?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Financing group decision-making (FGDM), which is an important stage of project financing, has unique characteristics: large investments and long payback horizons. Its evaluation results are likely to be distorted if we ignore the uncertain information and inconsistent assessment during the decision-making process. In this study, we propose a double interaction-based FGDM framework under uncertain information and inconsistent assessment. We modify the weight setting of evidence reasoning and aggregation method of probabilistic linguistic term sets to process the above two issues. The proposed framework is applied in a detailed case study analysis to display its effectiveness and stability. We expect the double interaction-based group decision-making framework under uncertain information and inconsistent assessment to be a useful tool to understand FGDM processes.

1. Introduction

Financing group decision-making (FGDM) refers to the important process of governments deciding to provide long-term funding, and plays a decisive role in large-scale projects, such as infrastructure development (Kissinger et al., Citation2019; Steffen, Citation2018). Understanding FGDM can directly and/or indirectly help governments to solve the funding problems of major projects (Chemmanur & John, Citation1996; Lamont, Citation1997), and thus deserves to be studied.

As an important stage of project financing, FGDM is a selection process that includes multiple factors (Tsai et al., Citation2013). Accordingly, it is also a complex multi-attribute group decision-making (MAGDM) problem. In contrast to general group decision-making problems, FGDM situations have unique characteristics, namely, they consider very large investments and long payback horizons. It is also almost impossible to change the financing scheme once it has been selected. Therefore, choosing a reasonable financing strategy is extremely important at the FGDM stage (Alavipour & Arditi, Citation2018).

This issue has both practical and theoretical significance. To investigate it, this study considers the following research question. What are the key factors while deciding? Different people have their own ideas. Past literature has identified the evaluation index system and applied it to the evaluation process (Chang, Citation2014; Grimsey & Lewis, Citation2002; Zhang, Citation2006). The consensus is that it is meaningful for decision makers to choose a reasonable evaluation index.

Other research has focused on information expression (Alonso, Citation2013; Gou et al., Citation2020; Sahi et al., Citation2013). Due to the incompleteness of information sets in real world decision situations, uncertainty often exists in the FGDM process (Jiang et al., Citation2005). To analyze this issue, Herrera et al. (Citation1997) put forward linguistic information expression in group decision-making. Rodriguez et al. (Citation2012) proposed to convert the natural language used in information evaluation into hesitant fuzzy linguistic term sets for analysis. In addition, Lourenzutti et al. (Citation2017) proposed a language distribution assessment to express experts’ evaluations of an object, which requires experts to have a definite evaluation for the evaluation object. However, most evaluations are not entirely certain. Thus, Pang et al. (Citation2016) proposed probabilistic linguistic term sets (PLTS), in which a set of linguistic terms and their corresponding probabilities are used to evaluate alternatives, and thereby, solve the complex problem of uncertain information. On this basis, Zhang et al. (Citation2016) defined the distance measure of PLTS and studied its additive consistency, and Cheng et al. (Citation2018) further combined PLTS and interactive technology to establish a risk investment evaluation model.

In addition to considering the evaluation index system and information expression, how to deal with uncertain information and aggregate the evaluated results are also important considerations in FGDM. The term “uncertain information” was defined by Zadeh (Citation1965) to represent the uncertainties caused by the limited cognitive ability of human beings. It has a significant influence in decision-making processes (Liu et al., Citation2019; Tao et al., Citation2020). Some methods have been established to manage the effects of uncertain information on decision-making, such as probability theory, fuzzy sets, and evidence reasoning (ER). Among them, the ER theory is widely used because of its simplicity and the ease of dealing with multi-attribute decision analysis problems under uncertainty. The ER theory proposed by Yang and Xu (Citation2002) and they distinguish indeterminate information, and ignorant information as distinct forms of uncertain information. This theory has a significant advantage regarding the fusion of multiple sources of information under uncertain information (Yang, Citation2001) and has been widely applied since it was proposed ( Chin et al., Citation2009; Kong et al., Citation2015; Tang et al., Citation2017; Wang, Kai, Guan, Yu, & Liu et al., Citation2019 ).

Additionally, the weighting assigned to different options in a decision, referred to as weight setting, has a significant influence on the decision result. Scholars have studied how decision-makers determine the relevant weights using the existing information in the decision-making process (Yuan et al., Citation2020). Specifically, the gray correlation helps study the problem of grey space, measuring the correlation between the reference sequence and the comparison sequence. Mao and Wu (Citation2019) improved the gray correlation analysis approach by using probabilistic linguistic measurement distance to determine the corresponding attribute weights. Wang et al. (Citation2019) used gray correlation analysis and the analysis hierarchy process to obtain the weight values of the indices. Yue (Citation2017) developed an entropy-based approach to understand the weight setting process of experts in a group decision-making setting. Chang et al. (Citation2013) proposed that the weights of options with high information consistency should be increased to prevent causing insufficient probabilities under uncertain information. Nonetheless, a research gap remains. In our framework, we propose the concept of “uncertainty degree” to investigate how uncertain information affects the weight setting process.

Another important issue is information aggregation. In recent years, some information aggregation approaches have been developed. Yang (Citation2001) developed an ER algorithm, which is a flexible and useful mathematical tool for combining uncertain information sets. Pang et al. (Citation2016) proposed the probabilistic linguistic weighted averaging (PLWA) operator based on the PLTS. However, in FGDM, each assessment of an expert’s decision-making process is carried out independently, which makes it difficult to draw a consistent conclusion using the above information aggregation method. Specifically, information interactions need to be considered.

Studies from the past few decades show that interactive decision-making with constant communication and interactions among evaluation experts means participants gradually and dynamically learn personal preference structures and thus, obtain the most satisfactory results (Bashiri & Badri, Citation2011; Han & Li, Citation1994; Reverberi & Talamo, Citation1999). To represent this, Han and Li (Citation1994) proposed a simple calculation formula to evaluate the revised priority order. Lourenzutti et al. (Citation2017) considered groups of decision makers with all their different opinions, heterogeneous types of information, criteria interaction, fuzzy measure identification and dynamic environments. Cheng at el. (2018) considered the consistency of assessing results and the weights of attributes through interactions among venture capital providers, and between venture capital providers and entrepreneurs. Chen and Zhang (Citation2020) focused on the interaction among criteria in their methodology to deduce the weighting system. Among the existing approaches to information aggregation with interaction, most of the existing research focuses on interaction between experts. It lacks consideration of interaction between decision parameters. Different parameters may lead to different results. Decision makers must decide which parameters should be chosen to influence decisions and which results are credible without interaction.

The above literature review highlights several research gaps. (1) It is not clear how to process uncertain information using PLTS. This implies that for FGDM, how to set and adjust weights in an uncertain environment has not been well-studied. (2) In the information aggregation process, interactions between experts have been considered, but the interactions between parameters are rarely considered. Further, analysis of these two types of interaction under uncertain information at the same time are even more scarce.

To construct an effective method in FGDM and choose the most appropriate financing scheme, we propose a double interaction-based FGDM under uncertain information and inconsistent assessment. The highlights of our study can be summarized as follows: First, we propose a double interaction-based aggregation framework, which considers the consistency and similarity of the PLTS matrix together with gray correlation analysis under uncertain information and inconsistent assessment. Second, we use the modified ER and PLTS to process uncertain information, and provide evidence of their effectiveness. Third, different tools are applied in robustness tests to verify the validity of our framework.

The remainder of this study is organized as follows: In Section 2, we introduce the basic concepts of PLTS and ER. In Section 3, we propose a double interaction-based MAGDM method using the improved ER and PLTS under uncertain information and inconsistent assessment. In Section 4, the FGDM process is shown with the help of a case study and the validity of our framework is further verified. The final section presents the conclusions and future research directions.

2. Preliminaries

Here, we introduce some basic concepts and features of PLTS and ER and describe the process of interactive decision making.

2.1. Probabilistic linguistic term set

According to Pang et al. (Citation2016), the PLTS formed by combining linguistic term sets and probability can be widely used. Thereby, the decision maker not only gives a language-based evaluation of a target object, but also supplies the probability information of the evaluation.

Definition 1

(Pang et al., Citation2016). Let be a linguistic term; then, a set of probabilistic linguistic terms

is defined as follows:

(1)

(1)

where

is the probability

of the linguistic term

represents the number of different linguistic terms in

According to Pang et al. (Citation2016), any two linguistic terms that belong to can be combined as follows:

(2)

(2)

Definition 2

(Pang et al., Citation2016). Let }

be the probabilistic linguistic term set; the corresponding weights are

and they satisfy

and

The PLWA operator is as follows:

(3)

(3)

Definition 3

(Pang et al., Citation2016). Let be a linguistic term;

} and

} are the sets of two probabilistic linguistic terms based on

and

are the linguistic terms corresponding to

and

respectively. Therefore, the distance between

and

is expressed as:

(4)

(4)

2.2. Evidence reasoning

ER is based on people’s understanding of objective existence. People use knowledge and clues to represent uncertain events using an uncertainty measurement method. This method is used in many uncertain multiple attribute decision-making problems.

For a specific decision-making problem, assume there are evaluation sets

The comprehensive attribute of evaluation is denoted by

which is determined by

basic attributes and denoted by

respectively. The weights of the attributes

and

We use

to represent the basic attribute

of

which is the reliability of the evaluation level

represents the reliability of the uncertain part of the basic attribute

of

with

In the evaluation of decision-making problems, any evaluation object can be expressed as follows:

(5)

(5)

Among them, the research object has attributes,

represents the attribute

judged as

and its reliability is

is set as the weight

of the attribute

Then, the ER of

is:

(6)

(6)

(7)

(7)

(8)

(8)

is the attribute

of

When added to the weight index

it is judged as the basic reliability probability distribution of

represents the basic belief probability that the weight-setting does not represent the real situation.

is not a complete understanding of the problem at hand, as the real results may not follow a specific analysis framework.

Then, each attribute is a piece of evidence in the recursive orthogonal summation process, where the basic reliability probability of evidence fusion is obtained as:

(9)

(9)

(10)

(10)

(11)

(11)

(12)

(12)

(13)

(13)

Finally, we obtain graded evaluation results for decision-making problems.

3. Evaluation framework of financing group decision-making

The choice among financing alternatives is usually a MAGDM, which reflects the preference characteristics of financing decision-makers and the knowledge limitations of evaluation experts. To describe each option at the FGDM stage and fully consider the problems caused by uncertain information, this study presents a double interaction-based MAGDM method using improved ER and PLTSs, which can directly process uncertain information under multiple level evaluation. The inconsistent assessment problem under uncertain information is resolved by combining the double interaction and gray correlation analysis. The modified ER and PLTS are used to aggregate all information into a comprehensive result. Finally, we evaluate the alternatives for a final decision.

3.1. Expression of financing information

Here, financing plan research refers to the selection of a relatively optimal plan among the possible alternatives when there is a funding gap throughout the course of an engineering project.

First, the factors with significant influence on FGDM are determined. The existing research shows that financing is mainly affected by four types of comprehensive factors, namely financing economy, risk, feasibility, and reliability (Chang, Citation2014; Grimsey & Lewis, Citation2002; Zhang, Citation2006). Each of these factors is refined and decomposed into several basic factors. To analyze the financing plan, it is necessary to further evaluate the identified influencing factors.

For the project financing problem, we assume that there are alternatives, denoted as

and

evaluation experts participate in the evaluation. The decision goal is composed of comprehensive attributes

where

indicates the number of comprehensive attributes. The comprehensive attributes

are composed of several basic attributes

where

indicates the number of basic attributes under each comprehensive attribute

In addition,

indicates the total number of basic attributes.

Generally, to facilitate the aggregation of basic attributes, we consider evaluating them using the same criteria they are associated with. At the same time, for data collection and collation, it is more natural to obtain evaluation information in a manner suitable to the specific attributes. That is, it is necessary to extract equivalent rules from the decision makers and then to convert the numerical information into equivalent expectations so that the quantitative and qualitative attributes can be considered simultaneously for analysis.

Experts usually evaluate qualitative evaluation indicators in the form of natural language. To make the evaluation information more convenient and intuitive, the corresponding evaluation levels can be used. These levels can be used to evaluate the overall situation of the financing scheme.

Additionally, it must be considered that an evaluation expert may not accurately determine the results at a specific evaluation level. Conversely, when evaluating qualitative basic attribute several evaluation levels are considered. Each level is given a corresponding degree of belief according to the expert’s knowledge structure and experience level. Therefore, when

evaluation experts

participate in the decision-making process, for

the probabilistic linguistic evaluation of the alternative

for the attribute

under evaluation expert

can be represented as:

(14)

(14)

Here, is the number of alternatives and

is the number of evaluation attributes. This means that the evaluation expert

’s basic attribute

of the alternative

is evaluated as

with probability

The judgment matrix given is

is the number of judgment matrices given by the

th evaluation expert (

).

(15)

(15)

Here, and this is referred to as the probabilistic linguistic term score. At the same time,

is also an element of the judgment matrix

3.2. Determination of weights under uncertain information

3.2.1. Experts’ weights

Reasonable and correct evaluations must fully consider the role that each evaluation expert plays. This requires financing decision-makers to attribute subjective weights according to the knowledge structures, experience levels, and personal preferences of evaluation experts. The subjective weights are given before the decision-making process is started and remain unchanged during this process. Another type of weight is the objective weight that evaluation experts use to express the information. The relevant combination of objective and subjective weights forms the final weight applied to the evaluation experts’ judgments. However, objective weights will dynamically modify the information expression according to conflicts in the decision-making process. In the proposed FGDM framework, assessment experts should give relatively consistent conclusions and there should be no conflicts.

The weight of the evaluation expert

is related to the consistency of its PLTS matrix and the uncertain information of experts, as well as to the similarity of the judgment matrix given by the evaluation experts

and

(

). Let the consistency of the evaluation expert

be

The similarity between the evaluation experts

and

is

Cheng et al. (Citation2018) pointed out that, according to Han and Li (Citation1994),

could be used to reflect the consistency harmonious weight index (CHWI):

(16)

(16)

where

Han and Li (Citation1994) proved that, if

then the matrix is a consistent judgment matrix. At the same time, the experts’ uncertain information could be expressed using the uncertain value of

(17)

(17)

The larger the value of the more uncertain is the information that the experts have. Based on the judgment matrix’s consistency and the uncertain information of experts’ evaluation,

can be expressed as follows:

(18)

(18)

When considering the objective weights of evaluation experts, Cheng et al. (Citation2018) proposed the use of the ratio of the similarity of judgment matrix to other judgment matrices, while also considering the total similarity between the judgment matrices.

The derivative vector of judgment matrix can be written as vec (

); let

be the angle between the judgment matrix

and the judgment matrix

(19)

(19)

It is easy to determine that and that

can express the similarity between evaluation experts

and

(20)

(20)

represents the similarity with other judgment matrices, and the normalization operation of

can get the objective weight

of the evaluation expert:

(21)

(21)

Through the linear combination of the subjective weight and the objective weight

the final expert weight

can be obtained:

(22)

(22)

In the first interactive stage of decision making, to obtain a more realistic decision result, the evaluation experts need to communicate with each other. The objective weights of the experts will also dynamically change with the information similarity after the test. Eventually, the evaluation information is consistent and recognized.

(23)

(23)

In the process of interaction between experts (first interaction), the objective weights of the evaluation experts will be adjusted according to the evaluation information of other experts. Then, we calculate the consensus coefficient which is determined by the

th adjustment, and compare it with the consensus value

If

then the objective weight setting is reasonable. If not, the evaluation experts need to carry out interactive communication and select the evaluation with the smallest objective weight, re-evaluate the information, and then recalculate

until

3.2.2. Attribute weights

After obtaining the judgment matrix of the evaluation expert, we determine the attribute weights. For probabilistic linguistic MAGDM, the gray correlation coefficient of the program evaluation value reflects the similarity between the attribute and its reference value. Therefore, it can reflect the importance of this attribute in the attribute system (Yang & Singh, Citation1994; Mao & Wu, Citation2019).

(1) Determination of analytical sequence

First, the evaluation information must be assembled using the PLWA operator and the weights provided by the evaluation experts, where The compared sequence

can be expressed as:

(24)

(24)

is a reference sequence, which means that all attributes’ highest evaluation probability is 1.

(2) Calculating the gray correlation level (GCL)

The GCL between two sequences at a certain time point is called the gray correlation coefficient. The correlation coefficient between the reference sequence

and the compared sequence

is calculated using the following formula:

(25)

(25)

The distinguishing coefficient is obtained in the range of

The smaller the

the higher the correlation coefficient. The correlation level between the comparison sequence and the reference sequence is reflected by all the correlation coefficients. The average of these is the GCL.

(26)

(26)

(3) Determining the interaction of the parameters

To obtain a more reliable GCL result, the gray correlation degrees need to be compared with each other under different values of To do this, we let

be the angle between the gray correlation degree

and the gray correlation degree

(27)

(27)

In the second interactive process of decision making, we calculate the consensus coefficient which is determined by combining the experts’ weights and the attributes’ weights and comparing the result with the consensus value

(28)

(28)

If then the second interaction is acceptable. If not, the second interaction is not acceptable. Evaluation experts need to carry out the first interaction again, re-evaluate the information and then recalculate

until

(4) Determining the attribute weight

After the second interaction, is used to determine the weight of each attribute.

(29)

(29)

3.3. Double interaction-based information aggregation

After adding the attribute weight index to basic attribute probability of the alternative

the basic belief probability of

is assigned as

The basic belief probability is assigned as

if it cannot be determined to a certain level.

(30)

(30)

(31)

(31)

There exists:

(32)

(32)

(33)

(33)

reflects the basic probability of the indeterminate information.

represents an incomplete understanding of the problem, as the information that is ignored will not be assigned to a certain evaluation level.

Considering each basic attribute, we use the ER analysis algorithm to aggregate the basic attributes separately, according to the comprehensive attribute division (Yang & Singh, Citation1994):

(34)

(34)

(35)

(35)

Here,

(36)

(36)

After the basic attribute aggregation is completed, the ER analysis algorithm is used again to aggregate the comprehensive attributes and obtain the total result of the target:

(37)

(37)

(38)

(38)

Here,

(39)

(39)

After the total belief probability distribution value of the decision target is obtained, the belief probability corresponding to each result level and the normalized uncertain belief probability, respectively, are:

(40)

(40)

(41)

(41)

3.4. Evaluation of alternatives

After obtaining the various graded evaluation results of decision-making problems, to compare similar results, it is common practice to introduce utility values and then quantify the values of the qualitative results. The corresponding utility function for each different evaluation level is expressed as:

(42)

(42)

Then, we use the results with unknown evaluation levels to obtain the minimum and maximum utility values, respectively:

(43)

(43)

(44)

(44)

The minimum and maximum utilities of the alternative constitute its utility interval,

For selecting the most reasonable utility result, we choose one option using the two alternatives method.

(45)

(45)

where

(

Then, the probability degree matrix

can be constructed. This matrix contains all the probability degree information derived from comparing all pairs of alternatives (Xu, Citation2015). Here, we utilize the priority formula to derive the score vector of

(46)

(46)

We obtain the score vector of the probability degree matrix

from the above equation. Finally, we rank the alternative scheme scores according to

and choose the best alternative

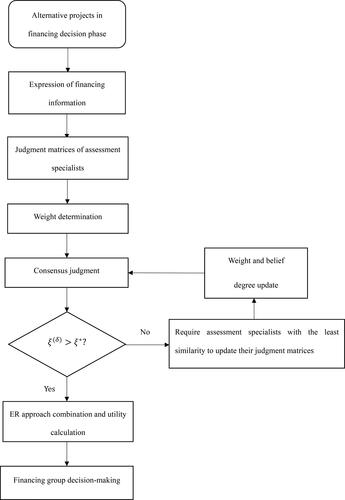

shows the above-described process of the FGDM framework, which is proposed in this study.

Figure 1. Multiple-attribute group decision-making process for project financing.

Source: drawn by authors themselves.

4. Case study

Here, a case is used to illustrate the interaction and judgment process in FGDM.

4.1. Background description

The Newly built Chengdu Tianfu International Airport will help Chengdu integrate into global resource networks. For Jianyang, where the airport is to be located, this is an important development opportunity. The Airport Avenue would connect Jianyang City and Tianfu Airport. This development has strategic significance for Jianyang’s regional economy. To construct the Airport Avenue, local government has proposed three alternative financing schemes Before choosing the final financing scheme, discussion and evaluation are essential.

Scheme 1. Issuing bonds of 1.5 billion yuan and setting the bond maturity to five years. At the same time, no more than 30% of the funds raised from the project's proceeds bonds will be used for supplementary flows. The comprehensive financing rate will be 9.8%.

Scheme 2. Creating the Jianyang Investment and Construction Fund. The 5-year benchmark interest rate of comprehensive financing cost is within 45%, and the total investment will be 2 billion yuan. The subscription method for units in the fund would be that the fund manager initiates subscriptions to financial institutions and other investors.

Scheme 3. Loaning a total amount of 1.6-billion-yuan from commercial banks. The comprehensive financing cost is 6.0% per year and the financing period is 6 years. After the loan is issued, the principal is returned once every 6 months after the grace period and the service fee is 3.0% per year.

To further analyze and evaluate each scheme, the evaluation index system for the financing scheme has been established according to Alonso (Citation2013), Chang (Citation2014) and Sahi et al. (Citation2013). This is shown in .

Table 1. Evaluation index system of the financing scheme.

Let four evaluation experts evaluate schemes

according to the evaluation index system. At the same time, the experts hope that their consensus coefficient is above 0.95 (

). We first consider

To avoid the subjectivity of the value of

the robustness test is further conducted by changing the value of

The evaluation expert ’s preliminary judgment information of each scheme is shown in . The preliminary evaluation information of the remaining evaluation experts is shown in Appendix A.

Table 2. Expert ’s evaluation of each scheme.

(1)Comprehensive Index

(2)Comprehensive Index

(3)Comprehensive Index

(4)Comprehensive Index

4.2. Aggregating assessments via evidence reasoning

Evaluating the alternative schemes can be computed according to the FGDM process proposed in this study and depicted in . This process includes the following steps.

Step 1. Obtain judgment matrix for the evaluation experts

is used as the linguistic decision matrix of the expert

(

) for the

th

comprehensive attribute in the first round of evaluation. We can obtain the linguistic decision of evaluation experts in the first round using equation

The linguistic decision matrix of the evaluation expert

is shown below. The linguistic decision matrix of the other evaluation experts is shown in Appendix B.

Step 2. Determinate the experts’ weights

According to the evaluation expert’s linguistic decision matrix, the evaluation experts’ subjective weights and the similarities between experts can be calculated according to the Equationequations (18)(18)

(18) and Equation(19)

(19)

(19) . The results are shown in .

Table 3. Evaluation experts’ subjective weights for the evaluation indexes.

At the same time, the similarities between the evaluation experts’ judgments are obtained using the Equationequation (20)(20)

(20) and are shown in .

Table 4. Similarities between experts’ judgments.

The total weight of the evaluation experts is calculated by the Equationequation (22)(22)

(22) . The consensus judgment is obtained using the Equationequation (23)

(23)

(23) . The results are shown in .

Table 5. Evaluation expert weights and consensus coefficient.

Step 3. Consensus judgment

Calculating the consensus coefficient of the evaluation experts shows that the consensus level is not reached because Therefore, we continue with Step 4.

Step 4. Interaction process

The fourth evaluation expert has the minimum weight in . This indicates that his or her information may have consistency issues. The low similarities between the fourth expert and the other evaluation experts indicates that his or her information is extreme. Therefore, the expert needs to modify his or her judgment information.

Table 6. Expert ’s evaluation of each scheme.

(1)Comprehensive Index

(2)Comprehensive Index

(3)Comprehensive Index

(4)Comprehensive Index

The corresponding attribute judgment information is updated as follows:

The adjusted similarities between experts, expert weights, and agreement coefficients are re-calculated. The updated similarities between experts are shown in .

Table 7. Revised similarities between experts.

We calculate the objective weights of the evaluation experts according to the Equationequations (22)(22)

(22) and Equation(23)

(23)

(23) . The results are shown in .

Table 8. Revised evaluation expert weights and consensus coefficient.

Calculating the consensus coefficient of the evaluation experts shows that which means the required consensus level has been achieved.

Step 5. Obtain attributes weights

Next, we calculate the gray correlation of the attribute and the attribute importance according to the Equationequations (25)–(29). The relative results are shown in .

Table 9. Attributes’ relative weights.

Step 6. Aggregating assessments

We can obtain the result on the multiple attributes according to the Equationequations (30)–(41). shows the result after information is aggregated. These are the evaluation experts’ comprehensive evaluation results of the alternative schemes.

Table 10. Comprehensive evaluation results provided by evaluation experts.

Step 7. Compare alternative schemes

The comprehensive score of the experts is determined using Equationequations (43)–(44), then this result is summed. Finally, the weights of the experts are integrated to obtain the final score of each financing scheme, as shown in .

Table 11. Final utility value of each scheme.

The comprehensive scores of each scheme are obtained according to Equationequations (43)–(44). The final scores are as follows:

The alternative financing schemes are ranked as according to the final score. Therefore, the best financing scheme is the second alternative.

4.3. Further analysis

In this subsection, three different approaches are used to verify the validity of our framework. One is to test the validity of the double interaction, the second is to show the effectiveness of the weight setting process, and the last one is the comparative analyses between the proposed approach in this study and the existing approaches of PLTS and ER. Through the robustness tests given below, it is proven that the method proposed in our study is not only effective, but also stable.

4.3.1. Validity of interaction between experts

In the decision-making process, significant differences in judgment information between experts can be avoided by the interaction between experts. However, if the interaction is not considered, the relative consistency between subjective weights and objective weights cannot be ensured, the total weights in will be the final weights, and the result is listed in accordingly. Here, the ranking is which is different from the one we obtained in .

Table 12. Final score of each scheme without interaction.

Table 13. Final score of each financing scheme.

To verify the validity of the interaction between experts, we change the value of which is treated as a subjective variable in the parameter setting. The results of the comparison are shown in .

Table 14. Ordering between schemes with different

In the absence of interaction between experts, the ranking of alternative schemes is unstable. When the ranking of the alternatives is

However, the situation differs once

that is

One possible explanation for this is that non-interaction is more likely to lead to a large difference between subjective weights and objective weights. With the increase of the subjective weights (

) ratio, the ranking of alternative schemes may change. It is difficult for decision makers to make optimal decisions under such unreliable results. As a result, they could miss out on the best financing scheme and may opt for a sub-optimal choice. However, once we allow for an interaction between experts, the ranking of schemes remains stable, regardless of the changes in

Therefore, we think that experts’ judgments are more stably through experts’ interaction, and the ranking results are more reliable, and the stability of the results is stronger.

4.3.2. Effectiveness of weight setting

Subsection 3.3 shows that the probability of uncertain information can be assigned to any level. Accordingly, the uncertain information also has a corresponding score in the probability term score setting process. Considering the experts’ uncertainty degree based on uncertain information could avoid the situation in which experts are not clear about the attribute information, but the subjective weight applied to the attribute is high through uncertain information. To verify the superiority of weight setting in this paper, we compare the results of the two processes by considering the

and not considering in .

Table 15. Ordering between schemes with different

The ranking of alternative schemes is also unstable under interaction without uncertainty degrees. This lack of stability may cause confusion for the decision maker trying to make a final decision. However, the above situation will be improved once we consider the uncertainty degree in the weight setting process. No matter how changes, the ranking of schemes is always

This is because we consider the uncertainty degree and reduce the impact this has on the weight setting process, thus the stability of the scheme ranking results improves. Based on the comparison in , one fact can be seen: considering the uncertainty degree, no matter how the value of

changes, the final sorting results will be consistent.

4.3.3. Comparative analysis

For the FGDM, we make some comparative analyses between the proposed approach in this study and the existing approaches of PLTS and ER with interaction between experts. The results of the comparison are shown in below.

Table 16. Ordering between schemes with different approaches.

It can be seen from that the PLTS is applied, the ranking of alternative schemes will change for different values of It is confusing for decision makers to make a scheme selection in facing ranking changes of alternative schemes. At the same time, we can still see that considering only the first interaction is insufficient, this ranking result will also change with the change of

By contrast, the double interaction proposed in this paper will keep the ranking schemes unchanged under different values of

Thus, the double interaction framework is validated, and the proposed approach is effective.

5. Conclusions

FGDM is crucial to the deployment and construction of major national engineering projects. The main participants in the FGDM process are evaluation experts. The decision analysis process must thus pay special attention to balancing the weights among experts. At the same time, when evaluation experts are asked for evaluations, they may be hesitant to choose between several linguistic terms. Therefore, how to effectively solve the above problems is very important in the FGDM process. However, most of the existing research on project financing focuses on the set of weights for decision alternatives but understanding how to adjust them to reflect an uncertain environment is not well studied. In addition, past research rarely considers the interactions between experts and between parameters under uncertain evaluation information.

To solve these problems, we combine ER and PLTS to process uncertain information, and further propose a double interaction-based multiple aggregation method to deal with inconsistent assessments. The case study shows the effectiveness and stability of the methodology under a double interaction-based decision-making scenario with uncertain information. It is expected that this framework will become a useful tool for FGDM.

Our research suggests that evaluation experts should provide specific probability values for an evaluation level. But we do not account for situations where it is difficult for experts to give an accurate probability value. Therefore, Further research can consider using intervals to represent incomplete information in the probability distribution.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Alavipour, S. M. R., & Arditi, D. (2018). Impact of contractor’s optimized financing cost on project bid price. International Journal of Project Management, 36(5), 808–818. https://doi.org/10.1016/j.ijproman.2018.03.001

- Alonso, S. (2013). Temporal discounting and number representation. Journal of Behavioral Finance, 14(3), 240–251. https://doi.org/10.1080/15427560.2013.820188

- Bashiri, M., & Badri, H. (2011). A group decision making procedure for fuzzy interactive linear assignment programming. Expert Systems with Applications, 38(5), 5561–5568. https://doi.org/10.1016/j.eswa.2010.10.080

- Chang, Z. (2014). Financing new metros—The Beijing metro financing sustainability study. Transport Policy, 32, 148–155. https://doi.org/10.1016/j.tranpol.2014.01.009

- Chang, L. L., Li, M. J., & Jiang, J. (2013). A variable weight approach for evidential reasoning. Journal of Central South University, 20(8), 2202–2211. https://doi.org/10.1007/s11771-013-1725-2

- Chemmanur, T. J., & John, K. (1996). Optimal incorporation, structure of debt contracts, and limited-recourse project financing. Journal of Financial Intermediation, 5(4), 372–408. https://doi.org/10.1006/jfin.1996.0021

- Chen, Y., & Zhang, D. N. (2020). Evaluation of city sustainability using multi-criteria decision-making considering interaction among criteria in Liaoning province China. Sustainable Cities and Society, 59, 102211. https://doi.org/10.1016/j.scs.2020.102211

- Cheng, X., Gu, J., & Xu, Z. S. (2018). Venture capital group decision-making with interaction under probabilistic linguistic environment. Knowledge-Based Systems, 140, 82–91. https://doi.org/10.1016/j.knosys.2017.10.030

- Chin, K. S., Yang, J. B., Guo, M., & Lam, J. P. K. (2009). An evidential-reasoning-interval-based method for new product design assessment. IEEE Transactions on Engineering Management, 56(1), 142–156.

- Gou, X. J., Xu, Z. S., & Zhou, W. (2020). Interval consistency repairing method for double hierarchy hesitant fuzzy linguistic preference relation and application in the diagnosis of lung cancer. Economic Research-Ekonomska Istrazivanja, 34(1), 1–20.

- Grimsey, D., & Lewis, M. K. (2002). Evaluating the risks of public private partnerships for infrastructure projects. International Journal of Project Management, 20(2), 107–118. https://doi.org/10.1016/S0263-7863(00)00040-5

- Han, X. L., & Li, S. R. (1994). The priority method in view of consistency harmonious weight index. Systems Engineering-Theory Methodology Applications, 3(1), 41–45.

- Herrera, F., Herrera-Viedma, E., & Verdegay, J. L. (1997). A rational consensus model in group decision making using linguistic assessments. Fuzzy Sets and Systems, 88(1), 31–49. https://doi.org/10.1016/S0165-0114(96)00047-4

- Jiang, G., Lee, C. M., & Zhang, Y. (2005). Information uncertainty and expected returns. Review of Accounting Studies, 10(2-3), 185–221. https://doi.org/10.1007/s11142-005-1528-2

- Kissinger, G., Gupta, A., Mulder, I., & Unterstell, N. (2019). Climate financing needs in the land sector under the Paris Agreement: An assessment of developing country perspectives. Land Use Policy, 83, 256–269. https://doi.org/10.1016/j.landusepol.2019.02.007

- Kong, G., Xu, D. L., Yang, J. B., & Ma, X. (2015). Combined medical quality assessment using the evidential reasoning approach. Expert Systems with Applications, 42(13), 5522–5530. https://doi.org/10.1016/j.eswa.2015.03.009

- Lamont, O. (1997). Cash flow and investment: Evidence from internal capital markets. Journal of Financial Economics, 52(1), 83–109.

- Liu, Z. B., Gao, R., Zhou, C., & Ma, N. (2019). Two-period pricing and strategy choice for a supply chain with dual uncertain information under different profit risk levels. Computers & Industrial Engineering, 136, 173–186. https://doi.org/10.1016/j.cie.2019.07.029

- Lourenzutti, R., Krohling, R. A., & Reformat, M. Z. (2017). Choquet based TOPSIS and TODIM for dynamic and heterogeneous decision making with criteria interaction. Information Sciences, 408, 41–69. https://doi.org/10.1016/j.ins.2017.04.037

- Mao, X. B., & Wu, M. (2019). Probabilistic linguistic multi-attribute group decision-making model based on interaction and feedback. Fuzzy Systems and Mathematics, 33(3), 134–143.

- Pang, Q., Wang, H., & Xu, Z. S. (2016). Probabilistic linguistic term sets in multi-attribute group decision making. Information Sciences, 369, 128–143. https://doi.org/10.1016/j.ins.2016.06.021

- Reverberi, P., & Talamo, M. (1999). A probabilistic model for interactive decision-making. Decision Support Systems, 25(4), 289–308. https://doi.org/10.1016/S0167-9236(99)00013-5

- Rodriguez, R. M., Martinez, L., & Herrera, F. (2012). Hesitant fuzzy linguistic term sets for decision making. IEEE Transactions on Fuzzy Systems, 20(1), 109–119. https://doi.org/10.1109/TFUZZ.2011.2170076

- Sahi, S. K., Arora, A. P., & Dhameja, N. (2013). An exploratory inquiry into the psychological biases in financial investment behavior. Journal of Behavioral Finance, 14(2), 94–103. https://doi.org/10.1080/15427560.2013.790387

- Steffen, B. (2018). The importance of project finance for renewable energy projects. Energy Economics, 69(1), 280–294. https://doi.org/10.1016/j.eneco.2017.11.006

- Tang, X. A., Feng, N. P., Xue, M., Yang, S. L., & Wu, J. (2017). The expert reliability and evidential reasoning rule based intuitionistic fuzzy multiple attribute group decision making. Journal of Intelligent & Fuzzy Systems, 33(2), 1067–1082. https://doi.org/10.3233/JIFS-162436

- Tao, Z. F., Shao, Z. Y., Liu, J. P., Zhou, L. G., & Chen, H. Y. (2020). Basic uncertain information soft set and its application to multi-criteria group decision making. Engineering Applications of Artificial Intelligence, 95, 103871. https://doi.org/10.1016/j.engappai.2020.103871

- Tsai, W. H., Yang, C. C., Leu, J. D., Lee, Y. F., & Yang, C. H. (2013). An integrated group decision making support model for corporate financing decisions. Group Decision and Negotiation, 22(6), 1103–1127. https://doi.org/10.1007/s10726-012-9308-4

- Wang, Y. L., Kai, L., Guan, G., Yu, Y. Y., & Liu, F. (2019). Evaluation method for Green jack-up drilling platform design scheme based on improved grey correlation analysis. Applied Ocean Research, 85, 119–127.

- Xu, Z. S. (2015). Uncertain multi-attribute decision making: Methods and applications. Springer press.

- Yang, J. B. (2001). Rule and utility based evidential reasoning approach for multi-attribute decision analysis under uncertainties. European Journal of Operational Research, 131(1), 31–61. https://doi.org/10.1016/S0377-2217(99)00441-5

- Yang, J. B., & Singh, M. G. (1994). An evidential reasoning approach for multiple-attribute decision making with uncertainty. IEEE Transactions on Systems Man and Cybernetics Part A-Systems and Humans, 24(1), 1–18.

- Yang, J. B., & Xu, D. L. (2002). On the evidential reasoning algorithm for multiple attribute decision analysis under uncertainty. IEEE Transactions on Systems Man and Cybernetics Part A-Systems and Humans, 32(3), 289–304.

- Yuan, G., Yang, Y. S., Tian, G. D., & Zhuang, Q. W. (2020). Comprehensive evaluation of disassembly performance based on the ultimate cross-efficiency and extension-gray correlation degree. Journal of Cleaner Production, 245, 118800. https://doi.org/10.1016/j.jclepro.2019.118800

- Yue, C. (2017). Entropy-based weights on decision makers in group decision-making setting with hybrid preference representations. Applied Soft Computing, 60, 737–749. https://doi.org/10.1016/j.asoc.2017.07.033

- Zadeh, L. A. (1965). Fuzzy sets. Information and Control, 8(3), 338–353. https://doi.org/10.1016/S0019-9958(65)90241-X

- Zhang, X. Q. (2006). Public clients’ best value perspectives of public private partnerships in infrastructure development. Journal of Construction Engineering and Management, 132(2), 107–114. https://doi.org/10.1061/(ASCE)0733-9364(2006)132:2(107)

- Zhang, Y. X., Xu, Z. S., Wang, H., & Liao, H. C. (2016). Consistency-based risk assessment with probabilistic linguistic preference relation. Applied Soft Computing, 49, 817–833.

Appendix A

Table A1. Expert ’s evaluation of each scheme.

(1)Comprehensive Index

(2)Comprehensive Index

(3)Comprehensive Index

(4)Comprehensive Index

Table A2. Expert ’s evaluation of each scheme.

(1)Comprehensive Index

(2)Comprehensive Index

(3)Comprehensive Index

(4)Comprehensive Index

Table A3. Expert ’s evaluation of each scheme.

(1)Comprehensive Index

(2)Comprehensive Index

(3)Comprehensive Index

(4)Comprehensive Index

Appendix B

Evaluation expert ’s linguistic decision matrix:

Evaluation expert ’s linguistic decision matrix:

Evaluation expert ’s linguistic decision matrix: