?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The paper demonstrates that Bitcoin is not money but rather a digital commodity that has value but no value-added. We show that both the production of and the speculation with Bitcoin draw from the existing global pool of value-added. By extending the Classical Political Economy approach and the New Interpretation of the labour theory of value to the domain of digital commodities, the paper argues that Bitcoin mining is an automated reproduction process that requires no direct (living) labour and thus creates no new value. Bitcoin, in this regard, is not ‘digital gold’. Between sectors, Bitcoin mining redistributes wealth and value-added already in existence, while Bitcoin miners with more computational power compete to appropriate the mining profits within the blockchain. The Bitcoin blockchain then creates rivalry in both the ownership and the use of the digital commodity through non-legal means. Our approach can be further expanded to the larger domain of automated digital commodities that are reproducible without the expenditure of direct, living labour.

Introduction

The paper argues that Bitcoin should be defined not as digital money or currency but rather as a digital commodity, an intangible product produced for profit but one that exists only in the electronic domain of bits and bytes. As is the case with other pseudo cryptocurrencies, Bitcoin has value but no value-added. Bitcoin mining originates neither new value-added nor new purchasing power, it merely reallocates them. This implies that both the profits made from the digital mining of new Bitcoins and the capital gains made from trading it are redistributions from the global pools of value-added and liquid wealth in the world economy.

Bitcoin’s nature as a commodity allows it to be created and accumulated as a digital asset that has no matching financial liability to its producer, unlike the issuance of currency or financial securities which necessarily give rise to a corresponding financial liability to the issuer. Bitcoin miners receive profits that are actually transfers of value-added and existing wealth. These mining profits then accrue to the nodes with the greatest computational power to process and verify transactions in the blockchain. Bitcoin has achieved worldwide popularity and the blockchain technology has spread to several industries, including recent advances in smart contracts and decentralised finance. But despite such achievements, Bitcoin has undermined its potential role as currency.

The issuance of money or financial assets such as stocks, bonds, bank loans, and derivatives necessarily entails the creation of a matching liability to the issuer. Bitcoin mining, however, does not create any corresponding liability. New Bitcoins come into existence as non-financial assets. This creates the illusion that new Bitcoins represent new wealth since the economy now has a new asset that has been produced and for which there is no corresponding liability, as if Bitcoin were simply ‘digital gold’. The illusion is further reinforced in the System of National Accounts (SNA) as its methodology classifies all market activities as producers of value-added. We argue, on the contrary, that the supply of Bitcoin as a new digital asset represents a mere reallocation of already existing wealth and a transfer of value-added from the productive sectors of the global economy.

To demonstrate these propositions we draw from Classical Political Economy and from recent advances in the labour theory of value under what has been called the New Interpretation. The New Interpretation offers a consistent theory of how the market prices of commodities represent redistributions of the labour time employed in the production sphere. It identifies the source of all new value-added in the direct (living) labour spent in the production of commodities, and it posits money as the main link that allows for the conversion between monetary units and hours of productive labour time. In the paper, we extend the New Interpretation to the domain of digital commodities. We demonstrate that the New Interpretation is robust to the existence of digital commodities and that the mining of pseudo cryptocurrencies such as Bitcoin actually draws from the aggregate pool of value-added.

The labour value of Bitcoin is the value transferred from its means of production, which consist of the indirect labour integrated into the inputs of production, comprising mainly massive usages of electricity, warehousing, and the computational power now mostly carried out by networked pools of ASIC computers and GPUs. These inputs to digital mining are reproducible commodities on their own, and thus gradually transfer their own values to Bitcoin as new digital replicas of Bitcoin are mined through the verification of transaction blocks. The labour value of Bitcoin, therefore, derives from the non-labour inputs required to verify and process the transactions in the blockchain network.

Despite the initial labour required to set up the mining facilities, there is essentially no direct labour put into work in the verification of transactions in the blockchain. In such a case, where there is virtually no living labour applied to the reproduction of the digital commodity, the labour theory of value posits that there can be no corresponding creation of new value-added. Only living, direct labour can originate new value-added. Bitcoin mining creates new use values in the form of digital commodities but there is no direct living labour to generate new value-added. For this reason, even though Bitcoins come into existence as new digital assets with no corresponding liability, they do not represent new wealth.

Bitcoin mining and trading draw from the global pools of value-added and existing wealth. As such, Bitcoin should not be classified as ‘digital gold’, for it gives rise neither to new value-added nor new wealth as real gold mining does. Between sectors, Bitcoin draws value-added and wealth from the productive sectors of the world economy without directly adding new value to them in return. Within the Bitcoin sector, the owners of the fastest computers then appropriate the majority of the mining profits. Bitcoin trading and speculation cannot create new value-added, as these activities obviously take place within the circulation sphere and thus merely redistribute value-added and wealth from elsewhere in the economy. What our labour theory of value of digital commodities reveals is that the production of Bitcoin merely transfers the values from the inputs and then earns profits that are in fact redistributions of value-added from other sectors of the global economy.

The argument that Bitcoin has value but no value-added is relevant because it clarifies why Bitcoin represents a mere reallocation of value at the aggregate level with no direct addition of new value to the economy: according to the labour theory of value, there cannot be value-added if there is no direct (living) labour. The argument is relevant not only to Bitcoin but also to the growing supply of digital assets that now include non-fungible tokens (NFTs), smart contracts, as well as virtual assets and virtual real estate within the metaverses. The aim of the paper is not primarily to ascertain the non-moneyness of Bitcoin but rather to develop a consistent value theory that applies to the growing domain of digital commodities such as cryptos, NFTs, smart contracts, virtual assets within metaverses, and other similar digital assets which have value but no value-added.

The paper is organised as follows. Section 2 compares and contrasts our approach to the existing literature, highlighting our main contributions. Section 3 develops the theory of digital commodities by extending the New Interpretation of the labour theory of value to the case of (pseudo) cryptocurrencies like Bitcoin. Section 4 introduces a simple mathematical presentation of the labour theory of value of digital commodities like Bitcoin. Section 5 presents a taxonomy of digital products and digital commodities, conceptualising the Bitcoin blockchain as a technology that creates rivalry in both the ownership and the use of a digital commodity via non-legal means and without third party enforcement. Section 6 addresses the question of whether or not a digital commodity could become digital money. We argue that Bitcoin does not function as money because it is not a general equivalent that represents abstract wealth (i.e. value) in an autonomous form with wide social acceptance, irrespective of the fact that Bitcoin contains value but no value-added. Section 7 concludes with some final remarks on how our approach can be expanded to the larger domain of automated digital commodities.

Comparison to previous approaches

Bitcoin remains at the centre of several debates on the true nature of cryptocurrencies. Arguing that it is de facto money, even though not de jure money, Bitcoin supporters often find inspiration in the more libertarian approaches to money (as in Von Mises Citation[1912] 1981, Hayek Citation1976). Bitcoin has also become a challenge for governments and regulators worldwide, who now face the need to properly classify and regulate the emerging digital commodities.

The scholarship on the nature of Bitcoin can be divided into two main groups. In the first group we find the scholars concerned with the ‘social content’ of Bitcoin, be it the political, symbolic, or ideological aspects of it (as in Maurer et al. Citation2013, Karlstrøm Citation2014, Kostakis and Giotitsas Citation2014, Golumbia Citation2016, Dodd Citation2018, Nelms et al. Citation2018, Swartz Citation2018, Hayes Citation2019). In the second group, we find the scholars focused on the economic properties of Bitcoin, paying particular attention to the contested status of Bitcoin as money (as in Tymoigne Citation2013, Yermark Citation2015, Aglietta Citation2018, Eichengreen Citation2019, Paraná Citation2021). Hayes (Citation2021), in this regard, claims that Bitcoin can be money but only within its own bounded virtual space.

While the first group tends to analyse the different sociological and philosophical aspects of Bitcoin, the second group tends to analyse its economic implications. The literature also features contributions from scholars that, in different but complementary ways, bring together the social and economic dimensions of Bitcoin (as in Varoufakis Citation2013, Barber Citation2015, Bjerg Citation2016, Paraná Citation2020). Despite the differences in perspectives, the consensus in the extant scholarship is that Bitcoin is neither money nor currency with general social acceptance, but is rather an asset mainly used as a vehicle for speculative investments.

The present paper makes a contribution to the literature by not only showing that Bitcoin is not money but, more importantly, by demonstrating that Bitcoin is in fact a digital commodity that has value but no value-added. By extending the Classical Political Economy approach and the Marxist theory of value to the domain of digital commodities, we are able to properly define and theorise what Bitcoin is and where its production (or digital mining) profits actually originate.

We provide a wider classification of digital commodities and show that the Bitcoin blockchain is able to maintain rivalry both in terms of the use and the ownership of a digital commodity which, in principle, should be infinitely reproducible at zero marginal cost. The Bitcoin blockchain has, therefore, revolutionised computer programming by effectively institutionalising private property into the digital domain, without any form of state intervention or legal enforcement by a third party.

Some previous contributions have highlighted the nature of Bitcoin as a commodity (as in Graf Citation2014, Barber Citation2015, Tamer Citation2019) but none within a systematic Marxist approach and even less within a consistent Marxist approach to digital commodities. Even though a few Marxist treatments of Bitcoin are present in the literature (as in Abramova et al. Citation2020, Nakatani and Mello Citation2019, Wang Citation2019, Bonilla Citation2020), these contributions did not go much beyond a critique of cryptocurrencies. In this regard, we complement the existing studies by offering a more consistent theoretical treatment of the production and circulation of Bitcoin.

Our theoretical framework and taxonomy of digital products can also shed light on the empirical side of the literature. Some empirical studies have attempted to gain insights into the nature of Bitcoin by analysing its price and transaction patterns, in some cases also establishing a comparison across a range of asset classes (as in Hayes Citation2017, Citation2018, Citation2019, Abbatemarco et al. Citation2018, Baur et al. Citation2018, Gronwald Citation2019, Baldan and Zen Citation2020, White et al. Citation2020). These empirical works aim to provide clues about the properties of Bitcoin by identifying common pricing patterns relative to a vast array of commodities, assets, and securities. Such empirical approaches, however, have not yet fully explained what Bitcoin is in the first place, and have not properly identified where the digital mining profits originate.

The present paper claims that Bitcoin mining does not generate new value-added and, hence, that it should be classified as an unproductive activity. The profits accruing to digital miners are in fact redistributions of value-added originated in productive activities located elsewhere in the global economy. Hayes (Citation2017, Citation2018) proposes that Bitcoin’s value corresponds to its marginal cost of production, where the main input for the cost is electricity, and hence that the origin of Bitcoin’s value lies mostly in the energy sector. Since the value of a commodity is determined by the direct and indirect labour time socially necessary to reproduce it, our approach based on the labour theory of value is in line with Hayes in this regard.

Bitcoin per se represents neither new value-added nor new purchasing power at the aggregate level. But because the official Systems of National Accounts (SNA) do not properly differentiate between productive and unproductive activities as Classical Political Economy does (Rotta Citation2018), Bitcoin mining might be inadvertently classified as contributing toward the official measures of GDP. According to our theoretical framework, Bitcoin mining increases the total gross product of the economy but not the net product (GDP), as there is no direct increase in the aggregate value-added.

The implications of Bitcoin mining are, therefore, better captured by input-output matrices, where the total gross product expands while the net national product does not. Contrary to the measurement of GDP, input-output matrices show how the output of some sectors (like electricity production, computer manufacturing, and warehousing) benefit from the input usage in the Bitcoin production process. Aggregate value-added and GDP, nonetheless, remain unaltered. While Bitcoin mining represents greater demand for inputs like electricity, computer manufacturing, and warehousing, in the aggregate the existing value of GDP is reallocated rather than increased.

Digital commodities and bitcoin

A commodity is a product of human labour, either a good or service, that is both useful and produced for profit. The widespread commodification of intellectual products like music scores, chemical formulae, and patented innovations further demonstrates that commodities are not solely restricted to tangible objects. Commodities might be immaterial products as well. In this regard, we define a digital commodity as a commodity that exists solely in electronic form, as a string of bits and bytes.

In this section, we use the definition of commodity from Classical Political Economy and our definition of a digital commodity to demonstrate that pseudo cryptocurrencies like Bitcoin are better conceptualised not as money but rather as digital commodities. We also demonstrate that pseudo cryptocurrencies like Bitcoin contain value but no value-added and, hence, that profits from its production and trading are transfers of value-added drawn from the global pool of aggregate value-added. The production of new Bitcoins merely reallocates existing value-added and wealth, without adding to them.

As in Classical Political Economy and in Marx, we define value as the social character of labour in an economy that predominantly produces goods and services in the form of commodities. Likewise, we define use value as the usefulness that a particular commodity might have for their buyers. Value and use-value comprise the basic determinations of commodities whether digital or not. The quantity of value of a commodity is then determined by the socially necessary labour directly and indirectly required to reproduce it according to the existing technology and current production conditions. The quantity of value of a commodity has, therefore, two sources: direct (or living) labour that creates new value-added, and indirect (or past) labour that transfers its value from the non-labour inputs to the output. According to the labour theory of value from Classical Political Economy, only direct (living) labour can create new value-added. The indirect (past) labour that is already objectified in non-labour inputs like plants and equipment is then gradually transferred to the output at the rate at which these inputs are used up over multiple production periods.

The best approach to the labour theory of value comes from the New Interpretation, also known as the single-system labour theory of value, which has been developed since the 1980s by the following authors: Duménil (Citation1980), Duménil and Lévy (Citation2000), Foley (Citation1982, Citation2000, Citation2018), Foley and Duménil (Citation2008), Mohun (Citation1993), Laibman (Citation2012), Mohun and Veneziani (Citation2018), Cogliano, Flaschel, Franke, Frohlich, and Veneziani (Citation2018). The New Interpretation makes the following claims regarding the labour theory of value. First, all value-added derives from the expenditure of direct living labour. Second, values are measured in hours of abstract labour time and prices are measured in monetary units. Third, the value of the output is determined by the sum of the values of the non-labour inputs used up (labelled past or indirect labour) and the direct labour time spent. The non-labour inputs transfer their value to the output, while direct living labour creates new value-added. The value of the output is the summation of the values transferred from the means of production plus the new value-added created by direct labour. Fourth, the value of labour power is the wage share of value-added converted to its labour time equivalent. Fifth, the monetary expression of labour time (MELT) measures the equivalence between abstract labour time in hours and the price of the aggregate net product in units of money. The price of the aggregate net product is the price of the total (gross) product minus the cost of the intermediate inputs used up. The MELT is defined in monetary units per labour hour and is computed as the ratio of the aggregate nominal price of the net product to the total expenditure of direct labour time in productive activities. Unproductive activities (like finance, trading, and real estate) do not create new value-added. The inverse of the MELT, defined in terms of labour hours per unit of money, is called the value of money. In this way, the rate of profit measured in prices matches the rate of profit measured in labour values. The rate of exploitation in value terms also matches the rate of exploitation in price terms. The price of the net product equals the monetary expression of aggregate value-added, and aggregate profit equals the monetary expression of aggregate surplus value. Surplus value (the value corresponding to unpaid labour time) is the origin of aggregate profits. Hence, the rate of exploitation measures surplus-value divided by the value of labour power or, equivalently, unpaid over paid labour time.

There is no expectation that market prices should be proportional to labour values at the microeconomic level. Individual prices can diverge from individual values in any way, subject only to two restrictions at the aggregate level: that aggregate profits in price terms match the aggregate surplus value in labour hours converted to its monetary expression; and that the aggregate net product in price terms matches aggregate value-added in labour hours, converted to its monetary expression, which is itself equal to the total living labour expended in productive activities. The price system merely redistributes, albeit in rather complex ways, the value originally created in production. There is no value originated outside of the productive sphere.

The rise of the digital economy, however, creates a novel situation for capitalism. Our current technology allows for the reproduction of some commodities through the intensive use of computers, robots, and energy but with virtually no direct (living) labour. Some minimal labour might be used to setup the infrastructure at the start, but no living labour is necessary to further reproduce the commodity. This novel configuration implies that commodities produced with a high usage of non-labour inputs but no (or very low) usage of direct labour will gradually transfer the value from the means of production to the output but will not directly create new value-added. Digital commodities are the best example of this process, since computers and automated production can reproduce them with virtually no direct labour input. New commodities with use-value are supplied but there is no corresponding increase in value-added and, hence, no new wealth is originated. The supply of a digital commodity which can be fully reproduced by machines, robots, and computers will increase the net output in quantity terms, such that the total supply of use-values increases, but it will not directly increase the value of the net output of the economy.

It is still possible, however, that the fully automated commodity can increase the productivity of labour elsewhere if employed as means of production into another production process. Even though the fully automated commodity does not directly create new value-added, it can still indirectly do so by enhancing the productivity of direct (living) labour in another productive activity. But because the fully automated commodity (that directly creates no new value-added) must still earn a profit to keep being produced, the profit it earns will, in fact, be a transfer of value-added from the aggregate pool of value-added of the world economy. The transfer of profits that takes place via the market price mechanism, whereby the price of the fully automated commodity is much above its own individual value, will therefore, draw value-added from other value-added-producing (that is, productive) activities.

An example might clarify the theoretical argument. Assume that Google is able to fully automate the reproduction of a certain device that is then used as a means of production by other companies. Because Google’s device can be reproduced without direct labour it does increase the net output of the economy in quantity terms, but because the device has value and no value-added it does not increase the value of net output of the economy. The total gross value of the economy increases, but not the value of the net output. If used by other companies as a means of production, Google’s device might substantially increase the labour productivity of the employees working at these other companies. Hence, Google’s device did not directly create new value-added but it indirectly increased the value-added in the economy by augmenting labour productivity elsewhere. Google’s profits in the reproduction of the device will then effectively represent transfers of value-added from the companies that purchased and then employed such device productively. These transfers consist of redistributed value-added, drawn from the global pool of value-added in the world economy.

If there is no new living labour to reproduce the commodity, there cannot be new value-added. Bitcoin, we argue, operates in a similar way, for it is a digital commodity that requires intensive usage of computational power and electricity but virtually no (or negligible) direct labour input. Bitcoin, rather than being money, is a digital commodity whose creation gives rise to no new value-added. Bitcoin mining and the complex verification of transactions in the blockchain network actually transfer value from the non-labour inputs (infrastructure, energy, and computational power) but do not create new value-added within the production process. Bitcoin mining and the blockchain verification process, therefore, do not increase the aggregate value-added of the global economy, for the only way to do so would be by expending socially necessary direct (living) labour.

Moreover, because Bitcoin is a commodity rather than money, it can be accumulated and stored as a digital asset without any matching liability to its creator. The production of new Bitcoins does not create a matching liability as the issuance of money by central banks and commercial banks do. Whenever money or financial instruments (such as stocks, bonds, derivatives, and bank credit) are issued they immediately give rise to a matching liability to its issuer. Bitcoin mining, however, does not entail any liability to anyone on the blockchain. Due to its digital durability, Bitcoin can then be accumulated as a digital asset and traded according to its use-values. And Bitcoin does have multiple use values, for it is on high demand for transfer payments across international borders, online transactions, speculation, tax avoidance, wealth sheltering, ransomware payments, and for transactions that can be settled in Bitcoin.

What, therefore, allows Bitcoin to originate as a digital asset with no matching liability is its nature as a commodity and not as money. The supply of new digital assets like Bitcoin and other pseudo cryptocurrencies, however, creates the illusion that new wealth is being originated when in fact it merely reallocates already existing wealth.

It is possible to decompose the origin of the Bitcoin profits into two stages. In the first stage, which we call the between sector component, the Bitcoin sector draws its profits and capital gains from two sources. In terms of flows of value-added, the Bitcoin sector draws its profit from the global pool of value-added. In terms of capital gains, the Bitcoin sector draws existing stocks of wealth from the global pool of liquid assets. This first stage thus represents a transfer of flows of value-added and also of stocks of wealth from the global economy into the Bitcoin sector, and both contribute to raise the price of Bitcoin against a core currency such as the dollar.

In the second stage, which we call the within sector component, the total profit drawn into the Bitcoin sector is then redistributed between the Bitcoin miners and traders. Across miners, those with greater computational power receive most of the mining profits, given that the Bitcoin software rewards the nodes that verify and broadcast new blocks of transactions in the shortest period of time. Across traders, those lucky enough to buy cheap and sell dear receive the trading profits. In both cases, neither mining nor trading can create new value-added or new wealth.

In sum, the origin of the Bitcoin profits is, first, from between-sector transfers of value-added and of stocks of liquid wealth; and, second, from a within-sector reallocation of these transfers to the most efficient miners and traders. Bitcoin profits, therefore, represent a reallocation of both flows of value-added and of stocks of liquid assets, with no direct net increase in them.

A formal representation of digital commodities

The claim that Bitcoin mining does not create value-added is counterintuitive if one follows the United Nation’s methodology for the System of National Accounts (SNA). The SNA rests on a central hypothesis, namely that all marketable activity creates value-added (Rotta Citation2018). From such perspective, Bitcoin mining creates value-added. From a Classical Political Economy perspective, however, the SNA’s central hypothesis has a fundamental problem, for it does not properly distinguish between productive and unproductive activities. According to the labour theory of value, productive activities are those that create new value-added while unproductive activities do not, which implies that the profits and revenues accrued to unproductive activities are redistributions of value-added originated in productive activities.

In the SNA, an increase in Bitcoin mining does increase GDP both in nominal and in real terms, as a new good or service is supplied to a market that has demand for it. But in the accounting framework of the labour theory of value, Bitcoin mining does not increase the expenditure of living labour and, hence, cannot increase the aggregate value-added of the economy. Bitcoin mining and trading are unproductive activities that reallocate value-added that already exists. In what follows we explain in more detail how the production of Bitcoin increases the net output in quantity terms but not in value-added terms.

Let the world economy be summarised as the production of commodities in a linear input-output model in which the

matrix

contains the input-output coefficients

that represent the use of input

per unit of output

. We consider the world economy for two reasons. First, Bitcoin is a global digital commodity that knows no international borders. Second, we can consider the entire global economy as a single domestic economy and avoid the decomposition of matrix

into the domestic and imported elements of production. Matrix

comprises both the usage of non-fixed capital

and the depreciation of fixed capital

, hence

. We assume no joint products, so each production process outputs a single type of commodity. Let the

vector

store the coefficients

of direct labour hours (living labour) per unit of output

. The labour value

of commodity

is determined by the direct and indirect abstract labour time socially necessary to reproduce it:

. For the entire economy we can supress the subscript

and use matrix notation to represent labour values in terms of abstract labour hours:

. Assuming the input-output matrix

satisfies the Hawkins-Simon conditions, we can solve the linear system for the values of each commodity in the economy:

, where

is the

identity matrix.

Let be the vector of gross outputs in quantity terms, and

be the vector of net outputs in quantity terms. The labour theory of value assumes that all new value-added

derives from the direct expenditure of living labour

:

, hence

. As in the New Interpretation, we do not assume any market price system

in particular. The monetary expression of labour time (MELT) is defined as the ratio of the nominal price of the aggregate net output to the total expenditure of labour time in the period:

. Using

to indicate the nominal wage per hour per unit of output, we have that the value of labour power

is the aggregate wage bill (

) converted to labour hours:

. The price of the aggregate net product is equal to the aggregate wage bill plus aggregate profits:

. Because

represents the aggregate amount of paid labour time, aggregate profits

in monetary units then match aggregate surplus value

measured in unpaid labour hours:

. Aggregate net income in monetary units match aggregate net value in (paid plus unpaid) labour hours:

.

Let denote the digital commodity, whose reproduction uses non-labour inputs

but no direct living labour:

. Some minimal labour input is initially needed to configure the Bitcoin miners and setup the networked pools of miners, but the verification of the transactions in the blockchain is assumed to be fully automated. The individual labour value of the digital commodity is then entirely determined by the means of production used up:

, where the coefficients

already include the gradual depreciation of the computers. Hence, there is no value-added created in the production of Bitcoins. There is only value transferred from the non-labour means of production consisting mostly of computing power, warehouses, and electricity. The supply of

units of the digital commodity does increase the total gross output

of the economy in quantity terms. The net output

of the digital commodity in quantity terms increases as long as its production process satisfies

. The profit

per unit of the digital commodity is the difference between the market price

(which can be subject to substantial speculation and fictitious valorisation) and its costs of production:

.

As long as , the production of the digital commodity increases the aggregate net output

in quantity terms and in price terms

. The supply of the digital commodity, however, does not increase the aggregate value of the net output

because the total living labour

spent remains unaltered due to

. This implies that the profits

accrued in the production of the digital commodity in fact represent value-added drawn from the existing pool of value-added

in labour value terms. Because

rises but

remains the same, the MELT

rises and, hence, the value of money (the inverse of the monetary expression of labour time) falls with the production of the digital commodity.

From the perspective of Classical Political Economy and Marxist theory, in particular, Bitcoin mining is an unproductive activity since it does not create value-added. Bitcoin traders, which are not necessarily Bitcoin miners, already have positive stocks of previously accumulated wealth in the form of cash balances and other liquid assets which are used to purchase Bitcoins for price speculation. The profits that accrue to miners and traders must be, therefore, value-added drawn from other sectors of the global economy. But it is crucial to understand that these Bitcoin profits represent both transfers of value-added from elsewhere as well as transfers of stocks of wealth from non-Bitcoin sectors into the Bitcoin sector. These Bitcoin profits are then redistributed within the Bitcoin sector across miners and traders.

Agents using their existing wealth or even borrowed money to speculate with Bitcoin trading are increasing the price of Bitcoin through a pure wealth effect that gives to one what it takes from another. There is no net wealth increase in the aggregate. Because Bitcoin does not create new value-added or new wealth, its production and trading comprise a zero-sum game in terms of aggregate purchasing power.

Speculation and greater demand for the digital commodity will then increase its market price and create further incentives for more computers to join the blockchain network, on top of the inherent incentives already built into the Bitcoin software, which allow nodes to collect verification fees in exchange for proof-of-work or, soon, proof-of-stake.

Digital commodities: ownership and use

The technological revolution that modern computers created has also paved the way for the proliferation of digital products, digital commodities, and information commodities. In this section, we explain the meaning and implications of these concepts and we further show how Bitcoin and the blockchain technology have affected both the ownership and the use of digital commodities.

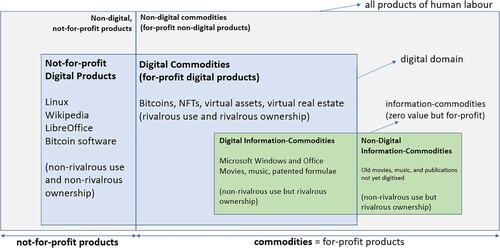

presents our taxonomy of products and commodities, indicating which elements are rivalrous in terms of ownership and usage. Rivalry in ownership means that there are legal or non-legal restrictions in terms of who owns the commodity. Rivalry in use means that there are physical or non-physical restrictions in terms of who can use a unit of the product at the same moment in time.

Figure 1. Taxonomy of products and commodities.

Bitcoin, in particular, introduces a new possibility: the existence of digital commodities, which in principle could be non-rivalrous both in ownership and use, but become rivalrous in both use and ownership via non-legal means. The crucial aspect is that the rivalry is maintained through non-legal means, without third party enforcement of monopoly rights. The Bitcoin blockchain maintains a permanent rivalry in terms of who can own and use the same unit of Bitcoin at any point in time, and this exclusion of access is accomplished without any juridical intervention by the state. By effectively instituting private property of digital assets that could in principle be infinitely reproducible at zero marginal cost, the blockchain technology is able to restrict both the ownership and the use of Bitcoins without resorting to any third party or legal apparatus.

We define as a digital product any product of human labour that exists solely as a string of bits and bytes, whether or not it is produced for profit. Digital commodities, which are digital products produced for profit, are a subset of the larger set comprising all digital products. Free and open-source software like Linux, LibreOffice, R, Python, Wikipedia, and also the Bitcoin software itself, are products of human labour and exist solely in the form of strings of bits and bytes, and for that matter are all digital products. They are certainly not produced for profit and, hence, cannot be classified as digital commodities.

The Bitcoin software is free and open source. It is a digital product not produced for profit and, thus, cannot be a digital commodity. Bitcoins themselves, however, are digital commodities since they are digital products explicitly produced for profit. Digital miners produce Bitcoins for profit, but they do so utilising a free open-source software that is not itself produced for profit. The Bitcoin software can be reproduced and used without legal restrictions. It is a non-rivalrous digital product in terms of both its use and its ownership. The units of Bitcoin, on the contrary, are rivalrous both in terms of their use and ownership. Cryptographed private keys, digital wallets, and the blockchain’s decentralised verification of transactions jointly prevent the unverified ownership, reproduction, and use of Bitcoins.

Within the domain of tangible commodities, rivalry often applies to both ownership and usage. A chair, a bicycle, and a toothbrush usually have a single owner and a single user at a specific point in time. It is not physically possible for more than one person to use the same toothbrush, to sit on the same chair, or to ride the same bicycle at the exact same moment in time. The purchase of these tangible commodities, moreover, also implies the transfer of its ownership. The buyer of a bicycle has the legal right to both the use and the private ownership over the tangible object that is being acquired.

Within the domain of intangible commodities like knowledge and information, goods can be reproduced indefinitely and, hence, are intrinsically non-rivalrous in their usage. But to ensure its profitable production, intellectual property rights are imposed on both its private ownership and use. A business idea or a drug formula that took years to be developed can be copied instantly once it is created. Patents, royalties, and intellectual monopoly rights then restrict the effortless reproduction of knowledge and information that were created for profit. These ‘new enclosures’ allow customers to use the commodified knowledge but also ensure that the ownership remains a private right of the creator. The buyer of a pair of jeans can do with them whatever pleases him: burn it, dress it, or cut into a pair of shorts. The user of commercial software like Microsoft Office, on the other hand, cannot do the same. Commodified knowledge is protected by intellectual property rights and its purchase only grants the right of usage, not the rights to ownership. The buyer of proprietary software is, in fact, purchasing a license to use the commercial software, not the right to own it as would happen with a standard tangible commodity.

The rise of the digital economy has also allowed for the creation and reproduction of commodities that have no value at all, which Teixeira and Rotta (Citation2012), Rotta (Citation2018), and Rotta and Teixeira (Citation2016, Citation2019) have called knowledge commodities or information commodities. The peculiarity of commodified knowledge and information is that, once produced, they require virtually no labour time either directly or indirectly to be further reproduced and, for this reason, are commodities with zero value. But despite having zero value (or very close to zero value), commodified information can have a high price tag, as is often the case with copyrighted intellectual property like software, chemical formulae, movies, music, scientific publications, product and process design. This is also the case with all other types of information that have zero marginal cost, and potentially non-rivalrous access if it were not for the ‘new enclosures’ of the digital age: the intellectual property rights protecting commodified information from free reproduction. In the case of commodified information, the difference between the market price and its zero value gives rise to information rents that also draw from the aggregate pool of value-added in the global economy.

By their own nature, information commodities can be reproduced indefinitely at zero marginal cost, or zero reproduction cost. A chemical formula can take years (and a lot of work) to be discovered, but once discovered it could be copied for free in unlimited amounts. The physical drug made using the formula requires labour time, but the reproduction of the formula itself does not. The formula, rather than the physical drug, is the information commodity. The physical drug has some value, which is the value that is transferred from its means of production and by the little amount of living labour that might be necessary. But the chemical formula itself has zero value given that once discovered it can be reproduced with virtually no labour time either directly or indirectly. One of the core features of commodified knowledge is that despite the substantial costs with research and development of the ‘mould’ (the first unit), the copies of the mould can be made at negligible cost. Software might take years to be developed, but once developed it can be reproduced at virtually no cost, thus creating a major source of tension between digital piracy and the copyright industry.

Despite being the product of a free open-source software, Bitcoin is a digital commodity but not an information commodity with zero value, as we indicate in , for its reproduction does require substantial expenditures of computational power and energy. Bitcoin, nonetheless, still shares two important features with information commodities: an artificially restricted supply, and rivalry in ownership.

Digital commodities can only be commodities if their supply is restricted artificially, otherwise, no profit could be earned from its production and ownership. Freely available software, for example, is not a commodity as it cannot be produced for profit. Bitcoin’s supply is artificially restricted by its own software which imposes three constraints: first, the software is hardcoded to keep a strict upper bound on the total supply of Bitcoins; second, the software diminishes the rate at which new Bitcoins can be mined over time; third, the software endogenously adjusts the difficulty of mining new Bitcoins as new miners enter or exit the blockchain.

Like knowledge-commodities, Bitcoin also relies on rivalry in ownership. But while knowledge-commodities need the legal apparatus of the state to enforce intellectual property rights, the Bitcoin blockchain achieves a similar result without third-party intervention. This key feature of the blockchain thus opens for the possibility of new digital commodities being sold through the blockchain and whose private ownership is automatically and securely verified by the blockchain itself, as is the case with non-fungible tokens (NFTs), smart contracts, and the expansion of the Ethereum blockchain. The development and exponential growth of the Ethereum network derives from the great potential that the blockchain technology offers in terms of automated verification of digital asset ownership with no state intervention.

The digital revolution that the Bitcoin and Ethereum blockchains created, especially regarding the institutionalisation of private property within the digital domain and without state enforcement, is now paving the way for the rapid proliferation of NFTs, virtual assets, and also of virtual real estate within the metaverses. NFTs, in particular, have two components. The first component of the NFT is the underlying asset, which could be a wide gamut of both digital and non-digital assets ranging from memes to industrial equipment. The second component is the registry on the blockchain which establishes the authenticity, uniqueness, and proprietorship of the underlying asset. The value of the NFT’s underlying asset and the value of the registry are both determined by the direct and indirect labour time socially necessary to reproduce them, as is the case with any other digital or non-digital commodity. The value of the NFT registry on the blockchain, moreover, is similar to the value of a Bitcoin: it is the value that gets transferred from the non-labour inputs (electricity, computational power, and warehousing) that keep the blockchain running. Similarly to a unit of Bitcoin, the NFT registry has value but no value-added. Within the metaverses, an analogous process takes place, for the virtual assets stored within them have a similar digital nature to Bitcoins and NFTs: they require either zero or negligible amounts of direct labour but substantial sums of non-labour inputs to be kept online.

Can a digital commodity become money?

A digital commodity, under certain conditions, could become money. The main task, however, is to understand what money is. In this section we define what money is according to the labour theory of value from Classical Political Economy and then show under what conditions a digital commodity could become money, irrespective of its value or value-added content.

One of the most common conceptualisations of money is to posit it as a unit of account created by the state (Keynes Citation[1930] 2011, Davidson Citation1999, Wray Citation1998, Ingham Citation2004, Graeber Citation2012). States issue money with which they can purchase assets from the market. The money issued is then recorded as a liability either for the central bank or for the treasury. The chosen unit of account is arbitrary and is implemented top-down from the state to the market. The ultimate constitutional power to issue money lies with the state, even though it can grant permission for private commercial banks to also create money endogenously upon the issuance of new loans.

The denomination of the unit of account is certainly arbitrary and defined by the state. But a deeper question must be addressed: What does the unit of account actually represent? Or, alternatively, what does the monetary unit represent? A dollar or a pound sterling of what exactly?

Classical Political Economy and the labour theory of value advocate the notion that all wealth in the economy requires labour time to be produced and, hence, that money is the general equivalent that represents quantities of abstract labour time. Money synthesises the equivalence between hours of abstract labour and monetary units. Marx, in particular, argued that money can be defined as the social character of labour (that is, value) objectified into an autonomous thing. Money is value as an autonomous object:

It is the foundation of capitalist production that money confronts commodities as an autonomous form of value, or that exchange-value must obtain an autonomous form in money. (Marx Citation[1894] 1994, pp. 648–649)

But in what way are gold and silver distinguished from other forms of wealth? Not by magnitude, for this is determined by the amount of labour embodied in them. But rather as autonomous embodiments and expressions of the social character of wealth. This social existence that it has thus appears as something beyond, as a thing, object or commodity outside and alongside the real elements of social wealth […] The social form of wealth exists alongside wealth itself as a thing. (Marx Citation[1894] 1994, pp. 707–708)

Money is the independent existence of exchange value. Viewed from the angle of its quality, it is the material representative of abstract wealth, the material existence of abstract wealth. To make money by means of money is the purpose of the capitalist production process – the increase of wealth in its general form, of the quantity of objectified social labour which is, as this labour, expressed in money. Whether the existing values figure merely as money of account in the ledger, or in whatever other form, as tokens of value, etc., is initially a matter of indifference. Money appears here only as the form of independent value. (Marx Citation[1861–63] 1988, p. 99)

As long as the social character of labour appears as the monetary existence of the commodity and hence as a thing outside actual production, monetary crises, independent of real crises or as an intensification of them, are unavoidable. (Marx Citation[1894] 1994, p. 649)

Money in its third quality, as something which autonomously arises out of and stands against circulation, therefore, still negates its character as coin […] Money is the negation of the medium of circulation as such, of the coin. But it also contains the latter at the same time as an aspect, negatively, since it can always be transformed into coin. (Marx Citation[1857–58] 1973, pp. 226–228)

For Marx, money is the result of an objective process of real abstraction through which it becomes the universal representation of autonomised abstract wealth. The unit of account can only truly represent abstract labour time if money operates the objective abstraction that goes from a universal property of commodities (that is, value as the social character of human labour) and then transforms the abstract character of value itself into an independent, autonomous object. The denomination of the unit of account (dollars, euros, or yuans) is an arbitrary choice of the modern state, but what the unit of account actually represents in a market economy is not in any way arbitrary.

Bitcoin's role as a speculative digital commodity, however, prevents it from being stablished as money. The instability that is created by its volatile demand actually undermines its own potential role as money. Furthermore, Bitcoin cannot fulfil the desired functions of money either: (i) stable store of value; (ii) efficient medium of exchange; (iii) widely accepted to settle transactions. The literature on the subject (Yermack Citation2015, Paraná Citation2020, Citation2021) has already demonstrated that Bitcoin has not been able to function as a stable store of value, as its exchange rate against other major currencies is extremely volatile and subject to massive appreciations and depreciations, even when compared to third-world currencies. Bitcoin has also been unable to become an efficient medium of exchange. Its decentralised blockchain can process only 4.6 transactions per second on average, greatly underperforming Visa’s average of 1700 transactions per second globally and its capacity of up to 56,000 transactions per second if needed. The Bitcoin network also consumes a massive amount of electricity per year, comparable to the total energy consumption of an entire country like Ireland. Bitcoin is extremely energy inefficient and has a massive carbon footprint. Bitcoin is also far from being widely accepted to settle transactions since very few places accept payment in Bitcoin or in any other cryptocurrency for that matter. And because of its anonymous private key technology, Bitcoin has become an important instrument for money laundering, wealth sheltering, financing of illegal activity, and means of payment for ransomware. Bitcoin’s failure to become true money has nonetheless not prevented it from becoming a world trend in gambling, even if its speculative role actually undermines its potential role as money. Bitcoin has become a highly speculative digital asset in a world awash in excess liquidity since the 2008 financial crisis, exacerbated by successive rounds of quantitative easing, negative interest rates, and the ultra-loose monetary policy after the Covid-19 pandemic.

Bitcoin’s fate demonstrates that it is unlikely for a digital commodity to become true money if greater demand for it triggers an unstable speculative process that undermines its potential character as a universal equivalent and autonomous representation of abstract social wealth. Bitcoin’s usefulness as a speculative digital commodity seems to be an impediment to its establishment as a universal equivalent that represents abstract labour time in a stable form. In this regard, we believe that it is more likely for a digital money to spring out of a central bank, from a powerful tech company, or from some kind of collaboration between them.

The blockchain technology behind Bitcoin, nonetheless, has true promising potential, much greater than Bitcoin itself, as it allows for the decentralisation and automation of many financial activities. Even if Bitcoin does not survive, the blockchain technology will, and will probably become the basis for automated, self-verified, self-executed financial contracts. It is possible, though difficult to foresee, that the permission-less and trust-less properties of the blockchain will have an impact on finance in the same order of magnitude as the impact that the mp3, the internet, and Napster had on the music industry.

Final remarks on digital commodities in general

In the paper, we employed the labour theory of value from Classical Political Economy to demonstrate that Bitcoin and other similar pseudo cryptocurrencies should be defined not as digital money or currency but instead as digital commodities. A digital commodity is a product of human labour that is both useful and produced for profit but restricted to the electronic domain of bits and bytes. Its nature as a digital commodity is what allows Bitcoin and other pseudo cryptocurrencies to be produced and accumulated as digital assets without any matching financial liability to its original producer.

We also employed the New Interpretation of the labour theory of value to show how the production of digital commodities like Bitcoin imply a transfer of value from its non-labour means of production without entailing the creation of new value-added. Because Bitcoin mining is mostly done by computers, with negligible amounts of direct labour input, it does not give rise to a corresponding value-added. In this way, the trading with and the mining of new Bitcoins merely redistribute existing value-added and wealth. Bitcoin mining does not create new purchasing power, it reallocates already existing purchasing power. Hence, even though it might seem to make a few people rich at the microeconomic level, Bitcoin is a zero-sum game at the macroeconomic level. It reallocates existing wealth without adding to it. The System of National Accounts (SNA), however, misses this important feature by incorrectly identifying all marketable activities as creators of value-added, therefore, not properly distinguishing between productive and unproductive activities.

The computer revolution and widespread adoption of the internet have allowed capitalism to commodify digital products on an unprecedented scale. The Bitcoin and blockchain technologies now institutionalise private property within the digital domain and without state enforcement. Automation in the digital world further allows for the reproduction of digital commodities without direct living labour, as is the case not only with cryptos but also NFTs, smart contracts, and virtual assets within metaverses. Our argument, therefore, extends to the larger domain of digital assets that can be reproduced with no expenditure of direct labour. The profits made out of their reproduction are redistributions of value-added originated in productive activities located elsewhere in the global economy. A digital commodity can certainly increase labour productivity in other productive activities and, hence, indirectly increase the aggregate value-added. But as long as a digital commodity requires no expenditure of living labour it will not directly originate new value-added and, hence, any profits made from its reproduction are reallocations of existing value-added.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abbatemarco, N., De Rossi, L., and Salviotti, G., 2018. An econometric model to estimate the value of a cryptocurrency network. The Bitcoin case. Association for Information Systems Electronic Library, Research Paper 164. Available from: https://aisel.aisnet.org/ecis2018_rp/164.

- Abramova, M., Dubova, S., and Krivoruchko, S., 2020. Marxism and digital money as a new reality of social and economic system. In: M. L. Alpidovskaya, and E. G. Popkova, eds. Marx and modernitiy: a political and economic analysis of social systems management. Charlotte, NC: Information Age Publishing Inc., 411–21.

- Aglietta, M., 2018. Money: 5000 years of debt and power. Brooklyn, NY: Verso.

- Baldan, C., and Zen, F., 2020. The bitcoin as a virtual commodity: empirical evidence and implications. Frontiers in artificial intelligence, 3, 1–13. Article 21.

- Barber, A., 2015. Bitcoin and the philosophy of money: evaluating the commodity status of digital currencies. Spectra, 4 (2). Available from: https://spectrajournal.org/articles/66/#.

- Baur, D.G., Hong, K., and Lee, A.D., 2018. Bitcoin: medium of exchange or speculative assets? Journal of international financial markets, institutions and money, 54, 177–89.

- Bjerg, O., 2016. How is bitcoin money? Theory, culture & society, 33 (1), 53–72.

- Bonilla, C.M., 2020. ¿Otro Dinero es Posible? Conexiones entre la Mercancía Dineraria dentro de la Teoría del Valor-Trabajo de Das Kapital, el Bitcoin y la Descentralización de la Economía. Teknokultura, revista de cultura digital y movimientos sociales, 17 (2), 141–8.

- Cogliano, J.F., et al., 2018. Value, competition and exploitation: Marx’s legacy revisited. Northampton: Edward Elgar.

- Davidson, P., 1999. The nature of money. In: L. Davidson, ed. Uncertainty, international money, employment and theory: the collected writings of Paul Davidson. London: Macmillan, 169–78.

- Dodd, N., 2018. The social life of bitcoin. Theory, culture & society, 35 (3), 35–56.

- Duménil, G., 1980. De la valeur aux prix de production. Paris: Economica.

- Duménil, G., and Lévy, D., 2000. The conservation of value: a rejoinder to Alan Freeman. Review of radical political economics, 32 (1), 119–46.

- Eichengreen, B. 2019. From commodity to Fiat and now to Crypto: what does history tell us? NBER Working Paper w25426. National Bureau of Economic Research.

- Foley, D., 1982. The value of money, the value of labor power, and the Marxian transformation problem. Review of radical political economics, 14 (2), 37–47.

- Foley, D., 2000. Recent developments in the labor theory of value. Review of radical political economics, 32 (1), 1–39.

- Foley, D., 2018. The new interpretation after 35 years. Review of radical political economics, 50 (3), 559–68.

- Foley, D., and Duménil, G., 2008. Marxian transformation problem. In: P. Macmillan, ed. The new Palgrave dictionary of economics. London: Palgrave Macmillan. https://doi.org/10.1057/978-1-349-95121-5_2082-1.

- Golumbia, D., 2016. The politics of bitcoin: software as right-wing extremism. Minneapolis: University of Minnesota Press.

- Graeber, D., 2012. Debt: the first 5000 years. New York: Penguin.

- Graf, K., 2014. Commodity, scarcity, and monetary value theory in light of bitcoin. Prices & markets, 3 (3), 1–24.

- Gronwald, M., 2019. Is bitcoin a commodity? On price jumps, demand shocks, and certainty of supply. Journal of international money and finance, 97, 86–92.

- Hayek, F.A., 1976. Choice in currency: a way to stop inflation. London: Institute of Economic Affairs.

- Hayes, A., 2017. Cryptocurrency value formation: an empirical study leading to a cost of production model for valuing bitcoin. Telematics and informatics, 34 (7), 1308–21.

- Hayes, A., 2018. Bitcoin price and its marginal cost of production: support for a fundamental value. Applied economics letters, 26 (7), 554–60.

- Hayes, A., 2019. The socio-technological lives of bitcoin. Theory, culture & society, 36 (4), 49–72.

- Hayes, A., 2021. World monies or money-worlds: a new perspective on cryptocurrencies and their moneyness. Finance and society, 7 (2), 130–9.

- Ingham, G., 2004. The nature of money. Cambridge: Polity Press.

- Karlstrøm, H., 2014. Do libertarians dream of electric coins? The material embeddedness of bitcoin. Distinktion: Scandinavian journal of social theory, 15 (1), 23–36.

- Keynes, J.M., [1930] 2011. A treatise on money. Eastford: Martino.

- Kostakis, V., and Giotitsas, C., 2014. The (a)political economy of bitcoin. TripleC: communication, capitalism & critique, 12 (2), 431–40.

- Laibman, D., 2012. Political economy after economics. London: Routledge.

- Marx, K., [1857–58] 1973.Grundrisse: foundations of the critique of political economy. London: Penguin Books.

- Marx, K., [1861–63] 1988. Marx and Engels collected works, vol. 30: 1861–63 economic manuscripts. New York: International Publishers.

- Marx, K., [1894] 1994. Capital: volume III. London: Penguin Books.

- Maurer, B., Nelms, T.C., and Swartz, L., 2013. When perhaps the real problem is money itself! The practical materiality of bitcoin. Social Semiotics, 23 (2), 261–77.

- Mohun, S., 1993. A note on Steedman’s joint production and the new solution to the transformation problem. Indian economic review, 28 (2), 241–6.

- Mohun, S., and Veneziani, R., 2018. Value, price, and exploitation: the logic of the transformation problem. In: Roberto Veneziani, and Luca Zamparelli, eds. Analytical political economy. Hoboken: Wiley-Blackwell, 269–306.

- Nakatani, P., and Mello, G.M.C., 2019. Crypto-currencies: from the fetishism of Gold to Hayek Gold. In: G. Mello, and M. Sabadini, eds. Financial speculation and fictitious profits: a Marxist analysis. London: Palgrave Macmillan, 63–85.

- Nelms, T.C., et al., 2018. Social payments: innovation, trust, bitcoin, and the sharing economy. Theory, culture & society, 35 (3), 13–33.

- Paraná, E., 2020. Bitcoin: a Utopia tecnocrática do dinheiro apolítico [Bitcoin: the technochractic Utopia of apolitical money]. São Paulo: Autonomia Literária. Forthcoming English translation: Money and Social Power: A Study on Bitcoin. Leiden, Boston: Brill.

- Paraná, E. 2021. The political economy of bitcoin. Current affairs lecture, University of Groningen. Working paper. Available from: https://edemilsonparanainfo.files.wordpress.com/2021/03/the-political-economy-of-bitcoin-lecture.pdf.

- Rotta, T.N., 2018. Unproductive accumulation in the United States: a new analytical framework. Cambridge journal of economics, 42 (5), 1367–92.

- Rotta, T.N., and Teixeira, R.A., 2016. The autonomisation of abstract wealth: new insights on the labour theory of value. Cambridge journal of economics, 40 (4), 1185–201.

- Rotta, T.N., and Teixeira, R.A., 2019. The commodification of knowledge and information. In: M. Vidal, etal, ed. The Oxford handbook of Karl Marx. New York: Oxford University Press, 79–399.

- Swartz, L., 2018. What was bitcoin, what will it be? The techno-economic imaginaries of a new money technology. Cultural studies, 32 (4), 623–50.

- Tamer, M., 2019. As criptomoedas como mercadoria-equivalente específica. Revista da procuradoria-geral do banco central, 12 (2), 110–21. Available from: https://revistapgbc.bcb.gov.br/index.php/revista/article/view/961.

- Teixeira, R.A., and Rotta, T.N., 2012. Valueless knowledge-commodities and financialization: productive and financial dimensions of capital autonomization. Review of radical political economics, 44 (4), 448–67.

- Tymoigne, E. 2013. The fair price of a bitcoin is zero. New economic perspectives. Available from: http://neweconomicperspectives.org/2013/12/fair-price-Bitcoin-zero.html [Accessed 9 Aug 2021].

- Varoufakis, Y. 2013. Bitcoin and the dangerous fantasy of ‘apolitical’ money. Available from: https://www.yanisvaroufakis.eu/2013/04/22/bitcoin-and-the-dangerous-fantasy-of-apolitical-money [Accessed 9 Aug 2021].

- Von Mises, L., [1912] 1981. The theory of money and credit. Indianapolis: Liberty Fund.

- Wang, G., 2019. Marx’s monetary theory and its practical value. China political economy, 2 (2), 182–200.

- White, R.S., et al., 2020. Is bitcoin a currency, a technology-based product, or something else? Technological forecasting and social change, 151, 1–13, 119877. https://doi.org/10.1016/j.techfore.2019.119877.

- Wray, L.R., 1998. Understanding modern money. Cheltenham: Edward Elgar.

- Yermack, D., 2015. Is bitcoin a real currency? An economic appraisal. In: D. L. K. Chuen, ed. Handbook of digital currency. San Diego: Academic Press, 31–43.