ABSTRACT

In Europe, very large distribution centres (XXL DCs) are increasingly appearing on planning agendas due to their growing spatial footprint and environmental impacts. Although the emergence of XXL DCs has gained traction in academic research, empirical knowledge about the process that leads to their oft-debated location choice, geometry and landscape integration is still scarce. This paper aims to improve our understanding of this process, analysing the decisions of key stakeholders in the planning-development dialectic behind four exemplary XXL DC transactions, in the Netherlands. Our analyses shed light on the motivations of public and private actors as well as the (lack of) planning rules that shape these transactions. We find that specific incentives in the Dutch decentralized planning and legal-financial system contribute to logistics sprawl. Existing planning instruments that could steer logistics developments, such as environmental and employment quality regulations, are largely left unused. Our study suggests that multilevel planning competencies and international market standards are important variables in explaining XXL DC outcomes. Unlike often assumed in the literature, internationalization has – next to stimulating the growth of XXL DCs – contributed to more sustainable location choices and landscape integration.

Introduction on the emerging of XXL DCs in Europe

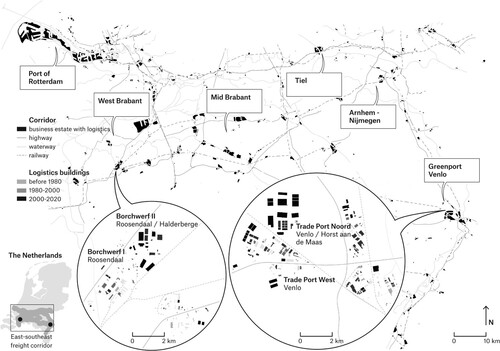

Since the 1980s, distribution centres in the logistics hinterland of main European ports have increased considerably (Flämig and Hesse Citation2011). Since 2000, there has also been a trend of developing so-called XXL DCs with floor areas above 40 thousand square metres. This phenomenon and its environmental effects have, until recently, been largely neglected in the policy and academic debates (Hesse Citation2020). In the hinterland of Rotterdam, Europe's largest port, the logistics building footprint has quadrupled since 1980. During this period, the average footprint of a single distribution centre (DC) in the exemplary East-Southeast corridor – stretching from Rotterdam to the German border – has tripled.Footnote1 Researchers estimate that not only the growth of the logistics complex, but also the changing location choice for individual DC developments is an important factor in the fragmentation of the logistics complex, a phenomenon described as logistics sprawl (Heitz, Dablanc, and Tavasszy Citation2017; Krzysztofik et al. Citation2019).

The growth and sprawl of the logistics complex – understood as a combination of DCs and transport infrastructure – challenges quality of life in hinterland locations in Europe and North America (Aljohani and Thompson Citation2016; Witte et al. Citation2016). Truck movement causes congestion and air pollution, and the footprint and elevation of DCs often eliminate alternative spatial functions while the added value of many DCs to the regional economy is increasingly questioned (OECD Citation2014; Rli Citation2016; Kuipers et al. Citation2018). Therefore, there is an increased interest, particularly among European policy advisors and planners, for understanding how to effectively steer logistics developments in order to mitigate their impacts (Hesse and Rodrigue Citation2004; Danyluk Citation2019). The Dutch Board of Government Advisors and Environmental Assessment Agency, for instance, have called for national regulations to steer logistics developments and avoid a ‘waterbed effect’ (CRa et al. Citation2019; PBL Citation2019). The recent Dutch National Spatial Vision has outlined some of such regulations (BZK Citation2020) and in response, government agencies and consultants have started to explore what planning tools could help steer XXL logistics developments towards predetermined clusters and stimulate brownfield over greenfield development (Stec Group Citation2020).

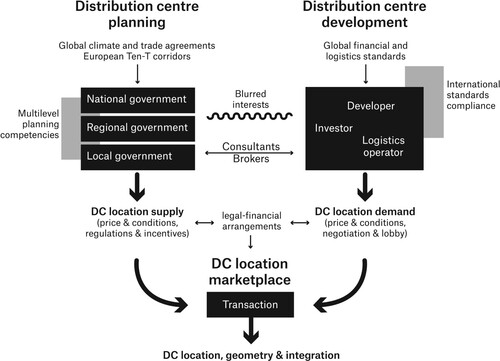

In the backdrop of these planning responses, this paper aims to contribute to academic insights into the forces shaping the remarkable growth of European distribution centres. We perceive these forces are part of a spatial planning-development dialectic (), revealed in the transactions between government agencies and companies, each with their respective motivations and scope of influence (Healey Citation1999; Heurkens, Adams, and Hobma Citation2015). Although logistics firms are often blamed for the poor spatial outcomes and impacts (Frejlachová et al. Citation2020), we assume that the local planning-development transactions, leading to the spatial outcomes of logistics centres witnessed across Europe, are also shaped by particular institutional arrangements. Hence, instead of merely focusing on the behaviour of particular actors, our approach aims to also understand the rules and resources that shape the transactions between them (North Citation1987; Scharpf Citation1997; Williamson Citation1998).

Figure 1. Framework of DC planning-development dialectic.

Although the problem of logistics sprawl has gained attention in the recent literature, in-depth empirical enquiries into recent DC developments as such remain scarce. We aim to contribute to the latter by exploring one of the busiest logistics corridors in Europe and provide an explanatory framework for XXL DC transactions. Regarding the Dutch logistics planning-development dialectic we ask: what are the key forces behind XXL DC transactions? We define XXL DCs as the tangible outcomes of these transactions in terms of location choice, geometry (shape and size) and landscape integration. In addition, we hypothesize that the DC transactions under study are influenced by (1) the involved tiers of government planning; and (2) the internationalization of the DC developer. These two forces emerged as key variables in our case study analyses. In the latter part of this paper, we propose to use them as the basis for a DC planning-development typology in the European context.

Below, we first present a framework to explain our conceptualization of the planning-development dialectic behind XXL DCs. This helps us to operationalize our main hypothesis about the two key forces that explain large-scale logistics development outcomes in Europe. In the next section, a literature review sheds light on the existing knowledge regarding spatial outcomes of DC planning and development, and discusses insights about key actor decision making in this field. In the subsequent section, we explain our research method and case study selection. Finally, we present, analyse and discuss the results of our case studies, draw our conclusions, and make recommendations for further research.

A framework for studying DC transactions and outcomes

We propose to view European XXL DCs as the spatial outcome of a transaction between DC development demand generated by logistics markets, and DC location supply generated by planning processes. This equilibrium of planning and development is established in dialectic processes as described by Healey (Citation1999). We divide the spatial outcomes in three components: location, geometry and landscape integration. Hitherto, most studies have focused on either logistics sector explanations, focusing on changing supply chains, or on (the lack of) planning requirements in relation to DC location and geometry, ignoring landscape integration. However, the latter is an increasingly important feature of the spatial outcomes observed by citizens and experts (CRa et al. Citation2019), and therefore of possible policy measures aimed at steering logistics developments.

The XXL DC transaction is conceptualized in . Adapting the theory of Edmondson, Kern, and Rogge (Citation2018), spatial planning is considered a part of the policy subsystem, influenced by international agreements regarding emissions, trade regulation and infrastructure. The logistics sector is part of the sociotechnical system, influenced by global finance and logistics standards. In this section, we identify the most important actors in these (sub)systems, because these play a key role in our case study approach. DC planning actors focus on making the best spatial conditions and trade-offs for society, while the DC development actors focus on their level of service, added value, and sometimes on the sustainability of their activities.

Government agencies (, left) typically have a broader scope than private actors since, besides supporting the development process, they also ‘moderate adverse externalities, safeguard social needs, conserve resources and environmental assets’ (Adams, Russel, and Taylor-Russell Citation1994). Furthermore, government regulations have helped to sustain industrial land values and decrease market risks. Local governments seem to have the most direct role in spatially accommodating DCs. At the same time, some municipalities seem to be insufficiently informed to make these decisions, while competition with other municipalities may create a race to the bottom in terms of land price and quality criteria (Louw Citation2009; Raimbault Citation2021). Regional organizationsFootnote2 attempt to avoid this by coordination of DC location planning. National and regional governments (provinces in the case of the Netherlands) may stimulate DC clusters through directive or restrictive planning decisions and (multimodal) infrastructure investments.

On the logistics sector side (right), the logistics operator typically looks for functional site requirements such as connectivity and building restrictions, while a developer concentrates on exchange value (Adams, Russel, and Taylor-Russell Citation1994). Large companies are increasingly expected to follow corporate social responsibility (CSR) and sustainability principles such as zero-emission logistics, besides their business interests. Institutional (e.g. pension funds) and private equity investors develop distribution centres with specialized developers, advised by consultants and brokers. The resulting pricing and other conditions, on both the supply and demand sides of the DC location marketplace, shape the transaction that determines the spatial outcome.

In recent DC developments, however, interests have blurred substantially. The operator of a DC may also be the investor and developer, while semi-governmental development companies under private law mix political and entrepreneurial goals (Raimbault, Jacobs, and Van Dongen Citation2016; Raimbault Citation2021). In this context, local authorities are easily biased towards the economic advantages of jobs and land sales despite the increasing environmental disadvantages, such as congestion and visual impact of DCs (Flämig and Hesse Citation2011; Yuan Citation2019). Additionally, corporate lobby and negotiationFootnote3 constantly influence regulations and incentives on various government levels.

The framework focuses on the changes within the timespan of a decade, playing what Williamson (Citation1998, 26) calls ‘the game of transaction cost economics’. The dialectic suggests an equilibrium, while the principal agent theory (Higgs Citation2018) suggests the possibility of a power and information asymmetry between companies and regulatory organizations in the determination of prices and conditions in land development. The case studies shed light on the transactions between the actors mentioned above. However, we first review the existing knowledge on the spatial outcomes and decision-making regarding distribution centres more in depth.

Location choice, geometry and landscape integration of XXL DCs

We address the spatial outcomes of logistics developments through the parameters location (demand side choices and supply side policies), geometry (DC size and shape) and landscape integration (quality standards in façade and public space design). In practice, there is an interdependency between these parameters. Location choice, for instance, depends on the availability of large sites to accommodate the increasing geometry of DCs (Onstein, Tavasszy, and Van Damme Citation2019; Bak Citation2020). Some studies speculate that between comparable sites, companies would prefer those with lower standards of integration to avoid extra investments and maintenance costs, and that local governments use this factor to compete amongst each other in search of blue-collar jobs and land sales (Louw Citation2009). Logistics real estate is distinct from traditional industrial, office and residential developments, since according to Raimbault (Citation2021), the integration of international real estate developers and fund managers is unique for the logistics sector. Secondly, the sector is more strongly determined by rapidly changing global construction and operating standards than other sectors (Santos Citation2006). Thirdly, logistics real estate is more dynamic, featuring typical short-term leases and profits (Hesse Citation2004). This means that to gain insight in DC development, existing knowledge on other developments is insufficient and specialized information from DC developers is necessary.

Location: beyond traditional factors

Logistics costs, generally mentioned as the main argument in location choice, still depend highly on traditional location factors such as connectivity through transport networks; availability of land, labour and consumer markets; and local economic factors such as taxation, labour union power, costs of doing business, cost of living and local economic incentives (Woudsma in: Hall and Hesse Citation2012; Verhetsel et al. Citation2015; Heitz et al. Citation2018; Onstein, Tavasszy, and Van Damme Citation2019; Strale Citation2020). Additionally, the spread of DCs along hinterland corridors is pushed by centralization of distribution networks, to serve for example the entire market of North-Western Europe, and high land prices and congestion near the seaport of Rotterdam, while it is pulled by the establishment of logistics hotspots near consumers (Flämig and Hesse Citation2011; Heitz, Dablanc, and Tavasszy Citation2017; Onstein, Tavasszy, and Van Damme Citation2019).

Over the years, authors have indicated that neoclassical location theory, assuming a market of perfect competition, cannot explain European practices of industrial land development (Adams, Russel, and Taylor-Russell Citation1994, 5; Bertaud Citation2018). There exist several restraints to land supply and other influences on location choice besides land price and profit maximization. Two international trends are increasingly pointed out. First, many distributors no longer make the location choice themselves in the emerging fourth-party logistics (4PL) networks, but rather a ‘service provider offering the use of several supply chains’ (Hines Citation2013). This volatility explains the decrease of building ownership by the user, as well as an increase in short term leasesFootnote4 (Hesse Citation2004). Second, logistics real estate development and investment firms, often integrated into international conglomerates with large portfolios (Flämig and Hesse Citation2011; Raimbault Citation2021), make location choices primarily based on real estate market arguments – based on expected profits rather than efficient logistics operations.Footnote5

Additionally, the Dutch Mainport strategy, including large hinterland infrastructure and land developments, has stimulated the logistics sector and increased the demand for logistics real estate in hinterland corridors since 1980 (Raimbault, Jacobs, and Van Dongen Citation2016; Rli Citation2016; Kuipers et al. Citation2018; Nefs, Zonneveld, and Gerretsen 2022). To guarantee the success of such developments, local governments often provide incentives to attract businesses. Multimodal logistics clusters in The Netherlands are often nationally planned, in the context of European freight corridors (Ten-T) and spatial-economic policies. These are referred to as outside-in developments (Raimbault, Jacobs, and Van Dongen Citation2016). Other clusters emerge from an existing concentration of growing logistics activities, stimulated by a local or regional government and then acknowledged as hub of national importance, known as inside-out. Given this difference, we hypothesize that DC location supply is more strictly planned in outside-in clusters. In both kinds of developments, there is still limited empirical knowledge on the role of the various stakeholders, as well as the legal-financial arrangements and regulations that shape their transactions.

Geometry: global standards

Between 2010 and 2020, the average footprint of large logistics buildings (>2.500 sqm) in the South-Southeast freight corridor of The Netherlands tripled from ca. 6.000 to 18.000 sqm, due to the rise of XXL DCs (>40.000 sqm). According to Valkanova in (Frejlachová et al. Citation2020), architects have little influence on the shape, size and functionality of a DC since these aspects are largely determined by lawmakers, international conglomerates and investment funds. The trend of large scale DCs, with footprints that can reach almost 200.000 sqm, is visible across Europe and is explained by three factors. First, the centralization of logistics facilitates the handling and value adding activities of goods in global supply chains (Hesse Citation2004; CRa et al. Citation2019). Such operations often serve multiple markets in North-Western Europe from a single – and thus larger DC (Andreoli, Goodchild, and Vitasek Citation2010). While according to Hesse (Citation2020) DC centralization in several countries peaked in the late 2000s, in The Netherlands this peak seems to occur at the time of writing.Footnote6 Second, the growth of e-commerce shifts demand from retail space to e-fulfilment. Competition between online platforms, as well as mergers, tend to increase the catalogue and service levels, while decreasing price and delivery time (Hesse and Rodrigue Citation2004; Andreoli, Goodchild, and Vitasek Citation2010). This calls for economies of scale in DCs, made possible by information technology, automation and larger building geometry. And third, logistics developments, which are increasingly performed by real estate firms rather than the users, opt for large multitenant DCs to decrease construction costs and the risk of vacancy. The demand for sites larger than 10 ha has therefore increased, a size that can rarely be found on brownfield sites (Flämig and Hesse Citation2011). We assume the increased scale of XXL DCs occurs in The Netherlands for the same reasons, given the large share of international DC developers and investors, apparently facilitated on greenfield sites by the traditionally strong Dutch spatial planning system.

Landscape integration: local variation

While geometry of large DCs seems to be highly standardized, the landscape integration – including façade and open space design – has more variation. The geographic and landscape literature rarely mentions the landscape integration of DC projects. Waldheim and Berger (Citation2008) see the rise of the logistics landscape as among the most significant transformations in recent years, and divide it in three emergent landscape categories: distribution and delivery, consumption and convenience, and accommodation and disposal. There are, however, spatial policy and design instruments available to guide the spatial outcome of DCs. Common instruments include the American concept of landscape embedded industry (Hough Citation1991) and building regulations – more common in Europe – concerning maximum building dimensions, style guidance, bulk envelopes and vegetation screens (Lehnerer Citation2009). In the Netherlands specifically, there exist spatial quality plans since the 1990s and so-called Q-teams since the 2000s (Van Assen and Van Campen Citation2014), both consisting of expert advice – sometimes legally binding – regarding architecture and landscape impacts of spatial developments. However, these instruments are rarely used in logistics developments.Footnote7

In several countries, European funds finance logistics developments, such as the European Investment Bank, the European Regional Development Fund and Joint European Support for Sustainable Investment in City Areas (Frejlachová et al. Citation2020). At the same time, national development programmes aim to increase competitiveness and attract foreign direct investment, for example ChechInvest and the Netherlands International Distribution Council. None of these programmes include quality criteria, concerning consequences of soil sealing, land-use change, or effects on social inclusion and added value.

In the academic literature and in journalism, multinational companies such as Amazon are often criticized for disruptive practices (Hesse Citation2020). This suggests that locally rooted companies might strive for better spatial outcomes than international developers. On the other hand, international investors often demand certificates with strict quality criteria, such as BREEAM (Bulwiengesa Citation2020). Critical literature suggests, however, that these standards may also be used to avoid stricter local quality regulation (Easterling Citation2014). We hypothesize therefore that the level of internationalization may affect the way stakeholders approach the location choice and integration of their DC, in different ways. Furthermore, similar to location supply, we presume outside-in clusters with multilevel planning to invest more efforts in landscape integration than inside-out clusters.

From the literature, we conclude that DC planning and development is a distinct emerging sector with strong information and competency asymmetries among actors, in need of additional empirical investigation. DC geometry seems to be generally determined by international standards. In our case study, we want to confirm whether this is also the case in the Netherlands, given its strong planning culture. Location choice and landscape integration seem to be influenced mainly by two factors: the requirements enforced by the relevant planning system(s), and the level of internationalization of the developer. In our case study, we specifically test and discuss the difference between outside-in and inside-out planning of DC clusters, as well as the influence of regionally versus internationally initiated DC developments, regarding the actual spatial outcomes.

Case study method and areas

Building an understanding of DCs as spatial outcomes of a planning-development dialectic requires a qualitative, in-depth approach. To prepare our case interviews, we compiled a repository of relevant planning documents, including property information, municipal land-use plans, provincial and national strategic plans, landscape and urban masterplans.Footnote8 Ten in-depth semi-structured individual interviews and several conversations (see acknowledgements) were conducted online in 2020 with all types of key actors defined in the framework: spatial planners on various levels, consultants and real estate brokers, as well as development-, distribution- and investment companies. The interviewees are familiar with one or both of the case study areas and the cases in that area. The purpose of the interviews was to identify patterns of stakeholder actions and motivations behind the spatial decisions regarding DCs, constrained or enabled by rules and (un)available resources.

The interviews focused on aspects typical for the interviewee's role, but all addressed the three spatial DC outcomes (location, geometry, landscape integration) in open questions, as well as the influence of involved planning tiers and internationalization of the logistics sector. The interviews were recorded and transcribed with the help of softwareFootnote9 and manual review. Prior to the interviews, all ten interviewees filled in a digital poll, scoring the influence of ten types of public and private actors in spatial decisions regarding DCs in the Netherlands, in a five-step range from none to dominant influence.Footnote10 The same poll was also filled in by twelve academic experts of spatial planning and development, to validate the scoring by case stakeholders.

The results section below presents the triangulated case findings in three steps. First, we present short descriptions of the planning-development process of the two case study areas, and analyse the influence of planning and internationalization levels in two DC transactions in each of the areas. Next, we present the views of the interviewees regarding the legal-financial arrangements that shape the current DC planning-development practice. And thirdly, we explain how the stakeholders and experts judge the influence of different actors on spatial DC decisions.

The case studies concern four XXL DCs in the East-Southeast freight corridor (), developed since 2015. The selection of the areas was guided by our aim to test the key variables of the hypothesis described above. Two DCs are therefore located in an outside-in location: Venlo Trade Port Noord; and two in an inside-out location: Borchwerf, Roosendaal. While all four DCs are largely financed internationally and represent a blurring of stakeholder roles, the VidaXL DC complex in Venlo is developed by a locally rooted e-commerce company for its own use, the DSV cluster (Venlo) by an international logistics operator for flexible operations, and both the Primark and VGP park DCs (Roosendaal) by pan-European logistics real estate companies with regional branches. Of the latter two, the first is dedicated to one large international retailer while the second is built for flexible lease.

Figure 2. Growth of the logistics complex in the East-Southeast freight corridor. Interactive map at https://mertennefs.eu/landscapes-of-trade/

Elements shaping transactions and spatial outcomes

We describe the planning and development process of four case DCs in two areas by focusing on the elements shaping the transactions – land pricing and other incentives, governance structure, land-use plans and regulations, actor competencies and resources – and their spatial outcomes.

Trade Port Noord, Venlo

In national planning documents, Venlo has been defined as an important inland logistics hub from the 1980s onwards, ‘building on its history as a border town with trade and customs functions’, explains an interviewed regional government official. After the year 2000, infrastructure and area developments have sought to strengthen Venlo as an agro-logistics hub, a so-called Greenport. In 2007 the development concept started in a multilevel collaboration, according to the project leader of one of the local governments involved: ‘our work group also included regional and national government, as well as the private sector’. In 2020, construction of a third rail terminal started in Venlo, initially planned as extended gate of the port of Rotterdam, which soon turned out to be rather an important e-commerce link to China via Central Asia.

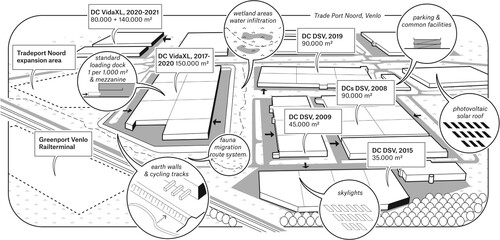

Trade Port Noord () is part of Greenport Venlo, for which the 2009 masterplan foresees an area development of 5.400 ha, combining agro-business estates with 600 ha nature development. In the area, the 2012 Floriade was organized, an international horticulture and landscape event. The Greenport Venlo Development Company, a merger of local land development vehicles with Limburg Province and three municipalities as exclusive shareholders, has since been in charge of land sales. Land price discounts incentivised initial DC developments. At the former Floriade site, the development of the Brightlands agro-innovation campus aims to retain talent in the region and stimulate the agro-food sector, ‘by bringing knowledge institutions, governments and entrepreneurs together in the field of healthy food and safe nutrition’.Footnote11

Figure 3. Trade Port Noord, Venlo.

Several of the high spatial ambitionsFootnote12 regarding landscape integration as well as nature development were realized successfully in Venlo. Other ambitions, such as attracting agro-food production companies and setting up a Cradle-to-Cradle business cooperation,Footnote13 have not (yet) been met.Footnote14 The last phase of nature development (200 ha) was cancelled after the withdrawal of national funding in 2011. The most successful sector occupying Trade Port Noord has been the European distribution of consumer goods, medical supplies and, above all, fashion. The local government project leader: ‘We agreed on mixing logistics with agro-food and manufacturing. Big fashion companies are not part of the regional DNA’. The commercial director remains optimistic:

Due to the recent DC real estate boom and the proven success of the location, the Greenport Venlo Development Company can select companies with socioeconomic relevance for the region. […] Developers of new DCs are required to show lease contracts of at least 5 years for at least half of the floor area in the masterplan, to avoid speculative developments and vacancy.

In the area, Dutch company Vida XL operates three e-fulfilment DCs for furniture and home accessories, while a fourth development started in 2021, increasing the company's building footprint here to 370.000 sqm. Danish-founded logistics multinational DSV operates four multitenant DCs here,Footnote15 from which the company provides logistics services to various producers and traders. Their DC footprint in Trade Port Noord measures 260.000 sqm, whereas DSV's portfolio in the Netherlands amounts to about 800.000 sqm in 2020.

Borchwerf, Roosendaal

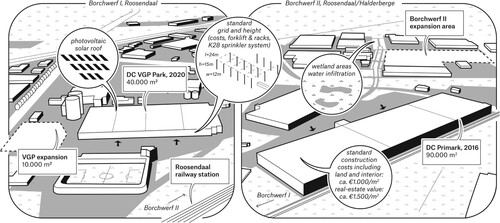

Borchwerf is a mixed industrial area at the northern fringe of Roosendaal, planned since the 1980s (). Some parts are recently being redeveloped. Its recent extension, Borchwerf II, became a logistics hotspot during the development process. This happened, according to the interviewees, mainly by coincidence, since a nearby multimodal location, Logistics Park Moerdijk, was put on hold due to legal issues concerning the European nitrogen emission ceiling. ‘Logistics developers, who had become interested in the area right in between Europe's largest ports, Rotterdam and Antwerp, decided to build in nearby Roosendaal. […] Like Trade Port Noord, Borchwerf II has a freight rail connection, paid by the national government. There is, however, no project for a rail terminal, since there is already one in Moerdijk’, explains a local economic policy advisor.

Figure 4. Borchwerf, Roosendaal.

The lots in the business estate are sold directly by a joint venture sales office of the municipalities Roosendaal and Halderberge. Also in Roosendaal, incentives have helped to attract the early businesses in the area, but these were non-monetary. Instead, local labour and education programmes facilitated the DCs, which would be needing thousands of employees. Borchwerf II has become a recognized cluster for e-commerce and other DCs targeting the Benelux, including food, consumer goods and fashion companies.

As in Venlo, the DCs in Roosendaal have in-between infrastructure zones, integrating a water buffer facility (wetlands) and a recreational cycling network. Buildings are slightly smaller and no earth walls are built here, because of limited space. The plans demonstrate moderate spatial ambitions regarding architecture, and some ecological performance.Footnote16 Both municipalities have realized temporary housing facilities for migrant workers near the DCs.

In the southern edge of Borchwerf II, Irish fast-fashion retailer Primark realized a 90.000 sqm e-fulfilment DC.Footnote17 There has been expert and public criticismFootnote18 on the extensively visible façade along the railway, as well as the façade pattern, which changed from horizontal to vertical in the second construction phase. On a brownfield site near the railway station of Roosendaal, pan-European developer VGP Group has developed a multitenant DC of 41.000 sqm, leased to small e-fulfilment operators such as Active Ant. An additional 9.000 sqm building across the street is planned to be built for a specific operation ().

Table 1. Case comparison.

Legal-financial arrangements influencing DC transactions

Interviewees explain that specific legal-financial arrangements observed in the cases – some aggravated by the governance structure in place, as well as the (lack of) regulations and actor competencies – tend to incentivise undesirable spatial outcomes such as logistics sprawl. Frequently mentioned are ‘quick flips’, in which developers and municipalities make land deals based on short-term lease contracts (ca. 3 years). According to a critical developer, ‘shortly after such a deal, property is sold to an investor, leaving the area with an uncertain future’. Short term profit-oriented companies with large financial resources tend to make deals with municipalities suffering from budget shortages, both hoping to take advantage of the high demand for logistics development sites in the region. According to a logistics real estate advisor ‘this can cause a speculative bubble and vacancy’. An investor regards it as ‘the main explanation for the boxification of the landscape’.

Semi-public development companies are also common. These provide more knowledge and better negotiation power than a municipality. At the same time, they are more distant from public scrutiny and democratic decision making,Footnote19 which increases the risk of watering down of social goals. For instance, in case of a lack of demand by the targeted manufacturing or agro-industrial companies, development companies approve developments that do not match the original high standards. According to a real estate advisor, ‘local governments should collaborate more in land banks, instead of competing amongst each other’.

The aforementioned sale-and-lease-back allows construction and financing of a large DC, quickly shifting the real estate from the company's balance sheet and liquidating the considerable profits,Footnote20 which can be invested in the supply chain or paid to shareholders. German investor Deka Immobilien explains that this usually includes forward purchase and funding:

In a matter of weeks, on paper, the DC is funded, bought and leased by Deka, before a developer such as Vida XL starts construction (6 months), followed by interior works (racking and conveyors, 4 months). This arrangement is used by Deka in 35 countries, with almost identical contracts.

Speculative developments, as opposed to built-to-suit developments, are often seen as an important factor in vacancy and logistics sprawl. ‘Developers take building lots hostage – out of the market – by making promises to the local government in exchange for land options, without actually constructing’, the spatial-economic advisor explains. An interviewed speculative developer, however, claims the opposite: that ‘speculative DCs are more flexible than custom-built ones, optimized for a broad range of tenants in the DC market on the long run’. Another expert claims that ‘while this is true, the flexible leases often attract companies that do not necessarily fit in the economic DNA of the region, and lead to shorter contracts and more migrant labour’.

Land price and scarcity are seen as key factors in location choice. Governments do not take sufficient advantage of these, to promote brownfield developments for instance.Footnote22 Stacked logistics developments, similarly, have not taken off in the Netherlands, due to the low land prices. An NIDC representative: ‘land scarcity is raising prices already, and government policies can further steer locations and innovative developments’. Deka recently financed its first stacked logistics project in the Netherlands.

Actor influence on DC transactions

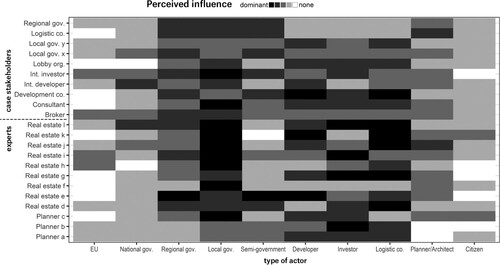

In the context of the cases, especially the interviewees of the logistics and real estate sectors surprisingly share the concerns regarding rapid logistics sprawl and the boxification of the Dutch landscape. Although their expressed estimation in the survey indicates a great fragmentation in influence (), the graph also demonstrates two clusters of relatively influential actors: the local and regional governments, and the combination of developers, investors and logistics operators. Municipalities are considered influential through land-use plans (Woudsma in: Hall and Hesse Citation2012), while they rarely acknowledge that power themselves. Planners, architects, citizens, as well as national and EU governments are considered of little influence.

Figure 5. Perceived actor influence on spatial decisions regarding DCs, estimated by the interviewed stakeholders and experts.

Besides pointing at each other – municipalities versus developers for instance, stakeholders point at specific subsets of other actors during the interviews, such as private equity investors who aim for short-term profits. These might be less interested in the sustainability of the development than institutional investors. Small municipalities (<100.000 inhabitants) are often mentioned too, because they are often not as experienced and informed as big cities. In the words of many interviewees, such municipalities ‘don't know what they’re doing and can be taken advantage of by developers’. In practice, there are many shared responsibilities. Location choice for example, according to most logistics developers and investors, is determined mainly by the choice of the client, e.g. a producer or trader. Corporate players, in turn, are regarded more powerful than local planners and might be making choices from foreign headquarters. Investors and consultants, however, do influence the location choice of their client, when they think it is too risky or not profitable enough.

The interviewees suggest a high level of corporate pan-European standardization, and in contrast a large diversity in government behaviour, including spatial and fiscal legislation, as well as facilitating government bodies who wish to attract logistics companies. Many stakeholders note that the DC planning focus in the Netherlands, compared to other European countries, is rather narrow – emphasizing visual impact, while it should emphasize social-economic effects and sustainability as well, including circularity, energy transition and modal shift.

Discussion

The presented Dutch case studies confirm that land pricing and incentives, governance structure, land-use plans and regulations, international standards, actor competencies and resources, are all relevant in explaining the spatial outcomes of European XXL DC transactions. While these variables are also found in other studies, our results suggest that two forces are particularly dominant: multilevel planning and internationalization.

Multilevel DC planning competencies

We found evidence in the cases that planning competencies – especially experience and knowledge about logistics developments – can deliver higher degrees of control over location choice (clustering near multimodal hubs for instance) and landscape integration (e.g. embedding ecological and recreational developments). In larger logistics-savvy cities such as Venlo, these competencies are stronger, and sometimes combined with planning efforts between the local, regional and national scales. The analysed planning documents regarding Venlo Trade Port Noord show the elaboration of spatial regulations and structures, based on expert views, (design) research and collaboration among the local, regional and national governments. Strict local planning, as in Roosendaal, entails less control and less use of specialized information, as is shown in the documentation regarding Borchwerf II and affirmed by both the private and public stakeholders during the interviews. In other more rural municipalities, non-institutional investors seem to cause fragmented DC developments associated with logistics sprawl. Since the 1970s, there has been a large information disparity between large logistics corporations and small municipalities (LeCavallier Citation2016). While governments use spatial-economic consultants and often publish the reports online, logistics firms are advised by specialized fiscal experts and real estate advisors/brokers. This increases the competency asymmetries between actors in the DC transaction.

According to Stec Group (Citation2020, 52–53) multilevel policy instruments could make a difference in location choice and landscape integration, if these were better used. Indeed, the Dutch instruments found in our study are quite similar to those used in most European municipalities and the US: ‘conditional land-use provisions on landscaping and sound proofing, minimum job density, infrastructure and traffic impact fees, property tax, truck exclusion/concentration zones, and land use buffers between logistics and housing’ (Yuan Citation2019, 534). Additionally, a brownfield redevelopment fund, filled by charges from greenfield developments, may be a good instrument too, as well as the emerging cross-regional coordination of the East-Southeast corridor (Panteia et al. Citation2019). The latter, however, we did not observe in our cases.

International DC developers: standards and blurring

Our cases show surprising evidence about the role of local rootedness – or by contrast the internationalization – of companies plays in the spatial outcome of DC developments. It turns out that multinationals do care about sustainable location choice (established multimodal logistics clusters) and landscape integration. Not only do they work with local representatives in the Netherlands, familiar with the regional landscape and socio-economic context. They also have various quality control and risk-avoiding mechanisms in place to safeguard their investments in DCs in the long run.Footnote23 Such developers invest in flexible building layouts, durable materials and higher than required energy standards, to keep buildings profitable for a period of 30–40 years. Both in Venlo and Roosendaal, there are examples of logistics or parcel operators that invest heavily in automated equipment, written off in about 15 years. By contrast, it appears that especially local and private equity investors, focused on short-term profits, have developed DCs outside of established clusters, with lower construction and integration standards.

Our interview results confirm a strong internationalization in DC development practices, standards and geometry related to the more general internationalization of supply chains. Local land-use plans have adapted to the growing scale of DCs. Integration of the DC in its surroundings often follows from international standards as well, unless a local or regional plan imposes additional requirements, such as Venlo's Trade Port Noord. It seems therefore, that the concern of Easterling (Citation2014, 200) about ‘international standards being used to undermine national environmental laws’ does not apply to Dutch DCs – sustainability standards of BREEAM NL are higher than its international peer. Some multinationals, such as Amazon, are held responsible for the decline of local businesses and reasonable working conditions (Hesse Citation2020) and are therefore, according to an interviewed investor, ‘explicitly not welcome in certain municipalities in Germany’. We did not find a similar restrictive practice in the Netherlands. Our study shows that, although government-owned land development companies have distanced logistics land transactions from public scrutiny, they enhance the competencies necessary to deal with (multinational) companies and uphold public values.

Finally, we find that logistics companies – regionally or internationally originated – that have strong regional ties depend on the economic vitality of the region as a whole and a positive public image for their ‘license to operate’. This matches a recent conclusion by Raimbault (Citation2021) that international DC developers depend on local coalitions to dominate the market. For example, Greenport Venlo and international parcel operator DPD have invested in landscape and cultural heritage as part of their CSR policies. The damaged sector image is a risk for long-term logistics investors and operators, who would therefore welcome stricter regulation of logistics greenfield developments and incentives for brownfield development,Footnote24 effectively creating a level playing field across the Dutch East-Southeast corridor.

Conclusion

In this paper, we assumed that very large distribution centres (XXL DCs) in Europe are the spatial outcomes of a specific planning-development dialectic (). In this view, the location choice, geometry, and landscape integration of XXL DCs are a combined result of transactions between localized planning and development efforts, which in turn are shaped by a variety of rules and available resources. Four Dutch DCs, with differing planning-development interactions confirm that, next to land pricing and other common incentives, multilevel planning competencies and international DC development standards strongly explain the Dutch DC transactions and outcomes studied. While internationalization of the sector has been an important driver of XXL DC growth, it appears that austerity and a lack of knowledge among local governments, best explain the logistics sprawl witnessed in Europe outside of established clusters.

Our framework goes beyond a neoclassical land price mechanism to include other transaction costs, particularly those associated with multilevel planning competencies and international development standards. An interviewed investor illustrated the relevance of such costs very clearly:

From an accessibility point of view, we would like to invest in DCs in Rotterdam. The maximum land-lease of 25 years typically offered by the Rotterdam Port Authority, however, does not match our investment horizon, in which we write a building off in 40 years. So, we take our demand to other locations.

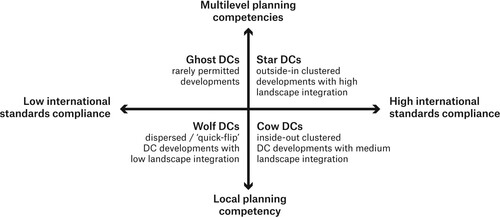

Figure 6. European DC planning-development typology.

The DC planning-development dialectic offers several pathways of further research, for example into how certain price conditions stimulate innovative sustainable DC practices – multifunctional, stacked, or DCs with climate adaptive landscapes. Developing empirical and normative DC assessment methods, e.g. to promote more sustainable spatial DC outcomes, also seems relevant and promising. Besides the two rational components of planning competence and internationalization, however, there is clearly a softer, more irrational component at work in the development and planning process of DCs that consists as much of rhetoric, persuasion and framing as of hard financial-economic assessment (Healey Citation1999; Nefs, Zonneveld, and Gerretsen Citation2022). Both rationalities and the irrational component should be part of further research.

For planning practitioners, the two variables that stood out in our analysis offer good starting points for effective policies aiming to influence transactions and hereby improve spatial DC outcomes. Existing local planning instruments and guidelines, if combined with regional and national coordination – perhaps with incentives such as a brownfield redevelopment fund – seem promising spatial steering tools. Also, in the high-profit margins of DC development, there seems to be enough room to improve landscape integration, given a level playing field across regions. Market demand could be enhanced by promoting higher (international) standards in logistics investment funds and the sharing of best practices, for example for creating high-density and landscape integrated DCs.

Research data

Nefs, Merten (2021): Distribution Center Development Cases Venlo and Roosendaal. 4TU.ResearchData. Dataset. DOI:10.4121/14717058

Nefs, Merten (2022): Dutch Distribution Centres 2021 Geodata. 4TU.ResearchData. Dataset. DOI:10.4121/19361018

Acknowledgements

The authors thank Christian Heerings, Hanneke Bruinsma and Erik Harting for their crucial introductions. And the (other) interviewees: commercial director Greenport Venlo Development Company, economic policy advisor Roosendaal, planning strategist Limburg, planning strategist Horst aan de Maas, logistics developers VGP Benelux, logistics development consultant Stec Group, director logistics real estate DSV, head strategic tenant relations logistics Deka Immobilien, international partner / head of industrial and logistics Netherlands Cushman & Wakefield, director of Holland International Distribution Council. We appreciate the valuable advice and information from BREEAM NL, REWIN, Buck Consultants International, Bouwinvest, LCB, Noord-Brabant, Ministries of Infrastructure and Water as well as Internal Affairs, Studio Marco Vermeulen, DPD, CTP and CBRE. Contacts are available via the authors. We also thank the reviewers who have helped to improve the structure of the paper considerably.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 Numbers and mapping from the open access research dataset DOI:10.4121/19361018

2 E.g. in the Netherlands: Oost NL, REWIN, Ontwikkelmaatschappij Midden-Limburg and Midpoint Brabant.

3 Dutch logistics lobby is performed by Transport & Logistiek Nederland (TLN) and Evo-fenedex, joined in the Logistiek Alliantie. The sector is promoted abroad by the Netherlands International Distribution Council.

4 Logistics real estate in Dutch provinces Noord-Brabant and Limburg is currently financed for 95% by foreign investors, while 75% of the buildings have a lease shorter than 5 years, and 50% are leased to logistics service providers with frequently changing client portfolios (Bak Citation2021).

5 Developers active in Europe have portfolios including millions of sqm in logistic space and land banks of hundreds of hectares (https://www.prologis.nl/over-ons, https://heylenwarehouses.com, https://www.vgpparks.eu/nl/properties/). Dutch logistics real estate development profits are comparable per sqm to the London office market (Trappenburg in Financieel Dagblad, 2019).

6 Logistics development in the US has recently shifted to smaller DCs near consumers in (sub)urban sites. This trend has only recently begun in Europe.

7 Spatial quality plans explained on https://iplo.nl/thema/ruimtelijke-ontwikkelingen/bijzondere-onderwerpen/beeldkwaliteitsplan/. The only two Logistics developments with a Q-team are the ones near the airports of Schiphol and Eindhoven.

8 Repository DOI:10.4121/14717058

9 MS Teams and Amberscript

10 See repository

12 Described in the regional and co-municipal visions, masterplan and landscape plan (Greenport Venlo & Studio Marco Vermeulen Citation2009; BRO Citation2010; Heusschen Copier Citation2010; Venlo Citation2012; Limburg Province Citation2014).

13 Described in masterplan, landscape plan and the national Greenports implementation (Government of the Netherlands Citation2010).

14 In 2021, a large agro-logistics company was landed in Trade Port Noord. Similar to the fashion DCs, the agro-logistic company's arrival was criticized in local politics for the dependence on migrant workers.

15 DSV is present in Venlo since around 1900, in the form of transport company Frans Maas, acquired by DSV in 2006.

16 Described in the land-use and spatial quality plans (Roosendaal Citation2012; Dhondt Citation2013; Roosendaal & Halderberge Citation2013; Halderberge Citation2017).

18 In our interviews as well as newspapers: https://www.ad.nl/binnenland/hoe-ze-roosendaal-tegenwoordig-noemen-dozendaal~a7f73b05/

19 The Greenport Venlo Development Company, although owned 100% by local governments, is not subject to the Public Administration Transparency Act (WOB).

20 In 2020, a typical DC of 100.000 sqm in the Netherlands has a land and construction cost of around 100 million, and a real estate value of 150 million on the balance sheet.

21 Dutch VAT legislation allows for an attractive delay for re-export and e-commerce: tax is not due until goods are exported from the warehouse. In contrast with Belgium, Dutch DCs can operate 24/7.

22 Recently, large logistics developments on brownfield sites have also been criticized, for competing over industrial land with small local companies.

23 Especially closed-end fund investors (not registered at the stock market) have a strong influence on DC location choice. They prefer larger clusters in the East-Southeast corridor of the Netherlands, within reach of 150 million consumers in a 500 km radius.

24 Sometimes as their personal opinion rather than an official company statement.

References

- Adams, D., L. Russel, and C. Taylor-Russell. 1994. Land for Industrial Development. 1st ed. London: Chapman & Hall.

- Aljohani, K., and R. Thompson. 2016. “Impacts of Logistics Sprawl on the Urban Environment and Logistics: Taxonomy and Review of Literature.” Journal of Transport Geography 57: 255–263. doi:10.1016/j.jtrangeo.2016.08.009.

- Andreoli, D., A. Goodchild, and K. Vitasek. 2010. “The Rise of Mega Distribution Centers and the Impact on Logistical Uncertainty.” Transportation Letters 2 (2): 75–88. doi:10.3328/TL.2010.02.02.75-88.

- Bak, R. 2020. Logistiek vastgoed in cijfers 2020.

- Bak, R. 2021. Logistiek vastgoed in cijfers 2021 [Logistics Real Estate in Figures]. NVM Business. https://www.nvm.nl/media/qkvlr155/logistiek-vastgoed-in-cijfers-2021.pdf

- Bertaud, A. 2018. Order Without Design—How Markets Shape Cities. Cambridge: MIT Press.

- BRO. 2010. Structuurvisie Bedrijventerrein Trade Port Noord. Venlo.

- Bulwiengesa. 2020. Logistics and Real Estate. Bulwiengesa. logistik-und-immobilien.de%0AScientific.

- BZK. 2020. National Strategy on Spatial Planning and the Environment. Ministry of the Interior and Kingdom Relations. https://iplo.nl/publish/pages/187168/national-strategy-on-spatial-planning-and-the-environment.pdf

- CRa, Rademacher & De Vries, & Stec Groep. 2019. (X)XL-verdozing [(X)XL Boxification] (Board of government advisors (Ed.)). CRa.

- Danyluk, M. 2019. “Fungible Space: Competition and Volatility in the Global Logistics Network.” International Journal of Urban and Regional Research 43 (1): 94–111. doi:10.1111/1468-2427.12675.

- Dhondt. 2013. Land-use plan Borchwerff II. NL.IMRO.1655.BP9004-C001

- Easterling, K. 2014. Extrastatecraft: The Power of Infrastructure Space. London: Verso.

- Edmondson, D., F. Kern, and K. Rogge. 2018. “The Co-evolution of Policy Mixes and Socio-Technical Systems: Towards a Conceptual Framework of Policy Mix Feedback in Sustainability Transitions.” Research Policy 48 (10): 103555. doi:10.1016/j.respol.2018.03.010.

- Flämig, H., and M. Hesse. 2011. “Placing Dryports: Port Regionalization as a Planning Challenge—The Case of Hamburg, Germany, and the Süderelbe.” Research in Transportation Economics 33 (1): 42–50. doi:10.1016/j.retrec.2011.08.005.

- Frejlachová, K., M. Pazdera, T. Riha, and M. Spicák, eds. 2020. Steel Cities: The Architecture of Logistics in Central and Eastern Europe. Zürich: Park Books.

- Government of the Netherlands. 2010. Nederland Verandert! Klavertje 4 (Greenport Venlo). The Hague: Government of the Netherlands.

- Greenport Venlo, & Studio Marco Vermeulen. 2009. Masterplan Gebiedsontwikkeling Klavertje 4 / Greenport Venlo.

- Halderberge. 2017. Welstandsnota Halderberge 2017. Halderberge.

- Hall, P. V., and M. Hesse, eds. 2012. Cities Regions and Flows. Routledge. doi:10.4324/9780203106143.

- Healey, P. 1999. “Sites, Jobs and Portfolios: Economic Development Discourses in the Planning System.” Urban Studies 36 (1): 27–42. doi:10.1080/0042098993718.

- Heitz, A., L. Dablanc, J. Olsson, I. Sanchez-Diaz, and J. Woxenius. 2018. “Spatial Patterns of Logistics Facilities in Gothenburg, Sweden.” Journal of Transport Geography, March, 0–1. doi:10.1016/j.jtrangeo.2018.03.005.

- Heitz, A., L. Dablanc, and L. Tavasszy. 2017. “Logistics Sprawl in Monocentric and Polycentric Metropolitan Areas: The Cases of Paris, France, and the Randstad, the Netherlands.” Region 4 (1): 93–107. doi:10.18335/region.v4i1.158.

- Hesse, M. 2004. “Land for Logistics: Locational Dynamics, Real Estate Markets and Political Regulation of Regional Distribution.” Tijdschrift Voor Economische En Sociale Geografie 95 (2): 162–173. doi:10.1111/j.0040-747X.2004.t01-1-00298.x.

- Hesse, M. 2020. “Logistics: Situating Flows in a Spatial Context.” Geography Compass 14 (7): 1–15. doi:10.1111/gec3.12492.

- Hesse, M., and J. Rodrigue. 2004. “The Transport Geography of Logistics and Freight Distribution.” Journal of Transport Geography 12 (3): 171–184. doi:10.1016/j.jtrangeo.2003.12.004.

- Heurkens, E., D. Adams, and F. Hobma. 2015. “Planners as Market Actors: The Role of Local Planning Authorities in the UK’s Urban Regeneration Practice.” Town Planning Review 86 (6): 625–650. doi:10.3828/tpr.2015.37.

- Heusschen Copier. 2010. Landschapsplan Klavertje 4. Venlo: Greenport Venlo.

- Higgs, R. 2018. “Principal-Agent Theory and Representative Government.” Independent Review 22 (3): 479–480.

- Hines, T. 2013. Supply Chain Strategies: Customer-Driven and Customer-Focused. London: Routledge.

- Hough, M. 1991. Out of Place: Restoring Identity To the Regional Landscape. Yale University Press. doi:10.3368/lj.10.2.194.

- Krzysztofik, R., I. Kantor-Pietraga, T. Spórna, W. Dragan, and V. Mihaylov. 2019. “Beyond ‘Logistics Sprawl’ and ‘Logistics Anti-Sprawl’. Case of the Katowice Region, Poland.” European Planning Studies 27 (8): 1646–1660. doi:10.1080/09654313.2019.1598940.

- Kuipers, B., L. Van der Lugt, W. Jacobs, M. Streng, M. Jansen, and J. Van Haaren. 2018. Het Rotterdam Effect—De Impact van Mainport Rotterdam op de Nederlandse Economie [The Impact of Mainport Rotterdam on the Dutch Economy]. Erasmus Centre for Urban, Port and Transport Economics.

- LeCavallier, J. 2016. The Rule of Logistics—Walmart and the Architecture of Fulfillment. Minneapolis: University of Chicago Press.

- Lehnerer, A. 2009. Grand Urban Rules. Rotterdam: Nai010.

- Limburg Province. 2014. Provinciaal Omgevingsplan Limburg. Maastricht: Provincie Limburg.

- Louw, E. 2009. Planning van Bedrijventerreinen. The Hague: Sdu Uitgevers.

- Nefs, M., W. Zonneveld, and P. Gerretsen. 2022. “The Dutch ‘Gateway to Europe’ Spatial Policy Narrative, 1980–2020: A Systematic Review.” Planning Perspectives, Forthcoming. doi:10.1080/02665433.2022.2053879.

- North, D. 1987. “Institutions, Transaction Costs and Economic Growth.” Economic Inquiry 25 (3): 419–428. doi:10.1111/j.1465-7295.1987.tb00750.x.

- OECD. 2014. “The Competitiveness of Global Port-Cities.” In The Competitiveness of Global Port-Cities. Paris: OECD Publishing. doi:10.1787/9789264205277-en.

- Onstein, A., L. Tavasszy, and D. Van Damme. 2019. “Factors Determining Distribution Structure Decisions in Logistics: A Literature Review and Research Agenda.” Transport Reviews 39 (2): 243–260. doi:10.1080/01441647.2018.1459929.

- Panteia, AT Osborne, Defacto, & Topcorridors. 2019. Goederenvervoer- corridors Oost en Zuidoost [Freight Corridors East and Southeast]. Topcorridors. http://d.efac.to/Tussenrapportage_GVC_Handelingsperspectief_Defacto_webversie.pdf

- PBL. 2019. [Care for Landscape] Zorg Voor Landschap. PBL-publicatienummer: 3346

- Raimbault, N. 2021. “Outer-Suburban Politics and the Financialisation of the Logistics Real Estate Industry: The Emergence of Financialised Coalitions in the Paris Region.” Urban Studies, February 2020, 004209802110144. doi:10.1177/00420980211014452.

- Raimbault, N., W. Jacobs, and F. Van Dongen. 2016. “Port Regionalisation from a Relational Perspective: The Rise of Venlo as Dutch International Logistics Hub.” Tijdschrift Voor Economische En Sociale Geografie 107 (1): 16–32. doi:10.1111/tesg.12134.

- Rli. 2016. Mainports Voorbij [Beyond Mainports]. Raad voor de Leefomgeving en Infrastructuur. http://www.rli.nl/sites/default/files/advies_mainports_voorbij_voor_website.pdf

- Roosendaal. 2012. Ontwerp-Structuurvisie Roosendaal 2025. Roosendaal: Roosendaal municipality.

- Roosendaal, & Halderberge. 2013. Bedrijvenpark Borchwerf. Roosendaal: Municipalities Roosendaal and Halderberge.

- Santos, M. 2006. “A Natureza do Espaço. Técnica e tempo, razão e emoção.” In GEOgraphia (Vol. 1, Issue 1). edusp. doi:10.22409/geographia1999.v1i1.a13370.

- Scharpf, F. 1997. Games Real Actors Play – Actor-Centered Institutionalism in Policy Research. London: Routledge.

- Stec Group. 2020. Ruimtelijke sturing op knooppunten [Spatial Steering on Logistic Hubs]. Edited by W. Eringfeld, E. Geuting, and H. Ploem. Arnhem: Stec Groep.

- Strale, M. 2020. “Logistics Sprawl in the Brussels Metropolitan Area: Toward a Socio-Geographic Typology.” Journal of Transport Geography 88 (October 2018): 102372. doi:10.1016/j.jtrangeo.2018.12.009.

- Van Assen, S., and J. Van Campen. 2014. Q-factor. Wageningen: Blauwdruk.

- Venlo. 2012. Structuurvisie Klavertje 4-gebied: Uitwerking werklandschap. NL.IMRO.0983.SV201201KLAVERTJE4-VA01

- Verhetsel, A., R. Kessels, P. Goos, T. Zijlstra, N. Blomme, and J. Cant. 2015. “Location of Logistics Companies: A Stated Preference Study to Disentangle the Impact of Accessibility.” Journal of Transport Geography 42: 110–121. doi:10.1016/j.jtrangeo.2014.12.002.

- Waldheim, C., and A. Berger. 2008. “Logistics Landscape.” Landscape Journal 27: 219–246. doi:10.3368/lj.27.2.219.

- Williamson, O. 1998. “Transaction Cost Economics: How It Works; Where It Is Headed.” Economist 146 (1): 23–58. doi:10.1023/A:1003263908567.

- Witte, P., B. Wiegmans, C. Braun, and T. Spit. 2016. “Weakest Link or Strongest Node? Comparing Governance Strategies for Inland Ports in Transnational European Corridors.” Research in Transportation Business and Management 19: 97–105. doi:10.1016/j.rtbm.2016.03.003.

- Yuan, Q. 2019. “Planning Matters: Institutional Perspectives on Warehousing Development and Mitigating Its Negative Impacts.” Journal of the American Planning Association 85 (4): 525–543. doi:10.1080/01944363.2019.1645614.