?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The G20 made a commitment to adopt financial inclusion as a major support towards the achievement of its 2030 Agenda for Sustainable Development of all member countries. Specifically, the sustainable development goals of employment creation, hunger elimination and poverty reduction would be addressed when those in the informal sector are captured into mainstream finance. This study investigated how financial exclusion impairs inclusive drive of 27 sub Saharan African countries using secondary data sourced from World Bank database for 10 years (2007–2017). Granger Error Correction Method (ECM) with General Methods of Moments (GMM) of Arellanon and Bond (1991) were used to analyse the short panel data obtained from the World Bank database. The ECM test result found evidence of a long-run relationship, however, in the short-run, there is an insignificant but positive relationship between financial inclusion and exclusion with values recorded at 0.33, 0.37 and 0.32 for low, moderate and high financial stable countries, respectively. This implies that, there is no correlation between financial inclusion and financial exclusion (proxy by unemployment) in the three sets of countries sampled. However, for the moderately stable financial system, exclusion has negative long run multiplier impact on inclusion. The study therefore recommends policies that could sustain and improve employment rate in poorly and highly stable financial system.

PUBLIC INTEREST STATEMENT

Financial inclusion has been in the front burner of public discourse in recent times. Most government and international financial institutions as well as donor agencies have made frantic commitments towards achieving an all-inclusive growth that will enable the poor and downtrodden have access to credit and financial instruments that will enable them to lead a normal and fulfilled life. The G20 leaders, World Bank and other supranational institutions reached a consensus in 2015 to adopt financial inclusion as a veritable platform for driving the SDGs of hunger and poverty eradication, gender equality as well as unemployment reduction by 2030. It is expected that increase in barriers to inclusion will hinder the various SDGs of hunger elimination, employment creation and poverty reduction. It is on this premise, this study examined the nexus between financial exclusion, represented by unemployment and financial inclusion of the poor into mainstream finance.

1. Introduction

In 2015, the United Nations (UN) general assembly set seventeen Sustainable Development Goals (SDGs) that will be achieved by 2030 by member nations. The post-2015 Development Agenda squarely puts financial inclusion as a key objective for UN member countries to address SDGs of hunger elimination, wealth or employment creation, and poverty eradication (Christine, Citation2016). The same year, the World Bank set out a global challenge of Universal Financial Access (UFA) to capture unbanked citizens without any formal financial access by the year 2020. The goal of the UFA is to ensure that every bankable adult owns an account with which to carryout basic financial transactions as a bedrock towards managing their financial lives (Universal Financial Access Report, Citation2017). The International Bank for Reconstruction and Development (IBRD), African Development Bank as well as the G20 Leaders have all made various commitments to capture more persons into mainstream finance and to remove all barriers preventing women from gaining access into the formal financial sector to increase their investment opportunities as well as reduce gender inequality (Aguera, Citation2015). Expectedly, achieving financial security and wellbeing by all economic agents will be a herculean task if the barriers to financial inclusion (exclusion) continues to widen as a result of unemployment, low income, poverty, loss of job, distance to point of financial service, harsh economic situation, high cost of fund, lack of trust in the financial products and institutions as well as other socio-cultural and religious barriers. In view of the above statement, this study examined how unemployment could be reduced by capturing unemployed persons in the informal sector into mainstream finance.

Poverty cannot be eradicated completely when a larger percentage of the populace continuously and persistently live and work within the informal financial environment that does not guarantee access to cheaper and adequate financial instruments that will help them build wealth and sustainable financial security for themselves and family, (Anyanwu and Anyanwu, Citation2017). According to the Global Findex report for 2017 as cited in the Small Scale Sustainable Infrastructure and Development Fund (S3IDF) report, India recorded high bank account ownership with about 48 percent of such account being inactive for the past twelve months (S3IDF, Citation2018). This is a typical case of secondary exclusion, which exposes the weakness in using access through ownership of bank account as an indicator for financial inclusion. Likewise, in the United Kingdom (UK), about two million persons are unbanked while three million persons could not attract credit facilities from the formal financial system, half of the individuals in the poor households have no contents insurance (Blake and De Jong, Citation2008).

When individuals, families and society at large are financially excluded, it lowers their self-esteem and disrupts families’ programmes and normal lives. This will further expose the rural poor and low-income earners to more expensive, unsteady and traumatic life style which constraints their individual growth and economic advancement. It is suggested that that lack of access to a bank account will prevent these category of individuals from enjoying the usual discounts (benefits) that accompany online and cashless transactions in the financial system. Also, when disaster occurs only those with active insurance policy can be compensated and reinstated into a normal social life. During old age, when there is no more strength to earn a living, only those that saved through contributory pension scheme can have a peaceful retirement without depending on relatives. According to Enhancing Financial Innovation and Access (EFInA) report for Nigeria, about forty one million persons out of ninety million four hundred refused to deposit their money into a formal bank account. This shows a rise in the rate of financial exclusion from 39.5 percent in 2014 to 41.6% as at December 2016, (EFInA, Citation2016). The same report recorded an increase in the number of lapsed users (self-excluded users) either due to tough economic situation or high cost of fund.

Although financial exclusion menace seems universal, report from the World Bank shows that the problem of financial and social exclusion is more prevalent among the underprivileged in emerging or developing economies. The gap in access, usage, and quality of savings, and in the availability of credit and indemnity products amongst diverse sections of the economy remain very huge (World Bank Group, Citation2015; Demirgüç-Kunt et al., Citation2015). About 80 percent of bankable adults in sub-Saharan Africa are financially exempted, this implies that about three hundred and twenty five million people are unbanked. Those lacking access to finance comprise certain disadvantaged cluster of persons who are a crucial part of a much extensive social exclusion. The same study shows an increase in lapse users where about one-third of households that do not have current account now, had one previously but closed or abandoned it (Kempson, Whyley, Caskey and Collard, Citation2000). To this end, to capture more persons into mainstream finance, there is an urgent need to reduce/and or eliminate the hurdles preventing individuals and groups in rural communities from mainstream finance. This study examined how through financial inclusion those not previously included into formal financial activities as a result of unemployment will be captured into the financial net. This no doubt will promote SDGs of employment generation, wealth creation, poverty and inequality reduction as well as hunger elimination. The question this study addressed is how financial exclusion of individuals and groups in rural communities worsen financial inclusive growth agenda pursued by government and its agencies? To this end, it important to know what extent financial exclusion of individuals and groups in rural communities impede financial inclusive growth in SSA? The hypothesis stated in its null is that financial exclusion does not prevent government and its agencies from capturing individuals and groups in rural communities into mainstream finance.

2. Literature review

2.1. Review of concepts and theories

According to the European Commission report, financial exclusion is a development, which occurs when citizens have problems of access and usage of financial products or services available in the formal financial market, which enables them to take care of their financial needs and lead a happy and fulfilled life in their communities (European Commision, Citation2008). Financial exclusion can also result when adults who were initially included in the formal financial net become excluded due to avalanche of barriers to financial access or usage. Factors responsible for financial exclusion may include: job loss/unemployment, low income, high cost of transaction and usage of such financial products. It also includes poor health and housing condition, distance to the point of service delivery, relocation of the user, loss of trust in the product or service delivered, insecurity in the community including cybercrimes, complexities in the use of the product, bank branch relocation or closure, stringent KYC requirements, demographic issues, socio-cultural and religious factors and so on, (Anyanwu and Anyanwu, Citation2017). This implies that factors that limit financial inclusiveness is related to the barriers to arrangement, stage of development and type of financial market in operation in that particular region and can also be part of social exclusion. It could also be a demand side oriented barriers (when caused by financial incapacity of the user) or supply side oriented barriers if related to product quality or cost. A financial product is appropriate if its access and or usage do not expose the user to difficulties in using such products (European Commission, Citation2008).

There are different forms of exclusion ranging from banking exclusion, savings/pension exclusion, credit exclusion as well as insurance exclusion. When the poor are perceived by traditional financial institutions (including some micro finance institutions) as high risk individuals with low credit rating they are exposed to very high interest as a premium for assuming high risk which most times could not be afforded by this category of customers thereby culminating to credit exclusion. To meet their financial needs and create wealth these categories of persons resort to borrowing from doorstep lenders, pawnbrokers or illegal loan sharks at a highly ridiculous cost of fund. Also, there is no gain saying the fact that insurance products are exclusively for the elite and rich citizens who places high premium on their asset and life as against the poor and downtrodden who most at times do not even have justifiable reason to buy insurance products and services. Because they lack the needed physical and financial assets to insure. Most times, those in the informal sector particularly the poor are apprehensive of insurance companies because of the cumbersome documentation processes and perception that insurance companies may not pay their claims when they incur any loss.

The low income and high inequality gap prevalent in most developing economies is also another key contributor to financial exclusion thereby making it impossible for the downtrodden and poor to be able to save and build financial assets for themselves and families. Contributory pension administration in any region can receive a boost if all workable adults are gainfully employed, however this may not be possible with the high rate of unemployment in SSA. It is expected that those in the informal sector comprising mostly of the rural poor who mostly use cash as a means of payment more often pay more service charge and other cost of transactions than their counterparts in the formal financial sector who often do cashless transactions via digital ecosystems. Also the Trading and Economics.com/National Bureau of Statics survey shows a downward trend in employment rate from an all-time high of 93.6 percent in 2015 to its lowest rate of 81.2 percent towards the third quarter of 2017 (Trading Economics.com/NBS, Citation2018). With this trend in view, financial exclusion rate will definitely increase because those who lost their jobs or remained unemployed will be unable to use their bank account because of low income.

This study is hinged on the traditional economic theory, which posits that individuals sell their labour power in the market to earn a living as well as smoothen life-cycle consumption. Younger persons tend to invest and save more when their strengths allows them to do more work and at old age they invest and save less because they are weak to work. On the other hand, companies struggle to access the investable funds accumulated by individual savers to finance their operations. In summary, individuals are net savers whereas firms are net users of the funds deposited by individuals. The financial intermediaries and institutions tasks is to mobilize the funds from the surplus sector (individual savers) and allocate the capital for use by the deficit sector (firms) in the most efficient manner (Mankiw & Ball, Citation2011). In a survey conducted on the Attitude of Workers towards National Health Insurance Scheme (NHIS). It was found that only about 5% acquired the NHI policy sold to Nigerians despite 62% awareness rate achieved. Of persons that acquired it, 90% of them are within the lower income class, (Amoo, Citation2011). The reason obviously is because of the subsidized cost of medical expenses of the holder and his family when compared with the premium paid by the holder of the policy.

However, the underprivileged poor are stereotypically disqualified from the wage-earning occupation openings that traditional economic theory presumes. By no choice of their own, these persons are excluded from the formal economy. They assume the dual role of household consumers and self-employed firms at the same time, thereby combining the production and consumption decision functions, which according to the theory should be separated. As a consequence, they require a comprehensive variety of financial facilities to make and sustain a living for themselves, build resources, mitigate risks, and smoothen consumption. This implies that the conservative dissimilarity between what consumers want and the financial desires of businesses is frequently hazy. It is worth mention that empirical evidence abound on how poor households in the informal sectors in most developing economies vigorously oversee their financial lives to attain these numerous goals (Darl, Jonathan, & Staurt, Citation2010). Through shadow banking and the informal sector, they save and borrow at any given time. For the poor, management of finance is a key and well-agreed everyday lifestyle. The traditional economy theory is related to this study in the sense that if the rural poor are prevented from accessing formal financial facilities to build wealth due to the avalanche of barriers to financial access, it will be difficult to provide the needed fund which the MSMEs will borrow to create employment and achieve economic growth. This therefore creates a vicious circle of unemployment and unavailability of investible funds to drive inclusive growth.

2.2. Empirical literature

Financial enclosure is crucial to decreasing the economic susceptibility of households, stimulating economic progress, easing poverty and enhancing the quality of lives (Christine, et al Citation2016). Studies have shown that financial access as well as easy and affordable sources of finance are necessary preconditions for accelerated economic progress and decline in income inequality and poverty alleviation (Serrao et al, Citation2012). Achieving macro-economic goals such as price stability, income equality, employment generation and poverty reduction will require all-inclusive financial support that will create equal opportunities, provide platform for economically and socially disadvantaged citizens to fit in properly into economic activities and contribute actively to development while protecting themselves against economic shocks. Demirguc-Kunt and Levine (Citation2007) argue that curtailing inadequacies in the financial market will help to boost investment opportunities, which will result to positive incentives for the players in the financial market. On the other hand, inadequate financial access will provoke income inequality and poverty trap as well as hamper economic progress. Achugamonu, Taiwo, Ikpefan, Olurinola, and Okorie (Citation2016) conducted a study on the relationship between agent banking and financial inclusion in Nigeria. The study revealed that high level of illiteracy among the unbanked populace constitutes a major barrier to achieving high financial inclusive growth in Nigeria.

Another study on the “Nexus between financial enclosure, poverty decline and Millennium Development Goals (MDGs), reveal that inclusive finance is the mediation approach that try to curtail market hurdles that prevent financial institutions from attending to the financial needs of the deprived and poor citizens (Chibba, Citation2009). Financial inclusion has the potential to provide sustainable solutions to eradicate poverty, engender inclusive growth as well as address the millennium development goals. Inclusive finance has the capacity to attract the underbanked in the informal sector into the formal financial net so as to enable them enjoy affordable and available financial services in the financial market. Mbutor and Uba (Citation2013) opine that inclusive finance will reduce the cost of managing cash and protect the local currency from adverse fluctuations due to foreign exchange risks as well as promote sound financial system in the economy. The study further revealed that at the micro level of the economy, increasing financial access portends so many developments with respect to increasing the growth rate of the economy.

Financial exclusion increases the cost of using informal financial services often borne by the active poor in remote communities. A strong financial structure available to all reduces information asymmetry and transaction costs, improves interest on savings, and engenders good investment choices. Furthermore, it activates technological innovation, and sustainable economic growth. (Beck et al., Citation2010). The same study found that transaction services increased with the introduction of M-Pesa in Kenya thereby reducing costs of financial transactions. It also found that women predominantly use orthodox financial services than men and persons in rural communities patronize informal financial products and services than their counterpart in urban cities. Finally, the study found a strong predictive power between income, education and using financial products and services in the formal sector (Beck et al., Citation2010). Adetiloye and Adegbite (Citation2013) examined the impact of financial globalization on local productions in developing economy like Nigeria, the study found a positive correlation between export and capital outflow and that capital outflow had dwindled existing local capitals and created a negative influence on local investment. The study therefore advocated for autonomous domestic investment to crowd out foreign direct investment and that this could only be possible if physical and social infrastructures are developed. Adigun and Kama (Citation2013) posit that to achieve an all-inclusive finance, users of financial products must be supported with financial information and other financial assistance with ease and at an affordable cost. By this, the economy will receive a boost and through its intermediation process, efficient resource allocation is achieved. By this process, financial business becomes relaxed, revenue level and progress rises with fairness, and poverty is eliminated, while the economy becomes insulated from external shocks.

Oyelami, Saibum, and Adekunle (Citation2017) examined the factors that determine inclusive finance among SSA countries using ARDL and found that financial literacy, income, interest rate and financial innovation are factors that determine financial inclusion in the affected region. It therefore advocated for an improvement in the monetary policy of the affected countries to help boost financial inclusive and economic growth. Osei-Assieby (Citation2009) examined factors responsible for terrestrial exclusion of financial services from individuals and households living in rural communities in Ghana. Using datasets from the rural communities, the study found that the banks choice of establishing a bank branch in rural communities has positive significance with factors such as the size of the market, rate of infrastructural development of the area, vitality with which the financial market operates. However, there exists a negative relationship between choice of siting a branch in rural locality with insecurity of the business. Furthermore, it was found that individual demand for a bank account is affected by issues such as bank charges, illiteracy, ethno-religious issues, reliance ratio, job engagement, affluence status and nearness to bank. Makoni (Citation2014), investigated the status of rural banking and financial exclusion in Zimbabwe. The motivation for this study stems from the fact that greater proportion of people in rural communities in Zimbabwe remained unbanked because microfinance institutions perceive them as persons who do not have the capacity to use financial services for investment and economic decisions Findings from this research conducted with data collected from individuals, microfinance institutions and commercial banks in Matabeleland North region shows that people residing in rural communities are actually highly bankable save for the dearth in infrastructural facilities in the area which deterred the commercial banks from establishing branches in that region.

From the international space, Coffinet and Jadeaus (Citation2017) studied the factors that determine financial exclusion using the data from the Eurosystems Household Finance and Consumption Survey (HFCS). Findings from the household individual characteristics survey shows that old age, low income, unemployment, low education and less wealthy individuals are more prone to face exclusion from mainstream finance. In like manner, owning a savings account is less discriminated by age but younger persons and low-income earners are more probably disposed to accessing credit facility. At the country level, the study found a strong heterogeneity among factors determining financial exclusion across the euro area. In another study from India, Choudhury and Bagchi (Citation2016) investigated the reason for financial exclusion in a developing country like India, using sampled data from 100 respondents in different locations in West Bengal, India. The study showed that work status, head of the family’s saving habit, education and location are significant factors for financial exclusion. Vo, Van, Vo, and McAleer (Citation2019) using panel estimation threshold technique investigated the linkages between financial inclusion and macroeconomic stability in 22 emerging economies from 2008 and 2015 focusing on the potential optimal level. The study found that financial inclusion improves stability under certain threshold. It also found that financial inclusion also helps in sustaining stable inflation and output growth in the affected countries.

2.3. Materials and methods

The study population comprises of 46 countries located within the sub-Saharan African region. However using a purposive sampling technique, only 27 countries were selected for the period between 2007 and 2017 from the data sourced from the World Bank database. This period covers the pre and post global financial meltdown experienced between 2008 and 2010. In obtaining the data, all ethical standards were put in place to ensure that the data were obtained in its raw form without manipulation and necessary credit accorded to World Bank. As information in the public domain necessary permission were obtained to use the data in its raw form. By implication, only data that meets the purpose of the study were obtained and analysed. The sample size therefore accounts for 59 percent of the total population. Twenty seven countries were selected because their data were available on the World Bank database as at the time of conducting this research. This study adopted a Granger Error Correction Method (ECM) specification for a short panel data structure. To deal with the problem of persistency, heterogeneity and endogeneity associated with short panel data the study employed differenced Generalize Methods of Moments (GMM) of Arellanon and Bond (Citation1991) for the model specification. The estimator is subjected to first and second order serial correlation test and test for valid instruments using Sargan over identifying restriction test. Therefore, the nature of our panel data is such that the individual dimension is larger than the time dimension (N > T). The justification for adopting this methodology is because of the nature of data involved (which is short panel data).

2.4. Sample identification number

The identification number of the countries sampled are as follows: Angola is 1, Burundi is 2, Botswana 3, Central African Republic 4, Cameroon 5, Congo Democratic Republic 6, Congo, Republic 7, Equatorial Guinea 8, Ghana 9, Guinea 10, Gambia 11, Kenya 12, Liberia 13, Lesotho 14, Madagascar 15, Mozambique 16, Mauritania 17, Mauritius 18, Malawi 19, Namibia 20, Nigeria 21, Rwanda 22, South Africa 23, Seychelles 24, Tanzania 25, Uganda 26 and Zambia which is 27. The choice of this identification number is based on the position of a country in the alphabetical order. Therefore, it does not have any statistical importance/value for explanation except for identification purpose.

2.5. Definition of variables

Financial inclusion is represented by two strands: (i) inclusion by usage, which is proxy by deposit in commercial banks per 1000 adults (dcpa) and (ii) inclusion by quality, proxy by ratio of depositors to borrowers (rdtb). While financial exclusion is represented by unemployment. The justification for using the variables mentioned is based on the recommendation of the World Bank of the choice of these variables as ideal for measuring financial inclusion and exclusion. The a priori expectation is a negative relation between financial exclusion proxy by unemployment and financial inclusion. This implies that increase in unemployment rate will reduce financial inclusive drive of government.

2.6. Model specification

This study follows the views of Chibba (Citation2009) and Cihak, Mare, and Melecky (Citation2016), to initiate a dynamic short run and long run specification, alternatively referred to as ECM-ARDL Granger frameworks. Thus, this augmented model is defined by financial inclusion as the endogenous (dependent) variable represented by deposits in the commercial bank per 1000 adults (dcpa), and ratio of depositors to borrowers (rdtb)} and financial exclusion as the exogenous (independent) variable {also proxy by unemployment rate}.

To understand the features of this model, the variables are stated in its general form as:

Where: is the response variable,

is the covariate variable,

is the time fixed effects,

is the composite error,

specific error, and

is the common error. The specific error is time invariant but the common error varies across time and units.

The specific or derived form of the model is stated as below:

Where: are natural log of deposits in commercial banks per 100 adults, ratio of depositors to borrowers and unemployment, respectively.

3. Results

3.1. Descriptive statistics-visual method

This study showed the movements and the distribution pattern of the underlying variables over time/across countries using line graphs, box and quarter-quarter plots. The line graphs are presented in the first set of figures, while the box and quarter-quarter plots are shown in the second and third sets of figures respectively.

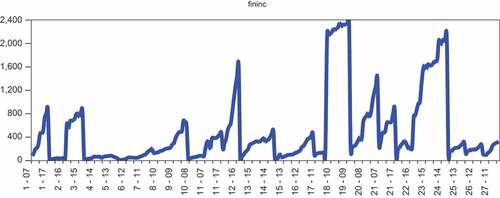

The first line graph (Figure ) shows the movements of financial inclusion by usage (number of deposits in commercial banks per 1000 adults). It is observed in the graph that Malawi, Mauritius, Seychelles and Tanzania respectively have the highest number of persons using the services of banks for depositing purpose. The study also observed that countries like Burundi, Central African Republic, Cameroon, Congo Republic and Congo Democratic Republic have the lowest usage of financial products. Meaning that they have very low magnitude of inclusion in terms of usage.

Figure 1. Line graph showing movements of financial inclusion by usage

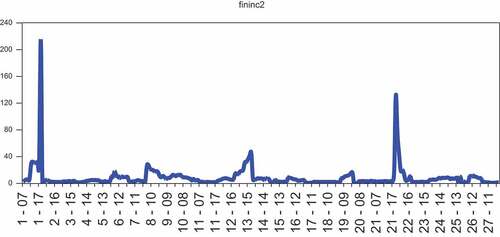

The second graph (Figure ) presents the movements of financial inclusion by quality of services (ratio of depositors to borrowers), it is conventionally agreed that high quality of bank service would generate sufficient deposits to satisfy the needs of borrowers). A high ratio mobilizes much from the surplus unit to deficit unit, and it is an indication of high quality of financial inclusion. The countries with the highest ratios are Nigeria, South Africa, Mauritania, Mauritius, Madagascar, Gambia, Burundi and Botswana, while those with the lowest ratios are Angola and Rwanda respectively. Therefore, Angola and Rwanda have the lowest financial inclusion in terms of quality.

Figure 2. Line graph showing movements of financial inclusion by quality

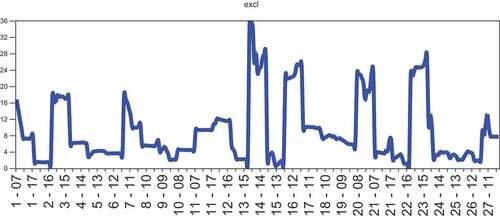

The movements of financial exclusion by unemployment is shown in the fifth line graph (Figure ). According to the graph, Lesotho and Madagascar are among the countries in SSA with the highest financially excluded persons by unemployment, while Tanzania and Uganda have the lowest financial excluded people by unemployment.

Figure 3. Line graph showing movements of financial exclusion by unemployment

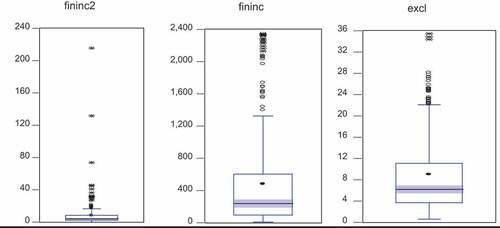

It is perturbing that all the box plots have almost the same features (Figure ). For example, in each case, the box is positioned at the centre and the lower whisker is shorter than the upper whisker. This is an indication that none of the variables follows a Gaussian distribution pattern. The study further confirms this by quarter-quarter plots.

Figure 4. Box plot showing the distribution pattern of underlying variables

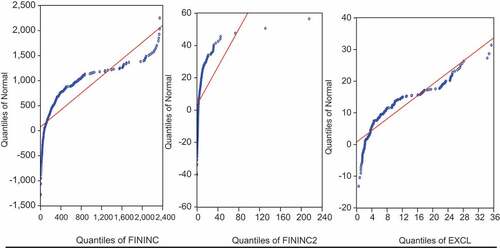

To reiterate our earlier observation about the nature of the variables, the quarter-quarter plots are presented to reaffirm the outputs of the box plots (Figure ). As shown in the quarter-quarter plots, there is visual evidence to confirm that in each plot; most of the dots do not rest on the seemingly straight line. Implying that the variables used to represent financial inclusion (usage and quality) and financial exclusion (unemployment) are not normally distributed. Hence, the need to log-transform the data to de-trend them and make them mean reversible. Though the problem of unit root is not a peculiar one in short panel data but all the data must be confirmed to the same unit. This could be achieved by log transformation.

Figure 5. Quarter-quarter plot showing the distribution pattern of underlying variables

3.2. Descriptive statistics-statistical method

Another means of describing data is to compute some statistics such as mean, standard deviation, skewness, kurtosis and Jarque-Bera (JB). The JB statistic is calculated with probability to test the null hypothesis of normality. Table below presents the outputs of these statistics.

Table 1. Showing statistics from 2007–2017 in their raw value quantities

The mean value of each of the variables is positive. Financial inclusion by usage, financial inclusion by quality and financial exclusion have the mean values of 4.90, 8.25 and 9.03%, respectively. This implies that all these variables have displayed increasing tendency throughout the sampling period. The average inclusion by usage is approximately 5 depositors for every 1000 adults. This average value is small when considering the number of banks/branches in this region. Furthermore, average inclusion by quality is approximately 8. This indicates that borrowers are eight times more than depositors. Average exclusion by unemployment is about nine percent. This suggests that people are not really excluded from financial services in SSA because of unemployment. All the variables except financial exclusion have larger value for their standard deviations more than their means. This is an indication that the variables are highly volatile around their mean values. The skewness scores for each of the variables is larger than zero and positive. By implication, the variables are each positively skewed, meaning that there is tendency of large values in the nearest future. The kurtosis value for each variable is approximately larger than 3, thus, the variables are leptokurtic in nature with indication of possible outliers. All the computed JB statistics are asymptotic with zero percent probability value. This means that each of the variables does not follow a Gaussian process confirming my earlier result.

3.3. Inferential statistic and post estimation results

In this section, the parameters of the models stated in section three are estimated using one-step Diff-GMM estimation technique. This technique provides robust test for the hypotheses stated for this study. The hypothesis focuses on the nexus of financial inclusion and financial exclusion (Table ). Before reporting the results on the tests of this hypothesis, the study displays graphical reports on sample identification number, average individual country financial inclusion usage and average group usage for the purpose of decomposing the countries into high usage (large saving countries) and low usage (small saving countries) to enhance the uniqueness of the results.

Table 2. Financial exclusion-inclusion nexus from 2007 to 2017

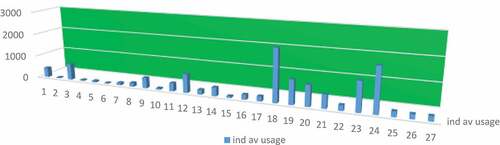

A sight view of Figure review that countries such as Burundi, Central Africa Republic, Cameroon, Congo, Congo Republic, Equatorial Guinea, Guinea, and Madagascar have very low usage of financial services, followed by countries such as Angola, Botswana, Ghana, Kenya and Nigeria with moderate use of financial service. Nevertheless, countries like Mauritius, Malawi, Namibia, South Africa and Seychelles are large saving countries because they display high usage of financial services.

Figure 6. Individual country’s average financial service usage

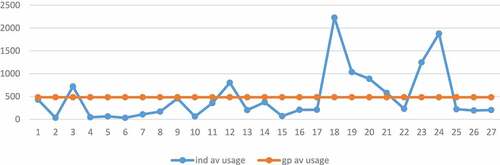

The line marked by blue colour indicates the movement of individual average usage, while the group average usage is marked by orange colour (Figure ). The group average usage is constant (value = 482.64 approximately) and any country that has average return above group average return is considered as large saving country or high usage of financial service; such countries are Botswana, Kenya, Mauritius, Malawi, Namibia, Nigeria, South Africa and Seychelles. While other countries whose individual average return falls below the group average return are called low saving countries, in this case countries such as Burundi, Central African Republic, Cameroon, Congo, Congo Republic, Equatorial Guinea, and Guinea have low usage. The tests of the hypothesis are conducted for low-financial stable, moderate-financial stable and high-financial stable countries.

Figure 7. Decomposing countries into high and low usage of financial services

The ECM coefficients for inclusion equations are −0.31 for countries with poorly stable financial system, −0.10 for countries with moderately stable financial system and −0.26 for countries with highly stable financial system, and all the coefficients are significant at one percent level. This means, for the three sets of countries, financial inclusion and exclusion maintain long run relationship; likewise, financial inclusion responds to temporal shocks in financial exclusion. However, the speed of the response is faster for countries with poorly stable financial system and slower in countries with moderately stable financial system. The coefficients of the short run effects are 0.33, 0.37 and 0.32, respectively for countries with poorly stable financial system, countries with moderately stable financial system and countries with highly stable financial system. None of these coefficients is significant even at 10 percent. Hence, there is a strong evidence that in the short run, financial exclusion has no significant impact on financial inclusion, though there is positive relationship between them. This is contrary to a priori. However, this could be that most of the unemployed still involves in some financial services through transfer. Lastly, the coefficient of long run elasticity for the three sets of countries (poorly, moderately and highly stable financial systems) are 0.03, −1 and 2.08, respectively. In view of these results, there is evidence that financial inclusion responds to permanent shocks in financial exclusion for each of the three countries. However, the long run multiplier effects are stronger for countries with highly stable financial system. The p values of the Sargan and Sargan in difference tests for the three equations are asymptotic and larger than alpha value at ten percent; this means that the hypothesis of overriding restrictions and strict exogeneity cannot be rejected. The second order autocorrelation has large p values for the cases, indicating a non-rejection of null hypothesis that there is no second order autocorrelation in stochastic terms. These are sufficient evidences supporting the adequacy of the models.

4. Discussion

The SDGs examined in this study include employment/job creation, poverty reduction and hunger elimination. The a priori expectation, is that when persons are included into mainstream finance, they should be able to access credit that will enable them create wealth, generate employment, eliminate hunger as well as reduce poverty and inequality. The major finding of this investigation is the existence of long run relationship between financial inclusion and financial exclusion for the three tiers of countries. This means that exclusion responds to temporal shocks in financial inclusion at a speed of 31% for low financial stable countries (LFSC). In like manner, financial exclusion responds to temporal shocks in inclusion at a speed of 10 and 26% for moderate financial stable countries (MFSC) and high financial stable countries (HFSC) respectively. In simple terms, increase in the number of persons depositing money in the bank for on lending to borrowers will make more loanable funds to be available and more persons will have access to credit facility. If the bank has enough cheap funds for investment in real sector, more persons will be employed by the private sector who are the growth engine of every nation. This position is in tandem with a priori expectation that financial inclusion reduces unemployment. On the other hand, the short-run coefficient shows a positive relationship between financial inclusion and exclusion for the sets of countries examined. Also none of the alpha values is significant even at 10%. The implication is that increase in the number of deposits in the bank does not reduce unemployment and unemployment is not a determinant for exclusion. There may be other factors responsible for exclusion, which was not included in the model. The reason, for this result may be that most persons involved in mainstream financial transactions may not necessarily be gainfully employed. This is the case with students and aged citizens who do not necessarily have a job but undertake pockets of financial transactions. This result is corroborated with the findings from the by Cardiff University which opined that the risk of poverty for adults living in working households increased by 26.5% from 12.4 to 15.7%, between 2004/5 and 2014/15. The same result shows that by the end of 2015, 60% of persons living in extreme poverty were persons of all age brackets working in one firm or the other (Hick and Lanau, Citation2018). On the contrary Choudhury and Bagchi (Citation2016) posit that work status, head of family’s savings habit, education and location have significant relationship with financial exclusion in India. In a related study Coffinet and Jadeaus (Citation2017) found that older, unemployed, lower-income, lower educated and less wealthy households of the euro area are less likely to owe a current account.

4.1. Conclusion and recommendations

The SDGs examined in this study include employment/job creation, poverty reduction and hunger elimination. The a priori expectation, is that when persons are included into mainstream finance, they should be able to access credit that will enable them create wealth, generate employment, eliminate hunger as well as reduce poverty and inequality. In view of the finding summarized above and based on the objective investigated, this study concludes that contrary to expectation/theory, financial inclusion does not decrease in either the short run or long run by financial exclusion (unemployment) for the sample of countries with poorly and highly stable financial systems. This is because inclusion and exclusion have positive relationship both in the short run and long run situations for these samples of countries. However, for the moderately stable financial system, exclusion has negative long run multiplier impact on inclusion. Thus, we conclude in respect of moderately stable financial system that financial exclusion, proxied by unemployment affect financial inclusion especially for moderately stable financial systems. Based on the findings revealed above, this study recommends that government should create an enabling environment and employment opportunities for bankable adults living in the rural communities in the affected sub Saharan Africa countries. This will enable them to create wealth and earn a living for themselves and families as well as reduce cost of engaging in the informal financial market. When people are empowered, they will be able to acquire financial assets, use financial services as well as buy financial products thereby increasing inclusive growth in the formal financial system.

Acknowledgements

The authors wish to appreciate the proprietor base of Covenant University for the financial support to conduct this research and publish the report.

Additional information

Funding

Notes on contributors

Uzoma B. Achugamonu

Uzoma B. Achugamonu is a Development Finance specialist with several publications in high impact journals on financial intermediation, financial inclusion and micro-finance. He is currently working on his PhD thesis on Financial Inclusion and Stability.

Kehinde A. Adetiloye

Kehinde A. Adetiloye is an Associate Professor in the department of Banking and Finance, Covenant University, Ota. His research interest is in International Finance and intermediation.

Esther O. Adegbite

Esther O. Adegbite is a distinguished Professor of Finance from the University of Lagos, Akoka, Lagos. She has graduated a lot of PhD students. Her research interest are development finance, international finance and SMEs.

Abiola A. Babajide

Abiola A. Babajide is an Associate Professor in the department of Banking and Finance, Covenant University. Her research interest are Development Finance, Portfolio Theory and Corporate Finance

Francis A. Akintola

Francis A. Akintola is a Senior Lecturer from the Finance Department, Babcock University. His research interest span across Corporate Finance, Strategic Financial Management and Accounting.

References

- Achugamonu, B., Taiwo, J., Ikpefan, A., Olurinola, I., & Okorie, U. (2016). Agent banking and financial inclusion: The Nigerian experience (pp. 4418–15). Spain: International Business Information Management Association (IBIMA.

- Adetiloye, K., & Adegbite, E. (2013). Financial globalisation and domestic investment in developing countries: Evidence from Nigeria. Mediterranean Journal Social Sciences, 4(6), 213–221.

- Adigun and Kama. (2013, August). Financial inclusion in Nigeria: Issues and challenges. Central Bank of Nigeria Ocassional Paper No. 45.

- Agarwal, A. (2010). Financial inclusion: Challenges & opportunities, 23rd Skoch Summit 2010.

- Aguera, P. (2015). Financial inclusion, grwoth and poverty reduction. ECCAS, Regional Conference (pp. 1–19). Brazzaville, Congo: World Bank Group.

- Amoo, E. (2011). Attitude of workers towards National Health Insurance Scheme: ImplicationforVision 2020. Internatiomal Journal of Management and Development Studies. Department of Buisness Studies, University of Ado Ekiti.

- Anyanwu, J. C., & Anyanwu, J. C. (2017). The Key Drivers of Poverty in Sub-Saharan Africa and What Can be Done About it to Achieve Sustainable Development Goal. Asian Journal ofEconomicModelling, 5, 297–317. Retrieved from www.aessweb.com

- Arellano, M., & Bond, S. (1991). Monte carlo evidence and application to employment equations. Review of Economic Studies, 58, 277–297.

- Beck, T., Cull, R., Fuchs, M., Getenga, J., Getere, P., & Randa, J., (2010). Banking sector stability, efficiency, and outreach in Kenya. World Bank Development Research Group. Retrieved from http://documents.worldbank.org/curated/en/428671468048252880/pdf/WPS5442.pdf

- Blake, S., & De Jong, E. (2008). Short changed: Financial exclusion a guide for donors and funders. New Philanthropy Capital Report for 2008.

- Chibba, M. (2009). Financial inclusion, poverty reduction and the millennium development goals. (M. F. Sinclair S, Ed.). European Journal of Development Research, 21, 213–230. doi:10.1057/ejdr.2008.17

- Choudhury, R., & Bagchi, D. (2016). Financial exclusion - A paradox in developing country. IOSR Journal of Economics & Finance, 7(3), 40–45. Retrieved from http://www.iosrjournals.org/iosr-jef/papers/Vol7-Issue3/Version-1/G0703014045.pdf

- Christine, L. (2016, April). Opening remarks — IMF-CGD event on “Financial inclusion: Macroeconomic and regulatory challenges”. Imf Communications Department. Retrieved from http://www.imf.org/external/pubs/cat/longres.aspx?sk=43163

- Cihak, M., Mare, D. S., & Melecky, M. (2016). The nexus of financial inclusion and financial stability: A study of trade-offs and synergies. World Bank Group. Retrieved from https://openknowledge.worldbank.org/handle/10986/24639

- Coffinet, J., & Jadeaus, C. (2017). Household financial exclusion in the Eurozone: The contribution of the household finance and consumption survey. Belgium Brussels: Bank for International Settlement. Retrieved from https://www.bis.org/ifc/publ/ifcb46o.pdf

- Darl, C., Jonathan, M., & Staurt, R. (2010). Portfolios of the poor: How the World’s poor live on $2 a day. New Jersy, NJ: Princeton University Press.

- Demirguc-Kunt, A., Klapper, L., Singer, D., & Van Oudheusden, P. (2015). The Global Findex Database 2014: Measuring financial inclusion around the world (English). Policy Research working paper; no. WPS 7255. Washington, DC: World Bank Group. Retrieved from http://documents.worldbank.org/curated/en/187761468179367706/

- Demirguc-Kunt, B., & Levine. (2007). Finance, inequality and the poor. Journal of Economic Growth, 12(1), 27–49.

- EFInA and NBS. (2016). 41.1 Million Nigerian adults keep money at home - survey. Lagos: Daily Trust. Retrieved from http://www.efina.org.ng/our-work/research/access-to-financial-services-in-nigeria-survey/efina-access-to-financial-services-in-nigeria-2016-survey/

- European Commision. (2008). Financial service provision and prevenetion of financial exclusion. European Commission. Retrieved from http://Ec.europa.eu/employment_social/spsi

- Hick, R., & Lanau, A. (2018). Moving in and out of in-work poverty in the UK: An analysis of transitions, trajectories and trigger events. Journal of Social Policy. doi:10.1017/S0047279418000028

- Kempson, W., Caskey, & Collard. (2000). In or out? Financial exclusion: A literature and research review. Report, Financial Services Authority.

- Makoni, P. L. (2014). From financial exclsion to financial inclusion through microfinance: The case of rural Zimbabwe. Corporate Ownership and Control, 11(4), 447–455. Retrieved from file:///C:/Users/user%20pc/Downloads/Fromfinancialexclusiontofinancialinclusionthroughmicrofinance-thecaseofruralZimbabwe_makoni.pdf

- Mankiw, G., & Ball. (2011). Macroeconomics and the financial system. New York: Worth Publishers.

- Mbutor and Uba. (2013). The impact of financial inclusion on monetary policy in Nigeria. Journal of Economics and International Finance, 8(5), 318–326. doi:10.5897/JEIF2013.0541

- Osei-Assieby, E. (2009). Financial exclusion: What drives supply and demand for basic financial services in Ghana. Savings and Development Journal, 207–238. Retrieved from file:///C:/Users/user%20pc/Downloads/SSRN-id1393318.pdf

- Oyelami, L., Saibum, O., & Adekunle, B. (2017). Determinants of financial inclusion in sub saharan African Country. Covenant Journal of Business and Social Science, 8(2), 104–116.

- Ratna, M., Diaye, B., Mitra, K., & Mooi. (2015). Financial inclusion: Can it meet multiple macroeconomic goals? International Monetary Fund (IMF), Monetary and capital markets department with inputs from strategy and policy review department and other departments1. Monetary and Capital Markets Department with inputs from Strategy and Policy Review Department and other departments.

- Serrao, M. V., Sequeira, A. H., & Hans, B. (2012). Designing a methodology to investigate accessibility and impact of financial inclusion. doi: 10.2139/ssrn.2025521. Available at SSRN: https://ssrn.com/abstract=2025521

- Small Scale Sustainble Instrastructure Development Fund (S3IDF). (2018). Defining financial exclusion: Why we need to focus on the problem and not just the solution.

- Trading Economics.com/National Bureau of Statistic. (2018)

- Universal Financial Access Report. (2017). Universal financial access report. World Bank Group. The World Bank. Retrieved from http://www.worldbank.org/en/topic/financialinclusion/brief/achievinguniversal-financial-access-by-2020

- Vo, A. T., Van, L. T.-H., Vo, D. H., & McAleer, M. (2019). Financial inclusion and macroeconomic stability in emerging and frontier markets. Vietnam: Instituto Complutense de Análisis Económico. Retrieved from http://www.ucm.es/fundamentos-analisis-economico2/documen

- World Bank Group. (2015). Global financial development report 2015/2016: Long-term finance. Washington DC: World Bank. doi:10.1596/978-1-4648-0472=4