?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article empirically examines the impact of tax structure on corporate tax compliance using Chinese industrial enterprise database and prefectural data. The results show that relying more on indirect taxes tends to decrease corporate tax compliance, while increasing the ratio of direct taxes of total tax revenues significantly enhances corporate tax compliance. To overcome endogeneity, the robustness is tested using instrumental variables and other robustness checks, such as changing variables and changing time windows. Mechanism analysis shows that it is conducive to reducing the complexity of the tax system, improving the quality of governance, and enhancing taxation efforts. This article examines the impact of tax system on corporate taxation behaviour from the perspective of the tax structure, which also provides microscopic empirical evidence for tax reform in China.

1. Introduction

Tax compliance is a long-standing goal for the government to raise tax revenues, which is also an important factor in determining the government’s capacity (Alm et al., Citation1990; Umar et al., Citation2019). Compared to developed countries, developing countries face serious problems of tax evasion. For example, China experiences significant tax evasion and fake invoices (Cai & Liu, Citation2009; Chen et al., Citation2014; Fisman & Wei, Citation2004). As such, the developing countries’ tax revenues cannot always finance their needs (Besley & Persson, Citation2014). One common feature of these countries is that they have more complex tax systems (Chau & Leung, Citation2009). Generally speaking, a country’s tax structure should coincide with its economic development. Unlike tax systems in developed countries which are based on direct taxes, many underdeveloped countries implement a tax system that mainly relies on indirect taxes. This means that underdeveloped countries have more complicated tax systems. In theory, when a taxation system is more complex, tax evasion is often much higher. Simplifying the tax system helps to reduce the complexity of tax system, which inhibits tax evasion (Chau & Leung, Citation2009; Milliron, Citation1985). In turn, increasing tax compliance can improve the government’s capacity to provide national public goods, and facilitate the fair distribution of the tax burden. Hence, it is vital for improving a country’s tax capacity. However, to date, little is known about the relationship between tax system and corporate tax compliance.

This article investigates the relationship between tax structure and tax compliance using Chinese industrial enterprise dataset and prefectural data, where tax structure is captured by direct versus indirect taxes and the ratio of direct taxes to total tax revenues. Since 1994, China has adopted a tax structure that is characterised by mainly indirect taxes and enterprise sources. By exploring this topic, this study aims to contribute to the literature from the perspective of tax system, which is an important part of a country’s institutional system. Theoretically, a country that mainly relies on indirect taxes usually has a more complicated tax system. This leads to fiscal illusion where taxpayers cannot determine the tax-price of public outputs and underestimate the actual tax burden, which facilitates corruption and decreases governance equality. This article finds strong evidence for this argument: the tax system relying mainly on indirect taxes tends to decrease corporate tax compliance, while increasing the ratio of direct taxes could help to increase tax compliance. Moreover, simplifying the tax structure decreases tax system complexity, enhances governance equality and reduces the tax officials’ efforts for collecting taxes. This study concludes that optimising the tax system is a key driver for corporate tax compliance. The results are found to be robust using alternative measures of tax compliance and tax structure and alternative estimations.

One challenge this study faced is that tax structure may not be exogeneous. Although tax rates are legislated at the national level, the local government can influence the effective tax rates in many ways. For example, a local government may conduct slack tax enforcement through delayed tax payments (Chen, Citation2017). To address this problem, the actual tax rates method (ATRM) is used in the baseline regression to measure tax compliance, and then the national income account (NIA) method is applied to verify its robustness (Cai & Liu, Citation2009). Moreover, this study also applies instrumental variable estimation (2SLS) to identify the causal effects of tax structure and tax compliance.

Finally, this article fills the gap between tax structure and tax compliance by using an enterprise dataset to test the tax structure’s effect on an enterprise. Few studies are known to have directly analysed the relationship between tax structure and corporate tax compliance, especially in developing countries, and only a few studies have focussed on personal tax compliance (Alm et al., Citation1990; Gómez Sabaini & Jiménez, Citation2012). Given that China’s tax revenue mainly comes from enterprises and mostly relies on indirect taxes, the past references may need to be tested.

The rest of this article is organised as follows: Section 2 presents the literature review and theoretical hypotheses. Section 3 summarises the empirical methodology and data. Section 4 presents the empirical results and the possible mechanisms, and Section 5 presents the discussion and conclusions of the article.

2. Theoretical hypotheses

Theoretically, tax structure mainly based on direct taxes will not only reduce the complexity of tax system, but will also force local governments to improve their governance and strengthen tax collection. This is also our starting point to link the tax structure and corporate tax compliance.

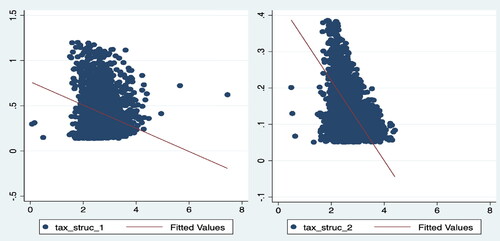

First, optimising the tax system supports reductions in tax complexity and tax compliance costs. As is known, for a tax system mainly relying on indirect taxes, tax revenues come mainly from enterprises and indirect taxes are mainly the value-added taxes (VAT) and business taxes. Hence, the tax system complexity is mainly reflected in the indirect tax. It is argued that a complex tax system creates unnecessary tax costs for taxpayers, leading them to more heavily rely on tax consulting agencies, or to hide transactions to evade taxes (Richardson, Citation2006). Compared to direct taxes, due to fiscal illusion, taxpayers usually underestimate the tax burden associated with public programs from indirect taxes. The taxpayers are usually the tax bearers due to the direct taxes that cannot shift easily, By contrast, indirect taxes are usually incorporated into the prices of goods and services, which causes the actual tax burden to be underestimated (Liu & Feng, Citation2015; Liu & Mikesell, Citation2019). Regardless of whether it is levied through the tax rates or a deduction, the complexity associated with indirect taxes is higher. As shown in , the correlation between tax structure and tax complexity is reported herein.Footnote1 It can be seen that tax structure based on indirect taxes increases the complexity of the overall tax system, and increasing the proportion of direct taxes can help reduce tax complexity.

Figure 1. Correlation between tax structure and tax complexity.

Notes: Tax_struc_1 and Tax_struc_2 represent the proportion of direct taxes in tax revenues and the ratio of direct to indirect taxes, respectively. Tax complexity is calculated using the sum of the squares of the total tax revenue proportion of each tax revenue and then taking its reciprocal.

Source: Authors’ Estimation.

Moreover, the indirect tax burden borne by the company is also greater compared to direct tax burden in China. In Chinese tax context, the enterprise is not the true tax bearer for personal income tax, and for corporate income tax, the company only pays on the premise of its positive pre-tax profit that year. However, regardless of whether a company is profitable, it must pay a value-added tax and business tax if its values increase. Even if the tax burden can be shifted, this part of the cash outflow also increases the enterprise’s operating burden. Therefore, when the profit is 0 or there is a loss, the enterprise may not pay a corporate income tax, while the indirect tax cannot be avoided. Additionally, the existing indirect tax system also fails to support corporate research and development (R&D) (Fan & Gao, Citation2019). Especially, for innovative enterprises, labour costs are often the most important R&D expenditure, but the labour costs paid to support the company's independent R&D cannot be deducted as a tax-entered amount under the current VAT system. By contrast, it can be used as R&D fee for additional deduction before the corporate income tax. As a result, a company will bear more tax burden in a tax system mainly relying on indirect taxes, which may motivate the company to evade taxes.

Second, the tax system’s reliance on indirect taxes does not generally support improvements in governance quality, which is an important factor for a good business environment to enhance tax compliance. Compared to direct taxes, indirect taxes are usually hidden into the prices for goods and services. As such, taxes and prices are not separated, directly distorting the normal market price mechanism, and also creating fiscal illusions (Buchanan & Wagner, Citation1978). To meet the demand for financial expenditures and to promote economic growth, a local government may rely more on indirect taxes, and use fiscal illusion-incomplete information to engage in corrupt activities, which would reduce the quality of governance. Umar et al. (Citation2019) compared government performance in Ghana, Nigeria, and other West African countries, and found that, due to the bad governance, taxpayers are not willing to pay taxes because they are unsatisfied with the level of governance. Liu and Feng (Citation2015) and Liu and Mikesell (Citation2019) found that relying on a tax system centred on indirect taxes supports the government’s ability to engage in corruption. Simultaneously, corrupt governments also tend to rely on more complex indirect taxation systems. Evidence from China also shows that tax evasion is serious where governance and the provision of public goods are perceived as being worse (Ma & Li, Citation2012). These studies indicate that tax systems that rely on indirect taxes can easily lead to corruption activities. Increasing the ratio of direct taxes will help to improve governance, and create a good political and business relationship to improve tax compliance.

In summary, this work considers the following two hypotheses.

Hypothesis 1: Increasing the ratio of direct taxes will help to improve corporate tax compliance.

Hypothesis 2: Increasing the proportion of direct taxes helps to improve corporate tax compliance through the following impact mechanisms: it helps to reduce tax complexity, improve the governance quality of government and reduce tax collection efforts.

3. Empirical methodology and data

3.1. Econometric specification

This section discusses the empirical strategy, with the objective of testing the hypotheses proposed above. Based on the previous theoretical analysis, the fixed effect model is set as follows:

(1)

(1)

where

represents the tax compliance of corporation i of industry c in prefecture j and year t. The variable

represents the prefectural tax structure;

represents control variables, such as capital intensity and industrial structure and so on.

is the industry-year effect, which is used to control the factors that change over time and do not change over time in the industry.

is the individual effect;

is the prefecture fixed effect;

is the time fixed effect; and

is the random disturbance. All regressions’ standard errors are clustered at the city-industry level. According to the previous hypotheses, it is expected that

If the value is significantly positive, the optimising the tax structure supports the increase in tax compliance.

3.2. Variables

3.2.1. Tax compliance

As mentioned before, in China’s existing tax system, tax evasion is common, especially for corporate income tax (Zhang et al., Citation2020). Therefore, this article first focuses on corporate income tax compliance in the base regression, then uses other measures to represent overall tax compliance and indirect tax compliance. As shown in previous literature, the most commonly used methods that measure tax compliance are account-tax difference method (ATDM), regression residual method of returns (RRMR), NIA, and the ATRM (Cai & Liu, Citation2009; Desai & Dharmapala, Citation2006; Hanlon & Heitzman, Citation2010). The ATDM and RRMR are often applied to measure tax compliance of listed companies. Similarly, the NIA and ATRM are usually used in the measurements for non-listed companies, because such companies do not disclose their book income, and taxable income cannot be obtained either. In this study, the data are taken from Chinese Industrial Enterprise Database from 1998 to 2007, so ATRM is first used to measure corporate tax compliance. Then, the NIA is applied for robustness tests. Specifically, the ratio of income tax paid to total profit is used to denote corporate tax compliance. To further verify the robustness of the conclusions, and avoid measuring errors, both measurements are used for robustness checks: the sum of direct and indirect taxes as a part of operating income represents the overall tax compliance, while indirect taxes as a proportion of operating income are used to denote indirect tax compliance.

3.2.2. Tax structure

Tax system is an important part of a country's institutional system, which reflects the allocation of tax burden across taxpayers. According to the difficulty of tax burden shifting, direct taxes are mainly personal income tax and corporate income tax, while indirect taxes are usually value-added tax and business taxes. Overall, China's tax system is characterised by two main factors: indirect tax and corporate sources, which account for more than 70% and 90% of the total tax revenues, respectively. As shown in the previous literature, the proportion of direct taxes in tax revenues (Tax_struc_1) is used, and the ratio of direct to indirect taxes (Tax_struc_2) represents the tax structure (Liu & Feng, Citation2015; Liu & Mikesell, Citation2019).

3.2.3. Other control variables

To further reduce the problems of heteroscedasticity and endogeneity, this article also considers the following variables at the enterprise and prefectural level. As reported by Cai and Liu (Citation2009) and Chen and Chen (Citation2019), the corporate variables are capital intensity, number of employees, age, and loan capacity. Among these variables, capital intensity is represented by net fixed assets as a proportion of total assets; the higher it is, the lower the company’s actual tax rate is. Large-scale enterprises usually have more standardised operations and management, and a higher cost of tax evasion, making their level of tax compliance significantly higher. This is calculated using the natural logarithm of the number of employees. Financial constraint is expressed as the proportion of corporate financial expenses to total assets. Lower financing constraints make it easier to obtain bank loans, increasing the level of external oversight.

Prefectural controls are also considered, including economic development, urbanisation, industrial structure, population density, local fiscal expenditure, and prefecture-level overall tax burden. Economic development indicates the ability of a region to provide high-quality public services, which could help to improve corporate tax compliance. Urbanisation means the concentration of urban population. On the one hand, it helps improve the quality of government public services, which in turn helps improve corporate tax compliance. On the other hand, overcrowding of the population also means traffic jams and crime rates, which may lead to an increase in corporate tax evasion. Therefore, theoretically, the impact of urbanisation on corporate tax compliance is uncertain. The increase in population density usually means the accumulation of human capital, especially the accumulation of high-quality human capital helps to improve corporate tax compliance. The fiscal expenditures indicate the size of the government, and the expansion of the size of the government will reduce the quality of public services and intensify corporate tax evasion. The overall tax burden indicates tax efforts of the local government, and it can be seen that the larger the tax burden, the higher the actual corporate tax rate.

3.3. Data

The data used in this article are taken from Chinese industrial enterprise database for the years between 1998 and 2007. Prefectural data, such as value-added tax, individual income tax, and corporate income tax data, are from corresponding year Quanguo Dishixian Caizheng Tongji Ziliao. Other data are collected from China Statistical Yearbook for Regional Economy. The following data processing is performed based on Brandt et al. (Citation2012): First, synthesise unbalanced panel data into balanced from 1998 to 2007, using the company’s legal person code, legal person name, province and prefecture-level city (including state union), legal representative, main business activities or main products, opening year, and regional code in different years. Second, delete data missing key variables, such as total assets, number of employees, total industrial output value, net fixed assets, product sales, and profit values that are less than zero. Third, delete observations that are clearly not in compliance with accounting standards, such as total assets that are less than current assets, total assets that are less than net fixed assets, total depreciation that is less than current depreciation, sales that are less than five million yuan, and an annual average number of employees that is less than eight. Fourth, all key variables are tailed at 1% and 99% quantiles. Finally, 1.36 million observations are obtained as the total sample. provides a detailed description of all main variables.

Table 1. Summary of statistics.

4. Empirical results

4.1. Baseline results

The baseline results are reported in . As shown, Tax_struc_1 and Tax_struc_2 represent the proportion of direct taxes to total tax revenues, and direct versus indirect taxes, respectively. Columns 1 and 4 only control the tax structure variables, and the results show a strong and positive relationship between tax structure and tax compliance, which is significant at the 1% level. This indicates that raising the proportion of direct taxes can help reduce tax evasion and increase corporate tax compliance. Given this, the Chinese government should gradually reduce the proportion of indirect taxes. Columns 2 and 5 include controlled enterprise explanatory variables based on Columns 1 and 4, and the factors that change within the cities. Columns 3 and 6 continually add the regional variables listed above.

Table 2. Baseline results: fixed effect.

All these results indicate that the impact of tax structure on corporate tax compliance remains significantly positive at the 1% level. Using Columns 3 and 6 as examples, increasing the tax structure represented by Tax_struc_1 and Tax_struc_2 by one unit increases corporate tax compliance by 0.8 and 2.4 percentage points, respectively. This result means that relying on indirect taxes enhances corporate tax evasion.

In addition, the number of employees, finance constraints, and age are significant and positive, indicating that as the company gets older and matures in business, it faces strict external financial oversight in China. The regression results of regional variables show that increasing the level of public services, and thereby increasing the proportion of fiscal expenditures, will help reduce the actual tax rates of enterprises. This is consistent with the Tiebout (Citation1956) hypothesis of voting with one’s feet. Government competition, including tax incentives and infrastructure construction, will attract enterprises to flow into the region, reducing the actual tax rates of enterprises. Increasing the level of government expenditures means increasing government scale and fiscal pressure, which does not necessarily improve the level of local tax collection and management. However, the population density, indicating the agglomeration effect of local human capital, can help improve company tax compliance, because companies that operate according to standards and laws are often the first choice for human capital, especially high-skilled human capital. This can lead to a higher level of tax compliance.

4.2. Robustness

The baseline results show that gradually increasing the ratio of direct taxes has a significant and positive effect on corporate tax compliance. However, the reliability of this conclusion may be misleading due to measuring errors and endogeneity. To test the robustness, several measurements are taken for a sensitivity analysis. First, estimates are replaced with the NIA, an approach often used in other studies (Cai & Liu, Citation2009). Second, instead of using actual tax rate, new variables are constructed to represent the tax system through the sample used. Third, in order to compare the regression results with Cai and Liu (Citation2009), the initial period of the sample is excluded to facilitate a further robust test, by using years from 1998 to 2001 and years from 2003 to 2007. Fourth, the overall tax burden and indirect tax burden are also used to indicate tax compliance.

4.2.1. Alternate estimation method

As discussed above, the NIA method proposed by Cai and Liu (Citation2009) is also commonly used to measure corporate tax compliance based on industrial enterprise data (Brandt et al., Citation2012). According to the NIA method, the reported profit of an enterprise is positively correlated with its real profit, and the sensitivity coefficient between the two is between 0 and 1. A higher value is associated with a higher degree of tax compliance by the enterprise. Since the real profit of an enterprise is not available, it is denoted by the imputed profit. It is calculated by deducting intermediate inputs, financial expenses, wages and benefits, current depreciation, and value-added tax from the gross industrial output value. Then, the reported profit and imputed profit of enterprises are divided by total assets for standardisation. The specific model is set as follows:

(2)

(2)

where,

represents the company's reported profits. The variables

represent time and regional dummy variables, respectively. The variable

denotes imputed profit. The other variables are defined the same way as in model (1). The variable

is the main coefficient this article is concerned with. According to Cai and Liu (Citation2009), a robust and reliable conclusion will increase the sensitivity between the reported profit and the imputed profit, so

will be greater than 0. presents the results. The main variable of interest is also significantly positive at the 1% level, further supporting the robustness of this study’s results.

Table 3. Robustness: national income accounting method.

4.2.2. Change independent variables and time window

First, based on Deng (2019), all direct and indirect taxes of every enterprise in prefecture-level cities are added, and then new variables Tax_struc_3 and Tax_struc_4 are constructed to replace tax_struc_1 and tax_struc_2, respectively. As most of the industry categories in the database begin with ‘C’ manufacturing industry, these accounts for more than 90% of all industries, and these industries are dominated by the value-added tax. Therefore, the value-added tax can be used to represent the indirect tax, and the direct tax is represented by corporate income tax. Second, it has been confirmed in the literature that the tax compliance of some companies has reduced due to the tax sharing reform implemented in 2002. In order to avoid the interference of this reform on the conclusions of this article, robustness is tested using two sub-sample intervals from 1998 to 2001 and from 2003 to 2007.

The results are presented in , which shows that the estimation coefficient is still significantly positive at the 1% level. Regardless of whether the index is a used or newly constructed sample, all tests confirm that the basic conclusion is robust.

Table 4. Regression with new variables and different time intervals.

4.2.3. Replace the dependent variable

To estimate the effect of tax structure on overall tax compliance and indirect tax compliance, the proportion of the sum of business tax, value-added tax, and corporate income tax to total business income is used to denote overall tax compliance, and the proportion of the sum of value-added tax and business tax to total business income is used to represent indirect tax compliance. If optimising the tax structure simultaneously and significantly increases the overall tax compliance and indirect tax compliance of enterprises, it further supports the robustness of the basic conclusions. The specific results are shown in . It can be seen that after replacing the explained variables, the impacts of the tax structure on the two new explained variables are significantly positive at the level of 1%. This demonstrates that the tax system expressed by increasing the proportion of the direct tax effectively improves the tax compliance of enterprises.

Table 5. Replacement of the interpreted variable.

4.2.4. Considering the full sample with negative profits

In the baseline regression, the enterprises with negative financial results are removed, which may motivate enterprises to underreport incomes or over report expenditures in order to not pay corporate income tax. Hence, they have the incentive to whitewash the financial results to be negative. Although the proportion of such enterprises is relatively small and does not affect the validity of the base conclusions, it may still cause bias in the estimation results. Therefore, we have reconsidered this part of the sample into the full sample to test the robustness of our conclusions. The results are shown in . It can be seen that the conclusions still hold when the firms with negative financial performance are further considered, thus illustrating the robustness of the findings.

Table 6. Considering the full sample with negative profits.

Table 7. Instrumental variable method.

4.2.5. Endogeneity

In the baseline regression, a multi-dimensional fixed effect model is applied to estimate the effect of the tax system on tax compliance. To alleviate endogeneity, the regional effect is also controlled to absorb the effects of these factors that change within regions, and robust checks are performed such as replacing the variables and changing the time window. However, this cannot completely overcome the endogeneity (Liu & Feng, Citation2015). As such, city-level factors that cannot be absorbed over time, local medium and long-term economic development goals, may also affect the local tax structure which is relatively stable in the short term. Hence, the tax structure may remain endogenous to some extent. Accordingly, this part analyzes the endogeneity by constructing instrumental variables (2SLS).

The instrumental variable method relies on both correlation and exogeneity: an applicable instrumental variable needs to be strongly correlated with the endogenous variable, and the residual term must be independent. If these two conditions are not met, the instrumental variable method is no longer applicable. Given the characteristics of the sample data, based on Liu and Feng (Citation2015), the weighted average of the tax structure for sibling cities within the same province in corresponding periods is used as the instrumental variable of the prefectural tax structure. This approach is justified as follows. First, municipal governments at different levels within the same province are under the same provincial government leadership, so the fiscal and tax systems of different prefecture-level cities are generally similar. As such, the weighted average of other sibling cities effectively represents the local tax structure. Second, logically, the weighted average of the tax structure of other sibling cities should not directly affect the local enterprises’ tax behaviour, which theoretically meets the conditions of exogeneity.

reports the results of instrumental variables by using the 2SLS method. The first stage shows that the effects of instrumental variables on tax structure are all significantly positive at the level of 1%. Moreover, F values exceed 10, indicating that the constructed instrumental variables do not have weak identification problems. In addition, the regression coefficients of the second stage (Column 3 and 6) show that when the tax structure represented by direct tax increases by 1 unit, the corporate tax compliance increases by 0.016 and 0.06, respectively. Both results are significant at the 1% significance level. Compared with the baseline regression results, the regression coefficients of the second stage change significantly. However, their coefficient signs are consistent with the results of the baseline regression, confirming the robustness of the basic regression conclusion.

4.3. Mechanism

As analysed before, increasing the proportion of direct taxes can help reduce the complexity of tax structure, improving the quality of government governance and tax collection efforts, which would improve corporate tax compliance. To verify the existence of the mechanism described above, according to Liu and Mikesell (Citation2019), the Herfindahl–Hirschmann index (HHI) is used to represent the complexity of the tax structure. It is measured by the sum of squares of the ratio of each tax type to the total tax. The natural logarithm of the inverse is taken to represent it. A larger HHI value is associated with a higher complexity index for the tax. Second, local tax efforts, first proposed by Lotz and Morss, are calculated using the proportion of actual tax revenue and predicted tax revenue. To calculate the city’s predicted tax revenue, the following factors are used: per capita GDP, the proportion of secondary and tertiary industries, demographic characteristics, urbanisation level, and the degree of opening to the outside world. Then, the fixed-effect model is used to fit the predicted tax revenue of each region. Third, the number of corruption cases per 10,000 public officials is used to assess the quality of governance. Due to the missing city-level corruption data, this article uses the provincial data instead.

presents the results of the impact mechanism of tax structure on tax compliance. It can be seen that optimising the tax system has a significant effect on the three mechanism variables: it reduces the complexity of the tax structure, improves local tax efforts, and decreases corruption, thus enhances the quality of governance. This means that while optimising the tax structure, the government should enhance governance quality, improve the local business environment, and strengthen the collection of direct taxes to achieve the full collection of receivables.

Table 8. Impact mechanism.

5. Discussion and conclusion

In the developing countries, optimising the tax structure can help reconstruct the relationship between the government and the market, and enhance the enterprises’ competitiveness. Since the reform of the tax-sharing system in 1994, China's tax structure has been continuously optimised. Previous studies have mainly analysed the economic effects of direct and indirect tax reforms from macro and micro perspectives. Few studies have examined the impact of optimising tax structures on corporate tax compliance. To address this topic, this article uses a multi-dimensional fixed effect model to test the effect of the tax system on enterprise tax compliance. The results are as follows. First, tax structure, represented by increasing the proportion of direct tax, can significantly improve the tax compliance of enterprises. This conclusion remains reliable after robustness checks and endogeneity tests. Second, the mechanism shows that optimising the tax structure supports a reduction in the complexity of the tax system and the resulting tax costs. Such an optimisation may also force the government to improve the relationship with the market, enhance the quality of governance, and strengthen tax collection efforts.

Previous studies showed that a tax system mainly relying on indirect taxes is likely to lead to local government corruption and reduce the quality and efficiency of public services (Liu & Feng, Citation2015; Liu & Mikesell, Citation2019). This article further verifies that tax structure that increases the proportion of direct taxes is helpful to improve corporate tax compliance. The studies on relationship between tax structure and corporate tax compliance from a micro-perspective are relatively few, so this article fills this gap. However, due to the failure to update the data of Chinese industrial enterprises in time, this article used the data from 1998 to 2007 to conduct a micro-empirical study. Based on the relatively large sample size, it covers most of the Chinese enterprises. Therefore, the conclusion of this article can also provide micro-evidence for the transformation of China's tax system.

This article’s conclusions can also help inform China’s approach to tax reform. China's current tax arrangements do not align with the current situation of economic development, inhibiting fair economic development. The current tax structure, emphasising the indirect tax, has been in a state of imbalance for a long time. This is because the indirect tax burden embedded in goods and services aggravates the burden on enterprises, and may increase the motivation to evade taxes. This article concludes that, in the context of the current global wave of tax reduction, optimising the tax structure will not increase the probability of tax evasion. A reasonable tax structure arrangement provides an institutional reason for taxpayers to pay their tax according to the law. Moreover, optimising the tax structure requires the government to address the relationship between the government and the market, provide more efficient public goods for enterprise development, and improve the quality of its governance. Taking these actions can foster good market and institutional environments that encourage corporate tax compliance.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 Since China's tax revenue mainly comes from corporate income tax, personal income tax, value-added tax and business tax. According to Liu and Mikesell (Citation2019), Chapman and Gorina (Citation2012), the tax complexity index is computed by using the inverse of the sum of squares of the corporate income tax, personal income tax, value-added tax and business tax used in the article as the proportion of the total tax revenues. And the larger the index, the higher the tax complexity.

References

- Alm, J., Bahl, R., & Murray, M. N. (1990). Tax structure and tax compliance. The Review of Economics and Statistics, 72(4), 603–613. https://doi.org/10.2307/2109600

- Besley, T., & Persson, T. (2014). Why do developing countries tax so little? Journal of Economic Perspectives, 28(4), 99–120. https://doi.org/10.1257/jep.28.4.99

- Brandt, L., Van Biesebroeck, J., & Zhang, Y. (2012). Creative accounting or creative destruction? Firm-level productivity growth in Chinese manufacturing. Journal of Development Economics, 97(2), 339–351. https://doi.org/10.1016/j.jdeveco.2011.02.002

- Buchanan, J. M., & Wagner, R. E. (1978). Dialogues concerning fiscal religion. Journal of Monetary Economics, 4(3), 627–636. https://doi.org/10.1016/0304-3932(78)90056-9

- Cai, H., & Liu, Q. (2009). Competition and corporate tax avoidance: Evidence from Chinese industrial firms. The Economic Journal, 119(537), 764–795. https://doi.org/10.1111/j.1468-0297.2009.02217.x

- Chapman, J., & Gorina, E. (2012). Effects of the form of government and property tax limits on local finance in the context of revenue and expenditure simultaneity[J]. Public Budgeting & Finance, 32(4), 19–45. https://doi.org/10.1111/j.1540-5850.2012.01022.x

- Chau, G., & Leung, P. (2009). A critical review of Fischer tax compliance model: A research synthesis. Journal of Accounting and Taxation, 1(2), 34–40. https://doi.org/10.5897/JAT09.021

- Chen, S. X. (2017). The effect of a fiscal squeeze on tax enforcement: Evidence from a natural experiment in China. Journal of Public Economics, 147, 62–76. https://doi.org/10.1016/j.jpubeco.2017.01.001

- Chen, Z., & Chen, Q. (2019). Energy Efficiency of Chinese Firms: Heterogeneity, Influencing Factors and Policy Implications. China Industrial Economics, 12, 78–95. doi:10.19581/j.cnki.ciejournal.2019.12.005.

- Chen, X., Hu, N., Wang, X., & Tang, X. (2014). Tax avoidance and firm value: evidence from China. Nankai Business Review International, 5(1), 25–42. https://doi.org/10.1108/NBRI-10-2013-0037

- Cummings, R. G., Martinez-Vazquez, J., McKee, M., & Torgler, B. (2009). Tax morale affects tax compliance: Evidence from surveys and an artefactual field experiment. Journal of Economic Behaviour & Organisation, 70(3), 447–457. https://doi.org/10.1016/j.jebo.2008.02.010

- Desai, M. A., & Dharmapala, D. (2006). Corporate tax avoidance and high-powered incentives. Journal of Financial Economics, 79(1), 145–179. https://doi.org/10.1016/j.jfineco.2005.02.002

- Fan, Z., & Gao, Y. (2019). How to promote the tax reform of high quality development. Exploration and Free Views, 7, 106–113. https://doi:CNKI:SUN:TSZM.0.2019-07-008

- Fisman, R., & Wei, S. J. (2004). Tax rates and tax evasion: evidence from “missing imports” in China. Journal of Political Economy, 112(2), 471–496. https://doi.org/10.1086/381476

- Gómez Sabaini, J. C., & Jiménez, J. P. (2012). Tax structure and tax evasion in Latin America (No. 118), Naciones Unidas Comisión Económica para América Latina y el Caribe (CEPAL). http://hdl.handle.net/11362/5350

- Hanlon, M., & Heitzman, S. (2010). A review of tax research. Journal of Accounting and Economics, 50(2-3), 127–178. https://doi.org/10.1016/j.jacceco.2010.09.002

- Liu, Y., & Feng, H. (2015). Tax structure and corruption: cross-country evidence. Public Choice, 162(1/2), 57–78. https://www.jstor.org/stable/24507571 https://doi.org/10.1007/s11127-014-0194-y

- Liu, C., & Mikesell, J. L. (2019). Corruption and tax structure in American states. The American Review of Public Administration, 49(5), 585–600. https://doi.org/10.1177/0275074018783067

- Ma, G., & R., Li, L., X. (2012). Government size, governance and tax evasion. The Journal of World Economy, 35(6), 93–114. https://doi:CNKI:SUN:SJJJ.0.2012-06-008.

- Milliron, V. C. (1985). A behavioural study of the meaning and influence of tax complexity. Journal of Accounting Research, 23(2), 794–816. https://doi.org/10.2307/2490838

- Ming, D. (2019). Effective corporate income tax and corporate capital structure. Business Management Journal, 41(9), 175–190. https:// https://doi.org/10.19616/j.cnki.bmj.2019.09.011

- Richardson, G. (2006). Determinants of tax evasion: A cross-country investigation. Journal of International Accounting, Auditing and Taxation, 15(2), 150–169. https://doi.org/10.1016/j.intaccaudtax.2006.08.005

- Tiebout, C. M. (1956). A pure theory of local expenditures. Journal of Political Economy, 64(5), 416–424. https://doi.org/10.1086/257839

- Umar, M. A., Derashid, C., Ibrahim, I., & Bidin, Z. (2019). Public governance quality and tax compliance behavior in developing countries: The mediating role of socioeconomic conditions. International Journal of Social Economics, 46(3), 338–351. https://doi.org/10.1108/IJSE-11-2016-0338

- Zhan, X., & Liu, W. (2020). Chinese fiscal decentralization and target management of local economic growth: Empirical evidence from work reports of provincial and municipal governments. Management World, 36(3), 23–39. doi:10.19744/j.cnki.11-1235/f.2020.0032

- Zhang, K., Ouyang, J., & Li, W. (2020). Why tax cuts cannot reduce the corporate burden: Information technology, taxation capacity and corporate tax evasion. Economic Research Journal, 50(3), 116–132. https://kns.cnki.net/kcms/detail/detail.aspx?FileName=JJYJ202003011&DbName=CJFQ2020