?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article explores the spatial heterogeneity and time-varying nature of FDI determinants. It also examines the impact of the Belt and Road Initiative (BRI) on regional FDI inflows. Applying both the long-term static model and the short-term dynamic model to a provincial-level dataset in China over the 1979–2018 period, we find that FDI is positively affected by market size, labour costs, openness, transport infrastructure, human capital, and the exchange rate, but negatively affected by population, and more importantly, these effects are heterogeneous across regions and over different time periods. We also find that provinces directly involved in the BRI became less attractive to foreign investors after the launch of the BRI in 2013.

1. Introduction

Foreign direct investment (FDI), as an important part of globalization since the 1980s, has been growing dramatically worldwide and has drawn extensive research attention over the past few decades. A large body of literature focuses on the impact of FDI on economic growth, but consensus is yet to be reached. Conflicting empirical evidence suggests that the impact of FDI may be country-specific and can be positive (Cai, Chen, and Fang Citation2018; Paul & Feliciano-Cestero 2019), negative (Doytch and Merih Citation2011), or insignificant (Anderson, Larch, and Yotov Citation2019), depending on the economic, institutional, technological conditions, human capital, etc., in host countries (Paul and Feliciano-Cestero Citation2021).

China, the largest developing country in the world, has experienced impressive economic growth and a dramatic increase in FDI inflows since the late 1970s. Over the past four decades, the economic growth and FDI inflows share a similar pattern of increasing rapidly but having an uneven distribution across regions, which has induced the debate over whether FDI is a contributing factor to regional inequality. Some studies claim that FDI leads to more poverty, isolation, neglection of local capabilities, and regional inequality (Roser and Cuaresma Citation2016), while others believe the opposite is true and that FDI can promote equality, reduce poverty, and accelerate the convergence process (McGrattan Citation2012). Wei, Yao, and Liu (Citation2009) suggest that FDI cannot be blamed for causing regional inequality, but the uneven distribution of FDI has caused regional growth disparities.

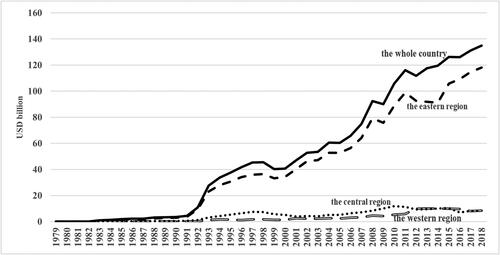

As shown in , the actual FDI used in China rocketed to $11 billion in 1992 after Deng Xiaoping’s ‘Southern Tour’. As the momentum continued, China became the largest FDI recipient among developing countries in 1996, surpassing the US and becoming the world’s most popular FDI destination. China’s total FDI amount climbed from $53.51 billion in 2003 to $134.97 billion in 2018. clearly exhibits the significant heterogeneity of FDI inflows across regions and over time in China. The east coastal region enjoyed preferential government policies, such as lower income tax rates and reduced tariffs for imports used in the production of exports, during China’s early attempts to attract FDI. Researchers argue that the uneven geographical distribution of FDI in China is mainly due to the initial preferential policies favouring the eastern coastal provinces (Yu, Xiangyong, and Xian Citation2008). However, similar preferential policies have been applied throughout the entire country since the late 1990s, while FDI inflows in inland China have failed to catch up. The eastern coastal region received more than 90% of the total FDI in China before 1992 and dropped slightly to 87% in 2018. The data indicate that the differences in the ability to attract FDI across regions are not driven by preferential policies. Against this backdrop, this article attempts to explain why inward FDI is unevenly distributed across regions by investigating the spatial heterogeneity and time-varying nature of FDI determinants.

Figure 1. Actual FDI inflows in China, 1979–2018.

Sources: China Statistical Yearbooks (1999–2019); China Statistical Data of 50 Years 1949–1998.

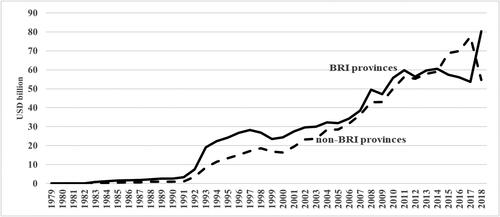

Moreover, the ability to attract FDI is not only determined by the host country's internal factors, but also influenced by the external environment. President Xi Jinping announced the Belt and Road Initiative (BRI) in September 2013, which aims to connect China to countries along the BRI, thereby promoting China’s opening up from coastal areas to inland areas. plots actual FDI inflows in BRI and non-BRI provinces over the 1979–2018 period. FDI in BRI provinces was slightly higher than that in non-BRI provinces before the launch of the BRI in 2013 but decreased sharply during the 2013–2017 period, followed by a surge in 2018. Undoubtedly, the BRI has significant implications for international trade and FDI, while the literature on the effect of the BRI on FDI is inadequate. As such, this study investigates how the distribution of inward FDI is affected by the BRI.

Figure 2. Actual FDI inflows in BRI and non-BRI provinces in China, 1979–2018.

Sources: China Statistical Yearbooks (1999–2019); China Statistical Data of 50 Years 1949–1998.

Applying both a long-run static model and a short-run dynamic model with an error-correction mechanism (ECM) to a provincial-level panel dataset over the 1979–2018 period, this article finds that FDI is positively affected by market size, labour costs, openness, infrastructure, human capital, and the exchange rate but negatively affected by population, and more importantly, these effects are heterogeneous across regions and over different time periods. We also find that the FDI distribution is affected by the BRI – provinces directly involved in the BRI became less attractive to foreign investors after the BRI launch in 2013. Our results are robust to different model specifications and estimation techniques.

This study adds new knowledge to the literature on FDI from three aspects. First, the extensive literature on FDI inflows addresses the following two broad issues: the impact of FDI on host countries and the driving factors of FDI. The literature, however, assumes a homogeneous effect of each driving factor on FDI. Our study provides evidence for heterogeneity in the effects of FDI determinants across regions and over time. Second, our study considers both the static effect in the long run and the dynamic effect in the short run, complementing the literature that mainly focuses on the static effect. Third, our study extends the literature on FDI from the perspective of foreign policies and the external environment by documenting a negative impact of the BRI on FDI inflows.

The rest of this article proceeds as follows. Section 2 presents the literature review. Section 3 illustrates the empirical models and data. Section 4 interprets the empirical results, and Section 5 concludes with policy implications.

2. Literature review

2.1. FDI determinants

FDI plays an important role in promoting MNE growth, industrial upgrading, and ultimately, economic development; hence, FDI has attracted extensive attention from MNE managers, policymakers, and researchers. The literature classifies FDI determinants at the following three levels: the micro, macro, and strategic levels (Keeley and Matsumoto Citation2018; Paul and Feliciano-Cestero Citation2021). The microlevel determinants focus on firm-specific factors, such as ownership, product advantage, cost advantage, economies of scale, multiplant economy, advanced technology, marketing, and product distribution. The macrolevel factors include market size, growth, taxation, infrastructure quality, political stability, exchange rates, and regulatory constraints in host countries. The long-run strategic factors include protecting existing foreign markets, diversifying business activities, gaining or maintaining a foothold in host countries, and complementing other investments.

Research on FDI from the macroeconomics perspective generally focuses on the following factors that affect FDI inflows in the host country: market size (demand), labour cost, international trade, infrastructure, human capital, population, exchange rate, country risk, institutional regime, taxes, and geographical location. The size of the economy directly indicates the market demand and market size. Product cycle theory indicates that market-share extension is the critical strategy utilized by mature multinational corporations (Dunning Citation1988). The literature generally agrees that market size has a positive impact on FDI inflows (Lin, Hsiao, and Lin Citation2015).

Lowering labour costs is an effective way of maximizing capital returns, especially in labour-intensive manufacturing industries. Foreign investors tend to take advantage of the host country’s cheap factor inputs where possible. Sun, Tong, and Yu (Citation2002) find that wages had a positive relationship with FDI inflows before 1991 but a negative relationship subsequently. The mainstream empirical research suggests that low wages in host countries encourage FDI (Rong et al. Citation2020). On the other hand, human capital not only raises output but also enables firms to use advanced technology in production. Cleeve, Debrah, and Yiheyis (Citation2015) suggest that human capital exerts a significant influence on FDI in Africa, and the results are robust to different measures, while Coughlin and Segev (Citation2000) argue that illiteracy has a negative effect on FDI.

A country’s openness indicates the extent to which the host country integrates with the rest of the world. Many studies find that openness and trade are complementary, and the higher the international trade (exports and imports) is, the higher inward FDI will be in the host country (Yao Citation2006; Sanchez-Martin, Arce, and Escribano Citation2014). However, some cross-country studies find that international trade and FDI are substitutes and negatively related (Horst Citation1972). If other things remain the same, the higher the international transportation costs and tariff/nontariff trade barriers are, the greater the amount of FDI that firms will undertake in the host country. Moshfique et al. (Citation2018) finds that trade freedom has a strong positive impact on the inflow of FDI. Hence, the exact relationship between the openness of the host country and FDI is an empirical issue.

An economy with good infrastructural investment is more attractive to foreign investors. Blyde and Molina (Citation2015) indicate that a better-developed transportation infrastructure is beneficial to a host country in terms of attracting FDI because foreign firms might be unfamiliar with the environment of the host country. Empirical evidence supports the importance of infrastructure in FDI location decisions (Hou et al. Citation2020). On the other hand, Peck (Citation1996) argues that although the presence of certain types of basic infrastructure may be significant in attracting the initial interest of potential new investors, some infrastructure types are designed for the specific demands made by new investors. The research results of Alfalih and Hadj (Citation2020) show that infrastructure has no impact on FDI in the short or long term. In the same vein, Coughlin and Segev (Citation2000) show that transportation did not yield statistical significance in attracting FDI.

The ‘new’ location theory (Krugman Citation1991; Venables Citation1993) emphasizes the ‘Pecuniary’ externalities associated with demand and supply linkages, such as the possibility of using joint networks of suppliers and distributors. It is also argued that knowledge-enhancing activities can only partly be appropriated by firms, implying that an externality is created and diffused to other firms, thereby reducing their costs (Romer Citation1986). If knowledge spill-overs and pecuniary externalities are important for a firm’s competitiveness, population forces will increasingly influence a firm’s location decisions. Thus, population is expected to be positively related to inward FDI.

The impact of exchange rates on FDI has been examined in terms of changes at bilateral exchange rate levels between countries and exchange rate fluctuations. Froot and Obstfeld (Citation1991) argue that the real depreciation of the host country's currency benefits home-country purchasers of host country assets, thus leading to an increase in FDI inflows. Harms and Knaze (Citation2021) assert that exchange rate fluctuations have an impact on FDI and that countries with nonfloating exchange rate systems tend to attract more FDI. In general, the higher the ratio of the host country's currency to the US dollar, the more FDI the host country absorbs.

In short, the literature on FDI determinants is extensive and mainly focuses on their static and assumed-homogeneous impacts. Our study extends the literature by exploring the spatial heterogeneity and time-varying nature of FDI determinants in both static and dynamic settings.

2.2. The BRI and FDI

FDI is also affected by the changing international political and economic environment, such as political stability, international cooperation, and free trade areas. After China joined the WTO in 2001, FDI inflows increased dramatically. However, regional economic disparities are significant, especially between the coastal and noncoastal central and western provinces. The coastal region has developed much faster and has benefited from easy access to sea routes at lower transportation costs. The geographical proximity of the coastal provinces to Hong Kong, Macau, Taiwan, Japan, and Korea makes them more attractive to foreign investors. Partially to address the regional disparity, China launched the BRI in 2013. The BRI is a plan to construct trade-boosting infrastructure projects not only for China but also for approximately 65% of the world’s population, covering one-third of the world’s GDP, and one-quarter of the total world trade. The core aim of the BRI is to promote interconnection between China and countries along the BRI and beyond, reaching out to Europe and African countries. Since the BRI was launched in 2013, international trade and investment between China and BRI countries have also increased significantly. China’s trade with BRI countries and investment in BRI countries reached USD1.1 trillion and USD14.4 billion, respectively, in 2017. In the same year, BRI countries launched 3857 firms in mainland China with USD 5.6 billion in investment.

The BRI has become a powerful platform for regional cooperation and integration and has the potential to enable many emerging and developing BRI countries to catch up and prosper, as well as serving as the impetus for sustainable development and growth worldwide. The BRI has attracted great research interest, and the related literature has addressed a wide range of issues. García-Herrero and Xu (Citation2017) estimate potential increases in trade among BRI countries, reporting considerable benefits to EU countries (especially landlocked countries), Eastern Europe and Central Asia and, to a lesser extent, Southeast Asia. Li, Huang, and Dong (Citation2019) confirm that the overall economic freedom, institutional entities, bilateral trade, GDP and patents of countries along the BRI all have a significant impact on outward FDI. Yu et al. (Citation2020) report that China's export potential to partner countries has increased significantly, especially to ASEAN countries and West Asian countries. Cheng and Qi (Citation2021) focus on the industry selection of China's direct investment in BRI countries and find that China's FDI potential in noncarbon-intensive industries is higher than that in carbon-intensive industries. Since the launch of the BRI, China's outward FDI has increased significantly, which has led to increased TFP in BRI countries (Wu et al. Citation2020) while reducing carbon dioxide emissions in regions along the routes (Li et al., Citation2021). Meanwhile, the BRI has a ‘signalling’ effect on foreign investors that China’s strategic priority has moved from ‘bringing in’ towards ‘going global’. In the short term, the BRI may trigger competition between ‘going global’ and ‘bringing in’ resources. FDI inflows to the BRI provinces decreased significantly compared to non-BRI provinces during the period of 2003–2015 (Luo, Chai, and Chen Citation2019). The limited literature on the relationship between the BRI and FDI primarily focuses on the impact of the BRI on China's outflow of FDI, while our study explores how the BRI affects regional FDI inflows.

3. Research methodology and data

3.1. Long-run static model

The FDI inflow level depends on government policies and local characteristics. In this study, we follow the literature and explain the variations in FDI in terms of market size, labour costs, openness, infrastructure, human capital, population, and exchange rate. Following Yao and Wei (Citation2007), the baseline empirical specification in natural logarithm is as shown in EquationEq. (1)(1)

(1) .

(1)

(1)

where i (i = 1,2, …, 29) and t (t = 1979, …, 2018) denote province i and year t, FDI is the dependent variable, Xit is a set of explanatory variables, including gdp (proxy for market size), wage (labour costs), export (proxy for openness), transport (proxy for infrastructure), human capital, population, exchange rate, and FE is a set of dummy variables to control the year (or period) and province (or region) effects.

In this study, we focus on the varying effect of FDI driving factors across regions and over time. We introduce a set of Region dummy variables and the interaction terms between the explanatory variables and Region dummy variables into EquationEq. (1)(1)

(1) , as shown in EquationEq. (2)

(2)

(2) :

(2)

(2)

where Region includes the dummy variables East, Central and West, taking a value of 1 for provinces in the respective region and 0 otherwise.

denotes the form of the interaction terms between the explanatory variables and Region dummy variables.

We then split the full sample period into the following three subsample periods: the pre-Deng south tour period of 1979–1991, the pre-WTO period of 1992–2000, and the post WTO period of 2001–2018. In a similar vein, we introduce a set of Period dummy variables and the interaction terms between the explanatory variables and Period dummy variables into EquationEq. (1)(1)

(1) , as shown in EquationEq. (3)

(3)

(3) :

(3)

(3)

where Period includes the pre-1992, 1992–2000, and 2001–2018 dummy variables, which take a value of 1 for that subperiod and 0 otherwise.

is the form of the interaction terms between the explanatory variables and Period dummy variables.

3.2. Short-run dynamic models with ECM

The long-run model may be subject to possible spurious results if the variables in the model are not cointegrated. Although other studies (e.g. Yao Citation2006; Yao and Wei Citation2007) have proven that cointegration relationships exist among the variables in the long-run models, it is still useful to run their short-run dynamic forms. The short-run Engel-Granger error-correction mechanism (ECM) model can also test the dynamic relationship between independent variables. If FDI is cointegrated with its influencing factors, the short-term disequilibrium relationship between them can be expressed by an error correction model. We conduct cointegration analysis on the variables to detect the cointegration relationships between the variables, that is, the long-term equilibrium relationships. Then, a short-term model is established based on those long-term relationships, where the error correction term is regarded as an explanatory variable. Moreover, the short-run dynamic model can derive short-run and long-run elasticities at the same time.

Engle-Granger’s ECM for cointegration analysis can be conducted using a two-step approach. The first step is to run a regression of EquationEq. (1)(1)

(1) and derive residuals (

). The second step is to run another regression based on EquationEq. (4)

(4)

(4) below.

(4)

(4)

where Δ denotes the first difference,

is the lagged term of the estimated residuals obtained from the first regression, and

denotes the short-run form of the original production function shown in EquationEq. (1)

(1)

(1) .

If θ is significant and positive, there is a long-run stable cointegration relationship between FDI and the explanatory variables. The main limitation of EquationEq. (4)(4)

(4) is that the long-run coefficients cannot be estimated, and the short-run coefficients have to be estimated in two steps. To overcome these limitations, EquationEq. (4)

(4)

(4) is transformed into EquationEq. (5)

(5)

(5) so that the coefficients can be estimated in one single step.

(5)

(5)

The short-run coefficients are obtained from the first term on the right-hand side of EquationEq. (5)(5)

(5) . The long-run coefficients are obtained from the coefficients derived from

divided byθ. The dependent variable and explanatory variables will be cointegrated if the long-run coefficients and θ are jointly significant.

There are a number of advantages of using the one-step ECM model specified in EquationEq. (5)(5)

(5) to study the dynamic relationship between FDI and its driving factors. First, both short-run and long-run elasticities can be estimated in one step. Second, the long-run disequilibrium can be corrected to give better estimates of the coefficients involved. Third, the problems of nonstationarity and simultaneity can be avoided because all variables are presented in their first (log) differences and predetermined values (lagged terms). Finally, the estimation process is simple, and the results are easy to interpret.

3.3. FDI and the BRI

To examine the impact of the BRI on the distribution of FDI, we introduce BRI_region and BRI_year to the baseline model in EquationEq. (1)(1)

(1) , as shown in EquationEq. (6)

(6)

(6) .

(6)

(6)

where BRI_region takes a value of 1 for provinces directly on the BRI route and 0 otherwise. BRI_year takes a value of 1 for years after 2013, which is when the BRI announced, and 0 otherwise.

3.4. Variables and data

This study employs a panel data analysis for 29 provinces and municipalities over the 1979–2018 period. Tibet is excluded, and the data for Chongqing are merged with those of Sichuan. Data are mainly collected from China Statistical Data 50 Years 1949–98 (NBS, 1999) and the China Statistical Yearbooks (NBS, various years, 1987–2019). The dependent variable FDI is the FDI inflows. GDP is the proxy for market size. Wage is the labour costs of employees in terms of annual salary. Human capital measures the education level, proxied by the number of students enrolled in higher education over the population in each province. Export is measured by the ratio of total exports to the GDP of a province. In China, railroads remain the most efficient mode of transportation for moving raw materials and most heavy-industry products over long distances (Sun Citation1988, pp. 311–68). Consequently, railroad mileage is frequently used as a proxy for transportation capability in the literature. In this article, we use the equivalent mileages of railways, highways and waterways per 1,000 km2 to measure the transportation capability. Transport is used as a proxy for infrastructure. Population is proxied by population density. Exchange rate controls for the impact of fluctuations in the value of the RMB, and we use the US price index to calculate the real exchange rate in terms of RMB against US dollars (RMB units per US dollar). We include the following set of Region dummy variables: East takes the value of 1 for an eastern province and 0 otherwise; Central takes the value of 1 for a central province and 0 otherwise; and West takes the value of 1 for a western province and 0 otherwise.Footnote1 We also include a set of Period variables. Pre-1991 indicates the period pre-Deng’s south tour, taking a value of 1 for years before 1991 and 0 otherwise; 1992–2000 is the period after Deng’s south tour but before WTO entry, taking a value of 1 for these years and 0 otherwise; 2001–2018 is the post-WTO period, taking a value of 1 for years after 2001 and 0 otherwise. BRI_region takes a value of 1 for provinces directly on the BRI route and 0 otherwise. BRI_year takes a value of 1 for years after 2013, which is when the BRI was announced, and 0 otherwise. provides the sample summary statistics. All monetary explanatory variables are measured at the 1990 price level.

Table 1. Summary statistics.

4. Empirical results

4.1. Estimation results from the long-run static model

4.1.1. Baseline model

The long-run static model in EquationEq. (1)(1)

(1) is estimated using OLS for the sample over the 1979–2018 period, and we consider heteroscedasticity and robust standard errors.Footnote2 The results are reported in , where we control the province and year fixed effects in Column (1), the region and year fixed effects in Column (2), and the region and period fixed effects in Column (3). The overall results from our baseline model are consistent with the literature and expectations.

Table 2. The determinants of FDI in China 1979–2018: Long-run static model.

The coefficients on all variables are statistically significant with the expected signs. GDP is found to have a significantly positive impact on FDI, consistent with previous findings in the US and other countries. Provinces with larger markets are attractive to foreign investors. The coefficient on Wage is significant and positive, suggesting that higher labour costs help attract more FDI, consistent with the conclusion in Cheng and Kwan (Citation2000). High wages can reflect more productive quality labour force, which is more attractive to foreign investors. The coefficient on exports is statistically significant in Columns (2) and (3), suggesting that the open-door policy and the resultant expansion of international trade play a positive role in attracting FDI. Transport also shows a significantly positive impact on FDI across all regressions, suggesting that as the investing environment matures, better-developed regions with superior transportation facilities become more attractive to foreign investors. The coefficient on human capital is statistically significant in all regressions, suggesting a positive impact on FDI. Provinces with higher human capital levels are more attractive to foreign investors. We find a negative impact of population on FDI, which is different from the findings in early studies (Head and Ries Citation1996). The possible reason could be that our sample period is long, and we are able to capture the effect that foreign investors tend to escape from more populated provinces due to the diminishing return on FDI in certain ‘hot’ provinces where the costs of production are rising rapidly. We find that the foreign exchange rate is positively associated with FDI, consistent with the expectation that RMB devaluation against the US dollar helps boost FDI. The RMB used to be overvalued in the earlier years of economic reform, which hampers business prospect in China for foreign investors and exporters. The gradual devaluation of the RMB has improved China’s international competitiveness and attracted more FDI.

4.1.2. Regional analysis

From the perspective of development and political factors, China is divided into the following three major regions: eastern, central, and western regions. FDI is very unevenly distributed across regions, and the coastal region has received the lion’s share of the total FDI in recent decades. In this subsection, we investigate how the effect of FDI determinants varies across different regions, namely, the eastern, central, and western regions. The estimation results from EquationEq. (2)(2)

(2) are reported in , where the eastern region is omitted for comparison purposes. The goodness-of-fit values are high in all regressions. Column (1) presents the results from the long-run static model, which is the same as in Column (2) to allow for convenient comparisons. We control for the year fixed effect in Column (2) and the period fixed effect in Column (3). The main effect of all variables is statistically significant with the correct signs, consistent with those from the baseline model.

Table 3. The determinants of FDI in China: Long-run heterogeneity across regions.

In this section, we focus on coefficients on the interaction terms between the region dummy variables and explanatory variables. When introducing interaction terms, the interpretation of the main effect (the individual factor) changes. The coefficient on the individual factor represents its effect on FDI in the omitted control group – the eastern region in our case. The coefficients on the interaction terms capture the heterogeneity of the effects of the explanatory variables on FDI across different regions. As shown in , the effect of GDP is stronger in the central and western regions than in the eastern region, as the coefficients on Centralgdp and West

gdp are positive and statistically significant. A 1% increase in GDP will attract approximately 1% more FDI in the central region than in the eastern region. This effect is approximately three times stronger than that in the western region – attracting approximately 0.3% more FDI than the eastern region. The impact of GDP on FDI is the lowest in the eastern region, suggesting that the market advantage of the eastern region has been declining and that the theory of diminishing marginal efficiency is working.

The coefficient on Wage is positive and significant (1.028), suggesting that high wages help attract more FDI in the eastern region (the omitted group in the regression). The coefficients on Centralwage and West

wage are negative and statistically significant, indicating that the impact of wages on FDI is smaller in the central and west regions. For a 1% increase in labour costs, the increase in FDI in the central region is 0.072% (=1.028–0.956), lower than that in the east region by 0.956% (column 3). Again, we observe this effect is smaller in the western region (weakly significant at the 10% level). A 1% increase in labour costs, causes a 0.693% (=1.028–0.335) increase in FDI, which is smaller than that in the eastern region by 0.335%.

The coefficients on Centraltransport and West

transport are also negative and statistically significant. Infrastructure is less important in attracting FDI in the central and western regions than in the eastern region. Holding all other things equal, with a 1% increase in transport facilities, the increase in FDI is 1.6% smaller in the central region and 0.9% smaller in the western region compared with that in the eastern region.Footnote3 Human capital helped raise more FDI in the central and western regions than in the eastern region, as indicated by the positive significant coefficients on Central

human capital and West

human capital. This effect is stronger in the central region than in the western region. Population also helps raise more FDI in the central and western regions than in the eastern region. Interestingly, this effect is stronger in the western region than in the central region. The impact of exchange rates on attracting FDI in the weaker in the central and western regions. As shown in Column (3), with a 1% increase in the exchange rate, compared to the eastern region, the western and central regions attract less FDI by 2.3% and 1.5%, respectively. We find no evidence for the varying impact of exports on FDI across different regions, as the coefficients on Central

export and West

export are insignificant.

In summary, the estimation results in support our expectation that since 1979, all regions have experienced tremendous growth in attracting FDI. However, the effects of those main drivers are different across regions, which partially explains the unevenly distributed FDI across regions.

4.1.3. Subperiod analysis

From the perspective of China's opening up policy, the degree of China's opening up to the outside world is gradually expanding, so the development speed of FDI is different in different periods. In this subsection, we study how the driving factors of FDI have different influences during different time periods (pre1992, 1992–2000, and 2001–2018). reports the estimated results of EquationEq. (3)(3)

(3) . For comparison purposes, pre-1992 is omitted in all regressions. Column (1) reports the results from the baseline long-run static model, which is similar to Column (3) in , for easy comparison. We control the provincial fixed effect in Column (2) and the region fixed effect in Column (3). All regressions have high goodness of fit values. The main effects of all variables are statistically significant and marked correctly, consistent with the baseline model in Column (1).

Table 4. The determinants of FDI in China: Long-run heterogeneity over time.

In this section, our main interest is the coefficients of the interaction terms between the Period variables and explanatory variables, which capture the differences in the effects of FDI determinants during different periods. As shown in , wages have a positive impact on FDI in the pre-1992 period. For a 1% increase in labour costs, the increase in FDI is 2.727% (Column 3). At the low wage level in the early years, foreign investors prefer a high wage labour force, perhaps for higher productivity. This effect turns negative after Deng Xiaoping's Southern Tour, as the coefficients on the interaction terms (1992–2000 × wage and 2001–2018 × wage) are negative and statistically significant with a larger magnitude. Rising labour costs discouraged FDI flows after 1992, and for every 1% increase in labour costs, FDI actually decreased by approximately 0.2% (=2.727–2.932 for 1992–2000; =2.727–2.925 for 2001–2018). With China’s rapid economic growth, wages in China have increased significantly, and foreign investors have begun to favour of lower wages for better cost control.

The coefficients on 1992–2000 × population and 2001–2018 × population are positive and statistically significant when the regional fixed effect is controlled. For every 1% increase in population density, the amount of FDI absorbed during the 1992–2000 period is approximately 0.5% higher than before 1992, and this figure for the 2001–2018 period is 0.773%. The influence of population on FDI is the lowest before 1992, indicating that over time, foreign investors have become more aware of the population effect. The results suggest that with the support of national policies, the population effect in the 2001–2018 period was strengthened, and economies of scale were formed, which were much stronger than they were in early periods. The coefficient on the exchange rate is positive and significant, suggesting that the exchange rate has a positive impact on FDI during the pre-1992 period. The negative and statistically significant coefficients on the 1992–2000×exchange rate and 2001–2018 × exchange rate indicate that compared with pre-1992, the impact of the exchange rate on FDI becomes weaker after 1992. For example, as shown in Column (2), after controlling for the province fixed effect, for an exchange rate increase of 1% (the devaluation of RMB by 1%), FDI increases by 1.7% before 1992 but decreases by 0.21% during the 1992–2000 period and by 0.28% during the 2001–2018 period. When controlling for the region fixed effect in Column (3), for an exchange rate increase of 1%, FDI increases by 1.74% before 1992, decreases by 0.4% during the 1992–2000 period, but increases by 0.27% during the 2001–2018 period.

When controlling for regional fixed effects in Column (3), exports' contribution to FDI absorption during the 1992–2000 period is higher than that during the pre-1992 period, while this effect disappears after China’s WTO entry in 2001. Meanwhile, we find that transport has a more negative impact on FDI absorption in the post-WTO period, as indicated by the negative and significant coefficient on 2001–2018transport. gdp and human capital have indifferent impacts on FDI during different time periods, as their respective coefficients on 1992–2000

gdp and 2001–2018

gdp are statistically insignificant.

In summary, the estimated results in support our expectation that all provinces and regions in China experienced significant changes in attracting FDI over the sample period. However, we show evidence that the FDI driver effects exhibit heterogeneity over time.

4.2. Estimation results from the short-run static model

The short-run dynamic model in EquationEqs. (4)–(5) is based on first difference; thus, region and period heterogeneity cannot be explored using dummy variables. As such, we estimate the short-run dynamic model using three regional subsamples (Eastern, Central, and Western) for the regional analysis and three period subsamples (pre-1991, 1992–2000, and 2001–2018) for the period analysis.

4.2.1. Short-run dynamic models with ECM: Heterogeneity across regions

reports the estimated results according to EquationEqs. (4)(4)

(4) and Equation(5)

(5)

(5) . For comparison, the short-run model without ECM is used as the treatment group, while the model with ECM is used as the control group. We divide the region into the following four groups: the whole region and three subregions. Columns (1), (3), (5) and (7) are the results without the ECM model, and Columns (2), (4), (6) and (8) consider the ECM model. The main effects of all variables are statistically significant and marked correctly, consistent with the baseline model.

Table 5. The determinants of FDI in China: Short-run heterogeneity across regions.

In the short-run model without ECM, Δgdp is significant and positive in all regions, Δwage and Δhuman capital are significant in the eastern region, and Δpopulation is important in the central region but not in other regions. The short-run dynamic model using ECM shows that the long-run coefficients of all variables are very significant across the full sample region. The coefficient θ in EquationEq. (5)(5)

(5) is equal to 0.373 and is statistically significant, which means that there is a cointegration relationship between all explanatory variables.

Starting from the lag dependent variable, the coefficients of the other three subregions are equal to 0.338, 0.383 and 0.509, which are all highly significant, effectively proving that the short-run dynamic model with ECM is more consistent with the data than the model without ECM. The lags of gdp, wage and exchange rate are statistically significant in all regions, which proves that a market size and higher exchange rate are important factors to attract FDI in all regions. Surprisingly, the lag in wage shows significant negative effects in all regions, in contrast to the positive impact found in our long-term static model. The results indicate that foreign investors strategically place more emphasis on productivity from the high-quality labour force in the long run, while they are more concerned about profitability and favour low-cost labour in the short run. The lag in Export is significantly positive in the full regional sample and the central region but not significantly positive in the western region and not significantly positive in the eastern region, and the symbol is found to be changed. The lag in Transport is insignificant in the three subregions. The lag in Human capital is only positive and not significant in western China, which may be related to the lack of high-quality labour in western China. The lag in Population is not significant in the eastern and central regions, which means that foreign investors will not prioritize the population factor when investing in these two regions. A comparison between the three subregions and the full sample region shows that the long-run coefficients of different variables are significantly different, which also indicates that the influencing factors of FDI attraction in different regions are different. The regression results of the short-run dynamic model with or without ECM support the conclusions of the long-run model to a large extent.

reports the results of short-run and long-run elasticity directly derived from EquationEq. (5)(5)

(5) . The long-run elasticity is obtained by dividing the short-run coefficients in by θ.

Table 6. Short-run and long-run elasticities across regions.

In all regions, the elasticity coefficient of gdp is the largest for both short-run and long-run coefficients, which means that among all explanatory factors selected by us, market size is the most important factor attracting FDI. The short-run coefficients on gdp are significant, which can be interpreted as the short-run elasticity of gdp to FDI. For every 1% increase in gdp, FDI will increase by 4.259% in the country, 3.682% in the eastern region, 2.816% in the central region, and 8.828% in the western region in the short run. In the long run, wages are negative in all regions, transport and exchange rates are positive in all regions, and exports are negative in the east and positive in the other regions. Population is positive and human capital is negative except for in the west.

4.2.2. Short-run dynamic models with ECM: heterogeneity over time

reports the estimated results according to EquationEqs. (4)(4)

(4) and Equation(5)

(5)

(5) . For comparison, the short-run model without ECM is used as the treatment group, while the model with ECM is used as the control group. The first group is the short-run dynamic regression results of the whole sample period, which is the same as the first group in . Columns (1), (3), (5) and (7) are the results without the ECM, and Columns (2), (4), (6) and (8) take the ECM into account. The main effects of all variables are statistically significant and marked correctly, consistent with the baseline model.

Table 7. The determinants of FDI in China: Short-run heterogeneity over time.

Without the ECM, the coefficients of Δgdp and Δhuman capital are significant across the board. The coefficients of Δwage and Δexchange rate are significant for the full sample from 1979 to 2018 only, while the coefficient on Δ export is significant for 2001 to 2018. However, the short-run coefficients of Δtransport and Δpopulation are not statistically significant in any real time period. The coefficient sign of Δwage has changed, showing a negative sign in all four periods, and the other coefficient signs are in line with expectations. However, the overall fitting degree of the model is low. When the ECM is included in the model, the symbol coefficient number of Δtransport changes and shows significant performance during the 1979–2018 period, while the short-run coefficient of Δpopulation still shows no significant performance. The interpretation of the estimated coefficient of ECM is complicated. Starting from the lagged dependent variable, the coefficient θ in EquationEq. (5)(5)

(5) is equal to 0.373, 0.296, 0.289, and 0.058 in the four periods. Since this coefficient is statistically significant, it is easy to prove that ECM is also significant in the short-run model and serves as strong evidence that there is a long-run cointegration relationship between all dependent variables and independent variables. During the 1979–2018 period, the long-run coefficients of all variables are extremely significant, so the explanatory variables we selected can all be considered to be closely related to FDI. In the other three subperiods, the performances of the long-run coefficients of different variables are different, which also indicates that the influencing factors of FDI will change accordingly in different periods. In conclusion, the regression results of the short-run dynamic model with or without ECM support the conclusions of the long-run model to a large extent.

reports the results of short-run and long-run elasticity directly derived from EquationEq. (5)(5)

(5) . The long-run elasticity is obtained by dividing the short-run coefficients in by θ.

Table 8. Short-run and long-run elasticities over time.

The gdp, export, transport and human capital variables are presented in the form of the expected signals, which are of high significance in both the short and long run. It has been proven that a large market size, a greater the degree of openness of the country, more convenient transportation and a higher labour force quality are undoubtedly the four leading factors for attracting foreign investment into China. In the long run, population is positive in the whole period but negative in the three subperiods. The exchange rate shows a negative effect from 1992 to 2000, while the other periods show a positive effect. This indicates that the influence of these two factors on attracting FDI fluctuates greatly under the influence of time and may be less important than other variables. Surprisingly, the elasticity of wages is negative in the short and long run, which does not support the assumption that high wages will accelerate FDI inflows.

Moreover, as shown in , the differences in the short-run and long-run elasticities are much smaller over a relatively longer period (e.g. the whole sample period from 1979 to 2018 and the third subperiod from 2001 to 2018) than that over a shorter period (e.g. the first and second subperiods). Within a relatively short period, there exists a huge gap between the short-run and long-run elasticities, which is perhaps because the long-run effect has yet to be fully materialized.

In conclusion, the estimation results of the long-run static model and the short-run dynamic model are consistent. The estimation of the short-run dynamic model is complementary to ensuring the stability of the long-run static model. Our results confirm that the large market size, greater openness, complete infrastructure, highly skilled workers, low population density and currency depreciation are the reasons for FDI inflow into China.

4.3. FDI and the BRI

In 2013, China announced the construction of the ‘One Belt and One Road’ and the development of the ‘Belt and Road’ economic zone, which is an important component of China's strategy to comprehensively open-up once again. We investigate how FDI varies across BRI and non-BRI regions and BRI announcement times. reports the estimated results from EquationEq. (6)(6)

(6) . The results for the main explanatory variables are consistent with those from our baseline model in . In this section, we focus on the coefficient on BRI_region, which captures the difference in attracting FDI between BRI provinces and non-BRI provinces; the coefficient on BRI_year, which captures the difference in attracting FDI before and after the BRI launch in 2013; and the coefficient on BRI_region

BRI year, which captures whether BRI provinces attract more (or few) FDI compared to non-BRI provinces after the BRI launch in 2013.

Table 9. Impact of the Belt and Road Initiative (BRI) on FDI.

In Columns (1)–(4), we examine the variation in FDI across the BRI region. The coefficient of BRI_region is positive and statistically significant, indicating that 18 provinces on the BRI corridor have attracted more FDI than non-BRI provinces. The results are robust after controlling for different fixed effects, for example, the year fixed effect in Column (1), the period fixed effect in Column (2), the year and region fixed effects in Column (3), and the region and period fixed effect in Column (4).

In Columns (5)–(6), we introduce BRI_year and the interaction terms between BRI-region and BRI-year. We control for period fixed effects in Column (5) and regions and period fixed effects in Column (6). The coefficient on BRI_year is positive and statistically significant, indicating that after the implementation of the BRI plan, China attracted more FDI.

The coefficients on BRI_region BRI year are negative and statistically significant, indicating that BRI provinces attracted less FDI after the BRI plan started in 2013. One plausible explanation is that since the launch of the BRI in 2013, China's opening policy has strategically changed from ‘bringing in’ (capital and/technology) towards ‘going out’ to shift production capacity to low-income BRI countries where there is ready demand. Most of China's ‘going out’ enterprises are from BRI provinces. ‘Going out’ may induce resource competition with ‘bringing in’, and the likely outflows of human capital, financial capital, and materials and other resources may make these BRI provinces less attractive to foreign investors. Our results are consistent with Luo, Chai, and Chen (Citation2019), who found that FDI in BRI provinces decreased significantly compared to non-BRI provinces during the period of 2003–2015.

5. Conclusion

In this study, we investigate the spatial heterogeneity and time-varying nature of FDI determinants over the 1979–2018 period. We also explore the impact of the BRI on regional FDI inflows. Our main findings are as follows. First, we find a positive impact on FDI from GDP, labour costs, exports, transport infrastructure, human capital, and exchange rate, while population has a negative impact on FDI. Second, the effects of these FDI determinants are heterogeneous across regions. All of their impacts are weaker in the underdeveloped central and western regions, except for GDP and human capital, whose impacts are stronger. Third, the effects of FDI determinants are, to a lesser extent, also heterogeneous over time. Their impacts are weaker in the underdeveloped central and western regions, except for GDP and human capital, whose impacts are stronger. The impacts of wage and exchange rates became weaker with more opening up after Deng Xiaoping's Southern Tour. Fourth, we find that BRI provinces attract more FDI than non-BRI provinces over the sample period. However, the BRI provinces have become less popular and have attracted less FDI than non-BRI provinces since the BRI was launched in 2013.

Our findings have important policy implications in China regarding regional economic convergence and balanced development. Policymakers should consider the level of economic conditions (i.e. wages, infrastructure) across different regions and design tailored policies to enhance the policy impact. For instance, to attract more FDI, the eastern region may increase investment in infrastructure as its impact is stronger in the eastern region than in the western and central regions, the central region should design policies to attract talent, and the west region should pay attention to population. Our findings are also of high policy relevance to BRI planning. Government policy should take a more balanced view regarding the ‘going out’ and ‘bringing in’ strategies. Policymakers should encourage BRI provinces to actively participate in international trade, explore local comparative advantages, optimize industrial layout, and enhance the attraction to foreign investment.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Kailei Wei

Dr. Kailei Wei is a professor in Economics at School of Management, Hainan University, China. Kailei holds PhD in Economics from Middlesex University Business School in UK and was a visiting scholar at Michigan State University in USA. Kailei's main research interests include foreign direct investment, high-quality development of regional economy, and rural tourism and internationalization of tropical agriculture. She has secured funding from National Natural Science Foundation of China to support three of her research projects, along with a number of other research projects funded by provincial (Hainan Province) and ministerial funding bodies. Her research works has been published in leading peer-reviewed academic journals such as Journal of Comparative Economics, Review of Development Economics, and Applied Economics Letters. Her research works has also appeared in China's top economics journals.

Suhan Li

Miss Suhan Li is a postgraduate student, under Professor Kailei Wei’s supervision, majored in Agricultural and Forestry Economics and Management at the School of Management, Hainan University, China. Suhan’s main research interests include foreign direct investment and economic growth of the agricultural sector.

Chunxia Jiang

Dr Chunxia Jiang is a Senior Lecturer (Associate Professor) in Finance at the Business School, University of Aberdeen, UK. Prior to joining Aberdeen in 2019, She was a Lecturer/Senior Lecturer at Newcastle University and Middlesex University Business School in UK. Chunxia holds PhD in Economics and MSc Money, Banking and Finance from Middlesex University Business School, UK. Chunxia’s main research interest include banking performance and competition, financial stability, monetary policy, and recently extend to fintech and cryptocurrency. Her research works have appeared in leading peer-reviewed academic journals such as the Journal of Banking & Finance, Journal of Financial Stability, and Energy Economics. Her research works have also appeared in top economics journal in China. Chunxia has published a research monograph: Chinese Banking Reform - From the Pre-WTO to Financial Crisis and Beyond by Palgrave Macmillan.

Notes

1 The Eastern region includes Beijing, Tianjin, Shanghai, Hebei, Liaoning, Jiangsu, Zhejiang, Fujian, Shandong, Guangdong, and Hainan; the Central region consists of Shanxi, Jilin, Heilongjiang, Anhui, Jiangxi, Henan, Hubei, and Hunan; and the Western region includes Inner Mongolia, Guangxi, Sichuan, Guizhou, Yunnan, Shaanxi, Gansu, Qinghai, Ningxia, and Xinjiang. Tibet is excluded due to incomplete data. Chongqing is included in Sichuan province due to lack of separate data.

2 We have checked for correlations among the main variables and performed the Variance inflation factor (VIF) test, and the results suggest that our data possess the required properties and our models do not suffer from serious multicollinearity problems.

3 Based on the results in Column (3), the impact of transport on FDI in the central region is negative 0.193% (=1.431-1.624).

References

- Alfalih, A. A., and T. B. Hadj. 2020. “Foreign Direct Investment Determinants in an Oil Abundant Host Country: Short and Long-Run Approach for Saudi Arabia.” Resources Policy 66: 101616. doi:https://doi.org/10.1016/j.resourpol.2020.101616.

- Anderson, James E., Mario. Larch, and Yoto V. Yotov. 2019. “Trade and Investment in the Global Economy: A Multi-Country Dynamic Analysis.” European Economic Review 120 (C): 103311–103311. doi:https://doi.org/10.1016/j.euroecorev.2019.103311.

- Blyde, J., and D. Molina. 2015. “Logistic Infrastructure and the International Location of Fragmented Production.” Journal of International Economics 95 (2): 319–332. doi:https://doi.org/10.1016/j.jinteco.2014.11.010.

- Cai, Z., L. Chen, and Y. Fang. 2018. “A Semiparametric Quantile Panel Data Model with an Application to Estimating the Growth Effect of FDI.” Journal of Econometrics 206 (2): 531–553. doi:https://doi.org/10.1016/j.jeconom.2018.06.013.

- Cheng, L., and Y. Kwan. 2000. “What Are the Determinants of the Location of Foreign Direct Investment? The Chinese Experience.” Journal of International Economics 51 (2): 379–400. doi:https://doi.org/10.1016/S0022-1996(99)00032-X.

- Cheng, S., and S. Z. Qi. 2021. “The Potential for China's Outward Foreign Direct Investment and Its Determinants: A Comparative Study of Carbon-Intensive and Non-Carbon-Intensive Sectors along the Belt and Road.” Journal of Environmental Management 282: 111960. doi:https://doi.org/10.1016/j.jenvman.2021.111960.

- Cleeve, Emmanuel A., Yaw. Debrah, and Zelealem. Yiheyis. 2015. “Human Capital and FDI Inflow: An Assessment of the African Case.” World Development 74: 1–14. doi:https://doi.org/10.1016/j.worlddev.2015.04.003.

- Coughlin, C. C., and E. Segev. 2000. “Foreign Direct Investment in China: A Spatial Econometric Study.” The World Economy 23 (1): 1–23. doi:https://doi.org/10.1111/1467-9701.t01-1-00260.

- Doytch, Nadia., and Uctum Merih. 2011. “Does the Worldwide Shift of FDI from Manufacturing to Services Accelerate Economic Growth? A GMM Estimation Study.” Journal of International Money and Finance 30 (3): 410–427. doi:https://doi.org/10.1016/j.jimonfin.2011.01.001.

- Dunning, J. H. 1988. “The Eclectic Paradigm of International Production: A Restatement and Some Possible Extensions.” Journal of International Business Studies 19 (1): 1–491. doi:https://doi.org/10.1057/palgrave.jibs.8490372.

- Froot, K. A., and M. Obstfeld. 1991. “Exchange-Rate Dynamics under Stochastic Regime Shifts: A Unified Approach.” Journal of International Economics 31 (3-4): 203–229. doi:https://doi.org/10.1016/0022-1996(91)90036-6.

- García-Herrero, A., and J. Xu. 2017. “China's Belt and Road Initiative: Can Europe Expect Trade Gains?” China & World Economy 25 (6): 84–99. doi:https://doi.org/10.1111/cwe.12222.

- Harms, Philipp and Jakub Knaze. 2021. “Bilateral de-Jure Exchange Rate Regimes and Foreign Direct Investment: A Gravity Analysis.” Journal of International Money and Finance 117. https://doi.org/https://doi.org/10.1016/j.jimonfin.2021.102438

- Head, K., and J. Ries. 1996. “Inter-City Competition for Foreign Investment: Static and Dynamic Effects of China’s Incentive Areas.” Journal of Urban Economics 40 (1): 38–60. doi:https://doi.org/10.1006/juec.1996.0022.

- Horst, T. 1972. “The Industrial Composition of U.S. exports and Subsidiary Sales to the Canadian Market.” American Economic Review 62: 37–45.

- Hou, Lei., Kunpeng. Li, Qi. Li, and Min. Quyang. 2020. “Revisiting the Location of FDI in China: A Panel Data Approach with Heterogeneous Shocks.” Journal of Econometrics 221 (2): 483–509.

- Keeley, A. R., and K. Matsumoto. 2018. “Relative Significance of Determinants of Foreign Direct Investment in Wind and Solar Energy in Developing countries - AHP Analysis.” Energy Policy 123: 337–348. doi:https://doi.org/10.1016/j.enpol.2018.08.055.

- Krugman, P. 1991. “Increasing Returns and Economic Geography.” Journal of Political Economy 99 (3): 483–499. doi:https://doi.org/10.1086/261763.

- Li, X., C. Liu, F. Wang, Q. Ge, and Z. Hao. 2021. “The Effect of Chinese Investment on Reducing CO2 Emission for the Belt and Road Countries.” Journal of Cleaner Production 288 (1): 125125. doi:https://doi.org/10.1016/j.jclepro.2020.125125.

- Li, Zhenghui., Zhehao. Huang, and Hao. Dong. 2019. “The Influential Factors on Outward Foreign Direct Investment: Evidence from the “the Belt and Road.” Emerging Markets Finance and Trade 55 (14): 3211–3226. doi:https://doi.org/10.1080/1540496X.2019.1569512.

- Lin, Hui-Lin., Yi-Chi. Hsiao, and Eric S. Lin. 2015. “The Choice between Standard and Non-Standard FDI Production Strategies for Taiwanese Multinationals.” Research Policy 44 (1): 283–293. doi:https://doi.org/10.1016/j.respol.2014.06.005.

- Luo, C., Q. Chai, and H. Chen. 2019. “Going Global” and FDI Inflows in China: “One Belt & One Road” Initiative as a Quasi Natural Experiment.” The World Economy 42 (6): 1654–1672. doi:https://doi.org/10.1111/twec.12796.

- McGrattan, Ellen R. 2012. “Transition to FDI Openness: Reconciling Theory and Evidence.” Review of Economic Dynamics 15 (4): 437–458. doi:https://doi.org/10.1016/j.red.2012.07.004.

- Moshfique, Uddin., Anup Chowdhury, Sheeba Zafar, Jia Liu. (2018). “Institutional Determinants of Inward FDI: Evidence from Pakistan.” International Business Review 28 (2): 344–358.

- Paul, J., and Maria M. Feliciano-Cestero. 2021. “Five Decades of Research on Foreign Direct Investment by MNEs: An Overview and Research Agenda.” Journal of Business Research 124: 800–812. doi:https://doi.org/10.1016/j.jbusres.2020.04.017.

- Peck, F. 1996. “Regional Development and the Production of Space: The Role of Infrastructure in the Attraction of New Inward Investment.” Environment and Planning A: Economy and Space 28 (2): 327–339. doi:https://doi.org/10.1068/a280327.

- Romer, P. M. 1986. “Increasing Return and Long Run Growth.” Journal of Political Economy 94 (5): 1002–1037. doi:https://doi.org/10.1086/261420.

- Rong, S., K. Liu, S. Huang, and Q. Zhang. 2020. “FDI, Labor Market Flexibility and Employment in China.” China Economic Review 61: 101449. doi:https://doi.org/10.1016/j.chieco.2020.101449.

- Roser, Max., and Jesus Crespo Cuaresma. 2016. “Why is Income Inequality Increasing in the Developed World?” Review of Income and Wealth 62 (1): 1–27. doi:https://doi.org/10.1111/roiw.12153.

- Sanchez-Martin, M. E., R. D. Arce, and G. Escribano. 2014. “Do Changes in the Rules of the Game Affect FDI Flows in Latin America? A Look at the Macroeconomic, Institutional and Regional Integration Determinants of FDI.” European Journal of Political Economy 34: 279–299. doi:https://doi.org/10.1016/j.ejpoleco.2014.02.001.

- Sun, J. 1988. The Economic Geography of China. New York: Oxford University Press.

- Sun, Q., W. Tong, and Q. Yu. 2002. “Determinants of Foreign Direct Investment across China.” Journal of International Money and Finance 21 (1): 79–113. doi:https://doi.org/10.1016/S0261-5606(01)00032-8.

- Venables, A. 1993. Equilibrium location of vertically linked industries. CPER Discussion Paper, 82. London School of Economics.

- Wei, K., S. Yao, and A. Liu. 2009. “Foreign Direct Investment and Regional Inequality in China.” Review of Development Economics 13 (4): 778–791. doi:https://doi.org/10.1111/j.1467-9361.2009.00516.x.

- Wu, H., S. Ren, G. Yan, and Y. Hao. 2020. “Does China's Outward Direct Investment Improve Green Total Factor Productivity in the “Belt and Road” Countries? Evidence from Dynamic Threshold Panel Model Analysis.” Journal of Environmental Management 275: 111295. doi:https://doi.org/10.1016/j.jenvman.2020.111295.

- Yao, S. 2006. “On Economic Growth, FDI and Exports in China.” Applied Economics 38 (3): 339–352. doi:https://doi.org/10.1080/00036840500368730.

- Yao, S., and K. Wei. 2007. “Economic Growth in the Presence of FDI: The Perspective of Newly Industrialising Economies.” Journal of Comparative Economics 35 (1): 211–234. doi:https://doi.org/10.1016/j.jce.2006.10.007.

- Yu, Kang, Tan. Xiangyong, and Xin. Xian. 2008. “Have China's FDI Policy Changes Been Successful in Reducing Its FDI Regional Disparity?” Journal of World Trade 42 (4): 641–652.

- Yu, Linhui., Dan. Zhao, Haixia. Niu, and Futao. Lu. 2020. “Does the Belt and Road Initiative Expand China's Export Potential to Countries along the Belt and Road.” China Economic Review 60 (C): 101419–101419. doi:https://doi.org/10.1016/j.chieco.2020.101419.