ABSTRACT

The fourth industrial revolution (4IR) presents many opportunities and challenges in a digitised world of work. This paper draws on a systematic literature review of recent research published by accounting professional bodies outlining the impact of digital technologies on the accounting profession. By taking advantage of this work this study critically assesses the types of skills and personal qualities that graduates as future accountants will need and explores the implications for accounting education and university curricula. The analysis reveals that necessary skills for future accountants may be summarised into four categories: (a) Ethical skills; (b) Digital skills; (c) Business skills; and (d) Soft skills. The analysis reveals ‘adaptability’ and ‘lifelong approach to CPD’ as the two essential personal qualities for future accountants. The practical implications for university accounting education are summarised in a proposed conceptual framework. The proposed conceptual framework: (1) acts as a roadmap for universities to align their accounting curricula with the developments in professional body syllabi; (2) helps university accounting education teachers to update, enrich, and refocus their teaching and learning approach to the requirements of the 4IR; and (3) promotes the coordination and rationalisation of the skills and personal qualities currently pursued by employability agendas at university, course, and module levels.

Introduction

This study seeks to explore, identify, and summarise the skills demanded of future accountants in response to the fourth industrial revolution (4IR) and reflect on the ramifications for university accounting education curricula development.

Through a systematic literature review of recently published research reports, this paper examines how the fourth industrial revolution (4IR) is shaping the skills and personal qualities that accountants are expected to possess. This is particularly relevant to graduate employability as it presents a challenge and an opportunity for universities to rethink their accounting curricula and for accounting educators around the world to inform their teaching practice. The value and relevance of this study are amplified by the acceleration of digital transformation and the adoption of technology in the workplace following the COVID-19 pandemic. So far, there is a plethora of scattered, and often conflicting, evidence on how the 4IR is expected to impact the types of skills and personal qualities demanded of accountants. This study seeks to address this by exploring and summarising the skills and qualities that future accountants are expected to possess in response to the emerging working environment of the 4IR. Also, the study proposes a framework to assist universities and accounting educators in existing professionals in the accountancy field.

Contribution

The study contributes a conceptual framework which summarises the skills and personal qualities for accounting graduates in the context of the 4IR. The proposed conceptual framework has practical applications across different levels of higher education planning and delivery. First, it provides universities with a roadmap to align their accounting curricula with the developments in professional body syllabi. Second, it assists university accounting education teachers in updating, enriching, and refocusing their teaching and learning approach to the requirements of the 4IR. Third, the proposed framework promotes the coordination and rationalisation of the skills and personal qualities currently pursued by employability agendas at university, course, and module levels.

The review of the literature opens the scene for a discussion on the skills required for future accountants in the broader context of the employability of the accounting graduate and the emerging impact of the 4IR. The concept of graduate employability is outlined and the skills gap which emerges from the ‘expectation gap’ about the skills possessed by university graduates and those required by the labour market is discussed (Freudenberg, Brimble, Cameron, & English, Citation2011; Low et al., Citation2016; Suleman, Citation2018). Next, the specific impact of the 4IR on the accounting profession and how digital technology shapes the broader business context and the accounting function is considered. The introductory literature review provides an outline of the increasing role of soft skills as a key driver of accounting graduate employability and considers the role of universities in developing the soft skills of accounting students. A review of the role of professional accounting bodies on accounting graduate employability is then provided. The introductory literature review concludes with a summary of the impact of the 4IR and COVID-19 as systemic factors that influence the world of work and therefore affect the employability of accounting graduates.

Following the introductory literature review, this paper discusses the method adopted in selecting and analysing research reports published by professional accounting bodies and the additional reports used for triangulating the findings. The findings are presented and discussed in three main sections which reflect the research questions; (1) broader trends; (2) the key skills for future accountants; and (3) ramifications for university accounting education curricula.

Review of the literature

Graduate employability

Employability is the set of skills, knowledge, experiences and personal attributes that make an individual more likely to obtain employment in their preferred field (M. Smith et al., Citation2013; Yorke, Citation2006). In this context, universities have been portrayed as producers of graduates that possess the skills required by employers. However, research (Clarke, Citation2018; Gibbs, Citation2010) shows that, beyond graduate skills and attributes, graduate employability is a function of several other variables which are external to the education process. For example, the reputation of the university plays a critical role in the employability of graduates and so do existing soft skills, defined as interpersonal and social skills, including behaviour and attitudes, which influence how people interact with others and which lead to success in the workplace (Matteson et al., Citation2016; Robles, Citation2012; Tan & Laswad, Citation2018). Therefore, graduate employability can be broken down into two components: (1) social capital and (2) human capital and individual attributes.

Social capital, in the form of social class, personal networks, and the university reputation, interacts with human capital to play a significant role in the employability of graduates (Clarke, Citation2018; Succi & Canovi, Citation2019). This is external to the education provision and therefore falls outside of the scope of this study.

The human capital component of graduate employability refers to the skills, competencies and work experiences of graduates (Clarke, Citation2018; Holmes, Citation2013). Alongside the human capital, graduate employability is increasingly influenced by the graduate’s personal attributes (i.e. adaptability and flexibility) and behaviours (i.e. initiative to develop and self-manage their career) which are summarised as soft skills (Schulz, Citation2008). The emphasis of this study is to identify the hard and soft skills – summarised as ‘skills’ – required to maintain the employability of university accounting education graduates.

The skills gap and role of universities

The skills gap refers to the mismatch between the skills of university graduates and the skills demanded by employers (Succi & Canovi, Citation2019). The size and the nature of the skills gap depend on whether the right skills are embedded in the university curriculum and how they are delivered and assessed (Tan & Laswad, Citation2018). Universities have attempted to align their curricula with the skills demanded by employers but have met challenges and the expectation gap is persistent (Bridgstock & Jackson, Citation2019; Osmani et al., Citation2019). However, considering the variability of job roles and the dynamic nature of the labour market, it may be impossible for universities to continually identify and meet the hard skills required by employers (Bennett, Citation2019; Pham & Jackson, Citation2020). Instead, there is more value for universities in emphasising the development of soft skills and personal competencies which are considered as having a long-lasting effect on graduate employability (Suleman, Citation2018). Bridgstock and Jackson (Citation2019) suggest that universities avoid the challenges and policy tensions of improving employability through specific skill development. They note that the aim of universities is to instil short-term graduate outcomes, professional readiness, and the capacity to live and work productively and meaningfully across the lifespan. Others also hold the view that adding more skills in the higher education institutions curricular is futile (Frankham, Citation2017), hence depriving universities of the benefits of liaising with employers to understand and potentially address the changing needs of the contemporary workplace.

The next section discusses the expected impact of the future of work for accountants and the changing demands to retain graduate employability in the accounting profession.

The 4IR and its impact on the accounting profession

The Fourth Industrial Revolution (4IR) is a term used to describe an emerging world of work which is shaped ‘by a range of new technologies that are fusing the physical, digital and biological worlds, impacting all disciplines, economies and industries, and even challenging ideas about what it means to be human’ (Schwab, Citation2017, p. 12). In the context of 4IR, the future of work is one where humans, information and communication technologies are intertwined and globalisation accelerates (Gabriel & Pessl, Citation2016). In the future of work, because of the expected automation of job tasks, there will be a reduction in the need for intensive human labour with consequently high unemployment rates, particularly among graduates throughout the world (Baygin et al., Citation2016).

Even before the 4IR, accounting employees operated in dynamic business environments which are governed by the extensive use of technology (Chaplin, Citation2017). Also, the globalisation of markets demanded a new set of aptitudes for accountants to perform effectively across a wide range of work environments, countries and cultures (Winterton & Turner, Citation2019). Recent industry research suggests that while shifts in work and skill demands arising from the 4IR may be little different to those experienced in earlier periods of rapid technological change the accounting profession is expected to be significantly impacted (Rumbens et al., Citation2019; Silva et al., Citation2020).

The anticipated impact of the 4IR on the accounting profession includes both opportunities and challenges for accountants. Through the use of digital technologies, accountants will be able to access previously unobtainable data in real time, improve data quality through greater accuracy and timeliness, and improve assurance of information for decision-making purposes (Hart, Citation2017). For these advantages to materialise, accountants need to possess a set of new skills, mainly revolving around data analytics. At the same time, the acceleration in the adoption of digital technologies is expected to automate a substantial part of accounting tasks (Bughin et al., Citation2018).

Despite suggestions that the accounting profession is one of the most vulnerable to disruption through automation and changed business models, Bowles et al. (Citation2020) report 24 capabilities, including six requirements considered essential for every professional seeking to work in accounting, finance, and related work roles. The findings provide evidence that these capabilities, in contrast to other reports suggesting that employment opportunities for accounting graduates are in decline, can create opportunities for sustainable careers. Nevertheless, Ghani and Muhammad (Citation2019) flag concern that employer expectations are set to change significantly in the 4IR environment, which raises uncertainty on whether accounting students will be able to secure jobs when they graduate.

The professional bodies cite that recruiting skilled and qualified talent is a significant business challenge for accounting practices. For example, two-thirds of participating CPA members in Australia state that job-ready university graduates were not easily available (CPA Australia, Citation2019). Reflective of this shortage of appropriately skilled and qualified graduates is a noticeable trend for the accounting industry to recruit from a range of disciplines (Eames et al., Citation2018). Eames et al. (Citation2018) noted the shortage of career ready accounting graduates created an opportunity for students with undergraduate degrees in other disciplines to undertake accelerated learning programs to complete the requirements to become professional accountants. This trend of recruitment from other disciplines suggests an overemphasis in accounting education on technical skills and a relatively weak development of professional capabilities.

The most sought-after capabilities of accounting graduates are IT proficiency, knowledge and programming skills, and problem-solving skills to provide advice on big picture strategies (Bonekamp & Sure, Citation2015; Ghani & Muhammad, Citation2019; Richardson, Citation2020). Burritt and Christ (Citation2016) suggest that the future of the accountant lies in the credibility and relevance of reporting.

The growing importance of soft skills

Historically it was technical skills that were necessary for career employment in accounting. However, in today’s fast changing environment it is more the interpersonal skills that are required as the accounting profession is transitioning away from technical activities (Rumbens et al., Citation2019). Employers perceive accounting graduates to have the required technical accounting skills but lacking important soft skills (Low et al., Citation2016; Tempone et al., Citation2012). Also, employers continue to require accounting graduates to possess a basic understanding of fundamental accounting skills but expect that these skills will be learned on the job. At same time, employers place a greater emphasis on the soft skills of graduates such as interpersonal and communication skills, including the ability to fit in and adapt to the firm’s organisational culture (Low et al., Citation2016).

The growing importance of soft skills is also identified by research conducted by several international accounting professional bodies (e.g. CIMA, AICPA, IFAC). More precisely, communication, teamworking, time management and problem-solving skills are identified by employers as key pre-requisites for accounting graduate recruitment, ongoing employment and promotion (Montano et al., Citation2001; Tempone et al., Citation2012). At the same time, research identifies that employers perceive that accounting graduates lack these important soft skills (Teng et al., Citation2019).

The analysis of accounting job advertisements shows that employers value soft skills over technical skills. The most frequently cited soft skills in accounting job advertisements were communication, teamwork and interpersonal skills (Dunbar et al., Citation2016) alongside the requirement for candidates to have a positive attitude (Tan & Laswad, Citation2018).

Studies in accounting show the presence of different perceptions between employers and university educators regarding the skills accounting graduates should possess (Bui & Porter, Citation2010; Howcroft, Citation2017; Pratama, Citation2015). Howcroft (Citation2017) explored the conflicting views between practitioner employers, university educators and chartered management accountants, and identified a range of problems beyond the content of the curriculum. The review of the literature reveals that alongside the persistent importance of technical skills there is a growing demand for critical soft skills which the industry expects accounting graduates to possess.

The role of universities in addressing the need for soft skills

One of the goals of tertiary education is to enhance the development of employability skills and to ensure that such acquisition is made more explicit. There has, however, been criticism of universities failing to teach accounting graduates generic skills or to prepare them for the emerging global world of work (B. Smith et al., Citation2018). As discussed above, there has been a notable shift in the type of knowledge and skills required in the workplace with a growing number of employers placing a greater emphasis on the soft skills and personal competencies of accounting graduates. Given the importance of soft skills in the workplace, employers tend to believe that universities have the responsibility for developing soft skills and, therefore, the professional identity of their graduates (Jackson, Rowbottom et al., Citation2017; Low et al., Citation2016).

There is a call on universities to improve their accounting programs by use of different strategies, such as real-life scenarios as suggested by Chaffer and Webb (Citation2017), as the deficiencies in graduate competency cannot be entirely attributed to a failure of accounting higher education programmes. Jackson and Meek (Citation2020) highlight that it is the stakeholders’ collective responsibility to shape accounting curricula to better prepare students for the future of work and the expectations of the accounting profession. Dolce et al. (Citation2020) suggest that specific training programmes should be created for the less developed skills to ensure a proper linkage between theory and practice. Case studies, role-plays, experiential learning, teamwork tasks and extracurricular activities are options that universities can use to do this (Wats & Wats, Citation2009).

One way that universities have responded to this growing demand for skills and improving the employability of accounting graduates is by embedding Work Integrated Learning (WIL) components within accounting degrees programmes (Freudenberg, Brimble, & Cameron, Citation2011; Henderson & Trede, Citation2017; Low et al., Citation2016).

WIL refers to such learning activities and experiences which connect universities with the workplace and allow students to integrate theory into practice, hence students are able to develop critical soft skills and prepare for the workplace (Jackson, Citation2013; Jackson, Jones et al., Citation2017; Smith et al., Citation2016). WIL components can be broadly classified into two types: (1) placement and (2) non-placement based. In placement-based WIL students gain hands-on experience in the workplace through work placements, internships, fieldwork, job shadowing, and service learning. In non-placement WIL students engage in project-based learning, simulations, case studies and industry mentoring (Ferns & Zegwaard, Citation2014; Jackson, Jones et al., Citation2017). The value of WIL lies in the fact that students are able to enact workplace norms and professional behaviours for an extended duration and this type of learning experience is difficult to simulate at university (Bolli & Renold, Citation2017; Ferns & Zegwaard, Citation2014).

Despite the wide adoption of WIL activities in university accounting education there are a number of challenges in their implementation. Lack of participating employers, shortage of enough placements, staffing and resource limitations are key challenges for universities implementing WIL activities (Stanley & Xu, Citation2019). Although employers recognise the benefits of WIL, they face limited capacity to mentor and supervise students, difficulties in finding suitable students who can perform in the workplace, and difficulty supplying universities with suitable student projects (Jackson, Rowbottom et al., Citation2017). This increases the pressure on universities to bridge the skills gap especially in relation to developing soft skills that are necessary in adapting to the changing demands of the workplace.

The role of accounting professional bodies in accounting graduate employability

Historically, accounting professional bodies and universities have co-existed as the two independent pillars of accounting training and education. Accounting professional bodies have been focusing on meeting the employment market needs for vocational skills whereas universities have been adopting a broader focus on accounting education and research (King & Davidson, Citation2009).

Due to their vocational focus and the arm’s length relationship with employers, professional accounting bodies have been more efficient than universities in tracking and responding to the changing needs of the employment market. Reflective of this is the fact that several professional bodies have conducted extensive research on the impact of the 4IR on the accounting profession. Also, following from this research, accounting professional bodies such as ACCA, CIMA and ICAEW have updated their syllabi and competencies framework to reflect the changing conditions in the employment market (e.g. digital transformation, accounting automation).

The work conducted by professional accounting bodies is primarily aimed at their key stakeholders (e.g. members, students and learning providers). Consequently, the discussion of the findings, and particularly of the necessary skills, is confined in the context of each professional body audience. Considering that these research reports include valuable insights from key external stakeholder groups (e.g. employers, professionals) there might be important findings for universities. Thus, this study aims to identify common patterns around the necessary skills for accounting graduates by conducting further analysis on the research reports of professional accounting bodies.

The impact of systemic events and economic conditions on graduate employability

Alongside the hard and soft skills, accounting graduate employability is largely affected by the economic conditions and the labour market supply and demand (Clarke, Citation2018). Significant disruptive events, like the current COVID-19 pandemic or the 2008 Financial Crisis, have a significant systemic impact on the economy thus impacting graduate employability and required skills.

The unexpected global pandemic crisis has created serious disruptions in the working patterns across the economy (Blum & Neumärker, Citation2020; Karabag, Citation2020). The COVID-19 pandemic has seen entire industry sectors take a downturn with redundancies and restructuring becoming the worldwide norm. Businesses scaled back graduate recruitment leading to fears of a ‘lost generation’ with limited career options and opportunities (Reidy, Citation2020). In relation to the accounting profession, Antonius (Citation2020) suggests that the COVID-19 pandemic is set to force a shake-out of the mid-tier accounting market with the big four consultancies (Deloitte, EY, KPMG and PwC) all targeting the same clients. Global redundancies in the big accounting firms have been witnessed and are underway in the entire sector (Lian, Citation2020). The crisis in the accounting graduate labour market, alongside the broader impact of COVID-19 on the higher education sector, creates an existential threat for universities. There is a pressing need for universities to reassess and align their curricula with the changing skills and the working conditions of the future.

Reflecting on these developments, this paper explores the broader attributes that define accounting graduate employability in the 4IR and post-COVID-19 employment market. This involves exploring the changing role of accountants and the ramifications for universities as the analytical lens for the discussion of the common patterns of skills for accounting graduates, as justified in the previous section.

Method

This paper uses a systematic literature review which involves the systematic selection, examination and interpretation of research published by professional accounting bodies and academics exploring the impact of digital technologies on the accounting profession. The purpose of this approach is to explore the published research and identify themes in the context of the research questions (Berg & Lune, Citation2013).

The aim of the paper is to provide a focused summary of the skills which are identified by the major accounting professional bodies as necessary for the future accountants. Therefore, the selection of the literature includes publications from accounting professional bodies with significant influence over the standards and curriculum content of higher education programmes. Also, the selected literature includes publications that provide comprehensive geographical coverage making sure that international and local contexts are captured. Thus, the selection of the reports includes publications from largeFootnote1 accounting professional bodies in Europe, the Americas, and Australasia. Additionally, to maintain the currency of the findings, the selection of literature includes publications from the past five years (e.g. published in and after 2016). There are 25 research publications that met the selection criteria above and were reviewed in this study.

As a way of triangulating the evidence and conclusions found in the accounting body and institution research reports, the literature review includes nine research reports, published by consultancy firms and other organisation, that consider the anticipated impact of technology on the accounting profession and/or more broadly on the ‘future of work’. Similar to the selection criteria applied in the accounting-focused research reports, the selection of ‘other’ research reports included recent publications (2015–2020) by reputable consultancy firms and other institutions. There were nine research reports reviewed for this purpose.

The data of all the reports listed in and were analysed using an inductive thematic analysis process based on the steps outlined by Braun and Clarke (Citation2006). The 34 reports were analysed for two broad themes (1) the key skills for future accountants and (2) the broader impact for accountants and universities. The initial codes were then further interrogated to be collated and merged into sub-themes which were then used in the deeper analysis of the reports. The sub-themes were further refined to construct the framework of the presentation and discussion of data. The coding, analysis and further interrogation of data (e.g. word searches, word frequencies) were conducted using NVivo 12.

Table 1. Accounting professional body and institution research reports reviewed.

Table 2. Other research reports reviewed.

Findings and discussion

The presentation and discussion of the findings are organised in three sections: (a) the broader trends that affect and shape employability and skills in the accounting profession; (b) the key skills for future accountants; and (c) the ramifications for universities and university accounting education.

Broader trends

Alongside the identification of specific skills for future accountants, the thematic analysis of the reports reveals a set of common trends that shape the broader context of the ‘future of work’ in accounting. There are two main broader trends that are discussed below.

From manual and basic cognitive skills to technological, social and emotional skills

The review of the reports reveals a consistent agreement about the need for technological, social and emotional skills for accountants in the future. At the same time there is a broad agreement about the reduced value of manual and lower cognitive skills.

The accountancy profession and accounting & finance professionals can adapt to their changing environment, and ultimately transform to ensure relevance in the future. Eliminating manual-based accounting roles provides the opportunity to shift to broader value-added roles. (IFAC, Citation2019, p. 7)

A change in services and how they are delivered will create a need for accounting staff with different skill sets, such as technology advisory, data analysis, and the ability to present effectively to clients. (Thomson Reuters, Citation2018, p. 18)

This is also in line with the findings of other research by McKinsey & Company that explores the impact of digital transformation across several sectors of the economy (Bughin et al., Citation2018). The grand challenge for accounting will be to transform from being perceived as primarily manual tasks that require basic cognitive skills to becoming a technology enabled value-adding profession.

The importance of the balance of skills

Across the reports, there is a consistent call for accountants to possess an optimal balance of skills. For instance, Tsiligiris (Citation2019, p. ii) state that ‘a set of soft skills like adaptability and excellent human interaction, coupled with technical knowledge like key data analytics, form the necessary combination of skills for the success of Accounting Technicians in the future.’ The ACCA (Citation2020b, p. 30) further state that as accountants ‘start their careers, they have both professional and technical skills of a certain level. As their job roles progress, they may, initially, need to develop deeper technical skills which in time are balanced by further professional skills.’

At a more senior level in the organisation they place greater reliance on the technical skills of others so the professional skills acquire increased emphasis. This balance of skills is pertinent to entry-level roles and they also need a certain level of skills to be employable and from which they can advance. As accountants progress in their careers they will also need to develop specific technical skills that reflect their working and contextual environment. At senior level, accountants will then need to focus on soft and leadership skills as they will have to cultivate the technical skills of others.

The key skills for future accountants

The analysis of the reports generated several types of skills which were grouped into broader categories. The grouping of these skills categories was then verified through analysis of key industry reports about the future of work (Accenture, Citation2017; Capita, Citation2019; Bughin et al., Citation2018) and its specific impact on the accounting profession (Thomson Reuters, Citation2018). The verified skills categories are: (1) ethical skills, (2) digital skills, (3) business skills and (4) soft skills. Within each of the core skill categories there are subcategories of specific skills as summarised in .

Table 3. Categories and subcategories of skills identified as important for future accountants.

The detailed discussion of the key skills for future accountants presented in the next section is structured around the four categories and the respective subcategories of skills.

Ethical skills

The adoption of new technologies in a context of advanced analytics, facilitated by big data, imposes a number of ethical implications for the accounting profession. The use of digital technologies for automating accounting tasks and assisting decision-making via predictive analytics raises concerns about the implications of misuse of data and its impact on internal and external stakeholders (ACCA, Citation2017a; Tsiligiris, Citation2019). This comes as an addition to the increasing criticism about the ethics and accountability of certain parts of the profession following a number of accounting scandals (Brunelli & Di Carlo, Citation2020). The CPA Australia report (Citation2019; p. 21) states that ‘the availability of advanced Artificial Intelligence (AI) and Data Analysis (DA) tools, and the associated massive data collection activities, raises legal and ethical considerations’ which present opportunities for accountants to engage in developing governance frameworks ().

Table 4. Ethical skills for future accountants.

Accounting professional bodies have responded to the growing importance of ethics by constantly updating and reinforcing professional codes of ethics and conducts for their members (IFAC, Citation2018). This is also reflected across the published research where there is a consensus for future accountants to possess a set of ethical skills that can be summarised in two broad dimensions: (1) technical and (2) interpersonal ethical skills. The review of the reports emphasised the challenge of hiring the workforce with the required skillsets. This is reinforced in the McKinsey& Company Report (2018) that building a workforce that is commensurate with a company’s ambitions for automation and AI adoption will require a strategic approach – and time (p. 57).

Technical ethical skills

The technical ethical skills relate to the guidelines and code of conduct of the respective accounting body. This should also include any other ethics requirements imposed by other regulatory bodies relevant to the accountant’s role in a specific country or/and industry setting. However, with the increasing use of digital technology, accountants need to develop the technical ability to understand how complex automation models work and be in position to evaluate the potential ethical implications of assumptions and outputs (ACCA, Citation2017a; FRC, Citation2017; Tsiligiris, Citation2019). This coincides with the findings of other research suggesting that the advancements in technology will increase the importance of accounting professionals who are able to challenge the inputs and the assumptions of the automation process (Li & Zheng, Citation2018).

Interpersonal ethical skills

The analysis of the reports shows a growing need for accountants to possess personal qualities that enable them to act as stewards and gatekeepers of corporate data and compliance (AICPA & CIMA, Citation2019; IFAC, Citation2019; IMA, Citation2019). One of the key concerns identified in the research reports and other literature is the potential blind spots in data management which are created by the complexity of digital systems (Sutton et al., Citation2018). The data from various perception surveys included in the reports show a broad agreement for the importance of accountants as ‘critical friends’ who possess the right level of professional scepticism against the practices and outputs of digital technologies (AICPA & CIMA, Citation2018).

Digital skills

Digital skills are difficult to define as these would be contextual to the individual and the organisation. However, digital skills can be broadly defined as ‘a range of abilities to use digital devices, communication applications and networks to access and manage information’ (UNESCO, Citation2018b). The analysis of the reports identifies that the required digital skills for accountants would vary according to an individual’s age and experience, and the nature, seniority, and the business sector of the job role.

As shown in , there are three broader categories of digital skills that emerged from the review of the reports. First, there are the standard digital skills that relate to core legacy technologies already adopted and used at scale by accountants. For example, the cloud-based accounting solutions, standard business intelligence (BI) applications, and the digitisation of tax return activities. Second, there are the advanced digital skills that concern the familiarity of accountants with disruptive technologies like AI, blockchain and advanced BI applications. Also, programming was identified as a specific skill but can be considered part of the broader category of advanced digital skills. Third, alongside these two categories of skills, the review identified data skills as another subset of digital skills which are necessary for accountants. Data management and analysis are the two most frequently occurring data skills.

Table 5. Digital skills for future accountants.

Basic digital skills

Accountants are already, or trained to become, familiar with key technologies like ERP, spreadsheets, and Business Intelligence (BI) applications which for a long time have been used as baseline technologies. This should continue to be the focus of accounting training and education. At the same time, the content analysis of the reports suggests that there is a shift in the nature and emphasis of the standard technologies used to perform core parts of the accounting function. For example, cloud-based accounting systems are increasingly adopted by business, primarily SMEs (Tsiligiris, Citation2019). Also, there is an increased interconnectedness of systems between companies which requires accountants to become familiar with online collaboration and shared systems (CIMA, Citation2019). With the broader adoption of mobile and digital technology by businesses and the government, important tasks, such as tax returns, are now fully performed online. Therefore, in addition to the core technologies used in different contexts and job roles, accountants should also be: (1) familiar with cloud-based applications; (2) able to work and collaborate online in internal and external shared systems; and (3) perform online real-time reporting.

Advanced digital skills

A consistent finding across all reports that were analysed in and was the urgency in improving the knowledge of newer technologies like AI and Blockchain. Rather than training accountants as experts in these technologies, it is suggested that accountants need to develop their understanding of the implications of these technologies from a user perspective (AICPA & CIMA, Citation2019).

At the same time, specific job roles, like auditors, would have to develop a more comprehensive and deeper understanding of these technologies (ACCA & CA ANZ, Citation2019). This is because AI and Blockchain are adopted as central technologies to perform parts of the auditing function and therefore they become essential parts of an auditor’s toolkit. Also, these technologies are increasingly at the core of new business models adopted by the clients of auditing firms. This increases the complexity of the performance management and internal control processes which in turn disrupt the traditional auditing model (ICAEW, Citation2018).

There is an expectation that, in the future, accountants should be able to understand some basic coding of core programming languages such as Python and R (ACCA, Citation2020a; Goh et al., Citation2019) and have knowledge of SQL (Tsiligiris, Citation2019). Overall, there is the need for accountants to be able to utilise these technologies as a way of improving the effectiveness of data analysis within the context of AI-based business models (ICAEW, Citation2018).

For accountants, this does not mean that jobs are getting more difficult; it’s simply that what is needed is changing. It is therefore necessary to pick up programming languages for statistical analysis, such as R or Python, SQL for data query, and Spark and Hadoop for big data analytics. For instance, if an accountant needs to prepare a weekly report, where he or she collects data from the same sources and combine the data in the same way each time, this process can be automated in Python or R, such that one command is run and all data work is done. (Goh et al., Citation2019, p. 58)

You don’t have to be a programmer but you have to be someone who is fully onboard with the digital revolution and finding digital solutions to the way organisations conduct their work. (ACCA, Citation2020a, p. 26)

Data skills

The digital transformation of business implies an expectation for the use of large volumes of financial and non-financial data in decision-making (WEF, Citation2020). Thus, accountants are expected to be able to handle, organise and audit a diverse range of data (Thomson Reuters, Citation2018). This is summarised as data management skills which relates to the need for the data to be cleaned and checked for its consistency before it reaches an automated process (e.g. machine learning model). Accountants are considered to be in a unique position whereby they can reflect on the corporate history of the organisation and therefore assess the accuracy of data (Tsiligiris, Citation2019). At the same time, data is the core asset in the emerging digital model (Davern et al., Citation2019; WEF, Citation2020). Thus, the ability of accountants to ‘know their data’ is considered a key skill for success. For example, ‘Technology is changing the way business is conducted and data is analysed. There is an increasing focus on data management; “Know Your Data” is the new buzzword replacing Know Your Client' (ICAEW, Citation2018, p. 5)

In the future, accountants will spend more of their time in synthesising, analysing, and reporting large volumes of diverse types of data in an effective way aimed at non-technical audience. Also, there is a broadening purpose of data analysis and reporting for supporting decision-making in risk and performance management, supply chain and other core parts of the business. The ability of accountants to explore and fully utilise the data will become as important as knowing their customer and stakeholder needs.

Professional accountants need to become accomplished exploiters and users of business intelligence and data analytics technologies, the better to identify, manage and mitigate risks in the business, supply chain and economies. (ACCA, Citation2016, p. 15)

Business skills

Reflecting on the anticipated impact of digital transformation, where conventional business strategies and tactical models are disrupted, accountants of the future are seen as potential internal business consultants (IFAC, Citation2019). Accountants can meet the need for real-time accurate data analytics to be explained in non-technical language. From the thematic analysis, there are two sets of business skills emerged as key for future accountants: (1) Consulting and business advisory skills; and (2) Strategic thinking. The growing importance of advisory and strategy skills is identified in recently published research about the future skills across the economy (WEF, Citation2020).

Consulting and business advisory skills

Accountants are increasingly seen as business partners and internal consultants (Tsiligiris, Citation2019). Most reports identified that, in the future, accountants will be expected to be directly involved in the decision-making process (AICPA & CIMA, Citation2020a; Goh et al., Citation2019; Thomson Reuters, Citation2018). At the same time, future accountants should be able to act as facilitators of internal business partnerships by enabling data-driven decisions through collaborations across departments (ICAEW, Citation2018). Partly, the growing emphasis on advisory skills emerges as a result of the expected automation of manual tasks and, therefore, the shift towards value-adding tasks.

Across the board, accountants expect to spend less time on compliance, with automation playing a leading role with these mundane labour-intensive tasks, freeing up more time for value-add advisory work, and reviewing the client’s business. (Thomson Reuters, Citation2018, p. 8)

A challenge identified by a majority of accountants in incorporating advisory services is the increasingly difficult hunt for staff with an appropriate mix of technical and interpersonal skills to support such a shift in focus. (CPA Australia, Citation2019, p. 52)

Strategic thinking

The shifting role of accountants in becoming more actively involved in the decision-making process requires them to possess a broader understanding of the business environment. There is an expectation that business vision and intelligence will be even more important than digital skills in the medium term (ACCA, Citation2020b).

A very important dimension is the ability of accountants to evaluate and understand the outcomes/implications of the use of technology by businesses (ACCA, Citation2020a). For example, it becomes important for auditors to understand the impacts of the adoption of new technologies by their clients, including on performance measures and internal control processes. This is imperative in enterprises where advanced technology is integral to their business models, such as many start-up businesses ().

Table 6. Business skills for future accountants.

Soft skills

The increasing importance of soft skills for accountants emerges as a common theme from the analysis of the reports. This is justified in the context of two key aspects: (1) expecting several manual and technical tasks to be replaced or aided by digital technologies which means that accountants will have more time available to pursue other activities that require a broader skillset; and (2) in a digital environment, the emphasis of the accountant’s role will shift to the synthesis and critical analysis of data.

Across the board, accountants expect to spend less time on compliance, with automation playing a leading role with these mundane labour-intensive tasks, freeing up more time for value-add advisory work and reviewing the client’s business. (Thomson Reuters, Citation2018, p. 15)

Table 7. Soft skills.

Adaptability

Adaptability and agility are considered to be included in the most important soft skills for future accountants. This relates to the need for accountants to be adaptable to the changing conditions of the working environment and the challenges emerging from evolving business models.

The new world of work prizes a flexible approach to building a career. Stepping stones are less obvious and future roles less certain. Having a career mind-set that is flexible and that can navigate uncertainty as the profession transforms is essential. (ACCA, Citation2020b, p. 64)

Accounting firms are finding it challenging to attract and retain accountants who possess the level of adaptability and agility required. Thus, future accountants who would be able to demonstrate adaptability as part of their broader skillset are likely to be more employable.

Our research shows that business already recognises this, with adaptability and agility rated highly, and being recognised as the most important but most difficult skills for business to attract and retain. (CA ANZ, Citation2017, p. 46)

Communication skills

In a digital context, the traditional top-down intra-company communication process is replaced with multi-channel and cross-unit communication. Additionally, with the use of big data and advanced analytics, accountants are becoming key information points for several internal and external stakeholder groups (AICPA & CIMA, Citation2018). Thus, across all areas of accounting, there is the need for accountants to possess broader and more diverse communication skills. For example:

All professional accountants will need support in the decade ahead if they are to complement their strong technical skills with the strong communication skills that appear to be lacking across all specialisms and at all levels of the profession. (ACCA, Citation2016, p. 62)

Lifelong approach to CPD

Upskilling employees is recognised as one of the key pre-requisites for enabling business success in a digital environment (WEF, Citation2020). For accountants to respond to the need for upskilling they need to adopt a ‘learning-for-life’ approach. This is necessary as the accounting profession will continue to be disrupted and evolve beyond the conventional rate in the years to come. For example The successful accountant of the future is one who recognises the need to develop their skills continuously (ACCA, Citation2018b, p. 44). Thus, using a self-initiative approach, accountants will need to be able to manage their learning development by continually reskilling and upskilling to meet the changing needs of the employment market.

Critical thinking

The need for accountants to possess critical thinkingFootnote2 skills is not new. Accounting professional bodies and other external organisations have argued for the importance of critical thinking in accounting and finance since the late 1990s (Reinstein & Bayou, Citation1997). However, in the digital world of large volumes of data and automation of repetitive tasks, there is a growing importance of critical thinking as a value-adding higher cognitive skill (McKinsey, 2018). Thus, critical thinking is identified as one of the most important skills for success in the ‘future of work’ (WEF, Citation2020).

One of these higher cognitive critical thinking skills for accountants would be their ability to act as stewards of corporate governance by evaluating the accuracy and ethical implications of the outputs of automated models (Gulin et al., Citation2019; Tsiligiris, Citation2019). Also, critical thinking is required for enabling accountants to fully interrogate and combine diverse types of data to construct multidimensional narratives (i.e. operational, strategic).

Problem solving

Across the reports and other research, problem solving is a soft skill that is identified amongst the top three skills that employers consider as important for the future.

Organisations have rated the most important skills for the talent of the future as communication, problem solving, adaptability, agility, and resilience. These skills are less able to be replaced by technology and will be vital in an uncertain world. These skills are also transportable across industries and roles. (CA ANZ, Citation2017, p. 2)

Emotional intelligence

The role of emotional intelligence (EI) as a critical factor that determines the success of accountants has been the subject of extensive research (Coady et al., Citation2018; Daff et al., Citation2012; Jonker, Citation2009). In the digital era, human and social skills are becoming more valuable in accountants. For example, ‘The ability to identify your own emotions and those of others, harness and apply them to tasks, and regulate and manage them’ (ACCA, Citation2020a, p. 49). This is because these skills are required to maximise the effectiveness of automated models and perform vital tasks that cannot be performed by digital systems. Also, with the adoption of digital technologies, accountants are expected to spend more time liaising with customers and other key internal and external stakeholders. Thus, accountants are anticipated to have ‘the ability and skills to understand customer expectations, meet desired outcomes and create value’ (ACCA & CA ANZ, Citation2019, p. 18).

Ramifications for university accounting education

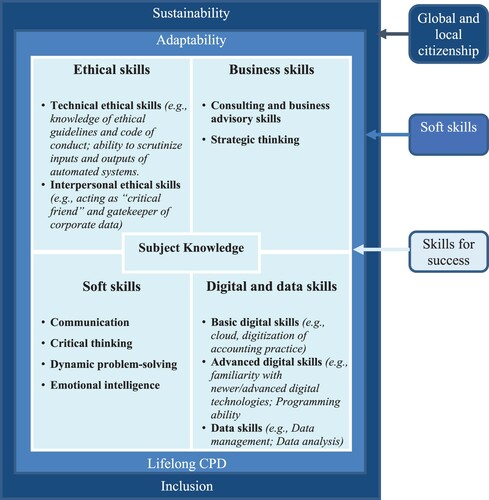

As was identified by the introductory review of the literature, there is an increased focus within university education on developing student skills and personal attributes to maximise graduate employability. At the same time, universities have a broader mission and purpose to perform that goes beyond the employability of graduates. Universities, as social enterprises, are responsible for educating global citizens who are aware of, and able to contribute in the effort to meet, the global societal challenges. As such, the discussion on how the research findings relate to university accounting education considers three different areas that form a proposed framework for university accounting education in the context of the 4IR. More specifically, the framework summarised in , includes (1) skills for success; (2) personal qualities; and (3) global and local citizenship. The framework captures the broader areas that are likely to shape the employability of accounting graduates in the futures. Regarding the specific skills embedded in each of the sections of the framework, these should be considered as dynamic.

Figure 1. A conceptual framework for university accounting education in 4IR.

Skills for success

At the core of accountants’ skills is subject knowledge. Despite the anticipated disruption in accounting jobs, and the flux of expectations about the role of technology, accounting knowledge remains the key pre-requisite for the success of future accountants. The value of all other skills (e.g. digital, soft, business, and ethical) is based on the existence of solid accounting knowledge foundations. Thus, subject knowledge should form the main pillar of university accounting education programmes in the 4IR context.

Building on the subject knowledge, university accounting education programmes should aim to achieve an optimum combination of skills across the four key categories that emerged from the analysis – (1) ethical skills; (2) digital and data skills; (3) business skills; and (4) soft skills. Some of these skills are already embedded in the accounting university education curriculum and graduate attributes. However, universities need to review their approach and focus on these skills to reflect the emerging changes in accounting job functions. For example, when it comes to soft skills, there is a pressing need to prioritise the higher cognitive skills such as critical thinking and synthesis of diverse types of data for decision-making. Similarly, digital and data skills now need to include advanced digital skills, such as basic programming and advance data analytics that form a core aspect of the future working environment for accountants. Most important, these skills require a systematic approach of teaching and learning which is best achieved in a university setting and often not easily attainable on professional courses.

Personal qualities

The second layer in the proposed framework in , refers to ‘adaptability’ and ‘lifelong CPD’ as distinct personal qualities essential to support the employability and personal wellbeing of graduates in the context of 4IR. These personal qualities extend beyond those identified as soft skills. Unlike the other soft skills, these two qualities will determine accountants’ longer-term employability and ability to perform their job role in a dynamic and often uncertain work environment. Adaptability is one of the core personal qualities identifies which refers to the ability of graduates to adapt in the changing working environment by embracing adversity, disruption, and uncertainty. This is particularly relevant in the case of unpredictable events, such as the COVID-19, that disrupt the norm of working patterns.

The analysis of the literature identified that the ability of graduates to engage in an ongoing process of unlearn, relearn, and upskill will determine their longer-term employability. Thus, a lifelong approach to CPD is an essential accounting graduate attribute that universities need to target as a way of enabling the success of their students in the future of work.

Global and local citizenship

Recent research about the impact of COVID-19 on accounting education across 45 countries has highlighted the need of university accounting education curriculum to consider ‘wider issues such as political, social and environmental matters’ (Sangster et al., Citation2020, p. 447). Thus, the third layer of the framework refers to the need for universities to raise the awareness of their graduates on a set of important global social and environmental issues. The ability of students to engage, locally and globally, in promoting a more equal, inclusive, peaceful, and environmentally sustainable society is a key graduate attribute that universities need to achieve (UNESCO, Citation2018a).

The sustainability agenda influences businesses and the accounting profession in a number of different ways. The broad adoption of the United Nations Sustainable Development Goals (UN SGDs) and their integration in business performance measurement has a direct and imminent impact in the job of accountants (ACCA, Citation2017b; Adams et al., Citation2020). At the same time, there is an increasing discussion about the suitability of existing business models and the need to capture value beyond the traditional balance sheet (ACCA, Citation2018a). Thus, there is a role of accountants to support this sustainability agenda as data champions. At the same time, there is the need for accountants to be in position to participate in the discussions for the business model for the 4IR.

Conclusions

This study aims to identify the skills and personal qualities that define the employability of accounting graduates in the context of the 4IR. To achieve this, the study conducts a systematic literature review and content analysis of a broad range of research reports published by prominent professional accounting bodies. Triangulation with evidence from non-accounting research reports about the future of work and the impact of technology is used to verify and expand the findings from the analysis of the accounting professional body reports.

The analysis of the findings shows the increasing importance of digital skills, ranging from basic IT literacy to data analytics and programming. Future accountants need to be able to understand the uses and limitations of digital technologies in the broader business context and not just limited to the accounting function. The evidence suggests that future accountants need to possess a balance of skills and a growing importance of soft skills. Soft skills are seen as paramount in helping accountants to be successful in the future of work where higher cognitive skills are valued. Also, in the context of global and local citizenship that becomes central to the society and economy, future accountants need to be introduced to the concepts of inclusivity and sustainability.

More broadly, the analysis of the reports identifies an implied expectation about the transformation of the accounting profession and the role of future accountants in it. The ability of accountants to embrace digital technologies and use soft skills will not only affect their employability but also plays a key role in the transformation of the accounting function from being transaction-based to become value-adding.

The findings of this study have direct and important practical implications for curricula which are summarily expressed in the proposed conceptual framework. This framework can generally be adapted to inform university accounting education in three respects.

First, the design of university accounting education programmes needs to reflect a balance of skills and personal qualities as these are summarised in the conceptual framework. This is essential to assure graduate employability and maintain the alignment with the professional, statutory, and Regulatory body (PSBR) syllabus. As it has been discussed earlier, accounting professional bodies have been faster than universities in adapting their syllabus to reflect the skills required in the emerging 4IR workplace. Thus, the proposed conceptual framework, provides a roadmap for universities to swiftly align their curriculum to updated syllabi of accounting professional bodies and maintain PSBR exemptions.

Second, the conceptual framework can be a practical guide for university accounting education teachers to update, enrich, and refocus their teaching and learning approach to the requirements of the 4IR. Moreover, university accounting education teachers can target the skills, personal qualities and global and local citizenship elements, suggested by the conceptual framework, within the existing course or/and module learning outcomes. For example, amongst the existing course or/and module learning outcomes there is the use and application of relevant technology in accounting practice. Teaching teams can use the findings of this study to decide on the exact types and uses of technology without the need to go through a process of course/module review. Furthermore, university accounting teachers can target soft skills, personal qualities, and global and local citizenship through formative assessment and teaching practice. For example, adaptability and critical thinking can be promoted via iterative formative assessment, and global and local citizenship can be introduced by case study and action learning teaching.

Third, the conceptual framework can be a reference for the coordination and rationalisation of the skills and personal qualities currently pursued at university, course, and module levels. With the increasing emphasis on employability in the recent past, there has been an influx of recommended skills and personal qualities added to the curriculum either as direct course learning outcomes or as indirect broader graduate attributes. Furthermore, because of the growing importance of employability in higher education, there are employability agendas at university, faculty, and course levels. This often creates increasing workload for teaching staff and students who are working hard to achieve multiple employability-driven outcomes. The conceptual framework can help reducing the workload burden by minimising overlapping and removing unnecessary employability objectives. For example, the conceptual framework can be used to coordinate the identification and effective implementation of employability objectives for the university, the faculty, and the course by identifying (a) What is important; (b) Who is leading; and (c) How it will be achieved.

The conceptual framework approach to distilling advances in various work fields and their ramifications for employability, as explained above, may also be applicable to other subject areas in university education.

Limitations

The findings of this study derive from research conducted by professional accounting bodies and other prominent organisations. There is a diverse set of robust methodological approaches and high-quality data included in these reports that provide a sound body of reliable evidence for this study. However, considering that the broader adoption of digital technologies is yet to happen, most of the data in the accounting professional body reports and the other research reviewed in this study refer to expectations and perceptions of key stakeholders about the future of work for accountants. Also, the research reports reviewed were conducted prior to the Covid-19 outbreak and the subsequent restrictions that led to an acceleration of digital transformation. Consequently, these developments, which are likely to impact the urgency and importance of the digital skills part, are not captured in the findings of this study.

Further research

Alongside the expectations and perceptions of key stakeholders about the impact of the 4IR on skills and personal qualities for accountants, there is the need for a focused investigation about the actual developments in the workplace and the accounting practice. This is even more pressing now with the acceleration in the adoption of digital technologies and the changes in work patterns as a result of the Covid-19 restrictions. As the adoption of digital technologies by different types and size of businesses grows, there needs to be further research that will investigate the post-adoption impact on the skills required by future accountants.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 In terms of number of members and role as benchmark for university exemptions.

2 Critical thinking is defined as “The intellectually disciplined process of actively and skilfully conceptualising, applying, analysing, synthesising, and/or evaluating information gathered from, or generated by, observation, experience, reflection, reasoning, or communication, as a guide to belief and action” (Scriven & Paul, Citation1987).

References

- ACCA. (2016, June). Professional accountants – The future: Drivers of change and future skills (pp. 1–88). The Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA. (2017a, August). Ethics and trust in a digital age (pp. 1–90). The Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA. (2017b, November). The sustainable development goals: Redefining context, risk and opportunity (pp. 1–28). Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA. (2018a, July). Business models of the future: Systems, convergence and characteristics (pp. 1–28). Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA. (2018b, October). Learning for the future (pp. 1–50). The Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA. (2018c, November). Learning for the future: Results from ACCA student and affiliates survey. The Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA. (2019, November). Machine learning: More science than fiction (pp. 1–52). The Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA. (2020a, March). Digital accountant (pp. 1–56). Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA. (2020b). Future ready: Accountancy careers in the 2020s (pp. 1–73). The Association of Chartered Certified Accountants. https://www.accaglobal.com/gb/en.html

- ACCA, & CA ANZ. (2019, June). Audit and technology. https://www.accaglobal.com/gb/en.html

- Accenture. (2017). New skills now: Inclusion in the digital economy (p. 46). https://www.accenture.com/t20171012t025413z__w__/in-en/_acnmedia/pdf-62/accenture-new-skills-now-report.pdf

- Adams, C., Druckman, P., & Picot, R. (2020). Sustainable development goals disclosure (SDGD) recommendations. IFAC & ACCA. https://www.ifac.org/system/files/publications/files/Adams_Druckman_Picot_2020_Final_SDGD_Recommendations_updated.pdf

- AICPA, & CIMA. (2018). The changing role and mandate of finance (p. 12). https://www.cgma.org/content/dam/cgma/resources/reports/downloadabledocuments/changing-role-mandate-finance-cgma.pdf

- AICPA, & CIMA. (2019). Future re-inventing finance for a digital world (pp. 1–44). https://www.cgma.org/content/dam/cgma/resources/reports/downloadabledocuments/future-re-inventing-finance-for-a-digital-world.pdf

- AICPA, & CIMA. (2020a). Building finance resiliency and returning the business to scale (Agile Finance Reimagined, pp. 1–20).

- AICPA, & CIMA. (2020b). Reimagining and reforming the business (Agile Finance Reimagined, p. 20).

- AICPA, & CIMA. (2020c). The key traits of digital finance leaders (Agile Finance Reimagined, p. 49).

- Antonius, P. (2020). Coronavirus Australia: Pandemic to challenge mid-tiered accounting firms. Australian Financial Review. . https://www.afr.com/companies/professional-services/pandemic-to-challenge-mid-tiered-accounting-firms-20200511-p54ry6

- Baygin, M., Yetis, H., Karakose, M., & Akin, E. (2016). An effect analysis of industry 4.0 to higher education. 2016 15th International Conference on Information Technology Based Higher Education and Training (ITHET) (pp. 1–4). https://doi.org/https://doi.org/10/gf83q7

- Bennett, D. (2019). Graduate employability and higher education: Past, present and future. HERDSA Review of Higher Education, 5, 31–61.

- Berg, B. L., & Lune, H. (2013). Qualitative research methods for the social sciences. Pearson New International edition, plus MyResearchKit without eText (8th ed.). Pearson.

- Blum, B., & Neumärker, B. (2020). Globalization, environmental damage and the corona pandemic – lessons from the crisis for economic. Environmental and Social Policy. https://doi.org/https://doi.org/10.2139/ssrn.3613719

- Bolli, T., & Renold, U. (2017). Comparative advantages of school and workplace environment in skill acquisition. Evidence-Based HRM: A Global Forum for Empirical Scholarship. https://doi.org/https://doi.org/10/ghh6ch

- Bonekamp, L., & Sure, M. (2015). Consequences of industry 4.0 on human labour and work organisation. Journal of Business and Media Psychology, 6(1), 33–40.

- Bowles, M., Ghosh, S., & Thomas, L. (2020). Future-proofing accounting professionals: Ensuring graduate employability and future readiness. Journal of Teaching and Learning for Graduate Employability, 11(1), 1–21. https://doi.org/https://doi.org/10.21153/jtlge2020vol11no1art886

- Braun, V., & Clarke, V. (2006). Using thematic analysis in psychology. Qualitative Research in Psychology, 3(2), 77–101. doi:https://doi.org/10.1191/1478088706qp063oa

- Bridgstock, R., & Jackson, D. (2019). Strategic institutional approaches to graduate employability: Navigating meanings, measurements and what really matters. Journal of Higher Education Policy and Management, 41(5), 468–484. doi:https://doi.org/10.1080/1360080X.2019.1646378

- Brunelli, S., & Di Carlo, E. (2020). Accountability, ethics and sustainability of organizations. Accounting, Finance, Sustainability, Governance and Fraud: Theory and Application, 4, 82–123. doi:https://doi.org/10.1007/978-3-030-31193-3

- Bughin, J., Hazan, E., Lund, S., Dahlström, P., Wiesinger, A., & Subramaniam, A. (2018). Skill shift: Automation and the future of the workforce. McKinsey Global Institute, 1, 3–84.

- Bui, B., & Porter, B. (2010). The expectation-performance gap in accounting education: An exploratory study. Accounting Education: An International Journal, 19(1–2), 23–50. doi:https://doi.org/10.1080/09639280902875556

- Burritt, R., & Christ, K. (2016). Industry 4.0 and environmental accounting: A new revolution? Asian Journal of Sustainability and Social Responsibility, 1(1), 23–38. doi:https://doi.org/10.1186/s41180-016-0007-y

- CA ANZ. (2017). The future of talent: Opportunities unlimited (p. 72). Chartered Accountants Australia and New Zealand. https://www.charteredaccountantsanz.com/news-and-analysis/insights/research-and-insights/the-future-of-talent

- CA ANZ. (2019). The future of trust: New technology meets old-fashioned values. Chartered Accountants Australia and New Zealand. https://www.charteredaccountantsanz.com/news-and-analysis/insights/research-and-insights/the-future-of-trust

- Capita. (2019). Robot wars or automation alliances? People, technology and the future of work (p. 17). https://www.capita.com/sites/g/files/nginej146/files/2019-11/capita-future-of-work-report.pdf

- Chaffer, C., & Webb, J. (2017). An evaluation of competency development in accounting trainees. Accounting Education, 26(5–6), 431–458. doi:https://doi.org/10.1080/09639284.2017.1286602

- Chaplin, S. (2017). Accounting education and the prerequisite skills of accounting graduates: Are accounting firms’ moving the boundaries? Australian Accounting Review, 27(1), 61–70. doi:https://doi.org/10.1111/auar.12146

- CIMA. (2019, January). Re-inventing finance for a digital world (The Future of Finance, pp. 1–44). Chartered Institute of Management Accountants. https://www.cgma.org/content/dam/cgma/resources/reports/downloadabledocuments/future-re-inventing-finance-for-a-digital-world.pdf

- Clarke, M. (2018). Rethinking graduate employability: The role of capital, individual attributes and context. Studies in Higher Education, 43(11), 1923–1937. doi:https://doi.org/10.1080/03075079.2017.1294152

- Coady, P., Byrne, S., & Casey, J. (2018). Positioning of emotional intelligence skills within the overall skillset of practice-based accountants: Employer and graduate requirements. Accounting Education, 27(1), 94–120. doi:https://doi.org/10.1080/09639284.2017.1384741

- CPA Australia. (2019). CPA Australia’s My Firm. My Future. Report. CPA Australia. https://www.cpaaustralia.com.au/-/media/corporate/allfiles/document/professional-resources/public-practice/my-firm-my-future-report-2019.pdf?la=en&rev=1d24c7ae609042c7b48f5273183b4729

- Daff, L., de Lange, P., & Jackling, B. (2012). A comparison of generic skills and emotional intelligence in accounting education. Issues in Accounting Education, 27(3), 627–645. doi:https://doi.org/10.2308/iace-50145

- Davern, M., Weisner, M., & Fraser, N. (2019). Technology and the future of the profession. Report by CPA Australia. The University of Melbourne retrieved October 2020 https://www.cpaaustralia.com.au/-/media/corporate/allfiles/document/professional-resources/business-management/technology-and-the-future-research-report.pdf

- Dolce, V., Emanuel, F., Cisi, M., & Ghislieri, C. (2020). The soft skills of accounting graduates: Perceptions versus expectations. Accounting Education, 29(1), 57–76. doi:https://doi.org/10.1080/09639284.2019.1697937

- Dunbar, K., Laing, G., & Wynder, M. (2016). A content analysis of accounting Job advertisements: Skill requirements for graduates. E-Journal of Business Education and Scholarship of Teaching, 10(1), 58–72.

- Eames, M., Luttman, S., & Parker, S. (2018). Accelerated vs. traditional accounting education and CPA exam performance. Journal of Accounting Education, 44, 1–13. doi:https://doi.org/10.1016/j.jaccedu.2018.04.004

- Ferns, S., & Zegwaard, K. E. (2014). Critical assessment issues in work-integrated learning. Asia-Pacific Journal of Cooperative Education, 15(3), 179–188.

- Frankham, J. (2017). Employability and higher education: The follies of the ‘productivity challenge’ in the teaching excellence framework. Journal of Education Policy, 32(5), 628–641. doi:https://doi.org/10.1080/02680939.2016.1268271

- FRC. (2017, May). Digital Future: A framework for future digital reporting (p. 15). Financial Reporting Council. https://www.frc.org.uk/getattachment/fd3054ee-b0f3-4968-8b20-d5bb262c4c54/Digital-Future_final.pdf

- Freudenberg, B., Brimble, M., & Cameron, C. (2011). WIL and generic skill development: The development of business students’ generic skills through work-integrated learning. Asia-Pacific Journal of Cooperative Education, 12(2), 79–93.

- Freudenberg, B., Brimble, M., Cameron, C., & English, D. M. (2011). Professionalising accounting education–the WIL experience. Journal of Cooperative Education and Internships, 45(1), 80–92.

- Gabriel, M., & Pessl, E. (2016). Industry 4.0 and sustainability impacts: Critical discussion of sustainability aspects with a special focus on future of work and ecological consequences. Annals of the Faculty of Engineering Hunedoara, 14(2), 131.

- Ghani, E. K., & Muhammad, K. (2019). Industry 4.0: Employers’ expectations of accounting graduates and Its implications on teaching and learning practices. International Journal of Education and Practice, 7(1), 19–29. doi:https://doi.org/10.18488/journal.61.2019.71.19.29

- Gibbs, G. (2010). Dimensions of quality. The Higher Education Academy. ISBN 978-1-907207-24-2 https://support.webb.uu.se/digitalAssets/91/a_91639-f_Dimensions-of-Quality.pdf

- Goh, C., Pan, G., Sun, S. P., Lee, B., & Yong, M. (2019). Charting the future of accountancy with AI (p. 74). CPA Australia and Singapore Management University School of Accountancy.

- Gulin, D., Hladika, M., & Valenta, I. (2019). Digitalization and the challenges for the accounting profession. SSRN Electronic Journal. https://doi.org/https://doi.org/10/gg53nv

- Hart, L. (2017). How industry 4.0 will change accounting? Newsletter. Journal of Accountancy, AICPA. https://www.Journalofaccountancy.Com/Newsletters/2017/Sep/Industry-4-0-Change-Accounting.html

- Henderson, A., & Trede, F. (2017). Strengthening attainment of student learning outcomes during work-integrated learning: A collaborative governance framework across academia, industry and students. Asia-Pacific Journal of Cooperative Education, 18(1), 73–80.

- Holmes, L. (2013). Competing perspectives on graduate employability: Possession, position or process? Studies in Higher Education, 38(4), 538–554. doi:https://doi.org/10.1080/03075079.2011.587140

- Howcroft, D. (2017). Graduates’ vocational skills for the management accountancy profession: Exploring the accounting education expectation-performance gap. Accounting Education, 26(5–6), 459–481. doi:https://doi.org/10.1080/09639284.2017.1361846

- ICAEW. (2018). Understanding the impact of technology in audit and finance (p. 16). ICAEW Middle East. https://www.icaew.com/-/media/corporate/files/middle-east-hub/understanding-the-impact-of-technology-in-audit-and-finance.ashx

- IFAC. (2018). Handbook of the international code of ethics for professional accountants (pp. 1–254). International Ethics Standards Board for Accountants (IESBA). https://www.ifac.org/system/files/publications/files/IESBA-Handbook-Code-of-Ethics-2018.pdf

- IFAC. (2019). Future-fit accountants: CFO & Finance function roles for the next decade (p. 16). International Federation of Accountants. ISBN 978-1-60815-418-0. https://www.ifac.org/knowledge-gateway/preparing-future-ready-professionals/publications/future-fit-accountants-roles-next-decade

- IMA. (2019). IMA management accounting competency framework. Institute of Management Accountants. https://www.imanet.org/career-resources/management-accounting-competencies?ssopc=1

- Jackson, D. (2013). The contribution of work-integrated learning to undergraduate employability skill outcomes. Asia-Pacific Journal of Cooperative Education, 14(2), 99–115.

- Jackson, J., Jones, M., Steele, W., & Coiacetto, E. (2017). How best to assess students taking work placements? An empirical investigation from Australian urban and regional planning. Higher Education Pedagogies, 2(1), 131–150. doi:https://doi.org/10.1080/23752696.2017.1394167

- Jackson, D., & Meek, S. (2020). Embedding work-integrated learning into accounting education: The state of play and pathways to future implementation. Accounting Education, 1–23. https://doi.org/https://doi.org/10/ghh6b2

- Jackson, D., Rowbottom, D., Ferns, S., & McLaren, D. (2017). Employer understanding of work-integrated learning and the challenges of engaging in work placement opportunities. Studies in Continuing Education, 39(1), 35–51. doi:https://doi.org/10.1080/0158037X.2016.1228624

- Jonker, C. S. (2009). The effect of an emotional intelligence development programme on accountants: Original research. SA Journal of Human Resource Management, 7(1), 1–9. https://doi.org/https://doi.org/10.4102/sajhrm.v7i1.180

- Karabag, S. F. (2020). An unprecedented global crisis! The global, regional, national, political, economic and commercial impact of the coronavirus pandemic. Journal of Applied Economics and Business Research, 10(1), 1–6. https://doi.org/https://doi.org/10.20409/berj.2019.152

- King, R., & Davidson, I. (2009). University accounting programs and professional accountancy training: Can UK pragmatism inform the Australian debate? Australian Accounting Review, 19(3), 261–273. doi:https://doi.org/10.1111/j.1835-2561.2009.00062.x

- Li, Z., & Zheng, L. (2018). 4th International Conference on Social Science and Higher Education. Atlantis Press. https://doi.org/https://doi.org/10.2991/icsshe-18.2018.203