ABSTRACT

The oil and gas industry is expected to develop and restructure into a sustainable energy industry. This in-depth case study investigates how business model innovation can contribute to industrial restructuring. Our findings imply that, while there is no ‘one size fits all’ business model, most oil and gas companies will need to innovate their customer segments, value propositions, key resources, key partners and cost structures to succeed. The oil and gas industry landscape significantly influences the need for adapting the business model to changing market forces, industry forces, key trends, and macroeconomic forces pushing for sustainable change, the emergence of new technologies and markets, and changes in market conditions. Our findings demonstrate that the need for change differs from the willingness to change. The production companies’ willingness to change is currently low as production is still highly profitable, while the supplier companies’ willingness is high because it is not profitable to expand. Oil and gas companies will face several internal barriers in the process, including challenges with the dominant logic of the company, deficient managerial knowledge, the uncertainty and complexity of new business models and limited business model routines or processes.

1. Introduction

The world faces massive challenges related to global warming and climate change. The urgency of energy transition is ‘further underscored by the evidence-based suggestion that humanity risks crossing critical tipping points of irreversible climate change because of growing emissions’ (Abraham-Dukuma Citation2021, 1). Sustainable ways of carrying out business are needed especially by the oil and gas industry, as it is this industry's contribution to climate change that necessitates energy transition (Abraham-Dukuma Citation2021; Boon Citation2019; Morgunova Citation2021). The Paris Agreement (UNFCCC) aims to ensure that all countries contribute to reducing climate change and greenhouse gases, with each involved country creating a national plan to reduce its greenhouse emissions (Horowitz Citation2016). In this vein, the EU Taxonomy Regulation is developed to meet the EU's climate and energy targets for 2030 and to reach the objectives of the European Green Deal (European Commission Citation2020). This can, potentially, force restructuring within the industry. However, despite the modern energy system being identified as a main cause of the problem and necessarily the locus of solution, the actors involved prove resistant to change (Geels Citation2014; Morgunova Citation2021).

Consequently, implementing the adjustments necessary to meet regulations and to achieve a massive cut in greenhouse gas emissions is likely to result in three different scenarios for the Norwegian oil and gas industry: (1) a more environmentally friendly production of oil and gas where companies comply with the sustainability goals, (2) restructuring into sustainable industries, or (3) oil and gas companies failing to adhere and make modifications, resulting in bankruptcies.

Innovation is a means to economic growth, sustainable development, technological development, and industrial restructuring (Bocken et al. Citation2014; Romer Citation1986; Maradana et al. Citation2017) and a central element towards the sustainable restructuring of the Norwegian oil and gas industry. To succeed, however, organizations must change more than just their products and services. Business model innovation can be crucial in a successful restructuring process, through several areas including customers, offerings, infrastructure and finance – change here will strengthen their strategic position. Business model innovation involves making simultaneous changes to an organization's value proposition and its underlying operating model to acquire a strategic competitive advantage (Osterwalder and Pigneur Citation2010). Firms can explore new innovations resulting from adapting their current business innovation model towards a particular archetype (Bocken et al. Citation2014), with the premise that changes in business models are crucial to successfully enable sustainable innovations. The ‘sustainable business model innovation’ concept emphasizes environmental and social value creation; see, for example, Bocken and Geradts Citation2020 and the review by Geissdoerfer, Doroteva, and Evans (Citation2018). However, little is known about adopting business innovation models, and a lack of case studies makes it challenging for firms to relate (Evans et al. Citation2017).

On this basis, we aim to investigate: how can business model innovation contribute to a restructuring of the Norwegian oil and gas industry to comply with Norway's climate ambitions for 2030 and 2050? We develop three sub-questions targeting decision aspects within the main research question: (1) Which parts of the business model should be emphasized the most when restructuring? (2) What external challenges do oil and gas companies face that may influence business model innovation? and (3) What are the internal barriers that oil and gas companies face in the process of change?

2. Theoretical framework and development of sub-questions

2.1. Business model innovation

Innovative organizations continuously learn, adapt to internal and external changes, and succeed in innovating in their environments (Schumpeter Citation1980; Teece, Peteraf, and Leih Citation2016). Efficacious businesses are often characterized by their ability to improve and nurture existing resources to maintain a strong strategic position while simultaneously exploring new opportunities, resulting in a more lasting competitive advantage (March Citation1991; Tushman and O’Reilly Citation1997). Business model innovation can play a crucial role in creating these long-lasting competitive advantages and enhance firm performance (Cucculelli & Bettinelli, Citation2015). However, Tidd and Bessant (Citation2014) argue that business model innovations are one of the most powerful challenges to already established players in an industry. This challenge to established inertia is further discussed in this article, but first, we establish what business model innovation can entail.

Business model innovation can be defined as making simultaneous changes to various aspects of a business at the same time to create long-term, sustainable, competitive advantages and to provide a higher return on invested capital (Boer and During Citation2001; Keeley et al. Citation2013). An organization's business model should describe the four fundamental areas of its business: their target customer, what they offer to the customer, how the value proposition is created, and why it is profitable (Foss and Saebi Citation2015; Keeley et al. Citation2013; Osterwalder and Pigneur Citation2010; Tidd and Bessant Citation2014) (for a recent review and overview of definitions, see Geissdoerfer, Doroteva, and Evans Citation2018). However, a weakness within business model innovation is that a lack of clarity and consistency could hamper the understanding and utilization of the construct of business model innovation (Evans et al., Citation2017, see also discussions in Joyce and Paquin, Citation2016, 1475–1746). The ‘Ten types of innovation’ framework and the ‘Business Model Canvas’ were created to help organizations evaluate and improve their business model and to realize that innovation entails more than merely creating new or improving existing products and services (Keeley et al. Citation2013; Osterwalder and Pigneur Citation2010). The frameworks cover the fundamental parts of any business, beginning with the customer interface comprising the customer segments, channels and customer relationships. The second aspect is the products and services that the business offers to a market, known as offerings or value propositions, and the third is the infrastructure and configuration surrounding the business's offerings, including its key resources, activities and partnerships. The last aspect is the financial elements involving the cost structure and revenue streams, also known as the profit model.

The above forms the basis for investigating which parts of the business model should be emphasized the most in the restructuring. [sub-question 1]

2.2. Business model environment

It is widely recognized that all business models are influenced by multiple external factors (Fagerberg, Mowery, and Nelson Citation2006; March Citation1991; Osterwalder and Pigneur Citation2010; Porter Citation1998; Schumpeter Citation1980; Shepard Citation1967; Tidd and Bessant Citation2014). A comprehensive understanding of the environmental factors is essential.

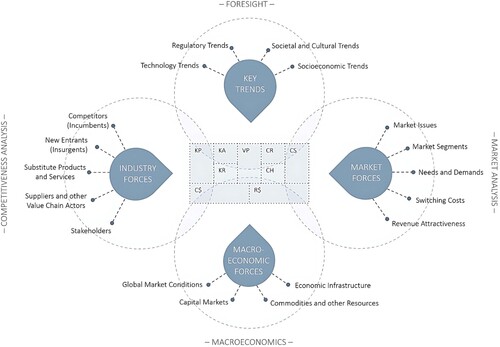

Osterwalder and Pigneur (Citation2010, 201) created a framework to illustrate how context, design drivers, and constraints influence the generation and development of business models. All businesses are influenced by market, industry and macroeconomic forces and key trends. The framework requires that businesses begin with conduct a market analysis to identify how they are influenced by market forces. The needs and demands of customers constantly change, and, as marketplaces evolve, the need for new ways to address markets becomes apparent. To stay competitive, organizations should analyse their own and new markets to identify market issues and segments, needs and demands, switching costs, and revenue attractiveness (Osterwalder and Pigneur Citation2010, 202). Second, they should conduct a competitiveness analysis to identify how suppliers, stakeholders, competitors, new entrants, and substitute products and services influence their strategic position (Osterwalder and Pigneur Citation2010, 204; see also Porter Citation1998). The purpose is to find opportunities for growth by identifying the strengths and weaknesses of competitors and recognizing how they can benefit the organization. Recognizing key trends can be crucial. Companies should look for current trends in technological development, regulations, social and cultural settings, and changes in socioeconomic tendencies, as they can threaten an existing business model or enable it to further improve and evolve (Osterwalder and Pigneur Citation2010, 206). Business model innovation can also be affected by macroeconomic forces including global market conditions, capital markets, commodities and other resources, and economic infrastructure (Osterwalder and Pigneur Citation2010, 208).

The above forms the basis for investigating which external challenges oil and gas companies face that may influence business model innovation. [sub-question 2]

2.3. The process of business model innovation

Most companies do not attain a secure competitive position based solely on their innovation activities like exclusive technology, intellectual property rights, and unique assets. These companies, therefore, should innovate their business model radically to secure competitive advantage (Taran, Boer, and Lindgren Citation2015, 302). By incorporating business model innovation, organizations can achieve benefits that are challenging for competitors to imitate (Björkdahl and Holmén Citation2013; Chesbrough Citation2010; Taran, Boer, and Lindgren Citation2015). This section presents how the process of business model innovation can be conducted, including an explanation of the different internal barriers companies may face during the process (see a recent review of the business model innovation process in Andreini et al. (Citation2022).

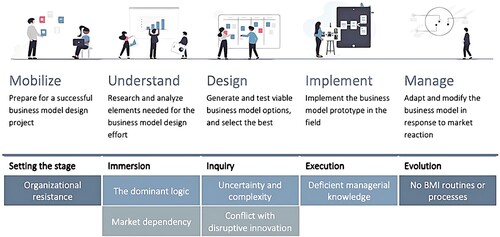

Osterwalder and Pigneur (Citation2010) propose a five-phase business model design process framework that identifies and illustrates the defined stages, processes, and activities, and can guide organizations by mapping their fundamental activities and potential challenges. The mobilization phase includes preparation for the new design: organizations form the purpose, objectives, and scope of the business model. The second phase involves understanding the context in which the business model will evolve, including analyzing environmental parameters such as potential customers and competitors. Third, the organization must generate and test viable options to determine the most appropriate business model. The fourth phase involves communication and execution by defining milestones and related projects, organizing legal structures, and preparing a specific budget and project roadmap. Lastly, business model innovation is an iterative process; the activities continue after initial implementation. Activities in the last phase comprise evaluation, managing synergies or conflicts between models, aligning the business model throughout the organization, and identifying how the business model can be influenced over the long term (Osterwalder and Pigneur Citation2010, 258).

Identifying barriers to achieving business model innovation is increasingly important, as research shows that most companies are not able to initiate nor achieve it (Björkdahl & Holmén, Citation2013; Chesbrough Citation2010; Foss and Saebi Citation2016). The framework addresses documented, current barriers of business model innovation and the key challenges (Björkdahl and Holmén Citation2013; Chesbrough Citation2010; Foss and Saebi Citation2015, Citation2016; Taran, Boer, and Lindgren Citation2015). Foss and Saebi (Citation2016) argue for five key challenges. The first is a cognitive barrier described as ‘the dominant logic’ (see Pralahad and Bettis Citation2000): managers often reject information that challenges their traditional ways of thinking and the prevailing knowledge within the firm (Foss and Saebi Citation2016). In certain situations, this can be perceived as positive as it reduces the costs of handling new information and allows for stability (for stakeholders). However, it also leads to the rejection of new information (Foss and Saebi Citation2016) which could be important for firms’ performance. Second, deficient managerial knowledge refers to managers lacking the ability to understand, evaluate, and experiment with the organization's business model (Björkdahl and Holmén Citation2013, 219). Third, the uncertainty and complexity of changing the business model can result in the current business model never being challenged on its competitive position or within new markets (Foss and Saebi Citation2016). Fourth, the challenges of not having business model innovation routines or processes are called ‘organizational barriers’ (Björkdahl and Holmén Citation2013, 221), and involve hindrance from organizational resistance and lack of motivation (Foss and Saebi Citation2016). For example, a new business model needed to exploit disruptive technology may conflict with the organization's existing business model (Chesbrough Citation2010, 358). Lastly, market dependency relates to how organizations are dependent on changes being implemented by other actors in the industry before they consider changing their own business model (Björkdahl and Holmén Citation2013, 221).

This forms the basis of investigating what internal barriers oil and gas companies face in the process of change. [sub-question 3]

3. Contextual background and methodology

3.1. Industrial restructuring and industry status

A substantial industry emerged after Norway discovered oil in 1969 (see Solheim and Tveterås Citation2017 and Engen Citation2009 for an overview of the development of the Norwegian oil and gas industry). In Norway, as in other countries, ‘the pressure to respond to sustainability concerns is increasing’ (Joyce and Paquin, Citation2016, 1474). It is clear that ‘business-as-usual’ cannot be sustained, necessitating a substantial shift in the purpose of business and all relevant aspects therein to support the much-needed transition (Bocken, Schuit, and Kraaijenhagen Citation2018, 79). At such, in recent years, the Norwegian economy has faced major restructuring, driven by digitalization and green restructuring, forcing the oil and gas companies to alter their business models to stay competitive. The current ‘modus operandi’ of the oil and gas industry is not compatible with the changes needed to comply with the Paris agreement, leading to what Halttunen, Slade and Staffell (Citation2022) argue is a fundamental tension between adhering to shareholder expectations (which involves engaging in activities that contribute to climate change) on the one hand, versus the pressure to contribute to climate change mitigation. Restructuring, therefore, holds potential environmental and financial consequences when renewing ‘economic structures by nurturing new green industries’ (Trippl et al. Citation2020, 189). In line with this, the changes currently undertaken by the industry are made visible through diversification into activities that make use of already existing competencies. One example of such, are shifts into related technological fields for which firms can use their already existing competences, such as employing their technology into other industries. For example, 60% of Norwegian oil and gas companies predict increased growth and turnover in the offshore wind industry towards 2023 (Menon Economics Citation2020). However, only 10% of the companies have revenues related to carbon capture and storage (CCS hereafter) as it is still in the development phase, and its future depends on cost, competing technologies, industrial sectors, and market developments. In addition, 36% of companies expect increased growth in hydrogen towards 2023.

With that inertia in mind, Ihlen (Citation2009) put the Norwegian oil and gas industry under a spotlight with an analysis of its rhetoric, arguing that the industry is ‘overselling its green credentials’ (Ihlen Citation2009; see also Halttunen, Slade, and Staffell, Citation2022). Deegan et al. (Citation2022), studying regional innovation systems and entrepreneurial discovery processes on the west coast of Norway, found stakeholders in Stavanger emphasizing that the oil and gas industry will remain the largest component of the future regional economy. As an example, one of their respondents argued: ‘We have a social responsibility to continue to deliver green oil. We can say it like that, green oil and gas’. Deegan et al. (Citation2022) moreover discusses the ‘rebranding’ attempt from ‘Oil Capital’ in Norway to ‘Energy Capital’. This falls in line with an observed trend: several oil companies have, in recent years, made public statements of investments in clean energy (Halttunen, Slade, and Stafell, Citation2022).

There is also an interesting discussion under way highlighting the significance of the oil and gas industry in the transition, on the one hand highlighting the crucial role played by the oil companies (keeping their power), and on the other hand, arguments (such as Newell, Geels, and Sovacool Citation2022) that the fossil fuel industry should not play an active role as it will further ‘entrench existing inequalities’ (see Halttunen, Slade, and Stafell, Citation2022).

Furthermore, an important point worth mentioning herein is the globalizing knowledge economy which embeds innovation processes across distant places. At such, Binz and Truffer (Citation2017, 1284) highlights that ‘the increased spatial complexity of innovation processes raises the question whether a territorial (local, regional, or national) system perspective is still a valid one as system boundaries get increasingly blurred and porous’. Moreover, that ‘technological innovation increasingly depends on multiscalar actor networks and institutions’ (Binz and Truffer Citation2021, 397), and at such Binz and Truffer (Citation2021, 397) call for an increased focus on Global Innovation Systems enabling researchers to capture ‘the emergence of system resources across spatial scales’. One example would be that the local industry, such as the Norwegian oil and gas industry to ‘access globally available innovative ideas and optimize their (economic/social/environmental) performance in demanding local application’ (Binz and Truffer Citation2021, 407), a trait also highlighted in Deegan et al. (Citation2022) emphasizing that the Stavanger region share similarities with a specialized and regionalized national regional innovation system. These developments require further studies potentially extended through disentangling the microfoundations of key factors and mechanisms within business model innovation allowing for distinction and identification of key actors involved (see Section 5.3).

3.2. Research strategy

To obtain data and insights into how business model innovation can contribute to industrial restructuring, we have scanned literature about industrial restructuring as a foundation for our in-depth case study. We collected qualitative data through semi-structured interviews with 10 companies and cluster networks in the oil and gas, offshore wind, hydrogen, and CCS value chains (see Appendix A1 for participant profiles). Our sample represents both the exploration and production, and the supply sides of the industry.

The interviews were carried out during the spring of 2021 and lasted 45–60 minutes (median length 55 minutes). As presented in Appendix A2, the interview guide comprised a total of 18 questions. The interview guide was structured around the following topics: (1) background information, (2) business model innovation, (3) business model environment, (4) the process of change, and (5) EU taxonomy and the oil price. The elements of the interview guide were derived from the existing theory presented in the framework reviewed above.

The interviews were recorded and transcribed, and the transcripts analysed thematically. Using NVivo software, we coded the interviews and looked for aspects related to the current situation regarding the restructuring of the industry, current business models, external influences, and potential challenges in the process of change (as per constructive thematic analysis identifying ‘meaning patterns’ in the data, see Braun and Clarke Citation2006; Solheim and Moss Citation2021). Emphasis was put on statements, examples, and text on how business model innovation can contribute to restructuring the Norwegian oil and gas industry. As per Appendix A3, we compiled illustrative interview quotes corresponding to the different themes discussed in the results section below. For transparency, we have attributed statements to the interviewees, using the participant numbering code in Appendix A1.

4. Results and discussion

4.1. Business models

The following discussion relates to the first sub-question and presents which parts of the business model should be emphasized the most during restructuring. Despite similarities between the oil-and-gas and renewable energy industries, transition challenges existing business models. Business model innovation helps the businesses to redefine who their target customer will be, what they should offer to their customers, how they will create their value proposition, and how to make money from it. As there is no perfect business model that can be duplicated from one company to another, or even between industries, our findings suggest that oil and gas companies transitioning to new markets need to modify several areas of their business models. The areas highlighted by the participants as the most critical to succeeding in new markets include re-evaluation of their target customer segments and value propositions, and exploration of alternatives for new key resources, key partners, and cost structures.

4.1.1. Customer segments

One business model element that needs attention is the company's customer segments. Several oil and gas suppliers have already found new customers in related markets due to the dwindling number of traditional oil and gas customers. This has resulted in higher competition on the supply side and an increased need and interest for new markets and sustainable industries. However, Norway is quite late in entering a number of these markets (Participant 6, 2021) which can be challenging for the oil and gas companies that want to evolve. Some markets like offshore wind, CCS, and hydrogen are already dominated by large foreign suppliers who have a competitive position that is difficult to penetrate due to economies of scale (Participant 6, 2021). Thus, while taking measures to grow in other industries, some companies will maintain their position in the oil and gas industry and simultaneously serve different customer segments within the oil and gas and renewable energy industries. Different customer segments have different needs, so the oil and gas companies will experience substantial differences between their current and new customer segments. A diversified customer business model will be required to meet the customer segments’ various needs and challenges.

4.1.2. Value propositions

The need for sustainable solutions, requires oil and gas companies to solve new types of problems, necessitating new value propositions. Our findings suggest that oil and gas companies rarely make significant changes to what they offer the market, but their products and services have been improved with a focus on zero-emission solutions (Participants 1 and 2, 2021). It may not be necessary to change the offering but rather to focus on decarbonized solutions with reduced CO2e emissions as customers are willing to pay more for products with a low CO2 footprint (Participants 7 and 10, 2021). Moreover, there is already a greater focus on software- and service-based solutions to increase the efficiency of existing equipment and physical machines (Participants 3 and 6, 2021). This trend might be equally important in offshore wind, hydrogen, and CCS. Combining equipment and physical machines with an offering that includes service, updates, and maintenance can increase the value created. Integrated offerings that combine otherwise separate components into a complete experience may be an important part of the industrial restructuring (as echoed in the literature in economic geography emphasizing that restructuring and identifying potential future economic opportunities are contingent upon resource bases already in place, and fostered through historically developed capabilities (see Boschma and Martin Citation2010; and Frenken and Boschma Citation2007 on re-combinations of knowledge and resources). As the offshore wind, hydrogen, and CCS industries already have some incumbent companies with strong market positions, its existing foundations can be a way for Norwegian oil and gas companies to enter the market. Moreover, rebranding can align the company's new set of values and offerings and reduce their associations with the negative impacts of the oil and gas industry.

4.1.3. Key resources

Companies require key resources and assets to offer and deliver the previously described elements. Our findings suggest that transferable knowledge and experience in the oil and gas industry can be of value in related industries like offshore wind, hydrogen, and CCS (Participants 1 and 10, 2021). The oil and gas companies have already played a central role in transforming the maritime industry as they have relevant technical and business expertise and experience running large projects. However, new markets and industries will necessitate acquiring new industry-specific skills and competencies, making the companies’ key resources an important area of innovation. This may particularly involve intellectual resources as many companies focus on developing new technologies and solutions, resulting in proprietary knowledge requiring patents and copyrights.

Additionally, oil and gas companies transitioning to renewable energy will likely rely heavily on capital-intensive physical resources. High costs are associated with testing technology on a full scale, and the possibility of a return on environmental technology projects is associated with high risk. Our findings imply that it is crucial that companies can profit from transitioning to new renewable industries; if not, they will resist change One of the main challenges is facilitating initiatives that make it financially possible to enter new industries, as companies depend on earnings and a stable bottom line. To ensure sustainable growth and innovation, suitable financial government incentives must be in place for oil and gas companies to have viable business models (Participant 1, 2021). This is in line with past research, such as Steen (Citation2016, 1609), emphasizing that

although new technologies may be promising, they compete with both extant technologies and other new technologies and therefore often fail to survive past infancy. In short, the selection environment is strongly shaped by mature technologies and the economic practices, actors, institutions and investments linked to these.

4.1.4. Key partnerships

Oil and gas companies entering related industries like offshore wind, hydrogen, and CCS will have to form alliances and partnerships with companies with complementary skills and competencies (as per Frenken and Boschma Citation2007). This would help oil and gas companies to optimize their business models, obtain economies of scale, reduce risk, and acquire valuable resources. Moreover, more players will be involved in the value chain of renewable energy industries (Participants 1 and 10, 2021). These players offer more input into decisions about customizing offerings to customer needs, but they also require different types of partnerships. Furthermore, the shift from product-only to product-and-services business models will drive increased demand for partners with software development competence, and a decreased demand for traditional suppliers and factories. Some oil and gas companies belong to constellations that have worked together for a long time and that have changed and adapted in the same manner (Participants 5 and 7, 2021). While there may be benefits of continuing such cooperation into new markets, companies should also widen their horizons and explore new opportunities with other partners.

4.1.5. Cost structure

Finally, the business model elements result in the company's cost structure, which includes all costs incurred in operating a business. When transitioning from oil and gas to renewable energy industries, companies must adapt their cost level to a market with lower margins than what they are used to (Participants 1 and 10, 2021) (see also findings in Morgunova Citation2021). There is ‘a constant pressure to drive costs down to remain competitive regardless of the oil price’ (Participant 2, 2021), and we argue that this will likely also entail a cost-driven business model in new industries where the focus is minimizing costs wherever possible. Our findings suggest that oil and gas companies have different measures of what is considered critical – they will only cut costs where they can tolerate fault in situations, and such situations will differ widely between the industries mentioned (Participant 9, 2021). Moreover, offshore wind and hydrogen are four times more expensive than other energy sources (Participant 7, 2021). Offshore wind will, for instance, require serial production; thus, succeeding with robotization and digitalization of production processes is crucial to ensuring a viable cost level. While the ideal profit model will vary widely by context and industries, innovating the cost structure may be key for oil and gas companies as new entrants to attain a market share in industries like offshore wind, CCS, and hydrogen.

4.2. The oil and gas industry landscape

Shifts in industrial trajectories are becoming apparent as oil and gas companies transition to new energies like offshore wind, hydrogen, and CCS. Our findings imply that oil and gas companies will operate in several different markets simultaneously, which will affect the industry landscape. As companies are influenced by their environment, the following discussion relates to the second sub-question and presents the external challenges that may influence business model innovation. Different market forces, industry forces, key trends, and macroeconomic forces affect the Norwegian oil and gas industry landscape, and our most prominent findings are illustrated in below.

Figure 1. The oil and gas industry landscape influencing business model innovation. Business models consist of nine building blocks (as depicted in the middle of the figure): key partners (KP), key activities (KA), key resources (KR), value proposition (VP), customer relationships (CR), customer segments (CS), channels (CH), cost structure (C$), and revenue streams (R$). Author's own compilation based on Osterwalder and Pigneur Citation2010, 201.

4.2.1. Market forces

Companies in the oil and gas industry are highly affected by market issues, market segments, needs, demands, switching costs, and revenue attractiveness. The most prominent market issue is related to the different sustainability goals and climate ambitions, as oil and gas production is more expensive for Norwegian companies than in other countries and, hence, influences their profitability. Moreover, there is stronger demand for sustainable solutions, with emphasis shifting from offering physical equipment to an increased focus on software- and service-based solutions (Participants 3 and 6, 2021). Due to the strong global competition and overcapacity in the oil and gas supplier industry, there is high pressure on the oil and gas supply side (Participant 7, 2021), resulting in companies’ investing in new energies like offshore wind, hydrogen, and CCS. However, there is still a great demand for oil and gas, reducing production companies’ desire and motivation to enter new, less profitable industries (see also Morgunova Citation2021, 1 on the discussion of intertwined trends). While the attractiveness of the oil and gas market can be debated, new technology has emerged, and the demand for sustainable solutions continues to increase, influencing the entire industry landscape.

As the industry's supplier side is substantially bigger than the producer side, one could argue that it is easy for production companies to switch suppliers. However, as oil and gas platforms are unique and, to a large extent, require customized equipment, they benefit from having suppliers that already know the platform and the challenges to be solved, making the cost of switching business to other suppliers high. This differs from industries like offshore wind, hydrogen, and CCS, where equipment is to a larger extent standardized and mass-produced. Findings indicate that the revenue attractiveness of different markets is governing for oil and gas companies, influencing which companies transition to new energies. Lastly, it is easier for supply companies to transition to other industries as they offer products and services, whereas production companies offer a natural resource commodity.

4.2.2. Industry forces

Industry factors like competitors, new entrants, suppliers and other value chain actors, and stakeholders strongly influence the oil and gas industry. Competition between oil and gas companies is increasing, and a single company does not need more than 2–3 competitors before they risk getting into a spiral that drives all profits down (Participant 6, 2021). Moreover, the production companies are challenged to coexist with their competitors as oil fields on the Norwegian continental shelf are often jointly owned, resulting in competitors having a powerful influence (Participant 8, 2021). At the same time, new entrants positively impact the oil and gas companies as they create new business opportunities. New players bring new technology, methods, and new ways of delivering value, challenging traditional mindsets. The supply chains of oil and gas companies are much more competitive today and can deliver offerings more cost-effectively. Furthermore, suppliers and other value chain actors are increasingly important in new energy industries as more players are involved in the value chain compared to the oil and gas industry.

4.2.3. Key trends

We are transitioning from simple digitalization to innovation-based problem-solving, forcing companies to reconsider their traditional business models (Saebi Citation2016; Sarasini and Linder Citation2018). Traditional oil and gas companies are highly affected by technology trends, regulatory trends, social and cultural trends, and socioeconomic trends. Technological developments draw on data science, software solutions, digitalization, automation, robotization, and artificial intelligence, and have been particularly associated with energy efficiency and electrification of oil and gas installations (Participant 6, 2021). Technology trends can threaten a company's business model or enable them to improve and evolve and will further influence the transition to new industries. Regulations will continue to influence the industry, particularly the Paris Agreement, which governs how oil and gas companies operate (Participants 7 and 10, 2021). The effect of the EU's taxonomy is widely debated as today's framework makes it impossible for oil and gas-related activities to be considered anything but brown, resulting in companies continuing their oil and gas offerings.

Social and cultural trends can influence oil and gas companies’ reputations as there is a growing social consciousness concerning global warming and sustainability. Social and cultural trends influence access to expertise and competencies through access to new talent (Participants 1 and 6, 2021). The increasing unfavourable image of the oil and gas industry poses a challenge in acquiring new competence and talent. There are also socioeconomic effects as new generations are more aware of global warming, climate change and what type of company they want to work in (Participant 3, 2021). It is increasingly important that oil and gas companies take a stand concerning sustainable development, to be attractive employers.

4.2.4. Macroeconomic forces

Lastly, oil and gas companies are influenced by macroeconomic forces, including global market conditions, capital markets, commodities and other resources, and economic infrastructure. The oil and gas industry is export-oriented, and companies are sensitive to changes in oil prices (see Aarstad, Kvitastein, and Solheim Citation2021, 9 on Europe Brent Spot Price). Price fluctuations influence companies’ focus on innovation and sustainable development, and their investment and transition to other industries require high and consistent oil prices (as highlighted in Deegan et al. Citation2022) for talent. Thus, when the oil price is high, talent returns might prevent sustainability transitions. While there are no prominent challenges from the international capital market, ensuring access to finance depends increasingly on whether the companies’ activities are considered sustainable. Investors show greater interest in sustainable projects, resulting in more favourable financing for companies with a green profile (Participant 3, 2021).

Access to commodities and other resources influences the industry. While the price of materials fluctuates and affects companies that supply physical equipment, companies are more influenced by access to prime talent with industry-specific knowledge and expertise, especially when transitioning to new industries. The above concerning access to talents, relates to the cultural and socioeconomic trends and can be a decisive success factor. Lastly, Norway's well-developed economic infrastructure has a positive impact on the oil and gas industry and the development of more sustainable industries. For instance, the Covid-19 pandemic released funds from the public sector to initiate many sustainable projects that accelerated the development of offshore wind, hydrogen and CCS industries (Participant 10, 2021).

4.3. The process of changing industrial trajectories

Identifying the different barriers and challenges facing oil and gas companies in the process of changing industrial trajectories is a vital part of recognizing how business model innovation can contribute to the restructuring of the Norwegian oil and gas industry. Also, recognizing how the need for change differs from the willingness to change is important to identify how willingness can impact the process of changing industrial trajectories. We find that the willingness to change differs between the production and supply companies: the production companies’ willingness is currently low as oil and gas production is still highly profitable, while the supply companies’ willingness is high because they have no other options. Oil and gas production and exploration will continue if there are significant investments in the industry. The process of changing industrial trajectories for oil and gas production companies requires radical business model innovation. We argue, therefore, that industrial restructuring will require sustaining business model innovation on the supplier side, as several companies have already entered renewable industries and can utilize more of their existing resources.

Oil and gas companies face several challenges as they change industrial trajectories. External factors (see Section 4.2, The Oil and Gas Industry Landscape) influencing the oil and gas industry receive more attention than internal barriers. The following challenges are the most prominent: uncertainty, the need for new competence, high cost, risk, new environment, and the requirement of large investment. Some companies have taken a clear position in renewable industries, whereas others continue within oil and gas production while waiting to evaluate the expenses and risks of the green transition. Even though much existing expertise can be used in new industries, oil and gas companies must still acquire new industrial expertise and knowledge. Another challenge will be facilitating initiatives that make it financially possible to enter new industries as companies depend on earnings and a stable bottom line.

illustrates the process of business model innovation; we have identified when the various barriers are likely to arise in the process of changing the business model based on our data analysis. In the following, we lay out our key findings in relation to the elements in . We find that the dominant logic, insufficient managerial knowledge, uncertainty and complexity, and the lack of routines are the most prominent barriers for successful sustainable transition to occur. Moreover, we find that organizational resistance is most likely during the mobilization phase, when organizations initiate the process. Organizational resistance can be prevented by designing organizational cultures that support innovation (Daher Citation2016; Saebi Citation2016). For the case presented here, we argue that organizations can overcome resistant and poor motivation by running a communication campaign announcing the new business model.

Figure 2. Barriers in the process of business model innovation. The barriers are colour-coded: dark blue = organizational barriers, light blue = cognitive barriers, grey = additional barriers. Source: Osterwalder and Pigneur (Citation2010), 249. Author's own compilation based on the findings.

Second, we find that organizations may face the barriers of the ‘dominant logic’ (see Pralahad and Bettis Citation2000) and market dependency in the ‘understanding’ phase of the process. One of the most challenging tasks in this phase is questioning a business model that has provided long-term success. This relates to the ‘dominant logic’ issue, where organizations keep their competence for too long and fail to exploit new opportunities. Market dependency describes companies that do not change their business model because they depend on competitors implementing these changes first. This is an observable challenge for the industry we have studied herein; for example, as we have described through the willingness to change being low when profit is high.

Third, in the designing phase, when organizations aim to find the most appropriate business model, they are likely to meet with uncertainty, complexity and conflicts through disruptive innovation. This was highlighted in our study as well, for example through emphasizing that uncertainty is a key challenge when entering renewable industries, as companies must work with completely new circumstances, including new customer segments, framework conditions and demands (Participant 4, 2021). Subsequently, the new business models are seen to bring high levels of risk, and finding investors willing to accept that risk and the associated expenses is challenging for oil and gas companies, as was also put forward in our study (Participant 10, 2021). Similarly, Deegan et al. (Citation2022), studying regional innovation systems and the entrepreneurial discovery process by looking at two cities, one of them Stavanger where also our study was executed, find this ‘conformity-seeking’ behaviour that lends support to what we note here. Changing industrial trajectories brings significant uncertainty because most renewable industries are start-ups, so it is difficult to predict the outcomes. Thus, we argue that the cognitive barrier of complexity and uncertainty observed in our sample is strong. Additionally, conflict with disruptive innovation is likely to happen at the designing phase, during which companies do not initiate business model innovation because the new business model conflicts with the pre-existing asset configurations. Organizations find it challenging to handle the conflict between the new business model required to exploit disruptive technology and the current business model suited to existing technology (Chesbrough Citation2010, 358; Christensen Citation1997). Oil and gas companies must gain new competence and utilize new technologies that will affect the entire value chain (Participant 8, 2021). The oil and gas industry can finance the development of new technologies using current revenue, however, the disruptive innovation required for entering new industries conflicts somewhat with the traditional configurations of company assets, including their current value creation methods.

Fourth, insufficient managerial knowledge can hinder the process of business model innovation as key activities in the implementing phase involve communication and execution by defining milestones and related projects, organizing legal structures, and preparing a specific budget and project roadmap, which requires managerial knowledge. Competence in changing the business model is crucial. However, several companies found the process of evaluating and changing the business model challenging. We emphasize the importance of developing capabilities to assess the company's own business model and to create systems and procedures for implementing changes. Attaining new competence is one of the main challenges in entering renewable industries. The oil and gas industry can experience the cognitive barrier of insufficient managerial knowledge through lacking the competence needed to understand and evaluate their current business model, and therefore, avoid initiating the innovation process.

Lastly, having no business model innovation routines or processes can disrupt the final phase of the process. Although the new business model has been implemented at this stage, the process of business model innovation is often repetitive, leading the activities to continue. Key activities in the managing phase include continuous evaluation, managing synergies or conflicts between models, aligning the business model throughout the organization and scanning the environment to find how the business model can be influenced over the long term (Osterwalder and Pigneur Citation2010, 258). Changing the business model is usually driven ad hoc rather than based on structured routines, especially in small and medium-sized companies. Larger companies tend to have established routines for changing their business model, such as yearly strategy reorganizations and business model assessments. Larger oil and gas companies will be at the forefront of industrial restructuring as they are more likely to follow structured routines for evaluating and changing their business model.

5. Concluding remarks

The restructuring of the Norwegian oil and gas industry has received considerable attention due to the need for sustainable change to reach the climate ambitions of the Paris Agreement. Most companies focus on developing new technologies and making processes less environmentally damaging, giving little attention to business model innovation. Nevertheless, business model innovation can contribute to restructuring by helping companies adapt to changing market conditions and gaining competitive advantages (Evans et al. Citation2017). The research objective of this study is to examine how business model innovation contributes to a restructuring of the Norwegian oil and gas industry to comply with Norway's climate ambitions for 2030 and 2050.

We conclude that business model innovation can decisively contribute to restructuring. Industrial restructuring requires companies to make several changes to different elements of their business simultaneously to position themselves in a new market or industry, necessitating business model innovation. While oil and gas companies may have sufficient competence and experience in developing new technologies, the process of innovating several aspects of their business at the same time is unfamiliar to most, yet crucial to success. Thus, business model innovation can provide companies with a comprehensive framework to structure the process of change that will contribute to a successful industry restructuring and compliance with the country's climate ambitions.

To reach our research objective, we developed three supplementary questions covering different aspects of the restructuring and, more specifically, how business model innovation is part of the solution. Sub-question 1 addresses which parts of the business model should be emphasized the most during restructuring. Companies’ customer segments, value propositions, key resources, key partners and cost structure must be changed to succeed in the industrial restructuring. Sub-question 2 covers the external challenges facing oil and gas companies that may influence business model innovation. By initiating business model innovation, oil and gas companies can adapt to changes in their market, the industry in which they operate, key trends and macroeconomic conditions. Focus on sustainable change influences all parts of the oil and gas industry landscape and is particularly important in creating a need for change and, thus, initiating business model innovation. Lastly, sub-question 3 concerns the internal barriers that oil and gas companies face in the process of change. Among the several internal barriers that may hinder the change process, the most prominent are the dominant logic (Pralahad and Bettis Citation2000), deficient managerial knowledge, uncertainty and complexity, and an absence of business model innovation routines or processes. The need for change differs from the willingness to change within the industry, where the supply side has a higher willingness to change than the production side. Oil and gas production will continue if there are significant investments, and as long as the industry is considered profitable. Due to the industry's status, oil and gas producers transitioning into other markets will necessitate radical innovation of their business model. In contrast, oil and gas suppliers will likely focus on sustaining business model innovation.

5.1. Contributions/managerial implications

Business model innovation is necessary for oil and gas companies to adapt to the need for sustainable change, and to position themselves in new markets. While companies may have sufficient competence and experience in developing new technologies, most are unfamiliar with changing several areas of their business simultaneously. Thus, it is crucial for oil and gas companies to learn how to change their business models and how to initiate the appropriate measures to succeed in the industrial restructuring. Doing so can allow them to explore innovations that can come as a result from adaptation of their business model (Bocken et al. Citation2014; Joyce and Paquin, Citation2016).

5.3. Limitations and future research agenda

Our use of purposive sampling, targeting specific companies and cluster network considered relevant for the study, resulted in a small sample size, precluding statistical analysis generalisable across the industry. However, we argue that, similarly to the contributions by Halttunen, Slade and Staffell (Citation2022) and Sovacool, Axsen, and Sorrell (Citation2018), our study contributes to empirical novelty by benefitting from qualitative data from an elite group complementing the existing literature in the field by extending the specific drivers and barriers for restructuring in the oil and gas industry. Another limitation to our study is the lack of previous research on business model innovation within similar industries, limiting the opportunities to compare results to existing research. This led our research to be exploratory in character, seeking novel insights into our theme, but without the possibility of testing our sub-questions against prior literature. Because of these constraints, we were not able to fully investigate all potential initiatives these companies might undertake, such as when experiencing high levels of risk and uncertainty upon entering new markets like offshore wind, hydrogen, and CCS. A suggestion for future research is to investigate the role of different innovation systems and initiatives, such as extending the scope to also encompass the Global Innovation System literature and the different mechanisms at play (see Binz and Truffer Citation2017; Citation2021). Moreover, the effect of public policy instruments and initiatives allocated to increase the knowledge of business model innovation should be investigated.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Aarstad, J., O. Kvitastein, and M. Solheim. 2021. “External Shocks and Enterprises` Dynamic Capabilities in a Time of Regional Distress.” Growth and Change 52: 2342–2363. doi:10.1111/grow.12531.

- Abraham-Dukuma, M. 2021. “Dirty to Clean Energy: Exploring ‘oil and gas Majors Transitioning’.” The Extractive Industries and Society 8 (3): 100936. doi:10.1016/j.exis.2021.100936.

- Andreini, D., C. Bettinelli, N. Foss, and M. Mismetti. 2022. “Business Model Innovation: A Review of the Process-Based Literature.” Journal of Management and Governance 26: 1089–1121. doi:10.1007/s10997-021-09590-w.

- Binz, C., and B. Truffer. 2017. “Global Innovation Systems—A Conceptual Framework for Innovation Dynamics in Transnational Contexts.” Research Policy 46 (7): 1284–1298. doi:10.1016/j.respol.2017.05.012.

- Binz, C., and B. Truffer. 2021. “The Governance of Global Innovation Systems: Putting Knowledge in Context.” In Knowledge for Governance, edited by J. Glückler, G. Herrigel, and M. Handke, 397–414. Cham: Springer International Publishing. doi:10.1007/978-3-030-47150-7_17.

- Björkdahl, J., and M. Holmén. 2013. “Business Model Innovation – the Challenges Ahead.” International Journal of Product Development 18 (3/4): 213–225.

- Bocken, N., and T. Geradts. 2020. “Barriers and Drivers to Sustainable Business Model Innovation: Organization Design and Dynamic Capabilities.” Long Range Planning 53: 101950. doi:10.1016/j.lrp.2019.101950.

- Bocken, N., C. Schuit, and C. Kraaijenhagen. 2018. “Experimenting with a Circular Business Model: Lessons from Eight Cases.” Environmental Innovation and Societal Transitions 28: 79–95. doi:10.1016/j.eist.2018.02.001.

- Bocken, N., S. Short, P. Rana, and S. Evans. 2014. “A Literature and Practice Review to Develop Sustainable Business Model Archetypes.” Journal of Cleaner Production 65: 42–56. doi:10.1016/j.jclepro.2013.11.039.

- Boer, H., and W. During. 2001. “Innovation, What Innovation? A Comparison Between Product, Process and Organizational Innovation.” International Journal of Technology Management 22 (1–3): 83–107. doi:10.1504/ijtm.2001.002956.

- Boon, M. 2019. “A Climate of Change? The oil Industry and Decarbonization in Historical Perspective.” Business History Review 93 (1): 101–125. doi:10.1017/S0007680519000321.

- Boschma, R., and R. Martin. 2010. The Handbook of Evolutionary Economic Geography. Cheltenham: Edward Elgar.

- Braun, V., and V. Clarke. 2006. “Using Thematic Analysis in Psychology.” Qualitative Research in Psychology 3 (2): 77–101. doi:10.1191/1478088706qp063oa

- Chesbrough, H. 2010. “Business Model Innovation: Opportunities and Barriers.” Long Range Planning 43 (2–3): 354–363. doi:10.1016/j.lrp.2009.07.010.

- Christensen, Clayton M. 1997. The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail. Boston, MA: Harvard Business School Press.

- Cucculelli, M., and C. Bettinelli. 2015. “Business Models, Intangibles and Firm Performance: Evidence on Corporate Entrepreneurship from Italian Manufacturing SMEs.” Small Business Economics 45 (2): 329–350. https://www.jstor.org/stable/43553781.

- Daher, N. 2016. “The Relationships Between Organizational Culture and Organizational Innovation.” International Journal of Business Administration 13 (2): 1–15. https://web.s.ebscohost.com/abstract?direct=true&profile=ehost&scope=site&authtype=crawler&jrnl=15474844&AN=122076853&h=ppHTXJBrw0HXGAthUfkzTxffzR9fb0Q01Kmi6TebZeFDpPr1BeWiXIqVBQxeh1wS50%2bAoD3XSkQs0hg1Jg3qTw%3d%3d&crl=c&resultNs=AdminWebAuth&resultLocal=ErrCrlNotAuth&crlhashurl=login.aspx%3fdirect%3dtrue%26profile%3dehost%26scope%3dsite%26authtype%3dcrawler%26jrnl%3d15474844%26AN%3d122076853.

- Deegan, J., M. Solheim, S.-E. Jakobsen, and A. Isaksen. 2022. “One Coast, Two Systems. Regional Innovation Systems and Entrepreneurial Discovery in Western Norway.” Growth and Change 53: 490–514. doi:10.1111/grow.12595.

- Engen, O. 2009. “The Development of the Norwegian Petroleum Innovation System: A Historical Overview.” In Innovation, Path Dependency, and Policy, edited by J. Fagerberg, D. C. Mowery, and B. Verspagen, 179–207. Oxford: Oxford University Press.

- European Commission. 2020. EU Taxonomy for Sustainable Activities | European Commission. February 1, 2021. European Commission website: https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainablefinance/eu-taxonomy-sustainable-activities_en

- Evans, S., D. Vladimirova, M. Holgado, K. Van Fossen, M. Yang, E. Silva, and C. Barlow. 2017. “Business Model Innovation for Sustainability: Towards a Unified Perspective for Creation of Sustainable Business Models.” Business Strategy and the Environment 26: 597–608. doi:10.1002/bse.1939.

- Fagerberg, J., D. Mowery, and R. Nelson. 2006. The Oxford Handbook of Innovation. Oxford: Oxford University Press.

- Foss, N., and T. Saebi. 2015. Business Model Innovation: The Organizational Dimension. Oxford: Oxford University Press.

- Foss, N., and T. Saebi. 2016. “The Bumpy Road to Business Model Innovation: Overcoming Cognitive and Organisational Barriers.” Europe Business Review. https://www.europeanbusinessreview.com/the-bumpy-road-to-business-model-innovation-overcoming-cognitive-and-organisational-barriers/

- Frenken, K., and R. Boschma. 2007. “A Theoretical Framework for Evolutionary Economic Geography: Industrial Dynamics and Urban Growth as a Branching Process.” Journal of Economic Geography 7 (5): 635–649. doi:10.1093/jeg/lbm018.

- Geels, F. 2014. “Regime Resistance Against Low-Carbon Transitions: Introducing Politics and Power Into the Multi-Level Perspective.” Theory, Culture & Society 31 (5): 21–40. doi:10.1177/0263276414531627.

- Geissdoerfer, M., V. Doroteva, and S. Evans. 2018. “Sustainable Business Model Innovation: A Review.” Journal of Cleaner Production 198: 401–416. doi:10.1016/j.jclepro.2018.06.240.

- Halttunen, K., R. Slade, and I. Staffell. 2022. “We Don't Want to be the Bad Guys”: Oil Industry's Sensemaking of the Sustainability Transition Paradox.” Energy Research & Social Science 92: 102800. doi:10.1016/j.erss.2022.102800.

- Horowitz, C. 2016. “Paris Agreement.” International Legal Materials 55 (4): 740–755. doi:10.1017/S0020782900004253.

- Ihlen, Ø. 2009. “The Oxymoron of ‘Sustainable Oil Production’: The Case of the Norwegian oil Industry’.” Business Strategy and the Environment 18: 59–63. doi:10.1002/bse.563.

- Joyce, A., and R. Paquin. 2016. “The Triple Layered Business Model Canvas: A Tool to Design More Sustainable Business Models.” Journal of Cleaner Production 135: 1474–1486. doi:10.1016/j.jclepro.2016.06.067.

- Keeley, L., R. Pikkel, B. Quinn, and H. Walters. 2013. Ten Types of Innovation: The Discipline of Building Breakthroughs. Hoboken, NJ: John Wiley Sons.

- Maradana, R., R. Pradhan, S. Dash, K. Gaurav, M. Jayakumar, and D. Chatterjee. 2017. “Does Innovation Promote Economic Growth? Evidence from European Countries.”Journal of Innovation and Entrepreneurship 6 (1). doi:10.1186/s13731-016-0061-9.

- March, J. 1991. “Exploration and Exploitation in Organizational Learning.” Organization Science 2 (1): 71–87. doi:10.1287/orsc.2.1.71.

- Menon Economics. 2020. “Omstilling i petroleumssektoren.” Menon Economics 124. https://www.menon.no/wp-content/uploads/2020-124-Omstilling-i-petroleumssektoren.pdf.

- Morgunova, M. 2021. “The Role of the Socio-Technical Regime in the Sustainable Energy Transition: A Case of the Eurasian Arctic.” Extractive Industries and Societym 8 (3): 100939. doi:10.1016/j.exis.2021.100939.

- Newell, P., F. Geels, and B. Sovacool. 2022. “Navigating Tensions Between Rapid and Just Low-Carbon Transitions.” Environmental Research Letters 17: 041006. doi:10.1088/1748-9326/AC622A.

- Osterwalder, A., and Y. Pigneur. 2010. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers. Hoboken, NJ: John Wiley Sons Inc.

- Porter, M. 1998. “Competitive Strategy: Techniques for Analysing Industries and Competitors.” Industrial Marketing Management 11 (4): 318–319. DOI:10.1016/0019-8501(82)90025-6.

- Pralahad, C. K., and R. A. Bettis. 2000. “The Dominant Logic. A new Linkage Between Diversity and Performance.” In Economics Meets Sociology in Strategic Management (Advances in Strategic Management, Vol. 17), edited by J. A. C. Baum, and F. Dobbin, 119–141. doi:10.1016/S0742-3322(00)17010-X

- Romer, P. 1986. “Increasing Returns and Long-run Growth.” Journal of Political Economy 98 (5): 71–102. doi:10.1086/261725

- Saebi, T. 2016. “Fremtiden for Forretningsmodell-Innovasjon i Norge.” MAGMA 07: 33–41. https://openaccess.nhh.no/nhh-xmlui/bitstream/handle/11250/2452407/Magma+1607_Saebi.pdf?sequence=2.

- Sarasini, S., and M. Linder. 2018. “Integrating a Business Model Perspective Into Transition Theory: The Example of new Mobility Services.” Environmental Innovation and Societal Transitions 27: 16–31. doi:10.1016/j.eist.2017.09.004.

- Schumpeter, J. 1980. The Theory of Economic Development – An Inquiry Into Profits, Capital, Credit, Interest, and the Business Cycle. Routledge. https://www.amazon.com/Theory-Economic-Development-Science-Classics/dp/0878556982.

- Shepard, H. 1967. “Innovation-Resisting and Innovation-Producing Organizations.” The Journal of Business 40 (4): 470–477. https://www.jstor.org/stable/2351629 doi:10.1086/295012

- Solheim, M., and S. Moss. 2021. “Inter-organizational Learning Within an Organization? Mainstreaming Gender Policies in the Swedish Ministry of Foreign Affairs.” Learn. Org 28 (2): 181–194. doi:10.1108/TLO-05-2020-0103.

- Solheim, M., and R. Tveterås. 2017. “Benefitting from co-Location? Evidence from the Upstream oil and gas Industry.” Extractive Industries and Society 4: 904–914. doi:10.1016/j.exis.2017.09.001.

- Sovacool, B. K., J. Axsen, and S. Sorrell. 2018. “Promoting Novelty, Rigor, and Style in Energy Social Science: Towards Codes of Practice for Appropriate Methods and Research Design.” Energy Research & Social Science 45: 12–42. doi:10.1016/j.erss.2018.07.007.

- Steen, M. 2016. “Reconsidering Path Creation in Economic Geography: Aspects of Agency, Temporality and Methods.” European Planning Studies 24 (9): 1605–1622. doi:10.1080/09654313.2016.1204427.

- Taran, Y., H. Boer, and P. Lindgren. 2015. “A Business Model Innovation Typology.” Decis 46 (2): 301–332. doi:10.1111/deci.12128.

- Teece, D., M. Peteraf, and S. Leih. 2016. “Dynamic Capabilities and Organizational Agility: Risk, Uncertainty, and Strategy in the Innovation Economy.” California Management Review 58 (4): 13–35. doi:10.1525/cmr.2016.58.4.13.

- Tidd, J., and J. Bessant. 2014. Strategic Innovation Management. Chichester: John Wiley Sons Ltd., The Atrium, Southern Gate.

- Trippl, M., S. Baumgartinger-Seiringer, A. Frangenheim, A. Isaksen, and J. Rypestøl. 2020. “Unravelling Green Regional Industrial Path Development: Regional Preconditions, Asset Modification and Agency.” Geoforum; Journal of Physical, Human, and Regional Geosciences 111: 189–197. doi:10.1016/j.geoforum.2020.02.016.

- Tushman, M., and C. O’Reilly. 1996. “Ambidextrous Organizations: Managing Evolutionary and Revolutionary Change.” California Management Review 38 (4): 8–29. doi:10.2307/41165852.