?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This paper provides the results and the analysis of a study conducted on the processes and technologies currently used by European Union shipyards, and their potential interest in new advanced composite construction technologies, including Adaptive Moulds, Automated Tape Laying, Automated Fibre Placement, Curved Pultruded Profiles, Additive Manufacturing, Hot Stamping, Modular and Serialised Shipbuilding and Digitisation of Production. A new set of indexes are also introduced with the objective of facilitating the evaluation of the technological level of the shipyard, thereby allowing the understanding of the shipyard's interest in new developments. The analysis of the survey conducted shows that almost the 95% of shipyards either currently use or plan to use composite materials, being the composites made of fibreglass and polyester resin the most used. These composites are mainly manufactured by manual lamination and vacuum infusion techniques. The survey has also shown that there is a high interest in the shipyard digitisation and the use of new technologies in the shipbuilding industry, especially for new construction shipyards. The study shows that despite shipyards want to adopt digitisation in engineering and design processes, implementation of new technologies and concepts is being held back by financial cost and uncertainty regarding outcomes such as improved operational efficiency of vessels. The shipyards that do not use composites are less technologically advanced than those that use them, according to the analysis of the technological indexes. This analysis has also shown that the shipyards with a high technological index have a more varied potential market offer.

1. Introduction

The science and technology of composite materials are evolving rapidly, providing new materials with higher performance. The origin of nowadays composites, based on polymer resins reinforced with synthetic fibres such as glass or carbon, dates back to the early 1960s. By then, the most common manufacturing procedure was the hand lay-up process. From 1970 onward, sandwich construction and the use of resins such as vinylester and epoxy began to be used (Marsh Citation2003). Since then, the increase in the use of composites has been exponential, and they have been incorporated into many applications. This growing demand for stiffer and tougher but lighter materials has occurred in different fields, especially in aerospace, energy and civil construction (Chawla Citation2019).

The implementation of composite materials in the aviation sector initially took place in military aircraft, followed by its integration into civil aviation. Today, most aircraft have their major parts made of composites (Meola and Boccardi Citation2017). This is due to high specific strength, anti-corrosion and temperature resistance (Xie et al. Citation2020). Boeing indicates that the use of composites has increased up to 50% of the aeroplane structural weight. Furthermore, of this 50%, up to 20% of the composites are recycled (Boeing Commitment Citation2007).

The use of composites in the automotive industry is also increasing, as it does in the aeronautical field, however actual composite material manufacturing processes are not suitable for high volume productions. Therefore, it is easier to see composites in high-end cars, such as Formula 1 (Mangino et al. Citation2007), than in mass consumption vehicles.

In the naval sector, the use of composite materials has clear advantages over metals, such as lighter weight, reduced corrosion and lower maintenance costs. Weight reduction also implies a reduction in costs and in marine and atmospheric pollution, as lighter vessels require less energy to propel, resulting in reduced fuel consumption and emissions, and therefore in a reduction of environmental pollution. Additionally, the lighter weight of composites can result in lower maintenance costs and increased operational efficiency, which can translate to cost savings. Overall, the use of composites in naval applications can have a positive impact on both the environment and the economic bottom line (Martinez et al. Citation2021). The first applications of composites in marine were found in military ships. From this initial application, their use has been extended to small and medium-sized vessels, specifically leisure, military and competition vessels. With regard to leisure and military boats, the use of composites has become widespread because quite often boats are built in production series, which enables the reuse of moulds, thus reducing costs. Applications also include high-speed crafts, as well as important parts of the superstructures of large passenger ships (Mathijsen Citation2016; Hayman et al. Citation2002).

The International Maritime Organisation's (IMO) regulations on carbon dioxide and greenhouse gas emissions that have come into effect require energy-saving and cost-effective materials technology. IMO ensures the safety, security and pollution prevention of ships, and their measures affect all aspects: design, construction, operation and disposal of the vessel. Processes automation and the use of lightweight materials are therefore aspects of high interest since they provide lower cost and more efficient ships with a lower environmental impact, while complying with the prescribed regulations. Hence, there is a need for lightweight materials that ensure durability in the marine environment and high performance. The aforementioned scenario explains why the demand for technologies using composite materials is increasing.

When looking at the impact of composites in the vessel costs, maintenance costs must be taken into account, not only engineering and production costs. Planning and design costs are fairly uniform for steel, aluminium and composite hull boats. Steel is the most economical material from a manufacturing point of view, and composite is the most expensive alternative. However, if the full life-cycle costs, which include operation and maintenance, are considered, steel requires higher fuel consumption and maintenance costs, while the composites have lower costs (Yoon Citation2021). Moreover, composite materials have greater durability, minor damage, and can be easily repaired.

In addition to the possible cost reduction, there are other advantages of composite materials that allow them to be an excellent alternative for the naval sector such as resistance to corrosion, design flexibility, and improved performance. Unlike metals, composite materials are not susceptible to rust and corrosion, which can extend the lifespan of vessels and reduce maintenance costs. Additionally, composite materials can be easily moulded and shaped to fit specific design requirements, allowing naval engineers to create custom solutions for unique challenges. Moreover, composite materials can provide superior strength, stiffness, and durability compared to traditional materials, which can lead to improved performance and safety for vessels (Kimpara Citation1991). Vessels are exposed to saline environments and fatigue situations that require light materials with high structural strength and resistance against corrosion. Weight reduction is also a factor that takes part in the selection of composite materials in boat manufacturing (Mouritz et al. Citation2001). These benefits make composite materials a highly attractive option for the naval sector, offering a range of advantages over traditional materials.

These benefits will allow composite materials to expand into fields where they currently have a limited presence. With this aim, the European Union is funding projects to promote the use of composites in the shipbuilding sector. FIBRESHIP was a naval innovation project that ended in 2020 in which the implementation of composite materials in ships over 50 m in length was studied. In this project, analyses and numerical models of composite materials for the construction of structural parts of the vessel were conducted (HOME – FibreShip Citation2017). RAMSSES project (Ramsses Project: Ramsses Project. Citation2022), which ended in 2021, aimed to introduce composite materials in different structural elements of the ship structure, from the superstructure to propeller blades, in order to improve the efficiency and sustainability of ships (Chalmers Citation1994). FIBRE4YARDS project (European Commission Citation2021b, Citation2021a) started in 2021 and it aims to provide a modular, digitised, automated and cost-effective approach to the production of FRP vessels to increase the competitiveness of European shipbuilders. Also in 2021 began FIBREGY project (Fibregy – Composites for a sustainable environment Citation2021), which will develop new construction and design procedures to implement composite materials in offshore wind and tidal turbine platforms.

The advantages of the use of composite materials in the naval sector and the increase of projects around it, leads to glimpse a change in the shipyards. It is estimated that the use of composites will continue to grow in structural marine applications, as new processes lead to the optimisation of the materials and their production methods. Despite this favourable scenario, it is important to highlight the possible difficulties that may arise in this process. Firstly, the economic limitations, hence the need for new engineering approaches. Secondly, the paradigm shift, as it is important for the customer to visualise the budget not only in the construction but also in the life cycle of the vessel. Finally, due to current regulations and the importance of recycling composite materials in terms of the environment, it could be assumed that the use of these materials will limit their use in terms of what can be recycled (Shenoi et al. Citation2011). Therefore, in order to achieve a good implementation of composites, and for them to be really effective, it is necessary to focus on the recycling of composite materials and to improve production methods for shipyards.

Currently, different construction sectors are developing advanced construction methods, both with composite and non-composite materials, that can be incorporated in the shipyards. New technologies and processes also facilitate production as well as the optimisation of material and human resources. The interest in improving efficiency in shipyards to achieve an effective production through efficient planning is a topic of significant concern, as evidenced by the studies presented in Kafali et al. (Citation2021) and Choi et al. (Citation2017). Naval companies have already seen the benefits of implementing new processes and technologies with composite materials (Mathijsen Citation2016; Chalmers Citation1994).

An evidence of the interest of shipyards in these technologies is found in Navantia, where they are producing large size elements using additive manufacturing procedures. They used Polymeric Pellet-Based Additive Manufacturing (PPBAM) systems and developed two functional prototypes with PLA and flame retardant ABS (Nieto et al. Citation2018). There are also classification societies such as DNV-GL or Bureau Veritas that are trying to encourage the implementation of additive manufacturing processes in ship construction (GL Citation2021a, Citation2022, Citation2021b; Veritas Citation2019).

Another example of technologies that can be used in shipbuilding is found in modular and serialised manufacturing with composites, which pursues a substantial change in design and construction: short production series that make the manufacturing process more efficient and flexible. In architecture, modular construction is used to produce structural elements in reusable, double-curvature moulds (Bolster et al. Citation2009).

Another technology, already used by the aerospace industry, that can be adapted to shipbuilding are Automated Tape Laying (ATP) and Automated Fibre Placement (AFP) (Bolster et al. Citation2009). AFP is a process that allows a good control of the final product and a high manufacturing speed. The use of fibre-reinforced plastic improves high strength and stiffness-to-weight ratio (Crosky et al. Citation2015). With regard to AFP, it can be used to manufacture complex structures that are not attainable through other methods. These materials, which offer lighter weight with equivalent or greater strength than metals, are increasingly being used in ship structures and other industrial products.

Curved pultruded profiles is another technology that has found significant application in the automotive industry. Studies are carried out on bumpers in order to absorb the energy of an impact (Belingardi et al. Citation2013; Tena et al. Citation2015). And these profiles can also be used in shipbuilding as a reinforcement element.

The integration of digitisation in production can offer a crucial enhancement to the shipyard by enabling ongoing validation of the constructed structure and real-time monitoring of the production process (Joppen et al. Citation2019). The aeronautical sector has already developed it, and it is looking to deepen applications and models that reinforce predictive maintenance. A technique that has been developed for the purpose of ensuring efficiency and accuracy in the manufacturing process is the utilisation of a digital twin. This virtual representation is capable of recreating actual manufacturing events and forecasting future ones in a specific aircraft during the production stage (Pohya et al. Citation2021; Cao et al. Citation2023). This application is also being implemented in shipbuilding, although for most shipyards this is an idea far from reality or difficult to achieve.

The shipbuilding industry is a unique and demanding field, with ships becoming more complex and delivery times becoming shorter. To respond to these demands, shipyards need to handle a larger workload in a shorter time-frame and to deal with these conditions, shipbuilding networks can be formed by combining the resources (processes, technologies) of several shipyards or other subcontractors, allowing more work to be done in parallel, reducing cycle times and improving product quality and productivity, due to the specialisation of facilities in one process (Sender et al. Citation2021). The actual use of all these processes and technologies in shipbuilding is unknown. In order to find out, this work carries out a study on the current technological situation of the shipyards based in the European Union, by means of a survey and some interviews. The survey aims to capture the current situation in the European shipyards, as well as their interest in new technologies that can improve their productivity. The scope of this study includes both new construction and refit shipyards, regardless of their size or level of production.

The current manuscript is organised as follows. First it begins with a description of the survey that was carried out and the answers that were gathered from it. Several indexes are defined afterwards in order to assess the technological state of the shipyards. These indexes will be also used to analyse which are the shipyards that could be more interested in the different technologies and processes considered in this study. Following this, the outcomes of the conducted interviews are presented to enhance the results gathered from the surveys. Finally, a series of actions are proposed aimed to increase the technological level of the shipyards, in order to improve their production capacity and the quality of the produced vessels.

2. Survey on EU shipyards

2.1. Survey description

The main objective of this survey is to know the current state of EU shipyards in relation to their production methods, and their interest in new ones. The survey is divided into two principal sections, each of which contains three sub-sections. The first section aims to gather information about the characteristics of the shipyard being surveyed, including its size and the ships manufactured. This section also explores the technologies used by the shipyard. The second section inquires the shipyards about their knowledge and interest in different upcoming technologies that can improve their productivity and the quality of the ship manufactured.

Hereafter are described the different subsections of the survey. The complete survey is included in Appendix A.3.

| (1) | Use of Composite Materials (Questions 1–2) These questions seek to know the use of composite materials in the shipyard.

| ||||||||||||||||||||||||||||||||||

| (2) | Processes and materials (Questions 3–7) In this part of the survey, the shipbuilding industry is asked about the use of composite processes and materials. The survey seeks information on the following topics:

| ||||||||||||||||||||||||||||||||||

| (3) | Manufacturing and production (Questions 8–11) The objective is to gain insights into the types of vessels produced by the shipyards. To achieve this, the survey requests information on the number of boats constructed between the years 2016 and 2019, as well as their displacement. It is worth noting that the study was conducted in 2021, and shipyards were not asked about their production during 2020. This year has not been considered in the study in order to avoid reflecting the impact of COVID-19 pandemic in it. | ||||||||||||||||||||||||||||||||||

| (4) | Production technologies (Questions 12–13) Through these questions, it is sought to know the shipyards' interests in reference to the new technologies that they could implement in order to improve their production and productivity. Several technologies have been targeted by the study and the shipyards are asked directly for their interest on those. | ||||||||||||||||||||||||||||||||||

| (5) | Design and Engineering (Questions 14–18) The survey also inquires about the shipyard capabilities regarding the design and engineering of the produced vessels, in order to know how easy will be for the shipyard to adapt them to the new advanced production technologies that can be implemented. To assess this, the survey asked about:

| ||||||||||||||||||||||||||||||||||

| (6) | Shipyard 4.0 (Questions 19–22) Finally, the survey also evaluates the deployment of Shipyard 4.0 concepts, in the composite materials shipbuilding industry, aimed to achieve a fully interconnected production. In this regard, the survey asks for the level of digitisation of the shipyards and for the advantages that they expect from such implementations. | ||||||||||||||||||||||||||||||||||

2.2. Survey data acquisition

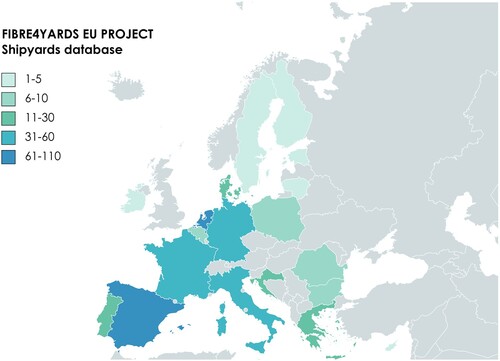

A database of 426 shipyards within the European Union has been compiled. The recruitment of participants was carried out through online channels, including professional email and web pages. shows a map that indicates the number of shipyards that where contacted, divided by country. Four separate monthly e-mails were sent to the shipyards to encourage them to participate in the survey. In return for their collaboration, shipyards were offered access to the details of the study conducted at the end of it. All data were collected between January 2021 and April 2021.

Figure 1. Shipyards to which the survey is sent (MapChart Citation2023). (This figure is available in colour online.)

2.2.1. Survey participation

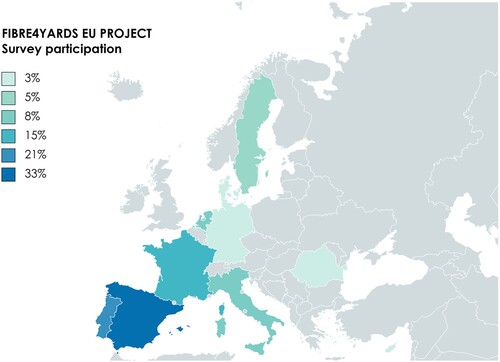

A participation rate of 9.2% was obtained from the survey, which corresponds to 39 shipyards. Although a greater participation was expected, the responses from 39 shipyards, representing a broad spectrum of EU countries, provide a sufficient sample size to yield representative results. shows the survey participation for the different countries.

Figure 2. Survey participation (MapChart Citation2023). (This figure is available in colour online.)

illustrates that the highest participation was found in Spain, France and Portugal. However, this figure also shows that there are answers from shipyards from nearly all EU countries contacted. Therefore, the results can be considered representative for all Europe. This assumption has been corroborated when analysing the results, as there has been no specific trend depending on the country in which the shipyard is based.

2.3. Survey results

The main results obtained from the survey are described hereafter. As it will be seen when presenting the results, most of the questions were asked in a closed form. This was done to facilitate the answering of the survey by the shipyards, and also to facilitate the analysis of the results afterwards.

2.3.1. Manufacturing and production

This first section of the survey aims to know the characteristics of the shipyards that have answered it. These will be classified based on the type of vessels produced, the size of these vessels, and the size of the shipyard which is measured based on its turnover.

The main market served by the shipyards that have answered the survey is Leisure Boats, with a 56% participation. It is followed by Service Vessels such as Tugboats or Work Boats with 50% and Naval Ships (mainly military) with a 40% participation. Special Purpose Ships, Passenger Vessels and Fishing Boats also have percentages close to 30%.

As can be seen, the sum of the percentages shown is larger than 100%. This is because most shipyards produce several vessel types, being the most common combination the production of Passenger Ships and Service Vessels and the combination of Special Purpose Ships and Service Vessels. These two production combinations are carried out by a total of 21% of the shipyards surveyed.

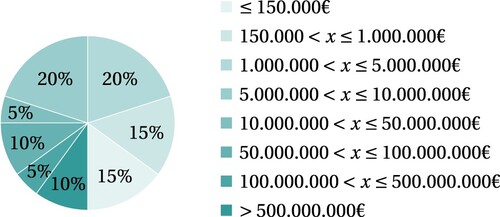

The survey showed that leisure boats are built both small and medium in length. There are many constructions of less than 10 m in length and quite a few between 10 and 50 m length. presents the Total Turnover of the surveyed shipyards. As it can be seen, the distribution of groups is quite uniform, indicating that both small and large shipyards participated in the survey. This desired diversity provides a more comprehensive understanding of the shipbuilding industry as a whole, and will allow reaching more generalised and representative conclusions.

Figure 3. Answers to the question: Total Turnover in EUR in 2020 (the total income the business generates). (This figure is available in colour online.)

The turnover data shown in reveal that 70% of the shipyards have a total turnover of less than EUR 10 million. The relationship between total turnover and the size of vessels built at each shipyard has been also analysed. shows the total turnover at the European scale for different ranges of vessels tonnage. This table shows that vessels with less than 50GT represent only a 3% of the total turnover, while vessels ranged between 50 and 500GT represent more than a 90% of the turnover.

Table 1. Total turnover by tonnage.

2.3.2. Use of composite materials

In , it is observed that 77% of the shipyards use composite materials, either by their own means or through subcontractors. And the other 23% do not use such materials.

Figure 4. Answers to the question: Do you use composite materials in your shipyard? (This figure is available in colour online.)

Of the shipyards surveyed that currently do not use composite materials, representing 23% of the total, 22% have expressed a lack of interest in implementing such materials, while 78% have indicated their interest in incorporating them. This implies that of the total of surveyed shipyards only 5.1% do not use composites and are not interested in their use, so 94.9% of shipyards use or plan to use them. Thus, we can assume that composites have and will have a strong impact on the naval industry. This is an interesting result, since the knowledge of the material by the shipyard will facilitate the implementation of technologies and processes in the coming years in order to optimise production and improve the final product.

2.3.3. Processes and materials

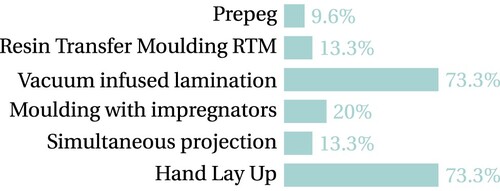

shows that manual lamination and infusion lamination, are the most used processes in shipyards. 73% of shipyards use these processes. This is in accordance with the statement made in Kim et al. (Citation2014) in which it is said that nowadays, structures are mainly manufactured using hand lay-up and infusion techniques, due to the advantageous cost-effectiveness relation of this procedure.

Figure 5. Answers to the question: Which of the following composites' manufacturing processes do you use? (This figure is available in colour online.)

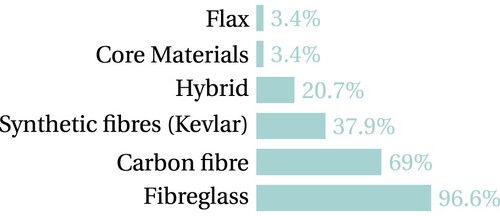

When asked about the reinforcement materials most used by the shipyards, the results showed that nearly all of them (97%) use fibreglass and that most of them (69%) also use carbon fibres. Other synthetic fibres. such as Kevlar or hybrid combinations are also used. Of this result is also interesting to point out how the most common natural fibre, flax, is barely used by shipyards. The predominant use of glass fibres, and the reason why it is widely used in boats, can be explained because they offer excellent mechanical strength, high resistance to humidity and excellent thermal insulation, as well as being low cost and easy to maintain (Chawla Citation2019). This is also confirmed in Kimpara (Citation1991) where it is stated that fibreglass has apparently reached a plateau in the marine sector. The results of show the materials that are used by the shipyards and not the proportion in which each material is used. However, it is known that fibreglass, apart from being the reinforcing material used in the vast majority of shipyards, is the most used fibre in the shipbuilding sector.

Figure 6. Answers to the question: Which reinforcement materials do you use? (This figure is available in colour online.)

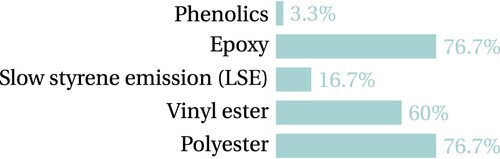

Regarding the results shown in and , it has to be stressed that the survey only asked about the materials used, and not which material was most used and in which proportion. Therefore, the result of a shipyard using mainly polyester and epoxy occasionally will be the same as the result provided by a shipyard that uses mainly epoxy and polyester occasionally. This was done in this way because the aim of the survey lays more in knowing which are the technologies and materials known by the shipyards, than knowing to what extent these technologies and materials are used.

Figure 7. Answers to the question: Which resins do you use? (This figure is available in colour online.)

2.3.4. Production technologies

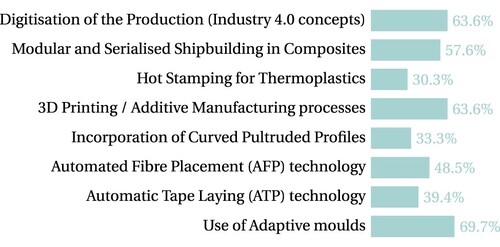

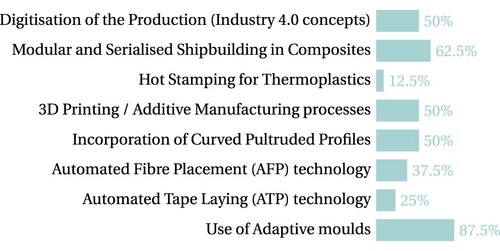

The second section of the survey is aimed to know the interest of the shipyards in the new production technologies targeted by the study. They were asked about their knowledge and interest on upcoming production technologies for composite manufacturing. shows the technologies targeted by the study and the interest shown by the shipyards in each one of them.

Figure 8. Answers to the question: Fibre4Yards will consider the following technologies. Which of the following would you be interested in? (This figure is available in colour online.)

As depicted in , the technologies that received the most interest from the shipyards surveyed are the use of adaptive moulds, production digitisation, additive manufacturing (3D printing) and modular and serialised construction with composites. It is noteworthy that there is a significant level of interest in all of the technologies, as at least one-third of the survey shipyards are interested in each one of them. This observation demonstrates that despite the maritime sector being a traditionally slow-moving industry in terms of the adoption of new materials, processes, and technologies, it is cognisant of the need to introduce innovative production technologies to enhance its competitiveness.

2.3.5. Design and engineering

When evaluating the ‘Design and Engineering’ capabilities of the shipyards, the survey showed that 81% of shipyards are interested in the production procedure, but also in the design and engineering work associated with it, while 19% are only interested in production. However, this result does not mean that this 81% have their own design and engineering offices. 30% of the shipyards subcontract engineering and design resources, 35% have their own resources and 35% have some resources and have to subcontract the rest. So, 70% of shipyards have their own engineering resources, even if they outsource some of them. This shows that shipyards tend to want to have their own technicians (designers and engineers).

Over half of the shipyards use Finite Element Analysis tools. Advanced numerical tools are not used more due to the difficulty of hiring qualified personnel and to the cost of having a suitable tool. 54% of the shipyards use specific analysis tools for the calculation of composite materials for their production. These tools are likely to come from classification societies. It is observed that 89% of the shipyards express interest in these tools to optimise their production. This percentage is in line with the percentage of shipyards that expressed the intention of maintaining or incorporating the use of composite materials.

2.3.6. Shipyard 4.0

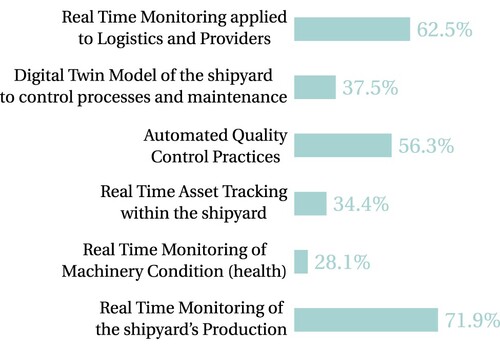

This study has also evaluated the implementation of Shipyard 4.0 concepts in the composite materials industry, in order to achieve an interconnected production. shows different technologies related to industrial digitisation and the Internet of Things (IoT), aimed to achieve a shipyard 4.0 environment. The results provided by the respondents show that the technologies that are of greatest interest to shipyards are real-time monitoring of production with 72%, real-time monitoring applied to logistics and suppliers with 63%, and practices of automated quality control with 56% of participation. The three developments are seen as a mainstay for Shipyard 4.0.

Figure 9. Answers to the question: Among the different developments select which ones you consider more interesting. (This figure is available in colour online.)

The survey also enquired about the shipyards' processes with a higher degree of digitisation. These are the technical manufacturing and engineering departments, followed by logistics. These departments are in the design and preparation phases where digitisation is less expensive and much needed. However, there is little digitisation in the production processes.

2.4. Indexes for the evaluation of the shipyard technological state

According to Carral et al. (Citation2021), the level of technological complexity of a product can be determined using three key indicators, each representing a distinct phase in the development of a ship: the conceptual stage, the design phase, and the production phase. Following this approach, this work proposes the use of several indexes that have been specifically defined to evaluate the technological state of the shipyard. These indexes have been defined based on the responses given by the shipyards to the survey questions aimed to understand their technological capabilities.

The indexes chosen are the following: Materials, Process, Digitisation, and Design and engineering. Material index measures the quality and availability of the materials used in construction, process index measures the efficiency and effectiveness of the processes used to build and maintain ships, digitisation index assesses the use of technology to improve processes and increase efficiency, and finally, the design and engineering index measures the innovation and sophistication of the designs used in shipbuilding. A last index, named Global technology index, has been defined to average the four other indexes calculated. These indexes classify each shipyard with a natural value, between 1 and 4, being 1 the value assigned to those shipyards with lower technological features, and 4 the value assigned to those with higher.

By using the indexes defined, it is possible to have a comprehensive view of the technology used in the shipyards. This information is useful for determining areas where the shipyards can improve their technology and become more competitive. Moreover, understanding the technological complexity of shipbuilding and the abilities of the shipyard can also help in planning future projects and allocate resources effectively. The indexes can provide valuable insights into the shipyard's strengths and weaknesses, allowing it to focus on areas that require improvement and capitalise on its strengths. Additionally, the information obtained through the evaluation can aid in the selection of appropriate technologies, materials, and processes for future projects, ensuring their success and cost-effectiveness.

2.4.1. Index definition

The different indexes proposed and defined in the framework of this work are the following:

Materials index (

)

Assuming that the shipyards that use a larger number of different materials will be more receptive to use new ones, the material index classifies the shipyards based on the number of different materials used. The survey proposed 11 different materials, therefore the material index is calculated as:

Based on the value obtained for Mat, a material index (

Processes index (

The process index accounts for the number of processes that are actually being used by the shipyard. The processes considered to calculate this index are the new production technologies targeted by this study and shown in . Of these, ATP and AFP have been grouped as a single process for their similarity. This index is calculated as:

Digitisation index (

This index provides the level of digitisation that is actually available at the shipyard. It is calculated in a similar way as previous indexes:

Processes

Logistics

Digital twin ship

Digital twin shipyard

Technical manufacturing department

Engineering department

Each shipyard has rated each of these six features from 0 to 4, where 0 means poor level and 4 means excellent level.

The digitalisation index has undergone a similar procedure to the material index, resulting in the calculation of

Design and Engineering index (

This index shows the level of Design and Engineering capacities of the shipyards that have answered the survey. There are three parameters that affect this analysis. The first is whether they use FEA (

Global Technology index (

The Global Technology index evaluates the total technological state of the shipyard based on the indexes previously calculated. Its value is obtained with the following formula:

2.4.2. Index analysis

summarises the indexes obtained by the shipyards that have answered the survey, grouped by the index value obtained. The indexes obtained by each one of the shipyards individually is shown in Appendix A.1 of the manuscript.

Table 2. Technology indexes.

shows that there is approximately the same number of shipyards in all indexes, which proves that the shipyards that have participated in the survey provide a fairly homogeneous representation of different technological levels coexisting in Europe. The only index that does not show an homogeneous distribution is the design and engineering index (), as nearly half of the shipyards have a value of 1. Based on Equation (Equation5

(5)

(5) ), this index gets a value of 1 if the shipyard does not use any simulation tool in their processes (FEA software or composites tools) or, if they use any, if it is outsourced. Based on this result, it can be concluded that the shipyards that have answered the survey either do not have a design and engineering office or, if they have it, its technological level is quite poor.

The analysis of also shows that the number of shipyards with a Global Technology index equal to 1 is quite low (8). This means that there are very few shipyards that have a low index in all aspects analysed. This statement can be verified by looking at the independent results for each shipyard (Appendix A.1), as only 5 of the 39 shipyards analysed (12%) have all indexes between 1 and 2. This analysis also shows that none of the shipyards in which all indexes are 1 work with composite materials. This result suggests that shipyards that do not use composites tend to be less technologically advanced (in all aspects) than the ones that do use composites.

The analysis of the different index values obtained for the different shipyards also allows reaching some conclusions when these are correlated. From the indices obtained for each shipyard (see Appendix A.1)) it can be seen that there are a 41% of the shipyards (16) in which both, the material index and a process index, have a value of 1 or 2, and that there is also a 41% in which these two indexes are equal to 3 or 4. This shows that either the shipyard uses several material and processes, or it is limited to a few of them. This correlation between material and processes does not occur when looking at the digitisation or the design and engineering index. In example, of the 16 shipyards with a low value in material and processes (indexes equal to 1 or 2), 10 (62%) of them have a digitisation value equal to 3 or 4.

The other correlation that can be seen when analysing together different indexes is between digitisation and design and engineering. Although there is not a clear correlation between the shipyards in which both values are between 3 and 4, this correlation does exist when the technological level is low: 49% of the shipyards (19) have both indexes between 1 and 2.

The independent analysis of all indexes by shipyard also shows that there are very few of them (8, which corresponds to a 21%) in which all indexes are between 3 and 4. And only one of them, based in Portugal, has all indexes equal to 4.

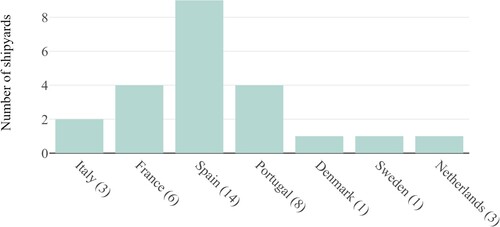

Regarding grade 4 shipyards, a study has been carried out to find out in which countries there are shipyards in which at least one of the indexes is equal to 4, which means that they have the maximum technological level in at least one of the items considered. There are a total of 22 shipyards out of the 39 surveyed, which stand out at grade 4 in some of the indexes. shows these 22 shipyards according to the country where they are located. In brackets, next to the name of the country, is shown the number of shipyards that participated in the survey, which facilitates the contextualisation of the values represented. This is, the values obtained in those countries in which only one shipyard has answered the survey cannot be considered representative of the whole country but, instead, have to be considered a one-shipyard case.

Figure 10. Countries with Shipyards with 4 grade in Global technology index. (This figure is available in colour online.)

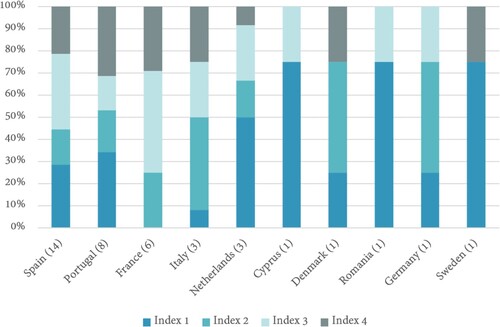

Finally, presents the percentage of index grades obtained by the different shipyards based on their country for all aspects analysed. This image does not differentiate between the different indexes, but it allows seeing that in the Netherlands nearly 70% of the indexes are 1 or 2, while in France more than a 70% of the indexes are 3 or 4.

Figure 11. Percentage of index grades obtained by the different shipyards according to their country. (This figure is available in colour online.)

Again, the results shown in this figure should be considered more representative for those countries in which more shipyards have answered the survey, than in those in which only one has done so. However, the result is still interesting as it shows very clearly the technological level of the shipyards that have participated in the study.

2.5. Survey analysis

After describing the main results obtained from the survey in Section 2.3, this section presents an analysis of these results and the relations that can be obtained among them. The main objective of this analysis is to find out which are the characteristics of the shipyards that are interested in the different technologies, processes and concepts proposed in the study. Two different analysis have been performed. In the first one, shipyards have been classified based on the type of construction that they do: refit, new construction (NC) or both. The second analysis made is based on the digitisation index defined in section 2.4. This analysis will show the interest of the shipyards in digitisation technologies, based on the level of digitisation that they already have. Additionally, this second analysis aims to identify the potential barriers that shipyards face when adopting new technologies and processes. By understanding these barriers, the study can provide recommendations for overcoming them and promoting the uptake of innovative production methods in the naval sector. The results of this analysis can be useful for stakeholders, such as shipyards, suppliers and regulatory bodies, to make informed decisions on investment in new technologies and processes. Furthermore, the insights gained from this analysis can inform future research aimed at improving the competitiveness of the shipbuilding industry in the European Union.

2.5.1. Interest in Fibre4Yards shipyard 4.0 concept according to the type of construction

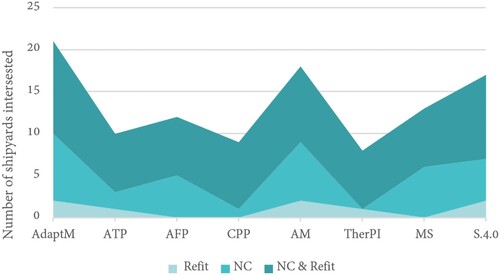

and show the interest of the shipyards that have answered the survey on the different production technologies presented, divided in function of the type of ship construction made: refit, new construction or both. The first thing that stands out from the results obtained is that shipyards that do only New Construction (NC), or Ship Refits (Refit) find that there are some technologies that are substantially more interesting than others, while shipyards that do both, NC & Refit, find all technologies equally interesting. An example of that is found in the Curved Pultruded Profiles (CPP) technologies, in which the interest is of 0% and 9% for the Refit and NC shipyards, respectively, and of a 57% for the NC&Refit shipyards. Similar values are found with the use of thermoplastics (TherPl) and Modular and Serialised Shipbuilding (MS). This is shown very clearly in , in which the band corresponding to NC&Refit is quite constant, while the peaks are defined by the bands corresponding to NC and Refit shipyards.

Figure 12. Interest in Fibre4Yards Technologies. Technologies vs Shipyard fields. (This figure is available in colour online.)

Table 3. Interest in Fibre4Yards Technologies according to the type of Shipyard.

Despite these differences between the type of shipyard, another result that can be drawn from and is that the technologies that currently are considered more interesting are: Adaptive Moulds (AdaptM), Additive Manufacturing (AM) and the Shipyard 4.0 concept (Shipyard 4.0).

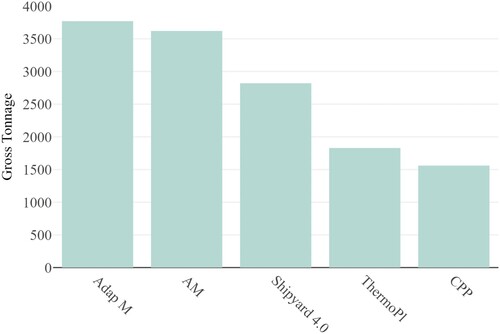

The results of the survey also allow us to study the impact of the different technologies in the market. and show the sum of the Gross Tonnage manufactured by the shipyards that have shown interests on some of the technologies targeted by the project: AdaptM, AM, Shipyard 4.0, ThermoPl and CPP. This value is a good indicator of the impact that can have each technology in the market.

Figure 13. Interest in Fibre4Yards Technologies. Technologies vs Impact on Gross Tonnage of surveyed shipyards production. (This figure is available in colour online.)

Table 4. Gross Tonnage according technologies.

These results show that the technology that can have more impact in the market is the use of adaptive moulds, as this technology is of the interest of shipyards that represent the 72% of the gross tonnage market that has participated in the survey. Although these data do not indicate that 72% of the production would be through this technology, it shows the size of the ship construction business interested in it. The next technologies that raise more interest, based on the market size, are additive manufacturing and the development of Shipyard 4.0 technologies, which can have an impact in the 69% and the 54% of the surveyed production market. Finally, it is also interesting to see that technologies that have rise fewer attention to shipyards, such as the use of thermoplastics or curved pultruded profiles, can also take an important size of the market, as the 35% and the 30% of the gross tonnage market surveyed is interested in them.

2.5.2. Interest in Fibre4Yards shipyard 4.0 concepts according to the shipyard's digitisation index

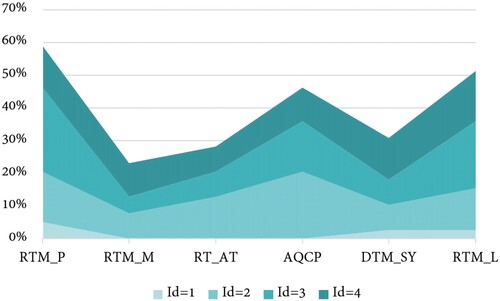

This analysis intends to understand the interest that shipyards have in the Shipyard 4.0 concepts, based on their current status regarding digitisation technologies, which has been measured using the digitisation index () previously defined. This index classifies each shipyard with a value between 1 and 4. Value 1 is assigned to shipyards that currently have very few digitisation features implemented in their production process, while value 4 is assigned to shipyards with a large amount of digitisation features implemented in their production.

and show the interest that have shown the shipyards on the different digitisation options considered in this study. The digitisation options considered by the project are:

AQCP: Automated Quality Control Practices

Figure 14. Interest in Fibre4Yards Shipyard 4.0 Concepts. Shipyard 4.0 vs Digitisation involvement. (This figure is available in colour online.)

Table 5. Interest in Fibre4Yards Shipyard 4.0 concepts according to Digitisation index.

The first set of data in shows the total number of shipyards interested in the different technologies. These values show that the technologies that raise more interest are , AQCP and

. This result is also shown by the peaks in . The results show that the shipyards with lower digitisation index

barely have any interest in any technology, and that this interest grows with higher

.

Another value that is interesting to analyse is the number of shipyards interested in a given technology depending on their number. This is shown in the last section with percentages in and in . Shipyards with low

number, in example 2, have a lot of interest in certain technologies and a few interest in others: all shipyards with

are interested in AQCP and only 38% of them are interested in

or

. On the other hand, as the

value increases their interest is equivalent for all technologies. This aspect is also shown by , in which the thickness of the line for

is practically constant.

It is important to note that the number not only represents the level of digitisation of the shipyard, but it also provides insight into the shipyard's willingness to adopt new technologies. The higher the

number, the more open the shipyard is to incorporating new technologies and processes into their operations. This can be seen in the consistent level of interest shown by shipyards with

across all technologies. However, shipyards with lower

values tend to be more selective in their technology choices and may only adopt technologies that they see as particularly relevant to their operations. Understanding this relationship between

values and technology adoption can be useful in targeting specific shipyards with technology offerings and assessing their level of receptiveness to new innovations.

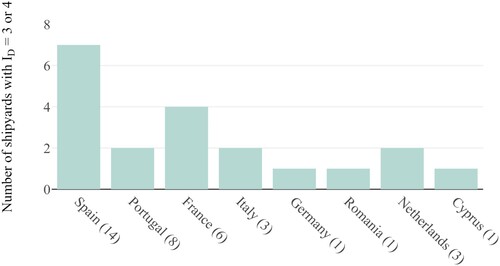

shows how many shipyards per country have a grade 3 or 4 of digitisation implemented. This figure allows concluding that Spain, France and Italy are the countries that have the highest level of digitisation in their shipyards.

Figure 15. High level of digitisation depending on the shipyard country. (This figure is available in colour online.)

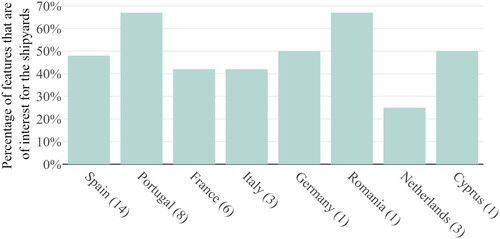

represented the percentage of Shipyard 4.0 features, of a total of 6, in which are interested the shipyards that have a digitisation index of 3 and 4. This figure shows that while Spain, France and Italy were the countries with the highest digitisation index, Portugal is the country that shows more interest in the different Shipyard 4.0 features proposed. The 68% value shown in means that in average Portuguese shipyards are interested in 4 of the 6 features considered to define the different shipyard 4.0.

Figure 16. Average interest in Shipyard 4.0 concepts of highly digitised shipyards. (This figure is available in colour online.)

The information represented in these last two figures provides valuable insight into the adoption of digital technologies in the shipyard industry. It allows to identify which countries are leading the digitisation process and to understand their level of interest in new and innovative concepts like Shipyard 4.0. This can help in the development of new strategies to promote the adoption of these technologies and to provide support to the shipyard industry in their digitisation journey.

3. Interview analysis

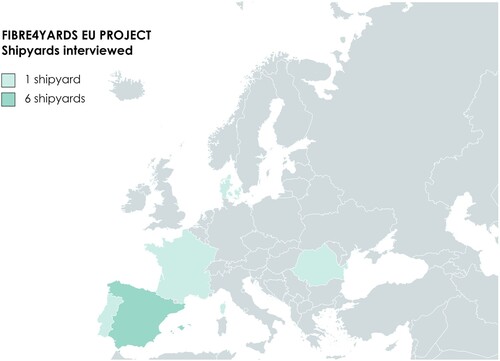

The survey previously presented has been complemented with several interviews. A total of 10 shipyards of those that had previously answered the survey were interviewed by the authors of the study. The interviews were conducted by telephone or by videoconference, following a previously prepared questionnaire. shows these 10 shipyards according to the country where they are located.

Figure 17. The number of shipyards by countries participating in the interview (MapChart Citation2023). (This figure is available in colour online.)

The main aim of these interviews was to corroborate some of the conclusions extracted from the survey responses, and to get a deeper understanding of some specificities of the shipyards working with composite materials. Hereafter are described the main results obtained from the interviews conducted in terms of:

The production carried out by the shipyards in reference to composite materials.

Composite waste manageme nt protocols in shipyards.

Shipyard market analysis.

Impact of the COVID pandemic on shipyards and the expectations of the industry in the post-COVID situation.

3.1. Production in shipyards

While the survey analysed the type of boats produced by the shipyards, based on their length and quantity, the interviews conducted were focused in analysing the types of structures and components that are manufactured with composites, and the types of ships in which these materials are used.

3.1.1. Processes and materials

Analysing the main materials used by the shipyards for hull construction, it is found that from the seven shipyards that use composites, five of them use FRP (Fibre-Reinforced Polymer) with a percentage in weight of more than 75%, while steel is used by three shipyards with a percentage of between 50 and 70%. For superstructure construction a similar pattern is observed. Therefore, this percentages can be considered a trend in the use of composite materials throughout the whole vessel.

In terms of manufacturing processes, there is an outstanding use of manual lamination and infusion lamination, an aspect already observed in the surveys and reiterated in the interviews. When the interviewees were asked about the reasons for the predominant use of this manufacturing procedure they explained that manual lamination is used because its low cost, and infusion lamination because the quality offered in large elements. Regarding the advanced manufacturing processes targeted by this study, the shipyards pointed out that in order to be able to incorporate them in their production chain, the main requirements are a good cost-production ratio, the ease of implementation, and the guarantee of quality.

3.1.2. Use of composite materials

70% of the interviewed shipyards use composite materials in their vessels. The interest of surveying shipyards that do not use composite materials was to know if they would be interested in using them through new processes and technologies. All of them expressed their interest in incorporating composites in their processes. This result differs from the results obtained from the survey, in which a 22% of the shipyards that do not use composites stated that they do not have any intention of using them. The different reasons indicated by the interviewed shipyards for not using composites were that they do not have enough space in their facilities, the lack of qualified personnel, the lack of knowledge of the material and the machinery and the lack of investment in this production methodology.

Interviewees also indicated that the process that they would be most keen to implement is moulding with impregnators followed by infusion lamination and manual lamination. The shipyards that currently do not use of composites show that, apart from the most currently implemented processes, they have interest in impregnator moulding. This is an indicative of the interest in making a change for productivity improvement. It can be deduced that the lack of interest in other processes can be due to either a lack of knowledge, or to the intention of a gradual implementation.

Regarding the shipyards that use composite materials, they were asked in which vessels parts they use of composite materials depending on the length of the vessel. The shipyards surveyed show that they make composite hulls for boats between 5 and 100 m in length, with hulls for boats between 20 and 50 m in length being the most frequent. Boats between 5 and 100 m in length also use composites for superstructures and cabins and, in this case, this use stands out in boats between 10 and 50 metres in length. This result corroborates the statement that composite materials are mainly used in small and medium size boats.

When analysing the type of boats constructed, the interviews showed that the use of composite materials in leisure boats, service vessels and special purpose ships between 10 and 50 m length is noteworthy. Vessels between 20 and 50 m with the greatest use of composite materials are Passenger Ships, Fishing Vessels and Naval Ships (mainly military). shows the number of vessels produced according to the type of vessel in which composite materials are implemented.

Table 6. Number of vessels manufactured in which composite materials have been implemented.

The results of the interviews also show that the European shipbuilding market is oriented towards small and medium-sized vessels, as was already concluded by the survey. And these vessels are the ones that make the greatest use of composite materials. As for the type of vessels, while the survey highlighted the construction of leisure and service vessels, the interview shows a more homogeneous distribution. This is an indicator that the selection of shipyards for the interview, being a smaller number than those surveyed, provides a sample that reflects the breadth of the market, which facilitates extrapolating the data obtained to the different shipyards. Furthermore, the homogeneous implementation of composite materials in the different vessel types indicates that the use of new processes would have an impact on all vessel types manufactured by EU shipyards.

Additionally, it is important to highlight the cost benefits of using composite materials in shipbuilding. The survey found that shipyards that use composite materials reported lower costs of raw materials and reduced production time, compared to traditional shipbuilding methods. These cost savings are not only attractive to the shipyards, but also to the end customers, as they can provide more competitive pricing for their vessels. Furthermore, composite materials offer improved mechanical properties and increased corrosion resistance, which results in a longer lifespan for the vessel and reduced maintenance costs for the owners. This highlights the significance of promoting and encouraging the use of composite materials in the shipbuilding industry.

3.1.3. Production technologies

shows the shipyards interests in new technologies in order to increase production. There is a greater interest in adaptive moulds and modular and serialised composite construction, followed by digitisation of manufacturing, 3D printing and curved pultrusion profiles.

Figure 18. What technologies would you like to use to increase production? Please specify. (This figure is available in colour online.)

It should be noted that the shipyards are constantly looking for new and improved technologies to increase their efficiency and competitiveness in the market. The use of adaptive moulds is seen as a key area for improvement, and the shipyards are open to exploring this technology further. Automation is also seen as an important area for improvement, although the shipyards acknowledged that the customisation of vessels makes it difficult to fully automate their processes. Currently, some shipyards are taking a phased approach to automation, implementing it in certain parts of their CAD/CAM software. Despite their interest in new technologies, some shipyards have had negative experiences with previous investments in new technologies that have not proven to be profitable. This serves as a reminder that careful consideration should be given before implementing new technologies in the shipbuilding industry.

3.2. Composite waste management

Different approaches were reported in reference to the implementation of any recycling protocol or circular economy standard with respect to the materials used in production. 30% of shipyards do not have a plan for waste management. The remaining 70% use different procedures and stated that they have been dealing with this aspect for some time. A common practice is to subcontract companies specialised in FRP waste treatment. Most shipyards show that waste materials are collected by contracted companies specialised in recycling. They also mention to regulations such as ISO 14000, in relation to the environment, and to the special treatment of waste according to European regulations by which they are governed.

From the responses obtained, it can be concluded that waste treatment in composite construction is a pending issue that requires more and better solutions and regulations in order to ensure the sustainability of the sector.

3.3. Shipyard 4.0

Those shipyards that are more aware of Shipyard 4.0 technologies were about their thoughts on the feasibility of having a 4.0 shipyard and if they found this concept useful. They noted that Shipyard 4.0 offers them the possibility of better planning, product quality, avoiding deviations in reference to the customer, shipyard and ship, optimising production processes and being able to carry out several processes simultaneously. They also recognise the improvement that will bring to the shipyard in terms of safety conditions at work and the efficiency in many production processes. However, they state that the processes and technologies offered by Shipyard 4.0 are more applicable to shipyards that produce in series.

When observing the low implementation of these concepts, the focus is on finding out what are the main limitations or fears that shipyards see regarding the implementation of Shipyard 4.0 technologies, what they need to overcome these limitations, and when do they believe they will be able to implement a Shipyard 4.0. They express that a significant change is needed in terms of the company's management philosophy, the need for high investments, qualified personnel and programs oriented to the ship's production. They also mention that they are looking to increase productivity, and for this they require monitoring programs in order to update the ship's condition. For most shipyards, all of this would entail a medium to long-term change. Finally, they stress that to achieve this change it is necessary to identify in which processes more time is lost, and in which one will benefit more from these new technologies, in order to know how to optimise their resources.

3.4. Shipyards market

The shipyards interviewed allocate a significant part of their production to the domestic market, both in the European Union and in their own country. They also mentioned other European countries (Eastern Europe, Russia and Northern European countries) and Asian countries (Middle East, Pacific Asia, China, India, Japan) as important customers. There is a high number of orders from repairs and refits, due to the proximity. The administration was reported as an important customer, as it tends to favour shipyards in the EU environment, although customers are mainly newbuildings coming from the private sector.

The significant presence of private customers in the European and Asian markets who entrust the construction of their vessels to EU shipyards means, on the one hand, a high degree of competitiveness, since Asia is home to shipping powers such as Japan and China, and, on the other hand, the loyalty of the states in the immediate vicinity. This assessment is especially useful for small- and medium-sized shipyards.

3.5. COVID-19 impact

When conducting the interviews, in May 2021, the 2020 COVID crisis have been affecting the sector for 10 months. The interviews conducted evaluated also this aspect. The shipyards show that the pandemic has affected the reduction of sales to external customers (up to 30% decrease in turnover), has delayed the processes, and has brought expenses due to established safety standards and lack of personnel.

Expectations of the trends following this situation are of two different types. On the one hand, there are the shipyards that wish to resume activity, recover the sector and improve the current market situation. On the other hand, there are the shipyards that want to take advantage of this crisis to regenerate themselves.

4. Conclusions

This study has analysed the shipyards' current situation in the European Union by means of a survey in which most of the existing EU shipyards were invited, and has been complemented with interviews made to some of them. The main aim of the study is to understand the current state of the shipbuilding industry and their interests in accommodating new processes and technologies.

The responses to the surveys and interviews have shown that almost all the shipyards use composite materials, mainly polyester, epoxy and vinylester resins, which are reinforced with fibreglass and carbon fibre. The study has also shown the percentage of implementation of each of these materials and the type of boat in which they are used. The good acceptance of these materials by shipyards allows stating that their strong impact on the shipbuilding industry will grow in the coming years as improvements in new materials and processes are brought to the market, are consolidated in it, and their price becomes more competitive. The use of these materials in shipyards will facilitate the implementation of technologies and processes to optimise manufacturing and improve the final product in the coming years.

In reference to the composite manufacturing processes, the study has shown that the criteria used by the shipyards to select a given process is its cost-effectiveness and the final result obtained. The survey results show that the most common processes are manual lamination and infusion lamination. The limitations that hinder the implementation of new processes is the lack of certainty in the feasibility of using different processes and technologies, compared to the ones that already exist and are profitable. It is necessary to establish a production and business model in which shipyards have to make a minimum investment in equipment, enhancing the use of these new manufacturing technologies through the strategy of subcontracting.

The interview and survey results show that most of the vessels built are of medium or small size, with a wide variety of typologies, although leisure, service and military use predominate. This can be seen as an opportunity to promote the transition to new technologies, processes and materials through subcontracting; in this case, the modulation would be more feasible. In addition, shipyards show a great interest in new technologies, especially in Use of Adaptive moulds, Additive Manufacturing processes and Digitisation of the production, Modular and serialised shipbuilding in composites and Automated Fibre Placement (AFP) technology. Having already consolidated the option in favour of new materials and processes, shipyards are open to the new technologies in which they can apply them.

This interest is reflected in the existence of engineers to take care of the design, calculations and process management, either directly or through subcontractors. This second option, subcontracting, is an interesting option to be encouraged as it optimises investments, and facilitates the transition, as well as gives access to innovations for small shipyards. Subcontractors will have to guarantee to the shipyards that the quality of the supplied materials, is in accordance with the standards and the requirements of Classification Societies, in order to earn the shipyards trust. The aim is for shipyards to gradually experience various improvements in costs, delivery times and vessel performance. Almost 90% shipyards want this change, but they want to be able to assume it with guarantees. This is why the Shipyards 4.0 concept is appealing to the shipyards surveyed and interviewed, as it is presented as a set of proposals that integrate different processes and technologies, based on digitisation.

As a final statement, it can be concluded that the shipyards that have participated in this study have predominantly expressed their wish to grow in digitisation and in the implementation of new materials, processes and technologies.

Acknowledgments

The authors thank the shipyards contribution of the shipyards that participated in the survey and in the interviews. They also thank all Fibre4Yards consortium for their generous support for this research.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Correction Statement

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

References

- Belingardi G, Beyene AT, Koricho EG. 2013. Geometrical optimization of bumper beam profile made of pultruded composite by numerical simulation. Compos Struct. 102:217–225. doi: 10.1016/j.compstruct.2013.02.013.

- Boeing Commitment. 2007. Aircraft & Composite Recycling. ENVIRONMENTAL TECHNOTES, 12. https://www.boeingsuppliers.com/environmental/TechNotes/TNdec07.pdf.

- Bolster ED, Cuypers H, Itterbeeck PV, Wastiels J, Wilde WPD. 2009. Use of hypar-shell structures with textile reinforced cement matrix composites in lightweight constructions. Compos Sci Technol. 69(9):1341–1347. doi: 10.1016/j.compscitech.2008.10.028. Special Issue on the 12th European Conference on Composite Materials, ECCM 2006

- Cao Y, Tang X, Zhang T, Chu W, Bai Y. 2023. Fast prediction of turbine energy acquisition capacity under combined action of wave and current based on digital twin method. Sh Offshore Struct. 1–15. doi: 10.1080/17445302.2023.2175962.

- Carral L, Tarrío-Saavedra J, Iglesias G, San-Cristobal JR. 2021. Evaluation of the structural complexity of organisations and products in naval-shipbuilding projects. Sh Offshore Struct. 16(6):670–685. doi: 10.1080/17445302.2020.1773049.

- Chalmers DW. 1994. The potential for the use of composite materials in marine structures. Mar Struct. 7(2–5):441–456. doi: 10.1016/0951-8339(94)90034-5.

- Chawla KK. 2019. Composite materials: science and engineering. Cham: Springer. doi: 10.1007/978-0-387-74365-3.

- Choi M, Kim SH, Chung H. 2017 May. Optimal shipyard facility layout planning based on a genetic algorithm and stochastic growth algorithm. Sh Offshore Struct. 12(4):486–494. doi: 10.1080/17445302.2016.1176294.

- Crosky A, Grant C, Kelly D, Legrand X, Pearce G. 2015 Jul. Fibre placement processes for composites manufacture. In: Boisse P, editor. Advances in composites manufacturing and process design. Woodhead Publishing; p. 79–92. doi: 10.1016/B978-1-78242-307-2.00004-X.

- DNV GL. 2021a. Class guideline. Additive manufacturing - qualification and certification process for materials and components. DNV AS. DNV-CG-0197.

- DNV GL. 2021b. Class programme. Type approval. Additive manufacturing feedstock DNV AS. DNV AS. DNV-CP-0291.

- DNV GL. 2022. Class programme. Approval of manufacturers. Additive manufacturing DNV AS. DNV AS. DNV-CP-0267.

- European Commission. 2021a. FIBRE4YARDS Project. https://www.fibre4yards.eu/.

- European Commission. 2021b. FIBRE composite manufacturing technologies FOR the automation and modular construction in shipYARDS, FIBRE4YARDS Project, H2020, CORDIS, European Commission. https://cordis.europa.eu/project/id/101006860. [accessed 2023 Mar 02].

- Fibregy – Composites for a sustainable environment. 2021. https://fibregy.eu/. [accessed 2023 Mar 02].

- Hayman B, Weitzenböck JR, Noury P, Hayman B, Mcgeorge D, Weitzenböck J. 2002. Lightweight construction for advanced shipbuilding-recent development. https://www.researchgate.net/publication/265101727.

- HOME – FibreShip. 2017. http://www.fibreship.eu/. [accessed 2023 Mar 02].

- Joppen R, Lipsmeier A, Tewes C, Kühn A, Dumitrescu R. 2019. Evaluation of investments in the digitalization of a production. Procedia CIRP. 81:411–416. doi: 10.1016/j.procir.2019.03.071.

- Kafali M, Eren S, Helvacioglu IH, Unsan Y. 2021. A study on sub-work based work package determination methodology for shipyards. Sh Offshore Struct. 17(1):177–187. doi: 10.1080/17445302.2021.1943848.

- Kim SY, Shim CS, Sturtevant C, Kim DDW, Song HC. 2014. Mechanical properties and production quality of hand-layup and vacuum infusion processed hybrid composite materials for GFRP marine structures. Int J Nav Archit Ocean Eng. 6(3):723–736. doi: 10.2478/IJNAOE-2013-0208.

- Kimpara I. 1991. Use of advanced composite materials in marine vehicles. Mar Struct. 4(2):117–127. doi: 10.1016/0951-8339(91)90016-5.

- Mangino E, Carruthers J, Pitarresi G. 2007. The future use of structural composite materials in the automotive industry. Int J Veh Des. 44(3/4):211–232. doi: 10.1504/IJVD.2007.013640.

- MapChart. 2023. https://www.mapchart.net/. [accessed 2023 Mar 02].

- Marsh G. 2003. Material trends for frp boats. Reinf Plast. 47(9):23–26. doi: 10.1016/S0034-3617(03)00931-7.

- Martinez X, Jurado-Granados J, Jurado A, Garcia J. 2021 Jul. FIBRESHIP: A great step forward in the design and construction of lightweight large-length vessels. In: Developments in Maritime Technology and Engineering - Proceedings of the 5th International Conference on Maritime Technology and Engineering, MARTECH 2020. Vol. 1. CRC Press/Balkema; p. 671–675. doi: 10.1201/9781003216582-75.

- Mathijsen D. 2016. Now is the time to make the change from metal to composites in naval shipbuilding. Reinf Plast. 60(5):289–293. doi: 10.1016/j.repl.2016.08.003.

- Meola C, Boccardi S. 2017. Composite materials in the aeronautical industry. Infrared thermography in the evaluation of aerospace composite materials; p. 1–24. doi: 10.1016/b978-1-78242-171-9.00001-2.

- Mouritz AP, Gellert E, Burchill P, Challis K. 2001. Review of advanced composite structures for naval ships and submarines. Compos Struct. 53(1):21–42. doi: 10.1016/S0263-8223(00)00175-6.

- Nieto DM, López VC, Molina SI. 2018 Oct. Large-format polymeric pellet-based additive manufacturing for the naval industry. Addit Manuf. 23:79–85. doi: 10.1016/j.addma.2018.07.012.

- Pohya AA, Wehrspohn J, Meissner R, Wicke K. 2021. A modular framework for the life cycle based evaluation of aircraft technologies, maintenance strategies, and operational decision making using discrete event simulation. Aerospace. 8(7):187. doi: 10.3390/aerospace8070187.

- Ramsses Project: Ramsses Project. 2022. https:www.ramsses-project.eu/ [visited on 2022 Jul 28].

- Sender J, Illgen B, Klink S, Flügge W. 2021. Integration of learning effects in the design of shipbuilding networks. Procedia CIRP. 100:103–108. doi: 10.1016/j.procir.2021.05.017.

- Shenoi RA, Dulieu-Barton JM, Quinn S, Blake JIR, Boyd SW. 2011. Composite materials for marine applications: Key challenges for the future. In: Nicolais L, Meo M, Milella E, editors. Composite materials. London: Springer London; p. 69–89. doi: 10.1007/978-0-85729-166-0_3.

- Tena I, Esnaola A, Sarrionandia M, Ulacia I, Torre J, Aurrekoetxea J. 2015. Out of die ultraviolet cured pultrusion for automotive crash structures. Compos B Eng. 79:209–216. doi: 10.1016/j.compositesb.2015.04.044.

- Veritas B. 2019. Additive manufacturing-guidelines for certification of product made using wire arc additive manufacturing (waam) process. https://marine-offshore.bureauveritas.com/bv-rules.

- Xie N, Zheng S, Wu Q. 2020 May. Two-dimensional packing algorithm for autoclave molding scheduling of aeronautical composite materials production. Comput Ind Eng. 146:106599. doi: 10.1016/j.cie.2020.106599.

- Yoon S-W. 2021 Apr. Advanced composites engineering and its nano-bridging technology. In: Application of composite materials for shipbuilding and marine engineering. WORLD SCIENTIFIC; p. 251–291. doi: 10.1142/9789811235320_0009.

Appendix

A.1. Indexes for the evaluation of the shipyard's technological state

Table

A.2. Table of acronyms

A.3. Survey

Fibre composite manufacturing technologies for the automation and modular construction in shipyards

The European Union has launched the FIBRE4YARDS project, which we believe it may be of your interest.

The main objective of the FIBRE4YARDS project is to maintain the European global leadership in ship building and ship maintenance, through the implementation of the Shipyard 4.0 concept in which advanced and innovative FRP manufacturing technologies are successfully introduced.

This survey aims to find out the present use of composite technologies in European shipyards, and the most interesting technologies that could be applied in the future.

We appreciate your help.

The purpose of the research is related to the objectives of the project ‘FiBRE4YARDS – FIBRE composite manufacturing technologies FOR the automation and modular construction in shipYARDS’. This project has received funding from the European Union's Horizon 2020 research and innovation programme under grant agreement no 101006860.

Personal data will be treated in accordance with the General Data Protection Regulation 2016/679. The information will be used only for the purposes of the above-mentioned project. Responding to this questionnaire confirms that your participation is voluntary and you have been informed about the treatment of your data by the FiBRE4YARDS consortium and you authorise their use. You are entitled to exercise your rights of access, rectification, elimination, limitation, opposition, portability and to not be subject to a decision based solely on automated processing by contacting the corresponding Data Protection Officer of CIMNE via email at the e-mail: [email protected] and consult the privacy policies at http://www.fibre4yards.eu.

As permitted by law, you have the right to be provided at any time with information free of charge about any of your personal data that is stored as well as its origin, the recipient and the purpose for which it has been processed. You can contact us at any time using the address given herein if you have further questions on the topic of personal data.

You are also entitled to lodge a complaint with the competent Data Protection Agencies

| (1) | Do you use composite materials in your shipyard?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (2) | Are you interested in using composite materials in a near future?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (3) | Which of the following composites' manufacturing processes do you use?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (4) | In what processes are you interested? (Skip to question 8)

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (5) | In which field do you apply composite materials?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (6) | Which reinforcement materials do you use?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (7) | Which resins do you use?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (8) | Main types of vessels manufactured at the shipyard, select all that apply

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (9) | Specify the average number of ships manufactured at the shipyard in the last 4 years | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (10) | Specify the average displacement of ships manufactured at the shipyard in the last 4 years per vessel type | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (11) | Total Turnover in EUR in 2020 (the total income of the business generates) | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (12) | FIBRE4YARDS will consider the following technologies. Which of the following would you be interested in?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (13) | What additional technologies do you believe could also be interesting for shipyards? | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (14) | Are you also interested in the design/engineering aspects, or just in the production?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (15) | Do you have your own resources for design/engineering, or do you outsource the calculations?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (16) | Do you currently use direct calculation tools (FEA software) in your production activities?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (17) | Do you currently use specific analysis tools for composites calculations in your production activities?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (18) | If necessary for improving and optimising the production, would you incorporate these tools (or hire the services) in your production activities?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (19) | Fibre4Yards will assess the deployment of Shipyard4.0 concepts in the composites' shipbuilding industry, aiming for a fully interconnected production. Among the different developments we will look into the following aspects. Which ones do you consider more interesting?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| (20) | What additional aspects do you think should be implemented in a Shipyard 4.0? | ||||||||||||||||||||||||||||||||||||||||||||||||||||