ABSTRACT

Financial risks related to climate change and biodiversity loss are currently being addressed in a largely siloed manner. Neglecting their interconnections, however, may lead to ‘blind spots’ and misestimations of systemic financial risk, potentially undermining progress on both climate finance policy and emerging policy on biodiversity-related financial risks (BRFR). In particular, the ‘risk measurement–based’ approach dominating climate finance policy, which is now being taken up to address BRFR, is poorly equipped to address the radical uncertainty that characterises both types of risks. Furthermore, many BRFR may materalise over a more immediate horizon than climate risks. In this paper, we examine how central banks and financial supervisors are approaching the topic of BRFR in relation to climate-related financial risk. We argue that policymakers should focus upon the broader concept of systemic environmental-financial risks to account for the interactions and trade-offs between both domains of biodiversity and climate change. Instead of seeking evidence of financial materiality before acting, focusing on how the financial system is actively facilitating direct drivers of environmental damage offers a way for financial policymakers to assess potential sources of such risks on the basis of information available today. In turn, policy interventions should aim to reduce harmful flows of finance that may lead to the crossing of dangerous ecological tipping points.

Key policy insights

Financial policymakers need to think beyond siloes, and act on a precautionary basis to manage climate- and biodiversity-related financial risks concurrently.

Financial authorities, coordinating with relevant government departments, should define business activities that are most harmful to climate and biodiversity, especially those contributing to ecological tipping points, e.g. activities linked to tropical deforestation, which will damage both domains.

To aid transparency and supervisory risk assessment, financial supervisors could require the mandatory disclosure of portfolio composition, risk management, and due diligence procedures relating to the financing of identified harmful activities.

Financial regulators could use their toolkits to discourage the financing of such activities, e.g. by applying punitive capital requirements.

This approach may require greater coordination between central banks and other government departments to maintain democratic legitimacy and support existing central bank mandates.

1. Introduction

Central banks and financial supervisors have acknowledged that climate change poses material risks to the financial system and that the management of climate-related financial risks (CRFR) falls within their mandates to preserve price and financial stability (Bank of England, Citation2017; ECB, Citation2020; NGFS, Citation2019a NGFS, Citation2020a). With the majority of biodiversity and ecosystem indicators precipitously declining (IPBES, Citation2019), attention is now also turning to the economic and financial threats posed by biodiversity loss (Dasgupta, Citation2021; NGFS-INSPIRE, Citation2022; OECD, Citation2019).

As with climate change, financial institutions are exposed to the dependencies and impacts of businesses on biodiversity through their lending, investing, insurance, and advisory activities (Kedward et al., Citation2021a). These biodiversity-related financial risks (BRFR) have been conceptualised in a similar manner to CRFR (Herweijer et al., Citation2020; NGFS-INSPIRE, Citation2022). Physical risk factors refer to disruptions to business inputs, operating environments, or consumer demand resulting from biodiversity loss, e.g. declines in pollinators adversely affecting crop yields. Transition risk factors refer to economic losses stemming from actions taken to mitigate biodiversity loss, including shifts in policy, regulation, technology, trade, or consumer preferences, e.g. the EU’s proposal to remove deforestation-risk commodities from EU supply chains (European Commission, Citation2021a).

The real economy impacts of biodiversity-related physical and transition risk factors – just as with climate change – could include disrupted production, (global) value chains, and productivity; lower corporate profitability; reduced cashflow; or impaired insurability. In turn, these effects can feedback through to the financial system via impaired asset valuations, reduced ability to service debts, liquidity difficulties, reputational damage, or legal costs; or through broader macroeconomic variables, such as shocks to exchange rates, volatile commodity prices, or sovereign debt sustainability (Pinzón & Robins, Citation2020; Rudgley & Seega, Citation2021). An emerging literature reveals potentially material exposures to BRFR within banks (Calice et al., Citation2021; Svartzman et al., Citation2021a; Van Toor et al., Citation2020), insurers (SIF, Citation2021), global asset managers (Galaz et al., Citation2018; Springer et al., Citation2020), pension funds (Global Canopy, Citation2022), development finance institutions (Dixon, Citation2020), and central bank asset portfolios (Kedward et al., Citation2021b).

Although at an early stage, financial initiatives focusing on biodiversity are following a similar trajectory to CRFR, with an emphasis on developing reporting and disclosure mechanisms to enable financial institutions to identify and manage financial risks (Finance for Biodiversity, Citation2021; NGFS-INSPIRE, Citation2022). For example, the Taskforce for Nature-related Financial Disclosures (TNFD) aims to establish a harmonised framework for financial institutions to report on BRFR from 2023 onwards (TNFD, Citation2021), following the model established by the Taskforce on Climate-related Financial Disclosures (TCFD).

Within the central banking community, researchers have undertaken studies to estimate BRFR exposure (Svartzman et al., Citation2021a; Van Toor et al., Citation2020). In a joint study group with external researchers, the Network for Greening the Financial System (NGFS) – a group of over 100 central banks and financial supervisors – also explored the implications of biodiversity loss on financial stability, concluding its relevance to primary mandates (NGFS-INSPIRE, Citation2022). Whilst its final report identifies a comprehensive research agenda and explores possible policy options for financial policymakers, it stops short of recommending concrete policy interventions to mitigate BRFR, citing a prerequisite need to develop risk assessment methodologies and capacity building within institutions.

This paper takes this important agenda a step further by exploring how central banks and financial supervisors can assess and manage BRFR in the context of existing policy agendas on climate finance. We find that BRFR and CRFR are being addressed in a siloed and sequential fashion, with insufficient focus on integrating biodiversity-related factors into existing approaches for assessing and managing CRFR. By neglecting the interconnections that exist between these two categories of risk, existing efforts to assess climate risk may be subject to ‘blindspots’ and significant misestimations, which could have adverse consequences for financial stability.

Financial policymakers are also largely pursuing a ‘risk measurement-based’ agenda to mitigating both CRFR and BRFR, which assumes that supporting the disclosure of relevant environmental information will be sufficient to ensure the management of potential financial risks via market price adjustments. This approach has been critiqued extensively in the context of climate change (Ameli et al., Citation2020; Bolton et al., Citation2020; Chenet et al., Citation2021; Christophers, Citation2017). We build on this literature to show that addressing climate and biodiversity risks together is a vastly more complex task than is recognised by current policy agendas due to the presence of radical uncertainty. Financial policymakers are also focusing too narrowly on attempting to quantify the materiality of both climate change and biodiversity loss to the financial system (‘single materiality’), with insufficient focus on the relevance of the negative impacts of the financial system on the climate and environment (‘double materiality’ – Adams et al., Citation2021).

In light of the limitations of risk measurement-based approaches, we propose new ways forward for central banks and financial supervisors to manage radically uncertain climate-related and biodiversity-related financial risks. Building upon recent calls for a ‘precautionary approach’ to financial policy (Chenet et al., Citation2021), we show how focusing on where and how the financial system is actively facilitating direct drivers of climate change and biodiversity loss offers a way for policymakers to assess potential sources of endogenous risk on the basis of information available today. Given that the capital allocation decisions of financial actors today will influence future climate and biodiversity trajectories, there is a case for financial policymakers to manage both CRFR and BRFR by taking more direct interventions to reduce harmful flows of finance, and support the transition of capital to more sustainable forms of economic activity. Such an approach warrants coordination between central banks and broader government objectives regarding environmental policy to maintain democratic legitimacy.

In this paper, we refer to environmental-financial risks to encompass climate change, biodiversity loss, and the broader deterioration of ecosystems – as well as the interconnections between them.Footnote1 We focus on central banks and supervisors as actors whose actions have already accelerated the uptake of CRFR management within financial institutions, and whose regulatory power is capable of expanding and shaping the climate finance policy agenda to include other interconnected environmental risks. However, our arguments also remain relevant to a broader range of financial institutions and policymakers.

The paper proceeds as follows. Section 2 outlines how financial institutions and supervisors are currently attempting to understand and manage BRFR in relation to their climate policy agendas, and the weaknesses of these approaches in light of the interactions between climate change and biodiversity loss. Section 3 considers the intellectual underpinnings of the CRFR measurement approach and its limitations when applied to biodiversity risks. Section 4 explores how financial policymakers can assess both CRFR and BRFR subject to radical uncertainty, focusing on the double materiality perspective. Section 5 considers alternative policy trajectories in the management of environmental-financial risks, and reflects on the institutional role of central banks. Section 6 outlines urgent areas for further research, and concludes.

2. The climate–biodiversity nexus and the emergence of financial risk

Progress by financial actors in addressing environmental-financial risks has so far focused mainly on climate change (Crona et al., Citation2021; NGFS, Citation2020c NGFS, Citation2021a). A number of novel frameworks focusing on broader environmental exposures are now under development by financial institutions (e.g. Finance for Biodiversity, Citation2021), although these remain exploratory and heterogenous (see Supplementary Information). Exploratory research on BRFR undertaken by researchers within central banks has aimed at quantifying the magnitude of potential financial risk exposure within domestic jurisdictions. For example, the Dutch central bank, De Nederlandsche Bank (DNB), quantitatively mapped the physical and transition risks of domestic biodiversity loss, estimating that 36% of Dutch financial institutions are highly dependent on at least one ecosystem service (Van Toor et al., Citation2020). Using an extended methodology that accounts for upstream effects, other central bank researchers have found that all securities held by French financial institutions are to a greater or lesser extent dependent on all ecosystem services through their supply chains (Svartzman et al., Citation2021a).

These emerging developments within the central banking community are welcome and are urgently needed in order to address the prominent knowledge gaps surrounding financial system exposures to biodiversity loss. However, it is revealing to contrast this very early research focus on biodiversity loss with equivalent workstreams on climate change, where the significance of CRFR is well-established and where some central banks and supervisors are now actively exploring and implementing policy options to manage such risks (Bank of England, Citation2021b; ECB, Citation2021) – albeit with this policy implementation itself still at an early stage (D’Orazio, Citation2021). Similarly, central bank speeches on climate change are now plentiful but, at the time of writing, there has yet to be an official speech that comprehensively presents the specific topic of BRFR, and its interconnections with CRFR, by any major central bank. A key concern at the current juncture is that financial policymakers are approaching CRFR and BRFR on different tracks and at different speeds, which may lead to them to neglect the potential interconnections that exist between these categories of environmental risk.

The European Central Bank (ECB) is an illustrative example in this regard. Despite President Christine Lagarde stating that ‘climate and biodiversity are two sides of the same coin; it is vital that we look at them together’,Footnote2 the ECB’s concrete policy developments regarding environmental risk – namely, the strategy review for monetary policy, the economy-wide climate stress test, and the supervisory climate risk stress test – focus on climate change and do not mention the potential relevance of BRFR (Alogoskoufis et al., Citation2021; ECB, Citation2021). Similarly, whilst the ECB’s supervisory guidance does emphasise the relevance of broader environmental risks, in practice this document is vague about the definition and transmission mechanisms of these risks and does not discuss how they may interact with CRFR (ECB, Citation2020).Footnote3 Existing studies by central bank researchers also underplayed the financial stability implications of interactions between CRFR and BRFR (Svartzman et al., Citation2021a; Van Toor et al., Citation2020); although the NGFS-INSPIRE Study Group identified this as an important research gap (NGFS-INSPIRE, Citation2022, pp. 18–20).

There are a number of concerns with this siloed and sequential approach to understanding environmental-financial risks. First, climate change interacts with and is reinforced by other environmental risks, especially biodiversity loss. Second, some biodiversity-related physical risk factors may become financially material within a much shorter time frame than the worst expected climate-related impacts. Third, the trade-offs and synergies between climate mitigation policies and biodiversity impacts, and vice versa, are neglected with implications for the estimation of transition risks. We now discuss each of these ‘blind spots’ in turn and their implications for effective financial policymaking.

From the physical risks perspective, the biophysical dynamics driving climate change and biodiversity loss are strongly interlinked and mutually reinforcing (Lade et al., Citation2020; Rockström et al., Citation2009; Steffen et al., Citation2018). The physical impacts of climate change – especially higher temperatures, shifting rainfall patterns, higher frequency of extreme weather events, and the acidification and oxygen depletion of water bodies – put ecosystems under stress and contribute to biodiversity loss (IPBES, Citation2019). In turn, the loss of key habitats and adverse changes in biodiversity negatively affect the climate system, through changes in the carbon, nitrogen, and water cycles, and via adverse effects on the carbon sequestration capabilities of biomass (IPBES and IPCC, Citation2021). Critically, changes affecting both the climate and biosphere are non-linear. Once critical thresholds or ‘tipping points’ are breached, natural systems can undergo rapid regime shifts with catastrophic and potentially irreversible consequences for biodiversity, the climate, and human activity (Lenton, Citation2013; Sharpe & Lenton, Citation2021; Steffen et al., Citation2015).

Importantly for businesses, financial institutions, and policymakers, the complex feedback loops governing these interactions mean that associated financial risks will be compounding rather than additive. Yet these non-linear dynamics are largely neglected by Environmental, Social, and Governance (ESG) frameworks, which for the most part simplistically aggregate estimations of risk factors without considering potential interactions between them (Crona et al., Citation2021). Similarly, by neglecting the interactions between various environmental dynamics, financial policymakers are likely to be generating potentially significant misestimations of financial exposure to climate change and biodiversity loss. This is because compound risks significantly magnify the impacts of individual shocks, in terms of both severity and duration (Ranger et al., Citation2021).

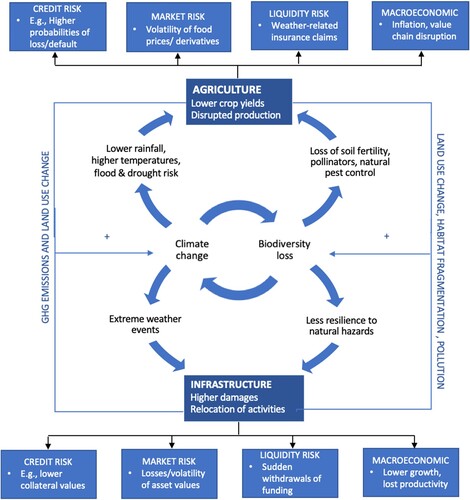

With reference to two sectors both exposed and contributing to climate change and biodiversity loss – agriculture and infrastructure (IPBES, Citation2019; UNEP-WCMC, Citation2020), illustrates how selected financial risks resulting from climate change, e.g. lower crop yields and higher infrastructure damages, are also exacerbated by the effects of biodiversity loss. These, in turn, may generate larger than expected financial losses for financial institutions.

Figure 1. Interconnected climate- and biodiversity-related physical impacts may have compounding economic impacts that result in higher than expected financial risks. Source: Authors’ own illustration

The significance of these interconnections is that current efforts to establish and measure climate-related physical risk exposures are likely to be misestimations unless other environmental dynamics are considered. Whilst existing climate-economy models that underpin the scenario analyses currently used by financial policymakers do include some feedback loops in the climate system (e.g. land use dynamics), at present these scenarios do not account for how biodiversity-specific physical risk channels may affect the resilience of the financial system (NGFS-INSPIRE, Citation2022).Footnote4 The ECB’s economy-wide climate stress test, for example, included only flooding, wildfires, sea-level rise, water stress, heat stress, earthquakes and hurricanes in its calculation of firm-level forward-looking physical risk scores (Alogoskoufis et al., Citation2021).

This oversight becomes even more problematic when considering the differing time horizons of climate- and biodiversity-related physical impacts. For example, the ECB expects physical risks to ‘primarily materialise in the medium to long term’ (ECB, Citation2020, p. 13). Similarly, the NGFS reference scenarios consider that the effects of climate change will adversely affect crop yields only from 2060 onwards (NGFS, Citation2020b; NGFS and INSPIRE, Citation2021). Yet it is increasingly acknowledged that agriculture is also exposed to shorter-term biodiversity-related physical risks, such as pollinator loss and soil erosion (Garibaldi et al., Citation2011; IPBES, Citation2016; Sartori et al., Citation2019) that may have financial impacts in the nearer term. Additionally, at the regional scale, several critical biomes involving tropical rainforests and coral reefs are considered to be rapidly approaching ‘tipping points’ (Lovejoy & Nobre, Citation2019; Schellnhuber et al., Citation2016; Staal et al., Citation2020; van Hooidonk et al., Citation2016). Tipping dynamics are also relevant to climate change (Lenton, Citation2013; Steffen et al., Citation2015). The presence of these non-linear dynamics suggest that some environmental-financial risks may materialise in the nearer term. As we discuss further in Section 3, this implies a trade-off between knowledge-building and policy intervention that is at present underappreciated by financial policymakers.

Climate change and biodiversity loss are also interconnected from a transition risks perspective, sharing common anthropogenic drivers of change. Yet the integrated assessment models (IAMs), which underpin the scenario risk modelling methodologies used by central banks, primarily focus on greenhouse gas (GHG) emitting sectors as the main sources of transition risk (e.g. using shadow carbon prices to proxy for the intensity of climate mitigation actions) (Ghersi et al., Citation2021; Hansen, Citation2022; Svartzman et al., Citation2021b). More recent studies have explored actions to mitigate the loss of biodiversity, focusing on the transition risks associated with the post-2020 Global Biodiversity Framework’s proposed target to conserve 30% of the earth’s surface (Waldron et al., Citation2020), or nitrogen-intensive fertiliser use (Van Toor et al., Citation2020). In general, however, the interactions between climate-related and biodiversity-related transition risks remain under-researched. By focusing on these risks in isolation, policymakers may be failing to account for the fact that actions designed to mitigate various environmental problems are not necessarily mutually supportive.

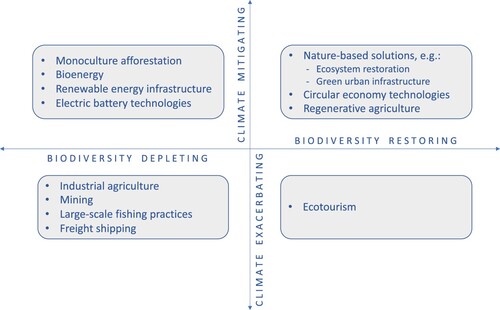

visualises where trade-offs and synergies between biodiversity and climate solutions may emerge. In the top left quadrant are some examples of climate mitigation activities that may have negative consequences for biodiversity. For example, several studies have shown that the land use change implied by low emission scenarios relying on bioenergy crops may have severe impacts upon biodiversity (Hof et al., Citation2018; Immerzeel et al., Citation2014; Tarr et al., Citation2017).Footnote5 If policy actions to protect biodiversity become more developed and widespread – as is the ambition following the forthcoming COP15 Biodiversity Conference – the climate mitigation activities in the top-left quadrant may become subject to biodiversity-related transition risks that are at present unaccounted for in environmental-financial risk analysis.

Figure 2. Selected sector-based examples of potential trade-offs and synergies between selected climate and biodiversity solutions. Source: Authors’ own illustration, based on literature detailed in the text

In other sectors – depicted in the bottom-left quadrant of – negative climate impacts are well-established, but there has been insufficient focus by financial actors on other sources of transition risk. The emissions associated with mining and real estate, for example, are well known but are considered largely abatable through electrification. Yet, these sectors may face additional and potentially significant financial risks should targets such as those proposed in the post-2020 draft Global Biodiversity Framework be enacted. The target to conserve 30% of land and sea areas globally, for example, could create stranded mining and infrastructure assets as conservation policies restrict development across certain ecosystems (Caldecott et al., Citation2013; Waldron et al., Citation2020). The bottom-left quadrant hence depicts where current efforts to understand transition risks may be significant underestimations.

Conversely, there are also important synergies to be gained from climate mitigation activities that are also protective or restorative for ecosystems, such as the ‘nature-based solutions’ shown in the top-right quadrant (IPBES and IPCC, Citation2021; Smith et al., Citation2019), which has implications for the appropriate definition and design of green financial instruments (Deutz et al., Citation2020; The Nature Conservancy, Citation2019). Indeed, an IPBES-IPCC joint report on climate and biodiversity found that ‘on balance, the evidence suggests more mutually synergistic benefits than antagonistic trade-offs between conservation actions and [climate] mitigation objectives’ (Citation2021, p. 20). One exception – depicted in the bottom right quadrant – might be the negative impacts on GHG emissions of ‘ecotourism’, which has been proposed as one type of market-based mechanism for funding conservation efforts (Deutz et al., Citation2020), given that tourism today accounts for around 8% of global emissions (Lenzen et al., Citation2018). Overall, the precise dynamics of potential climate–biodiversity trade-offs and synergies from a financial risk perspective are not well-established and remain in need of further research.

In summary, the interconnected dynamics of climate- and biodiversity-related physical risks together with the interactions between various types of mitigation policies mean that CRFR and BRFR cannot be considered in isolation to each other. Policymakers should be cognisant that the siloed and sequential approach that currently characterises environmental-financial risk assessment may result in ‘blind spots’ and potentially significant underestimations of financial risk exposure.

3. Current financial policy approaches to environmental-financial risks

The most prominent sustainable financial policy initiatives (e.g. BEIS, Citation2019; European Commission, Citation2018) take the position that the measurement and disclosure of environmental-financial risks is itself a means of managing these risks (Chenet et al., Citation2021). This approach is grounded in a ‘market failure’ understanding of environmental threats, which are assumed to result from negative externalities, i.e. the fact that environmental damages are not priced into existing markets (Christophers, Citation2017; Ryan-Collins, Citation2019). According to this perspective, encouraging firms to disclose the risks that environmental threats pose to their own private balance sheets will, through increased awareness of financial materiality, lead to more sustainable resource allocation and mitigate potential sources of financial risk (e.g. TCFD, Citation2017).

This market-led perspective has dominated central bank and financial supervisors’ approaches to managing CRFR in advanced economies (Baer et al., Citation2021; Bailey, Citation2020; Brainard, Citation2021; Schnabel, Citation2020; Weidmann, Citation2021). Risk disclosure and transparency is central to Pillar 3 of the international Basel III regulatory framework and has accordingly become one of the key recommendations of the NGFS with respect to CRFR management (NGFS, Citation2019b). So far, financial authorities seem to be prioritising the same logic in their early explorations of BRFR. For example, Dutch supervisors identified material exposures to BRFR within the Dutch financial sector, yet their recommendations focused on the development of BRFR disclosure and risk modelling frameworks (Van Toor et al., Citation2020). For both climate and non-climate environmental risks, the ECB’s supervisory guidance advises financial institutions to estimate the magnitude of their environmental exposures, using tools such as forward-looking scenario-based risk modelling, and to adapt their operating procedures and risk limits accordingly (ECB, Citation2020). The NGFS Study Group’s recommendations focused on developing risk assessment methodologies and signaling the importance of BRFR to financial institutions under their supervision (NGFS-INSPIRE, Citation2022).

Indeed, a challenge facing financial policymakers is that the conceptual framework for measuring and understanding BRFR is less advanced compared with progress made in climate finance, as summarised in .

Table 1. Frameworks and indicators for understanding and measuring BRFR compared to CRFR.

These emerging policy initiatives are laudable in their ambitions. Yet, market-led approaches to managing environmental-financial risks suffer from several flaws that limit their effectiveness.

First, financial authorities have so far failed to acknowledge that they face a trade-off between knowledge-building and policy action to reduce the materiality of future risks. Whilst it is true that policymakers’ understanding of environmental risks can be improved through more research and that this may enable more effective interventions, it is also true that some biodiversity-related impacts may become financially material within a much shorter time frame than climate-related physical risks – as discussed in Section 2. Comprehensive accounting, reporting, and risk modelling methodologies may take years to become established, by which time some biodiversity-related threats may already be undermining economic and financial stability. The same concern applies to some climate risks that are also becoming increasingly financially material over the nearer term, e.g. Californian wildfires. The slow progress of voluntary climate risk initiatives does not provide encouraging evidence of a favourable outcome from this trade-off. Since the TCFD launched in 2017, climate risk disclosures have yet to materially affect investment decisions for the majority of financial institutions (Ameli et al., Citation2020; Christophers, Citation2019; Hook & Vincent, Citation2020).

Second, biodiversity-related physical risks are arguably even more complex to estimate in financial terms than CRFR (Chenet, Citation2019; Kedward et al., Citation2021a). Unlike climate change, which at its core concerns the effect of anthropogenic GHG emissions on atmospheric temperature increases, biodiversity loss encompasses multiple distinct phenomena, in turn the result of multiple anthropogenic drivers, acting upon different scales – from local ecosystems to the planetary level. Quantitative estimations will hence require multiple indicators to capture progress across various spatial and ecological dimensions, posing extraordinary challenges for financial risk modelling (Chenet et al., Citation2021). Impacts are most directly identifiable at the micro-level: one firm will be both exposed to multiple biodiversity-related threats with differing effects within different local ecosystems and across different points in time. Replicating such granular analysis from asset location to financial portfolio level implies an unmanageable degree of complexity unless very broad and aggregative abstractions are made, which may reduce the reliability, and hence utility, of the exercise as a justification for policy intervention.

Third, biodiversity-related transition risks also face significant uncertainty in terms of identification and measurement. Unlike CO2 emissions, many features of biodiversity and ecosystems cannot be conceptualised as a fungible concept; gains in one location cannot fully offset losses elsewhere via a ‘compensation scheme’. Consequently, there is no obvious carbon price equivalent for biodiversity loss, which complicates the design of ‘transition pathways’ for financial risk modelling. Emerging policy consensus suggests that reversing biodiversity loss will require a mixture of institutional, policy, and regulatory reform at local, national, and global scales (e.g. European Commission, Citation2020; G7 Leaders, Citation2021). Such reforms will be unavoidably political and will vary considerably in implementation across sectors and jurisdictions, raising questions about the feasibility of selecting meaningful transition assumptions for scenario-based risk modelling.

Fourth, even if a sophisticated database of asset-level environmental information could be imagined, financial policymakers should be aware of the inherent limitations of financial risk modelling approaches to generate even broadly accurate estimations of environmental-financial risk exposure at the systemic level due to the presence of complex system dynamics. Both climate and biodiversity transmission channels are interconnected and governed by non-linear processes, such as feedback loops, emergent phenomena, rapid regime shifts, and tipping points (Dasgupta, Citation2021; Lenton, Citation2013; Steffen et al., Citation2018). Importantly, whilst the physical phenomena alone are subject to significant modelling uncertainty, so too are the second- and third-order effects that cascade from interactions with socioeconomic phenomena (Keys et al., Citation2019), such as complex global supply chains and highly interconnected financial networks (Liu et al., Citation2015).

Furthermore, the current trajectories of both climate change and biodiversity loss are unprecedented within recorded human history (Barnosky et al., Citation2011), impeding the calculation of probabilities needed to estimate future outcomes in conventional financial models. For these reasons, environmental-financial risks cannot be easily conceptualised as probabilistic risks, which form the basis of traditional financial models, or even as forward-looking risks that would become precisely measurable through scenario-based risk modelling. Just as with climate change (Chenet et al., Citation2021), biodiversity loss and its socioeconomic consequences are subject to radical uncertainty, where future outcomes are inherently unknowable. No matter the quality of the input information, therefore, scenario-based modelling approaches cannot reliably quantify all of the possible future outcomes resulting from the dynamic interaction of multiple human and environmental variables (Chenet et al., Citation2021; Svartzman et al., Citation2021b).

Central banks and financial supervisors traditionally operate by establishing evidence on the characteristics of particular risks as a prerequisite to formulating policies to manage them. However, financial policymakers should be cognisant that disclosure and reporting initiatives may never obtain sufficiently good data on CRFR and BRFR, whilst quantitative financial risk assessment methods cannot be relied upon to capture all relevant tail risks. Quantitative approaches may be important in exploring environmental-financial risks and raising awareness among financial players, but these limitations mean that alone they are insufficient to ensure the effective risk management. Indeed, the ‘measurement-first’ approach currently favoured by financial authorities may leave them failing to deliver on their primary mandates to protect price and financial stability – if, as is feared, physical risks emerge over the nearer-term. To better manage the trade-off between knowledge-building and policy action, financial policymakers should consider how to assess and manage on the basis of information available today. It is to this question that we now turn.

4. Assessing environmental-financial risks under radical uncertainty

An emerging literature has argued for more considered use of quantitative modelling for assessing CRFR, whereby limitations on estimates of risk are appreciated within the context of radical uncertainty (Chenet et al., Citation2021; Svartzman et al., Citation2021b). These authors called for policymakers to explore nonequilibrium-based methodologies, such as input-output analysis (Cahen-Fourot et al., Citation2019), network-based approaches (Battiston et al., Citation2017), agent-based models (Balint et al., Citation2017), and stock-flow consistent modelling (Dafermos et al., Citation2018), in order to capture some of the financial and non-linear dynamics not usually accounted for in traditional climate-economy models. Chenet et al. (Citation2021) also call for more qualitative means of understanding climate risk, building on indicator-based approaches already used by financial authorities to assess thresholds for the implementation of macroprudential policies (e.g. simple indicators of size, leverage, and institutional interconnectedness).

The extension of these alternate risk assessment methods to BRFR is an important avenue for future research and is even more warranted given its enhanced complexity. For example, policymakers could also focus their quantification efforts on key transmission channels where dynamics and drivers of critical environmental threats – such as ‘tipping points’ (Lenton, Citation2013) – are particularly interlinked with the financial system, complementing these efforts with qualitative assessments to evaluate the degree of potential systemic risk (Svartzman et al., Citation2021b).

Recent studies provide some examples of emerging approaches, including those already mentioned (Svartzman et al., Citation2021a; Van Toor et al., Citation2020). Kedward et al. (Citation2021b) qualitatively assess supply-chain linkages related to deforestation-linked commodities in the ECB’s corporate bond portfolio. Ranger et al. (Citation2021) incorporate compounding risks into macroeconomic scenario analysis, focusing on linkages between climate change and pandemics. Galaz et al. (Citation2018) estimate financial interactions with ecological tipping points, linking large equity exposures to industries modifying critical forest biomes. While not precise measures of financial risk, per say, such approaches can still give financial authorities valuable insights into where physical and transition risk factors may become material.

As mentioned, current financial supervisory approaches consider environmental changes from a financial materiality perspective, i.e. in terms of the impacts environmental threats may have on the balance sheets of firms and financial institutions. More recently, there have been increasing calls for financial policymakers also consider environmental materiality – i.e. the negative environmental impacts that result from certain financing activities (Adams et al., Citation2021; Kedward et al., Citation2021a). Double materiality was first formally proposed by the European Commission (Citation2019) and has since been adopted by the five leading sustainability reporting standards bodies (CDP et al., Citation2020). Building on these developments, we argue that understanding the harmful impacts of finance may help policymakers to better assess environmental-financial risks at a more systemic level and design effective policy on the basis of information available today.

Researchers within central banks exploring BRFR have emphasised that understanding the environmental impacts of finance can contribute to building a comprehensive understanding of potential risks posed to the financial system (Boissinot et al., Citation2022). First, exposure to environmentally-harmful activities may provide an operational proxy for identifying potential climate and biodiversity transition risks. Second, given that one firm’s impact upon the environment may affect other firms’ ability to operate, negative impacts may contribute to the emergence or accumulation of physical risks elsewhere, or at a systemic level.

These arguments are important because they reveal the existence of feedback loops between financial impact and financial risk. Environmental-financial risks are at least in part endogenous because financial institutions facilitate business activities driving climate change and biodiversity loss through their capital allocation choices (Kedward et al., Citation2021a). For BRFR, Svartzman et al. (Citation2021a) and NGFS-INSPIRE (Citation2022) both explore potential ‘biodiversity alignment’ strategies for the financial sector but stop short of suggesting concrete policy actions to directly mitigate biodiversity-harmful finance, citing the need for further research in this area – including, for example, the development of methodologies to quantify the alignment of financial portfolios with biodiversity policy goals.

Yet, given the critical ‘research versus action’ trade-off articulated in the previous section, we go beyond these perspectives to propose that the feedback effects of negative financing impacts do not have to be established in terms of losses to the financial system in order for policymakers to take action. Indeed, as others have argued, evidence of environmental materiality should itself be sufficient evidence for financial actors, including policymakers, to act upon negative impacts associated with financing activities (Galaz et al., Citation2015; Scholtens, Citation2017). This is because the financial system is not just a passive intermediary of capital flows responding only to pricing mechanisms, but it has considerable agency in shaping the direction of economic activity (Campiglio, Citation2016; Ryan-Collins, Citation2019; Schumpeter, Citation1934). In other words, the alignment of financial flows should not just be seen as an implementing mechanism, but a policy objective itself that is necessary to achieve climate and biodiversity goals (Likhtman et al., Citation2022). Whilst the potential for new green financial instruments to mobilise financing for decarbonisation and conservation has attracted much attention (e.g. Deutz et al., Citation2020), financial institutions and policymakers have arguably paid less attention to the concurrent need to define and reduce harmful financing practices (Schreiber et al., Citation2020).

Such an oversight represents a missed opportunity for better understanding sources of CRFR and BRFR. The continued financing of environmentally-harmful activities enables damaging stakeholders, technologies, and infrastructures to retain a persistently dominant position in the economy, thus making the transition to more ecologically-sustainable alternatives more difficult and costly – i.e. ‘lock-in’ effects (Galaz et al., Citation2018; Unruh, Citation2000). Indeed, the Dasgupta Review on the Economics of Biodiversity has noted that ‘existing private financial flows that are adversely affecting the biosphere outstrip those that are enhancing natural assets, and there is a need to identify and reduce financial flows that directly harm and deplete natural assets’ (Dasgupta, Citation2021, p. 474).

A prominent gap in proposed risk assessment approaches for both CRFR and BRFR is a systematic assessment by financial authorities into how financial institutions are financing key activities that drive climate change and biodiversity loss, such as fossil fuels and agriculture. We propose that financial policymakers also complement quantitative risk assessments with measures including the mandatory disclosure of portfolio composition and due diligence procedures related to the financial of identified harmful activities. Whilst existing policy approaches focus on quantifying risks in terms of losses to private balance sheets, we go beyond this to argue that the identification of financial flows to climate- and biodiversity-negative activities is a more precise and measurable exercise to identify drivers of potentially endogenous risks. Additionally, such an approach may be more achievable within the limited timeframes remaining for action, rather than the time-intensive evolution in disclosure and modelling required to fulfil market-led approaches.

5. Discussion: alternative policy trajectories

One implication of the endogeneity of environmental-financial risks is that using financial policy to mitigate financial flows supporting environmentally-harmful activities may be a simpler mechanism by which to manage the emergence of CRFR and BRFR – given the limitations of market-led approaches. Indeed, some have called for the alignment of the private financial system with governments’ Net Zero transition policy as more direct means of mitigating systemic CRFR (Barkawi & Zadek, Citation2021; Robins et al., Citation2021). Others have called for more interventionist financial policy, focused on steering capital away from harmful and towards sustainable activities, that is justified by the need to take precautionary action where the consequences of inaction would be catastrophic and potentially irreversible (Chenet et al., Citation2021; Chenet et al., Citation2022). The potential need to act sooner in order to avoid the worst environmental risks is increasingly acknowledged by some central bankers (e.g. Elderson, Citation2021).

But beyond protecting the financial system from the compounding interactions of climate change and biodiversity loss, there is also a strong case for financial authorities to use their policy toolkits because a climate- and biodiversity-positive transition is unlikely to be achieved without aligning the financial system with environmental targets such as the Paris Agreement and the forthcoming Post-2020 Global Biodiversity Framework. Of course, financial policy is not a panacea; national policy defining a green transition should be led by governments. Yet assessing how capital flows determine human-environment interactions offers the potential to identify ‘sensitive intervention points’ (Farmer et al., Citation2019) or ‘positive tipping points’ (Sharpe & Lenton, Citation2021) where financial policy interventions may stimulate positive feedback loops that accelerate a green economic transition.

One immediate step is for financial policymakers, in coordination with government-led green industrial strategy (Mazzucato, Citation2021), to define harmful business activities that are incompatible with mitigating climate change and reversing biodiversity loss. A combination of approaches could be used to define the list of excluded practices, such as scientific consensus linking the activity to negative impacts, or clear policy direction (e.g. the EU’s Biodiversity Strategy). Policymakers could focus initially on sectors most directly implicated negative drivers of change, such as fossil fuel infrastructure and agriculture, and harmful practices taking place in critical biomes (e.g. coral reefs, rainforest, and tundra) – the loss of which would accelerate tipping points (Mace et al., Citation2014).

Policy developments in the EU give some relevant examples of how this approach could be applied. As well as the ‘do no significant harm’ (DNSH) principle which already features in the Taxonomy Regulation (EU, Citation2020), the EU Platform on Sustainable Finance recently advised that the Taxonomy should be extended to classify harmful activities including those that are ‘always significantly harmful’ and ‘where urgent, managed exit/decommissioning is required’ (European Commission, Citation2022, p. 8) – suggesting activities such as thermal coal mining and peat extraction, for climate mitigation, and the destruction of high biodiversity-value ecosystems, for environmental protection.

A taxonomy might have the advantage of being a more systematic approach of designating harmful activities in relation to green alternatives, but the EU’s Taxonomy experience has not been without controversy – criticised especially for bowing down to vested interests (Schreiber et al., Citation2020; Rauhala, Citation2022). A faster and potentially less politically-contested alternative could be for public bodies to use their discretion to designate priority harmful activities based on scientific consensus. One proposal has called for new institutional configurations (e.g. a ‘Green Finance Action Taskforce’) to formalise the coordination required between central banks, financial supervisors, and government departments for finance, industrial policy, and the environment (Dafermos et al., Citation2021).

Once harmful activities are democratically defined, financial policies can then be targeted to influence capital reallocation. For instance, assets linked to harmful activities could also be excluded from collateral operations and monetary policy operations (Jourdan & Kalinowski, Citation2019) and micro- and macroprudential tools could be used to disincentivise or restrict harmful financing (D’Orazio & Popoyan, Citation2019), such as through levying punitive capital requirements (Philipponnat, Citation2020). Indeed, the use of macroprudential tools is especially warranted by the fact that harmful financing contributes endogenously to the build-up of systemic macrofinancial risk – as explored in Section 4.

Financial authorities could also explore using credit guidance tools to directly prohibit certain forms of financing (Kedward et al., Citation2022). Such quantity-based mechanisms may be more effective than price-based approaches in managing the non-linearities associated with tipping points (Dasgupta, Citation2021). Regardless of the chosen policy tools, the onus of proof should be on the financial institution to demonstrate that they are not facilitating designated environmentally-harmful activities – a requirement that can help to strengthen due diligence and risk management procedures across the financial sector.

Central banks and supervisors can build on the fact that many financial institutions already define excluded practices within sector-specific ESG investment criteria. In practice, these voluntary exclusion policies are inconsistent across firms and often not ambitious enough to materially shift capital allocation (Crona et al., Citation2021; Thomson, Citation2020), and could potentially be improved by integration into financial supervision. Targeted interventions are also not without precedent within central banks. For example, the Brazilian central bank restricted rural credit in the Amazon to firms compliant with environmental regulations under Resolution 3545 in 2008, resulting in a material reduction in deforestation between 2003 and 2011 (Assunção et al., Citation2020). Investigating the environmental outcomes of other quantity-based central bank interventions – such as those featured in Dikau and Ryan-Collins (Citation2017) – would be a worthy avenue for future research.

The use of financial policy to directly steer finance presents some trade-offs for policymakers to consider. In particular, the implementation of the policies proposed above may crystallise the emergence of transition risks in certain sectors. We suggest that this challenge could be managed by ensuring that financial policy on environmental risk is deployed in coordination with relevant government departments, as part of a broader packet of industrial policy measures to alleviate the economic dislocations associated with transitioning sectors. Additionally, financial policy could be deployed on an escalating basis – with ‘forward guidance’ clearly communicating to financial institutions when policy will be tightened in line with the environmental transition. As part of this, financial policymakers should also require financial institutions to publish their own transition plans for climate and biodiversity, as some have already started to do, and report their progress on meeting timelines for reducing environmentally-harmful financing activities – as has been introduced in France.Footnote6

A second challenge concerns the political acceptability of coordinated financial policy interventions within current institutional paradigms, which presently emphasise central bank independence. As highlighted above, active coordination with broader government departments will be essential to ensure the efficacy as well as democratic legitimacy of the proposed policy interventions. However, such collaboration is hardly novel. Since the 2008 financial crisis and 2020 pandemic, central banks have increasingly put aside notions of market neutrality to deliver stimulus to targeted parts of the economy – often in direct collaboration with treasury departments (Cavallino & De Fiore, Citation2020). Furthermore, a recent systematic analysis of 135 central bank mandates showed that over 50% have a mandate to support government policy objectives on sustainable development (Dikau & Volz, Citation2021). Ultimately, central bank mandates are always interpreted and reflect what is politically acceptable at the time. The limitations of market-led approaches outlined in this paper would suggest that an institutional shift from ‘prudential’ to ‘promotional’ policy approaches (Baer et al., Citation2021) is necessary for central banks to deliver on their primary mandates.

Finally, central banks and financial supervisors may be faced with the prospect of being unable to proceed with the policy approach outlined here if their national governments are not willing to take the lead in designing long-term industrial strategy for a green transition. This is especially a risk for BRFR, where biodiversity policy remains in its infancy and lags far behind the Net Zero emissions commitments made by various nations. As has been argued for climate change, a role that financial authorities should consider in this scenario is to actively lobby governments to take action due to the implications on systemic macrofinancial risks (Svartzman et al., Citation2021a).Footnote7 Given that the financial risks of environmental threats escalate the longer that mitigation action is delayed, such a lobbying role for the central bank should be understood as an integral part of taking precautionary action to deliver on its primary mandates of preserving price and financial stability.

6. Conclusion

Financial authorities are beginning to recognise the importance of environmental risks beyond climate change to their financial and price stability mandates. As with CRFR, emerging policy initiatives for BRFR have cited a need for new disclosure frameworks, quantitative risk modelling methodologies, and more research on financial materiality as a prerequisite to further policy interventions (e.g. NGFS-INSPIRE, Citation2022).

This paper explored the limitations of the ‘measure in order to manage’ approach that currently dominates climate finance policy. We proposed alternate options for policymakers to both assess and manage CRFR and BRFR on the basis of information available today, emphasising the importance of identifying and reducing flows of finance that are facilitating the persistence of environmentally-harmful economic activities, that contribute to climate and biosphere tipping points.

Nevertheless, it is true that critical research gaps remain. First, the interconnections between BRFR and CRFR remain underexplored; there is a particular need to understand how trade-offs and synergies between climate and biodiversity solutions will affect transition risks. In particular, identifying climate mitigation and biodiversity protection synergies could then enable central banks to use their policy toolkits to incentivise and steer finance to these activities. Second, future developments in risk modelling should focus on accounting for climate–biodiversity risk interactions into the environment-economy models that underpin supervisory risk assessment processes. Quantitative approaches should also focus on quantifying key risk transmission channels, such as potential ecological tipping points. Finally, financial policymakers should conduct a systematic assessment into how financial institutions are financing key sectors implicated in driving climate change and biodiversity loss, in order to inform the design of policy instruments to reduce such activities.

Acknowledgements

The authors are grateful to the Editor and three anonymous referees for suggestions to improve the paper. The research received financial support from Partners for a New Economy, the Laudes Foundation and INSPIRE. Chenet acknowledges the support of the Chair Energy and Prosperity, under the aegis of the Fondation du Risque.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 In line with the emerging terminology in this field (e.g, NGFS-INSPIb122RE, Citation2022), we refer to the more precise terms of biodiversity and ecosystems, rather than ‘nature’ – which is less specific conceptually, but is used by some to encompass biodiversity and/or the environment.

2 Comments at the IUCN Congress in Marseille, 4th September 2021, and posted on Lagarde’s official Twitter: https://twitter.com/Lagarde/status/1434170468525871109?s=20&t=gmNm-G5yVWD9b2tUX3-7bQ

3 Indeed, the term ‘biodiversity loss’ is mentioned in the main body of the report’s text only six times, and ‘ecosystem services’ only twice.

4 For a review of emerging biodiversity-economy models, see NGFS-INSPIRE (Citation2022) and Svartzman et al. (Citation2021a).

5 Scientific studies relating to the conservation/climate mitigation interconnections of the other examples in this Table are summarised in the Supplementary Information.

6 See Article 29 of the French Energy and Climate Act: https://www.tresor.economie.gouv.fr/Articles/80af1116-2fcd-47d0-ad1d-ea24352e6295/files/273f9026-bbc4-4fc2-ba60-f86f6fe16c1f

7 The Bank of England is reported to have lobbied the UK Treasury to ‘green’ its monetary policy remit (Giles & Binham, Citation2021).

References

- Adams, C. A., Alhamood, A., He, X., Tian, J., Wang, L., & Wang, Y. (2021). The double-materiality concept: Application and issues [online]. Global Reporting Initiative. https://researchbank.swinburne.edu.au/items/23c31bbe-27c4-43e9-9422-d6b5f2dfcde9/1/

- Alogoskoufis, S., Dunz, N., Emambakhsh, T., Hennig, T., Kaijser, M., Kouratzoglou, C., Muñoz, M. A., Parisi, L., & Salleo, C. (2021). ECB economy-wide climate stress test: Methodology and results [online]. European Central Bank. https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op281~05a7735b1c.en.pdf

- Ameli, N., Drummond, P., Bisaro, A., Grubb, M., & Chenet, H. (2020). Climate finance and disclosure for institutional investors: Why transparency is not enough. Climatic Change, (160), 565–589.

- Assunção, J., Gandour, C., Rocha, R., & Rocha, R. (2020). The effect of rural credit on deforestation: Evidence from the Brazilian Amazon. The Economic Journal, 130(626), 290–330. https://doi.org/10.1093/ej/uez060

- Baer, M., Campiglio, E., & Deyris, J. (2021). It takes two to dance: Institutional dynamics and climate-related financial policies [online]. Grantham Research Institute on Climate Change and the Environment. https://www.lse.ac.uk/granthaminstitute/wp-content/uploads/2021/04/working-paper-356-Baer-et-al.pdf

- Bailey, A. (2020). The time to push ahead on tackling climate change. https://www.bankofengland.co.uk/speech/2020/andrew-bailey-speech-corporation-of-london-green-horizon-summit

- Balint, T., Lamperti, F., Mandel, A., Napoletano, M., Roventini, A., & Sapio, A. (2017). Complexity and the economics of climate change: A survey and a look forward. Ecological Economics, 138, 252–265. https://doi.org/10.1016/j.ecolecon.2017.03.032

- Bank of England. (2017). The bank of England’s response to climate change [online]. https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2017/the-banks-response-to-climate-change.pdf?la=en&hash=7DF676C781E5FAEE994C2A210A6B9EEE44879387

- Bank of England. (2021a). Key elements of the 2021 biennial exploratory scenario: Financial risks from climate change [online]. London: Bank of England. https://www.bankofengland.co.uk/stress-testing/2021/key-elements-2021-biennial-exploratory-scenario-financial-risks-climate-change

- Bank of England. (2021b). Options for greening the bank of England’s corporate bond purchase scheme [online]. https://www.bankofengland.co.uk/-/media/boe/files/paper/2021/options-for-greening-the-bank-of-englands-corporate-bond-purchase-scheme-discussion-paper.pdf?la=en&hash=9BEA669AD3EC4B12D000B30078E4BE8ABD2CC5C1

- Barkawi, A., & Zadek, S. (2021). Governing finance for sustainable prosperity [online]. Council on Economic Policies. https://www.cepweb.org/wp-content/uploads/2021/04/Barkawi-and-Zadek-2021.-Governing-Finance-for-Sustainable-Prosperity.pdf

- Barnosky, A. D., Matzke, N., Tomiya, S., Wogan, G. O. U., Swartz, B., Quental, T. B., Marshall, C., McGuire, J. L., Lindsey, E. L., Maguire, K. C., Mersey, B., & Ferrer, E. A. (2011). Has the earth’s sixth mass extinction already arrived? Nature, 471(7336), 51–57. https://doi.org/10.1038/nature09678

- Bassen, A., Busch, T., Lopatta, K., Evans, E., & Opoku, O. (2019). Nature risks equal financial risks: A systematic literature review [online]. University of Hamburg. https://d2ouvy59p0dg6k.cloudfront.net/downloads/nature_risks_equal_financial_risks_rg_sustainable_finance_hamburg_2019_final.pdf

- Battiston, S., Mandel, A., Monasterolo, I., Schütze, F., & Visentin, G. (2017). A climate stress-test of the financial system. Nature Climate Change, 7(4), 283. https://doi.org/10.1038/nclimate3255

- BEIS. (2019). Green finance strategy: Transforming finance for a greener future [online]. HM Government. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/813656/190701_BEIS_Green_Finance_Strategy_Accessible_PDF_FINAL.pdf

- Boissinot, J., Goulard, S., Le Calvar, E., Salin, M., Svartzman, R., & Weber, P.-F. (2022). Aligning financial and monetary policies with the concept of double materiality: Rationales, proposals and challenges [online]. LSE Grantham Research Institute on Climate Change and the Environment. [Accessed 30 June 2022]. https://inspiregreenfinance.org

- Bolton, P., Després, M., Pereira da Silva, L., Samama, F., & Svartzman, R. (2020). The green swan: Central banking and financial stability in the age of climate change [online]. Bank for International Settlements. https://www.bis.org/publ/othp31.pdf

- Brainard, L. (2021). The role of financial institutions in tackling the challenges of climate change. New York: Federal Reserve Board. https://www.federalreserve.gov/newsevents/speech/brainard20210218a.htm

- Cahen-Fourot, L., Campiglio, E., Dawkins, E., Godin, A., & Kemp-Benedict, E. (2019). Capital stranding cascades: The impact of decarbonisation on productive asset utilisation [online]. WU Vienna University of Economics and Business. https://ideas.repec.org/p/wiw/wus045/6854.html

- Caldecott, B., Howarth, N., & McSharry, P. (2013). Stranded assets in agriculture: Protecting value from environment-related risks [online]. Oxford Smith School of Enterprise and the Environment. https://www.smithschool.ox.ac.uk/publications/reports/stranded-assets-agriculture-report-final.pdf

- Calice, P., Diaz Kalan, F., & Miguel, F. (2021). Nature-Related financial risks in Brazil [online]. World Bank. https://documents1.worldbank.org/curated/en/105041629893776228/pdf/Nature-Related-Financial-Risks-in-Brazil.pdf

- Campiglio, E. (2016). Beyond carbon pricing: The role of banking and monetary policy in financing the transition to a low-carbon economy. Ecological Economics, 121, 220–230. https://doi.org/10.1016/j.ecolecon.2015.03.020

- Cavallino, P., & De Fiore, F. (2020). Central banks’ response to COVID-19 in advanced economies [online]. Bank for International Settlements. https://www.bis.org/publ/bisbull21.pdf

- CBD. (2021). First draft of the new post-2020 global biodiversity framework [online]. Convention on Biological Diversity. https://www.cbd.int/article/draft-1-global-biodiversity-framework

- CDP, CDSB, GRI, IIRC and SASB. (2020). Reporting on enterprise value: Illustrated with a prototype climate-related financial disclosure standard [online]. Impact Management Project. https://29kjwb3armds2g3gi4lq2sx1-wpengine.netdna-ssl.com/wp-content/uploads/Reporting-on-enterprise-value_climate-prototype_Dec20.pdf

- Chenet, H. (2019). Planetary health and the global financial system. Rockefeller Foundation Economic Council on Planetary Health.

- Chenet, H., Kedward, K., Ryan-Collins, J., & van Lerven, F. (2022). Developing a precautionary approach to financial policy – from climate to biodiversity [online]. LSE Grantham Research Institute on Climate Change and the Environment. [Accessed 22 June 2022]. https://www.lse.ac.uk/granthaminstitute/publication/developing-a-precautionary-approach-to-financial-policy-from-climate-to-biodiversity/

- Chenet, H., Ryan-Collins, J., & Lerven, F. v. (2021). Finance, climate-change and radical uncertainty: Towards a precautionary approach to financial policy. Ecological Economics, 183, 106957. https://doi.org/10.1016/j.ecolecon.2021.106957

- Christophers, B. (2017). Climate change and financial instability: Risk disclosure and the problematics of neoliberal governance. Annals of the American Association of Geographers, 107(5), 1108–1127. https://doi.org/10.1080/24694452.2017.1293502

- Christophers, B. (2019). Environmental beta or How institutional investors think about climate change and fossil fuel risk. Annals of the American Association of Geographers, 109(3), 754–774. https://doi.org/10.1080/24694452.2018.1489213

- Crona, B., Folke, C., & Galaz, V. (2021). The anthropocene reality of financial risk. One Earth, 4(5), 618–628. https://doi.org/10.1016/j.oneear.2021.04.016

- Dafermos, Y., Gabor, D., Nikolaidi, M., & van Lerven, F. (2021). Greening the UK financial system – a fit for purpose approach [online]. SUERF The European Money and Finance Forum. Available from: https://www.suerf.org/docx/f_55c6017b10a9755ef3681b09ccb01e94_21233_suerf.pdf

- Dafermos, Y., Nikolaidi, M., & Galanis, G. (2018). Climate change, financial stability and monetary policy. Ecological Economics, 152, 219–234. https://doi.org/10.1016/j.ecolecon.2018.05.011

- Dasgupta, P. (2021). The economics of biodiversity: The dasgupta review [online]. London: HM Treasury https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/962785/The_Economics_of_Biodiversity_The_Dasgupta_Review_Full_Report.pdf

- Deutz, A., Heal, G., Niu, R., & Swanson, E. (2020). Financing nature: Closing the global biodiversity financing gap [online]. The Paulson Institute, The Nature Conservancy, and the Cornell Atkinson Center for Sustainability. https://www.paulsoninstitute.org/wp-content/uploads/2020/10/FINANCING-NATURE_Full-Report_Final-with-endorsements_101420.pdf

- Dikau, S., & Ryan-Collins, J. (2017). Green central banking in emerging market and developing country economies [online]. New Economics Foundation. https://eprints.soas.ac.uk/24876/1/Green-Central-Banking.pdf

- Dikau, S., & Volz, U. (2021). Central bank mandates, sustainability objectives and the promotion of green finance. Ecological Economics, 184, 107022. https://doi.org/10.1016/j.ecolecon.2021.107022

- Dixon, C. (2020). Aligning development finance with nature’s needs: Protecting nature’s development dividend [online]. Finance for Biodiversity Initiative. https://a1be08a4-d8fb-4c22-9e4a-2b2f4cb7e41d.filesusr.com/ugd/643e85_332117f2a1494bbe90a42835c99963b8.pdf

- D’Orazio, P. (2021). Towards a post-pandemic policy framework to manage climate-related financial risks and resilience. Climate Policy, 21(10), 1368–1382. https://doi.org/10.1080/14693062.2021.1975623

- D’Orazio, P., & Popoyan, L. (2019). Fostering green investments and tackling climate-related financial risks: Which role for macroprudential policies? Ecological Economics, 160, 25–37. https://doi.org/10.1016/j.ecolecon.2019.01.029

- ECB. (2020). Guide on climate-related and environmental risks - supervisory expectations relating to risk management and disclosure [online]. Frankfurt am Main. Available from: https://www.bankingsupervision.europa.eu/ecb/pub/pdf/ssm.202011finalguideonclimate-relatedandenvironmentalrisks~58213f6564.en.pdf

- ECB. (2021). ECB presents action plan to include climate change considerations in its monetary policy strategy. Press Release. [online]. https://www.ecb.europa.eu/press/pr/date/2021/html/ecb.pr210708_1~f104919225.en.html

- Elderson, F. (2021). Patchy data is a good start: From kuznets and clark to supervisors and climate (policy brief No. 152). SUERF: The European Money and Finance Forum. https://www.suerf.org/suer-policy-brief/30261/patchy-data-is-a-good-start-from-kuznets-zu

- European Commission. (2018). Action plan: Financing sustainable growth [online]. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52018DC0097&from=EN

- European Commission. (2019). Guidelines on reporting climate-related information [online]. Brussels. https://ec.europa.eu/finance/docs/policy/190618-climate-related-information-reporting-guidelines_en.pdf

- European Commission. (2020). EU biodiversity strategy for 2030 bringing nature back into our lives [online]. https://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1590574123338&uri=CELEX:52020DC0380

- European Commission. (2021a). Proposal for a regulation on deforestation-free products [online]. Brussels: European Commission. https://ec.europa.eu/environment/publications/proposal-regulation-deforestation-free-products_en

- European Commission. (2021b). Draft report by the platform on sustainable finance on preliminary recommendations for technical screening criteria for the EU taxonomy [online]. Brussels: European Commission. https://ec.europa.eu/info/publications/210803-sustainable-finance-platform-technical-screening-criteria-taxonomy-report_en

- European Commission. (2022). Platform on Sustainable Finance's report on environmental transition taxonomy [Online]. Brussels: European Commission.

- Farmer, J. D., Hepburn, C., Ives, M. C., Hale, T., Wetzer, T., Mealy, P., Rafaty, R., Srivastav, S., & Way, R. (2019). Sensitive intervention points in the post-carbon transition. Science, 364(6436), 132. https://doi.org/10.1126/science.aaw7287

- Finance for Biodiversity. (2021). Finance and biodiversity: Overview of initiatives for financial institutions [online]. https://www.financeforbiodiversity.org/wp-content/uploads/Finance_and_Biodiversity_Overview_of_Initiatives_April2021.pdf

- G7 Leaders. (2021). G7 2030 nature compact [online]. Group of Seven. https://www.consilium.europa.eu/media/50363/g7-2030-nature-compact-pdf-120kb-4-pages-1.pdf

- Galaz, V., Crona, B., Dauriach, A., Scholtens, B., & Steffen, W. (2018). Finance and the earth system – exploring the links between financial actors and non-linear changes in the climate system. Global Environmental Change, 53, 296–302. https://doi.org/10.1016/j.gloenvcha.2018.09.008

- Galaz, V., Gars, J., Moberg, F., Nykvist, B., & Repinski, C. (2015). Why ecologists should care about financial markets. Trends in Ecology & Evolution, 30(10), 571–580. https://doi.org/10.1016/j.tree.2015.06.015

- Garibaldi, L. A., Aizen, M. A., Klein, A. M., Cunningham, S. A., & Harder, L. D. (2011). Global growth and stability of agricultural yield decrease with pollinator dependence. Proceedings of the National Academy of Sciences, 108(14), 5909. https://doi.org/10.1073/pnas.1012431108

- Ghersi, F., Hourcade, J.-C., Lefèvre, J., Tankov, P., & Voisin, S. (2021). Integrated economy-climate models and their uses for decision-making [online]. Institut Louis Bachelier. https://www.institutlouisbachelier.org/wp-content/uploads/2021/09/ilb-opinions-debats-n23.pdf

- Giles, C., & Binham, C. (2021). Problems mount for Bank of England governor after weathering Covid storm. Financial Times. 15th March 2021.

- Global Canopy. (2022). Cutting deforestation from Our pensions [online]. https://globalcanopy.org/press/300-billion-of-uk-pension-money-invested-in-companies-linked-to-deforestation

- Hansen, L. P. (2022). Central banking challenges posed by uncertain climate change and natural disasters. Journal of Monetary Economics, 125, 1–15. https://doi.org/10.1016/j.jmoneco.2021.09.010

- Herweijer, C., Evison, W., Mariam, S., Khatri, A., Albani, M., Semov, A., & Long, E. (2020). Nature risk rising: Why the crisis engulfing nature matters for business and the economy [online]. World Economic Forum and PwC. http://www3.weforum.org/docs/WEF_New_Nature_Economy_Report_2020.pdf

- Hof, C., Voskamp, A., Biber, M. F., Böhning-Gaese, K., Engelhardt, E. K., Niamir, A., Willis, S. G., & Hickler, T. (2018). Bioenergy cropland expansion may offset positive effects of climate change mitigation for global vertebrate diversity. Proceedings of the National Academy of Sciences, 115(52), 13294-13299. https://doi.org/10.1073/pnas.1807745115

- Hook, L., & Vincent, M. (2020). Green business reporting rules at risk of pale response. Financial Times [online]. https://www.ft.com/content/ad01f2c9-9eb0-4db6-9898-220c688d16c2

- Immerzeel, D. J., Verweij, P. A., van der Hilst, F., & Faaij, A. P. C. (2014). Biodiversity impacts of bioenergy crop production: A state-of-the-art review. GCB Bioenergy, 6(3), 183–209. https://doi.org/10.1111/gcbb.12067

- IPBES. (2016). Summary for policymakers of the assessment report of the intergovernmental science-policy platform on biodiversity and ecosystem services on pollinators, pollination and food production [online]. Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES). https://doi.org/10.5281/zenodo.2616458

- IPBES. (2019). The global assessment report on biodiversity and ecosystem services: Summary for policymakers [online]. Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES). https://ipbes.net/sites/default/files/2020-02/ipbes_global_assessment_report_summary_for_policymakers_en.pdf

- IPBES and IPCC. (2021). IPBES-IPCC co-sponsored workshop report on biodiversity and climate change [online]. Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) and Intergovernmental Panel on Climate Change (IPCC). https://ipbes.net/sites/default/files/2021-06/20210609_workshop_report_embargo_3pm_CEST_10_june_0.pdf

- Jourdan, S., & Kalinowski, W. (2019). Aligning monetary policy with the EU’s climate targets [online]. https://www.veblen-institute.org/IMG/pdf/aligning_monetary_policy_with_eu_s_climate_targets.pdf

- Kedward, K., Buller, A., & Ryan-Collins, J. (2021b). Quantitative easing and nature loss [online]. London: UCL Institute for Innovation and Public Purpose (IIPP). https://www.ucl.ac.uk/bartlett/public-purpose/publications/2021/jul/quantitative-easing-and-nature-loss

- Kedward, K., Gabor, D., & Ryan-Collins, J. (2022). Aligning finance with the green transition: From a risk-based- to allocative green credit policy regime. UCL Institute for Innovation and Public Purpose (IIPP), Working Paper No. 2022(11). https://www.ucl.ac.uk/bartlett/public-purpose/publications/2022/jul/aligning-finance-green-transition

- Kedward, K., Ryan-Collins, J., & Chenet, H. (2021a). Understanding the financial risks of nature loss: Exploring policy options for financial authorities. SUERF: The European Money and Finance Forum.

- Keys, P. W., Galaz, V., Dyer, M., Matthews, N., Folke, C., Nyström, M., & Cornell, S. E. (2019). Anthropocene risk. Nature Sustainability, 2(8), 667–673. https://doi.org/10.1038/s41893-019-0327-x

- Lade, S. J., Steffen, W., de Vries, W., Carpenter, S. R., Donges, J. F., Gerten, D., Hoff, H., Newbold, T., Richardson, K., & Rockström, J. (2020). Human impacts on planetary boundaries amplified by earth system interactions. Nature Sustainability, 3(2), 119–128. https://doi.org/10.1038/s41893-019-0454-4

- Lenton, T. M. (2013). Environmental tipping points. Annual Review of Environment and Resources, 38(1), 1–29. https://doi.org/10.1146/annurev-environ-102511-084654

- Lenzen, M., Sun, Y.-Y., Faturay, F., Ting, Y.-P., Geschke, A., & Malik, A. (2018). The carbon footprint of global tourism. Nature Climate Change, 8(6), 522–528. https://doi.org/10.1038/s41558-018-0141-x

- Likhtman, S., Isciel, E., O’Malley, T., & Reesink, M. (2022). Aligning financial flows with biodiversity goals and targets [online]. Finance for Biodiversity Initiative. https://www.financeforbiodiversity.org/wp-content/uploads/Finance-for-Biodiversity-Foundation-Paper_Financial_Flows_16Feb2022.pdf

- Liu, J., Hull, V., Luo, J., Yang, W., & Wei, L. (2015). Multiple telecouplings and their complex interrelationships. Ecology and Society, 2(3), 44. https://doi.org/10.5751/ES-07868-200344

- Lovejoy, T., & Nobre, C. (2019). Amazon tipping point: Last chance for action. Science Advances, 5(12), eaba2949–eaba2949. https://doi.org/10.1126/sciadv.aba2949

- Mace, G. M., Barrett, M., Burgess, N. D., Cornell, S. E., Freeman, R., Grooten, M., & Purvis, A. (2018). Aiming higher to bend the curve of biodiversity loss. Nature Sustainability, 1(9), 448–451. https://doi.org/10.1038/s41893-018-0130-0

- Mace, G. M., Reyers, B., Alkemade, R., Biggs, R., Chapin, F. S., Cornell, S. E., Díaz, S., Jennings, S., Leadley, P., Mumby, P. J., Purvis, A., Scholes, R. J., Seddon, A. W. R., Solan, M., Steffen, W., & Woodward, G. (2014). Approaches to defining a planetary boundary for biodiversity. Global Environmental Change, 28, 289–297. https://doi.org/10.1016/j.gloenvcha.2014.07.009

- Mazzucato, M. (2021). Mission economy: A moonshot guide to changing capitalism. Penguin UK.

- NGFS. (2019a). A call for action: Climate change as a source of financial risk [online]. Network for Greening the Financial System. https://www.banque-france.fr/sites/default/files/media/2019/04/17/ngfs_first_comprehensive_report_-_17042019_0.pdf

- NGFS. (2019b). A call for action: Climate change as a source of financial risk [online]. Network for Greening the Financial System. https://www.banque-france.fr/sites/default/files/media/2019/04/17/ngfs_first_comprehensive_report_-_17042019_0.pdf

- NGFS. (2020a). Guide for supervisors: Integrating climate-related and environmental risks into prudential supervision [online]. Network for Greening the Financial System. https://www.ngfs.net/sites/default/files/medias/documents/ngfs_guide_for_supervisors.pdf

- NGFS. (2020b). Guide to climate scenario analysis for central banks and supervisors [online]. Network for Greening the Financial System. https://www.ngfs.net/sites/default/files/medias/documents/ngfs_guide_scenario_analysis_final.pdf

- NGFS. (2020c). Overview of environmental risk analysis by financial institutions [online]. Network for Greening the Financial System. https://www.ngfs.net/sites/default/files/medias/documents/overview_of_environmental_risk_analysis_by_financial_institutions.pdf

- NGFS. (2021a). Adapting central bank operations to a hotter world: Reviewing some options [online]. Network for Greening the Financial System. https://www.ngfs.net/sites/default/files/media/2021/06/17/ngfs_monetary_policy_operations_final.pdf

- NGFS and INSPIRE. (2021). Biodiversity and financial stability: Building the case for action. Study group interim report [online]. Network for Greening the Financial System. https://www.ngfs.net/sites/default/files/medias/documents/biodiversity_and_financial_stablity_building_the_case_for_action.pdf

- NGFS and INSPIRE. (2022). Central banking and supervision in the biosphere: An agenda for action on biodiversity loss, financial risk and system stability. Final Report of the NGFS-INSPIRE Study Group on Biodiversity and Financial Stability.

- OECD. (2019). Biodiversity: Finance and the economic and business case for action [online]. OECD. https://www.oecd.org/env/resources/biodiversity/biodiversity-finance-and-the-economic-and-business-case-for-action.htm

- Philipponnat, T. (2020). Breaking the climate-finance doom loop [online]. Finance Watch. https://www.finance-watch.org/wp-content/uploads/2020/06/Breaking-the-climate-finance-doom-loop_Finance-Watch-report.pdf