ABSTRACT

Financial access is considered a crucial element of entrepreneurship. Much of the literature focuses on how individual actors demand or supply finance, but rarely within the context of systemic entrepreneurship. The current entrepreneurial finance literature is fragmented and rooted in various traditions. However, the entrepreneur’s perceived role in aggregated wealth creation is currently being strengthened, most recently by the emerging entrepreneurial ecosystem perspective. This calls for exploring the role of finance in systemic entrepreneurship and entrepreneurial ecosystems. By conducting a systematic literature review of financial determinants, sources and effects, the study synthesizes debates across the different research fields, i.e. finance, entrepreneurship and regional development. As the entrepreneurial ecosystem concept is considered a pre-paradigmatic approach, the paper argues that the role of finance depends on how we regard and define ecosystems. The state of knowledge is also underdeveloped due to the obstacles of acquiring longitudinal data. Such issues keep us from achieving a better evolutionary and processual understanding of the financial dynamics in ecosystems and, therefore, presents a promising avenue for future research.

1. Introduction

Financial access is a critical asset in contemporary firm formation, innovation and entrepreneurial performance in general (Cassar Citation2004; Cumming and Groh Citation2018; Kerr and Nanda Citation2015). Yet, on the systemic level, within the emerging entrepreneurial ecosystem framework, the financial mechanisms are yet to be understood (Frimanslund and Nath Citation2022). The current literature review describes how finance is a crucial element of entrepreneurship and its role in explaining systemic entrepreneurial development. The literature review builds upon two strands of research. The first derives from a series of publications from the field of entrepreneurial finance, while the second pertains to current knowledge about finance in systemic entrepreneurship and, more specifically, entrepreneurial ecosystems. Together, the two research avenues serve as a sound basis for investigating the financial aspects of ecosystems.

On an aggregate level, financial access that helps entrepreneurs perform and succeed, create jobs and increase economic activity (see Armington and Acs Citation2002; Benneworth Citation2004; Cross Citation1981; Fritsch and Mueller Citation2004; Leendertse, Schrijvers, and Stam Citation2021, to name but a few). However, and despite the elevated status of financial access, there is limited knowledge on early-stage financing, which is considered more complex than corporate financing (Nofsinger and Wang Citation2011). This complexity arises from the inherent informational asymmetries that characterize innovative and uncertain start-up projects without track records. The extant literature on entrepreneurial finance originates mainly from the domain of corporate finance (Landström Citation2017, 5). Here, the perspectives and methods mostly adhere to positivistic and quantitative traditions that are limited to testing causal relations between measures such as determinants, financial sources and performance. The traditional methods of science is regressing isolates (Wurth, Stam, and Spigel Citation2021), which, in isolation, may not be suitable to understand the evolutionary and systemic dynamics of entrepreneurial ecosystems. That is why this literature review will attempt to explore lessons in existing literature regarding entrepreneurial finance and place those lessons within the context of ecosystems.

Performance in this context is normally referred to as the performance of the individual firms (e.g. sales, employees, financing, profitability or dividends) and aggregated measures of entrepreneurs as a group (e.g. taxes or employment rates). In the following, the term aggregated refers to data, measures or perspectives that include a sum of something. Such measures are often used at regional or national levels or research or policy where micro-level data about individual firms are less critical.

A next assertion is the disproportionate position of systemic entrepreneurship in the literature compared to its importance. The role of finance in entrepreneurship has to a certain extent been explored in fields such as regional development and economic geography, but its role in such well-known areas as regional innovation systems has been overlooked (Gjelsvik and Trippl Citation2018). It is noted that this role has recently been made more explicit within the emerging entrepreneurial ecosystem perspective (Acs et al. Citation2017; Bonini and Capizzi Citation2019; Isenberg Citation2011). In the latter, the ecosystem enhances access to some ‘ecosystem resources’ in general, including finance (Spigel Citation2017). The same branch theorizes that human and financial capital are recycled within business networks (Spigel and Harrison Citation2018). Still, a recent literature review on entrepreneurial ecosystems revealed no mentioning of finance whatsoever (Kang et al. Citation2021). Instead, they find that the highest frequency of keywords relates to innovation, entrepreneurship, performance, firm, knowledge, policy, industry, university and network – despite a paradoxical stronghold within the discipline of economics.

Therefore, the starting point is a situation in which finance is more or less absent from the literature. The lack of literature makes highly systematic and popular approaches to conducting a literature review futile. Hence, the method of this paper relies on looking for lessons and insight from previous streams of literature that can be brought into the debate on entrepreneurial ecosystems. This is useful as new theoretical advancements in entrepreneurial finance and in general (such as entrepreneurial ecosystems) should build on previous knowledge (Landström Citation2017).

Even when looking into the predecessors of the ecosystem approach, the financial dimension rarely takes a dominant position. An early example is the entrepreneurial system of Spilling (Citation1996), which contains a process labelled the economic cycle where financing entrepreneurial growth happens in the wake of a mega-event. If one uses this principle in other contexts, it may require individuals with the right idea, at the right place and at the right time that may spur such growth. Following Spilling, the phenomenon will be more difficult to predict and stimulate from birth but easier to follow up on and enhance through stimulation and policy. A second example is the conceptualization of an ecosystem triangle in the Silicon Valley system, where venture capital (VC) has been defined as one of three main pillars (Zacharakis, Shepherd, and Coombs Citation2003). Further interests in understanding entrepreneurship practices within the context of regional development lead to the development of entrepreneurial regional innovation systems (ERIS) (Cooke and Leydesdorff Citation2006; Farinha, Ferreira, and Ratten Citation2018). There seems to be little mention of finance within this industry, although there are notable examples of how early-stage finance contributes to R&D partnerships within national innovation systems (Lee and Park Citation2006).

Based on these two acknowledgements (i.e. (1) financial access is a crucial element of successful entrepreneurship and (2) the role of finance is underdeveloped in the field of systemic entrepreneurial development) the objective of the paper is to gain an overview of the current knowledge in the context of systemic entrepreneurship and recommend a path for future research. Therefore, the quest can be defined by the following research question: What do we know about financial access for entrepreneurial ecosystems and systemic entrepreneurship?

After the introduction, section two contains the review protocol where the literature search procedures are explained. In the two next sections, the results sum up the key issues and knowledge provided by the search. For simplicity, the results are divided between (1) the main lessons from entrepreneurial finance, and (2) the main lessons from the literature on entrepreneurial ecosystem. Section five discusses the link between these issues before a conclusion is provided in section six.

2. Review protocol

As mentioned above, the starting point is a situation in which the literature is largely absent. Therefore, the method is to explore the extant finance and entrepreneurship literature to look for lessons that can be brought into the arena of finance in the entrepreneurial ecosystem. The paper applies the structured literature review methodology advised by Fink (Citation2013) and Kraus, Breier, and Dasí-Rodríguez (Citation2020) and start by establishing inclusion and exclusion criteria for the literature search. These criteria are summed up in below.

Table 1. Selection criteria for literature search.

contains a list of the search words that were employed to search for specific concepts and relations. Boolean operators allowed for combining searches for broader results. The search terms were matched against those applied in related literature reviews, both older and more recent (see e.g. Claire, Lefebvre, and Ronteau Citation2019; Doloreux and Gomez Citation2017; Kang et al. Citation2021; Pato and Teixeira Citation2016; Titman and Wessels Citation1988). Newer articles were prioritized, although older influential and frequently cited works were also included. The first search did not address scientific quality other than adherence to methodological norms, practices and listing to obtain a general and better overview. However, only peer-reviewed publications accepted and appearing in scientific journals were included in the final literature matrices attached to this paper. The exceptions were a few studies from the World Bank that were considered appropriate due to their relevance. The databases and search engines used were Scopus and Business Source Elite for the keyword-based searches and Google Scholar for snowballing and tracking references.

Table 2. Selected search words.

The first step of the search process was designing strings of keywords covering the relevant sources of entrepreneurial finance to investigate the relations among the conceptual elements. The initial selection filter was therefore studies related to ‘entrepreneurs’ and ‘startups’. The large body of research on SMEs also provided relevant results in many cases. For the determinants of capital access and firm performance, the string ‘“venture capital” OR “business angel” OR “business angels” OR “investor” OR “bootstrapping” OR “grants” OR “governmental capital” OR “grants” OR “capital” OR “crowdfunding” OR “bank” OR “loan” OR “credit”’ was applied with a few variations. Next, two parallel searches were performed in Scopus and Business Source Elite with the Boolean operators ‘AND “determinants” AND “firm performance”’. ‘Determinants’ obtained 16.973/15.731 results in Business Source Elite and Scopus, respectively, while firm performance obtained 7.290/9.154 results. ‘Firm performance’ includes a wide range of measurements, such as dividends, sales, full-time equivalents (FTEs), profits, and exit performance, but the inclusion of such keywords proved to complicate the search process, and extensive initial results called for measures to narrow the search.

Concerning the reliability of the screening method, intra-rater reliability was achieved as the participation of the main author was consistent throughout the complete literature search, and inter-rater reliability was achieved in that the literature matrices was examined by the team of authors (Fink Citation2013, 116). To avoid selection bias, the selection include all financial sources that emerge from the general literature on entrepreneurial finance. All sources are with within life cycle theory of entrepreneurial finance. By including alternative finance, the selection also includes newer forms.

For the research question, using such screening methods resulted in a wide body of literature where the majority was uninteresting or only vaguely relevant from the current literature review standpoint. To distinguish the relevant research, a ‘qualitative’ process of extracting the most relevant papers and reports was conducted by tracking the references of key papers. Therefore, the literature review was not a one-time search operation but rather a back-and-forth process, where new strands of research across different fields were continuously examined. After a careful screening process by the authors, the result was 135 representative studies in addition to a few selected reports. However, it was decided to only include peer-reviewed studies in acknowledged journals (such as the ABS list or with similar status) that specifically and concisely addressed the research problems of this review. This way, predatory journals or less serious outlets were avoided. Therefore, the attached literature matrix now contains 70 representative search results.

As this review set out to identify studies that explicitly examined determinants and outputs of entrepreneurial finance, the most frequent outlets did not necessarily match other and more general reviews, such as the extensive work of Cumming and Johan (Citation2017). By carefully boiling down the data to only the papers that clearly and directly provided relevance to the research questions, the selection avoided being influenced by what Cumming and Johan (Citation2017) referred to as the highly fragmented fields or ‘silos’ of literature on entrepreneurial finance.

Once retrieved, the literature was indexed and classified by (1) name, (2) author, (3) dependent variable, (4) independent variables, (5) effect, (6) direction, (7) context of the selected study, (8) theoretical background, (9) type of study, (10) analytical method, (11) publishing journal/outlet and (12) comments and other main findings. The selected literature on the firm-level determinants of financial access is summarized in Appendix 1, and that on the aggregate-level determinants is summarized in Appendix 2.

3. Main lessons from entrepreneurial finance

3.1. Common contexts

Regarding the common research contexts, the literature on financial sources is often centred around Western economies (see also Bonini and Capizzi Citation2019; Cao Citation2018; Kang et al. Citation2021). Much of the literature on entrepreneurial finance examines the equity-based US/UK contexts. Here, VC has a central position, while other accounts in other economies mention such capital as being unavailable (Gjelsvik and Trippl Citation2018). As a result of this unavailability, the field of entrepreneurial finance, despite its increased attention in the last couple of decades, has yet to fully employ a theoretical foundation regarding credit- and subsidy-based as well as emerging economies.

Context does not necessarily matter as much in financial research, as the positivistic traditions of entrepreneurial research tend to focus on universal patterns of financial phenomena (Ucbasaran, Westhead, and Wright Citation2001). In contrast, research relevant to entrepreneurial finance that stretches into the fields of economic geography and regional development tend to assume contextual differences (Steyaert and Katz Citation2004). Contextual approaches therefore warrant different methodological approaches, which may be a reason one sees, for example, case studies in regional development more frequently than in finance.

A critique of the contextual bases of financial studies is that the respondents to surveys tend to be rewardees or investees of specific programmes or funds. This might cause biased results. Researchers may benefit from applying network analyses in order to learn more about these dynamics.

3.2. Common determinants to financial access

First of all, the determinants of financial access can be categorized into three main groups: (1) micro-level, (2) macro-level and (3) geographical determinants. Among micro-level determinants, the following two additional lines of inquiry can be identified: the impact of firm characteristics and innovativeness and the age and maturity of the start-up. Macro-level determinants are dominated by studies on the impact of market entry regulations, financial crises and the roles and effects of governmental venture capital (GVC) programmes for entrepreneurship. Finally, among geographical determinants, the debate mainly focuses on urban vs. rural financial market structures or variations in such a distinction or university-centred entrepreneurship. Please note that innovation can serve as both a determinant and performance measure, and the following should therefore be read in the context of the overarching topic.

3.2.1. Micro-level factors

This group of considerations among business-level determinants pertains to firm characteristics and innovativeness (see e.g. Brown, Martinsson, and Petersen Citation2012). The rationale for innovativeness as a determinant is that innovation often is equal to growth-orientation among start-ups The pecking order framework (POF) and agency theory predict that access to finance is reduced when there is a lack of track records and a high degree of asymmetric information. Such characteristics are typical of most innovative start-ups and R&D activities and are frequently identified in the literature, at both the micro and macro levels. Among many examples, Demirel and Parris (Citation2015) explored how innovative activities and applicable and non-applicable R&D affected bank loans, VC and GVC. On the one hand, the results showed that even low-risk R&D projects resulted in a lower likelihood of obtaining bank loans. On the other hand, VC filled the finance gap to a marginal degree. A basic assumption in the field of entrepreneurial finance is, unsurprisingly, that innovativeness is negatively associated with ease of financial access.

Another relevant group of micro-level determinants relates to the firm’s track record, such as age and maturity. The influence of VC investments on firm performance in 36,567 firms across 76 studies was analysed in an extensive review by Rosenbusch, Brinckmann, and Müller (Citation2013), which found that a start-up’s age and maturity are critical to its acquisition of VC.

3.2.2. Macro-level factors

Market entry regulations have received considerable research and policy attention due to their alleged role in new firm formation and entrepreneurship (see, e.g. GEM Citation2016). In general, market entry regulations are seen as enhancers of firm establishment and growth. However, context matters. For instance, some studies show no difference in start-up rates due to different barriers to entry, such as minimum financial capital requirements, labour market regulations and the administrative costs of starting a business (see e.g. Van Stel, Storey, and Thurik Citation2007). Lower barriers to entry are also found to benefit only marginal firms with lower survival rates (Branstetter et al. Citation2014).

Another notable strand of the literature discusses how crises affect access to finance. Substantial evidence shows that both the dotcom crisis in 2002 and the mortgage crisis in 2008 immediately reduced access to private capital for startups. Berger and Udell (Citation1998) and Lee, Sameen, and Cowling (Citation2015) argue that there is a financial gap among innovative firms that is exacerbated during financial crises. On the one hand, a financial crisis is thought to affect investors’ risk assessment and access to financial capital for innovative firms as they seek ‘financial safe havens’ or mature and more solid industries. Due to cyclical effects, this will also impact non-innovative firms (Ferrando, Popov, and Udell Citation2017). On the other hand, governmental capital is found to increase in the aftermath of financial crises due to attempts to compensate for the emerged market failures (Mason and Pierrakis Citation2013).

The final group of macro level considerations pertains to studies on the role of GVC in entrepreneurship. GVC is examined in this section due to its ability to facilitate and stimulate private investments. For instance, among frequent examples, Toole and Turvey (Citation2009) showed that entry into the governmental Small Business Innovation Research (SBIR) programme increased the likelihood of follow-up investments in the US. Leleux and Surlemont (Citation2003) found evidence that the presence of GVC programmes increases not only the total amount of venture capital in the market but also the size of the VC industry as a whole.

3.2.3. Geographical determinants

For the context of this study, this category entails mainly the distance to financial milieus. Asymmetric information predicts that the distance to the start-up will negatively affect the investor’s likelihood of investing. GVC has the potential to address this issue in general (see, e.g. Leleux and Surlemont Citation2003; Toole and Turvey Citation2009). Distance to the investee may negatively affect the possibility of VC-stage financing (Avdeitchikova Citation2008; Landström Citation1993; Tian Citation2011), in accordance with theoretical predictions. Labelled the home bias, both US and Australian investors show an increased preference for investing close to home and for locally-headquartered firms (Coval and Moskowitz Citation1999, Citation2001; Guenther, Johan, and Schweizer Citation2018). Therefore, access to finance is considerably better in places close to financial milieus. As mentioned above, innovative activities induce a high rate outcome due to uncertainty and therefore often disqualify start-ups from acquiring bank loans (Demirel and Parris Citation2015) but are less disadvantageous for large firms that can rely on internal finances (Beck, Demirguc-Kunt, and Maksimovic Citation2008).

It follows that distance to investor and home bias are dependent on geographic and demographic distributions among other things, so one should be careful not to generalize or make overly bold statements about differences across regions or countries.

3.3. Common effects of financial sources

This section presents the results of the search on the finance-related firm/venture performance of each group of financial sources. Financial performance is a well-studied phenomenon in the financial literature (see e.g. Bititci et al. Citation2018; Neely Citation1999). The search results on entrepreneurial performance are summarized in Appendix 3. This section reports on the patterns of findings on the most identified sources of entrepreneurial finance.

3.3.1. Governmental capital

Governmental venture capital shows varying effects, which are likely caused by design and/or context. Governmental capital normally comprises equity investments that often match VC/BAs, but also includes grant programmes, loans and guarantees. Especially in subsidy-based capital structures, the first step on the growth path for many start-ups is receiving a grant from governmental or public support agencies (PSAs). Grants often provide the entrepreneur with time to acquire a proof concept and a position for higher valuation when seeking to obtain external financing in the next step. Searches of governmental grants indicate that programme design may influence outcome. For instance, governmental subsidy support has been found to positively affect innovative activities (Almus and Czarnitzki Citation2003). A notable US-based study found an increase in small business growth from governmental Community Reinvestment Act (CRA) loans (Rupasingha and Wang Citation2017). In contrast, business start-up awardees in Germany were smaller, generated higher losses, and yielded lower returns on financial capital than science-based entrepreneurial firms with comparable characteristics in the first five years after their establishment (Ayoub, Gottschalk, & Müller, Citation2016).

Such issues must also be taken into account when examining the more extensive body of literature on GVC (matching capital), as it tends to evaluate the effects of specific programmes. Although such programmes depend on context, policy and maybe even non-economic objectives, it should still be elaborated. Notable examples of research on GVC are Cumming and Johan (Citation2016), who found that GVC-backed firms had worse exit performance by investees than both independent VC and mixed patterns in the US, and Brander, Du, and Hellmann (Citation2015), who found contradicting positive effects in an Asian sample. GVC may still increase the total invested amount (Brander, Du, and Hellmann Citation2015; Leleux and Surlemont Citation2003), for both each firm and the market as a whole. Well-designed public GVC programmes may even enhance entrepreneurial activity, employment, R&D expenditures, patents and the time to IPO (Cumming and Johan Citation2009, Citation2016). Similar effects on firm sales growth were found in Europe when GVC was mixed with VC (Grilli and Murtinu Citation2014). In this study, GVC alone did not have any effect. In the US context, the Small Business Innovation Research (SBIR) programme has been examined several times and through different lenses. The well-established programme has, for instance, had a positive effect on the growth time of investees (Lerner Citation1996) and on the government’s risk acceptance (Link and Scott Citation2010). In summary, it would seem that GVC policies can achieve entrepreneurial stimulation and various growth measures, although the results vary and the measured variables are not always comparable, indicating that GVC has promising potential but that the design and implementation are crucial.

3.3.2. Private and institutional finance

Private and institutional investments are undoubtedly one of the most critical ingredients when financing non-organic growth. This section contains an overview of different traditional sources of private equity (PE), i.e. money that is exchanged with shares in a growth firm when the provider sees a sufficient possibility of gaining a profit, normally through dividends or exits. Available equity is often seen as important for securing R&D processes and, thus, is a critical element of micro-level firm performance and macro-level economic growth. The literature normally differs between the sources and entry at certain stages in a venture’s lifecycle. First, BAs are individuals who invest their own money. This form of investment should not be mistaken for crowdfunding, as the latter refers to the acquisition method (see the section on alternative financing below). Furthermore, VC funds are categorized as focusing on the early stage. VC funds have received a great deal of attention in the literature, despite not being central in all economies. A plausible explanation for this attention is that the finance literature often focuses on the US, a country assumed to have a developed equity-based capital system, in which VC plays a more important role than in credit-based and subsidy-based systems (Black and Gilson Citation1998; Landström Citation2017, 26; Zysman Citation1984).

As with GVC, private capital has been examined in a vast number of contexts and measures. The results are mixed, although there is no doubt that private risk finance is a key source that facilitates the external know-how and network access critical for new ventures. This relevant literature can be boiled down to a few key findings.

First, VC fund investments are frequently found to be superior to those of GVC, with more positive effects on various performance measures. However, this situation is not black and white. In two Belgian studies, VC did not necessarily perform better than firms with GVC or non-VC-backed firms (Alperovych, Hübner, and Lobet Citation2015; Manigart, Baeyens, and Van Hyfte Citation2002). Nonetheless, the majority of VC research displays positive effects. For various US, European, Chinese and Australian contexts, studies on VC performance have unanimously drawn a positive picture concerning the performance of VC investments. VC has been found to enhance exits, employee growth/employment and sales, R&D expenditures/innovation, new firm formation and aggregated income and to surpass GVC (Brown, Martinsson, and Petersen Citation2012; Cumming and Johan Citation2016; Davila, Foster, and Gupta Citation2003; Dutta and Folta Citation2016; Faria and Barbosa Citation2014; Feldmann Citation2014; Grilli and Murtinu Citation2014; Samila and Sorenson Citation2011; Zhang and Mayes Citation2018). In summary, VC has been associated with not only different measures of firm performance but also the likelihood of going private (Sørensen Citation2007), enhancing stage financing (Tian Citation2011) and value adding on firm growth and innovation (Peneder Citation2010). This result is similar to the extensive meta-analysis of Rosenbusch, Brinckmann, and Müller (Citation2013) confirming the positive effects of VC on firm performance but providing nuance and showing how industry selection accounts for most of these positive effects.

Digging further into the data on private finance in general, there seems to be a negative relation between the total number of investments and the number of dividends, implying that performance is lower for firms with dispersed ownership structures (Fama and French Citation2002). Austrian micro-data have curiously shown that VC is primarily invested in firms with high-performance potential and that VC added value regarding growth but not innovation output (Peneder Citation2010). Such findings have frequently been found in venture research, for both VC and BAs, and can be explained by post-investment non-financial value added. The evidence shows that private investors (regardless of classification) provide long-term competency, networks, governance and passion, which grants, some GVC and internal funds are not able to provide (see e.g. Cumming, Werth, and Zhang Citation2019; Fraser, Bhaumik, and Wright Citation2015; Large and Muegge Citation2008; Politis Citation2008; Proksch et al. Citation2017). In a recent relevant study on governance related to EEs, start-ups in technology parks were found less likely to be acquired by VC, and the governance provided by VC is superior to that of technology parks (Cumming, Werth, and Zhang Citation2019).

3.3.3. Bank financing

Bank finance has a central place in the financial literature, but banks are believed to be one of the least accessible sources of finance for innovative start-ups, which cannot present qualifying collateral (Hall and Lerner Citation2010; Petersen and Rajan Citation1995). This inaccessibility has given rise to allegations of market failure in the literature (see, e.g. Fraser, Bhaumik, and Wright Citation2015; Gustafsson and Autio Citation2011; Landström Citation2017; Stiglitz and Weiss Citation1981; Westhead, Wright, and Mcelwee Citation2011). Bank loans can be used for long term investments while credits are often used for day-to-day working financial capital. There are, however, contradicting arguments that banks play a surprisingly important role in financing innovation after all (Kerr and Nanda Citation2015; Nanda and Nicholas Citation2014; Robb and Robinson Citation2014), especially where patents can be used as collateral (Mann Citation2018). Concerning the performance of debt financing, firm debt has been found superior to the owner’s (or founder’s) debt in relation to firm performance (Cole and Sokolyk Citation2018). Furthermore, bank loans have been found inferior to VC in terms of firm growth (Cole, Cumming, and Li Citation2016).

3.3.4. Alternative financial capital

Alternative sources of finance such as crowdfunding have taken an important position for start-up financing (Ziegler, Shneor, and Wenzlaff Citation2020). Using search words such as ‘crowdfunding’ AND ‘performance’/‘survival’ did not yield any direct results for now. Crowdfunding is first and foremost a mass acquisition method of private investments. As researchers can now access the track records of crowdfunded firms, relevant evidence of crowdfunding performance starts to emerge. Walthoff-Borm, Vanacker, and Collewaert (Citation2018) provided evidence of an adverse selection problem on crowdfunding platforms, where equity crowdfunded firms have 8.5 higher failure rates than non-equity crowdfunded firms. This could perhaps be interpreted as the best start-up cases being able to access the ‘best’ money (high-ranking VC and BAs in positions to supply considerably more competence and governance), but future research will hopefully shed light on this issue. Although the authors above argue that crowdfunding platforms facilitate higher innovation rates, those numbers are also in contrast to a recent report by Capital Crowdfund Investors indicating that crowdfunding increases sales, job creation, ROI and follow-up investments.Footnote1 Although this report is not peer-reviewed, it is still assumed that crowdfunding addresses a financial gap for many start-ups, even though there should be an adverse selection problem.

4. Finance in entrepreneurial ecosystems

The next step is to decide on what an ecosystem is in order to get a clear picture of the role of finance in ecosystems. Despite its popularity, there is still no consensus on a single definition (Da Rin and Hellmann Citation2020; Leendertse, Schrijvers, and Stam Citation2021, 554; Spigel Citation2020). One reason may very well be that the concept is rooted in two different research fields, namely strategic management and regional development (Acs et al. Citation2017). In addition, the term ‘ecosystem’ has an established place among practitioners of entrepreneurial finance, which does not necessarily resonate with the academic understanding.

In any case, the common denominator for most definitions is actors and factors of an entrepreneurial system. Strategic management emphasizes how actors of an ecosystem interact, while advocates of regional development may be more concerned with the factors that promote entrepreneurship. Of course, the boundary between them is not at all clear-cut. In the first perspective, the actors are primarily investors and investees, for example. In the latter, one factor is the availability of venture capital in general. The problem occurs if one side of the table proclaim that vital ecosystems can emerge without the other. In any case, this dichotomy might be exaggerated as all definitions imply some sort of agglomeration effect.

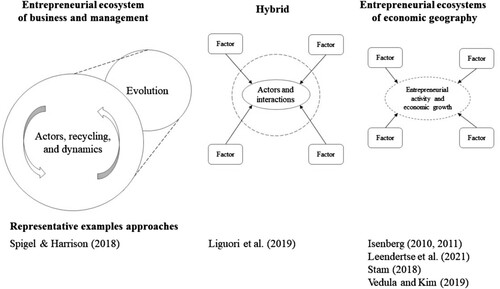

In general, the literature on ecosystems can be divided in other ways. For example, Theodoraki and Catanzaro (Citation2021) categorized the literature along five existing dimensions, namely structural, systemic, evolutionary, spatial and international. Wurth, Stam, and Spigel (Citation2021) recommend seeing ecosystems as their context, structure, micro-foundations or as complex systems. In respect of this paper, only a very small number of studies provide us with information to build on. The most prominent examples are recent studies that measure the scope of venture capital investment in a region (see e.g. Leendertse, Schrijvers, and Stam Citation2021; Stam Citation2018; Vedula and Kim Citation2019). As said, this gives us little clue about how finance is distributed among actors within the system. To our knowledge, all of the current literature on ecosystems inquires about the relation of the regional/national scope of finance as a factor. One exception is the one of Liguori et al. (Citation2019), who developed measures of financial availability in entrepreneurial ecosystems. These measures go beyond venture capital availability as a conditional and regional factor and ask the actors about the perceived access. Therefore, from the standpoint of financial distribution, studies that aim to understand the role of finance must relate to the dichotomy of finance as as a conditional factor or something that is determined by the interactions between the actors.

5. Discussion

5.1. The roles of finance in various ecosystem perspectives

Spigel (Citation2020) synthesized several interpretations of entrepreneurial ecosystems based on the use and context. As mentioned, most definitions refer to the presence of factors or actors that enhance entrepreneurship, and within those boundaries lies finance. Its role is shown both through financial actors and as a supporting factor. It is not clear when ecosystems should be viewed as an interacting group of startups and stakeholders, when they form a business cluster interacting with externalities or when they form a prosperous region due to vital entrepreneurial activity. This is important if the goal is to achieve economic growth or to help a rural ecosystem cluster develop.

The various stances also means that there are various approaches to measuring ecosystems. Recent and notable approaches include Liguori et al. (Citation2019) with a perceptual measure of factors, Vedula and Kim (Citation2019) on the national scale and Leendertse, Schrijvers, and Stam (Citation2021) with a ‘city-region’ focus. In the latter, the financial focus is limited to the average amount of venture capital per capita and the percentage of SMEs that is credit constrained. Neither of these approaches has aimed to provide an understanding of how the flow of money takes place within an ecosystem of businesses, thereby providing an agenda for future research.

This paper therefore argues that the distinction between the perspectives must be clarified further because it sets the stage for how to study phenomena such as how finance flows between the actors of an ecosystem. If policymakers seek to build on lessons from ecosystem research, the lessons will likely be applied to deprived or rural regions lacking such entrepreneurial vitality. In such cases, this study argues that the best approach would be to build on existing and nascent ecosystem structures according to the process theory developed by (Spigel and Harrison Citation2018). A well-suited policy for rural ecosystem may be how actors should overcome the hindrances arising from absent ecosystem conditional factors. The following figure therefore illustrates the key takeaways from this study ().

Figure 1. Various ecosystem approaches relevant for financial research.

The literature search gives the impression that there is more empirical research on the side of regional development, but it is suspected that this may be because statistical and macro-level data is easier to acquire. The Achilles heel of process theories is that data can be more difficult and time-consuming to obtain, especially for entrepreneurial ecosystems. In addition, various accounts (see e.g. Feld Citation2012 and various case studies) give the impression that, among practitioners, the term ‘ecosystem’ refers to certain communities of entrepreneurs, which includes aspects from both approaches.

All in all, the ecosystem concept sounds promising for unleashing more entrepreneurial activity and aggregated output. But as many have pointed out in the past, it still suffers from a lack of clarity and single interpretation across stances and disciplines. The question now is whether the extended literature can shed light on how finance flows in ecosystems.

5.2. What are the lessons from the extended finance literature?

The field of finance and entrepreneurship is dominated by quantitative methods and traditions (Bruce Citation2007; Neergaard Citation2014). Therefore, the literature is often concerned with testing the effects of financial sources or entrepreneurial programmes. Very few of the identified studies were longitudinal, and none examined entrepreneurial processes that included finance. The vast tendency is cross-section design studies with limited ability to say anything about the larger context in which the entrepreneurs interact. This is what Wurth, Stam, and Spigel (Citation2021) referred to as regressing isolates. The financial literature presented in section 3 is unclear about the systemic interactions that define ecosystems. For example, the ecosystem literature posits that core ecosystem actors can enhance the financial access for other and new members of the start-up community. This implies that ecosystems can be described as autocatalytic systems, where a reaction of an interaction is also a catalyst for the same or a coupled reaction. Therefore, when studying finance in entrepreneurial communities, we have to look past the vast number of cross-sectional designs and ask how such relations play out over time.

Other issues relevant for policymakers include how government matching capital plays an important role by reducing the threshold for private venture and angel investments. Whereas distance and the home bias are an issue (Avdeitchikova and Landström Citation2005; Coval and Moskowitz Citation1999), such programmes should be able to bridge networks and reduce asymmetric information among established actors in mature ecosystems and nascent ecosystems. This means that there should be a possibility for policymakers to catalyze ecosystem emergence depending on their initial conditions. Policymakers should then acknowledge that importance of the systemic and autocatalytic effects in systemic entrepreneurship.

The next lesson is about the determinants to business and venture capital investment decisions and the theories that predict their behaviour. Role models and networks of resource providers reduce the uncertainty of start-ups without tangibles and track records – networks and interactions according to business and management theories relevant to entrepreneurial ecosystems. Within the paradigms of transaction cost economics (such as agency), there are numerous issues that can be contextualized to business ecosystems.

Similar to the findings of Kang et al. (Citation2021), financial issues are not top-of-mind in ecosystem literature. The absence of financial knowledge in ecosystems was the point of departure for this study and the study upholds that there is a gap in the literature. To find novel insights into how ecosystems work, there needs to be more knowledge about their financial interactions. This requires going beyond exploring the factors and actors of ecosystem and knowing how the ‘recycling’ (Spigel and Harrison Citation2018) of entrepreneurial resources such as finance plays out over time.

6. Conclusion

The goal for this paper was to explore the current state of knowledge about finance in entrepreneurial ecosystems. To sum up, the paper add value to the literature about finance in systemic entrepreneurship and entrepreneurial ecosystems with three contributions.

First, the paper highlights how entrepreneurial finance is important also at the systemic level, despite a lack of scholarly and theoretical focus. The theoretical development of systemic entrepreneurship has culminated into the entrepreneurial ecosystem approach. However, financial interactions are left unexamined even though the practical use of the term to a large extent addresses the relationship between investors and start-ups.

Second, the entrepreneurial ecosystem theory needs to be fully crystallised and defined before the role of finance is examined. Finance can be treated a supporting and conditional factor or the result of the interactions within the system. In some cases, thriving ecosystems can exist in areas without the agglomerated ecosystem factors, which warrants a closer look and perhaps also a division of the concepts.

Third, the paper addresses how the traditional and widespread quantitative methods of entrepreneurial finance is not sufficient for explaining the autocatalytic processes of entrepreneurial ecosystems. The traditional and mainstream research designs of entrepreneurial finance may provide valuable insight on the micro-level, but not on the aggregated or systemic level. When the determinants and effects of financial sources become autocatalytic in entrepreneurial systems, the literature should pursue evolutionary and longitudinal methods to account for such processes.

As a result, this determines how measurements are conducted. The issue can be understood when a dominant strand of the literature views functioning ecosystems as a way to achieve higher aggregated economic output. In the most influential conceptualisations, the presence of venture capital or similar funding is one of several factors that can indicate economic rates. Another strand of literature focuses on the entrepreneurs and stakeholders within the system and how resources flow among them. To the current knowledge, there are no follow-up empirical studies that have examined such interactions and it is suspected that the reason is that longitudinal and processual data of ecosystem networks is more challenging to acquire than statistical macro data that is publicly available.

7. Future research

As indicated above, it is suggested that future research pursue evolutionary approaches to the financial interactions of entrepreneurial ecosystems. This may require a departure from the mixed actors and factors perspective that most of today’s definitions apply. The autocatalytic and non-linear financial dynamics of entrepreneurial ecosystems calls for mixed-methods and evolutionary and longitudinal research designs. The lessons and insights from the linear and regression methods of entrepreneurial finance should be used to provide guidelines for which dynamics and theoretical mechanisms to examine by evolutionary methods. Phenomena such as asymmetric information and signalling/screening and the pecking order framework that governs the relationship between key actors, investors and investees can be used as a theoretical fundament to see how these issues play out over time in systems.

Supplemental Material

Download MS Word (67.3 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

All the literature data are available in the appendices.

Notes

References

- Acs, Z., E. Stam, D. Audretsch, and A. O’Connor. 2017. “The Lineages of the Entrepreneurial Ecosystem Approach.” Small Business Economics 49 (1): 1–10.

- Almus, M., and D. Czarnitzki. 2003. “The Effects of Public R&D Subsidies on Firms’ Innovation Activities.” Journal of Business & Economic Statistics 21 (2): 226–236. doi:10.1198/073500103288618918.

- Alperovych, Y., G. Hübner, and F. Lobet. 2015. “How Does Governmental versus Private Venture Capital Backing Affect a Firm’s Efficiency? Evidence from Belgium.” Journal of Business Venturing 30 (4): 508–525. doi:10.1016/j.jbusvent.2014.11.001.

- Armington, C., and Z. Acs. 2002. “The Determinants of Regional Variation in New Firm Formation.” Regional Studies 36 (1): 33–45. doi:10.1080/00343400120099843.

- Avdeitchikova, S. 2008. “On the Structure of the Informal Venture Capital Market in Sweden: Developing Investment Roles.” Venture Capital 10 (1): 55–85. doi:10.1080/13691060701605504.

- Avdeitchikova, S., and H. Landström. 2005. “Informal Venture Capital: Scope and Geographical Distribution in Sweden.” In Paper presented at the Babson-Kauffman Entrepreneurship Research Conference, 2005.

- Ayoub, M. R., Gottschalk, S., and Müller, B. 2017. “Impact of Public Seed-funding on Academic Spin-offs.” The Journal of Technology Transfer 42 (5): 1100–1124.

- Beck, T., A. Demirguc-Kunt, and V. Maksimovic. 2008. “Financing Patterns Around the World: Are Small Firms Different?” Journal of Financial Economics 89 (3): 467–487. doi:10.1016/j.jfineco.2007.10.005.

- Benneworth, P. 2004. “In What Sense ‘Regional Development?’: Entrepreneurship, Underdevelopment and Strong Tradition in the Periphery.” Entrepreneurship & Regional Development 16 (6): 439–458. doi:10.1080/0898562042000249786.

- Berger, A., and G. Udell. 1998. “The Economics of Small Business Finance: The Roles of Private Equity and Debt Markets in the Financial Growth Cycle.” Journal of Banking & Finance 22 (6-8): 613–673. doi:10.1016/S0378-4266(98)00038-7.

- Bititci, U., M. Bourne, J. Cross, S. Nudurupati, and K. Sang. 2018. Towards a Theoretical Foundation for Performance Measurement and Management. International Journal of Management Reviews. Special Issue: Towards a Theoretical Foundation for Performance, Measurement and Management.

- Black, B., and R. Gilson. 1998. “Venture Capital and the Structure of Capital Markets: Banks Versus Stock Markets.” Journal of Financial Economics 47 (3): 243–277. doi:10.1016/S0304-405X(97)00045-7.

- Bonini, S., and V. Capizzi. 2019. “The Role of Venture Capital in the Emerging Entrepreneurial Finance Ecosystem: Future Threats and Opportunities.” Venture Capital 21 (2-3): 137–175. doi:10.1080/13691066.2019.1608697.

- Brander, J., Q. Du, and T. Hellmann. 2015. “The Effects of Government-Sponsored Venture Capital: International Evidence.” Review of Finance 19 (2): 571–618. doi:10.1093/rof/rfu009.

- Branstetter, L., F. Lima, L. Taylor, and A. Venâncio. 2014. “Do Entry Regulations Deter Entrepreneurship and Job Creation? Evidence from Recent Reforms in Portugal.” The Economic Journal 124 (577): 805–832. doi:10.1111/ecoj.12044.

- Brown, J., G. Martinsson, and B. Petersen. 2012. “Do Financing Constraints Matter for R&D?” European Economic Review 56 (8): 1512–1529. doi:10.1016/j.euroecorev.2012.07.007.

- Bruce, B. 2007. “Qualitative Research in Finance – Pedigree and Renaissance.” Studies in Economics and Finance 24 (1): 5–12. doi:10.1108/10867370710737355.

- Cao, Z. 2018. “Entrepreneurial Ecosystems in Emerging Economies (E4s): What Is Similar and What Is Different?” Academy of Management Proceedings 2018 (1): 17341. doi:10.5465/AMBPP.2018.17341abstract.

- Cassar, G. 2004. “The Financing of Business Start-ups.” Journal of Business Venturing 19 (2): 261–283. doi:10.1016/S0883-9026(03)00029-6.

- Claire, C., V. Lefebvre, and S. Ronteau. 2019. “Entrepreneurship as Practice: Systematic Literature Review of a Nascent Field.” Entrepreneurship & Regional Development, doi:10.1080/08985626.2019.1641975.

- Cole, R., D. Cumming, and D. Li. 2016. “Do Banks or VCs Spur Small Firm Growth?” Journal of International Financial Markets, Institutions and Money 41: 60–72. doi:10.1016/j.intfin.2015.12.005.

- Cole, R., and T. Sokolyk. 2018. “Debt Financing, Survival, and Growth of Start-up Firms.” Journal of Corporate Finance 50: 609–625. doi:10.1016/j.jcorpfin.2017.10.013.

- Cooke, P., and L. Leydesdorff. 2006. “Regional Development in the Knowledge-Based Economy: The Construction of Advantage.” The Journal of Technology Transfer 31 (1): 5–15.

- Coval, J., and T. Moskowitz. 1999. “Home Bias at Home: Local Equity Preference in Domestic Portfolios.” The Journal of Finance 54 (6): 2045–2073. doi:10.2469/dig.v30.n4.768.

- Coval, J., and T. Moskowitz. 2001. “The Geography of Investment: Informed Trading and Asset Prices.” Journal of Political Economy 109 (4): 811–841. doi:10.1086/322088.

- Cross, M. 1981. New Firm Formation and Regional Development. Aldershot: Gower Publishing Company.

- Cumming, D., and A. Groh. 2018. “Entrepreneurial Finance: Unifying Themes and Future Directions.” Journal of Corporate Finance 50: 538–555. doi:10.1016/j.jcorpfin.2018.01.011.

- Cumming, D., and S. Johan. 2009. “Pre-seed Government Venture Capital Funds.” Journal of International Entrepreneurship 7 (1): 26–56. doi:10.1007/s10843-008-0030-x.

- Cumming, D., and S. Johan. 2016. “Venture’s Economic Impact in Australia.” The Journal of Technology Transfer 41 (1): 25–59. doi:10.1007/s10961-014-9378-3.

- Cumming, D., and S. Johan. 2017. “The Problems with and Promise of Entrepreneurial Finance.” Strategic Entrepreneurship Journal 11 (3): 357–370.

- Cumming, D., J. Werth, and Y. Zhang. 2019. “Governance in Entrepreneurial Ecosystems: Venture Capitalists vs. Technology Parks.” Small Business Economics 52 (2): 455–484. doi:10.1007/s11187-017-9955-6.

- Da Rin, M., and T. Hellmann. 2020. Fundamentals of Entrepreneurial Finance. Oxford: Oxford University Press.

- Davila, A., G. Foster, and M. Gupta. 2003. “Venture Capital Financing and the Growth of Startup Firms.” Journal of Business Venturing 18 (6): 689–708. doi:10.1016/S0883-9026(02)00127-1.

- Demirel, P., and S. Parris. 2015. “Access to Finance for Innovators in the UK’s Environmental Sector.” Technology Analysis and Strategic Management 27 (7): 782–808. doi:10.1080/09537325.2015.1019849.

- Doloreux, D., and I. Gomez. 2017. “A Review of (Almost) 20 Years of Regional Innovation Systems Research.” European Planning Studies 25 (3): 371–387. doi:10.1080/09654313.2016.1244516.

- Dutta, S., and T. Folta. 2016. “A Comparison of the Effect of Angels and Venture Capitalists on Innovation and Value Creation.” Journal of Business Venturing 31 (1): 39–54. doi:10.1016/j.jbusvent.2015.08.003.

- Fama, E., and K. French. 2002. “Testing Trade-off and Pecking Order Predictions About Dividends and Debt.” Review of Financial Studies 15 (1): 1–33. doi:10.1093/rfs/15.1.1.

- Faria, A., and N. Barbosa. 2014. “Does Venture Capital Really Foster Innovation?” Economics Letters 122 (2): 129–131. doi:10.1016/j.econlet.2013.11.014.

- Farinha, L., J. Ferreira, and V. Ratten. 2018. “Regional Innovation Systems and Entrepreneurial Embeddedness.” European Planning Studies 26 (11): 2105–2113. doi:10.1080/09654313.2018.1530146.

- Feld, B. 2012. Startup Communities: Building an Entrepreneurial Ecosystem in Your City. Hoboken, NJ: John Wiley & Sons.

- Feldmann, H. 2014. “Venture Capital Availability and Labour Market Performance Around the World.” Applied Economics 46 (1): 14–29. doi:10.1080/00036846.2013.826874.

- Ferrando, A., A. Popov, and G. Udell. 2017. “Sovereign Stress and SMEs’ Access to Finance: Evidence from the ECB’s SAFE Survey.” Journal of Banking & Finance 81: 65–80. doi:10.1016/j.jbankfin.2017.04.012.

- Fink, A. 2013. Conducting Research Literature Reviews: From the Internet to Paper. Thousand Oaks, CA: Sage Publications.

- Fraser, S., S. Bhaumik, and M. Wright. 2015. “What Do We Know about Entrepreneurial Finance and Its Relationship with Growth?” International Small Business Journal 33 (1): 70–88. doi:10.1177/0266242614547827.

- Frimanslund, T., and A. Nath. 2022. “Regional Determinants of Access to Entrepreneurial Finance: A Conceptualisation and Empirical Study in Norwegian Start-Up Ecosystems.” Journal of Small Business & Entrepreneurship, In press. doi:10.1080/08276331.2022.2035171.

- Fritsch, M., and P. Mueller. 2004. “Effects of new Business Formation on Regional Development Over Time.” Regional Studies 38 (8): 961–975. doi:10.1080/0034340042000280965.

- GEM. 2016. GEM – Entrepreneurial Finance Special Report 2015–2016. http://gemconsortium.org/report

- Gjelsvik, M., and M. Trippl. 2018. “Financial Organisations: An Overlooked Element in Regional Innovation Systems.” In New Avenues for Regional Innovation Systems – Theoretical Advances, Empirical Cases and Policy Lessons, edited by A. Isaksen, R. Martin, and M. Trippl, 107–125. Cham, Switzerland: Springer International Publishing.

- Grilli, L., and S. Murtinu. 2014. “Government, Venture Capital and the Growth of European High-Tech Entrepreneurial Firms.” Research Policy 43 (9): 1523–1543. doi:10.1016/j.respol.2014.04.002.

- Guenther, C., S. Johan, and D. Schweizer. 2018. “Is the Crowd Sensitive to Distance?—How Investment Decisions Differ by Investor Type.” Small Business Economics 50: 289–305. doi:10.1007/s11187-016-9834-6.

- Gustafsson, R., and E. Autio. 2011. “A Failure Trichotomy in Knowledge Exploration and Exploitation.” Research Policy 40 (6): 819–831. doi:10.1016/j.respol.2011.03.007.

- Hall, B., and J. Lerner. 2010. “The Financing of R&D and Innovation.” In Handbook of the Economics of Innovation, Vol. 1, edited by B. H. Hall, and N. Rosenberg, 609–639. Amsterdam, Netherlands: Elsevier.

- Isenberg, D. 2011. “The Entrepreneurship Ecosystem Strategy as a New Paradigm for Economic Policy: Principles for Cultivating Entrepreneurship.” Presentation at the Institute of International and European Affairs.

- Kang, Q., H. Li, Y. Cheng, and S. Kraus. 2021. “Entrepreneurial Ecosystems: Analysing the Status Quo.” Knowledge Management Research & Practice 19 (1): 8–20. doi:10.1080/14778238.2019.1701964.

- Kerr, W., and R. Nanda. 2015. “Financing Innovation.” Annual Review of Financial Economics 7: 445–462. doi:10.1146/annurev-financial-111914-041825.

- Kraus, S., M. Breier, and S. Dasí-Rodríguez. 2020. “The Art of Crafting a Systematic Literature Review in Entrepreneurship Research.” International Entrepreneurship and Management Journal 16 (3): 1023–1042.

- Landström, H. 1993. “Informal Risk Capital in Sweden and Some International Comparisons.” Journal of Business Venturing 8 (6): 525–540. doi:10.1016/0883-9026(93)90037-6.

- Landström, H. 2017. Advanced Introduction to Entrepreneurial Finance. Cheltenham: Edward Elgar Publishing, Inc.

- Large, D., and S. Muegge. 2008. “Venture Capitalists’ Non-financial Value-Added: An Evaluation of the Evidence and Implications for Research.” Venture Capital 10 (1): 21–53. doi:10.1080/13691060701605488.

- Lee, J., and C. Park. 2006. “Research and Development Linkages in a National Innovation System: Factors Affecting Success and Failure in Korea.” Technovation 26 (9): 1045–1054. doi:10.1016/j.technovation.2005.09.004.

- Lee, N., H. Sameen, and M. Cowling. 2015. “Access to Finance for Innovative SMEs Since the Financial Crisis.” Research Policy 44 (2): 370–380. doi:10.1016/j.respol.2014.09.008.

- Leendertse, J., M. Schrijvers, and E. Stam. 2021. “Measure Twice, Cut Once: Entrepreneurial Ecosystem Metrics.” Research Policy, 104336. doi:10.1016/j.respol.2021.104336.

- Leleux, B., and B. Surlemont. 2003. “Public Versus Private Venture Capital: Seeding or Crowding Out? A Pan-European Analysis.” Journal of Business Venturing 18 (1): 81–104. doi:10.1016/S0883-9026(01)00078-7.

- Lerner, J. 1996. The Government as Venture Capitalist: The Long-Run Effects of the SBIR Program. Cambridge, MA: National Bureau of Economic Research.

- Liguori, E., J. Bendickson, S. Solomon, and W. C. McDowell. 2019. “Development of a Multi-Dimensional Measure for Assessing Entrepreneurial Ecosystems.” Entrepreneurship & Regional Development 31 (1-2): 7–21.

- Link, A., and J. Scott. 2010. “Government as Entrepreneur: Evaluating the Commercialisation Success of SBIR Projects.” Research Policy 39 (5): 589–601. doi:10.1016/j.respol.2010.02.006.

- Manigart, S., K. Baeyens, and W. Van Hyfte. 2002. “The Survival of Venture Capital Backed Companies.” Venture Capital: An International Journal of Entrepreneurial Finance 4 (2): 103–124. doi:10.1080/13691060110103233.

- Mann, W. 2018. “Creditor Rights and Innovation: Evidence from Patent Collateral.” Journal of Financial Economics 130 (1): 25–47. doi:10.1016/j.jfineco.2018.07.001.

- Mason, C., and Y. Pierrakis. 2013. “Venture Capital, the Regions and Public Policy: The United Kingdom Since the Post-2000 Technology Crash.” Regional Studies 47 (7): 1156–1171. doi:10.1080/00343404.2011.588203.

- Nanda, R., and T. Nicholas. 2014. “Did Bank Distress Stifle Innovation During the Great Depression?” Journal of Financial Economics 114 (2): 273–292. doi:10.1016/j.jfineco.2014.07.006.

- Neely, A. 1999. “The Performance Measurement Revolution: Why Now and What Next?” International Journal of Operations & Production Management 19 (2): 205–228.

- Neergaard, H. 2014. “The Landscape of Qualitative Methods in Entrepreneurship: A European Perspective.” In Handbook of Research On Entrepreneurship: What We Know and What We Need to Know, edited by A. Fayolle, 86–106. Cheltenham: Edward Elgar Publishing.

- Nofsinger, J., and W. Wang. 2011. “Determinants of Start-up Firm External Financing Worldwide.” Journal of Banking & Finance 35 (9): 2282–2294. doi:10.1016/j.jbankfin.2011.01.024.

- Pato, M., and A. Teixeira. 2016. “Twenty Years of Rural Entrepreneurship: A Bibliometric Survey.” Sociologia Ruralis 56 (1): 3–28. doi:10.1111/soru.12058.

- Peneder, M. 2010. “The Impact of Venture Capital on Innovation Behaviour and Firm Growth.” Venture Capital 12 (2): 83–107. doi:10.1080/13691061003643250.

- Petersen, M., and R. Rajan. 1995. “The Effect of Credit Market Competition on Lending Relationships.” The Quarterly Journal of Economics 110 (2): 407–443. doi:10.2307/2118445.

- Politis, D. 2008. “Business Angels and Value Added: What Do We Know and Where Do We Go?” Venture Capital 10 (2): 127–147. doi:10.1080/13691060801946147.

- Proksch, D., W. Stranz, N. Röhr, C. Ernst, A. Pinkwart, and M. Schefczyk. 2017. “Value-Adding Activities of Venture Capital Companies: A Content Analysis of Investor’s Original Documents in Germany.” Venture Capital 19 (3): 129–146. doi:10.1080/13691066.2016.1242573.

- Robb, A., and D. Robinson. 2014. “The Capital Structure Decisions of New Firms.” The Review of Financial Studies 27 (1): 153–179. doi:10.1093/rfs/hhs072.

- Rosenbusch, N., J. Brinckmann, and V. Müller. 2013. “Does Acquiring Venture Capital Pay Off for the Funded Firms? A Meta-Analysis on the Relationship Between Venture Capital Investment and Funded Firm Financial Performance.” Journal of Business Venturing 28 (3): 335–353. doi:10.1016/j.jbusvent.2012.04.002.

- Rupasingha, A., and K. Wang. 2017. “Access to Capital and Small Business Growth: Evidence from CRA Loans Data.” The Annals of Regional Science 59: 15–41. doi:10.1007/s00168-017-0814-9.

- Samila, S., and O. Sorenson. 2011. “Venture Capital, Entrepreneurship, and Economic Growth.” The Review of Economics and Statistics 93 (1): 338–349. doi:10.1162/REST_a_00066.

- Sørensen, M. 2007. “How Smart Is Smart Money? A Two-Sided Matching Model of Venture Capital.” The Journal of Finance 62 (6): 2725–2762. doi:10.1111/j.1540-6261.2007.01291.x.

- Spigel, B. 2017. “The Relational Organisation of Entrepreneurial Ecosystems.” Entrepreneurship Theory and Practice 41 (1): 49–72.

- Spigel, B. 2020. Entrepreneurial Ecosystems: Theory, Practice and Futures. Cheltenham: Edward Elgar Publishing.

- Spigel, B., and R. Harrison. 2018. “Toward a Process Theory of Entrepreneurial Ecosystems.” Strategic Entrepreneurship Journal 12 (1): 151–168. doi:10.1002/sej.1268.

- Spilling, O. 1996. “The Entrepreneurial System: On Entrepreneurship in the Context of a Mega-Event.” Journal of Business Research 36 (1): 91–103. doi:10.1016/0148-2963(95)00166-2.

- Stam, E. 2018. “Measuring Entrepreneurial Ecosystems.” In Entrepreneurial Ecosystems, 173–197. Cheltenham: Springer.

- Steyaert, C., and J. Katz. 2004. “Reclaiming the Space of Entrepreneurship in Society: Geographical, Discursive and Social Dimensions.” Entrepreneurship & Regional Development 16 (3): 179–196.

- Stiglitz, J., and A. Weiss. 1981. “Credit Rationing in Markets with Imperfect Information.” The American Economic Review 71 (3): 393–410.

- Theodoraki, C., and A. Catanzaro. 2021. “Widening the Borders of Entrepreneurial Ecosystem Through the International Lens.” The Journal of Technology Transfer. doi:10.1007/s10961-021-09852-7.

- Tian, X. 2011. “The Causes and Consequences of Venture Capital Stage Financing.” Journal of Financial Economics 101 (1): 132–159. doi:10.1016/j.jfineco.2011.02.011.

- Titman, S., and R. Wessels. 1988. “The Determinants of Capital Structure Choice.” The Journal of Finance 43 (1): 1–19. doi:10.1111/j.1540-6261.1988.tb02585.x.

- Toole, A., and C. Turvey. 2009. “How Does Initial Public Financing Influence Private Incentives for Follow-on Investment in Early-Stage Technologies?” The Journal of Technology Transfer 34 (1): 43–58. doi:10.1007/s10961-007-9074-7.

- Ucbasaran, D., P. Westhead, and M. Wright. 2001. “The Focus of Entrepreneurial Research: Contextual and Process Issues.” Entrepreneurship Theory and Practice 25 (4): 57–80.

- Van Stel, A., D. Storey, and A. Thurik. 2007. “The Effect of Business Regulations on Nascent and Young Business Entrepreneurship.” Small Business Economics 28 (2-3): 171–186. doi:10.1007/s11187-006-9014-1.

- Vedula, S., and P. Kim. 2019. “Gimme Shelter or Fade Away: The Impact of Regional Entrepreneurial Ecosystem Quality on Venture Survival.” Industrial and Corporate Change 28 (4): 827–854.

- Walthoff-Borm, X., T. Vanacker, and V. Collewaert. 2018. “Equity Crowdfunding, Shareholder Structures, and Firm Performance.” Corporate Governance: An International Review 26 (5): 314–330. doi:10.1111/corg.12259.

- Westhead, P., M. Wright, and G. Mcelwee. 2011. Entrepreneurship: Perspectives and Cases. London: Pearson.

- Wurth, B., E. Stam, and B. Spigel. 2021. “Toward an Entrepreneurial Ecosystem Research Program.” Entrepreneurship Theory and Practice. doi:10.1177/1042258721998948.

- Zacharakis, A., D. Shepherd, and J. Coombs. 2003. “The Development of Venture-Capital-Backed Internet Companies: An Ecosystem Perspective.” Journal of Business Venturing 18 (2): 217–231. doi:10.1016/S0883-9026(02)00084-8.

- Zhang, Y., and D. Mayes. 2018. “The Performance of Governmental Venture Capital Firms: A Life Cycle Perspective and Evidence from China.” Pacific-Basin Finance Journal 48: 162–185. doi:10.1016/j.pacfin.2018.02.002.

- Ziegler, T., R. Shneor, and K. Wenzlaff. 2020. The Global Alternative Finance Benchmarking Report. Cambridge, UK: Cambridge Centre for Alternative Finance.

- Zysman, J. 1984. Governments, Markets, and Growth: Financial Systems and the Politics of Industrial Change. Vol. 15. Ithaca, NY: Cornell University Press.