

Source: Federal Reserve. https://fred.stlouisfed.org/series/MBM0UKM

As can be seen from , it is not only licensed commercial banks that can create new money; the central bank (orange oval) can also create new money. However, the money that the central bank creates is not the same as the bankmoney that circulates as either electronic bank deposits or physical cash within the economy; rather, it is a special type of official money known as “reserves” (technically referred to as M0, or “base” money, in the UK), which is used by commercial banks to settle balances between each other within the central bank “circuit.” Reserves are also used by the government to dispense payments (e.g., pay public sector salaries) and receive taxes—both of which it does via a convoluted “circuit” system that runs parallel to the main bankmoney system (more on this highly unintuitive concept in the next section). Reserves are generally created by the central bank to be temporarily swapped for banks’ assets, and so the creation of new central bank reserves does not in itself increase the total money supply within the economy; it is more of a “swap” of one type of money (reserves) for another (debt). This is represented by the red (“debt/loan repayments”) and green (“reserves/cash”) arrows at the bottom of . The creation of new central bank reserves has some influence over how much new credit banks are prepared to create, as will be explained in the next section.

Existing money circulating

As previously mentioned, the blue arrows in represent flows of money that was originally borrowed into existence (green arrows) by a borrower but which thereafter circulates within the economy among subsequent users. These users may receive this money in their salaries, may use it to pay taxes, and may use it for purchasing goods and services. However, these millions of transactions don’t add to the overall money supply: the money is just transferred from a bank account of one of the yellow squares within the economy to another. It is only through the creation of new bankmoney (by people within the economy borrowing new money into existence from commercial banks) that the money supply within the economy expands. As can be seen from , it is not only households, businesses, nonbank financial institutions, and public institutions who use this already-existing money for their spending purposes; it is also governments. Governments can either capture this circulating money by levying taxes, or else they can “borrow” money via a special mechanism known as issuing bonds. When governments issue bonds, they borrow “spare” bankmoneyFootnote15 from institutional investors who agree to temporarily “lend” the government this bankmoney in exchange for an interest-bearing government “bond” (called a “gilt” in the UK). Government borrowing therefore does not add new money to the overall stock of bankmoney in existence within the economy; it merely makes use of previously-created money that was not being used (Huber Citation2016).

Money leaving the economy and being destroyed

The flows of repayments of bankmoney from the yellow entities within the economy back to the commercial bank sector (the red arrows) represent money “leaving” the economy (Huber (Citation2016) terms this as money being “deleted”). As this money leaves the economy, the money supply shrinks; as such, the functioning of the economy depends on a continuous cycle of new money being created (through new borrowers borrowing money into existence) in order to compensate for those loans being repaid (Huber Citation2016). If no new loans are granted (i.e., if no new money is introduced into the economy via new loans being made) at the same time as money is continuously leaving the economy via the routine process of loan repayments (red arrows), the amount of money within the economy would—hypothetically—disappear. This dynamic is a result of the fact that money effectively exists purely as debt, and once the principal has been destroyed by being paid off, it no longer exists (Mellor Citation2019).

While all actors and institutions within the economy can use and hold the circulating money (blue arrows), it is only the original borrower who is faced with the loan contract with the bank, and who is therefore obliged to pay back the value of the money originally created in their account by the bank (the principal) plus the interest that the bank demands. Money itself then has a dual character, representing both (i) a credit-debt relationship between the creator of the credit (the bank) and the original recipient (the debtor) and, (ii) simply money that can then circulate within the economy. Thus, for Huber (Citation2016, 96):

there is no such thing as ‘debt money’ or ‘credit money.’ What really exists are credit-and-debt relationships on the one hand and money—just money—on the other hand, once a deposit has been entered into a bank account and starts circulating. It keeps circulating irrespective of the creditor-bank and debtor-customer that were at the origin of a respective amount of bankmoney. Only as the debtor pays back an according amount of money (principal plus interest) to the creditor-bank is that amount of bank-money deleted.

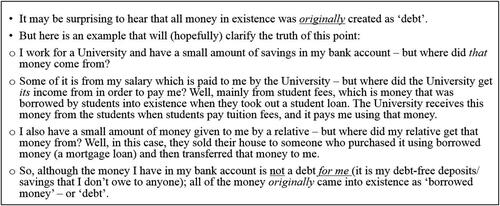

This understanding is, of course, distinct from the neoclassical story, where money is seen mainly as a commodity that is lent from a saver to a borrower simply to facilitate current spending or investment. provides an accessible explanation of how money comes into being as debt but can thereafter circulate among subsequent users “debt-free.”

Figure 3. A Practical Illustration of How Money is Created as Debt.

Source: Author.

Different actors’ roles in the modern money system

The money co-creation process: Private banks and the central bank

As is evident from the previous discussion, it is banks that are the prime creators of money within the economy. However, as was alluded to, this process depends on coordination and cooperation between the commercial banks and the central bank—hence it is a process that is best thought of as a “public-private deal” (Koddenbrock Citation2019, 2). As was also indicated, understanding exactly the nature of this coordination relies on grasping the notion of what Huber (Citation2016) terms a “split circuit” model of the money system, which consists of a “bankmoney” circuit comprising bankmoney (electronic and cash) created by commercial banks that actors and institutions within the economy use; and a central bank “reserve” circuit comprising reserves that circulate between the reserve accounts held by commercial banks and the government within the central bank itself. This arcane system has been around in various forms since the 17th century when the Bank of England was first established (Quinn Citation1995).

The bankmoney circuit comprises the customer bank accounts of all customers within the banking system. So, within the UK, this is 77 million bank accounts across 42 banks (FCA Citation2017). These bank accounts can only contain what Huber (Citation2016) terms bankmoney, which can also be withdrawn by the customer as cash. Indeed, as previously mentioned, 97 percent of all bankmoney is electronic, and only 3 percent is cash. Within these 77 million customer accounts are the £2.8 trillion of bankmoney deposits that customers hold from, for example, salary payments paid to them by firms or bank loans (FCA Citation2017). All of this bankmoney has originally been created by banks when someone, somewhere within the economy, has taken out a loan. The central bank circuit of reserve accounts, on the other hand, refers to a system of parallel accounts that all commercial banks have at the central bank. So, there are 42 banks in the UK, and therefore 42 commercial bank reserve accounts at the central bank (one for each bank) (Ryan-Collins et al. Citation2012). The UK government also has a reserve account at the Bank of England, known as the Consolidated Fund (this is the account it uses to receive taxes and execute spending). In these reserve accounts, commercial banks are required to hold a level of central bank reserves. They acquire these reserves by borrowing them from the central bank, by selling the central bank an asset, or else by borrowing them from a rival bank for an interest charge (Ryan-Collins et al. Citation2012; Huber Citation2016).

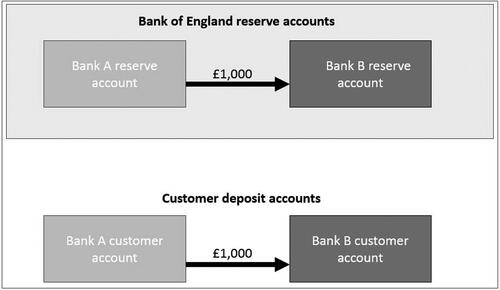

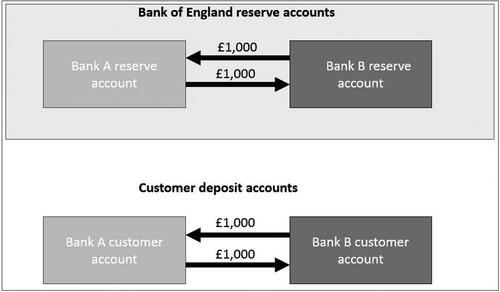

Central bank reserves are related to the money creation process in a complex way that will now be explained using and . Whenever a bank makes a new “loan” to a customer, the bank creates a new bankmoney deposit within the customer’s account equal to the value of the loan. It also creates an asset for itself of equivalent value, which represents the amount of money it is anticipating that the customer will pay back to it over the course of the loan period. (This is the rule of “double-entry bookkeeping,” where there must always be an equal amount of assets [what the bank is owed] and liabilities [what the bank owes] [Werner Citation2014a, Citation2014b]). At the same time, the bank must be prepared to transfer an amount of “reserves” equivalent to the value of the newly created bankmoney from its own reserve account at the central bank to the reserve account of a rival commercial bank, should the customer happen to spend the newly created bankmoney in such a way that it ends up in the account of someone at a rival bank. For example, in , it is seen that when the customer from Bank A transfers £1,000 of bankmoney from his/her customer deposit account at Bank A to a customer’s deposit account at Bank B, £1,000 of central bank reserves must also be ultimately transferred from Bank A’s central bank reserve account to the central bank reserve account of Bank B.

Figure 4. A Representation of the Relationship Between the Bankmoney and Central Bank Reserve Circuits.

Source: Adapted by Author from Ryan-Collins et al. (Citation2012).

Figure 5. A Representation of the “Canceling Out” of Transfers of Money Between Different Banks.

Source: Adapted by Author from Ryan-Collins et al. (Citation2012).

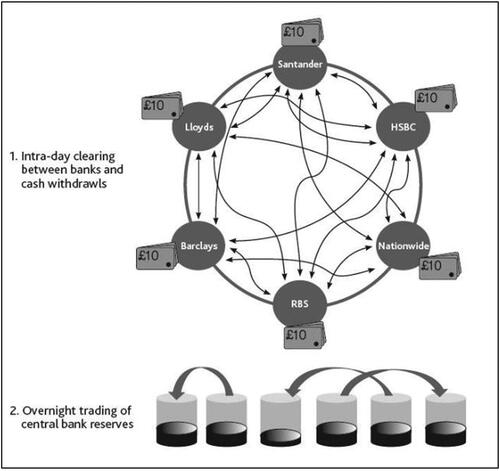

However, here is where the story gets complicated. This is because banks don’t have to transfer the actual reserves from their own account to the account of another bank “in real time”; rather, while real-time records of the multiple transactions between banks are recorded, “who owes what reserves to whom” among the 42 commercial banks is calculated at the end of every day, with outstanding debts settled between the 42 banks using their own stocks of central bank reserves (Ryan-Collins et al. Citation2012; Huber Citation2016). Banks have calculated from experience that the “outstanding” balances they will owe each other after all amounts have been tallied will typically only be a very small fraction of the total customer deposits within the banking system that have been transferred between accounts during any given day. This phenomenon is illustrated on a small scale in , where, as in , a customer from Bank A spends £1,000 from his/her account, which ends up in the account of a customer at Bank B. However, in this example, a customer from Bank B also spends £1,000 from his/her account that ends up in the account of a customer from Bank A. Thus, overall, even though £2,000 have been spent by customers on goods and services within the economy, neither Bank A nor B has any outstanding reserve balance with each other, and so zero reserves are required by either to settle with each other. Thus: the required movement of reserves in both directions has canceled the other out.

The upshot of this is that, over the course of a day, all such outstanding inter-bank reserve imbalances will most likely cancel themselves out, with only very small outstanding balances generally occurring, as illustrated in . Because of this canceling out process, commercial banks in most countries only need to hold a tiny percentage of the total value of the new bankmoney they create as reserves in their central bank reserve account. In many countries, this figure is as low as 1 percent (or even zero), although in others (where the banking system is less trusted or where there is a perception that excessive credit creation could drive inflation), the figure is as high as 20 percent (e.g., in China) (Ryan-Collins et al. Citation2012). Nonetheless, as banks are required to hold only a fraction of the value of the total new bankmoney they create as central bank reserves, this clearly enables them to create significantly more bankmoney as loans to customers than they hold reserves in their central bank reserve accounts. For instance, in 2010, banks held only £1.40 of reserves with the central bank for every £100 of new bankmoney they had created (Ryan-Collins et al. Citation2012). Because they have to hold only a small quantity of reserves at any one time, this enables larger banks in particular to use any “excess” reserves to purchase more profitable assets (Ryan-Collins et al. Citation2012).

Figure 6. A Representation of the Interbank Clearing Process.

Source: Ryan-Collins et al. (Citation2012).

Are there no limits to bank money creation?

The Bank of England’s 2014 clarification that commercial banks create new money in the act of lending led many to claim that this proved that money creation takes place “out of thin air,” or “out of nothing” (Wolf Citation2014). Others argue that banks’ obligation to transfer equivalent reserves to another bank as their own customers transfer bankmoney means that the “out of thin air” characterization doesn’t hold (e.g., Rendahl and Freund Citation2019). However, Huber (Citation2016) argues that banks still ultimately take the lead in creating unlimited amounts of new money even in the absence of reserves; and only need to think about “covering” this money with reserves at a later date. And in practice, banks know that their demand for reserves will always be accommodated by the public central bank, which ultimately wants to do everything it can to encourage new borrowing (Hail Citation2018). So, what does limit banks’ credit creation?

For McLeay, Radia, and Thomas (Citation2014), the single biggest potential brake on new credit creation by commercial banks is the interest rate demanded by central banks on reserve borrowing: if it is very costly for commercial banks to obtain reserves, it will mean that they will have to pass on these costs to consumers in the form of higher interest rates, reducing consumer demand for loans and reducing overall credit creation. There are, however, further important non-monetary policy brakes on credit creation. In a logical economic sense, banks will not create credit where they see that there is a danger that the loan they create will not be paid back by a risky or unreliable borrower (MacKenzie Citation2011). This is because, if a customer does not pay back their loan to the bank, the bank will have to “write off” the asset represented by the customer’s loan from its own balance sheet (Carruthers and Ariovich Citation2010). This asset was something of financial value that the bank could have otherwise sold to another investor; it also represented an asset that the bank could have used to access additional central bank reserves, and it was a long-term source of profits in terms of interest payments (Huber Citation2016). Most crucially, even though the bank will have lost the asset, it is still obliged (i.e., it is “liable”) to transfer some of its own reserves equivalent to the loan value to another bank, in the event that its own customer spends the newly created bankmoney (loan) in such a way that it ends up in a customer’s account at another bank (as outlined above).

There are also a number of further institutional and financial restrictions on banks’ new money creation activities beyond the need to somehow obtain reserves to settle interbank balances. One such limit is the Basel III rules, introduced in 2013, which state that banks can only create a certain multiple of new bankmoney (credit) relative to their own capital value (Huber Citation2016). This means that banks are—in theory—restricted from creating new bankmoney (credit) once the value of their own loan portfolio reaches a certain multiple of the total value of the bank (i.e., what the bank is “worth” once it has sold all its assets and returned all its deposits to its customers). However, as well as the fact that these rules are not strictly enforced, banks have found creative ways around them by, for example, artificially increasing their own value by issuing shares, thus enabling them to increase the amount of new credit that they create (Werner Citation2016). A more serious limit on new credit creation was seen in 2008, when a lack of confidence among banks led new credit creation to freeze up. Suspecting that their rivals were holding “bad” debts, banks lost confidence in each other’s ability to transfer reserves as part of the interbank settlement process (Langley Citation2014). They thus stopped lending to each other, and the central banks had to step in to inject billions of new reserves into commercial banks’ reserve accounts in exchange for their bad assets.

The “borrowers” of money

Governments

In , the government is shown as a yellow square within the economy, signifying that it cannot create money to spend. The money it spends is what it has captured from the economy in the form of taxes, which are paid by the publicFootnote16 (the blue arrows directed toward the government from other institutions within ). Where governments need to “run a deficit” (i.e., spend more than they have raised in taxes), they can borrow “spare” bankmoney from institutional investors (e.g., the savings of pension holders that institutional investors are looking to invest on their behalf). The two main stages of this process as it occurs in the UKFootnote17 are as follows. First, a group of large banks known as the Gilt-edged Market Makers (GEMMs)Footnote18 agree to sell newly issued government bonds (gilts) on behalf of the government’s Debt Management Office (DMO) (1). The GEMMs sell these gilts to institutional investors, who pay for them via their own commercial bank account: the institutional investor’s deposit account at their commercial bank is deducted the amount equal to the gilts’ value; meanwhile, the institutional investor’s commercial bank transfers equivalent reserves to the reserve account of the relevant GEMMFootnote19 (McLeay, Radia, and Thomas Citation2014). The GEMMs then pass these reserves to the government’s DMO, which in turn sends these to the Consolidated Fund as fresh reserves for the government to spend (2). At the end of the agreed period of the bond (which can be anywhere from a few months to 50 years), the government can choose to return the reserves to the investors via the reserve accounts of the GEMMs (3). The investors will return the bond to the government (DMO) via the GEMMs (4). Overall, the government has been able to make use of “idle” money within the financial system (e.g., institutional investors’ money) by receiving it in the form of reserves, and investors have benefited from the interest earned on lending the government their savers’ money.

Nonbanks, households, businesses, and public institutions

The remaining yellow squares in represent the actors and institutions that cannot create or originate money. For example, nonbank institutions (which could include hedge funds, private equity firms, and International Financial Institutions (IFIs) such as the International Monetary Fund (IMF)) cannot create new money; however, they can borrow money from the commercial banks (as newly created credit) or from any other actor within the economy (in the form of already-circulating money) and then use that money for whatever purpose they wish (Huber Citation2016). They may then lend this money back out to others at a higher rate of interest (thereby profiting from the difference) (e.g., payday loan companies). Or they may buy up other financial assets (such as property or shares) with the hope of selling them for a higher price in the future (Huber Citation2016). Nonbanks such as institutional investors are also major lenders of “spare” money to the government, as outlined above.

For actors and institutions such as households and businesses, many activities, such as buying houses or paying for university, cost much more than salaries or savings can cover; and so those activities tend to necessitate borrowing money (Montgomerie Citation2019). These actors and institutions then have two options: borrow new money into existence from the private/commercial banking sector (the orange oval on the left of ) or else borrow from the “nonbank” financial institutions (yellow squares) such as payday loan companies (Langley et al. Citation2019). Public institutions are in the same position as households and businesses, although they may also be able to rely on transfers of money from the government that the government itself has obtained via taxes or borrowing (as per the blue arrows in ); they may also access private sector credit via various public-private financing arrangements (Broadbent and Laughlin Citation2005). Larger corporations and some public bodies may also borrow money by issuing bonds, similar to the process described for governments.

Discussion

This section will now reflect critically on some of the implications of these expositions of the modern money creation process for a range of contemporary macroeconomic and normative debates. While there are multiple debates stimulated by this clearer understanding of money creation, this section will focus on the following issues: questions about monetary sovereignty; public spending; the privatization of credit creation; and the debt-based nature of the money system.

Monetary sovereignty and the state

The preceding analysis has shown how governments can only spend money that they have collected from within the economy as taxes, and if they need additional money, they must borrow from private creditors, such as pension funds (or indeed public creditors, such as foreign governments). The conventional justification for building these restrictions into the “monetary design,” to use Desan’s (Citation2017) term, is that limiting government money creation prevents a politicization of spending that has led elsewhere in history to hyperinflation and instability (Epstein Citation2019). The role of the central bank and GEMMs in the bond issuance process meanwhile ensures that government borrowing is always “market-tested,” and that it doesn’t direct scarce money away from the private sector (the so-called “crowding out” argument) (e.g., Palley Citation2019; Mueller Citation2019).

The limited role for governments in money creation, however, continues to be a source of debate, particularly in the so-called “austerity” era, with the public increasingly asking why governments are unable (or unwilling) to create and direct new money in ways that mobilize domestic resources or drive counter-cyclical growth (Kelton Citation2020a). The lack of action appears stark when contrasted with the ease with which billions of dollars have been conjured up by central banks over the past decade in order to “bail out” failing commercial banks and corporations (Wray Citation2014). Neo-Chartalists claim that these restrictions are undemocratic and that states should exert more democratic control over money. Some argue, for example, that money should be able to be channeled directly from the central bank to the government (the checked green “monetary financing” arrow in ). Some scholars have highlighted that such monetary financing of government spending has been used multiple times in history (e.g., in Canada between 1945 and the 1970s) and does not necessarily lead to hyperinflation (Ryan-Collins 2017). “Public money” and “sovereign money” reformers meanwhile argue the central bank (or a public alternative) should take over the role as the ultimate creator of the money supply (Dyson, Hodgson, and Lerven Citation2016). These measures would—in theory—reduce the government’s debt and borrowing costs: for example, the UK government currently owes more than £2.3 trillion to various creditors and pays more than £50 billion per year in interest on the money it has borrowed (OBR Citation2021).

The COVID-19 period has proved particularly interesting for these debates as it has seen central banks, such as the Bank of England, create vast new reserves in order to buy up previously issued government bonds that private investors, such as pension funds, were holding (Myant Citation2020). Private investors have then used their freshly received reserves to buy up newly issued UK government bonds, in accordance with the process of government borrowing outlined above—effectively enabling these investors to replace the government bonds they were holding with newly issued ones. The government has meanwhile had a debt that was owed to a private investor (the government bond) transferred over to the books of the central bank, which will (most likely) not demand that the government pay it back. The government has also—ultimately—gained access to new money to borrow via the act of central bank reserve creation. These developments have led some to argue that central banks have effectively been engaging in the indirect monetary financing of governments. Murphy (Citation2020) and Kelton (Citation2020b) argue that central banks follow the above process—rather than simply engaging in the direct monetary financing of governments—in order to sustain the illusion that money is still effectively being “borrowed” by governments from the private sector. These transactions nonetheless highlight the actual degree of freedom and creativity that could be used to create and direct credit for any other hypothetical purpose, such as a “Green New Deal” (Galvin and Healy Citation2020).

The limits to public spending

Connected to these debates is the question of whether or not governments themselves have a “magic money tree” that they can summon to pay for the things that are judged as necessary within society (Montgomerie Citation2019). As the preceding analysis has demonstrated, the answer is clearly: at present, no. Governments cannot create their own money, nor can they borrow (anymore) directly from their own central bank. They can borrow money from institutional investors and run deficits, and for countries such as the UK and United States, this is far easier to do than for countries in the Global South (Alami Citation2018; Kaltenbrunner and Painceira Citation2018). This is because Global North countries can borrow cheaply in their own currency due to the large stores of “spare” U.S. dollar and other main currencies available within the global financial system (e.g., around 60–70 percent of all currency in existence is U.S. dollar currency) (Ito and McCauley Citation2020). For Global South countries that are lower down the “currency hierarchy,” on the other hand, their own domestic financial markets tend to be small, and so they will have to borrow in more expensive foreign currencies. In so doing, they will be charged higher interest and will be exposed to currency market fluctuations out of their control (Hardie Citation2011; Eichengreen and Flandreau Citation2012).

Even for powerful economies, though, there may be financial, ideological, and political restrictions on government borrowing. In many countries, there are externally imposed limits on government borrowing. For example, in the Eurozone, member countries are required by Stability and Growth Pact (SGP) rules to keep the size of their deficits to within 3 percent of Gross Domestic Product (GDP) (Koehler and König Citation2015). Countries taking out IMF (and other) loans also face the imposition of strict borrowing conditions, as the IMF itself acknowledges (e.g., Kern, Reinsberg, and Rau-Goehring Citation2020). There may also be ideological limits on what is considered an acceptable level of borrowing among neoclassical commentators and market actors, who will be able to “punish” governments that they perceive to be borrowing too much by betting against their bonds or currencies (Rommerskirchen Citation2015).

The privatization of credit creation

Further concerns about the current money creation model relate to the fact that it is private interests that largely determine decisions over new destinations for credit (Werner Citation2014a, Citation2014b, Citation2016). In many countries, these private interests constitute an increasingly small numberFootnote20 of very large banks—itself a product of deregulation-driven consolidation (Block Citation2019). This means that a relatively small number of institutions now exert significant economic and political influence over the direction and character of development (Robinson Citation2017). Some argue that this banking structure creates a bias toward large-scale, profit-driven lending, and a reluctance to invest in small firms (Werner Citation2014a, Citation2014b, Citation2016; Lee, Sameen, and Cowling Citation2015). Others have observed that, in the absence of credit guidance, banks tend to create more credit for asset purchases, such as stocks and property, driving up prices in those markets (Green and Lavery Citation2015). For example, in recent years, Shaxson (Citation2018) has shown how only 25 percent of bank lending is now made to the “productive” economy, with 75 percent of loans being made for purchases of financial assets (e.g., debt or shares) and property. Such patterns are clearly beneficial for banks and for those holding such assets (largely the wealthiest in society), but they also mean that banks play an active role in widening and systematizing asset-based inequality (Piketty Citation2018). As credit creation is dictated purely by the profit and risk calculations of banks, a significant amount of credit creation still goes to “legacy” (and still-profitable) sectors, such as the fossil fuel sector (Semieniuk et al. Citation2021). Some argue that this is stalling the transition to more sustainable pathways and that, as a result, states and central banks need to intervene to make credit less expensive for lending to “green” sectors (Svartzman et al. Citation2021; Campiglio et al. Citation2018). However, these patterns of private sector credit creation have also been replicated in the public central bank asset purchase programs of the last decade, where central banks used newly created reserves to buy up a large amount of debt and equity in so-called “brown” sectors (such as fossil fuels) (van’t Klooster and Fontan Citation2020).

The long-term impacts of a debt-based system

A final set of debates concern the implications of the mushrooming level of debt that is a function of an inherently debt-based money system (Langley et al. Citation2019). For some, a build-up of debt only becomes a problem when borrowers fail to manage their finances responsibly (Montgomerie Citation2019). And yet, for others, there are a number of reasons to be concerned about a debt-based economy. Mounting debt generates stress for individuals and creates a burden that psychologically hangs over the future, limiting choice and freedom (Harker, Sayyad, and Shebeitah Citation2019). Moreover, the tradability of debt presents a concerning information asymmetry problem, where those buying debt as a way of earning a regular stream of income (e.g., from a set of mortgage borrowers repaying their loans) lack information about the financial circumstances of the mortgage holders themselves. This latter dynamic was, of course, a key catalyst of the 2008 global financial crisis (Montgomerie Citation2019).

A broader set of debates concern exactly why society has become so much more reliant on debt in the first place (Dagdeviren et al. Citation2020; Streeck Citation2014; Klein and Winkler Citation2019). For example, in the UK, the level of public debt increased from 40 percent of GDP in 1994 to 85 percent of GDP in 2020; the level of private household debt meanwhile increased from 50 percent of GDP to 90 percent of GDP over the same period (ONS 2021; BIS Citation2021). As illustrated by , new bankmoney (M4) has dramatically outstripped GDP in the UK since the 1980s. In this regard, there has been considerable attention on the possible factors that explain why both private individuals and institutions, and governments within the purple square of ’s economy are having to borrow more and more money. Factors examined within the literature related to public debt include: falls in corporation tax takes (Streeck Citation2014); tax avoidance and evasion (McBride and Evans Citation2017); and costly public-private partnership agreements (Kellaway Citation2008). Factors examined related to private debt include privatization of formerly public services that now have to be paid for (Roberts Citation2016), decreasing real wages due to low union power (Johnston, Fuller, and Regan Citation2021), declining state benefits (Cooper and Paton Citation2021), and rising costs of living (especially for housing) due in part to what Ryan-Collins (Citation2021, 480) terms the “housing-finance cycle.”

Figure 7. Broad Money (M4) and GDP in the UK, 1970–2021. Source: Federal Reserve. https://fred.stlouisfed.org/series/MBM0UKM

Indebtedness may not, however, only be a social concern: it may also relate to the environment and climate change. Some critics have argued that the debt-based money system is an inherent obstacle to sustainability. This is because—so they suggest— money’s interest-bearing nature means that further growth is always required to enable economic actors to produce enough to service the principal plus the interest charged by the bank (Binswanger Citation2009). While acknowledging the “intuitively appealing” nature of this relationship between interest and growth, Jackson and Victor (Citation2015, 32), running Stock-Flow Consistent models, found no evidence of a “growth imperative” driven by the existence of interest-bearing debt. They argue that, because the interest payments from those who borrow money often end up back within the economy as salaries of bank workers and are not in reality “withheld” by banks, further material growth in the economy is not necessarily required to service existing debts (ibid.). They do, however, acknowledge the need to reform the current money system, which they claim drives “unsustainable levels of public and private debt, increased price and fiscal instability, speculative behavior in relation to environmental resources, greater inequality in incomes and in wealth, and a loss of sovereign control of the money system” (Jackson and Victor Citation2015, 46).

Conclusion

I have attempted to explain in this article how money is created—and, crucially, by whom—according to the increasingly accepted “credit theory” of money creation that was clarified by various central banks over the past decade. It has shown that commercial banks and central banks are the only sets of institutions that can create new money, either in the form of new “bankmoney,” which is created by commercial banks when they extend credit to customers; or “reserves,” which exist purely within the central bank “circuit.” While central banks can create new reserves for commercial banks, they cannot, however, channel these reserves directly to other actors and institutions within the economy. New money can enter people’s bank accounts only as bankmoney created by a customer taking out a new loan. Thereafter, it circulates for subsequent users within the economy as salaries and payments and remains only as a credit-debt relationship for the original borrower. Governments, nonbanks, households, nor businesses can create money, and they therefore all must rely on obtaining either existing circulating money or else borrowing new money into existence from banks. As Koddenbrock (Citation2019) has characterized, the money governance system is best thought of as a “public-private deal” between states and banks, in which banks nonetheless take the lead in creating new money by extending loans.

I have also attempted to reflect on the relevance of the updated empirical realities described for broader macroeconomic and normative debates, including questions around monetary sovereignty, public spending, growing private debt, and the relationship between money creation and “just” transitions toward sustainability. Because many argue that monetary institutions are currently not serving—or not operating according to—the broader public purpose, it is sometimes said that “something needs to be done” to reform them (Feinig Citation2020). The first task, however, is to understand them, and it is hoped that this article’s exposition of the processes of modern money creation has provided a constructive pedagogical tool upon which both technical and normative discussions among academics, activists, and students about our current money system can be based.

Acknowledgments

The author thanks three anonymous reviewers for their very helpful comments on previous drafts of this article, and Professor Joseph Huber for the valuable email exchanges over the years.

Additional information

Funding

Notes

1 The post-2008 instances of so-called “quantitative easing” and the COVID-19-era instances of large-scale central bank money creation have complicated even this interpretation, as will be discussed later on in the article.

2 For example, see Jordan (Citation2018).

3 See Nietlisbach (Citation2015).

5 For example, see https://positivemoney.org/how-money-works/advanced/how-do-banks-become-insolvent/

6 For an excellent overview, see Davies (Citation2010).

7 The reserve requirement is however around 1 percent in most industrialized countries, and is zero in the UK (Ryan-Collins et al. Citation2012).

8 This is known as an exogenous theory of money creation, where the origin of money is determined outside the banks, with the banks serving the role as mere intermediaries of this pre-existing money.

9 See for example Kern, Reinsberg, and Rau-Goehring (Citation2020).

10 See Jakab and Kumhof (Citation2015).

11 Also known as the endogenous theory of money creation (Ingham Citation2004).

12 In line with the reality described by the credit theory of money, terms such as “created” and “destroyed” will be generally favored over terms such as “lent” and “borrowed” to reflect the fact that no money is technically being “borrowed” from anyone else in order to be “lent.” (See McLeay, Radia, and Thomas [2014] and Werner [2014b]). The exception to this is the area of government borrowing, where it is (to an extent) true that already-existing, “idle” bankmoney within the financial system (invariably pension savings being held and managed by institutional investors) is lent temporarily to governments for them to fund their own spending.

13 This is the term used by Huber (Citation2016) to distinguish the type of electronic and physical cash money that circulates within the “circuit” that consists of customers’ bank accounts. It is distinct from the “reserves” which are the type of official money that circulates purely within what Huber characterizes as the central bank “circuit.”

14 For Huber (Citation2016), physical cash (notes and coins) is not a different type of money, but rather a physical version of customers’ bankmoney.

15 Although governments are, in effect, temporarily borrowing bankmoney held by institutional investors, confusingly, they do not literally receive this bankmoney as bankmoney. Rather, as will be described in the next part, a group of commercial banks borrow that bankmoney from the institutional investors on the government’s behalf, and transfer equivalent reserves to the government’s own account within the central bank reserve system, (in the UK known as the “Consolidated Fund”).

16 The government does not literally receive the money that the public pays in taxes directly as bankmoney. Rather, when a business or a household pays taxes to the government, their own bank accounts are marked down (i.e. bankmoney is deducted), while the Consolidated Fund (the government’s ‘reserve’ account) receives reserves of an equivalent amount from the reserve account of the relevant commercial bank that the household or business is banking with.

17 Although the terminology in other countries will differ from that of the UK’s, the broad process being described here will more or less be the same. See, for example, the Swedish government’s bond issuance process as described on the Swedish National Debt Office’s Web site: https://www.riksgalden.se/en/our-operations/central-government-debt/how-does-the-government-borrow/

18 These include banks such as Santander, Barclays Bank, BNP Paribas, Goldman Sachs, and HSBC. See https://www.dmo.gov.uk/responsibilities/gilt-market/market-participants/

19 This procedure happens this way because institutional investors such as pension funds do not hold a ‘reserve’ account with the Bank of England; thus, the commercial bank with whom they hold a bank account acts as an intermediary. At the end of this part of the transaction, deposits are deducted from the pension fund’s commercial bank deposit account, and they receive the gilts in return. The pension fund’s commercial bank meanwhile transfers equivalent reserves to the relevant GEMM’s commercial bank reserve account, so that they can in turn pass these on to the government’s own reserve account.

20 For example, between 1990 and 2010, 37 U.S. banks became four huge banks: JP Morgan Chase, Bank of America, Wells Fargo, and Citigroup (Adams and Gramlich Citation2014). In countries such as the UK, a similar pattern has emerged, particularly through the 2008 crisis period. In the UK, for example, six banks (RBS, Barclays, HSBC, Lloyds Banking Group, Santander, and Nationwide) together account for almost 80 percent of the stock of UK customer lending and deposits (Davies et al. Citation2010).

References

- Adams, R. M., and J. P. Gramlich. 2014. Where are all the new banks? The role of regulatory burden in new charter creation. Washington, DC: Board of Governors of the Federal Reserve System (U.S.).

- Alami, I. 2018. Money power of capital and production of ‘New State Spaces’: A view from the global south. New Political Economy 23 (4): 512–29. doi: https://doi.org/10.1080/13563467.2017.1373756.

- Bank of England. 2021. M4 Database. https://www.bankofengland.co.uk/boeapps/database/fromshowcolumns.asp?Travel=NIxAZxSUx&FromSeries=1&ToSeries=50&DAT=RNG&FD=1&FM=Jan&FY=1963&TD=31&TM=Dec&TY=2025&FNY=Y&CSVF=TT&html.x=66&html.y=26&SeriesCodes=LPMAUYM&UsingCodes=Y&Filter=N&title=LPMAUYM&VPD=Y (accessed March 25, 2021).

- Binswanger, M. 2009. Is there a growth imperative in capitalist economies? A circular flow perspective. Journal of Post Keynesian Economics 31 (4): 707–27. doi: https://doi.org/10.2753/PKE0160-3477310410.

- BIS. 2021. Total credit to households (core debt) As a percentage of GDP. https://stats.bis.org/statx/srs/table/f3.1 (accessed March 26, 2021).

- Block, F. 2019. Financial democratization and the transition to socialism. Politics & Society 47 (4): 529–56. doi: https://doi.org/10.1177/0032329219879274.

- Boehnert, J. 2018. Anthropocene economics and design: Heterodox economics for design transitions. She Ji: The Journal of Design, Economics, and Innovation 4 (4): 355–74. doi: https://doi.org/10.1016/j.sheji.2018.10.002.

- Braun, B. 2016. Speaking to the people? Money, trust, and central bank legitimacy in the age of quantitative easing. Review of International Political Economy 23 (6): 1064–92. doi: https://doi.org/10.1080/09692290.2016.1252415.

- Broadbent, J., and R. Laughlin. 2005. The role of PFI in the UK government’s modernisation agenda. Financial Accountability and Management 21 (1): 75–97. doi: https://doi.org/10.1111/j.0267-4424.2005.00210.x.

- Campiglio, E., Y. Dafermos, P. Monnin, J. Ryan-Collins, G. Schotten, and M. Tanaka. 2018. Climate change challenges for central banks and financial regulators. Nature Climate Change 8 (6): 462–68. doi: https://doi.org/10.1038/s41558-018-0175-0.

- Carruthers, B. G., and L. Ariovich. 2010. Money and credit: A sociological approach, Vol. 6. Cambridge, UK: Polity.

- Christophers, B. 2013. Banking across boundaries: Placing finance in capitalism. Hoboken, NJ: John Wiley & Sons.

- Cohen, B. J. 2018. The geography of money. Ithaca, NY: Cornell University Press.

- Cooper, V., and K. Paton. 2021. Accumulation by repossession: The political economy of evictions under austerity. Urban Geography 42 (5): 583–602. doi: https://doi.org/10.1080/02723638.2019.1659695.

- Dagdeviren, H., J. Balasuriya, S. Luz, A. Malik, and H. Shah. 2020. Financialization, welfare retrenchment and subsistence debt in Britain. New Political Economy 25 (2): 159–73. doi: https://doi.org/10.1080/13563467.2019.1570102.

- Davies, G. 2010. History of money. Cardiff, UK: University of Wales Press.

- Davies, R., P. Richardson, V. Katinaite, and M. J. Manning. 2010. Evolution of the UK banking system. Bank of England Quarterly Bulletin, Q4. https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2010/evolution-of-the-uk-banking-system.pdf?la=en&hash=1B96013BA769A71DD3E49FE4590FD8719DA767A1 (accessed March 2, 2021).

- Desan, C. 2017. The constitutional approach to money. In Money talks: Explaining how money really works, ed. N. Bandelj, F. F. Wherry, and V. A. Zelizer, 109–30. Princeton, NJ: Princeton University Press.

- Di Muzio, T., and L. Noble. 2017. The coming revolution in political economy: Money creation, Mankiw and misguided macroeconomics. Real-World Economics Review 80 (2017): 85–108.

- Dodd, N. 2016. The social life of money. Princeton, NJ: Princeton University Press.

- Dyson, B., G. Hodgson, and F. V. Lerven. 2016. Sovereign money. An introduction. http://positivemoney.org/wp-content/uploads/2016/12/SovereignMoney-AnIntroduction-20161214.pdf (accessed March 20, 2021).

- Eichengreen, B., and M. Flandreau. 2012. The Federal Reserve, the Bank of England, and the rise of the dollar as an international currency, 1914–1939. Open Economies Review 23 (1): 57–87. doi: https://doi.org/10.1007/s11079-011-9217-1.

- Epstein, G. 2006. Central banks as agents of economic development. No. 2006/54. WIDER Working Paper Series from World Institute for Development Economic Research. https://econpapers.repec.org/scripts/redir.pf?u=https%3A%2F%2Fwww.wider.unu.edu%2Fsites%2Fdefault%2Ffiles%2Frp2006-54.pdf;h=repec:unu:wpaper:rp2006-54

- Epstein, G. A. 2019. What’s wrong with modern money theory?: A policy critique. Springer.

- Federal Reserve Bank of Chicago. 1992. Modern money mechanics: A workbook on bank reserves and deposit expansion. Chicago: Federal Reserve Bank of Chicago.

- Feinig, J. 2020. Toward a moral economy of money? Money as a creature of democracy. Journal of Cultural Economy 13 (5): 531–47. doi: https://doi.org/10.1080/17530350.2020.1729223.

- Fessler, P., M. Silgoner, and R. Weber. 2020. Financial knowledge, attitude and behavior: Evidence from the Austrian Survey of Financial Literacy. Empirica 47 (4): 929–47. doi: https://doi.org/10.1007/s10663-019-09465-2.

- Financial Conduct Authority (FCA). 2017. Retail banking sector: Overview. Accessed March 25, 2021. https://www.fca.org.uk/publication/research/rb_sector_overview_final_jan17.pdf.

- Galvin, R., and N. Healy. 2020. The green new deal in the United States: What it is and how to pay for it. Energy Research & Social Science 67 (2020): 101529. doi: https://doi.org/10.1016/j.erss.2020.101529.

- Gamble, R. C. 1991. The money-creation model: Another pedagogy. Journal of Economic Education 22 (4): 325–29. doi: https://doi.org/10.1080/00220485.1991.10844725.