Abstract

Companies increasingly work in a global context and need to be relevant in it. In addition to focus on customers, companies need to identify and attend to the needs of various stakeholders. The quality principle of customer focus has been used for identifying stakeholders, their needs and how to manage them. The Planetary Boundaries, the UN Sustainable Development Goals and The Natural Step have been used to identify performance targets for stakeholder needs. Results indicate that People and Planet could be defined as the main stakeholders and that these stakeholders could be further detailed in order to more easily link them with company business. Critical Planet stakeholders could be such as the Atmosphere and Biosphere. Based on the Pareto principle, People needs focus should be on alleviating poverty with a highest priority given to those living in extreme poverty. Absolute and relative indicators for sustainability performance with focus on core stakeholders have been proposed. The indication is that a paradigm shift from Profit to Planet and People focus is needed. The proposed strategy is to combine customer wants focus with a focus on defined critical stakeholder needs.

Introduction

Companies increasingly work in a global context and need to be relevant in it. Apart from customer focus, companies need to identify and attend to the needs of a variety of stakeholders. When studying sustainability reports there is frequently a strong focus on Profit (Isaksson, Citation2018). The Profit dimension in the Triple Bottom Line seems in most cases to be interpreted as standard financial performance. In the Global Reporting Initiative standards the main indicator for Profit is the sales value (GRI-201, Citation2016). Under social indicators in GRI, there are two standards, 416 Customer Health and Safety and 418, Customer Privacy that identify some customer needs (https://www.globalreporting.org/standards/). However, generally in the GRI standards there is almost nothing indicating any focus on customer value. This indicates that customer needs play a minor role in sustainability reporting.

Targets in current sustainability reporting seem often to have internal references and are more seldom linked to external global limits (Haffar & Searcy, Citation2017). There seems to be limited focus on true sustainability – a state where systems can continue to exist without any deterioration as described e.g. by the The Natural Step (TNS) (Robèrt, Citation2000). The four system conditions for sustainability are described as: In order for society to be sustainable, nature’s functions and diversity are not systematically subject to:

I. increasing concentrations of substances extracted from the Earth’s crust;

II. increasing concentrations of substances produced by society;

III. physical impoverishment by over-harvesting or other forms of ecosystem manipulation; and

IV. resources are used fairly and efficiently in order to meet basic human needs worldwide.

The TNS definition is compatible with ideas of the circular economy and the cradle-to-cradle concept. With humanity consuming the production of 1.7 planets per year (https://www.footprintnetwork.org) and with important planetary boundaries being transgressed (Steffen et al., Citation2015) the pressure for change is there. Focus on true sustainability might require a paradigm shift from focus on Profit to focus on People and Planet. Such a change of focus would require important changes in what Business Excellence is and how it is managed. Quality and Sustainability should be merged.

Deming defined quality as: ‘Quality should be aimed at the needs of the customer, present and future’ (Bergman & Klefsjö, Citation2010, p. 22). This focus on needs in quality could be translated to stakeholder needs in sustainability. In both customer and stakeholder focus there are multiple challenges in defining who the customers/stakeholders are and what their wants and needs are.

This conceptual paper discusses how we could identify main global stakeholders and their needs and how this could help in managing sustainability. Generally, the issue is to discuss the need for a paradigm shift from Profit focus to focus on People and Planet and what the consequences for companies would be. More specifically the following issues will be discussed:

Globally, who are the key stakeholders to focus on in a sustainability context?

Which are the prioritised needs of the key stakeholders identified?

How could sustainability performance, with focus on key stakeholder needs, be measured?

How could performance targets, for key stakeholder needs, be set?

Which are the consequences for maintaining the company license to operate with a paradigm shift from Profit focus to People and Planet focus?

Methodology

The principle of Customer Focus has been used as a starting point and its usability for stakeholder needs focus has been discussed. For identifying main customer needs the Pareto principle, or the 80:20 rule indicating that out of a total number of problems roughly 20% explain 80% of the consequences, has been used.

The priorities for the identified key stakeholders have been set using input from the 17 UN Sustainable Development Goals (SDGs) (https://sustainabledevelopment.un.org/sdgs) and the Planetary Boundaries framework (Rockström et al., Citation2009; Steffen et al., Citation2015).

Sustainability performance is viewed using both absolute and relative indicators. Performance targets for 2030 are set based on the needs of the global system as defined by the SDGs and the Planetary Boundaries following the logic of needs based externally set targets. For addressing climate change the Carbon Law is used (Rockström et al., Citation2017). The Carbon Law presents a credible and unbiased view on the changes needed to achieve the goals of the 2015 Paris Agreement of limiting global warming from pre-industrial times to less than 2°C. Long-range targets are set based on the principles in The Natural Step (Robèrt, Citation2000) that presents a definition for true sustainability. Additionally the logic of Backcasting is applied, which means that goals are set based on true sustainability requirements and not based on forecasting from the current situation (Robèrt, Citation2000).

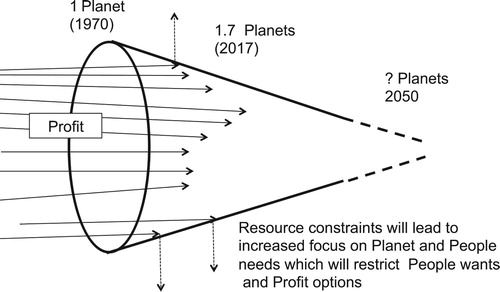

The consequences of the paradigm shift for companies are discussed using an adaptation of the funnel metaphor from The Natural Step (Robèrt, Citation2000). This metaphor describes how company operations are being increasingly restricted by Planet and People needs, see .

Results

The results section is divided into five parts, with headlines corresponding to the research questions.

(1) Who are the global key stakeholders?

In Total Quality Management (TQM), which theoretically constitutes the foundation of Business Excellence Models, customer focus, is a core principle (Bergman & Klefsjö, Citation2010). The underlying belief is that satisfying customers will boost business. Customers are those we produce value for. In a world living over its resources, other stakeholders are requiring attention. Here, stakeholders are viewed as all those that are affected or can affect the company such as customers, potential customers, future customers, authorities, employees, financers, other organisations, nature, people now and in the future. The principle of customer focus could seemingly be converted into stakeholder focus by extending the customer definition. Customers are those that value is created for. In a parallel with customer focus the assumption is that company success in a resource-restricted world is based on creating stakeholder satisfaction. Defining key stakeholders is therefore the first thing to do. In Quality Management focus is on the customer with a particular focus on the paying customer. Here, both wants and needs have to be respected. Customers might occasionally want things that they do not need. An example of this could be a patient wanting to continue life as usual, but receiving medical advice on needs such as loosing weight, reducing drinking and quitting smoking. Customer focus could be seen as both wants and needs focus but with emphasis on the latter. Stakeholder focus could be clarified as needs focus. Stakeholder focus, including customers would accordingly be based on needs. Based on Deming (Bergman & Klefsjö, Citation2010, p. 22) this could be defined as: ‘Sustainability should be aimed at the needs of the stakeholder, present and future’. This definition implies that needs need to be viewed over time, which could be interpreted as having a life cycle approach.

With diminishing resources it becomes logical to award the business to companies that best serve People needs without damaging the Planet. This indicates that there could be a flaw in the logic of the Triple Bottom Line. Profit might not be a stakeholder at the same level as People and Planet, but instead a means to an end (Isaksson, Garvare, & Johnson, Citation2015).

User value is a challenging concept, which needs to be defined and which includes both performance and price and which includes needs and wants (Flint, Woodruff, & Gardial, Citation1997; Woodruff, Citation1997). The company that offers the best user value compared to price and that manages to minimise its Costs of Poor Quality should in a free market be the winner. In a world that yearly consumes the production of 1.7 planets and that exceeds safe planetary limits (Rockström et al., Citation2009; Steffen et al., Citation2015), resource scarcity is a major issue. Apart from the serious Planet issues there is also the People issue of poverty. There are still some 800 million people living in absolute poverty (http://datatopics.worldbank.org/sdgatlas/SDG-01-no-poverty.html). Identifying important stakeholders could be done by reviewing the SDGs.

A review of the 17 SDGs indicates that most are focused on People (16) and several on Planet (5) with only a few linked to Profit (2). The two with ingredients of Profit focus, goals 8 and 9, are mainly focusing on People but with Profit indicated as a means to achieve these goals, see .

Table 1. The 17 SDGs analysed based on stakeholder focus and importance (https://sustainabledevelopment.un.org/sdgs).

Based on the system conditions in TNS mentioned above, conditions I-III could be seen to focus on Planet and IV on People with a note that resources should be used efficiently, which implies a role for Profit.

The Brundtland Commission definition states that: ‘Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs.’ Focus is clearly on People today and tomorrow. A corollary of the focus on tomorrow is that we should take care of the Planet in order not to compromise the possibilities of future generations. The interpretation of this is that the findings support the focus on People and Planet (Isaksson & Garvare, Citation2003).

The brief review above supports the view of a need to revise the TBL and to shift from a paradigm with Profit focus to one with focus on People and Planet. Profit is needed for company survival, which means that there needs to be both shareholder and customer satisfaction, but achieving sustainability will impose the prerequisite of satisfying Planet and People needs.

Planet as a stakeholder could be further clarified. Planet needs can be defined using the Planetary Boundaries framework (Steffen et al., Citation2015). Planet provides humanity with a number of ecosystem services and material services that constitute the basis for human survival. Based on the four identified stakeholders are atmosphere, biosphere (land), biosphere (sea) and lithosphere.

Table 2. The planetary boundaries and high level Planet stakeholders (Steffen et al., Citation2015).

The lithosphere has been included because it relates to the first of the four system conditions in The Natural Step definition of sustainability – I: ‘In order for society to be sustainable, nature’s functions and diversity are not systematically subject to: I. increasing concentrations of substances extracted from the Earth’s crust.’

The corollary from not extracting material from the Earth’s crust quicker than it is returned, is that e.g. existing water resources should remain intact.

Steffen et al. (Citation2015) write: ‘Two core boundaries – climate change and biosphere integrity – have been identified, each of which has the potential on its own to drive the Earth system into a new state … ’. This puts focus on atmosphere-greenhouse gases – SDG 13 Climate Action – and on the biosphere-loss of species both on land and in sea – SDG 14 Life Below Water – SDG 15 Life on Land.

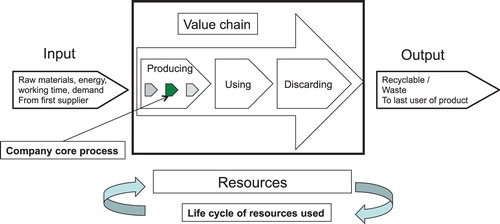

An analysis of the People goals based on a needs analysis grounded in Maslow’s hierarchy of needs (McLeod, Citation2007) indicates SDG 2 – Zero Hunger as a basic physiological need. What leads to hunger is poverty and therefore SDG 1 – No Poverty is important. Further the SDG target 1.1 of: ‘By 2030, eradicate extreme poverty for all people everywhere, currently measured as people living on less than $1.25 a day’ is particularly important (https://sustainabledevelopment.un.org/sdgs). People in extreme poverty are often hungry, have little access to health services and have problems with access to schooling. Therefore SDG 1.1 is seen to have substantial impact on other SDGs, which makes it suitable as a priority goal. Based on the Pareto principle the proposed priority People goal is eradicating extreme poverty. The GRI standards suggest identifying impacts in the value chain, which could be portrayed as the value creating process from first suppliers to last users. The value chain could be seen as forming part of the life cycle, but excluding the effect generated by resources used, see . In sustainability reports it is common that companies report only the footprint for the core processes, often citing difficulties in obtaining good data from suppliers as an excuse. Since the company promoting a product, e.g. yoghurt, is the one driving the entire value chain, fair reporting should look at the footprint from raw materials to discarding or reusing the yoghurt container. The value chain would normally not account for the footprints created when producing the resources needed, like the dairy needed for yoghourt production, the transport equipment used for its delivery and the private cars used for buying it. In order to identify key stakeholders the impacts in the value chain could be used as a basis to start with. This would mean, in most cases, disregarding the impact of resources. In the company core process is where current sustainability reporting often is focused. GRI promotes reporting the value chain (GRI 101, Citation2016a), which will provide comparable values. In processes with heavy resource investments the life cycle of these resource investments should be included. Examples of such business are heavy industries, nuclear power plants and railways.

Figure 1. A process based interpretation of how company core process could be seen as part of the value chain and part of the entire life cycle.

The difference with the discussed approach and the materiality analysis recommended by GRI is that in the ordinary materiality analysis the company identifies stakeholders based on the perceived effect they can have on the company (GRI 101, Citation2016b). These effects are probably a mixture of wants and needs. It also is less common to identify nature as a stakeholder. People or social needs are almost always focused on employees in the core business and occasionally on people working for suppliers.

Based on the above reasoning the proposal is that companies should particularly identify which direct or indirect impacts their value chain has on the climate, land use, effects on life in seas and how the value chain could contribute to reducing extreme poverty. In addition they should identify any other important impacts in the value chain.

(2) Which are the prioritised needs of the key stakeholders identified?

The main stakeholders identified are Atmosphere, Biosphere and People in extreme poverty. The prioritised needs for Atmosphere are to stop increasing the level of radiative forcing and in the continuation to reduce it (Rockström et al., Citation2017). This is done by reducing the emissions of greenhouse gases and by creating methods for increased carbon sinks including large-scale techniques for Carbon Capture and Storage.

Changes in biosphere integrity could mean losses of the eco-system services provided with severe consequences for humanity. The current rate of extinction of species is about 100–1000 times that of the background extinction rate (Steffen et al., Citation2015). The main causes are the conversion of natural land, pollution but also carbon emissions leading to ocean acidification (see ). Steffen et al. (Citation2015) propose to express the biosphere need using the Biodiversity Intactness Index (BII).

People in extreme poverty need to have some ways of supporting themselves and they are depending on having access to affordable goods and services. This provides businesses with the opportunity of including business ideas that target affordable products for the poorest and that also provide them with means of employment. These ideas are expressed in the ‘Bottom of the Pyramid’ that identify the poor as a business opportunity (Prahalad, Citation2012).

Shareholders are also stakeholders, but in a sustainability context profit maximisation with focus on enriching stakeholders has low priority. The GRI views economic sustainability in terms of sales value and how the sales value is distributed (GRI-201, Citation2016). With focus on sales value it does not matter what is produced or if there is any user needs value. With dwindling resources and with focus on reducing poverty it seems logical to prioritise businesses that create value for those needing it. An important difference in needs focus, is that it requires a review of the business idea to see how well opportunities to improve needs value satisfaction, are taken care of. That is, it could be seen as a moral obligation to review the business idea based on business opportunities in the ‘Bottom of the Pyramid’. In addition, focus on the Planet footprint is needed, but also on identifying business opportunities for increasing Planet value. This could be e.g. when a telecom company provides services reducing business travel.

The principal Planet needs identified are reduced radiative forcing and retaining or improving the level of the Biodiversity Intactness Index (BII). The main People needs are increased employability of those living in poverty and particularly those in extreme poverty and providing them with affordable products.

(3) How could sustainability performance be measured?

The Triple Bottom Line proposed by Elkington (Citation1998) expands the traditional focus on Profit to include concern for People and Planet. Since its introduction 20 years ago there is little change in how value is assessed, focus still seems to be on company profits often measured in terms of sales value (Isaksson, Citation2018).

The definition inspired by Juran and proposed by Sörqvist (Citation2008) of poor quality costs as: ‘those costs which would disappear if the company’s products and processes were perfect’ could be useful in highlighting that quality is doing the right thing – the perfect product – in the right way – the perfect process. The perfect product being any combination of goods and services should delight the customer, while creating customer value and the perfect process with no errors would minimise costs leading to good profitability. This could be extended to apply for sustainability by adding stakeholder needs focus and generalising costs to general harm including different footprints. Garvin (Citation1984) proposes five quality principles out of which one is the value-based principle that compares what the customer gets for the price paid. This principle could be extended to a more general form expressed as value per harm (Isaksson & Hallencreutz, Citation2008; Isaksson, Johansson, & Fischer, Citation2010; Isaksson et al., Citation2015).

Value would, unlike the definition in Eco Efficiency (Verfaillie & Bidwell) and in the GRI standards be focused on user value and not on the sales value. The company that offers the best user value compared to price and compared to its footprints should be the obvious choice for the concerned customer.

Here, it is proposed to work with People and Planet, focusing on value and harm (Isaksson et al., Citation2015). This means that Profit is substituted by user value. The traditional financial success of companies will be secured by providing the best user value for the lowest price. The main identified People value is employability with focus on the poorest. The main People harm identified is the price for products in the segment of poor customers. An example of this could be prices for basic food and medicines.

For Planet, the effect on climate is measured in carbon dioxide (CO2) emissions or in CO2-equivalents (e) that include other greenhouse gases, notable methane (CH4). Measuring effects on the Biodiversity Intactness Index (BII) could be a challenge. However, thinking of its importance it is reasonably to urge companies to study the effects on biodiversity in the entire value chain and to highlight all effects. This could be done applying Life Cycle Analyses with focus on pollutants and on the company Ecological Footprint.

Performance should be measured using both absolute and relative indicators, preferably related to references and benchmarks, which makes it easy for the reader to assess the magnitude and the comparative performance. For absolute indicators this could e.g. be reporting tons of CO2-e and then comparing results to branch and national performance. Examples of relative indicators, based on the value per harm logic, are such as sales value compared to CO2-e emissions and value of poverty reduction per Ecological Footprint.

Each company needs to identify areas of significant impact in the value chain. It is argued that in addition all companies need to measure actual or potential impacts, positive or negative, on CO2-e emissions, on BII and on poverty in the value chain.

(4) How could performance targets, for key stakeholder needs, be set?

Company sustainability goals are often organisation-centric and not based on the needs of the global system (Haffar & Searcy, Citation2017). A typical example of this is when a company states that it will reduce its carbon footprint with e.g. 20% over a period of 10 years without referring to any external requirements. This is improvement, but if the rate of change is too slow to comply with global requirements, then it is not sustainable development.

A typical problem is that we are bound with our ideas to how current reality looks like and consider legitimate requirements for change as unrealistic and impossible when doing forecasting. This is where Backcasting can be used. Backcasting starts by creating a vision of the system in a state of sustainability and then studying how the road map towards sustainability looks like (Robèrt, Citation2000). The visionary states should be based on agreed goals such as the SDGs and the Paris Agreement from 2015 to keep global warming under 2°C. The Carbon Law is based on an analysis of what is needed to keep the temperature increase as less than 2°C and suggest that CO2-e must be halved every 10 years, (Rockström et al., Citation2017). It should be relatively simple for companies to assess how they are doing. Using 2010 as reference, the required reduction of carbon emissions until 2030 is 75%. Proposing targets for value adding for the poorest and targets for effects on BII are left for later research. A start for comparing current performance with required performance is to look at how much traditional sales value is created per carbon footprint and how much that should be increased based on requirements for reduced carbon emissions. Comparing world GNP with world carbon emissions provides an approximate reference figure for average global performance. This was in 2011 approximately 2500 US$/ton of CO2 (Isaksson et al., Citation2015). This indicator should be further refined to focus on value added for those needing it. A first simple refinement of the sales value could be to study the user value of the products and where they are placed in Maslow’s hierarchy of needs. A simple assumption based on risk analysis could be that products catering for basic biological and physical needs of those needing them would have priority over products targeting self-actualisation. The five levels in Maslow’s hierarchy are: 1. Biological and Physiological needs – 2. Safety needs – 3. Social Needs – 4. Esteem needs – 5. Self-Actualisation needs (McLeod, Citation2007). The higher on the scale of needs the product is the more sales value should be produced compared to harm done such as carbon emissions. In average the sales value in relation to CO2-emissions should increase from 2500 to 10,000 US$/ton CO2 in 2030 due to targeted reductions in carbon emissions. Business with products catering for high level needs should probably plan for considerably higher performance. It is important to note that the carbon footprint should be accounted for in the way costs are, which means including incoming footprints. When selling an end product, which is not further refined, then also the carbon footprint until the product is discarded should be included.

Targets for important impacts should be based on external requirements and they should include long-range targets for at least until 2030, corresponding with the SDGs. All companies should in addition to identified targets on important impacts have targets for carbon reduction corresponding to at least a 75% reduction of CO2-e emissions from 2010 to 2030. Additionally companies should target achieving at least 10,000 US$ sales value/ton CO2 emitted in the value chain. Companies should also work on setting externally based targets on reduction of effects on BII and on reduction of poverty.

(5) Which are the consequences for maintaining the company license to operate with a paradigm shift to People and Planet focus?

There is pressure for a paradigm shift from Profit focus to focus on People and Planet. To describe this, the funnel metaphor from TNS has been used (Robèrt, Citation2000). In the funnel describes how the passage is getting narrower for companies to make Profit and how the funnel might close entirely, leading to system collapses, if necessary change is not taking place.

Figure 2. The funnel metaphor, describing how companies (Profit) will be struggling with increasing Planet and People constraints. Based on Robèrt (Citation2000).

Being in the centre of the tunnel is seen as benchmarking performance with a good TBL-performance. Customer wants and stakeholder needs satisfaction are high which ensures profitability for the company. The shifting focus from Profit to Planet and People should be interpreted, as an inclusion of stakeholder needs requirements that will guarantee the license to operate for the chosen business model. Business ideas based on burning fossil fuels, polluting cities and on generally using non-renewable resources might face difficulties.

Simultaneously with increased focus on Planet and People, Profit is still needed. This means that customer wants need to be assured. The shift can be described, as one going from shareholder wants focus over customer wants focus towards addressing customer wants and stakeholder needs. Customers should be seen as part of the group of stakeholders and therefore need to have both their wants and needs satisfied.

Discussion

The paper starts from quality principles with focus on customer value. The discussion is based on an idealised situation where companies make rational decisions based on long-range goals and where there is a genuine interest to provide value for customers and society. Reality is often not like this and short time priorities such as satisfying shareholders could be in conflict with long-range goals. As humans we are genetically programmed to react on things, which are close in time and space. We are neither as individuals nor as companies designed to think of what could go wrong in 50 or 100 years. It is easy to overlook needs, distant in time and place, for the short range wants. However, if we cannot overcome this problem there is a risk that the old predictions from ‘Limits to Growth’ suggesting large-scale system collapses could become reality (Meadows, Meadows, Randers, & Behrens, Citation1972). The longer we wait, the more expensive it will be. This was one of the conclusions in the Stern Review looking at the costs of climate change (Stern, Citation2006). A recommendation from the report was to internalise the cost of carbon emissions. We cannot solve problems if we do not face ‘The brutal facts’ as is postulated in the book ‘Good to Great’ (Collins & Collins, Citation2001). Backcasting, visualising a truly sustainable future based on the four system conditions could be seen as ‘facing the brutal facts’. Even without a first class moral compass companies should consider the possibility of increasing stakeholder requirements as part of ordinary risk management. Part of this could be reviewing the business idea in terms of stakeholder value creation, compared to harm done. Companies with a moral compass could benefit from following the principle of stakeholder needs instead of only following guidelines and directives that tend to be negotiated compromises. It might not always be profitable to be a first mover, but laggards could end up in the walls of the funnel.

Conclusions

On a global level the main stakeholders to focus on have been identified as People and Planet. The paradigm shift from Profit focus to focus on People and Planet have been discussed with the conclusion that serious resource constraints at the planetary level, notably climate change and change of biosphere integrity will accelerate this change, see and . The UN Sustainable Development Goals identify global challenges that need to be addressed by countries and companies until 2030, see . From a People perspective, Goal 1 – No Poverty and Target 1.1 to eradicate extreme poverty highlight the poor as key People stakeholders.

The conclusion that follows from this is that all companies need to proactively work with the impacts they have on the vital few global stakeholder needs in their entire value chain, see . More precisely work needs to be done with reducing greenhouse gas emissions, limiting effects on biodiversity and proactively working for reduced poverty with focus on those living in extreme poverty. In addition companies need to identify other important impacts they have on People and Planet in their value chain.

Sustainability performance needs to be reported for the entire value chain using both absolute and relative indicators. For greenhouse gas emissions the absolute values are tons of CO2-equivalents (e) and relative figures are such as sales value per CO2 or CO2-e. Indicators expressing stakeholder needs value such as reducing poverty and effects on Biodiversity Intactness Index (BII) need to be developed.

Performance targets should be externally set and based on planetary needs and agreed goals such as the UN SDGs. With reference to the Carbon Law (Rockström et al., Citation2017) goals proposed for carbon emissions are to reduce CO2-e from 2010 levels with 75% until 2030. The ratio of sales value per ton of CO2 should increase from an average of 2500 US$/ton CO2 in 2010 to above 10,000 US$/ton CO2 in 2030. Companies producing goods or services that are not basic needs, but higher on the Maslow hierarchy of needs, should aim at higher value per harm production. Targets for effects on poverty and on BII need to be developed.

The foreseeable consequences for maintaining the company license to operate are that in addition to satisfying customer wants companies also need to satisfy stakeholder needs. The competition will increase with increasing resource scarcity and some business ideas might no longer be viable. The company that manages to have satisfied customers, while providing better user value compared to harm done should come out as a winner. The indicative overarching conclusion is that excellence for sustainability could prove to be a strategy for profitability and for maintaining the license to operate.

Disclosure statement

No potential conflict of interest was reported by the author.

References

- Bergman, B., & Klefsjö, B. (2010). Quality from customer needs to customer satisfaction. Stockholm: Studentlitteratur.

- Collins, J. C., & Collins, J. (2001). Good to great: Why some companies make the leap … and others don't. Random House.

- Elkington, J. (1998). Partnerships from cannibals with forks: The triple bottom line of 21st-century business. Environmental Quality Management, 8(1), 37–51. doi: 10.1002/tqem.3310080106

- Flint, D. J., Woodruff, R. B., & Gardial, S. F. (1997). Customer value change in industrial marketing relationships: A call for new strategies and research. Industrial Marketing Management, 26(2), 163–175. doi: 10.1016/S0019-8501(96)00112-5

- Garvin, D. A. (1984). What does “product quality” really mean? Sloan Management Review, 26, 25–45.

- GRI 101. (2016a). Global reporting initiative, GRI 101 Foundation: 2016 – sustainability context, p. 9. Retrieved from https://www.globalreporting.org/standards

- GRI 101. (2016b). Global reporting initiative, GRI 101 foundation: 2016 – materiality, p. 10. Retrieved from https://www.globalreporting.org/standards

- GRI-201. (2016). Global reporting initiative – 201: Economic performance 2016. Retrieved from https://www.globalreporting.org/standards/getting-started-with-the-gri-standards/

- Haffar, M., & Searcy, C. (2017). Target setting for ecological resilience: Are companies setting environmental sustainability targets in line with planetary thresholds? Business Strategy and the Environment.

- Isaksson, R. (2018, September 4–6). Revisiting the triple bottom line. Proceedings of 10th international conference on sustainable development and planning, Siena, Italy.

- Isaksson, R., & Garvare, R. (2003). Measuring sustainable development using process models. Managerial Auditing Journal, 18(8), 649–656. doi: 10.1108/02686900310495142

- Isaksson, R. B., Garvare, R., & Johnson, M. (2015). The crippled bottom line – measuring and managing sustainability. International Journal of Productivity and Performance Management, 64(3), 334–355. doi: 10.1108/IJPPM-09-2014-0139

- Isaksson, R., & Hallencreutz, J. (2008). The measurement system resource as support for sustainable change. International Journal of Knowledge, Culture and Change Management, 8(1), 265–274.

- Isaksson, R., Johansson, P., & Fischer, K. (2010). Detecting supply chain innovation potential for sustainable development. Journal of Business Ethics, 97(3), 425–442. doi: 10.1007/s10551-010-0516-z

- McLeod, S. (2007). Maslow's hierarchy of needs. Simply Psychology, 1.

- Meadows, D. H., Meadows, D. L., Randers, J., & Behrens, W. W. (1972). The Limits to Growth – A Report for the Club of Rome’s Project on the Predicament of Mankind. London: Potomac Associates Book, Earth Island Ltd.

- Prahalad, C. K. (2012). Bottom of the pyramid as a source of breakthrough innovations. Journal of Product Innovation Management, 29(1), 6–12. doi: 10.1111/j.1540-5885.2011.00874.x

- Robèrt, K. H. (2000). Tools and concepts for sustainable development, how do they relate to a general framework for sustainable development, and to each other? Journal of Cleaner Production, 8(3), 243–254. doi: 10.1016/S0959-6526(00)00011-1

- Rockström, J., Gaffney, O., Rogelj, J., Meinshausen, M., Nakicenovic, N., & Schellnhuber, H. J. (2017). A roadmap for rapid decarbonization. Science, 355(6331), 1269–1271. doi: 10.1126/science.aah3443

- Rockström, J., Steffen, W., Noone, K., Persson, Å, Chapin, F. S. III, Lambin, E., … Foley, J. (2009). Planetary boundaries: Exploring the safe operating space for humanity. Ecology and Society, 14(2). doi: 10.5751/ES-03180-140232

- Sörqvist, L. (2008). On poor quality costing (Ph.D. thesis). Royal Institute of Technology, Department of Production Engineering, Stockholm.

- Steffen, W., Richardson, K., Rockström, J., Cornell, S. E., Fetzer, I., Bennett, E. M., … Folke, C. (2015). Planetary boundaries: Guiding human development on a changing planet. Science, 347(6223), 1259855. doi: 10.1126/science.1259855

- Stern, N. (2006). Stern review report on the economics of climate change.

- Woodruff, R. B. (1997). Customer value: The next source for competitive advantage. Journal of the Academy of Marketing Science, 25(2), 139–153. doi: 10.1007/BF02894350