IMPACT

Although bridging policy and financial resources is considered important in public sector organizations, making this connection is difficult in daily practice. The authors show how policy control, a new approach that has been initiated in Dutch central government, can help bridge this gap. The traditional methods of performance-based budgeting focus on the idea that resources should be spent rationally in terms of economy, efficiency and effectiveness. Policy control, in contrast, approaches the linkage of resources and policy objectives from the perspective of the intended societal added value of policy plans.

ABSTRACT

Whereas in many countries efforts have been made to implement performance-based budgeting (PBB), the application of this method is difficult. This exploratory study shows, from both an organizational and an operational perspective, how a new approach—policy control—can improve the alignment between policy and means. Instead of being involved in the budget cycle, in policy control controllers interact in the policy cycle. However, the specific role and activities of the policy controller differ from one government department to another. The authors call for far more attention to be paid to organizational and human factors in PBB.

Introduction

Society, citizens and politicians are increasingly interested in the extent to which public sector organizations realize planned policy objectives and how taxpayers’ money is being used for this purpose. To this end, budgeting and management reforms have been carried out in order to improve the efficiency and effectiveness of public spending and to enhance rational decision-making in administrative and political processes (Grossi et al., Citation2016). Many public sector organizations see performance-based budgeting (PBB) as an appropriate and transparent method of allocating public resources as it relates budgets, programmes and performance. PBB is therefore expected to provide information to all stakeholders about the goals a public organization is trying to achieve, the costs involved and what citizens receive in exchange for their taxes. However, the practical application of PBB is complex and difficult due to conflicting technical, policy and political rationalities (Pollitt, Citation2018; Ho & de Jong, Citation2019b; Budding et al., Citation2022).

The aim of PBB is to improve the quality of public spending, which is traditionally expressed in terms of economy, efficiency and effectiveness (Liu et al., Citation2010). Part of PPB is the integration of budget planning into policy planning where there has been an increased focus on value-for-money considerations such as efficacy, effectiveness and public satisfaction of spending (Ho, Citation2018).

Although PBB has been widely adopted, it remains a major challenge to include performance information (PI) in the decision-making process on budgets and policy programmes (Budding & Grossi, Citation2014; OECD, Citation2007). Recurring challenges are related to improving performance measurement, the quality of PI, and processing this information so that decision-makers can take well-informed decisions. Several researchers have argued that the issue of how best to use PI in budgeting remains unresolved (OECD, Citation2007; Lu et al., Citation2015; Mauro et al., Citation2017; Ho & de Jong, Citation2019a).

In the Netherlands, which during the New Public Management (NPM) reform wave was considered one of the leading OECD countries in terms of PPB implementation (OECD, Citation2007), a new approach has been initiated to improve the effective allocation and control of public resources in order to increase the value of public spending. This new approach—'policy control’—has some similarities with approaches from the NPM and Public Value Management (PVM) era which aimed to enhance the link between policy and financial resources and rationalize decision-making in this regard. Although policy control has several similarities with PVM (and to a lesser extent NPM), it concentrates more on improving the coherence between the policy and budget rationality of PBB, by assessing policy plans for their expected societal impact and financial feasibility. The policy control approach also includes a new role for management accountants.

The aim of the research reported here was to explore what this new approach, policy control, entails from a practical point of view. We used the multi-layered institutional framework of performance budgeting formulated by Ho (Citation2018) because it is a useful tool for systematically analysing PBB practices from a multi-level perspective. This article contributes to the literature in at least two ways:

We describe what policy control means.

We analyse the role of the policy controller by exploring the role from the perspective of professional practice. We do so by investigating how Dutch ministries have organized this function.

Our analysis revealed several findings. First, in general, policy control appears to be about independently testing and issuing advice about policy documents that have financial implications. Second, the ministries we studied all had their own interpretation of what policy control actually is. Third, in practice, there is no uniform set of instruments to test policy plans. Fourth, human factors, such as individual attitudes and interpretations of general financial frameworks, seem to determine the way policy control is carried out.

Literature review

Budget and management reforms

Improving the efficiency and effectiveness of public spending is one of the key themes of more than half a century of budget and management reforms (Budding & Grossi, Citation2014). To this end, performance oriented management and budgetary reforms have been carried out. From the 1990s onwards, there has been renewed attention on measuring and managing performance, with performance measurement being used on the one hand as a tool to improve efficiency, effectiveness and productivity, and, on the other hand, as a means to account for the societal outcomes achieved (Budding et al., Citation2019). Since 2000, under the umbrella of Public Value, this last aspect is considered to be increasingly important in the activities and behaviour of public sector organizations.

In addition to management reforms, various budgeting reforms have been undertaken to strengthen the relationship between policy and financial means and rationalize decision-making. These are the planning–programming–budgeting–system (PPBS), zero-based budgeting (ZBB), and performance based budgeting (PBB). These initiatives were prompted by the desire to bring clarity about the goals of government, to use public resources more effectively in order to fulfil these goals and to rationalize budget decision-making (Budding & Grossi, Citation2014). Nowadays PBB is considered the most appropriate budgeting tool to link financial resources to measurable results, as PI is used in the budgeting process and the allocation of resources to programmes (OECD, Citation2007; Budding & Grossi, Citation2014). Ho and de Jong (Citation2019a) define performance budgeting as:

The integration of performance information and analysis into the full budgetary process, from budget preparation by the executive branch and appropriation decision-making by the legislature, to budget execution by line ministries and departments, and auditing and spending review, so that government resources can be used more efficiently, cost effectively, and accountably to achieve policy goals and policy-makers’ priorities.

PBB is based on the assumption that the use of PI leads to better-informed decision-making. However, research shows that most governments find it difficult to provide decision-makers with good-quality, credible and relevant information in a timely manner, let alone incentives to use this information in budgetary decision-making (Budding & Grossi, Citation2014; Budding et al., Citation2022).

In the public sector, performance management grew in importance from the 1980s onwards, and is often regarded as an element of NPM reforms (Budding & Grossi, Citation2014). Performance management in the public sector is a complex and challenging issue for many reasons (Pollitt, Citation2018). This has to do, among other things, with explicating political objectives, and making performance measurable, together with measuring unintended effects. de Vries and Nemec (Citation2019) argue that defining performance and measuring performance is a classic ‘wicked problem’ because performance has multiple and ambiguous meanings and involved actors each have their own interpretation and opinion about how performance should be measured. The difficulty with performance measurement is that the effects of government interventions are often hard to measure because public performance has to take multiple values into account and is achieved in co-production (de Bruijn, Citation2003). In addition, the ultimate effect of government intervention—the outcome—is often only noticeable after many years.

Budget and policy alignment

Over time, the emphasis of budgeting has changed from a traditional financial control instrument, to a planning instrument, and now to a performance budget management approach that places more emphasis on the importance of budget and policy alignment. The latter is seen as a platform for various management, budgetary and policy-making purposes so that budgetary planning, policy planning, performance management and the achievement of strategic objectives can be more effectively aligned (Ho, Citation2018). The extent to which PBB can serve as a tool for policy planning, financial planning and management control depends on many factors, with the integration of PI being considered most important (Schick, Citation2014; Grossi et al., Citation2016). The use of PI in budgeting can be encouraged by linking the budgeting process to other fundamental cycles, such as the policy cycle (Grossi et al., Citation2016).

The policy planning function can be strengthened by creating a network of PBB supporters and good government advocates that can span multiple electoral cycles and take a long view of government performance, policy and budgetary challenges (Ho, Citation2018). These networks might include civil servants, academics and national institutes for strategic policy analysis. Based on policy insights, PI and multi-year financial insights, these networks could encourage policy-makers and decision-makers to understand the importance of performance logic and evidence-based policy-making in the political process of budgeting. However, budgeting is a political process that involves different rationales, where the importance of performance logic and evidence-based policy-making is not always acknowledged (Schick, Citation2014; Ho, Citation2018; Ho & de Jong, Citation2019b). As a result, the policy function is deployed selectively and therefore has limited impact on performance budgeting and management. This effect is reinforced because of the political and economic institutional design that, in many countries, encourages politicians to focus on the short-term demands of their electorate (Ho, Citation2018).

An example of an initiative resembling a network of good governance advocates is the introduction in 2004 of the Performance Assessment Rating Tool (PART) in the USA. PART was designed by the Office of Management and Budget (OMB) to assess the effectiveness and efficiency of programmes in a transparent and systematic manner (Moynihan & Kroll, Citation2016). PART classified the effectiveness of all federal programmes based on a mixture of performance data, evaluations and policy information but has been discontinued due to limited effectiveness and replaced by the Obama Performance Agenda (Joyce, Citation2011).

The Dutch initiative to improve the effective allocation and control of public resources in order to increase the societal added value of public spending builds on the idea of creating a network of good governance advocates. It has similarities with PART—the Government Accounts Act was amended in 2019 requiring that all proposals sent to parliament include an explanation of the effectiveness, efficiency, policy instruments and financial consequences. It also seems to have similarities with other initiatives, such as the value-for-money movement, because the ‘Insight Into Quality’ programme started in 2018 has the aim of gaining more information about the results of policies to add value to public programmes. The reasoning behind this is that citizens are entitled to effective and efficient spending of public resources and the Dutch ministries want to do better in this respect (House of Representatives, Citation2018–2019).

Focus of this article and methodological approach

We explored the meaning of policy control from a practical point of view, and more specifically, the role of the policy controller. We did so by investigating how Dutch ministries have organized this function. Our research question was: what does policy control mean from a professional perspective?

Analytical framework

Since policy control seems to build on the idea of creating a network of good governance advocates, but for which there is hardly any information available in the literature, we used the multi-layered Institutional Framework of Performance Budgeting as the framework to analyse practice policy control (Ho, Citation2018). This framework provides useful guidelines to systematically analyse the practice of policy control from different practitioner-oriented perspectives, including the political–institutional, the organizational and the operational context. Within these perspectives, several aspects can be analysed that are considered important for the implementation of PBB and thus for the effectiveness of the instrument.

The framework was not used to determine the extent to which these factors were present in practice, but as a tool to describe how these aspects were interpreted from a policy control perspective. From the perspective of departmental and programme operations, we wanted to describe the role of the policy controller and the instruments used for policy control.

Research setting

In the Dutch central government, PBB started to be used in the 1980s. Dutch central government has been increasing its focus on the effectiveness and efficiency of government spending and improving their understanding of the link between policy, performance, and resources. Various operations and quality programmes have been executed in the central government, to slim down, increase manageability and improve the effectiveness and efficiency of government spending (see ). Examples of these operations and programmes are the Accounting Framework (Operatie Comptabel Bestel) in the 1980s, the government memorandum From Policy Budgets to Policy Accountability (Van Beleidsbegroting Tot Beleidsverantwoording) in the late 1990s, and the development of the methodology of accountable budgeting (Verantwoord Begroten) in 2013 (Budding et al., Citation2019). Despite all these initiatives to integrate budgets, programmes and PI, in practice ministers still do not have sufficient insight into the extent to which objectives are achieved, how taxpayers’ money is used for this purpose and how far societal added value has been created (Court of Audit, Citation2013, Citation2016; Study Group for Budgetary Space, Citation2016). Since 2012, the Netherlands Court of Audit has found in various studies that it is insufficiently clear what results are desired by the ministries and what results have been realized in practice with public funds. Other findings include that the quality of policy information is not appropriate in many cases, ministers do not evaluate their own performance, and that ministries generally lack good evaluation.

Figure 1. Summary and timeline operations and quality programmes in Dutch central government.

When the cabinet Rutte III took office in October 2017, ministers stated that the quality of policy should be improved by increasing knowledge about the effectiveness and efficiency of policy and improving the evaluation system. In order to improve the societal added value of government resources, the cabinet wanted to make clear at the start of policy processes, what works and what doesn’t work, why this is so and what costs are involved (House of Representatives, Citation2018–2019). As a result, the operation ‘Insight into Quality’ started in 2018. As well, the Government Accounts Act was amended in 2019, with a new rule prescribing that all proposals and intentions that will be sent to parliament need to include an explanation of the effectiveness, efficiency, policy instruments and financial consequences. This was done because quantifying the societal impact of policy is difficult and, by amending the Government Accounts Act, the cabinet tried to ensure that the ‘right’ questions (such as ‘what are the benefits of the policy?’) were asked, before proposals were submitted.

Research method

The empirical research was carried out on the basis of a multiple case study. Six out of 12 ministries were selected. An overview of the departments and job titles of the interviewees is shown in . The main selection criteria were that a policy control department existed and that the ministry used the function title ‘policy controller’. In total, nine interviews were conducted, and 11 people were spoken with. The civil servants who were interviewed all performed policy control tasks and they all had a position in which it was possible to explore how policy control was organized in their ministry. The list of interview questions is included in . The interviews lasted 45 minutes on average and were fully transcribed, coded and then analysed. Various documents were handed over during the interviews, describing the function of policy control in the ministry. These documents were also used in our analyses. We tried to limit individual biases by triangulating the opinions of the interviewees with the findings from a document analysis of documents collected during the interviews.

Table 1. Interviewed officials.

Table 2. Questionnaire.

Results

The results of the research were interpreted using Ho’s (Citation2018) multi-layered framework, as shown in . This framework provides useful guidelines to systematically analyse policy control from different perspectives, including the political–institutional context, the organizational context and the operational context. It is used as a tool to systematically describe what policy control means from different organizational perspectives. Our study focused on the administrative implementation of policy control practice and therefore concentrates primarily on the organizational and operational context and was not concerned with the political–institutional issues.

Figure 2. The analysis framework based on the the multi-layered framework.

The political–institutional context of the policy control process

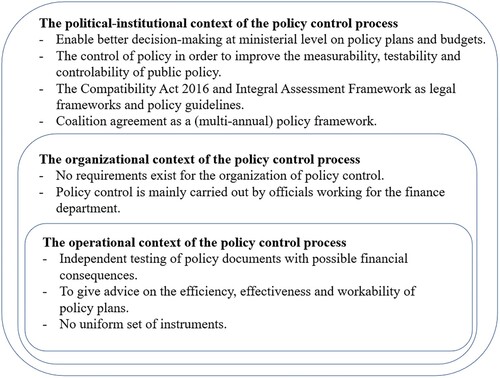

The first layer of the multi-layered framework analysed the political–institutional context, including the executive and legislative relationship and relevant legislative frameworks.

The executive and legislative relationship: The Netherlands is a democratic constitutional state with a dualistic parliamentary system. The parliament controls the government in the implementation of legislation. Each of the 12 ministries is headed by a minister, who is fully responsible for policy implementation and accompanying financial management issues, including budget control.

Legislative frameworks: The Compatibility Act 2016 is the foundation of the Dutch central government’s budget cycle. This act prescribes rules on the establishment of the budget and other financial management issues of ministries. Each ministry has its own budget statement which forms part of the state budget. By means of a coalition agreement, the political leaders in the government set (multi-annual) policy objectives. Ministries work out the policy objectives in concrete policy plans and incorporate the financial consequences in the budget. The budget of a ministry gives an overview of the policy, the available budget and the budget instruments used for the intended policy. For each budget article, budget indicators are drawn up to monitor the policy. Each budget is passed as a separate law by the parliament. During the legislative process, the parliament can amend the budget law.

Policy control: Our research showed that policy control is generally initiated within the ministries of the Dutch central government and is designed to improve the effective allocation and control of public resources in order to increase the societal added value of public spending (see for a summary of the findings, as well as an explanation of the abbreviations used). Policy control is about improving the measurability, testability and accountability of public policy. The aim of policy control is to enable better decision-making at ministerial level on policy plans and budgets by involving management accountants—policy controllers—in the policy cycle. According to one policy controller:

The core of policy control is to look at how the policy cycle at the department is structured and how it works. And that means that you also have to make sure that all phases in the policy cycle are properly dealt with.

Table 3. Overview of differences and features of policy control between the ministries.

We found that policy control tries to clarify the relationship between the intended societal effect and the planned activities that ministries want to implement in order to monitor and evaluate to what extent the intended effects are achieved. In addition, some policy controllers indicated that the amendment to the Government Accounts Act broadened their scope—the focus of control shifted or, at least, was extended from the budget to the policy. For example, the policy controller at I&W said:

The difference with perhaps the old method of control is that it was often very financially oriented … Is there a budget, does it fit within the budget? Perhaps even a bit of efficiency but efficacy, for example, was much less on the real control point of view.

Regarding the political–institutional context of the policy control process, we found that the coalition agreement largely forms the policy framework guiding government policy, which is elaborated in specific policy proposals. For the execution of policy control, article 3.1 of the Government Accounts Act and the Integral Assessment Framework (Integraal afwegingskader) were the most commonly used legal frameworks. Article 3.1 of the Compatibility Act prescribes that proposals, intentions and commitments to parliament must include an explanation that addresses: the objectives, the effectiveness and the efficiency that are being pursued; the policy instruments that will be used; and the financial consequences for the national government and, where possible, the financial consequences for societal sectors.

In addition, the Integral Assessment Framework is a guideline for policy-makers and contains standards that good policy should meet.

Organizational context of the policy control process

The second layer of the multi-layered framework analysed the organizational set-up of policy control within ministries, including organizational mandate, positioning within the ministries and organizational design.

Mandate: Minsters are responsible for the financial management of their budget and their ministry. They are supported in this by the finance and economics department (FEZ). For the implementation of policy plans ministers are supported by civil servants. The administrative leadership is represented on the board of directors general (DGs). These include the secretary general (SG), the deputy SG, and DGs, who are each fully responsible for policy implementation and budget control for a particular policy area of the ministry. In addition, the finance and economics department director is often a member of the administrative board.

Organizational positioning: Policy control is mainly carried out by officials working for the finance department, so their activities are closely related to the processes of financial management. All finance departments of the interviewed policy controllers had a division for policy control. Within this division, different clusters are involved. Generally, a distinction is made within this division between clusters with policy controllers who support the SG and the minister at corporate level and clusters of policy controllers who support other members of the administrative top management, DGs. The administrative leadership is formed by DGs who are each fully responsible for the policy implementation and financial management of the related budgets for a specific policy area of the ministry.

Organizational design: Policy control appears to be organized on a situational basis—there are no requirements for the organization of policy control. There are some differences between the ministries in the organization of policy control (refer to for a comparison of organizational characteristics). At four of the six interviewed ministries (SZW, J&V, FIN and I&W), control of policy implementation was seen as part of policy control, while in two ministries it was not. The policy controllers of these four departments give advice on the policy proposals and on the arrangements that are made within executive agencies about the frameworks within which the implementation is carried out, such as price, quality and quantity. Two ministries (LNV and EZK) have a separate monitoring committee, which provides an expert opinion on new policy proposals, specifically for financial instruments of ‘a certain size’. Three of the six ministries have a policy evaluation committee that gives an expert opinion about evaluation design. Finally, one ministry (SZW) has economists in their finance department, of which the policy control team is a part. Economic forecasting is not a policy control activity, but it does help policy controllers to fulfil their role, because they are asked to calculate policy alternatives. At the other ministries, this function is executed by another department.

The operational context of the policy control process

The third layer of the multi-layered framework analysed the operational context which we have translated into the interpretation of policy controllers, the tools and information they use in performing their role.

Role interpretation task goals: The interviews revealed that, at the operational level, the ministries have different views on what policy control is. All ministries indicated that the policy controller has both a testing and advisory role. The interviews revealed that policy control relates to the independent testing of policy documents, such as policy plans and memorandums with possible financial consequences, to give advice on the efficiency, effectiveness and workability of these plans. This entails the budget, budgetary fit, efficiency, effectiveness, legality, and workability. Policy control focuses on all phases of the policy cycle, but its main focus is on the policy-making phase when a policy theory is written down and the set of instruments devised. The interviewed policy controller of EZK expressed this as follows:

We actually keep a critical eye on everything that is financial or potentially financial-like in relation to policy and often have an opinion about it. From the very first policy phase of policy development to the end: the evaluation.

The interviews showed that policy controllers have different perceptions of their role and that there are differences in the way controllers fulfil their role. All controllers had slightly different views as to what they believed policy control is in practice and how the ‘test role’ is interpreted. This was reflected in the way they described their role. There are controllers who stated that they think along with the policy-makers and see themselves as a ‘critical friend’ (EZK). The policy controllers at LNV, FIN and I&W emphasised the controlling role and tested different versions of policy plans before sending them to the minister for decision-making. Finally, some controllers stated that they ensure that all relevant information is included in the plans so that the minister can make a well-considered decision. This was the case for the policy controllers interviewed at SZW who indicated that it was particularly important for a proposal to be ‘ready for decision’ when it goes to the ministers. According to them, this meant that all relevant information is included and that all actors are involved in the preparation of the proposal. They do this by collecting and interpreting information and ensuring that all relevant actors are involved, for example for an implementation or a legal test. According to the interviewed controllers at J&V, the role of the policy controller is more than just testing policy documents and advising managers to improve the expected effectiveness and efficiency of policy plans. They argued that they should also have a role in formulating policy objectives.

The research shows that, in accordance with the Government Accounts Act 2016, all proposals with financial consequences are submitted to the finance director to get a go-ahead for approval. The interviewed policy controllers stated that they perceived it as a challenge to be involved in the policy-making process, so that advice can be given and proposals tested.

Other frequently mentioned tasks of the policy controller included monitoring policy developments, assessing evaluations in terms of design and operation, writing the budget texts, maintaining the network with internal actors, and filling the budget administration.

Instruments: The interviews revealed that policy control focuses on how to achieve objectives by using public money as efficiently and effectively as possible. However, in practice, there is no uniform set of instruments to test policy plans. In addition, the interviewed policy controllers found it difficult to describe how they can test efficiency and effectiveness and described this as a ‘continuous search’. One of the interviewed controllers stated that policy control is not an exact science and that there is no checklist that can be used:

We do not have … an instrument for this. So that is something that I think we are doing to a large extent within the own standards and values of the employees involved (policy controller at J&V).

The most important tool is common sense. And a kind of natural attitude of a controller, to create as much effect as possible for the euro that has been used (policy controller at EZK).

The interviews showed that ‘common sense’ and ‘awareness that taxpayers’ money is being handled’ are two important aspects of the policy controller's work. However, existing legislation and regulations, budgetary rules and internal financial policy frameworks are important elements in the assessment of efficiency and effectiveness issues. In practice, the way in which these frameworks are used differs from ministry to another. Some ministries use a questionnaire or checklist to assess policy proposals. However, no uniform checklist is used by all ministries to determine whether a policy proposal is effective or whether a letter can be sent from the minister to parliament.

Available information: Ministries aim to develop as many evidence-based policies as possible, but in practice they find this particularly difficult. The interviews showed that it is difficult to actually apply policy insights. This complicates the assessment of the assumptions underpinning the policy because there is no qualitative standard available. As a result, the qualitative elaboration of policy control differs between ministries and between policy controllers. Therefore, policy evaluations and other policy evaluation studies are seen as an important part of the policy control function, so that qualitative and relevant policy information can be used. The interviews revealed that policy evaluations are considered to be very important and attention to their quality has increased in recent years. This is especially the case when new policy measures are being drafted and thought has to be given to how that policy will be monitored. For instance, the policy controller in ministry EZK emphasised the importance of good-quality evaluations:

This is really a few steps beyond where we were some 10 years ago. Then you would evaluate and think ‘oh well, complicated and what is the policy theory?’ We had never really written that down. Let's let a consultant firm sort that out.

Generally, the interviews showed that the policy controllers mainly have a process-oriented role with regard to the execution of policy evaluations and they do not carry out evaluations themselves.

Conclusion and limitations

This research explored what the renewed Dutch policy-oriented application of PBB—policy control—entails and how it is organized within the ministries of the Dutch central government.

Policy control in the Netherlands is designed to improve the effective allocation and control of public resources in order to increase the societal added value of public spending. This is being done by involving policy controllers in the policy cycle, where they interact in all phases of the cycle but with their main focus on the decision-making phase. In professional practice, policy control means clarifying the relationship between the intended societal effect and the planned activities that ministries want to conduct, in order to be able to monitor and evaluate the extent to which the intended effects are being achieved. Policy controllers do this in practice by independently testing policy such documents as policy plans and memorandums with possible financial consequences, and giving advice on the efficiency, effectiveness and workability of these plans. This entails the budget, budgetary fit, efficiency, effectiveness, legality, and workability. Therefore, with the appearance of policy control, the orientation of controllers seems to have shifted from the budget cycle and the integration of PI to the whole policy cycle where the policy controller uses policy and PI in testing proposals and giving advice on improving policy proposals. Additional activities of the policy controller include participating in policy evaluation and monitoring committees, writing budget texts and handling the budget administration.

The traditional methods of PBB address the link between means and policy objectives from the angle of the budget cycle and the idea that resources should be spent rationally in terms of economy, efficiency and effectiveness. Policy control, in contrast, approaches the linkage of resources and policy objectives from the perspective of the intended societal added value of policy plans. Policy control distinguishes itself from the traditional elaboration of PBB by improving the decision-making for budgets and policy plans by interacting in the policy-making process. In doing so, policy control is involved in the policy cycle, rather than the budget cycle. The policy controller plays an active role in the policy process, testing proposals and advising on improving these plans. Furthermore, policy control includes the assessment of policy proposals on the coherence of goals, instruments, budget and societal impact. Therefore, policy control is about strengthening the coherence between goals, instruments and means by interacting in the policy process. Although policy control is a promising initiative, it is difficult to find out in practice how it can be organized, implemented and carried out effectively. To get a better understanding of the differences between PBB and policy control, compares the distinguishing characteristics of PBB and policy control.

Table 4. Comparison of characteristics between performance-based budgeting (PBB) and policy control.

With regard to the political–institutional context of the policy control process, the parliament and the cabinet Rutte III had great ambitions with regard to the improvement of insights into the quality of policy and to act accordingly. However, there is no uniform framework in place for achieving this. In practice, the policy controllers apply financial and policy regulations in their own way. In daily practice, ‘common sense’, the awareness that taxpayers’ money is being spent and the controller's personality are important aspects. In the absence of clear guidelines on how to conduct policy control, ministries are reliant on how policy control is actually practised by the individual policy controller.

The aim of policy control is to enable better decision-making at the ministerial level on policy plans and budgets. With regard to the organizational context of the policy control process, we found that the role of policy controller is primarily performed by officials in finance departments. The way in which policy control is organized and implemented varies from one ministry to another and seems to be determined on a situational basis. This may be due to the differences in the character of the ministry (for example more directed on policy-making or policy execution) or the way it is organized (for example whether it makes use of executive agencies). Further research in this area could focus on the differences between ministries and whether the size of the departmental agencies influences the role of the policy controller in the phases of the policy cycle.

With regard to the operational context of the policy control process, the policy controllers we interviewed tried to be involved as early as possible in the policy process in order to provide advice on the instruments to be used, the financial consequences and the expected effectiveness and efficiency. In practice, it is difficult to determine and clearly measure the societal added value of government resources. However, evaluations were being conducted and there was a focus on evidence-based policy-making in order to optimize the value of government resources used. In addition, policy plans were being assessed to ensure that they contain the information ministers need to make informed decisions. Further research in this area could focus on what types of policy information is used and what factors influence the degree of involvement of the policy controller.

Our study has some limitations. First, it is exploratory in nature and the results are based on a limited number of observations. Second, the results reflect individuals’ perspectives and interpretations of what policy control is, how policy control is organized and who is involved in it. However, we tried to limit interviewees’ biases by triangulating their opinions with the findings from a document analysis of documents collected during the interviews. Therefore, we do not claim to present findings that can be generalized to all public sector organizations or even all Dutch ministries but, rather, we offer a starting point for further analysis of the policy control function and role of the policy controller, which seems to depend to a large extent on organizational and human factors. Despite these limitations, our article will be helpful to further explore ways to better align the coherence between public policy and public finance.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Budding, G. T., Faber, B., & Vosselman, E. (2019). Performance budgeting in the Netherlands. In M. S. de Vries, J. Nemec, & D. Špaček (Eds.), Performance-based budgeting in the public sector. Springer.

- Budding, G. T., & Grossi, G. (2014). Public sector budgeting. In G. T. Budding, G. Grossi, & T. Tagesson (Eds.), Public Sector Accounting. Routledge.

- Budding, T., Faber, B., & Schoute, M. (2022). Integrating non-financial performance indicators in budget documents: the continuing search of Dutch municipalities. Journal of Public Budgeting, Accounting & Financial Management, 34(1), 52–66.

- Court of Audit. (2013). Effectiviteitsonderzoek bij de rijksoverheid.

- Court of Audit. (2016). Staat van de rijksverantwoording 2015, Rijksbrede resultaten verantwoordingsonderzoek.

- de Bruijn, H. (2003). Managing performance in the public sector. Routledge.

- de Vries, M. S., & Nemec, J. (2019). Dilemmas in performance-based budgeting. In M. S. de Vries, J. Nemec, & D. Špaček (Eds.), Performance-based budgeting in the public sector. Springer.

- Grossi, G., Reichard, C., & Ruggiero, P. (2016). Appropriateness and use of performance information in the budgeting process: some experiences from German and Italian municipalities. Public Performance & Management Review, 39(3), 581–606.

- Ho, A. T. K. (2018). From performance budgeting to performance budget management: theory and practice. Public Administration Review, 78(5), 748–758.

- Ho, A. T. K., & de Jong, M. (2019a). Rethink performance budgeting presumed dead or alive and well? In A. T. K. Ho, M. de Jong, & Z. Zhao (Eds.), Performance budgeting reform: theories and international practices. Routledge.

- Ho, A. T. K., & de Jong, M. (2019b). From Practice to Theory The Future of Performance Budgeting Research. In A. T. K. Ho, M. de Jong, & Z. Zhao (Eds.), Performance Budgeting Reform: Theories and International Practices (pp. 279–295). Routledge.

- House of Representatives of the Netherlands. (2018–2019). 31865, No. 126 [Letter of government].

- Joyce, P. G. (2011). The Obama administration and PBB: Building on the legacy of federal performance-informed budgeting? Public Administration Review, 71(3), 356–367.

- Liu, W. B., Cheng, Z. L., Mingers, J., Qi, L., & Meng, W. (2010). The 3E methodology for developing performance indicators for public sector organizations. Public Money & Management, 30(5), 305–312.

- Lu, E. Y., Mohr, Z., & Ho, A. T. K. (2015). Taking stock: Assessing and improving performance budgeting theory and practice. Public Performance & Management Review, 38(3), 426-458.

- Mauro, S. G., Cinquini, L., & Grossi, G. (2017). Insights into performance-based budgeting in the public sector: a literature review and a research agenda. Public Management Review, 19(7), 911-931.

- Moynihan, D. P., & Kroll, A. (2016). Performance management routines that work? An early assessment of the GPRA Modernization Act. Public Administration Review, 76(2), 314–323.

- OECD. (2007). Performance budgeting in OECD countries.

- Pollitt, C. (2018). Performance management 40 years on: a review. Some key decisions and consequences. Public Money & Management, 38(3), 167-174.

- Schick, A. (2014). The metamorphoses of performance budgeting. OECD Journal on Budgeting, 13(2), 49–79.

- Study Group for Budgetary Space (Studiegroep Begrotingsruimte). (2016). Van saldosturing naar stabilisatie (Report No. 15). The Hague, 1 July, Annex to Kamerstuk 34 300, nr. 74.