ABSTRACT

The benefits of biofuels depend on the feedstock, conversion pathway and local context. This paper assesses biofuels technology readiness and developments to provide foresight to biofuels development in Southern Africa. Efficient conversion pathways, coupled with biomass from waste or high-yielding energy crops, will reduce both the costs of biofuels production, and the environmental impacts. Compared to petroleum fuels, the current commercial biofuels (ethanol, biogas and biodiesel) typically offer carbon emission reductions of 30–50% but are marginally more expensive. The extent of biofuels market penetration will therefore be influenced by mandates (blending targets) and subsidies (green premium). Advanced biofuels promise greater efficiencies and carbon emission reductions at reduced cost but will require further research and development to reach commercialisation. If developed appropriately, biofuels can reduce carbon emissions and improve energy security, while enabling sustainable agriculture and improved natural resources management.

1. Introduction

Biofuels are energy carriers derived from biomass. Biofuels include liquid, solid and gas fuels (such as wood pellets, biogas, ethanol and biodiesel) which are used to deliver renewable energy services in the form of heating and cooling, electricity and transportation. There are various biomass sources that can be converted to biofuel products via thermochemical, physicochemical and biochemical processes. For transportation, liquid biofuels are seen as the preferred route to easily replace current liquid petroleum fuels, since this incurs relatively little additional infrastructure cost, and offers an immediate route to decarbonise the transport system. However, the use of electric vehicles, hydrogen and compressed biomethane are becoming increasingly attractive alternatives to the current liquid fuels and internal combustion engines used in the prevailing transport system.

Biofuels can deliver benefits to society, such as reducing greenhouse gas emissions and the dependency on fossil fuels, and offering new opportunities for socio-economic development. The global demand for biofuels is expected to grow rapidly because of mandates to reduce carbon emissions, and the escalating prices of finite petroleum fuels. Most of the growth is expected to come from the United States and the European Union, but many other countries also have biofuel mandates and targets that will drive biofuels demand and growth. The predicted increase in the demand for biofuels will provide opportunities for African exporters, because neither the European Union nor the United States is expected to be able to meet their consumption mandates completely from domestic production. In addition, African countries generally have abundant natural resources and high unemployment, and the cultivation of biofuel feedstocks therefore offers opportunities for economic growth and rural development. The domestic markets for biofuels are also expected to grow as many African countries face high fuel prices and energy security issues, as well as a rapid growth in energy demand. Southern African countries, with the exception of Angola, have limited oil reserves and require imports to meet the region’s needs (Feygin & Satkin Citation2004; Department of Energy Citation2012; IEA Citation2014). Biofuels can be used for transport, heat and electricity and thereby improve energy access and security by replacing oil imports and the unsustainable use of charcoal and firewood that occurs in many African countries.

Biofuel developments are part of a growing bioeconomy that requires a sustainable supply of biomass (Johnson Citation2017). Biofuel developments can bring a range of impacts and risks, including: the expansion of agriculture into natural areas, land-use conflicts, land degradation, the depletion of water resources and soil nutrients, soil erosion, greenhouse gas emissions, air pollution, biodiversity loss, as well as risks to food security (Scharleman & Laurence Citation2008). These complexities require that bioenergy and agriculture are integrated and effectively managed. If developed appropriately, sustainable bioenergy projects offer not only an opportunity for the production of low-carbon renewable energy and the displacement of fossil fuels as energy sources, but also the development of more integrated and sustainable agricultural systems that are based on energy efficiency and improved natural resource management (IAASTD Citation2009; Kline et al. Citation2009; Tilman et al. Citation2009; de Vries et al. Citation2010). Since changes in conversion technologies may have profound impacts on the feedstocks available for biofuels and hence the production zones suitable for feedstock production, the strategic planning of regional biofuel developments will need to consider technologies currently available and those likely to emerge in the future (Kline et al. Citation2017). This paper furthers our working paper on trends in biofuels research and development, with the aim of assessing biofuels technology readiness and the time to reach commercialisation and widespread adoption in Southern Africa (Stafford et al. Citation2017). We carry out an integrated foresight analysis that combines the current and future biofuels technology trends with developments in transportation and relevant policy targets.

2. Biofuels: Current status and future potential

2.1. Biofuels pathways

The biomass feedstock, conversion technology and other requirements of the biofuels value chain will determine the overall costs and benefits. Several types of biomass can be used as feedstocks to produce biofuels through various conversion pathways. These feedstocks can be categorised as:

Sugary and starchy crops, which are typically food crops. Sugary crops include sugarcane, sugar beet and sweet sorghum; starchy crops include maize, wheat, triticale and rye.

Lignocellulosic biomass, which includes dedicated energy crops (grass, herbaceous plants, trees), agricultural residues (post-harvest residues that need to be collected, such as straw and corn stover; captive processing residues such as bagasse, husks, shells and cobs) and forestry residues (branches and leaves, and residues from wood-processing activities, such as sawdust and cutter shavings).

Oil-rich crops and oil wastes include oils from food crops, such as canola, soya and sunflower oil, and non-food oils, such as Jatropha.

Organic wastes include manures, sewage, the organic fraction of municipal solid wastes and other food wastes.

Algal biomass refers to aquatic micro-algae or macro-algae, with species grown in freshwater and seawater, using open ponds or photobioreactors.

Fermentation of sugary and starchy crops to produce ethanol and other alcohols such and butanol;

Mechanical pressing and transesterification of oils (from oil-rich crops and oil waste) for the production of biodiesel;

Mechanical pressing and hydrogenation of oils (from oil-rich crops and oil waste) to produce hydrotreated vegetable oil;

Anaerobic digestion of various organic biodegradable wastes to produce biogas, which is then upgraded to (bio)methane;

Pre-treatment of lignocellulosic biomass by hydrolysis to provide sugars for fermentation to produce ethanol and other alcohols;

Pre-treatment of lignocellulosic biomass by hydrolysis to provide substrates for anaerobic digestion to produce biogas, which is upgraded to (bio)methane;

Hydrothermal liquefaction of biomass to produce biocrude, which can be upgraded to biofuels by refining and hydrogenation;

Pyrolysis of lignocellulosic biomass to produce pyrolysis oil and charcoal (biocrude) that can subsequently be refined to produce long-chain hydrocarbon biofuels;

Pre-treatment of biomass by hydrolysis or aqueous phase reforming of biocrude, followed by reforming to produce hydrocarbon biofuels and hydrogen;

Gasification of lignocellulosic biomass to produce hydrogen;

Gasification of lignocellulosic biomass to produce methane, which can be further converted to methanol, methoxymethane or long-chain hydrocarbon synfuels;

Gasification of lignocellulosic biomass, followed by the fermentation of syngas to produce ethanol;

Algal biomass for the production of biogas, ethanol or biodiesel through the routes described in 1–7; and

Genetic engineering of microorganisms to produce long-chain hydrocarbon fuels.

Since crops used for ethanol (i.e. maize, sorghum, sugarcane) and biodiesel (i.e. soya, canola, sunflower) may compete with food production and affect food prices, there is a growing interest in the use of organic wastes and non-food crops for biofuels production. The wastes from the food production chain are an example of such a resource, and their use brings other development benefits in terms of avoiding pollution, but they are necessarily limited in quantity. However, the potential from non-food crops is substantial, since the overall energy stored in plant biomass each year is approximately 30 times greater than the energy consumed for transportation (Hermann Citation2006). Lignocellulose biomass is available from agriculture and forestry residues, and grassy, herbaceous and woody energy crops. Since lignocellulose is resistant to degradation, a key challenge is the hydrolysis pre-treatment necessary for biochemical processing via fermentation or anaerobic digestion to produce ethanol and biomethane. An alternative pre-treatment and conversion process for lignocellulose is gasification, followed by conversion to synfuels (hydrogen, methane, methanol, methoxymethane and long-chain hydrocarbon synfuels). Other non-food biomass feedstocks for biofuels are algae that offer high levels of productivity and can grow on land unsuitable for agriculture, but require large amounts of water for cultivation and are energy-intensive in harvesting. Algae can accumulate a high percentage of oils under nutrient starvation and are being explored as a source for biodiesel production. However, algal biomass may also be suitable for other biofuels conversion processes (fermentation and anaerobic digestion of wet algae and, after drying, gasification, pyrolysis or combustion).

2.2. Biofuels conversion technology readiness

There are a range of biofuels technologies at research and development, demonstration, deployment and established commercial stages. The conventional first-generation biofuels – ethanol, biodiesel and biogas – are commercially established and produced from food and fodder crops, food wastes and sewage. Advanced, second- and third-generation biofuels aim to access residuals of food crops (stems, leaves and husks) and non-food crops (grasses, bamboo, trees and algae), and are at various stages of development. Many of these biofuels can readily replace petrol, diesel and natural gas, with little additional infrastructure and vehicle modification, and therefore can be blended to facilitate gradual market uptake and adoption.

The production of ethanol from the fermentation of starch/sugar crops, biogas from organic wastes and biodiesel from oil transesterification, are established commercial technologies that are becoming price-competitive with petroleum fuels. Continued improvements in pre-treatment and hydrolysis technologies will significantly reduce capital and operating costs, as will opportunities for process integration. Hydrolysis and fermentation of lignocellulosic feedstock to produce ethanol has reached early commercial phase – DuPont, Abengoa and Poet-DSM have been operating commercial-scale lignocellulosic ethanol plants in the United States with an installed capacity of 285 million litres per annum; GranBio and Raizen have started production in Brazil with an installed capacity of 80 million litres and 40 million litres per annum, respectively; Shandong Longlife has started production in China with an installed capacity of 60 million litres per annum; and Beta Renewables has started production in Italy with an installed capacity of 50 million litres per annum. In Finland, St1 produces ethanol from waste using a number of fermentation plants situated near the sources of waste, and carries out ethanol upgrading by dehydration in a central plant. Ethanol from syngas fermentation is also an emerging option that offers increased yields, and is currently at the late demonstration to deployment phase, with the US company, IneosBio, operating a demonstration plant with an installed capacity of 30 million litres per annum (Ineos Citation2013).

Synthesis of biofuels via biomass gasification is an attractive option that can access a range of biomass is at demonstration and early commercial stage; Enerkem in Canada are operating the first commercial-scale Fischer–Tropsch plant with an installed capacity of 28 million litres per annum of methanol, using municipal solid waste as a feedstock. German-based company Choren has demonstrated a methanol-to-gasoline processes (EBTP Citation2016). There is also R&D for new biological routes to biofuels through genetic engineering and synthetic biology; with companies such as LS9, Joule Unlimited and ExxonMobil pioneering the development of engineered bacteria and algae (Berry Citation2010; ExxonMobil Citation2017). The production of hydrocarbon fuels by upgrading pyrolysis oil is at demonstration and early commercialisation, with Ensyn currently producing around 12 million litres of biofuel per annum in Brazil and Malaysia (Ensyn Citation2016). Other conversion routes that are in the early stages of R&D include aqueous phase reforming, direct sugar to hydrocarbon routes and the production of hydrocarbon fuels from micro-algae.

The advanced biofuels pathways can be defined by the technology readiness level (TRL) and classed at stages 1–4 (NASA Citation2017):

Research and development (TRL0–TRL4). Bringing new technology to fruition requires a substantial amount of research, planning and experimentation. Unproven concepts are tested and specific applications formulated. Subsequently, applied research is conducted at laboratory scale and the technology developed into a proof of concept via small-scale prototyping.

Pilot and demonstration (TRL5–TRL7). Larger-scale prototypes and pilot plants are developed in order to determine the scaling potential and the intended operating environment of new technologies.

Early commercial deployment (TRL8–TRL9). For any technology developed at commercial scale it is necessary to create first-of-a-kind systems and flagship plants. This proves to consumers and investors the viability and commercial readiness of the proposed technology.

Commercially established. A technology is considered to be commercially established when it is readily available to consumers, comes with performance guarantees and economically competitive with similar market items.

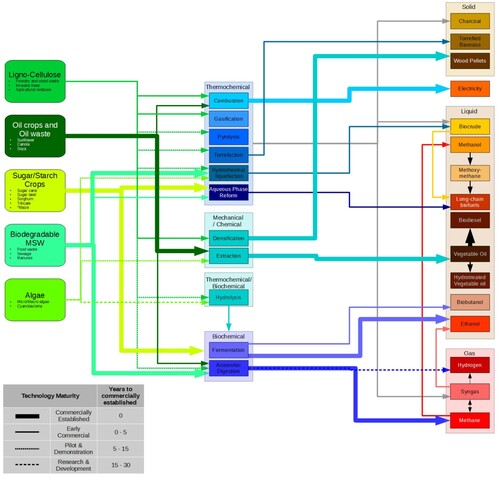

Figure 1. Biofuel pathways and stage of technology readiness. See text for details.

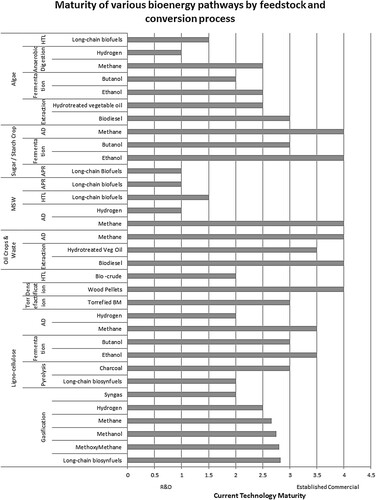

Figure 2. Biofuel feedstock, conversion process and energy carrier readiness from pathways shown in .

Notes: AD, anaerobic digestion; APR, aqueous phase reforming; HTL, hydrothermal liquefaction; HVO, hydrogenated vegetable oil. See text for details.

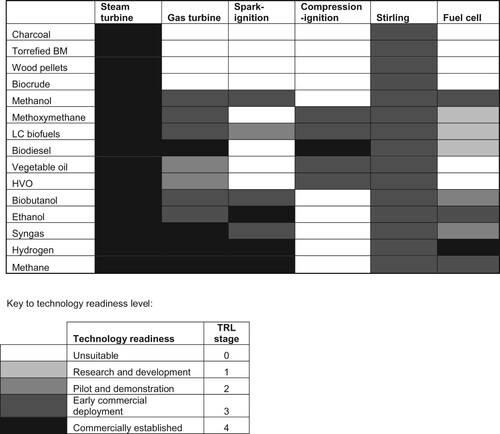

Figure 3. Technology readiness and/or suitability of various prime-movers for different energy carriers.

The extent of biofuels market penetration will depend on competing alternative fuels, as well as global targets, country-specific mandates and policies. The European Union has set targets to reduce global energy-related greenhouse gas emissions and this requires an increase of biofuels in the transport fuel mix from 2% currently to reach 27% by 2050 in order to avoiding 2.1 Gt of CO2 emissions per year (IRENA Citation2016a). This level of adoption will require considerable technology developments so that conventional ethanol and biodiesel production are gradually superseded by advanced cellulosic and advanced biodiesel, respectively. Although residues and wastes can supply some of the biomass feedstock required for biofuels production, the land for biofuels use will likely triple between 2010 and 2050, to reach about 110 Mha (IRENA Citation2016a). These carbon-reduction targets are also partly achieved by an increase in electric vehicles to reach 13% in 2050, with the electricity substantially supplied from low-carbon, renewable sources. Several countries have made similar commitments to transition to electric vehicles and the developing nations of China and India and South Africa have joined the global electric vehicle initiative (IEA Citation2011b, Citation2016). Natural gas vehicles are also alternative transport fuels that will compete with biofuels in current and future transport fuel markets. Natural gas currently powers approximately 2% of the global vehicle fleet, and has seen an annual growth rate of 25% between 2001 and 2010. Several countries in Africa have natural gas fields in their territories (South Africa, Namibia, Angola, Mozambique and Tanzania), and could supply fuel for the natural gas vehicles fleet, as well as providing electricity and heat to households and industry (Kilian Citation2016). Similarly, hydrogen is an alternative transport fuel that can power vehicles using internal combustion engines and fuel cells; and is at demonstration and deployment stage with Toyota, Hyundai and Honda offering vehicles in selected markets.

3. Performance criteria for biofuels development

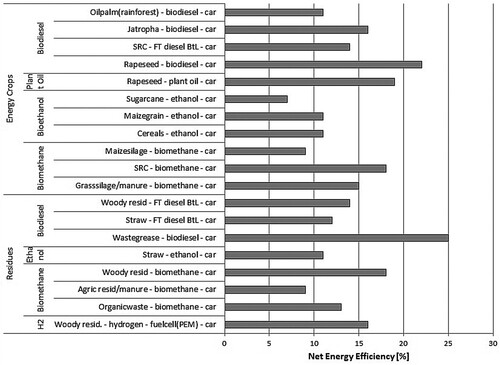

3.1. Biofuels energy yield, conversion efficiency and net energy balance

The conversion efficiency of biofuels is typically expressed as the energy yield of biofuel per unit biomass feedstock input. However, biomass productivity varies widely with locality due to climate and soil conditions, so that the biofuel yields per unit land area is a preferred measure of local biofuels conversion efficiency. Good biomass productivity with optimal yields requires land and inputs of water and nutrients, as well as plant species suited to the specific agro-ecology and local climatic conditions. The biofuels energy yield is mainly determined by the yield of biomass feedstock and the biofuels conversion efficiency (). However, there are other energy requirements that will affect the overall or net energy efficiency. This includes energy required for: the production of the seeds, pesticides and fertilisers; irrigation; land cultivation; transportation to the biofuels conversion facility; and the energy losses in biofuels end-use. There is considerable inconsistency in the literature when calculating the net energy efficiency due to the use of different indicators, system boundaries and assumptions (Davis et al. Citation2009). For example, net energy balance, net energy balance ratio, fossil energy ratio, energy return on investment, net energy value and life-cycle energy efficiency have been used to describe the energy efficiency of biofuels pathways. Further, varied results are obtained by allocating resource and energy flows between biofuels and other co-products according to either market price, weight, energy content or the avoided processes from product substitution (Malça & Freire Citation2006). Life-cycle assessment (LCA) (ISO Citation2006) provides a useful framework and tools to assess the net energy of various biofuels from biomass to wheel, and is expressed as life-cycle energy efficiency (see ).

Figure 4. Net energy efficiency of biofuels (biomass-to-wheel) from feedstock production to end-use in transportation.

Notes: Life-cycle energy efficiency = (energy output/energy input) × 100. Adapted from Schubert et al. (Citation2008).

Table 1. Yields of biofuels and co-products per land area.

3.2. Cost competitiveness of biofuels compared to fossil fuels

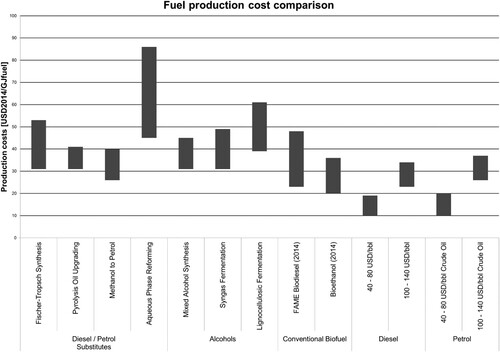

The economics of biofuels production is particularly sensitive to feedstock prices, as well as the competing fossil fuel price. In general, biofuels are not yet economically competitive with conventional fuels such as petrol and diesel. A possible exception is Brazilian sugarcane ethanol that can now produce ethanol at US$20/GJ (). At an oil price above US$100/bbl, most advanced biofuels pathways may be able to compete directly with petrol and diesel by 2030–45. Currently, advanced and second-generation biofuels are significantly more expensive than conventional biofuels. In all cases, the feedstock is a significant cost component and can account for 60–90% of the overall cost of a biofuels production facility (IRENA Citation2016b). Many of the advanced biofuels technologies are at an early stage of R&D and therefore have large uncertainties in costs (). As these technologies mature, the uncertainties in cost and risk of technology performance will be diminished.

Figure 5. Biofuel production cost, compared to diesel and petrol equivalents. Assumes oil price of either 40–80 US$/bbl or 100–140 US$/bbl). (USD/bbl = US$ per barrel oil). Adapted from IRENA (Citation2016b).

Ideally, the biomass used for biofuels should be low-value residues and waste or high-yielding energy crops that do not compete with food production. Energy crops such as Jatropha, Miscanthus, Camelia and Arundo are currently favoured for biofuels production instead of crops used for food – such as maize, sorghum and sunflower (von Maltitz & Stafford Citation2011). An additional determinant of biofuels feasibility is the ability to sell valuable co-products that can add value and increase the revenue of the biofuel business. Examples include glycerine, bagasse, lignin, seed cake and meal, heat and power (Worldwatch Institute Citation2006).

The optimum plant size of biofuels conversion is significantly influenced by the scaling exponent for production. Historical data from the chemical industry indicates that the scaling exponent for industrial production is on average 0.6 (Leboreiro & Hilaly Citation2011); and studies of biofuels facilities range between 0.5 and 0.8 (Fisher et al. Citation1986; Nguyen & Prince Citation1995; Wright & Brown Citation2007; Searcy & Flynn Citation2009). The optimum plant size at a given locality is influenced by the feedstock transportation costs in addition to the scale of biofuels production (Overend Citation1982; McIlveen-Wright et al. Citation2001; Perlack and Turhollow Citation2003). The increasing costs to transport and storage required to supply biomass feedstock and to distribute the biofuel to market will limit the cost reductions that come with larger biofuels facilities. Both ethanol and biodiesel can be produced at almost any scale, but it appears that there are better economies of scale for ethanol production (Nguyen and Prince Citation1995; Nolte Citation2007).

The development of biofuels will also be highly dependent on the ease of market uptake. Important aspects include blending mandates, biofuels distribution infrastructure and vehicle modifications needed. To maintain octane rating, ethanol is typically blended at 10–25% with petrol (E10 and E25 blends) and higher percentages of ethanol are only possible in special Flexfuel vehicles (Gupta et al. Citation2010). In contrast, biodiesel can effectively be blended at any percentage with conventional diesel, although more regular filter changes may initially be required and biodiesel may accelerate deterioration of rubber gaskets present in older vehicles.

Biofuels are in the early stages of development in most Southern African countries and most implementations are at domestic and small- to medium-scale. Few countries in Southern Africa have government policy to enable biofuels developments – either through fiscal incentives for biofuels or disincentives or fossil fuels. Several biofuels technologies are well developed, but a lack of cost competitiveness with fossil fuels is a major obstacle to commercialisation and widespread adoption (Chakauya et al. Citation2009). Many of the economically viable biofuel opportunities utilise wastes, which avoids disposal costs and thereby reduces the levelised cost of energy produced. However, the use of waste limits the overall biofuels production potential and does not allow flexibility in production in order to respond to fluctuating market demands. For example, bioethanol production from sugar cane can either use the waste molasses from conventional sugar production or diversify the process at the raw sugar stage to produce bioethanol instead of sugar. In both cases, the economic viability depends on the economies of scale, transport costs, costs of processing and distribution, as well as market prices for bioethanol and sugar. If molasses is the feedstock, the scale is fixed and limited to the amounts of molasses waste from existing sugar refineries. While if raw sugar is diverted from sugar production to ethanol, greater scale can be achieved and there is flexibility of producing bioethanol and sugar in response to fluctuating market demands.

South Africa is the most industrialised country in Southern Africa and most developed in terms of biofuels production. There are several hundred small-scale biogas plants supplying heat for cooking; several small- and medium-sized enterprises utilising waste from abattoirs and animal husbandry; and a few industrial-scale (several MW) plants using biogas from municipal organic waste, sewage and animal husbandry to produce heat and electricity, as well as initiatives to develop biogas as a transport fuel (Department Environmental Affairs Citation2013, Citation2015; ESI Africa Citation2013). There are also many small- and medium-scale biodiesel production plants utilising waste cooking oil, and a few industrial scale (more than 20 million litres per annum) bioethanol plants (Chakauya et al. Citation2009).

South Africa, Mozambique and Zambia do have biofuels blending targets, but these have not been implemented or enforced, while Malawi and Zimbabwe have successfully implemented blending of bioethanol with petrol up to 20%. However, the demand for transport fuels is also low in most Southern African countries due to low vehicle ownership per capita. Less than 1% of the total global ethanol produced comes from Africa due to low domestic market demand, and the fact that many African countries are landlocked with underdeveloped transport infrastructure that limits export opportunities (Chakauya et al. Citation2009; Fundira & Henley Citation2017). The lack of business opportunities for profitable commercial biofuels production, coupled with a lack of policy support, has often hampered the development of viable biofuels value chains in Africa (Fundira & Henley Citation2017). From a Southern African perspective, most of demand for biofuels is in South Africa; while neighbouring countries – especially Zambia and Mozambique – have greater biomass productivity and available land (von Maltitz & van der Merwe Citation2017). This suggests that a regional supply-demand model of cooperation could enable biofuel developments in the Southern African Development Community (SADC). In addition to techno-economic feasibility, biofuel developments will need to include a range of aspects to ensure that the production of biomass, biofuels and bioenergy is both renewable and sustainable (Amigun et al. Citation2011; von Maltitz & Stafford Citation2011).

3.3. Greenhouse gas emissions and air pollutants

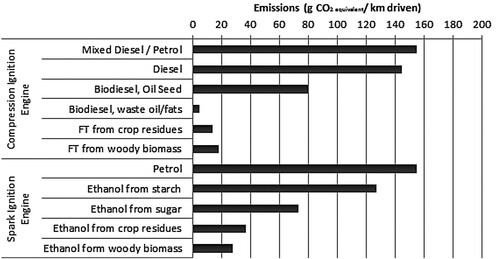

A significant driver of biofuels adoption is the reduction in the emission of greenhouse gases and other pollutants. In general, biofuels reduce both local pollution (particulate emissions, nitrous oxides) and global carbon dioxide levels, compared to reference fossil fuels. The greenhouse gas emissions from biofuels have been extensively published and most studies reveal significant carbon savings compared to petroleum fuels (). The use of sugary biomass (sugarcane and sweet sorghum) for ethanol production using first-generation technology has greater carbon savings compared to ethanol produced from starchy sources. Second-generation and advanced technologies that utilise lignocellulosic biomass offer even better carbon emission reductions. However, these technologies are not yet established at commercial scale, nor are the benefits fully proven and verified. Using wastes and biomass residues offers the greatest carbon savings, since there are no emissions for cultivation of the biomass resource and the use of waste avoids emissions from disposal and treatment (Transport Research Centre Citation2008).

Figure 6. Greenhouse gas emissions of biofuels from lignocellulose feedstocks and energy crops, compared to reference fossil fuels (petrol and diesel). Adapted from IEA (Citation2008).

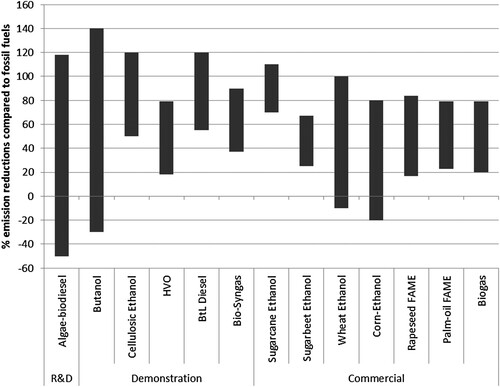

The published studies on the carbon emission reductions of biofuels report a wide range of values for a given biofuel pathway, and this has caused considerable debate. The differences are due to various factors such as the locality of the biofuels development (biomass productivity and transportation requirements), the conversion technology and the methodology used in the assessment. The loss of natural areas for agriculture and the fuel-intensive farming practices already account for a significant portion of global greenhouse gas emissions, and the carbon emissions from the land-use change of agricultural expansion can completely negate the carbon savings of the biofuel (Schubert et al. Citation2008). In the Southern African context the land-use change impact is dependent on the vegetation status prior to the project implementation, and may be trivial in already degraded landscapes, but high if virgin forest is cleared (Romeu-Dalmau et al. Citation2016). However, a meta-analysis of carbon emissions from numerous studies suggests that biofuels typically deliver carbon savings, compared to reference fossil fuels. However, actual carbon savings are context-specific, and in some cases, carbon emissions may be greater than reference fossil fuels. The certainty of achieving carbon emission reduction benefits will increasingly affect investment decisions, given the growing carbon markets and imperatives to reduce greenhouse gas emissions and mitigate global climate change. From published data, there is a large degree of uncertainty in achieving the expected carbon emission reductions of advanced biofuels that are at early stages of development ().

Figure 7. Meta-analysis of greenhouse gas emission reductions of various biofuels, compared to reference fossil fuels (diesel and petrol). The assessments exclude indirect land-use change. Emission savings of more than 100% are possible through use of co-products. BtL = biomass-to-liquid; FAME = fatty acid methyl esters; HVO = hydrotreated vegetable oil. Results are from numerous LCA studies; the figure is adapted from IEA (Citation2011a).

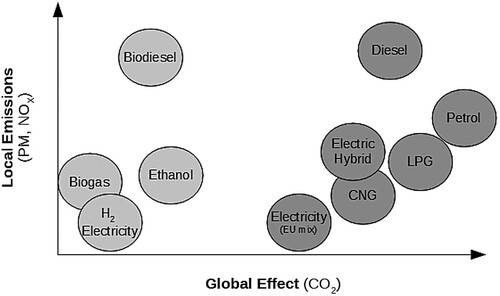

There are a range of other environmental impacts to consider in addition to carbon emissions. Compared to petroleum fuels, a noteworthy benefit of biofuels is a reduction in air pollution from sooty particulate matter, nitrogen oxides and sulphur oxides. is a diagrammatic representation of how biofuels perform in terms of global effect (greenhouse gas emissions) and local emissions (air pollutants), compared to fossil fuels. Furthermore, there are other environmental impacts to consider, including: water consumption, water acidification and eutrophication, soil degradation, pesticide impacts and biodiversity loss (Frischnecht et al. Citation2006; Scharleman and Laurence Citation2008; von Maltitz et al. Citation2010; Blanchard et al. Citation2011). Agriculture and farming practices are already using approximately 70% of water from surface rivers and streams (IPCC Citation1997), and contribute to water pollution from excess nutrients, pesticides and herbicides (Gerbens-Leens et al. Citation2009 Gopalakrishnan et al. Citation2009). Since current estimates indicate that 1388 to 19 924 litres of water are needed per litre of biofuel produced (Gerbens-Leens et al. Citation2009; World Energy Outlook Citation2012), and most of Southern Africa is semi-arid and water scarce, water availability will likely constrain biofuel developments (Rulli et al. Citation2016). As with all land transformation activities, the effects of biofuel developments on biodiversity and ecosystem services are highly variable and context-specific (Efroymson et al. Citation2012). Where feedstocks for biofuels are planted in pristine landscapes significant biodiversity losses can be expected (Harrison and Berenbaum Citation2013; Leal et al. Citation2013; Phalan et al. Citation2013). In addition, many dedicated energy crops are chosen for their high productivity and vigorous growth that presents risks of plant invasion and biodiversity loss (Blanchard et al. Citation2011).

Figure 8. Diagrammatic representation of the performance of biofuels compared to petroleum fuels in terms of global effect (greenhouse gas emissions) and local emissions (air pollutants). Adapted from the Baltic Biogas Bus (Citation2009).

The lack of infrastructure in rural areas presents additional challenges to the expansion of biofuels production in Africa and there are also issues of land tenure. Biofuel developments could threaten the livelihoods of many of Africa’s rural poor through the displacement of indigent people from communal lands – ‘land grabs’ (Robertson et al. Citation2008; Scharleman & Laurence Citation2008; Kline et al. Citation2009; Gasparatos et al. Citation2012). Biofuel developments should therefore be tailored to local needs and priorities within the context of sustainable development, in order to deliver the benefits of improved renewable energy access with the enhanced management of natural resources (IAASTD Citation2009; de Vries et al. Citation2010).

4. Conclusions

Biofuels can help mitigate climate change by reducing carbon emissions while also reducing local air pollution, improving energy security and offering new opportunities for rural development. However, the benefits of biofuels depend on the feedstock, conversion pathway and local context. The various biofuels conversion technologies are at different stages of R&D and this defines their technology readiness and maturity. The currently established commercial biofuels use food crops, manure, crop residues and food wastes to produce ethanol, biodiesel and biomethane, and generally provide 20–80% savings on carbon emissions compared to the petroleum fuels they replace (petrol, diesel and natural gas). The use of wastes and biomass residues offers the greatest carbon reductions, since there are no emissions for cultivation of the resource and reduced emissions and costs from avoiding the disposal of these wastes. However, resources are limited. Currently, first-generation technologies are mature and in wide-scale operation in many regions. Biofuel based on sugarcane ethanol is well established in Brazil – with a long history of policy support and R&D investment that has developed high yielding sugarcane and optimised value chains to enable a competitive and viable biofuels industry. Emulating these aspects are critical for the development of biofuels in Southern Africa. First-generation biofuel options based on oil crops are also possible, although per-hectare energy returns are far lower than the ethanol options. However, the sale of co-products, such as seed cake and meal for animal feed, could increase the economic viability of the biofuel business and diversification enables a more stable and secure revenue stream. In the medium- to long-term it is foreseen that technologies that can use the non-food components of biomass (lignocellulose) are likely to dominate. These technologies can give better yields of biofuel and outperform first-generation technologies in most respects, but are not proven and/or cost-competitive with either first-generation technologies or fossil fuel prices. These advanced second- and third-generation technologies are at various stages of research and development. Hydrolytic pre-treatment of crop residues, such as straw, for ethanol fermentation is at an early commercial stage, as is the pre-treatment of organic waste for enhanced anaerobic digestion. Gasification of lignocellulosic biomass and either ethanol fermentation or synfuel production is currently at the pilot and demonstration stage. Pyrolysis and upgrading of biocrude (oils and char) is at the pilot and demonstration stage, while aqueous phase reforming and the use of algae and engineered microorganisms are at research to early pilot and demonstration stages.

Since most biofuels are currently more expensive than their petroleum counterparts, the extent of biofuels’ market penetration will be influenced by mandates (blending targets) and subsidies (green premium). The market uptake will also be governed by competing alternative fuels and technologies, such as natural gas, hydrogen and battery-electric vehicles, although these options may require additional distribution infrastructures and will only deliver carbon benefits if the electricity mix is substantially powered by renewables. It is likely that ethanol and biodiesel will be able to readily displace petrol and biodiesel in existing transportation combustion engines, with biofuels blending enabling the uptake. However, given the rapid development of the electric vehicle market, it is possible that electric vehicles powered by battery or fuel cell may leapfrog the use of internal combustion engines with biofuels as a future renewable transport fuel. This will depend on an adequate grid infrastructure (electrification) for extensive electricity access, security of electricity supply and increase in the proportion of renewable energy in the electricity supply mix in order to achieve environmental benefits, such as greenhouse gas emission savings (IEA Citation2011a; IRENA Citation2013). Given the rapid global development of electric vehicles and hydrogen fuel cells, it is likely that South Africa will meet its 2–10% biofuels blending mandate in the short term (5–20 years), while moving to adopt electric vehicles at scale in the longer term (20–40 years). Other Southern African countries will likely follow suit in electric vehicle adoption, but with considerable delay since many countries have a poor level of electricity access and security of supply.

Developing biofuels will require a careful assessment and certification of the supply chain and biofuels life-cycle to avoid unintended consequences. If biofuels development clears natural areas, and biofuels are produced from low-yielding crops, grown with heavy inputs of water, fertilisers and energy, and/or processed into biofuel using fossil energy, they could threaten food security and generate as much (or more) carbon emissions than petroleum fuels. However, if developed appropriately, biofuels offer an opportunity for the production of renewable energy and a reduction in carbon emissions, together with the development of more integrated and sustainable agricultural systems and improved natural resource management.

Acknowledgements

This work was supported by United Nations University World Institute for Development Economics Research (UNU-WIDER): Regional growth and development in Southern Africa.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Amigun, B, Musango, JK & Stafford, W, 2011. Biofuels and sustainability in Africa. Renewable and Sustainable Energy Reviews 15(2), 1360–72. doi:10.1016/j.rser.2010.10.015.

- Baltic Biogas Bus, 2009. Biogas: The natural choice for city buses. www.rdsd.lv/uploads/media/551a5ad84b3fe.pdf Accessed 15 December 2016.

- Berry, D, 2010. Engineering organisms for industrial fuel production. Bioengineered Bugs 1(5), 303–8. doi: 10.4161/bbug.1.5.12941

- Blanchard, R, Richardson, D, O’Farrel, P & von Maltitz, G, 2011. Biofuels and biodiversity in South Africa. South African Journal of Science 107(5–6), 19–26. doi:http://doi.org/10.4102/sajs.v107i5/6.186.

- Chakauya, E, Beyene, G & Chikwamba, RK, 2009. Food production needs fuel too: Perspectives on the impact of biofuels in Southern Africa. South African Journal of Science 105(5–6), 174–81.

- Davis, S, Anderson-Teixeira, KJ & DeLucia, E, 2009. Life-cycle analysis and the ecology of biofuels. Trends in Plant Science 14(3), 140–6. doi: 10.1016/j.tplants.2008.12.006

- de Vries, S, van de Ven, G, van Ittersum, M. & Giller, K, 2010. Resource use efficiency and environmental performance of nine major biofuel crops, processed by first-generation conversion techniques. Biomass and Bioenergy 34, 588–601. doi: 10.1016/j.biombioe.2010.01.001

- Department Environmental Affairs, 2013. Overview of biogas potential in South Africa. Author: Munganga. G, GreenCape-Waste Economy Sector Manager. http://www.energy.gov.za/files/biogas/presentations/2013-NBC/2013-Overview-of-biogas-market-in-South-Africa.pdf Accessed 26 March 2018.

- Department Environmental Affairs, 2015. Biogas report: Facilitation of large-scale uptake of alternative transport fuels in South Africa- the case for biogas. https://www.environment.gov.za/sites/default/files/reports/bioagas_report.pdf Accessed 22 March 2018.

- Department of Energy, 2012. Energy statistics. www.energy.gov.za/files/energyStats_frame.html Accessed 17 January 2017.

- EBTP, 2016. Biomass to liquids BtL. www.biofuelstp.eu/btl.html Accessed 16 January 2017.

- ESI Africa, 2013. ‘Biogas – South Africa’s great untapped potential’ June 2016. ESI Africa: Africa’s power journal. https://www.esi-africa.com/biogas-south-africas-great-untapped-potential/ Accessed 26 March 2018.

- Efroymson, RA, Dale, VH, Kline KL, McBride, AC, Bielicki, JC, Smith, RL, Parish, ES, Schweizer PE, Shaw DM, 2012. Environmental indicators of biofuel sustainability: What about context? Environmental Management 51(2), 291–306. doi: 10.1007/s00267-012-9907-5

- Ensyn, 2016, 13 July. Ensyn, Arbec and Rémabec Begin Construction of the Cote Nord Biocrude production facility in Quebec. http://advancedbiofuelsassociation.com/blog/wp-content/uploads/2016/07/Ensyn-CN-Release-2016.7.13-As-Issued.pdf Accessed 23 January 2017.

- ExxonMobil, 2017. Advanced biofuels. http://corporate.exxonmobil.com/en/energy/research-and-development/advanced-biofuels/advanced-biofuels-overview Accessed 9 January 2017.

- Feygin, M & Satkin, R, 2004. The oil reserves-to-production ratio and its proper interpretation. Natural Resources Research 13, 57–60. doi: 10.1023/B:NARR.0000023308.84994.7f

- Fisher Jr, C, Paik, S & Schriver, W, 1986. Power plant economy of scale and cost trends: Further analyses and review of empirical studies. Ornl U S. Atomic Energy Commission 857685, 1–11.

- Frischnecht, R, Steiner, R, Braunschweig, A, Norbert, E & Gabi, H, 2006. Swiss ecological scarcity method: The New version. ESU-services GmbH, Zurich.

- Fundira, T & Henley, G, 2017. Biofuels in Southern Africa: Political economy, trade, and policy environment. WIDER Working Paper Series 048, World Institute for Development Economic Research (UNU-WIDER).

- Gasparatos, A, Lee, L, von Maltitz, G, Mathai, M, de Oliveira, JP & Willis, K, 2012. Biofuels in Africa: Impacts on ecosystem services, biodiversity and human well-being. UNU-IAS Policy Report. United Nations University Institute of Advanced Studies, Yokohama.

- Gerbens-Leens, P, Hoekstra, A & van der Meer, T, 2009. The water footprint of energy from biomass: A quantitative assessment and consequences of an increasing share of Bio-energy in energy supply. Ecological Economics 68, 1052–60. doi: 10.1016/j.ecolecon.2008.07.013

- Gopalakrishnan, G, Cristina Negri, M, Wang, M, Wu, M & Snyder, SL, 2009. Biofuels, land, and water: A systems approach to sustainability. Environmental Science & Technology 43, 6094–100. doi: 10.1021/es900801u

- Gupta, P, Sae-wang, V, Kanbua, P & Laoonual, Y, 2010. Impact of water contents blended with Ethanol on SI engine performance and emissions. The First TSME International Conference on Mechanical Engineering, TSME-ICOME, 20–22 October, Ubon Ratchathani, 1–9.

- Harrison, T & Berenbaum, M, 2013. Moth diversity in three biofuel crops and native prairie in Illinois. Insect Science 20(3), 407–19. doi: 10.1111/j.1744-7917.2012.01530.x

- Hermann, W, 2006. Quantifying global exergy resources. Energy 31(12), 1685–702. doi: 10.1016/j.energy.2005.09.006

- IAASTD, 2009. Agriculture at a crossroad: Global report. Island Press, Washington, DC.

- IEA, 2008. From 1st to 2nd generation biofuel technologies. IEA, Paris.

- IEA, 2011a. Technology roadmap: Biofuels for transport. IEA, Paris.

- IEA, 2011b. Technology roadmap: Electric and plug-in hybrid electric vehicles. IEA, Paris.

- IEA, 2014. International energy statistics. www.eia.gov/beta/international/data/browser/#/?vs=INTL.44–1-AFRC-QBTU.Aandvo=0andv=Handstart=1980andend=2014 Accessed 16 January 2017.

- IEA, 2016. Global EV outlook: Beyond one million electric cars. International Energy Agency, Paris.

- Ineos, 2013. First facility in the world using new advanced bioenergy technology to convert waste to renewable fuel and electricity. www.ineos.com/news/ineos-group/ineos-bio-produces-cellulosic-ethanol-at-commercial-scale Accessed 21 January 2017.

- IPCC, 1997. The regional impacts of climate change: An assessment of vulnerability. Cambridge University Press, Cambridge.

- IRENA, 2013. Production of liquid biofuels: Technology brief. IRENA, Masdar City.

- IRENA, 2016a. Boosting biofuels: Sustainable paths to greater energy security. IRENA, Masdar City.

- IRENA, 2016b. Innovation outlook: Advanced liquid biofuels. IRENA, Masdar City.

- ISO, 2006. ISO 14040:2006: Environmental management – LCA – Principles and framework. www.iso.org/iso/catalogue_detail?csnumber=37456 Accessed 17 January 2017.

- Johnson, FX, 2017. Biofuels, bioenergy and the bioeconomy in north and south. Industrial Biotechnology Dec 1;13(6), 289–91. doi: 10.1089/ind.2017.29106.fxj

- Kilian, A, 2016. Novo energy launches CNG dispensing facility. Engineering News, 28 October.

- Kline, K, Dale, V, Lee, R & Leiby, P, 2009. In defense of biofuels, done right. Issues in Science and Technology 25(3), 75–84.

- Kline, KL, Msangi, S, Dale, VH, Woods, J, Souza, GM, Osseweijer, P, Clancy, JS, Hilbert, JA, Johnson, FX, McDonnell, PC & Mugera, HK, 2017. Reconciling food security and bioenergy: Priorities for action. Global Change Biology Bioenergy 9(3), 557–76. doi: 10.1111/gcbb.12366

- Leal, M, Silva Walter, A & Seabra, J, 2013. Sugarcane as an energy source. Biomass Conversion and Biorefinery 3(1), 17–26. doi: 10.1007/s13399-012-0055-1

- Leboreiro, J & Hilaly, A, 2011. Biomass transportation model and optimum plant size for the production of ethanol. Bioresource Technology 102(3), 2712–23. doi: 10.1016/j.biortech.2010.10.144

- Malça, J & Freire, F, 2006. Renewability and life-cycle energy efficiency of bioethanol and Bio-ethyl tertiary butyl ether (bioETBE): Assessing the implications of allocation. Energy 31, 3362–80. doi: 10.1016/j.energy.2006.03.013

- McIlveen-Wright, D, Williams, B & McMullan, J, 2001. A re-appraisal of wood-fired combustion. Bioresource Technology 76, 183–90. doi: 10.1016/S0960-8524(00)00129-2

- NASA, 2017. Technology readiness level definitions. www.nasa.gov/pdf/458490main_TRL_Definitions.pdf Accessed 2 February 2017.

- Nguyen, M & Prince, RH, 1995. A simple rule for bioenergy conversion plant size optimisation: Bioethanol from sugar cane and sweet sorghum. Biomass and Bioenergy 10(5–6), 361–65. doi: 10.1016/0961-9534(96)00003-7

- Nolte, M, 2007. Commercial biodiesel production in South Africa: A preliminary economic feasibility study. MSc thesis. University of Stellenbosch, Stellenbosch.

- Overend, R, 1982. The average haul distance and transportation work factors for biomass delivered to a central plant. Biomass 2, 75–9. doi: 10.1016/0144-4565(82)90008-7

- Perlack, R & Turhollow, A, 2003. Feedstock cost analysis of Corn Stover residues for further processing. Energy 28, 1395–403. doi: 10.1016/S0360-5442(03)00123-3

- Phalan, B, Mertzky, M, Butchart, S, Donald, P, Scharlemann, J & Stattersfield, AB, 2013. Crop expansion and conservation priorities in tropical countries. PLoS ONE 81, e51759. doi:http://doi.org/10.1371/journal.pone.0051759.

- Robertson, GP, Dale, VH, Doering, OC, Hamburg, SP, Melillo, JM, Wander, M, Parton, WJ, Adler, PR, Barney, JN, Cruse, RM, Duke, CS, Fearnside, PM, Follett, RF, Gibbs, HK, Goldemberg, J, Mladenoff, DJ, Ojima, D, Palmer, MW, Sharpley, A, Wallace, L, Weathers, KC, Wiens, JA & Wilhelm, WW, 2008. Agriculture: Sustainable biofuels Redux. Science 322(5898), 49–50. doi: 10.1126/science.1161525

- Romeu-Dalmau, C, Gasparatos, A, von Maltitz, G, Graham, A, Almagro-Garcia, J, Wilebore, B & Willis, KJ, 2016. Impacts of land use change due to biofuel crops on climate regulation services: Five case studies in Malawi, Mozambique and Swaziland. Biomass and Bioenergy 111. doi:http://doi.org/10.1016/j.biombioe.2016.05.011.

- Rulli, M, Bellomi, D, Cazolli, A, de Carolis, G & D’Odorico, P, 2016. The water–land–food nexus of first-generation biofuels. Scientific Reports 6. doi:10.1038/sre2521p2.

- Stafford, W, Lotter, A, Brent, A & von Maltitz, G, 2017. Biofuels technology: A look forward. UNU-WIDER. Working Paper No: 2017/87. https://www.wider.unu.edu/sites/default/files/wp2017-87.pdf.

- Scharleman, J & Laurence, W, 2008. How green are biofuels? Science 319(5859), 43–44. doi: 10.1126/science.1153103

- Schubert, R, Schellnhuber, H, Buchmann, N, Epiney, A, Grießhammer, R, Kulessa, M, et al. 2008. Future bioenergy and sustainable land use: Flagship report. German Advisory Council on Global Change, Berlin.

- Searcy, E & Flynn, P, 2009. The impact of biomass availability and processing cost on optimum size and processing technology selection. Applied Biochemistry and Biotechnology 154, 92–107. doi: 10.1007/s12010-008-8407-9

- Tilman, D, Socolow, R, Foley, JA, Hill, J, Larson, E, Lynd, L, Pacala, S, Reilly, J, Searchinger, T, Somerville, C, Williams, R, 2009. Beneficial biofuels—The food, energy, and environment Trilemma. Science 325(5938), 270–1. doi: 10.1126/science.1177970

- Transport Research Centre, 2008. Biofuels: Linking support to performance. OECD, Danvers.

- von Maltitz, G, Nickless, A & Blanchard, R, 2010. Maintaining biodiversity during biofuel development. In Amezaga, JM, von Maltitz, G & Boyes, S (Eds.), Assessing the sustainability of bioenergy projects in developing countries: A framework for policy evaluation. Newcastle University, Newcastle Upon Tyne, 81–118.

- von Maltitz, G & Stafford, W, 2011. Assessing opportunities and constraints for biofuel development in sub-Saharan Africa. CIFOR. Working Paper 58. Bogor, Indonesia. http://www.cifor.org/publications/pdf_files/WPapers/WP58CIFOR.pdf.

- von Maltitz, M & van der Merwe, M, 2017. Land and agronomic potential for biofuel production in Southern Africa. WIDER Working Paper 2017/85. Helsinki: UNU-WIDER.

- World Energy Outlook, 2012. World energy outlook. www.worldenergyoutlook.org/media/weowebsite/2012/WEO_2012_Water_Excerpt.pdf Accessed 2 March 2017.

- Worldwatch Institute, 2006. Biofuels for transportation: Global potential and implications for sustainable agriculture and energy in the 21st century. Worldwatch Institute, Washington, DC.

- Wright, M & Brown, R, 2007. Establishing the optimal sizes of different kinds of biorefineries. Biofuels, Bioproducts and Biorefining 1, 191–200. doi: 10.1002/bbb.25