Abstract

Countries in Africa have since joined their counterparts in other regions of the world in adopting IFRSs with over 30 countries either requiring or permitting its use for its companies. This study contributes to academic literature as it presents a bibliometric analysis on the state of IFRS research in Africa. The analysis involves 73 published articles listed on Scopus database between 2005 and 2018. Key findings in the study indicate that the first research document on Scopus database on IFRS in Africa was in 2005, despite its early adoption since 1993 in Zimbabwe. There is a continued upward growth in the volume of publications and citations over the years. The year of first IFRSs adoption is not associated with the volume of publication. Top five leaders in the volume of publication on IFRSs include Tunisia and Egypt, these countries are yet to adopt IFRSs. The dominant subject areas on IFRSs research are Business, Management & Accounting, Economics, Econometrics & Finance and Social Sciences. Only 21 authors and 18 institutions out of over 600 institutions in Africa contribute more than one publication to IFRS research. These institutions and authors are all in six African countries (South Africa, Nigeria, Tunisia, Egypt, Uganda and Ghana). Recommendations from the result include the need for higher visibility of research on IFRS. Approximately 87% of the publications are non-open access and the need for more academic conference on IFRS as conference proceedings accounts for only 11%.

PUBLIC INTEREST STATEMENT

The need for a scholarly work that provides a quantitative and statistical overview on the growth of IFRSs research publication in Africa is overdue. This research is deemed very relevant owing to some of the notable findings. There is a dearth of research publications on IFRS in Africa even though over 30 countries either requiring or permitting its use for companies. Strikingly, much of the heralded publications on IFRS are concentrated in only about six nations. Even more surprising, some of the nations in the top category of IFRS research publications are yet to adopt IFRSs. Noteworthy is the growing trend of publications in this regard in recent years. The number of publications peaked in 2018 with only Eighteen (18) publications. Standard adoption requires a concerted effort from all stakeholders to review and revise. Thus, there is a call to all stakeholders for in-depth research and visibility of IFRSs adoption in Africa.

1. Introduction

Globally, more than 140 countries require the use of IFRSs, with 12 countries permitting its use for most or all of its companies. While, many others express their commitment to adopt IFRSs. Since 2005, countries in Europe and Australia were the forerunners of IFRSs adoption (Maradona & Chand, Citation2018). However, Africa has since come to terms with adopting IFRSs with over 30 countries either requiring or permitting it to use for its companies. The suitability of the world wide adoption of IFRSs has been quizzed.

Arguments ensue on the differences in the financial reporting environment across jurisdictions that adopt IFRSs (Maradona & Chand, Citation2018). Also, its value relevance is still unclear (Trimble, Citation2018). For instance, full IFRS adoption impacts negatively on Africa Countries; Foreign Direct Investment and perceived corruption in a country (Houqe & Monem, Citation2016; Nnadi & Soobaroyen, Citation2015). Conversely, other studies show a positive impact of IFRSs on; earnings value relevance (Odoemelam et al., Citation2019), income smoothing (Uwuigbe et al., Citation2016), environmental pollution (Efobi, Citation2015). Consequently, research on implication of IFRS adoption in Africa has gained considerable research attention (Elbannan, Citation2011).

Nevertheless, there is a need for literature to provide a scholarly view on the growth of IFRSs research across Africa. A bibliometric review applies statistics and mathematics in measuring the volume and impact of scientific work quantitatively. Also, it provides a broader insight into the area being studied. This approach has been applied to other Accounting related research domain (Baker et al., Citation2020; Chiu et al., Citation2018; Ezenwoke et al., Citation2019). To date, there is little or no literature on a bibliometric analysis that maps the state of IFRS research output in Africa.

This research fills the gap as it provides a bibliometric analysis that identifies the pattern of publication, authorship, productive institution, document type, subject area, publication access, research outlet, year-wise growth and citations. More precisely, the specific goals of this study are; to understand the relationship between year of IFRSs adoption and research output in Africa; to define the relationship between volume of publication and citation count; to know the publication access types; to identify country’s contributions to IFRS research; to enumerate subject areas linked to IFRS research; to identify the top productive institutions on IFRS research; to know document types published on IFRS research; to determine the most prolific contributors of IFRS research in Africa; to examine top research outlets on IFRS research in Africa; to ascertain the most cited documents on IFRS research in Africa.

In this review, data were collected on 54 African countries IFRSs adoption status from www.ifrs.org. The IFRSs adoption status is based on the following classification; First, if IFRSs are mandatory for domestic public companies; Second, if IFRSs are voluntary for domestic public companies; Third, if IFRSs are mandatory or voluntary for listings by foreign companies; Fourth, if IFRSs are mandatory or voluntary for SMEs; Fifth, if IFRSs are being considered for SMEs and the year of IFRSs adoption. In addition, data on each country’s research outputs were gotten from Scopus database. Statistical and mathematical analyses were carried on the data to achieve the goal of the study. The study provides a standpoint in understanding the state of IFRS research in Africa. Consequently, the study outcome would engender research guidelines, policies, agenda and standards.

The remaining part of this paper is outlined as follows. Following the brief introduction, section 1 defines the data and methods use in the study. The results were reported in section 3, while the implications of the results are discussed in section 4. Finally, section 5 concludes on the study.

2. Data and methods

The data used for the analysis is obtained from the Scopus Database. The Scopus database is a multidisciplinary database of peer-reviewed works with over 39,000 titles launched in 2004. However, the data from Scopus database is subject to certain ambiguities. For instance, subject areas in earth and planetary sciences, nursing, material science, immunology and microbiology etc not linked to IFRS research were listed in the search result. Also, country affiliations like United Arab Emirates, United Kingdom, France, Sweden, Germany etc not linked to IFRS research in Africa were included in the search result. The study excludes documents that were published after 2018 due to the incompleteness of the archive as the time when the search was done (14 October 2019, 08:53 PM). Therefore, in generating a clean data set, a considerable amount of time and effort was required to enhance data integrity and accurate analysis.

On IFRSs adoption, data on IFRSs mandatory for domestic public companies; IFRSs voluntary for domestic public companies; IFRSs mandatory or voluntary for listings by foreign companies; IFRSs mandatory or voluntary for SMEs; IFRSs being considered for SMEs and the year of IFRSs adoption were extracted from https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/

A total of 73 documents formed the Corpus used for the analysis having met the search criteria. The data for the 73 documents include the Author name, article title, citation count, year of publication, publication outlet, Authors affiliations and territories, document type, abstract and publisher. The specific objectives of the study were realised with the use Google sheets, MS Excel and STATA for visualizations and relevant statistical analyses.

3. Results

3.1. Descriptive statistics on international financial reporting standards (IFRSs) adoption across Africa

The summary of the use of IFRS across Africa is shown. Here, we show mandatory adoption of IFRS for domestic public companies, voluntary use of IFRS for domestic public companies, the use of IFRS for listing by foreign companies and the use of IFRS for SMEs in -, respectively. Based on the data from www.ifrs.org, the blue dot represents 18 (33%) countries that do not require public companies to use IFRS while the red circles represent 36 (67%) countries that require public companies to use IFRS. The following outliers are identified. All the countries in North Africa do not require domestic public companies to report using IFRS. All countries in South Africa require IFRS for domestic public countries. All countries in Central Africa except Sao Tome & Principe require the use of IFRS. All countries in West Africa except Cape Verde and Mauritania require the use of IFRS for domestic public countries. Nine out of eighteen countries in East African require IFRS for domestic public companies while the remaining nine do not require IFRS (see Figure ).

Madagascar is the only country that permits the voluntary use of IFRS for domestic companies. This means that the rest of 53 (98%) Africa countries either mandate the use of IFRS or do not permit the voluntary use of IFRS for domestic companies (see Figure ). Of the 54 African Countries 33 (61%) require the use of IFRSs by foreign companies for listings while and 21 (39%) do not require the use of IFRS for listings by foreign companies (see Figure ). On the use of IFRSs by SMEs, only 19 (35%) countries require the use of IFRS for SMEs while 35 (65%) do not require the use of IFRS by SMEs (see Figure ).

Figure 1. Mandatory adoption of IFRSs for domestic public companies.

Figure 2. Voluntary use of IFRS for domestic public companies.

Figure 3. IFRSs required for listing by foreign companies.

Figure 4. IFRSs required or permitted for SMEs.

3.2. Analysis of IFRS adoption and research output

Table , shows the relationship between the year of first IFRS adoption and number of research documents on Scopus database. The year of first adoption seems to have no statistically significant relationship with number of documents published yearly (coefficient: 0.004, p-value:0.513). This implies that year of IFRS first adoption is not connected to the number of documents produced yearly by the countries. IFRS adoption by domestic public companies seems to significantly and positively trigger the use for listing by foreign companies and by SMEs (coefficient: 0.689, p-value:0.000) and (coefficient: 0.2660, p-value:0.002) (see Table ).

Table 1. Regression results of year of first IFRS adoption and number of documents

Table 2. Regression results of IFRS adoption by domestic public companies, voluntary use for domestic public companies, listing by foreign companies and use by SMEs

3.3. Publication and citation count analysis

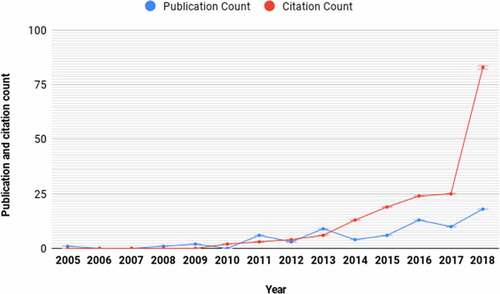

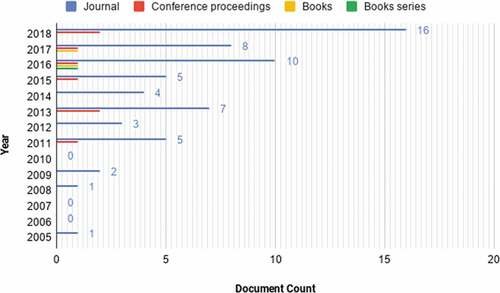

The yearly distribution of publication and citation was analysed as shown in Figure . Only 1 document was published in 2005 being the first with no citation that year. The title of the publication is “Compliance with IAS disclosure requirements by financial institutions in Uganda”. However, in 2018, 18 documents were published being the highest number published with 83 citations that year. Overall there is a steady increase in the volume of publication and a steep increase in the citation count in 2018. To further Statistical test the relationship between publication and citation count a correlation and regression analysis was conducted. Table depicts a strong and positive (86.2%) relationship between publication and citation count. Table shows that the number of publications significantly and positively impacts on the number of citations (coefficient: 3.463, p-value:0.000)

Figure 5. Yearly publication and Citation Count.

Table 3. Pearson Correlation Matrix for Publication and Citation count

Table 4. Regression results for Publication and Citation count

3.4. Publication access analysis

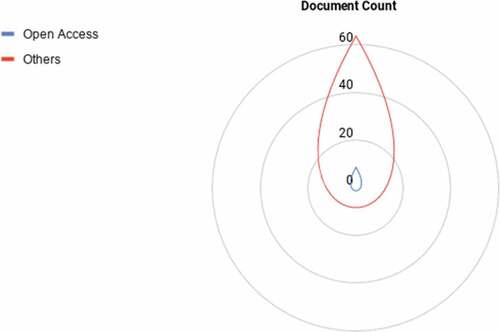

From the analysis of the corpus, only 9 (12.3%) of the 73 publications are open access while the 64 (87.7%) are not open access (see Figure ).

Figure 6. Publication Access.

3.5. Country distribution analysis

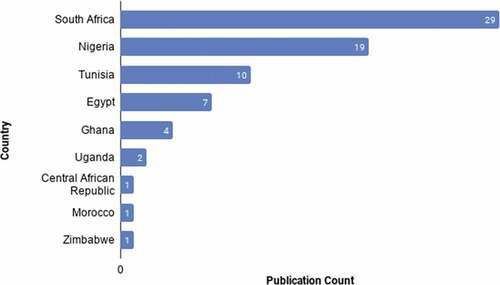

From Figure , only Nine countries in Africa contribute to at least one publication on IFRS research. South Africa contributes the highest number with 29 (39%). This is followed by Nigeria 19 (26%), Tunisia 10 (14%), Egypt 7 (9%), Ghana 4 (5%), Uganda 2 (3%). Central African Republic, Morocco and Zimbabwe contribute the least with only 1 (1%) publication each.

Figure 7. Number of publications per Country.

3.6. Subject area analysis

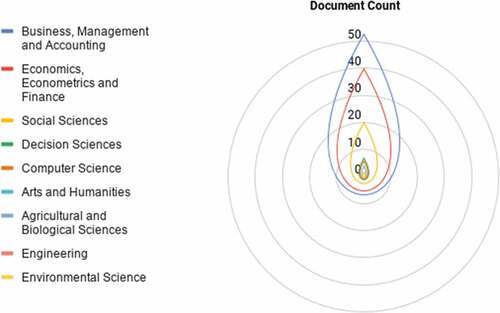

The exploration shows that 73 publications are linked to nine subject area however, some of the publications are linked to one or more subject area. From Figure , of the 136-count linked publication, 113(83.1%) publications are cumulatively linked to Business, Management & Accounting; Economics, Econometrics & Finance and Social Sciences while 23 (16.9%) are linked to Decision Sciences; Computer Science; Arts & Humanities; Agricultural & Biological Sciences; Engineering and Environmental Science. These imply that subject areas of Business, Management & Accounting; Economics, Econometrics & Finance and Social Sciences are dominant.

Figure 8. Subject Area.

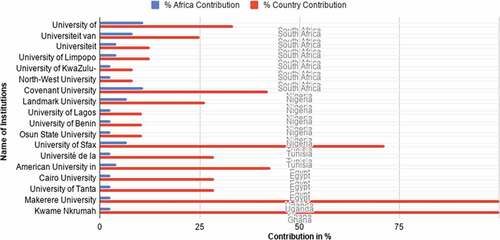

3.7. Top productive institution analysis

Figure shows the percentage of publications contributed by institutions in Country of existence and in Africa overall. From the analysis, only 18 institutions have more than one publication. University of Witwatersrand (10.9% in Africa and 33.3% in South Africa) and Covenant University (10.9% in Africa and 42.1% in Nigeria) contribute the highest with 8 publications. This is followed by Universiteit van Pretoria (8.2% in Africa and 25% in South Africa) with 6 publications. University of Sfax (6.8% in Africa and 71.4% in Tunisia) and Landmark University (6.8% in Africa and 26.3% in Nigeria) have 5 publications. Universiteit Stellenbosch (4.1% in Africa and 12.5% in South Africa), University of Limpopo (4.1% in Africa and 12.5% in South Africa) and American University in Cairo (4.1% in Africa and 42.8% in Egypt) have 3 publications. University of Lagos (2.7% in Africa and 10.5% in Nigeria), Cairo University (2.7% in Africa and 28.6% in Egypt), University of KwaZulu-Natal (2.7% in Africa and 8.3% in South Africa), University of Tanta (2.7% in Africa and 28.6% in Egypt), University of Benin (2.7% in Africa and 10.5% in Nigeria), Osun State University (2.7% in Africa and 10.5% in Nigeria), North-West University (2.7% in Africa and 8.3% in South Africa), Université de la Manouba (2.7% in Africa and 28.6% in Tunisia), Makerere University (2.7% in Africa and 100% in Uganda) and Kwame Nkrumah University of Science and Technology (2.7% in Africa and 100% in Ghana) all have 2 publications.

Figure 9. Most Productive Institution Analysis.

3.8. Document type analysis

The document type is presented in Figure . From the 73 documents, 62 (85%) are Journal publications, 8 (11%) are conference proceedings, 2 (3%) are books while only 1(1%) is a book series

Figure 10. Document Type Analysis.

3.9. Top published authors

In the analysis of the most prolific author with more than one publication in IFRS research, 21 authors from 8 institutions featured. Maroun, W. from University of Witwatersrand, Johannesburg, South Africa emerged top with 5 documents, 432 citations and 11 H-index. Otekunrin, A.O. from Landmark University, Omu Aran, Nigeria also has 5 documents but have 38 citations and 4 H-index.

3.10. Top research outlets

Research outlets with more than publication were considered in this analysis. From the table, South African Journal of Economic and Management Sciences published by Open Journals Publishing AOSIS has the highest number of publication (4 documents) with 6 citations and 0.58 cite scorelisted on Scopus in 1999. British Accounting Review Journal published by Elsevier, listed on Scopus in 1988 has the highest citation (34 citations) with 2 publications and 3.73 cite score. Table indicates that the year a journal is listed on Scopus has no statistical significant relationship with its citation count (coefficient: −0.086, p-value:0.720)

Table 5. Top 21 Prolific Authors

Table 6. Top 11 Research Outlets

Table 7. Regression analysis of Outlet Citation count and year in Scopus

3.11. Top cited documents

The title ‘Accounting and stock market effects of international accounting standards adoption in an emerging economy, authored by Elbannan M.A. emerged as the most cited article. The document was published in the review of Quantitative Finance and Accounting with 27 citations. The work aimed to examine the impact of mandatory adoption of International Accounting Standards (IASs) on Earnings quality and firm valuation. The study finds a significant and negative impact of IAS on firm valuation. Of the top 20 cited documents 8 (40%) are archival, 4 (20%) are interview, 3 (15%) are survey, 2 (10%) are literature review while only 1 (5%) are mixed method, content analysis and historical method, respectively. 10 (50%) of the documents seek to see the relationship, influence, effect and impact of IFRS. (see Table )

Table 8. Top 20 Cited Documents

4. Discussion

The study provides a bibliometric review on IFRSs adoption and the state of IFRS research publication in Africa. Key issues emanating from the study include; Despite the upward trend in the adoption of IFRSs in Africa, Northern Africa countries (Tunisia, Sudan, Algeria, Egypt, Morocco and Libya) have not come to terms in adopting IFRSs. Reasons to this are traced to the predominance of Islam oriented norms and religion that reinforces its economic, political, cultural and legal environment (Boolaky et al., Citation2018). Unlike Northern Africa, much of the other parts of Africa have adopted the civil law system without a mix while others adopted the common law which makes it easier for them to align easily with IFRS which was modelled after the common law. Another reason is if a country perceives its present financial reporting quality is high coupled with its ability to generate adequate internal capital then it may resist the conversion to a different financial reporting standard (Graham et al., Citation2017).

The first research document on Scopus database on IFRS in Africa was in 2005 despite its early adoption since 1993 in Zimbabwe. Also, the year 2018 produced the highest number of research documents on Scopus database with 18 publications. The year of first IFRSs adoption is not associated with the volume of publication. Indicatively, its envisaged that countries like Zimbabwe, Uganda and Kenya were foremost in the adoption of IFRSs as far back as 1993, 1998 and 1999, respectively, would be leading the pack in terms of volume of publications. However, this is not the case as the top five leaders in the volume of publication on IFRSs were South Africa (adopted IFRSs in 2005) Nigeria (adopted IFRSs in 2011), Tunisia (yet to adopt IFRSs), Egypt (yet to adopt IFRSs) and Ghana (adopted IFRSs in 2007). Interestingly, Tunisia and Egypt are yet to adopt IFRS but contributes to the top five in the volume of research output. This suggest that one of the influencing factors in the volume of publication is as a result of the strength of the research institutions and maybe not necessary the effect of the year of first IFRSs adoption. This is confirmed by the 2020 Times Higher Education World University rankings, the ranking has its top 5 research university in Africa located in South Africa, Nigeria and Egypt.

Even though, many Africa countries such as Angola, Cameroon, Central African Republic, Benin, Burkina Faso, Guinea, Guinea-Bissau, Senegal and Togo that have adopted IFRSs are yet to adopt it for SMEs. From the study, countries that mandate or voluntary allow the use of IFRSs for SMEs and for listing by foreign companies easily come to terms to adopting it for domestic public companies. Meanwhile, studies outside Africa are of the view that IFRS for SMEs still appears to be challenging in application, implementation, recognition and measurement (Perera & Chand, Citation2015; Quagli & Paoloni, Citation2012; Uyar & Güngörmüş, Citation2013). This raises a question though, if the adoption of IFRSs for SMEs in Africa was a rush?

The continued upward growth in the volume of publications and citations on IFRS research over the years in Africa indicated the continued interest of researcher in the field of IFRS. In fact, it is envisioned that the number will be on the increase as inquiries, investigations are made on the impact and quality of IFRSs in Africa. Rightly put, ‘Standards adoption requires a sustained, technical effort to review, revise, and formally promulgate updated requirements, including translation’ (IFAC, Citation2019).

There is still need for higher visibility of research on IFRS, from this review approximately 87 % of the publications are non-open access. This implies that, it is not freely available for anyone to benefit from reading or using the research. This is however, not encouraged for a topical area as IFRS undergoing developments. Relevant data and knowledge if freely accessible can impact on the adoption and implementation success. Open access publications remove the barriers that afflict researchers as it takes articles behind publishers’ paywalls available to other researchers for use (Martín-Martín et al., Citation2018).

The dominant subject areas on IFRSs research are Business, Management & Accounting; Economics, Econometrics & Finance and Social Sciences. While, 16.9% are linked to Decision Sciences; Computer Science; Arts & Humanities; Agricultural & Biological Sciences; Engineering and Environmental Science. This validates the multidisciplinary nature of IFRS research thus, going beyond the borders of Accounting. Despite, Africa comprising 12.5% of the world’s population, it global research output accounts for less than 1% (Duermeijer et al., Citation2018). More intriguing, only 18 institutions and 21 authors out of over 600 institutions in Africa contributes more than one publication to IFRS research. These institutions and authors are all in six African countries (South Africa, Nigeria, Tunisia, Egypt, Uganda and Ghana).

Journals publication represents 85% of the published articles with only 11% representing conference proceedings. Also, there is no significant relationship between the year a journal is listed on Scopus database and the citation count. This implies that other factors such as relevance and impact of research publication are vital metrics for measuring citation (Atayero, Citation2018). The study finds that 40% (being the highest) of the 20 most cited works are archival-based study. The increasingly use of archival data sources for research is due to its advantage of long-term evaluation that provides a more diverse participant population (Nicholas, Citation2014). Hence, the relevance and impact of such works thereby impacting on study citations.

5. Conclusion

The study offers a bibliometric analysis on the state of IFRS research in Africa. The goal of the study is to identify the pattern of publication, authorship, productive institution, document type, subject area, publication access, research outlet, year-wise growth and citations of 73 published articles listed on Scopus database between 2005 and 2018. The findings show that despite the upward trend in the adoption of IFRSs in Africa, Northern Africa countries (Tunisia, Sudan, Algeria, Egypt, Morocco and Libya) are yet to adopt IFRSs. The first research document on Scopus database on IFRS in Africa was in 2005 despite its early adoption since 1993 in Zimbabwe.

There is a continued upward growth in the volume of publications and citations over the years. Zimbabwe, Uganda and Kenya were foremost in the adoption of IFRSs since 1993, 1998 and 1999, respectively, yet are not top five in the volume of publications. The year of first IFRSs adoption is not associated with the volume of publication. Top five leaders in the volume of publication on IFRSs include countries (Tunisia and Egypt) yet to adopt IFRSs. Dominant subject areas on IFRSs research are Business, Management & Accounting; Economics, Econometrics & Finance and Social Sciences but, also includes other subject areas such as Decision Sciences; Computer Science; Arts & Humanities; Agricultural & Biological Sciences; Engineering and Environmental Science.

Only 18 institutions and 21 authors out of over 600 institutions in Africa contribute more than one publication to IFRS research. These institutions and authors are all in six African countries (South Africa, Nigeria, Tunisia, Egypt, Uganda and Ghana). There is no significant relationship between the year a journal is listed on Scopus database and the citation count. The study finds that 40% (being the highest) of the 20 most cited works are archival based study.

In conclusion, the substantial growth in the volume of published works and citation in indicative of researchers continued interest in IFRS research in Africa. Though the key limitation of the study is its restriction of the data to Scopus database as incorporating other database may alter the result of the study. However, the study provides a comprehensive example for this genre of research.

Acknowledgements

The Authors are grateful to the Covenant University Centre for Learning Resources (CLR) for providing access to the SCOPUS database used in the study.

Additional information

Funding

Notes on contributors

Omotola Ezenwoke

Omotola Ezenwoke holds a PhD in Accounting. She is a faculty of Covenant University, where she teaches Financial, Management Accounting and Accounting Information System courses at undergraduate and post-graduate level. Her research interests are in Financial Reporting, Accounting Information System and Accounting Education.

Williams Tion

Tion Williams holds a B.Sc. in Accounting from Bingham University. He is presently a Masters Student at Covenant University. His research interests are in Accounting Information System and Contemporary Electronic accounting.

References

- Atayero, A. (2018). Citation analytics: Data exploration and comparative analyses of CiteScores of open access and subscription-based publications indexed in Scopus (2014–2016). Data in Brief, 19, 198–20. https://doi.org/10.1016/j.dib.2018.05.005

- Baker, H. K., Kumar, S., & Pattnaik, D. (2020). Twenty-five years of the journal of corporate finance: A scientometric analysis. Journal of Corporate Finance, 101572. https://doi.org/10.1016/j.jcorpfin.2020.101572

- Boolaky, P. K., Omoteso, K., Ibrahim, M. U., & Adelopo, I. (2018). The development of accounting practices and the adoption of IFRS in selected MENA countries. Journal of Accounting in Emerging Economies, 8(3), 327-351 https://doi.org/10.1108/JAEE-07-2015-0052

- Chiu, V., Liu, Q., Muehlmann, B., & Baldwin, A. A. (2018). A bibliometric analysis of accounting information systems journals and their emerging technologies contributions. International Journal of Accounting Information Systems, 32, 24-4 https://doi.org/10.1016/J.ACCINF.2018.11.003

- Coetzee, S. A., Janse van Rensburg, C., & Schmulian, A. (2016). Differences in students’ reading comprehension of international financial reporting standards: A South African case. Accounting Education, 25(4), 306–326. https://doi.org/10.1080/09639284.2016.1191269

- Coetzee, S. A., & Schmulian, A. (2013). The effect of IFRS adoption on financial reporting pedagogy in South Africa. Issues in Accounting Education, 28(2), 243–251. https://doi.org/10.2308/iace-50386

- Dahawy, K. M. (2009). Company characteristics and disclosure level the Egyptian. International Research Journal of Finance and Economics, 34, 194–208. https://www.scopus.com/record/display.uri?eid=2-s2.072249105383&origin=resultslist&sort=plff&src=s&st1=Company+characteristics+and+disclosure+level+the+Egyptian&st2=&sid=a8491b8a60424554049240e4ac0359c0&sot=b&sdt=b&sl=72&s=TITLE-ABS-KEY%28Company+charac

- Duermeijer, C., Mohamed, A., & Schoombee, L. (2018). Africa generates less than 1 % of the world ’ s research. https://www.elsevier.com/connect/africa-generates-less-than-1-of-the-worlds-research-data-analytics-can-change-that

- Efobi, U. R. (2015). IFRS adoption and the environment: Is Africa closing her eyes to something? Advances in Sustainability and Environmental Justice, 17. https://doi.org/10.1108/S2051-503020150000017016

- Elbannan, M. A. (2011). Accounting and stock market effects of international accounting standards adoption in an emerging economy. Review of Quantitative Finance and Accounting, 36(2), 207–245. https://doi.org/10.1007/s11156-010-0176-1

- Ezenwoke, O., Ezenwoke, A., Eluyela, D., & Olusanmi, O. (2019). A bibliometric study of accounting information systems research from 1975-2017. Asian Journal of Scientific Research, 12(2), 167–178. https://doi.org/10.3923/ajsr.2019.167.178

- Fakhfakh, M. (2015). The readability of international illustration of auditor’s report: An advanced reflection on the compromise between normative principles and linguistic requirements. Journal of Economics, Finance and Administrative Science, 20(38), 21–29. https://doi.org/10.1016/j.jefas.2015.02.001

- Farag, S. M. (2009). The accounting profession in Egypt: Its origin and development. The International Journal of Accounting, 44(4), 403–414. https://doi.org/10.1016/j.intacc.2009.09.001

- Graham, A., Nandialath, A. M., Skaradzinski, D., & Rustambekov, E. (2017). Macroeconomic determinants of International Financial Reporting Standards (IFRS) Adoption: Evidence from the Middle East North Africa (MENA) Region. Accounting & Taxation, 9(1), 39-48. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3025011

- Houqe, M. N., & Monem, R. M. (2016). IFRS adoption, extent of disclosure, and perceived corruption: A cross-country study. International Journal of Accounting, 51(3) 363-378 https://doi.org/10.1016/j.intacc.2016.07.002

- IFAC. (2019). International standards: 2019 global status report. https://www.ifac.org/system/files/publications/files/IFAC-International-standards-2019-global-status-report

- Kouki, A. (2015). Accounting valuation models under international financial reporting standards: Evidence from some European listed companies. International Journal of Managerial and Financial Accounting, 7(1), 82. https://doi.org/10.1504/IJMFA.2015.067504

- Maradona, A. F., & Chand, P. (2018). The pathway of transition to International Financial Reporting Standards (IFRS) in developing countries: Evidence from Indonesia. Journal of International Accounting, Auditing and Taxation, 30, 57–68. https://doi.org/10.1016/j.intaccaudtax.2017.12.005

- Maroun, W. (2017). Assuring the integrated report: Insights and recommendations from auditors and preparers. The British Accounting Review, 49(3), 329–346. https://doi.org/10.1016/j.bar.2017.03.003

- Maroun, W. (2018). Modifying assurance practices to meet the needs of integrated reporting: The case for “interpretive assurance”. Accounting, Auditing and Accountability Journal, 31(2), 400–427. https://doi.org/10.1108/AAAJ-10-2016-2732

- Maroun, W., & van Zijl, W. (2014). Isomorphism and resistance in implementing IFRS 10 and IFRS 12. British Accounting Review, 48(2), 220-239. https://doi.org/10.1016/j.bar.2015.07.003

- Martín-Martín, A., Costas, R., Van Leeuwen, T., & Delgado López-Cózar, E. (2018). Evidence of open access of scientific publications in Google Scholar: A large-scale analysis. Journal of Informetrics, 12(3), 819–841. https://doi.org/10.1016/j.joi.2018.06.012

- Motelle, S., & Biekpe, N. (2015). Financial integration and stability in the Southern African development community. Journal of Economics and Business, 79(C), 100–117. https://doi.org/10.1016/j.jeconbus.2015.01.002

- Negash, M. (2008). Liberalisation and the value relevance of accrual accounting information: Evidence from the Johannesburg securities exchange. Afro-Asian Journal of Finance and Accounting, 1(1), 81. https://doi.org/10.1504/AAJFA.2008.016892

- Newman, W., Edmore, T., Milondzo, K., & Ongayi, W. V. (2016). A literature review on the impact of IAS/IFRS and regulations on quality of financial reporting. Risk Governance and Control: Financial Markets and Institutions, 6(4), 102–109. https://doi.org/10.22495/rcgv6i4art13

- Newman, W., Mhaka, C., Katiyo, E. M., Ongayi, W., & Milondzo, K. (2017). An Evaluation of the effectiveness of financial statements in disclosing true business performance to stakeholders in hospitality industry (A case of Lester-Lesley limited). Academy of Accounting and Financial Studies Journal, 21(3). https://www.abacademies.org/articles/an-evaluation-of-the-effectiveness-of-financial-statements-in-disclosing-true-business-performance-to-stakeholders-in-hospitality-6735.html

- Nicholas, A. T. (2014). Archival data analysis introduction. The International Journal of Aging and Human Development, 79(4), 323–325. https://journals.sagepub.com/doi/abs/10.1177/0091415015574188

- Nnadi, M., & Soobaroyen, T. (2015). International financial reporting standards and foreign direct investment: The case of Africa. Advances in Accounting, 31(2), 228–238. https://doi.org/10.1016/j.adiac.2015.09.007

- Odoemelam, N., Okafor, R. G., & Ofoegbu, N. G. (2019). Effect of international financial reporting standard (IFRS) adoption on earnings value relevance of quoted Nigerian firms. Cogent Business and Management, 6(1). https://doi.org/10.1080/23311975.2019.1643520

- Otekunrin, A. O., Iyoha, F. O., Uwuigbe, U., & Uwuigbe, O. R. (2017). Adoption of international financial reporting standard, capital structure and profitability of selected quoted firms in Nigeria. Proceedings of the 29th International Business Information Management Association Conference - Education Excellence and Innovation Management through Vision 2020: From Regional Development Sustainability to Global Economic Growth, Milan, Italy.

- Otekunrin, A. O., Nwanji, T. I., Olowookere, J. K., Egbide, B. C., Fakile, S. A., Lawal, A. I., Ajayi, S. A., Falaye, A. J., & Eluyela, D. F. (2018). Financial ratio analysis and market price of share of selected quoted agriculture and agro-allied firms in Nigeria after adoption of international financial reporting standard. Journal of Social Sciences Research, 4(12), 736-744. https://doi.org/10.32861/jssr.412.736.744

- Perera, D., & Chand, P. (2015). Issues in the adoption of international financial reporting standards (IFRS) for small and medium-sized enterprises (SMES). Advances in Accounting, 31(1), 165–178. https://doi.org/10.1016/j.adiac.2015.03.012

- Quagli, A., & Paoloni, P. (2012). How is the IFRS for SME accepted in the European context? An analysis of the homogeneity among European countries, users and preparers in the European commission questionnaire. Advances in Accounting, 28(1), 147–156. https://doi.org/10.1016/j.adiac.2012.03.003

- Trimble, M. (2018). A reinvestigation into accounting quality following global IFRS adoption: Evidence via earnings distributions. Journal of International Accounting, Auditing and Taxation, 33, 18–39. https://doi.org/10.1016/j.intaccaudtax.2018.09.001

- Urban, B., & Govender, D. P. (2012). Empirical evidence on environmental management practices. Engineering Economics, 23(2), 209-215. https://doi.org/10.5755/j01.ee.23.2.1549

- Uwuigbe, U., Emeni, F. K., Uwuigbe, O. R., & Maryjane, A. C. (2016). IFRS adoption and accounting quality: Evidence from the Nigerian banking sector. Corporate Ownership and Control, 14(1), 287–294. https://doi.org/10.22495/cocv14i1c1p12

- Uyar, A., & Güngörmüş, A. H. (2013). Perceptions and knowledge of accounting professionals on IFRS for SMEs: Evidence from Turkey. Research in Accounting Regulation, 25(1), 77–87. https://doi.org/10.1016/j.racreg.2012.11.001

- Van Zijl, W., & Maroun, W. (2017). Discipline and punish: Exploring the application of IFRS 10 and IFRS 12. Critical Perspectives on Accounting, 44, 42–58. https://doi.org/10.1016/j.cpa.2015.11.001

- Welbeck, E. E. (2017). The influence of institutional environment on corporate responsibility disclosures in Ghana. Meditari Accountancy Research, 25(2), 216–240. https://doi.org/10.1108/MEDAR-11-2016-0092

- Wingard, C., Bosman, J., & Amisi, B. (2016). The legitimacy of IFRS an assessment of the influences on the due process of standard-setting. Meditari Accountancy Research, 24(1), 134–156. https://doi.org/10.1108/MEDAR-02-2014-0032

Appendix A.

Data Search Query on Scopus database

The resultant search query eventually used to search for documents is framed thus: TITLE-ABS-KEY (international AND financial AND reporting AND standards) AFFILCOUNTRY (“Nigeria” OR “Ethiopia” OR “Egypt” OR “Democratic Republic of the Congo” OR “South Africa” OR “Tanzania” OR “Kenya” OR “Sudan” OR “Algeria” OR “Uganda” OR “Morocco” OR “Mozambique” OR “Ghana” OR “Angola” OR “Ivory Coast” OR “Madagascar” OR “Cameroon” OR “Niger” OR “Burkina Faso” OR “Mali” OR “Malawi” OR “Zambia” OR “Somalia” OR “Senegal” OR “Chad” OR “Zimbabwe” OR “South Sudan” OR “Rwanda” OR “Tunisia” OR “Guinea” OR “Benin” OR “Burundi” OR “Togo” OR “Eritrea” OR “Sierra Leone” OR “Libya” OR “Republic of the Congo” OR “Central African Republic” OR “Liberia” OR “Mauritania” OR “Namibia” OR “Botswana” OR “Gambia” OR “Equatorial Guinea” OR “Lesotho” OR “Gabon” OR “Guinea-Bissau” OR “Mauritius” OR “Swaziland” OR “Djibouti” OR “Réunion” OR “Comoros” OR “Cape Verde” OR “Western Sahara” OR “Mayotte” OR “São Tomé and Príncipe” OR “Seychelles” OR “Saint Helena” OR “eSwatini”) AND (EXCLUDE (PUBYEAR, 2019)) AND (EXCLUDE (SUBJAREA, “MEDI”) OR EXCLUDE (SUBJAREA, “EART”) OR EXCLUDE (SUBJAREA, “IMMU”) OR EXCLUDE (SUBJAREA, “MATE”) OR EXCLUDE (SUBJAREA, “NURS”) OR EXCLUDE (SUBJAREA, “PSYC”) OR EXCLUDE (SUBJAREA, “VETE”)) AND (EXCLUDE (AFFILCOUNTRY, “Malaysia”) OR EXCLUDE (AFFILCOUNTRY, “United Arab Emirates”) OR EXCLUDE (AFFILCOUNTRY, “United Kingdom”) OR EXCLUDE (AFFILCOUNTRY, “France”) OR EXCLUDE (AFFILCOUNTRY, “Saudi Arabia”) OR EXCLUDE (AFFILCOUNTRY, “United States”) OR EXCLUDE (AFFILCOUNTRY, “Belgium”) OR EXCLUDE (AFFILCOUNTRY, “Canada”) OR EXCLUDE (AFFILCOUNTRY, “Germany”) OR EXCLUDE (AFFILCOUNTRY, “Japan”).