ABSTRACT

While in the most developed European countries the combination of falling robot prices and high wages boosts robotization, these driving factors do not sufficiently explain why we are experiencing today a sharp increase in deployment of industrial robots in European countries with low wages. Particularly, in Central and Eastern Europe where a decade ago industrial robots were almost non-existent but today more than 30,000 robots are at work. Hence this paper, by recalculating the data of International Federation of Robotics and EU-KLEMS addresses the main question: What drives and hinders the robotization in Central and Eastern Europe?

1. The illusions of future of work and the realities of industrial robots

When it comes to the delicate topic of robotization there is a popular narrative that dominates thinking. This is a story about the expected adverse effects on jobs and employment that robotization and automation may cause, and though this story has revolved many times over the past half-century, today we are experiencing its revival (Shiller, Citation2019). It is a popular narrative not at least because it places robotization and automation in a wide social and political context and includes issues from hollowing out of the middle class and growing inequalities partly driven by job losses in robotized industries (Cowen, Citation2014; Frey, Citation2019; Temin, Citation2017; WEF, Citation2018) over detailed analyses on labour market polarization caused by automation (Autor & Dorn, Citation2013; Goos, Manning, & Salomons, Citation2009; Sebastian & Biagi, Citation2018) to the changes in voting behaviour to some extent also driven by jobs losses in particular industries with high degree of automation or by people's fear of losing jobs for the sake of robots (Acemoglu & Restrepo, Citation2017; Baldwin, Citation2019; Frey, Berger, & Chen, Citation2018).

There are, however, some theoretical and methodological drawbacks of this narrative. First, the majority of studies takes as face value what today (or in the future) technologically is possible. Although as Acemoglu and Restrepo (Citation2017) rightly recognize, technological possibility does not immediately and directly translate into economic reality, and what technologically is possible is not necessarily feasible in economic terms or workable in the business world.

Second, they almost exclusively focus on the quantitative side of the potential labour market effects and whether it comes to replacement of humans by robots or transformation of humans’ jobs because of robotization, it is the potential number of jobs affected that takes the centre stage (Acemoglu & Autor, Citation2010; Chui, Manyika, & Miremadi, Citation2015; Nedelkoska & Quintini, Citation2018). Nevertheless, the nature of work and the quality of those jobs that remain us humans and the new jobs that robot-based production could create are equally important for striking the right balance.

Third, these studies predict the potential labour market effects by applying a comparison between the skills needs of current jobs and the (future) skills of robots. They assess workers’ risk of being displaced by automation (Arntz, Gregorie, & Zierahn, Citation2016; Frey & Osborne, Citation2013), calculate the routine-task intensity index of different jobs and activities (Autor & Dorn, Citation2013; Lordan, Citation2018) and measure the regional exposure to robots (Acemoglu & Restrepo, Citation2017). In the last decade, the incontrovertible conventional wisdom has been that robotization and automation will mainly affect simple, routine physical and intellectual occupations and tasks (Autor, Levy, & Murnane, Citation2003; Levy & Murnane, Citation2004) while for today due to the latest technologies such as Artificial Intelligence, Big Data analysis and the Internet of Things the idea has become widespread that robots are already capable of taking over non-routine physical and complex cognitive tasks from people too, and they will be even more capable of doing so in the future (Brynjolfsson & McAfee, Citation2014).

To date, however, and most strikingly in the literature on future of work, industrial robots are overwhelmingly deployed in sectors with middle or higher skills requirements and their penetration is very limited in those manufacturing sectors (e.g. textile, food, beverage) where the majority of low-skilled are employed and the tasks carried out are easily replaceable by robots also at the current level of technology (OECD, Citation2019; UNCTAD, Citation2017). Hence, it comes no as surprise that there is a very high degree of uncertainty as estimates for replacement of humans’ jobs by robots range from 14 to 50% of all jobs (Arntz et al., Citation2016; Frey & Osborne, Citation2013) while those for transformation of human jobs range between 25 and 60% (Chui et al., Citation2015; OECD, Citation2016).

In these studies, the Central and Eastern European countries are classified among those economies where jobs are at highest risk of being automated. Lordan (Citation2018) calculates that given the technologies recently available the share of automatable jobs in total employment is expected to be 69% in Czechia, 61% in Hungary and 58% in Slovakia. According to Nedelkoska and Quintini (Citation2018) in Slovakia 62%, in Slovenia 53%, in Poland 52% and in Czechia 49% of the workers are threatened by the loss of their occupation because of the high probability of being automated. By contrast, Arntz et al. (Citation2016) found that only 11% of workers in Slovakia, 10% in Czechia and 7% in Poland are at great risk of experiencing the disappearance of their jobs (though for an additional 35% of workers in Slovakia, 35% in Czechia and 30% in Poland their occupations are expected to be dramatically transformed). These studies mostly highlight the high share of manufacturing jobs in total employment in Central and Eastern Europe as a primary cause of the high risk of job disappearance due to automation. Although, in these countries exactly because of the high proportion of workers in labour-intensive manufacturing and the relatively low share of employees in service sectors there is room for switching of people into services when by further robotization jobs in manufacturing might be redundant.

Finally, the dominant narrative is by no means a global or a whole European story. On the contrary, it is designed for highly developed economies with mature industries and advanced technologies, where the employment structure is characterized by an overwhelming dominance of a service sector, where after World War II a strong middle class emerged, the welfare system has became extremely wide-ranging and society is facing the mounting problem of aging. By doing this, the dominant narrative is inherently based on a specific but widely shared assumption that today’s technological change is fundamentally different from earlier industrial revolutions when a new industry or another economic sector absorbed the labour that became available due to the use of the new technology.

In contrast to the dominant narrative, however, a rising number of studies on the current deployment of industrial robots pinpoint the economic benefits of robotization (IFR, Citation2018; OECD, Citation2017; UNCTAD, Citation2017) while they assess the labour market challenges of manageable magnitude for which policy-makers will have to develop appropriate policy responses (Craglia, Citation2018; European Commission, Citation2018). Today in the literature a new consensus is emerging that adoption of industrial robots considerably increases productivity and contributes significantly to economic growth. According to Graetz and Michaels (Citation2018), robot densification increased the annual growth of labour productivity between 1993 and 2007 by 0.36 percentage points across the 17 developed countries analysed. This is a magnitude similar to the contribution of steam engine technology to annual labour productivity growth in Britain during the first industrial revolution. The CEBR (Citation2017) report estimates that between 1993 and 2015 investment in robots contributed to almost 10% of cumulative GDP per capita growth in the majority of the OECD countries. The increase in robot density (measured as number of robots per million hours worked) by one unit was associated with a 0.04% increase in labour productivity. Dauth, Findeisen, Südekum, and Wössner (Citation2017) found that in Germany, the country with by far the highest number of industrial robots installed in Europe every additional robot per thousand workers raised the growth rate of GDP per person employed by 0.5% over the period 2004 and 2014. What is more, according to their calculation while in Germany in the last two decades each robot installed has destroyed on average two manufacturing jobs, this loss was entirely offset in the total employment by job gains outside manufacturing.

Since the deployment of industrial robots is coupled with GDP growth and improved productivity the eminent question is which countries in Europe have access to these gains? For this study, in particular, the basic question is what in Central and Eastern Europe drives and hinders the adoption of industrial robots and the diffusion of economic benefits that coupled with.

2. Data and methodology

To answer these questions this paper applies a threshold that in 2015 the robot stock in a given country musts exceed the level of 1000 robots and accordingly 18 EU member states have been analysed: Austria, Belgium, Czechia, Denmark, Finland, France, Germany, Hungary, Italy, Netherlands, Poland, Portugal, Romania, Sweden, Slovakia, Slovenia, Spain and United Kingdom. In this study, the notion of Europe refers to these countries while the term of Central and Eastern Europe includes Czechia, Hungary, Poland, Romania, Slovakia and Slovenia. For global comparison the analysis has been expanded to the U.S.A., China, Japan, Korea, furthermore to the South-East Asian countries (Indonesia, Malaysia, Philippines, Singapore, Thailand, Taiwan and Vietnam) and the category of Rest of the World (Australia, Argentina, Brazil, Canada, Hong Kong, India, Israel, Mexico, New-Zeeland, Norway, Russia, South Africa, Turkey and Switzerland)

The primary source of information is the International Federation of Robotics (IFR) that defines the industrial robot as ‘an automatically controlled, reprogrammable, multipurpose manipulator, programmable in three or more axes, which can be either fixed in place or mobile for use in industrial automation applications’ (IFR, Citation2017, p. 32). Based on annual sales data the IFR provides consolidated measures of robot stock by country and year, assuming an average service life of 12 years for an industrial robot, but some studies recalculate the IFR robot stock by using different depreciation rates (Artuc, Bastos, & Rijkers, Citation2018; Graetz & Michaels, Citation2018). Nevertheless, it is difficult to set a single depreciation rate across the IFR data as this rate could greatly vary regarding countries, industries and companies, and hence this paper is based on the robot stock as it is calculated by IFR.

The IFR offers detailed breakdown of robot stock at industry level with a handicap of a relatively high number of robots in the category of unspecified, e.g. the application of robots is unknown.Footnote1 Because in Europe the lion's share of robots is deployed in industries (86% in manufacturing, 44% in automotive industry) for which the IFR reports very accurately the breakdown at three- or two-digit level, this paper treats the unspecified robots as robots which are not belonging to manufacturing or automotive industries.

The second main information source of this study comes from EU KLEMS that provides data on employment at industry and country level in Europe (EU KLEMS, Citation2018) while the IFR uses OECD STAN and ILOSTAT data. For global comparison this paper applies in the case of employment the ILOSTAT data and in case of labour cost The Conference Board data, by contrast, the IFR studies are based on OECD STAN, ILOSTAT and other national sources in these respects. As a consequence, in this paper both for European and Non-European countries the robot density values, calculated as the number of industrial robots per 10,000 persons employed in respective industries differ from the IFR measures because of the different denominators (persons employed), though, the orders of magnitude of densities in this study are similar to the densities computed by IFR. Definitely, the data available pose clear limits to the analysis and particularly the robot density values should be interpreted carefully by looking at primarily the order of magnitude.

3. Global convergence of Central and Eastern Europe in robotization

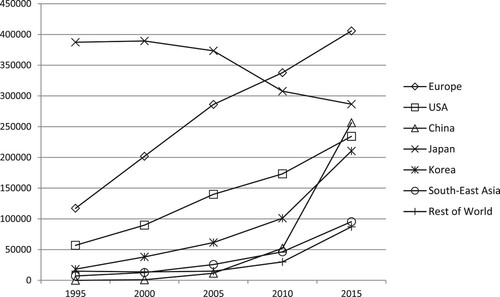

While at global level, the robot stock increased impressively between 1995 and 2015 from 600,000 to almost 1,600,000 there has been a significant reshuffling process regarding the different regions of the world economy (see ).

Figure 1. The development industrial robot stock by macro regions of the world, 1995–2015 (number of industrial robots installed). Source: author’s calculation based on data of International Federation of Robotics (Citation2017).

First, in Europe, in the U.S.A. and in Korea the steady growth of the robot stock was coupled with their persistently stable global share throughout this period and now one out of four robots is deployed in Europe (26%) and around one out of seven in the U.S.A. (15%) and in Korea (13%). Second, in Japan, in the early robotization forerunner country (which in 1995 concentrated almost two-thirds of the global robot stock) the number of robots drastically decreased and correspondingly for today its global share plummeted to 18%. Third and this is the most stunning development, the industrial robot stock skyrocketed in China in the recent years and that led to its current high global share of 16%.

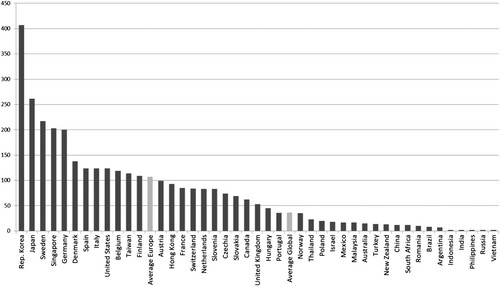

Rising robot stock and high global share, however, have not gone hand in hand with a significant convergence of robot densities in all regions (see ). First and foremost, and despite the quick rise of robot stock, in China the robot density remained extremely low (12 robots per 10,000 employees) and well below the global average (36 robots). The majority of the South-East Asian emerging economies are also lagging far behind, with exception of small countries, such as Singapore, Taiwan and Hong Kong, where robot densities are higher than the European average or close to this. By contrast, within Europe the convergence process was much faster and more pronounced, and though robot densities in all Central and Eastern European countries were below the Europe-average (107 robots per 10,000 employees), they all had significantly higher densities that the South-East Asian emerging economies (exceptions are again Singapore, Taiwan and Hong Kong).

Figure 2. Robot density in manufacturing in the world, selected countries, 2015 (global average = 36, Europe average = 107 robots per 10,000 employees in manufacturing). Source: author’s calculation based on data of International Federation of Robotics (Citation2017) for robot stock and ILOSTAT (Citation2018) for manufacturing employment.

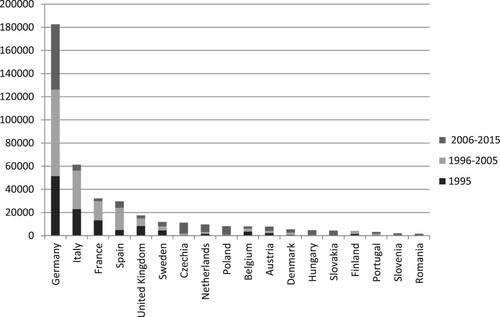

Nevertheless, the convergence with respect to robot densities within Europe over the past two decades was a result of two distinct time–space diffusion waves (see ). The first wave, between 1996 and 2005 were the years for catching-up of large economies (Italy, France and Spain) with some highly robotized industries (e.g. car manufacturing, aerospace), and to lesser extent of the other old member states. In this period their growth rate reached or even surpassed Germany's growth rate, but later their growth has become moderate. By contrast, the second wave between 2006 and 2015 were characterized by entering an entirely new group of countries in the adoption process of robots, that of the countries of Central and Eastern Europe.

Figure 3. Time-space diffusion waves in the adoption of robots in Europe, selected countries, 1995–2015 (number of industrial robots installed). Source: author’s calculation based on data of International Federation of Robotics (Citation2017).

Taking into account the classic categories of different territorial diffusion patterns, such as expansion diffusion, relocation diffusion and cascade diffusion (Cliff, Haggett, Ord, & Versey, Citation1981; Haggett, Citation1984), the adoption process of industrial robots in Europe seems to follow the expansion diffusion model. Throughout the period between 1995 and 2015 the centre, Germany, was able to keep its dominant position with a steady growth rate. Due to time, however, the deployment of robots has appeared at large scale in other countries, first in large economies with some highly developed industries, and later even in new countries, in Eastern and Central Europe, where robots were rarely to be found at the beginning of the period.

4. Economic reasoning – the driving force beyond territorial disparities in robotization

While recent studies clearly show that robotization is associated with economic growth and productivity gains, at present does not exist a coherent theoretical approach that explains the territorial differences of industrial robot deployment and the drivers and barriers beyond these differences. Nevertheless, pure economic consideration suggests that it is the falling robot prices in relation to labour costs that primarily might boost robotization. According to economic theory when the cost of a particular production factor is decreasing this factor will soon substitute other factors with higher costs; thus, due to declining prices the robots could substitute human labour with high wages. High wages could create strong incentives for companies to take capital-intensive investments in robot-based automation while availability of labour force at low wages is a disincentive to companies considering investing more in robots.

Indeed, in the past three decades, the efficiency and competence of industrial robots continuously improved and parallel to this their prices constantly decreased. Chiacchio, Petropoulos, and Pichler (Citation2018) calculate that between 1990 and 2006 robots have become around three times more efficient than those that were introduced in 1990 while their prices halved in real terms and dropped to 20% in quality adjusted. The CEBR (Citation2017) report underlines a clear downward trend development in prices and estimates that in countries with the highest robot penetration the price of industrial robots declined by 55% throughout the period of 1993 and 2015. Melrose and Tilley (Citation2017) note that in the U.S.A. over the past 30 years the price of an average industrial robot has halved in real terms while the cost of labour has almost doubled.

Due to the falling prices of robots and the increasing wages of humans the so-called robots’ payback period, the period during which the price of a robot reaches the ‘price’, i.e. the wages of the workers working two shifts who are replaced by robots, has also dramatically diminished. It is easy to concede that the impact of the payback period on robot adoption is stronger in the high-wage than the low-wage economies because the time of return from deploying robots is much shorter due to the smaller differences between the price of robots and the compensation of workers (Atkinson, Citation2018). For instance, the recently introduced FlexArc 250R welding robot system substitutes the work of three workers per shift, i.e. six in all, if we assume two shifts, and in high-wage countries, such as the U.S.A. and Germany, the payback period of this robot is less than half a year, while in countries competing by low wages it is considerably longer, two years in China and five years in Thailand (Citigroup and Oxford Martin School, Citation2016). Since high wages lead to a faster return, investment in robot-based automation is becoming more profitable. This obviously influences the adoption of industrial robots both in geographic and sectoral terms and the robots will be increasingly deployed in countries and sectors with high wages relative to robot’s prices (OECD, Citation2019; UCTAD, Citation2017).

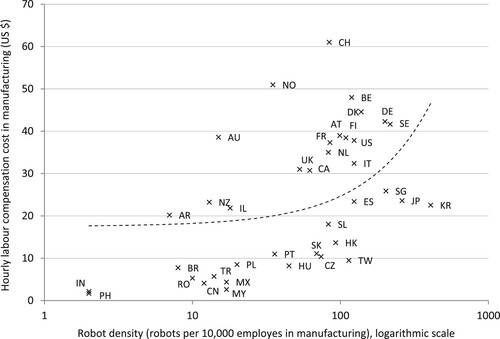

The different robot densities across the world and the European economies clearly respond to the economic assumption: high labour costs are coupled with high robot densities while low wages are accompanied with low robot densities. Although at global level, this relationship is rather moderate (Pearson's r = .3769), in 2015 the group of the top ten countries with the highest robot densities (from 119 to 407 robots per 10,000 employees) included the most developed Asian countries with hourly labour compensation costs between 22 and 26 dollars (Korea, Japan and Singapore) and the European countries with hourly labour costs above 40 dollars (Sweden, Germany, Denmark and Belgium) (see ). By contrast, in the bottom ten countries regarding robot densities (below 18 robots per 10,000 employees) the labour compensation costs were below 10 dollars per hour in manufacturing (with exception of Australia, Argentina and New Zeeland).

Figure 4. Robot density and hourly labour compensation costs in manufacturing in the world, selected countries, 2015. Source: author’s calculation based on data of International Federation of Robotics (Citation2017) for robot stock, ILOSTAT (Citation2018) for employment, The Conference Board (Citation2016) for labour cost, and ILOSTAT (Citation2019) for labour cost in Hong Kong (2015), Malaysia (2012), and Romania (2016).

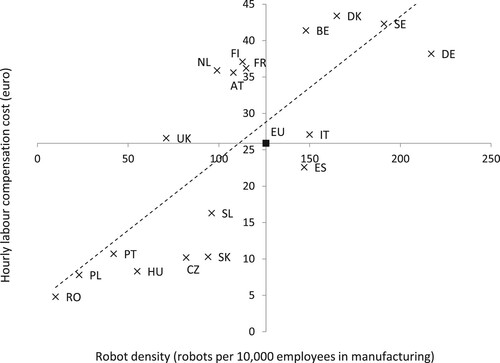

Within Europe, however, the relationship between labour costs and robot density is more straightforward (Pearson's r = .7936), as in 2015 in four of the top five countries with highest robot densities, in Germany, Sweden, Denmark and Belgium the labour cost were above 35 euros per hour (Italy is the exception), while in four of the bottom five countries, in Romania, Poland, Portugal, Hungary the labour costs were below 12 euros per hour (exception is the United Kingdom) (see ). The most striking is the West–East divide, as in almost all Central and Eastern European countries (with exception of Slovenia) the hourly labour costs with 9.6 euros on countries’ average were less than a half of the European average (25.9 euros), while robot densities in these countries (on average of 60 robots per 10,000 employees) were also less than a half of the European average (126 robots).

Figure 5. Robot density and hourly labour compensation costs in manufacturing in Europe, selected countries, 2015. Source: author’s calculation based on data of International Federation of Robotics (Citation2017) for robot stock, EU KLEMS for employment, and EUROSTAT (Citation2019) for labour cost.

Since the combination of falling robot prices and high labour compensation cost boosts robotization, the most developed European countries with high wages, mature industries and advanced innovation systems are becoming highly robotized. By contrast, the pace of industrial robot adoption is much weaker in European countries with low wages, labour-intensive industries and moderate innovation performance.

5. The role of industrial dynamics in European robotization

The differences regarding labour costs are clearly at play when it comes to robot deployment in particular European countries, though this factor alone does not sufficiently explain why we are experiencing today a stark increase of robot stock and density in European countries with low wages, particularly in Central and Eastern Europe. Hence, it is the industrial dynamics that could offer further explanations to the eminent question: What drives robotization in Central and Eastern Europe?

First, there are technological burdens that hinder a fully-fledged implementation of industrial robots in different production processes. The present-day industrial robots are used in industrial automation application for a relatively small and well-defined scope of tasks, such as assembling and disassembling, processing (e.g. cutting and grinding), dispensing (e.g. panting and spraying), material handling (e.g. picking, placing, packaging, measuring and testing) and welding and soldering (IFR, Citation2017). At current technological level, the robot-based production is not by any means fully automated; on the contrary, it needs human collaboration even in the most robotized sectors and factories. Consequently, the availability of relatively well-skilled labour at low costs remains a factor of great importance and this is exactly the point where the countries of Central and Eastern Europe could step in.

Second, for the reason that at present the relatively high prices of industrial robots and their specific and limited application possibilities greatly favour large-scale mass production, the adoption of industrial robots depends very strongly on global firms and their investment and localization decisions. At the time of this writing industrial robots were mainly deployed by global corporations and as in the European Union the latest figures show the take-up rates for robotics technologies are still very low in the SME sector. In 2018 on average only 5% of SMEs used industrial robots, while one out of five large companies (250 persons employed or more) reported the deployment of industrial robots (EUROSTAT, Citation2018). Although, a survey conducted at firm-level in 2015 indicates substantially higher utilization rates – 36% of the companies with 50–249 employees used industrial robots, compared to 74% of companies with 1,000 or more employees - the gap between the small and the large companies remains as a key feature (European Commission, Citation2015).

Large companies have significantly more financial resources than their smaller counterparts, are more experienced with the introduction of new and advanced production technologies, and – perhaps most importantly – have higher economies of scale to make the deployment of industrial robots more efficient. Therefore, the decision of global firms about how to develop and reconfigure the territorial structure of their supply chains across different economies have an immediate impact on the adoption of robots and the robot densities in the affected countries. Indeed, in Central and Eastern Europe in most of the cases robot stock development and robot densities cannot be understood without including the global value chains and the foreign direct investments in the picture.

For instance, in France the manufacturing robot stock has remained almost unchanged between 2005 and 2015 (29,700 and 28,200 robots respectively). Consequently, robot densities have also not changed significantly, in 2005 with 99 robots per 10,000 employees slightly above European average (84 robots), and in 2015 with 115 robots slightly below European average (126 robots). The only reason for the nominal increase of robot density was the fact that in this period in France the number of employees in manufacturing (the denominator of robot density) dropped from 3 million to 2.5 million.

In the meantime, however, French global companies, particularly the car manufacturers have boosted their outsourcing strategy following the globally rising trend of the industry (Sturgeon, Biesebroeck van, & Gereffi, Citation2008), first of all with nearshoring to Central and Eastern Europe (Pavlínek, Citation2018). Taking only one example, in 2017 the French car manufacturer, Renault deployed over 600 industrial robots in SloveniaFootnote2; in the country where in 2015 the manufacturing robot stock was 1800, including 960 robots in the extended automotive sector. Among other factors, this nearshoring has contributed to the increase of robot density in Slovenia, having in 2015 relatively high, although below European average robot density of 96 robots per 10,000 employees, but clearly above European average density in the extended automotive sector with 633 robots per employees.

Finally, looking at the growing robot stock in Central and Eastern Europe there is a strong effect of the European Single Market at work. Since the economic transformation from central planning into market economy in 1990, and particularly after their accession to the European Union in 2004, the Central and Eastern European countries have become fully integrated part of the European Single Market. One of the main drivers of this integration was the large-scale foreign direct investment flow into the region, partly in search for new consumer market, but to a very great degree in search of relatively well-skilled labour at low costs. During almost three decades, however, these countries were able not only to attract low value-added assembly manufacturing but also by moving up in the integration ladder they now concentrate a vast number of higher value-added suppliers and supportive activities. In some sectors, first and foremost in the automotive industry, the assembly manufacturing is now deeply embedded in the supplier clusters and the ecosystems of the different Central and Eastern European countries (Pavlínek & Ženka Citation2011). It is one of the characteristic features of agglomeration economies that regional clusters after a certain scale and critical mass could become self-sustaining and self-reinforcing systems (Fujita & Thisse, Citation2013; Glaeser, Citation2010). Similarly, the growing supplier clusters in the countries of Central and Eastern Europe could work as a driver to attract new investments into the region, among others, investments in robot-based industries.

In short, it seems that at current technological level of automation there may be a winning formula for the European global companies that are working in industries with middle or higher skills demands: deploying industrial robots for routine and highly automatable tasks and parallel to this employing human labour with low costs for the supplementary activities, preferably in regions of close geographic proximity to the main consumer markets. While in the heydays of globalization these global companies outsourced the production and the jobs that coupled with from the developed countries to the countries with large labour force reserves and cheap labour (overwhelmingly to South-East Asia), today there are the robots what they are outsourcing to the countries with low labour costs and relatively well-skilled labour force. Because the production processes are highly automated it is preferably for the European global companies to locate the robot-based manufacturing near to the Western European consumer market. Obviously, this winning formula now appears in the rising robot stock and density figures in Central and Eastern Europe.

6. Specialization versus diversification

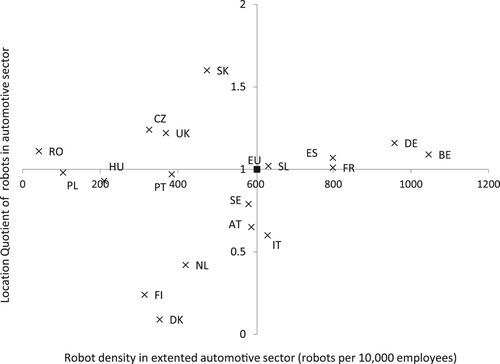

It is a unique feature of European robotization that the automotive industry plays an enormous role in deployment of industrial robots, and in 2015 almost one out of two industrial robots has been installed in the extended automotive sector.Footnote3 Since in Europe in the same year only three million workers were working in the automotive industry, this sector is characterized by an extremely high robot density of 604 robots per 10,000 employees on average. Though, the range is stunningly wide (42 robots per 10,000 employees in Romania and 1046 in Belgium) and robot densities in the extended automotive sector are in Central and Eastern Europe (with exception of Slovenia) well below the European average (see ).

Figure 6. Robot density and location quotient in extended automotive sector in Europe, selected countries, 2015. Source: author’s calculation based on data of International Federation of Robotics (Citation2017) for robot stock and EU KLEMS for employment.

Evidently, the changing geographic pattern of European car production has a strong influence on deployment of automotive robots. In European Union, the motor vehicle production was almost at the same level both in 2005 and in 2015 (18.4 and 18.3 million vehicles respectively) but during this period production in the Central and Eastern European countries doubled from 1.9 million to 3.8 million vehicles (OICA, Citation2019). As a result of three decades continuous nearshoring of European car manufacturers and investments of overseas global players, the region has become an automotive production hub with European significance (Pavlínek, Citation2018), and today one out of five European motor vehicles is produced in Central and Eastern Europe.

The sharp increase of automotive production has led in almost all Central and Eastern European countries to a strong sectoral specialization in robot adoption. To measure the extent of specialization this study calculates the Location Quotient (LQ) as the share of automotive robots in manufacturing robot stock in a given country relative to the European average in this respect. Values over 1 indicate countries’ disproportionally strong specialization in the automotive sector while values less than 1 highlight that the deployment of automotive robots plays lesser role in a given country compared to Europe as a whole.

Within Central and Eastern Europe Slovakia, Czechia, Romania and Slovenia with LQ values well above the threshold are the countries with strongest specialization in the automotive robotization, although Germany, Belgium, Spain and the United Kingdom are specializing in the automotive industry too (see ).

There are, however, significant differences. On the one hand, in the Central and Eastern European countries the robot densities in the automotive sector are despite the specialization clearly below the European average, while in Germany, Belgium and Spain, the high Location Quotients are coupled with very high robot densities. On the other hand, in Central and Eastern Europe the industrial robots are – in contrast to more sophisticated but to lesser extent automated car components and parts production – disproportionally at work in assembly, which from technological reasons is the most automatized procedure in car manufacturing, particularly in case of new state-of-the-art investments (in Slovakia, Romania and Hungary over 70% of the automotive robots are deployed in assembly while the European average is 61%).

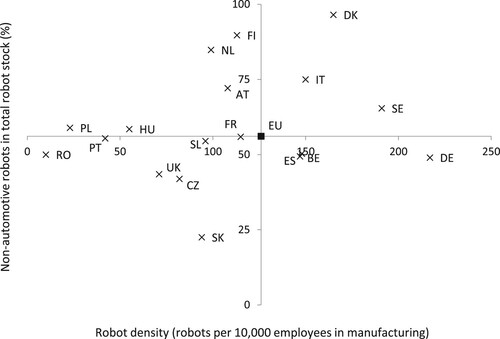

Nevertheless, the strong specialization of the Central and Eastern European countries goes against the recently emerged trend towards more diverse deployment of industrial robots in sectoral terms and the increasing deployment of industrial robots in sectors other than automotive (see ). In Europe between 2005 and 2015, the robot stock increased by 120,000 robots, but more than two-thirds of the increase was because of the rise of number of robots in non-automotive industries.Footnote4 As a result, the proportion of robots in automotive and non-automotive sectors changed too and while in Europe in 2005 the proportion of the two sectors was almost fully balanced, in 2015 the share of non-automotive sector in total robot stock increased to 56%.

Figure 7. Robot densities and non-automotive robots in total robot stock (%) in Europe, selected countries, 2015. Source: author’s calculation based on data of International Federation of Robotics (Citation2017) for robot stock and EU KLEMS for employment.

Beyond this general shift towards deployment of robots in non-automotive industries the particular groups of European countries are showing significantly different development paths (see ). In Germany the shift was coupled with a continuous rise of robot stock in both of the sectors, but because the growth rate in the non-automotive industries was more pronounced, the proportion of the two sectors has become more balanced and the share of automotive robots in total robot stock dropped from 58% in 2005 to 51% in 2015.

Table 1. The stock of industrial robots by sectors and country groups in Europe, 2005–2015 (number of industrial robots installed, rounded to 1000).

In the group of large economies with highly robotized industries, the trend change was the result of a turbulent reshuffling process, and while between 2005 and 2015, the countries’ combined robot stock in automotive sector dropped remarkably, this was largely surpassed due to increased deployment of robots in non-automotive industries. Therefore, the sectoral proportion changed too; in 2005 only one out of two in 2015 almost two out of three robots were deployed in non-automotive industries. Taking the example of France again; French car manufacturers have outsourced some parts of their production to Central and Eastern Europe, and in this way contributed to the increase of robot stock in these countries, in France, however, between 2005 and 2015 the robot stock in automotive sector decreased from almost 20,000 to around 15,000 robots. Since this drop was fully offset by the increase of robot stock in other industries, now France has more diverse sectoral distribution of robots, although the robot stock and density remained almost at the same level.

The group of other old member states is traditionally characterized by a dominance of robots in non-automotive industries and also at present we can find the highest proportions of non-automotive robots in these countries (85% in the Netherlands, 90% in Finland and 96% in Denmark). By contrast, in Central and Eastern Europe a reverse trend was observable, as between 2005 and 2015 around one out of two new European automotive robots were installed here. Therefore, Central and Eastern Europe is now the only region in Europe where the share of robots in automotive sector (53%) surpasses the share of robots in non-automotive sectors (Slovakia with 77% and Czechia with 58% have the highest values in Europe in this respect).

These regional differences between specialization and diversification are of crucial importance regarding the future development of robotization in Central and Eastern Europe. Bresnahan and Trajtenberg (Citation1995) already warned us in the mid-1990s that the innovations they described as general-purpose technologies can be applied in many ways and in many areas with far-reaching economic and social consequences, and while the classification of these key technologies may differ widely (Helpman, Citation1998; Lipsey, Carlaw, & Bekhar, Citation2005) industrial robots and Artificial Intelligence are treated as general-purpose technologies. Similarly, in the current decade, the European Commission (Citation2012) introduced the term of key enabling technologies and six technologies have been identified and garnered high policy attention, among others the advanced manufacturing technologies, such as robotization and automation.

General-purpose and key enabling technologies are common in the point that they are widely used and spread across different sectors. Therefore, in countries that are able to deploy robots in a wide sectoral scope robotization could work as general-purpose or key enabling technology. While countries that in deployment of robots are strongly specializing in a single or few industries – in some cases despite relatively high robot densities – miss the cross-fertilization effects in the economy and the additional productivity gains that coupled with.

7. Concluding remarks – robotization challenges for Central and Eastern Europe

Based on the analysis of robot deployment across the world and Europe it can be drawn three major trends that now shape robotization in Central and Eastern Europe:

− First, as the close link between high labour costs and high robot density clearly indicates there is in Europe a strong path-dependency at work. At its current stage, the robotization is deeply embedded in the path-dependent developmental differences of the particular European countries and the adoption of industrial robots seems to reflect the already existing economic and geographic disparities.

− Second, factors of industrial dynamics, such as the currently limited application possibilities of industrial robots, the localization strategies and practices of global firms and the effects of the Single Market have ignited a convergence process of the Central and Eastern European countries. This convergence is more pronounced in a global comparison, as in the majority of the Central and Eastern European countries robot densities are well above the global average.

− Third, the convergence of the Central and Eastern European countries is currently determined by the fact that robot deployment is strongly concentrated in a single sector, practically in the automotive industry, although this is in striking contrast to the development of other European countries that are now moving to a sectorally more diversified industrial robot deployment.

This special combination of drivers and barriers raises in Central and Eastern Europe the concern of a dependent robotization which appears at two levels; first is a sectoral dependence from a single industry (car manufacturing), while the second is a structural phenomenon, meaning that robotization in the region is largely relying on the localization decisions of global firms.

Looking at sectoral dependence, on the one hand, specialization obviously helps to introduce robots into manufacturing processes and to upskill employees, it helps society to adapt to robotization, and in this sense may help to further the increase of robot deployment. On other hand, whole process of robotization could become dependent on a single sector and eventual changes in this industry might block the deployment of robots in the future.

This is particularly valid for the automotive sector which – by contrast to previous decades – currently is facing very serious challenges. One big challenge is posed by the increased implementation of digital technologies in cars and car manufacturing (Dudenhöffer, Citation2016). For instance, according to Kearney (Citation2016) estimates the expected development and appearance of autonomous, driverless cars will produce a new market that could soar to U.S.D. 560 billion or 17% of the automotive industry by 2035. Moreover, McKinsey & Company (Citation2016) predicts that in terms of value added, in the driverless car, the ratio of the hardware manufactured will be reduced to 40%, while the proportion of the software and digital equipment will also reach 40%, and the remaining 20% will be covered by digital content service. In other words, when the autonomous car becomes reality the majority of content values could come from production processes that might have a different degree of automation, compared to the current production model. The other great challenge is the changing pattern of car use with the principle of ‘car as a service’ driven by platform-based business models (Parker, Alstyne van, & Choudary, Citation2016), such as ride-hailing services, car rental platforms, carpooling services and car-sharing systems, and this will also have a significant impact on the automotive market and production.

Looking at dependent robotization as a structural phenomenon it is worth noting that robotization and automation might substantially transform global value chains. The global value chains could be barraged by the latest digital technologies, such as industrial robots, 3D printing, Internet of Things, big data analysis, Artificial Intelligence and cloud computing, and their combined application in manufacturing in two ways; first is the opportunity for reducing the complexity of product and production processes, while the second way is the option to produce near the consumer market. With robots and automated machines, it is possible to produce the product parts in a more compact structure and this could drastically diminish the number of parts, components and intermediaries that are currently assembled in traditional manufacturing. Parallel with this as the complexity of products and production processes diminishes the opportunity for producing geographically closer to the consumer markets of the developed countries increases. In other words, the global value chains may become structurally less complex and geographically much shorter in the future (De Backer & Flaig, Citation2017; De Backer, Menon, Desnoyers-James, & Moussieget, Citation2016), and as a consequence, value creation within chains will be more and more detached from territories offering cheap and low-skilled labour. Evidently, this could also have an influence on robotization in Central and Eastern Europe, as long as one of the risks of the dependent robotization is that robotized factories might make possible the reshoring of previously outsourced production processes.

Although longitudinal studies are sparely available, it is a warning sign that this process has already been started in Europe and the gap between the offshoring and backshoring companies seems to be closing (Di Mauro, Fratocchi, Orzes, & Sartor, Citation2018; Kinkel, Citation2014). For instance, in Germany at present, there is one backshoring company for every third offshoring company (Kinkel, Citation2019). According to Dachs, Kinkel, Jäger, and Palčič (Citation2019) in 2015 on average around 12% of the European companies analysed offshored their activities, while more than 4% of the companies have moved production back to their home country. It is likely that in the future labour-intensive production activities with low skills demand might continuously be offshored, among others to Central and Eastern European countries, while complex and robotized production processes comprising capital-, skills- and R&D-intensive activities could be increasingly reshored into the most developed European countries.

When robotization appeared with a considerable delay of almost two decades in Central and Eastern Europe the economies of these countries were characterized by a relatively well-skilled labour force with low costs and a large labour-intensive manufacturing, and hence robotization is now extreme strongly concentrated in few skill-intensive industries, particularly in automotive sector. It was then the industrial dynamics that sparked a quick convergence process in the past decade, and this convergence is now also appearing in the rising robot stock and density figures. In the future, however, it remains as one of the main industrial policy challenges for Central and Eastern Europe to avoid the trap of dependent robotization.

Disclaimer

The views expressed are purely those of the author and may not in any circumstances be regarded as stating an official position of the European Commission.

Acknowledgements

The author wishes to thank Enrique Fernández-Macías and Cesira Urzi Brancati for their helpful remarks, the anonymous reviewers for their very valuable suggestions in finalizing the manuscript, and Alexander Tübke and Pietro Moncada-Paternò-Castello and his colleagues in IRI Team at JRC Unit B.3. Seville, for fostering his interest in the subject that led to this paper.

Disclosure statement

No potential conflict of interest was reported by the author.

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes

1 In Europe, the proportions of robots belonging to category ‘unspecified’ have fluctuated between 8% and 18% of the total robot stock for the period of 1995 and 2015.

2 Revoz is one of the biggest Slovenian companies and the only car manufacturer in the country which produces Renault models in their robotised plants (https://revoz.si/en/).

3 Because of the different industry classifications of the IFR and the EU KLEMS this study uses the term extended automotive sector for calculating the robot densities in this field and the robot stock refers to IFR categories automotive industry and other vehicles, while the employment corresponds to EU KLEMS category transport equipment.

4 The analysis is based on the IFR robot stock and the term non-automotive sector comprises all industries (including robots in the category ‘unspecified’) except the automotive industry.

Related Research Data

References

- Acemoglu, D., & Autor, D. H. (2010). Skills, tasks and technologies: Implications for employment and earnings. NBER working paper 16082, national Bureau of economic research. Cambridge: Mass.

- Acemoglu, D., & Restrepo, P. (2017). Robots and jobs: Evidence from US labor markets. NBER working paper 23285, national bureau of economic research. Cambridge: Mass.

- Arntz, M., Gregorie, T., & Zierahn, U. (2016). The risk of automation for jobs in the OECD countries: A comparative analysis. OECD Social, Employment and Migration Working Papers 189, OECD Publishing, Paris.

- Artuc, E., Bastos, P., & Rijkers, B. (2018). Robots, tasks and trade. Policy Research Working Paper Series 8674, The World Bank.

- Atkinson, R. D. (2018, November). Which nations really lead in industrial robot adoption? Information Technology & Innovation Foundation. Retrieved from https://ssrn.com/abstract=3324659

- Autor, D. H., & Dorn, D. (2013). The growth of low-skill service jobs and the polarization of the US labor market. American Economic Review, 103(5), 1553–1597. doi: https://doi.org/10.1257/aer.103.5.1553

- Autor, D. H., Levy, F., & Murnane, J. R. (2003). The skill content of recent technological change: An empirical exploration. Quarterly Journal of Economics, 118(4), 1279–1333. doi: https://doi.org/10.1162/003355303322552801

- Baldwin, R. (2019). The Globotics upheaval: Globalisation, robotics and the future of work. London: Weidenfeld and Nicholson.

- Bresnahan, F. T., & Trajtenberg, M. (1995). General purpose technologies: Engines of growth? Journal of Econometrics, 65(1), 83–108. doi: https://doi.org/10.1016/0304-4076(94)01598-T

- Brynjolfsson, E., & McAfee, A. (2014). The second machine age. Work, progress, and prosperity in a time of Brilliant technologies. New York: W. W. Norton and Company, Inc.

- CEBR (Centre for Economics and Business Research). (2017). The impact of automation: A report for Redwood. January, London.

- Chiacchio, F., Petropoulos, G., & Pichler, D. (2018). The impact of industrial robots on EU employment and wages: A local labour market approach. Working Paper 2, Bruegel, Brussels.

- Chui, M., Manyika, J., & Miremadi, M. (2015). Four fundamentals of workplace automation. McKinsey Quarterly, November.

- Citigroup and Oxford Martin School. (2016). Technology at work v2.0: The future is not what it used to be. Citi GPS: Global Perspectives & Solutions, January.

- Cliff, A. D., Haggett, P., Ord, J. K., & Versey, G. R. (1981). Spatial diffusion: An historical geography of epidemics in an Island community. Cambridge: Cambridge University Press.

- Cowen, T. (2014). Average is over: Powering America beyond the age of the great stagnation. New York, NY: Dutton (Penguin Group).

- Craglia, M. (Ed.). (2018). Artificial intelligence – a European perspective. European Commission, Joint Research Centre, EUR 29425 EN, Publication Office, Luxemburg. Retrieved from http://publications.jrc.ec.europa.eu/repository/bitstream/JRC113826/ai-flagship-report-online.pdf

- Dachs, B., Kinkel, S., Jäger, A., & Palčič, I. (2019). Backshoring of production activities in European manufacturing. Journal of Purchasing and Supply Management, 25(3). doi:https://doi.org/10.1016/j.pursup.2019.02.003

- Dauth, W., Findeisen, S., Südekum, J., & Wössner, N. (2017). German robots – the impact of industrial robots on workers. IAB Discussion Paper, No. 30, Institute for Employment Research, Nuremberg.

- De Backer, K., & Flaig, D. (2017). The future of global value chains: Business as usual or “a new normal”? OECD Science, Technology and Industry Policy Papers, No. 41, OECD Publishing, Paris. Retrieved from https://doi.org/https://doi.org/10.1787/23074957

- De Backer, K., Menon, C., Desnoyers-James, I., & Moussieget, L. (2016). Reshoring: myth or reality? OECD Science, Technology and Industry Policy Papers, No. 27, OECD Publishing, Paris. Retrieved from https://doi.org/https://doi.org/10.1787/5jm56frbm38s-en

- Di Mauro, C., Fratocchi, L., Orzes, G., & Sartor, M. (2018). Offshoring and backshoring: A multiple case study analysis. Journal of Purchasing and Supply Management, 24(2), 108–134. doi:https://doi.org/10.1016/j.pursup.2017.07.003

- Dudenhöffer, F. (2016). Wer kriegt die Kurve? Zeitenwende in der Autoindustrie. Frankfurt am Main: Campus Verlag.

- EU KLEMS. (2018). Growth and productivity accounts: Statistical module, ESA 2010 and ISIC Rev. 4 industry classification (September 2017 release, Revised July 2018). Retrieved from http://www.euklems.net/

- European Commission. (2012). A European strategy for key enabling technologies – a bridge to growth and jobs. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions, Brussels, 26.6.2012, COM(2012) 341 final. Retrieved from https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2012:0341:FIN:EN:PDF

- European Commission. (2015). Analysis of the impact of robotic systems on employment in the European Union. 2012 update. A study prepared for the European Commission, DG Communications Networks, Content & Technology by Fraunhofer Institute for System and Innovation Research, ISI, Karslruhe, (Jäger, A., Moll, C., Som, O. and Zanker, C.), Publications Office of the European Union, Luxembourg.

- European Commission. (2018). Employment and social developments in Europe. Annual review 2018. Directorate-General for Employment, Social Affairs and Inclusion, Publications Office of the European Union, Luxembourg. Retrieved from https://ec.europa.eu/social/BlobServlet?docId=19719&langId=en

- EUROSTAT. (2018). 3D printing and robotics, [isoc_eb_p3d], last update 13.05.2019.

- EUROSTAT. (2019). Labour cost levels by NACE Rev. 2 activity, [lc_lci_lev], last update: 13-05-2019. Labour cost for LCI (compensation of employees plus taxes minus subsidies) in manufacturing. Retrieved from http://appsso.eurostat.ec.europa.eu/nui/submitViewTableAction.do

- Frey, C. B. (2019). The technology trap: Capital, labor, and power in the age of automation. Princeton, NJ: Princeton University Press.

- Frey, C. B., Berger, T., & Chen, C. (2018). Political machinery: Did robots swing the 2016 US presidential election? Oxford Review of Economic Policy, 34(3), 418–442. doi: https://doi.org/10.1093/oxrep/gry007

- Frey, C. B., & Osborne, M. (2013). The future of employment: how susceptible are jobs to computerisation? Oxford Martin School Working Paper, Oxford.

- Fujita, M., & Thisse, J.-F. (2013). Economics of agglomeration. Cities, industrial location, and regional growth. Cambridge, MA: Cambridge University Press.

- Glaeser, E. L. (Ed.). (2010). Agglomeration economics. Chicago: The University of Chicago Press.

- Goos, M., Manning, A., & Salomons, A. (2009). Job polarization in Europe. American Economic Review, 99(2), 58–63. doi: https://doi.org/10.1257/aer.99.2.58

- Graetz, G., & Michaels, G. (2018). Robots at work. The Review of Economics and Statistics, 100(5), 753–768. doi: https://doi.org/10.1162/rest_a_00754

- Haggett, P. (1984). Geography: A modern synthesis. London: Longman Higher Education.

- Helpman, E. (Ed.). (1998). General purpose technologies and economic growth. Cambridge, MA: MIT Press.

- IFR (International Federation of Robotics). (2017). World robotics 2017. Industrial robots. International Federation of Robotics, Frankfurt am Main. Retrieved from http://www.worldrobotics.org

- IFR (International Federation of Robotics). (2018). The impact of robots on productivity, employment and jobs. Positioning Paper, International Federation of Robotics, Frankfurt am Main.

- ILOSTAT. (2018). Employment by sector – ILO modelled estimates, November 2018, Last update on 28OCT19. Retrieved from https://www.ilo.org/ilostat/faces/oracle/webcenter/portalapp/pagehierarchy/Page3.jspx?locale=EN&MBI_ID=33

- ILOSTAT. (2019). Labour costs. Last update on 30SEP19. Retrieved from https://www.ilo.org/ilostat/faces/oracle/webcenter/portalapp/pagehierarchy/Page3.jspx?locale=EN&MBI_ID=443

- Kearney, A. T. (2016). How automakers can survive the self-driving era. ATKearney, August. Retrieved from https://www.atkearney.es/automotive/article?/a/how-automakers-can-survive-the-self-driving-era

- Kinkel, S. (2014). Future and impact of backshoring – some conclusions from 15 years of research on German practices. Journal of Purchasing and Supply Management, 20(1), 63–65. doi: https://doi.org/10.1016/j.pursup.2014.01.005

- Kinkel, S. (2019). Zusammenhang von Industrie 4.0 und Rückverlagerungen ausländischer Produktionsaktivitäten nach Deutschland. FGW-Publikation Digitalisierung von Arbeit 20, Forschungsinstitut für gesellschaftliche Weiterentwicklung, Düsseldorf. Retrieved from https://www.fgw-nrw.de/fileadmin/user_upload/FGW-Studie-I40-20-Kinkel-2019_05_08-komplett-web.pdf

- Levy, F., & Murnane, J. R. (2004). The new division of labor: How computers are creating the next job market. Princeton, NJ: Princeton University Press.

- Lipsey, R., Carlaw, K. I., & Bekhar, C. T. (2005). Economic transformations: General purpose technologies and long-term economic growth. Oxford: Oxford University Press.

- Lordan, G. (2018). Robots at work. A report on automatable and non-automatable employment shares in Europe. Directorate-General for Employment, Social Affairs and Inclusion, European Commission. Retrieved from https://ec.europa.eu/social/main.jsp?catId=738&langId=en&pubId=8104&furtherPubs=yes

- McKinsey & Company. (2016, January). Automotive revolution – perspective towards 2030. How the convergence of disruptive technology-driven trends could transform the auto industry. McKinsey, Advanced Industries. January. Retrieved from https://www.mckinsey.com/~/media/mckinsey/industries/high%20tech/our%20insights/disruptive%20trends%20that%20will%20transform%20the%20auto%20industry/auto%202030%20report%20jan%202016.ashx

- Melrose, C., & Tilley, J. (2017). Automation, robotics, and the factory of the future. In: The great re-make: Manufacturing for modern times, Manufacturing, McKinsey & Company, 67–72. Retrieved from https://www.mckinsey.com/business-functions/operations/our-insights/automation-robotics-and-the-factory-of-the-future

- Nedelkoska, L., & Quintini, G. (2018). Automation, Skills Use and Training. OECD Social, Employment and Migration Working Papers 202, OECD Publishing, Paris.

- OECD. (2016). Enabling the Next Production Revolution: The Future of Manufacturing and Services – Interim Report. Meeting of the OECD Council at Ministerial Level, June 1–2, OECD, Paris.

- OECD. (2017). The next production revolution: Implications for governments and business. Paris: OECD Publishing.

- OECD. (2019). Determinants and impact of automation: An analysis of robots’ adoption in OECD countries. OECD Digital Economy Papers 277, OECD Publishing, Paris. Retrieved from https://doi.org/https://doi.org/10.1787/ef425cb0-en

- OICA (Organisation Internationale des Constructeurs d’Automobile). (2019). World Motor Vehicle Production by Country and Type, 1999–2018. Paris, OICA. Retrieved from http://www.oica.net/production-statistics/, accessed 24. 06. 2019

- Parker, G. G., Alstyne van, M. W., & Choudary, P. S. (2016). Platform revolution: How networked markets are transforming the economy – and how to make them work for you. New York, NY: W. W. Horton and Company.

- Pavlínek, P. (2018). Global production networks, foreign direct investment, and supplier linkages in the integrated peripheries of the automotive industry. Economic Geography, 94(2), 141–165. doi: https://doi.org/10.1080/00130095.2017.1393313

- Pavlínek, P., & Ženka, J. (2011). Upgrading in the automotive industry: Firm-level evidence from Central Europe. Journal of Economic Geography, 11(3), 559–586. doi: https://doi.org/10.1093/jeg/lbq023

- Sebastian, R., & Biagi, F. (2018). The routine biased technical change hypothesis: A critical review. JRC Technical Reports, European Commission, Luxembourg.

- Shiller, R. J. (2019). Narrative economics: How stories go viral and drive major economic events. Princeton, NJ: Princeton University Press.

- Sturgeon, T., Biesebroeck van, J., & Gereffi, G. (2008). Value chains, networks and clusters: Reframing the global automotive industry. Journal of Economic Geography, 8(3), 297–321. doi: https://doi.org/10.1093/jeg/lbn007

- Temin, P. (2017). The vanishing middle class: Prejudice and power in a dual economy. Cambridge, MA: MIT Press.

- The Conference Board. (2016). International Labor Comparisons, Table 1: Hourly compensation costs in manufacturing, in US dollars and as a percent of costs in the United States (US=100). Retrieved from https://www.conference-board.org/ilcprogram/index.cfm?id=38269#Table1

- UNCTAD. (2017). Trade and Development Report 2017. Beyond Austerity: Towards a Global New Deal. Chapter III (Robots, Industrialization and Inclusive Growth), United Nations, New York and Geneva.

- WEF (World Economic Forum). (2018). The Future of Jobs Report 2018. Centre for the New Economy and Society, World Economic Forum, Geneva. Retrieved from http://www3.weforum.org/docs/WEF_Future_of_Jobs_2018.pdf