?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper evaluates about 146,000 home sales from the Multiple Listing Service (MLS) of Bexar County (San Antonio), Texas, from January 2009 to April 2019 to measure the extent that a home’s selling price reflects a Green premium which is identified in the MLS. We exclude new houses from this analysis. For the span of our data, we find a 4.2% increase in the sale price of Green homes, holding other features constant. When evaluated by Area (approximate selling price quintile), we find premiums of 6.9%, 5.7%, 1.2%, 3.5%, and 5.3% by order of increasing neighborhood value quintile. When assessing Homestead versus Non-Aomestead homes, we find a premium of 2.8% for Homesteads and 6.4% for Non-Homesteads. Considering the time trend, we found the premium starting under 3% in 2009 and increasing to a little over 5% where it remained for three years and decreased to about 4% in 2014 where it remained through the end of the data in 2019.

Introduction

The value which Green features add to real estate is an ongoing area of study both for its own sake and because real estate is long-lived and a large user of energy and water. Houses with Green features may be both more comfortable and exhibit lower operating costs through energy or water efficiency. Increased insulation and multi glazed windows, for example, both increase energy efficiency, will make a home quieter and have less cycling of the heating and air conditioning (HVAC). Water-conserving landscapes may also reduce landscape maintenance time, as well as water bills. Living with a lower carbon footprint, or a Greener lifestyle may add intrinsic benefits to an owner that are not easily measured directly through energy and water saving, or less maintenance time or more home comfort. All these effects can add Green value to a home. In the fall of 2008, the San Antonio Board of Realtors® Multiple Listing Service (SABOR MLS) added fields for listing agents to specify Green features, Green certification, and energy efficiency measures. If one or more notations were in these fields, for this paper, we set a Green indicator variable to the value one to analyze its effect on the sale price.

Literature Review

We conceptualize the literature as follows: (1) Is green important to real estate? (2) Do people indicate a willingness to pay for green in real estate? (3) How large is the premium for green features in residential real estate? Turning first to the matter of is it important, Ciochetti and McGowan (Citation2010) summarize information from the U.S. Energy Information Administration that shows the largest user of energy in the U.S. is buildings at 41% of total consumption. They also show that the square footage of residential real estate far exceeds that of commercial buildings, and although they use less energy per square foot, in total, they consume the most energy. Sewalk and Throupe (Citation2014) examine the costs in Denver to bring existing homes up to current energy efficiency standards and find the costs exceed the projected benefits. They also find, however, that adding insulation and using energy-efficient appliances and lighting when replacing the current items is cost-effective.

Considering the second question of whether people are willing to pay a premium, Goodwin (Citation2011) studied the demand for Green amenities and determined that buyers of new homes are more interested in Green amenities than those purchasing resales. She also found buyers under age 40 and buyers with incomes over $100,000 were less interested in Green features. Levinson (Citation2016) questions why residential building energy codes never save the amount of energy that the codes predict. He states, “Plus, new and old buildings might use similar amounts of energy today because residents of efficient houses respond to the lowered cost of lighting, air conditioning, and heating by using more: the so-called “rebound” effect. In that case, the codes may make homeowners warmer in winter and cooler in summer but not save as much energy as promised.” This result does not mean owners do not value the Green improvements. Owners may make improvements on existing structures that could exceed requirements. Those who prefer to keep their homes very warm in winter and very cool in summer may use much energy and value Green improvements highly as the financial consequences of their comfort is dampened.

Exploring the answer to the third question is the crux of this paper—“How is Green valued in the residential single family market?” This is an essential question for residential real estate appraisers, real estate agents, and developers. One approach to addressing this question, when there are direct dollar savings, is to take the present value of these savings as an estimate of the increased value. Adomatis (Citation2010), for example, outlines this approach in a residential context. She follows this up with a more comprehensive paper describing a more extensive set of Green improvements (Adomatis, Citation2012). This study, however, like a number of previous studies, seeks a direct measure of the increase in sales price from green features. summarizes eight papers that have directly addressed this question. This table notes the paper, the location and study objective, the data sample, and the green premium that is measured. Green premiums were measured in the 2.5-5.9% for most of these papers.

Table 1. Summary of recent studies of the green sales premium in residential real estate.

Research Questions and Hypotheses

The papers noted in address the value green brings to residential real estate. Ma and Narwold (Citation2019) found that to detect a premium for the value of house orientation they had to limit their sample to higher valued houses, using the sense that for tract houses on small lots, orientation is not an important concern to purchasers. They found the largest values when they restricted their results to custom houses on large lots. We propose a much simpler approach that addresses a related question—is the value of green dependent on the average house value in the neighborhood the house is sited in?

Our second extension to existing research is to determine whether the value of green depends on whether sale if by owner occupant or not. To our knowledge this question has not been addressed in previous research. Our third extension follows Aroul and Rodriguez (Citation2017) in addressing whether green values change over time. Our first extension of Aroul and Rodriguez is to pick up, time wise, where they leave off and to continue to a more recent date. We have a longer time horizon to address this question. We also address whether the Green Area effect and Green Homestead effect is stable over time. In summary this paper addresses whether the green premium varies among neighborhood value quintiles (Area), varies by homestead status at time of sale, or varies over time. We do not have strong priors regarding any of these research questions and thus our research hypotheses are general.

Hypothesis 1. The Green premium is the same (percentwise) among value stratified neighborhoods.

Hypothesis 1A: The Green premium is not the same (percentwise) among value stratified neighborhoods.

One could conjecture that in lower priced neighborhoods incomes are constrained so that anything that lowers housing costs (such as energy efficiency) will be highly valued and capitalized into the selling price of the house. For high priced neighborhoods, costs savings could be less than important the psychic benefits from living a greener lifestyle for those who have the means and choose to own houses with green features. It is also possible that for house purchasers for whom green is important, their actions will create a green premium that is similar across neighbor value. To test this hypothesis, we segment the MLS neighborhoods into approximate value quintiles (Areas) to determine whether the premium varies by Area.

Hypothesis 2: Green premium does not vary by the ownership status of the house being purchased.

Hypothesis 2A: Green premium varies by the ownership status of the house being purchased.

Home purchasers may not be aware of the ownership status when purchasing, but the ownership may affect the combination of features the house offers which may affect the green premium. We evaluate this hypothesis by determining the homestead status of the house at the time of sale and evaluating the premium for Homestead versus Non-Homestead status.

Hypothesis 3: Green value is constant over time.

Hypothesis 3A: Green value is not constant over time.

Although recognizing green value is not new, our data starts in 2009 when green may have been coming into its own. Aroul and Rodriguez (Citation2017) end their data in 2009 and showed an increasing trend over time that was leveling off by the end of their data. While the green premium cannot increase indefinitely it could fluctuate over time. Also, just prior to 2009 is when the MLS used in our study added the new green fields to the database, so there may be a period for real estate agents to become familiar with the new fields and to employ them when listing a house for sale. This could affect our results in the early period. An additional possibility is that green may be more, or perhaps less, important in a flat real estate market, as was observed after the great real estate recession brought on by the subprime mortgage crisis. As markets returned to full health a wider spectrum of houses may be on the market which could affect the value of green. Another possibility is that green could be somewhat of a fad, and have some short lived value, or it could show some shorter term excitement (high value) before settling in at a long term value. Overall we remain agnostic as to what the analysis will show. To test for any time trend, we run annual regressions on the data to determine whether the value of green changes over time. We also run regressions on Area and Homestead status over time to determine whether Green premiums related to these measures are constant over time.

Data

Our data is primarily drawn from the San Antonio Board of Realtors® Multiple Listing Service (SABOR MLS). This provides the sale price, date of sale, the time on market, and associated information about the house and other potentially relevant information regarding the sale, such as source of financing. Three new fields were introduced into this data set in October of 2008, and it is from these new fields we extract our green identifier. These new fields are labelled “Green Designations,” “Green Features,” and “Energy Efficient Features.” Using earlier data, Cadena and Thomson (Citation2015) evaluated these fields and found that parsing this data into one “Green” identifier provide the most consistent result. We follow this approach and if there is an entry into any of these fields we set the Green identifier to one. Cadena and Thomson reported that almost 97% of new homes exhibit Green features; thus, we exclude new homes from the analysis presented here. Given that distressed properties may not fully reflect the values of typical transactions, we also removed short sales and foreclosure sales from this analysis.

To investigate the green premium for homes designated as the owner’s principal residence at their time of sale compared to other homes (primarily rental units) we required a second data source. In the State of Texas, a homeowner may declare their primary residence a homestead.

There are no specific qualifications for the general homestead exemption other than the owner has an ownership interest in the property and uses the property as the owner’s principal residence. However, an applicant is required to state the applicant does not claim an exemption on another residence homestead inside or outside of Texas.Footnote1

Homestead status adds legal protections to the property that non-homesteads do not enjoy. More important for most homeowners, however, is that if they declare homestead status to the local appraisal district, they receive some mandated property tax relief. The amount of relief in taxes varies by taxing jurisdiction, as the dollar amount of an exemption may vary for a school district, city, or other taxing authority. In Bexar County, the annual property tax savings will typically be in the $200–400 range per year. In times of rapidly increasing property values, declared homesteads are limited to an annual increase in taxable value of 10%, which may provide further property tax relief due to the homestead declaration. In addition, homeowners over 65 or disabled qualify for additional property tax relief. These financial benefits provide a strong incentive for homeowners to declare their primary residence as a homestead. To aid in this process, a notice is sent with the property tax appraisal to new owners informing them that, if they qualify, they may apply for the homestead exemption.

Non-homestead declared houses generally fall into one of three categories: (1) Rental Property, (2) Second Home Property, or (3) Owner-occupied principal residence that did not apply for the homestead exemption. Because of the adverse financial consequences of (3), we expect few properties that qualify for the homestead exemption would fail to apply for itFootnote2. We assume most non-homestead homes are rental properties, and this to be especially true in the low and moderate house price areas where the localized economic profile may prevent a high proportion of homeowners.

We were able to purchase Bexar County Appraisal District data for the period of our analysis that allows us to determine the homestead status of each property on January 1 of each year. For every sale, we were able to cross-reference its homestead status using this data and merge this into our home sale data set.

We examined our data for nonsensical values and other coding errors and removed these observations from our data. Extreme outliers in terms of house price or size, are not cogent to this analysis and were also eliminated. presents the descriptive statistics for our data. House prices in our dataset range from $20,000 to $2,000,000 with an average selling price of $207,000; size ranges from 300 to 12,000 square feet with an average size of 2,100 square feet; and age ranges from two to 143 years with an average age of 27 years. Because some new homes are completed near the end of the year and sold the next, they are computed (Age = Year Sold – Year Built) to be 1-year-old when they are in fact new; thus, we start our analysis using home computed to be at least 2 years old. Overall, in our data, 35% of sales are designated Green and 55% are Homesteads. The average time on market (TOM) is 73 days (0.199 years). We present many covariates that describe the house such as size, age, number of bathrooms, garage spaces, indicator for single story and whether or not it has a swimming pool. We provide further information about the house including exterior cladding, style, type of roof, HVAC, flooring, and foundation. Also included is other information related to the transaction such as whether the house had a recent rehab, needs tender loving care, was vacant or leased, whether it was part of a required home owner association, whether it was broker or agent owned, and how the sale was financed. For attributes described via several indicators such as flooring, HVAC, or financing, the most common indicator is not reported and its effect will be part of the regression intercept.

Table 2. Variable names and descriptive statistics (N = 145,983).

To study whether green has the same value across neighborhoods, we grouped the 49 MLS recognized neighborhoods by ranking their average sales price and then created approximate quintiles based on the average sale price, which we refer to as Areas. Because we wanted to retain as many observations as possible in each area we did not employ any formal clustering analysis, but instead used the straightforward procedure of grouping neighborhoods by average selling price. presents some descriptive data about these areas illustrating there remains a large range of sale prices, but the mean and median are distinct among areas. We also see that green is more common in the higher valued Areas (though this paper addresses its value rather than its frequency) and that homestead homes are also more common in the higher value areas. The average sale price, by approximate quintile is: Area1=$115,000; Area2=$151,000; Area3=$184,000; Area4=$272,000; and Area5=$345,000. While this table shows both homestead and green frequency, it does not show their interaction. While Green is 35% of all data, Green is present for 26% of Non-Homesteads and 42% of Homesteads.

Table 3. Summary information for approximate value quintile areas.

Methods

Valuation of residential properties and the features that add or subtract to their value is an ongoing topic of interest in real estate. Following an influential early paper on hedonic valuation by Rosen (Citation1974), a hedonic approach to valuation has taken hold in real estate. Rosen (Citation2002) in his section on interpreting the implicit value of characteristics, states “The hedonic regression method regresses product prices on product characteristics…. In land and housing markets, site and structure prices are regressed on house attributes (size, architectural style, and age) and on-site characteristics…”) Malpezzi (Citation2003) and Chin and Chau (Citation2003) review hedonic house pricing studies and summarize their structure and their applications to locational, structural, and neighborhood factors that influence housing values. Herath and Maier (Citation2010) reviewed 471 papers that address hedonic price models for real estate and housing studies. They note that 178 of these consider neighborhood factors and a further 16 consider property characteristics. Dastrup et al. (Citation2012) note, “In reality, homes are differentiated products that differ along many dimensions. No home has a ‘twin.’” Hedonic pricing models were employed for most of the literature previously noted where the value of Green characteristics was estimated.

We employ a series of standard hedonic pricing models similar to those used other in real estate valuation research. Some of our models disaggregate our data by year. Our model uses the semi-log form:

(1)

(1)

where: Ln(Sale Price)i is the natural log of the House Sale Price; Gi is a Green indicator value; Ai is a vector of Area neighborhood value quintile indicators (Areas); Hi is an indicator of homestead status. CVi is a vector of control variables frequently used in hedonic real estate studies. Mi is a vector of monthly indicator variables to capture time trend in value.

As is common in such models, we use the Log of Sales price, rather than Sales price as the dependent variable. By using the log of house price, we can interpret indicator variable coefficients as the percentage effect on sales prices; thus, the results apply across a spectrum of home prices. If a Green coefficient is 0.05, it means when the green feature is present, the house will sell for about 5% more. We estimate our models using Ordinary Least Squares regression.

Because Green features may be part of several features common to high -quality houses, we constructed an extensive set of control variables to prevent the Green indicators from simply indicating a highly valued house. If we simply compare the average price of houses with some type of Green feature to the average price of those without, we find the Green homes sell for approximately 27% more than houses without Green features ($248,000 v. $186,000). Green homes are larger (2340 square feet v. 1980) and newer (21.3 years v. 29.5 years), which in part describes their higher sale value. This quick check illustrates the need to have a complete set of covariates to isolate the Green effect from other desirable features a house may exhibit.

There has been some discussion regarding hedonic model specification. Pride et al. (Citation2017) note that the hedonic framework has been criticized. They state that Chin and Chau (Citation2003) note they are often misspecified by either including irrelevant variables or omitting relevant variables. Hedonic models will not include everything that may affect house value, so a reasonable question is whether this leads one astray in making inferences. Butler (Citation1982) states,

The purpose of this paper is to fill part of that gap by examining briefly the theoretical and empirical parameters of an ‘approximately correct specification,’ and to present some evidence that approximate correctness can be achieved with significantly fewer characteristics than is generally supposed… . Given that the arguments of the hedonic function must be limited to housing characteristics, the natural next question is: which housing characteristics? In principle, all characteristics relevant to the determination of market price-i.e., those that both yield utility to residents and are costly to produce- should be included. In practice, this cannot be done because the number of such characteristics is unmanageably large. Data on many of these are either unavailable or of exceedingly poor quality.

Butler estimates a hedonic model with four covariates, and another that adds six additional covariates for which three are not statistically significant. He then analyses the modeled pricing errors with both models and concludes that either model works well. Butler does not try to make inferences about how accurate the assessment of the effect of each of the covariates is—which is what we wish to do in this study. In other words, the purpose of this study is not to determine whether we accurately predict selling price overall, but in estimating an accurate measure of the Green premium.

We examine whether the inclusion of a large number of housing characteristics matter for accurately estimating the Green premium. We first employ a “Basic” model to estimate the Green premium, and then estimate with our full model that includes many more covariates. We provide results that demonstrate that without a deeper level of control variables, the value to Green could be substantially overestimated.

Two other potential concerns are considered here. One is that Green, to the extent it is a desirable feature may be highly correlated with other desirable features leading to imprecise measures of the Green effect. A way to detect whether this correlation is a problem is through the Variance Inflation Factor (VIF). The VIF’s are reported along with the parameter estimates and they are low for our green estimates in all models presented (never higher than 1.9) so collinearity is not deemed a concern for the reported results.

A second concern is that Green is also known to affect time on market (TOM); thus, time on market should be controlled for in our models. When possible, this would be corrected via a 2-stage approach. We estimated a time on market model and used it to create a predicted time on market to use as a covariate in our models. The VIF was above 160 for this variable when it was included in our estimated model; therefore, we include the actual time on market as a covariate and results presented in and show its VIF is low (less than 1.7).

Table 4. Ordinary least squares regression results summary for basic model.

Table 5. Ordinary least squares regression results summary for full model.

Results

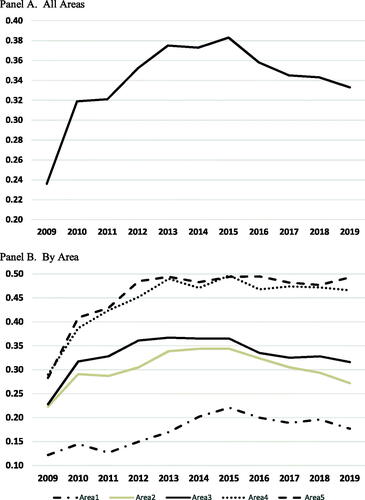

Thirty-five percent of our sales exhibit the Green indicator. Looking more closely, we find () that in our first year of data, about 23% of sales had a Green indicator. This presence increased through 2015 when it reached 38% of sales before dropping to about 34% of sales. It may be that it took a few years for real estate agents to take advantage of the Green fields in the MLS, leading to the increase in Green identified houses after the early data period. Our data shows the average age of home sales increasing over the decade. Our data also shows that older houses are less likely to be Green. The combination of these facts may explain the small downward trend in Green in more recent years.

Figure 1. Proportion of sales with Green Indicator by year. Panel A. All Areas. Panel B. By Area.

, Panel B, disaggregates the annual data by neighborhood value quintile (Area). We note here that the median age of sale is highest in Area1 (44 years) and shows lower values for the other quintiles (24, 27, 20, 23 years). We have already noted that Green is more common in newer homes. The lowest valued quintile (Area 1) shows the lowest proportion of Green sales—starting at about 12% and increasing through 2015 after which it levels at about 20% of sales. Area2 and Area3 start about 22%, increase to about 35% and then fall to about 30%. Area4 and Area5 start out about 30% and increase to about 50% by 2013 where they remain.

We begin our hedonic regression analysis with a set of house characteristics commonly used in such models, plus neighborhood value quintile indicators, and month of sale indicator variables (Basic Model). shows that for this model with the full 145,983 observations, the Green coefficient is 0.082 (p < 0.0001), and the Adjusted R-square is 0.778, demonstrating this model explains much of the variation in sale price. TOM is a statistically significant variable (homes that sell quicker sell for more), as are all of the included covariates. An innovation in this paper is to evaluate the homestead effect for green, so it is useful to note that the Homestead parameter estimate is 0.06 demonstrating that Homestead houses sell for more than Non-Homesteads. The highest variance inflation factors (VIF) are for house size and number of bathrooms. It is reasonable to expect that larger houses will have more bathrooms. We computed the correlation between these two variables as 81%. Our goal in this paper is not to separate the influence of square feet versus number of bathrooms so the somewhat higher variance inflation for these variables is not a concern for this paper.

To begin assessing our first hypothesis, that is, to determine whether the green effect is constant by neighborhood value quintile, we interact the Area variables with the Green variable to create five green by area variables and rerun our regression including these in place of the single Green variable. These results, presented as Panel B , shows Green is most valuable in the lowest valued neighborhoods (near 17%) and lowest in the middle quintile area (about 5%). The other Area quintiles show a Green premium of about 6-11%.

To address our second hypothesis, the value of green by homestead status, we run a model that interacts the Green indicator with homestead status. , Panel C estimates that Non-Homesteads show a Green effect of 12.5% while Homesteads show a 5.5% green premium. This Green-Homestead premium is in addition to the estimated 8.3% premium noted for a Homestead. These results give us our initial conclusions that green is valuable, that green varies by value quintile, and that green varies by homestead status.

As shown in , we have a large set of housing attributes we can incorporate to better specify the determinants of house prices. presents the regression results which includes our complete set of covariates (Full Model) using the complete time span of the data. The increase in Rsquare for the Full Model demonstrates increased explanatory power (Adjusted Rsquare = 0.849 vs 0.778 for the Basic Model). These result shows the direction and magnitude the additional covariates housing attributes contribute to value (monthly indicator variables are not included in the table). Comparing the parameter estimates of the Full Model to the Basic Model we see the Full Model dampens the effect of the covariates of the basic model—in other words, each covariate in the Basic Model seems to be pulling more than its true weight as measured in the Full Model. Two variables that have large dampening in the Full Model are Green and Homestead—both of which fall by half. Examining the confidence intervals for the green measures for the corresponding Basic and Full model we observe they do not overlap. An exception to this dampening is TOM - the TOM effect is accentuated (from −0.010 to −0.026) in the Full Model. Given that many desirable factors may be correlated with the desirable Green feature we examine its VIF and see that it remains low (1.098 in the basic model vs. 1.164 in the full model) indicating that collinearity does not appear a problem in estimating the green parameter using the Full Model. Given that adding covariates has reduced the measured Green premium, we surmise that the Green covariate was measuring, in addition to the Green premium, a premium for other desirable factors correlated with green. All results from this point forward refer to the Full Model.

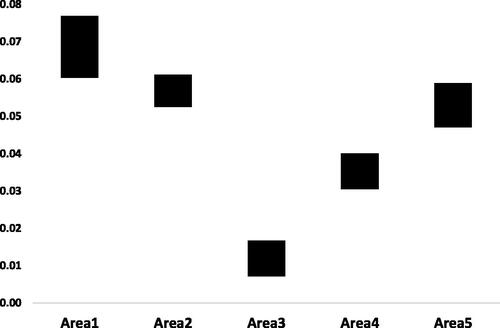

Our first hypothesis addresses whether the green affect varies by neighborhood. To test we ran the Full Model with each neighborhood interacted with the Green indicator to determine if there is a neighborhood green effect. Panel B presents the regression results for these results. The Green premium is highest in the lowest value quintile (Area1) at almost 7%. The effect is not monotonic by value quintile. The rank order is; Area1 (6.9%), Area2 (5.7%), Area5 (5.3%), Area4 (3.5%), Area3 (1.2%). Examining the Confidence Intervals, we see that Area1 and Area2 are not statistically different and Area 2 and Area 5 are not statistically different. Area3 and Area4 are statistically different than the other Areas. To visualize the area effect, plots the confidence intervals by Area. Overall we can conclude that the green effect is highest in Area1, Area2, and Area5 and weaker in Area4 and weakest in Area3. If graphed, the coefficients show a U shape with lower values in the middling value quintiles. We reject our null hypothesis that there is no difference in Green premium by Area as there are non-overlapping confidence intervals as illustrated on .

Figure 2. 95% Confidence Intervals for Green Premium by Area from Panel B.

Our second hypothesis regards whether the green premium depends on homestead status. We interact the Green indicator with Homestead to create two variables to capture green effect by homestead status. The results, presented in Panel C show a show that Non-Homestead homes have a much higher Green premium, 6.4%, while Green Homesteads show the lower 2.8% figure. Examining the confidence intervals shows this is a statistically significant difference which leads us to reject our null hypothesis that there is no difference by ownership status. We can only conjecture the reason for this strong result. Sellers of Non-Homestead properties may choose to distinguish their properties versus other Non-Homestead properties through their green investment, knowing green is less common in Non-Homestead properties.

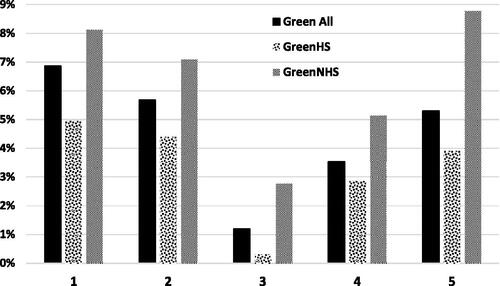

A logical extension to the area and homestead effect is to see whether the homestead effect has a similar affect across areas. For this we interact Homestead, Area, and Green to split the green indicator into 10 categories. We add control variables of homestead by area to better evaluate the green effect by area by homestead. Panel D presents the results. Turning first to Area1, we find Non-Homesteads have a higher green coefficient (8.1%) than for Homesteads (5.0%). This result confirms the large green premium for Area1 and that Non-Homesteads have the larger premium. The confidence intervals for these estimates do not overlap demonstrating a statistically significant difference by homestead status. Moving to Area2 we find a premium of 7.1% for Non-Homestead and 4.4% for Homesteads. Once again the confidence intervals do not overlap showing there is a statistically significant green premium for Area2 by homestead status. For Area3, Non-Homesteads show a 2.8% Green premium, while the premium for Homesteads at 0.3% is not statistically different from zero. Their confidence intervals do not overlap. This is the only disaggregation thus far that finds no green premium. For Area4 and Area5 the results tell the same story that Non-Homesteads have a statistically larger Green premium than Homesteads. To visualize these results, plots the Green Premiums by area for all data, and disaggregated by Homestead status. The U shape is observed for all specifications across area.

Figure 3. Green Premium by Area by Homestead Status. Regression Coefficients from Panel B and Panel D.

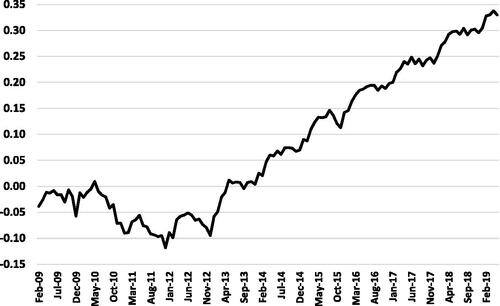

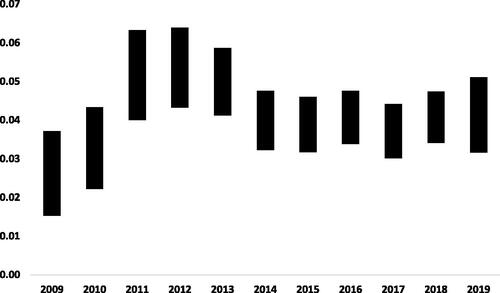

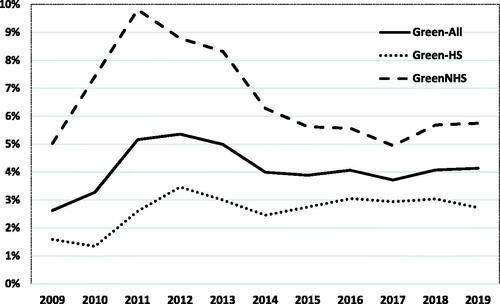

Our third hypothesis was to examine whether the Green premium was constant over time. One reason we do so is that market conditions may have changed over the period, or consumer demand for Green attributes may have changed. To demonstrate the change in market conditions over time, plots the monthly indicator variables that are not reported in Panel A. The results reflect the relatively mild Texas effect of the great recession followed by robust recovery beginning in 2013 and continuing through the remainder of the data period. To evaluate a time trend in Green valuation, we ran a series of three regressions, for each of our eleven data years and report Green measures of interest in . The first regression uses a single Green indicator variable. , Panels A - K shows the results by year. In all cases the Green variable is statistically significant, though the estimated coefficient varies over time. From we see the Green premium rose from less 3% in 2009 to about 5% for the 2011–2013 period, which roughly corresponds with the period where house prices did not rise. To quickly visualize this change over time, the 95% Confidence Intervals for the Green premium are plotted on . Our point estimate for all years, 0.042, would pass through all of these confidence intervals, except for 2009 when it would be above the confidence interval, and for 2012 where it would be below the confidence interval. If we consider the confidence interval for all years combined of 0.039–0.045 we note it would touch the annual confidence intervals for all years except for 2009. So we must accept the Hypothesis 3 in that there is not a statistically significant time trend after 2009. For the years after 2014 the Green Premium remained about 4% and the confidence interval is quite stable through the beginning of 2019, where our data ends.

Figure 4. Monthly Indicator Variables for Regression Model reported in .

Figure 5. Confidence Intervals for Green Premium by Year. Confidence Interval Regression Results from , Panels A–K.

Table 6. Ordinary least squares regression results summary for full model by year.

, in addition to the point estimate for Green premium each year, also plots the results interacting Green with Homestead to determine whether the homestead effect is similar over time. This figure plots the GreenHomeStd and GreenNotHomeStd regression coefficients presented in , Panels A–K. The trend result is the same each year—Non-Homesteads have a higher Green Premium. Examining the confidence intervals by year, we find this difference is statistically significant in every year.

Figure 6. Green Premium by Year by Homestead Status. Regression Coefficients from , Panels A–K.

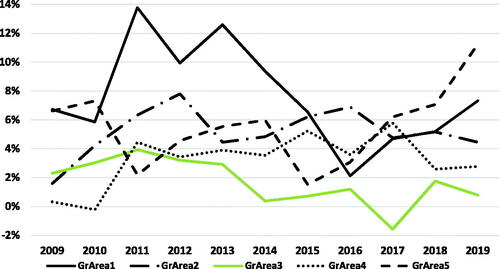

Finally, we address whether the Green premium difference by Area remain constant over time. The regression coefficients are presented in Panels A–K. There are numerous regression coefficients presented in this table so we plot the coefficients to more easily assess their stability over time. presents this result. A cursory look at shows the Green by Area affect does change over time as the coefficients do not rise and fall in unison over time. Some outcomes can be gleaned from studying the plot and the table. Area1 showed the highest Green Premium for the combined data. Disaggregating it by year shows that there were 5 of the years where its premium was highest (2011, 2012, 2013, 2014, 2015), but only 2 years where it was statistically higher (2011, 2013) than all other Areas. Area3, which showed the lowest Green premium for the entire data set showed the lowest Green premiums from 2012 through the end of the data, but this result was not statistically different from other Areas. With the exception of 2018, it did not show a statistically positive coefficient after 2013. And, for 2017 it presented the only statistically negative coefficient in our analysis. Area4, which showed the second smallest green premium using the entire data, shows a coefficient not statistically different from zero for the first two years, and then seems to settle to about 4%. Overall there is substantial variation in the Green premium by Area result when disaggregated by year.

Figure 7. Green Premium by Year by Area. Regression Coefficients from , Panels A–K.

Conclusions

Houses with Green characteristics include energy and water savings, enhanced comfort, and potentially increase an owner’s sense of environmental responsibility—all of which should add value to a home. The analysis presented here measures a statistically significant increase in the sale price for properties with Green characteristics. For resale properties, with just over a decade worth of data, we find Green property sells at a 4.2% premium to otherwise identical properties.

Our goal in this paper was to use our extensive database to more deeply probe the value of Green. In particular, we address the Green premium by Area (approximate neighborhood value quintiles), homestead status, and time trend. When we disaggregate by Area, we find that the lowest value neighborhoods showed the greatest value premium from Green (almost 7%), and the median value neighborhoods provided the lowest premium (about 1.2%). Other neighborhoods provide a Green premium in the 3.5–5.7% range. When we disaggregate the result between Homestead and Non-Homestead, we find that Non-Homestead homes have a larger Green premium of 6.4% versus the 2.8% Green premium of Homestead homes. When we disaggregate the Green premium by Area and Homestead, the estimated Green Premium for Homestead homes in the middle value neighborhoods is not statistically different than zero.

We find that at the beginning of our data period (2009) the Green premium was 2.6%. It rose as high as 5.4% in 2012 and then settled on a value of about 4% from 2014 through the end of our data period. While the point estimates varied by year, the confidence intervals for most years overlapped so we cannot reject the null hypothesis that the Green premium was stable after 2009. When we evaluated the Green premium by year for Homestead and Non-Homestead homes, the Non-Homestead homes showed a statistically significant higher premium over Homestead homes in every year. When we examined the Area effect by year, we found the results were unstable on a year to year basis. Overall, we find a significant and enduring Green premium in resale residential real estate that we estimated at 4.2% of sales price over our entire data.

While this paper has extended the literature on the value of green in residential real estate, it has limitations. The data is from South Texas so the results may be more applicable to warmer climates than colder ones. The novel analysis here, including effect of value quintiles and ownership status, would benefit from confirmation in other locations and datasets. This paper notes how the model specification and depth of data affects the magnitude of the measured green effect. Should covariates that were unavailable in our data be correlated with the green variable it is possible that our green measures lack precision. The Variance Inflation Factors for our green estimates are all below 2.5 which indicates that collinearity with our covariates are not unduly affecting our estimated green measures.

Notes

1 Texas Comptroller of Public Accounts Publication #96-1740 February 2018.

2 For some high-end properties, a homeowner, for privacy reasons, could chose to the hold the home in an entity that does not qualify for homestead. In such cases presumably the owner believes that privacy is more valuable than the property tax savings and other protections.

References

- Adomatis, S. K. (2010). Valuing high performance houses. The Appraisal Journal, 78, 195–201.

- Adomatis, S. K. (2012). Describing the green house made easy. The Appraisal Journal, 80 (Winter), 21–29.

- Aroul, R. R., & Hansz, J. A. (2011). The role of dual-pane windows and improvement age explaining residential property values. Journal of Sustainable Real Estate, 3(1), 142–161. https://doi.org/https://doi.org/10.1080/10835547.2011.12091822

- Aroul, R. R., & Hansz, J. A. (2012). The value of “green”: Evidence from the first mandatory residential green building program. Journal of Real Estate Research, 34(1), 27. 49. https://doi.org/https://doi.org/10.1080/10835547.2012.12091327

- Aroul, R. R., & Rodriguez, M. (2017). The increasing value of green for residential real estate. Journal of Sustainable Real Estate, 9(1), 112–130. https://doi.org/https://doi.org/10.1080/10835547.2017.12091894

- Bloom, B. C., Nobe, M. C., & Nobe, M. D. (2011). Valuing green home designs: A study of ENERGY STAR® homes. Journal of Sustainable Real Estate, 3(1), 109–126. https://doi.org/https://doi.org/10.1080/10835547.2011.12091818

- Butler, R. V. (1982). The specification of hedonic indexes for urban housing. Land Economics, 58, 94–108. https://doi.org/https://doi.org/10.2307/3146079

- Cadena, A., & Thomson, T. A. (2015). An empirical assessment of the value of green in residential real estate. The Appraisal Journal, Winter, 83, 32–40.

- Chin, T. L., & Chau, K. W. (2003). A critical review of literature on the hedonic price model. International Journal for Housing and Its Applications, 27(2), 145–165.

- Ciochetti, B. A., & McGowan, M. D. (2010). Energy efficiency improvements: Do they pay? Journal of Sustainable Real Estate, 2(1), 305–333. https://doi.org/https://doi.org/10.1080/10835547.2010.12091807

- Dastrup, S. R., Zivin, D. C., & Kahn, M. E. (2012). Understanding the solar home price premium: Electricity generation and “green” social status. European Economic Review, 56(5), 961–973. https://doi.org/https://doi.org/10.1016/j.euroecorev.2012.02.006

- Goodwin, K. R. (2011). The demand for green amenities. Journal of Sustainable Real Estate, 3(1), 27–41. https://doi.org/https://doi.org/10.1080/10835547.2011.12091827

- Herath, S. K., & Maier, G. (2010). The hedonic price method in real estate and housing market research. A reviewq of the literature. In Institute for regional development and environment (pp. 1–21). University of Economics and Business.

- Levinson, A. (2016). How much energy do building energy codes save? Evidence from california houses. American Economic Review, 106(10), 2867–2894. https://doi.org/https://doi.org/10.1257/aer.20150102

- Ma, A., & Narwold, A. (2019). Which way is up? Orientation and residential property values. Journal of Sustainable Real Estate, 11(1), 40–59. https://doi.org/https://doi.org/10.22300/1949-8276.11.1.40

- Malpezzi, S. (2003). Hedonic pricing models: A selective and applied review. In T. O’Sullivan, K. Gibb, & M. A. Malden (Ed.), Housing economics and public policy (pp. 7–89). Blackwell Science.

- Pride, D. J., Little, J. M., & Mueller-Stoffels, M. (2017). The value of energy efficiency in the anchorage residential property market. Journal of Sustainable Real Estate, 9(1), 172–194. https://doi.org/https://doi.org/10.1080/10835547.2017.12091897

- Rosen, S. (1974). Hedonic prices and implicit markets: Product differentiation in pure competition. Journal of Political Economy, 82(1), 34–55. https://doi.org/https://doi.org/10.1086/260169

- Rosen, S. (2002). Markets and diversity. American Economic Review, 92(1), 1–15. https://doi.org/https://doi.org/10.1257/000282802760015577

- Sewalk, S., & Throupe, R. (2014). The fesibility of reducing greenhouse gas emissions in residential buildings. Journal of Sustainable Real Estate, 5(1), 35–65.