?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Article title: On a discrete-time risk model with time-dependent claims and impulsive dividend payments

Authors: Lianzeng Zhang and He Liu

Journal: Scandinavian Actuarial Journal

DOI: http://dx.doi.org/10.1080/03461238.2020.1726808

The authors regret to inform the reader that the structural form of has to be adjusted. For

, the identity

does not hold, and

should be treated in the following manner. Since

for

, it follows from (10) that

,

. Hence, formula (15) should read

(15)

(15)

Analogously, by noticing the identity ,

, formula (40) should read

(40)

(40)

Under the above-mentioned modifications, it happens that the numerical results for 's and

remain unchanged, while the numerical results for

's and

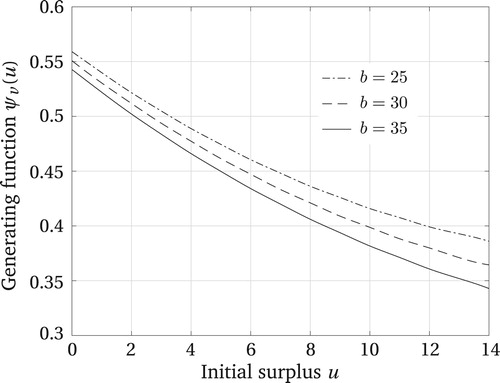

are different from the original. As the values of

in Figures 1(a), 2(a) and 3(a) change slightly, the corresponding observations are still valid. However, the numerical results in Figure 4(a) change a lot (see and Figure below). It is shown that a larger value of b corresponds to a larger expected time of ruin, when a is fixed.

Figure 4. Impact of b on for a = 20.