Abstract

This study examines customer interaction in the banking sector. These interactions are strongly influenced by the dimensions of interpersonal trust, namely benevolence, cognitive, and affective trust. A survey was conducted in the banking sector of Sokoto State, Nigeria. A questionnaire was administered to 500 bank customers from 10 commercial banks, in which the respondents were asked to select their preferences based on a five-point Likert scale. The data were analyzed using PLS-SEM version 3.2. The results showed that benevolence, cognitive, and affective trust positively influence customer interaction in the banking sector in Sokoto State, Nigeria. In financial transactions, benevolence trust, in the form of care and protection from harm by the bank staff; cognitive trust, manifesting as reliability, reputation, competence, and commitment of bank staff; and affective trust, in the form of attention, emotional connection, and empathy shown by bank staff positively influence customer interaction in a bank. Bank executives and policymakers can draw lessons from these results and create awareness within the banking sector on factors that contribute toward retaining and attracting new customers. This will contribute significantly to the growth and development of the banking sector.

PUBLIC INTEREST STATEMENT

The influence of globalization and modernization in the Nigerian banking sector has raised concerns about customers’ financial interactions with a bank. These complexities of modern banking institutions have prompted this inquiry into the influence of interpersonal trust, and its various dimensions vis-à-vis customer interaction with the bank with the aim of bridging the gap in knowledge. This study was conducted on bank customers in Sokoto State, Nigeria. It investigates the influence of benevolence, cognitive, and affective trust on customer interaction in a bank. Benevolence trust, in the form of care shown to customers by bank staff during financial interactions, cognitive trust, manifesting as reputation and commitment of bank staff during financial interactions, and affective trust, in the form of emotional connection and empathy shown by bank staff influence customer interaction with the bank positively. These results indicate factors that contribute toward retaining existing and attracting new customers to the banking sector.

1. Introduction

Customer interaction is important in the study of organizations in society (Foss et al., Citation2011; Schaarschmidt et al., Citation2018) because it offers a strategic opportunity for organizations to weaponize it to achieve optimal performance, including growth and development of the firm. Deep customer interaction, as well as switching costs, affect a client’s ability to change business organizations easily (Brush et al., Citation2012), thus making clients more dependent on a particular business organization and more susceptible to new products and services developed by that organization. This indicates that the ability of organizations to establish linkages with their customers is fundamental to their growth and development (Danneels, Citation2003). This interaction is imperative because customers are considered important stakeholders in an organization (Matthing et al., Citation2004). Therefore, customer interaction is significant for the innovation of goods and services and can support growth and development in organizations.

To date, most research on customer interaction has focused on customer satisfaction (Cameron et al., Citation2016; Muhammad et al., Citation2011), innovation (Laursen & Salter, Citation2006; Uzkurt et al., Citation2013), and service development (Alam, Citation2011; Ozdemir et al., Citation2007). AlHarbi et al. (Citation2016) suggested that organizations should develop a robust approach to customer interaction in order to arrive at a holistic understanding of customers’ perspectives toward products and services. Understanding customer interaction is fundamental for supporting policy and decision-making in organizations, especially in making the right decisions to improve their products and services. Alam (Citation2011) noted that customer interaction is so important that organizations should develop new products and services with inputs from their customers. Most studies on customer interaction have focused on improving the organization rather than on understanding what affects client interactions with the organization positively or negatively.

Vinokurova (Citation2019) suggested that the best way to change customers’ preferences to accommodate new organizational products is to convince them that a combination of qualities offered by the organization is more valuable than the various qualities that the customer has consumed individually. Cameron et al. (Citation2016) indicated that older people are generally satisfied with their interactions with service providers in the organization. Their satisfaction was largely because of repeated and face-to-face interactions, reliability, and integrity ensured by service providers. Laursen and Salter (Citation2006) posited that 66% of their sample of manufacturing firms in the United Kingdom had indicated the importance of customers as a source of knowledge for innovation, and 16% rated this source very high. Von Hippel (Citation2005) highlighted that customers are the genesis of the growth and development of organizations. He explained how customer-oriented products and services were often invented, prototyped, and field-tested by users before being modernized and introduced to the end market by established firms. Given the implication that customers have in an organization, the dearth of research on the antecedents of customer interaction is surprising.

To address this problem, this study investigates the antecedents of customer interaction in the banking sector. Understanding customer interaction and its antecedents can enrich the literature by adding insights on ways to sustain and attract new customers as well as improve growth and development. Letki (Citation2006) argued that the interpersonal dimension of trust is essential in addressing issues associated with interactions with modern organizations. The importance of the interpersonal dimension of trust was discussed extensively after the 2008 global economic crisis, with individuals prioritizing economic interactions associated with trust-building at an interpersonal level (Habibov & Afandi, Citation2015). This indicated that customers showed positive signs while engaging in business transactions at an interpersonal level after the global economic crisis. This is because customers saw that they could derive greater benefit from face-to-face interactions with the personnel of the organizations they were dealing with (Krot & Rudawska, Citation2016). It is crucial to study the interpersonal dimension of trust in an organization (Evans & Krueger, Citation2009; Lewicki et al., Citation2006) as organizations are formal settings with people working at individual or group levels to promote its objectives. Therefore, this study investigates the influence of the interpersonal dimension of trust on customer interaction in the banking sector in Sokoto State, Nigeria.

2. Interpersonal dimensions of trust and organization

The interpersonal dimension of trust has received much attention in research in recent years. Tan and Sutherland (Citation2004) defined the interpersonal dimension of trust as an individual’s confidence vested in another party based on their face-to-face interactions. Daniele and Geys (Citation2015) posited that interpersonal connections that exist between individuals and personnel of an organization can prevent parties involved from engaging in distrustful behavior during their interactions. Krot and Rudawska (Citation2016) highlighted that customers derived benefits from face-to-face interactions with the personnel of an organization. Adiele et al. (Citation2018) argued that interpersonal relationships at workplace significantly influenced customer satisfaction in the deposit banks in Port Harcourt. Nejad et al. (Citation2016) noted that face-to-face communication with bank staff, and close acquaintances were seen as the most reliable and persuasive means of acquiring information related to banking. Customers believe that face-to-face interactions with banking staff gives them the opportunity to acquire assistance that may otherwise be unavailable in formal interactions with the banking industry.

Mosch and Prast (Citation2008) established that the interpersonal dimension of trust plays an essential role in influencing customers’ trust in the banking sector in the Netherlands. They argued that citizens in the Netherlands trust each other, and those who trust each other display higher trust in organizations, including financial ones. The interpersonal dimension of trust is fundamental to a study of individual confidence levels in the banking sector. Scholars have added that healthcare professionals and providers (Russell, Citation2005) and honesty of staff (Poon et al., Citation2017) are essential in sustaining or destroying the interpersonal dimension of trust in the organization. The use of benevolence, cognitive, and affective trust in customer interaction with the banking sector has remained underexplored by researchers. Benevolence trust is concerned with the care, prevention of harm, and protection of information offered by banking staff to their customers during their financial interactions. Cognitive trust focuses on the reliability, reputation, competence, and commitment of the banking staff toward customers during their financial interactions. Affective trust pertains to the attention, emotional connection, and empathy shown by banking staff toward their customers during financial interactions. There is a dearth of research on these constructs on customer interaction in the banking sector of Sokoto State, Nigeria.

Sokoto State is a conservative society that values mechanical rather than organic solidarity. Citizens feel more connected with others who share their common values and beliefs. The most common values and beliefs in Sokoto State are that a human being can be trusted, and that the best connection is through religion, which encourages face-to-face interactions. People tend to define their interactions with the banking staff by operating with the belief that a positive outcome is within reach during and after their business interactions. Sokoto State citizens tends to show interest in face-to-face interactions with banking staff who share their values and beliefs. They easily develop confidence in staff who come from their social background, speak their language, and wear the same type of clothes. This perception prompted research on the influence of the interpersonal dimension of trust (benevolence, cognitive, and affective trust) on customer interaction in the banking sector of Sokoto State, Nigeria. Therefore, this study explores the dispositional dimension of trust: benevolence (McKnight & Chervany, Citation2001), cognitive, and affective trust (Lewis & Weigert, Citation1985) on customer interaction in the banking sector of Sokoto State, Nigeria.

3. Benevolence trust

According to McKnight and Chervany (Citation2001), benevolence trust is a belief developed by an individual that other people care and are also motivated to act in one’s interest. Peng and Moghavvemi (Citation2015) asserted that customers believed that service providers will act with integrity in performing their job, make achievable and good-faith agreements, act ethically, and agree to provide clients with true information to influence customer interaction. Wu et al. (Citation2017) indicated that benevolence trust reduces uncertainties and feelings of anxiety and increases feelings of optimism, symbolic benefits, and perceived price value while adopting daily eco-friendly products. Svare et al. (Citation2019) opined that perceived benevolence, ability, and integrity influence different aspects of network interaction and outcomes against the background of the network members’ perception risk. Nguyen (Citation2016) described that competence and benevolence of employees can influence customer loyalty. Benevolence can be used to increase the impact of competence on customer loyalty. The literature reviewed identifies the importance of benevolence trust in the study of social and business situations in society.

Benevolence trust is fundamental to customer interaction with a business organization wherein they have limited knowledge of its operations. Customers feel more comfortable when they have people in the organization who are ready to provide them with personal assistance when the need arises. Benevolence trust is concerned with commonality, and the goodwill of people involved in the interaction (Drake & Mehta, Citation2006). Colquitt and Salam (Citation2009) posited that ability, benevolence, and integrity are the most important aspects of trustworthiness as they cultivate a sense of trust in the leader by followers within their organizations. This study argues that the idea of benevolence is necessary because of the dynamic nature of the banking sector, as well as its products, and services. Customers are now looking for the banking sector that can afford face-to-face interactions, which can help reduce the anxiety and uncertainty in the system. However, despite the importance of benevolence trust, the extent to which the staff are ready to provide help to customers remains unexamined (Xu et al., Citation2013). Therefore, this study attempts to use benevolence trust as one of the sub-scales to investigate the influence of the interpersonal dimension of trust on customer interaction in the banking sector in Sokoto State, Nigeria. Thus, the following hypothesis is proposed:

Hypothesis 1: Benevolence trust is positively related to customer interaction in the banking sector.

4. Cognitive trust

Cognitive trust is a strategy developed by an individual to choose who to trust based on a reasonable assessment of how trustworthy the person or the organization is (Chhetri, Citation2014; Lewis & Weigert, Citation1985). Zur et al. (Citation2012) showed that cognitive trust provides individuals with the ability to evaluate the performance and commitment of the staff of an organization. Parayitam and Papenhausen (Citation2016) asserted that cognitive trust has a positive impact on an individual’s decision to be committed to another party, as well as team effectiveness. Eastlick and Lotz (Citation2011) posited that cognitive and institutional information have comparable and contrasting effects on purchasing intent through initial trust-building. Yang et al. (Citation2009) indicated that cognitive trust is related to the work that has occurred on numerous occasions, which later establishes reputation. This indicates that a party involved in the interaction analyzes the motto of the relationship to see if it has satisfied them or not. Morrow et al. (Citation2004) argued that cognitive trust enables a party to determine another’s trustworthiness by assessing facts in both the transaction’s features and the characteristics of the other party to the transaction. This suggests that cognitive trust is essential in understanding an individual’s interactions with another party.

The importance of cognitive trust has been established in social and business interactions. Chua et al. (Citation2008) suggested that cognitive trust is associated with the willingness of an individual to be vulnerable to another person based on the belief in their ability and integrity in their business interactions. In the study of an organization like a bank, the staff play an important role in establishing cognitive trust in the minds of their customers, as this form of trust is special to customers since personal information will be shared between the parties involved. Thus, if the staff has a good reputation and commitment, most encounters will serve as an opportunity to affirm or reject previous expectations of customers in the organization. Johnson and Grayson (Citation2005) argued that service delivery performance contributes positively to cognitive trust. The greater the service delivery, the greater the individual cognitive trust. The lower the service delivery, the lower the level of individual cognitive trust. As cognitive trust is fundamental to individual interactions with another party, this study explores it as a sub-construct to investigate interpersonal dimensions of trust on customer interaction in the banking sector in Sokoto State, Nigeria. Thus, the following hypothesis is proposed:

Hypothesis 2: Cognitive trust is positively related to customer interaction in the banking sector.

5. Affective trust

Affective trust is associated with emotional connections developed in life based on interpersonal relationships with other individuals or personnel in an organization (Ha et al., Citation2011). The central component of affective trust relies on the emotional characteristics of a specific partner (Fard, Citation2012). The emotional connection lays the foundation for an individual to develop confidence in the organization. This means as emotional connections deepen, trust in a partner may venture beyond what is justified by available knowledge (Udechukwu et al., Citation2012). Hanzaee and Norouzi (Citation2012) argued that affective trust has a significant influence on customers’ anticipation of future interactions with a service provider. Wang et al. (Citation2010) indicated that customer interaction with the personnel of an organization grows over time and can reach a very high level, thus creating a deeper form of trust that implies a strong affective attachment to both the trustee and the relationship. Andersen and Kumar (Citation2006) posited that affective trust creates positive emotions that create a reciprocal attachment between the customer and the seller, favoring stronger and more durable personal links. Such a connection helps define future interactions between customers and organizations.

Considering the aforementioned literature, it is established that affective trust is fundamental in understanding an individual’s relationship in a social and business organization. Wasti et al. (Citation2011) found that affective trust grows over time as the parties involved continue to engage in a social exchange by showing reciprocated and genuine care, thus developing a relational bond. Webber (Citation2008) confirmed that affective trust is closely related to the perception that a partner’s actions are motivated by emotions. This form of trust is concerned with strong personal bonds developed to curtail the challenges associated with social and business relationships in society (Chen et al., Citation2014). Customers participate in the ongoing service delivery process and are exposed to organizational socialization that produces positive effects and elicits customers’ commitment. Johnson and Grayson (Citation2005) argued that emotional exchange is a critical and ongoing part of consumer-service relationships and the basis for trusting bonds. This relates to the argument in this study that bank customers tend to develop deep emotions through interpersonal interactions with the personnel of the banking sector to protect themselves from issues related to the institution, as business relationships built through emotional connections are difficult to break. This paper therefore explores affective trust as a sub-construct to investigate the influence of the interpersonal dimension of trust on customer interaction in the banking sector in Sokoto State, Nigeria. Thus, the following hypothesis is proposed:

Hypothesis 3: Affective trust is positively related to customer interaction in the banking sector.

6. Theoretical framework

6.1. Facework commitment

This study employed Giddens (Citation1990) assumption on facework commitment in modern society and institutions to explain the interpersonal dimension of trust on customer interaction in the banking sector in Sokoto State, Nigeria. Facework commitments (also called interpersonal trust) are concerned with the ties that are established, expressed, and maintained by individuals at the interpersonal level (Giddens, Citation1990, p. 80). Such behavior is concerned with trust relations established by individuals based on the integrity of the representative of an institution. Giddens considered facework commitment or interpersonal trust as learned behavior that is negotiated between an individual and personnel of an organization (Ward & Meyer, Citation2009). For example, customers tend to interact at an interpersonal level with the banking sector and its officials based on formal organizational ethics. This interaction forms the basis of establishing close contact that will directly or indirectly motivate customers to show commitment to the banking sector. The levels of professionalism, mannerism, and personality of the representative tend to influence customers’ impressions and expectations. Hence, individuals in society relate to the representative of an organization based on the reputation and image created (Meyer et al., Citation2008). Gidden referred to the point marking this interaction between individuals and the staff of an organization as the access point.

In Giddens’ words (Giddens, Citation1990), the access point refers to the place of interaction between individuals and the representatives of abstract systems or organizations. This is a place where abstract systems or organizations are not only vulnerable, but also function as junctions where trust can be preserved or built up (Giddens, Citation1990, p. 88). The access point is concerned with where individuals meet and interact with the representatives of an abstract or expert system, or organization. They are incidents or places where individuals who have little or no knowledge of a phenomenon, establish a connection with the representative of the abstract system who knows about the social phenomenon in question. It is also a place where trust is established and maintained among individuals and in the organization in general, thus the professionalism and mannerism of the representative plays a major part in reducing the vulnerability associated with the abstract system (Schlichter, Citation2010).

The discussion of facework commitment or interpersonal trust, as it is known, can be found in different organizational settings. Meyer and Ward (Citation2008) explained that the trust that patients place in healthcare professionals and their guidance was shown to promote positive results in the organization. This study revealed that the professionalism and mannerism through which the personnel of the healthcare department present themselves influence the trust that an individual or patient has on the system in general. This argument relates to the fact that facework commitment or interpersonal trust involves setting up a beneficial relationship between two important parties, that is, the trusting party and the one to be trusted (Delgado-márquez et al., Citation2013). Such a relationship is thus established and promoted to develop confidence in the mind of the individual based on the fact that the activities of the other party in an organization cannot be monitored and explained by a layman.

The relationship between doctor and patient is complicated, as the latter lacks the knowledge of the hospital’s operation as an institution or a system. A patient develops confidence in doctors, who they see as the access point in their interactions with them. Throughout the doctor-patient interaction cycle, the act of doctors can reinforce the patient’s trust in the system or raise concerns about the quality of the products and services they provided (Jalava, Citation2006). For example, whereas a good treatment can strengthen the patient’s confidence, poor treatment can strengthen distrust and suspicion. This study corresponds with the literature above that the banking sector’s ability to understand the importance of interpersonal interactions between customers and the banking sector representative will go a long way in creating trust in the system. A failure to identify the importance of the interpersonal dimension of trust in determining customer interaction in the banking sector may lead to mistrust and may affect customers’ patronage of the system in general.

An account of how benevolence, cognitive, and affective trust may be applied to understand facework commitment to trust in the banking sector will now be presented. Benevolence trust is a belief developed by an individual that other people care and are also motivated to act in one’s interest (McKnight & Chervany, Citation2001). For benevolence trust, the ability of the bank staff to show care and protect customer information can influence their financial interactions with the system. Cognitive trust is a strategy developed by an individual to choose who to trust based on a reasonable assessment of how trustworthy the person or the organization is (Chhetri, Citation2014; Lewis & Weigert, Citation1985). For cognitive trust, the ability of the bank staff to show their commitment and competency to customers during their business interactions can influence their financial interactions. Affective trust is associated with emotional connections developed in life based on interpersonal relationships with other individuals or personnel in an organization (Ha et al., Citation2011). For affective trust, the ability of banking staff to show attention and empathy toward their customers during a transaction can influence their financial interactions. To understand the impact of facework commitment (interpersonal dimension of trust) on customer interaction in the banking sector, it is important to explore benevolence, cognitive, and affective trust.

6.2. Method

A quantitative research method was used to examine the influence of the interpersonal dimension of trust on customer interaction in the banking sector in Sokoto State, Nigeria. Quantitative research offers approaches to test objectives and theories by examining the relationships among variables (Creswell, Citation2013). These variables can be measured on instruments so that the data generated in numbers can be analyzed using statistical tools. In this study, data were generated in numerical form, and a code book was developed so that the researcher could ascertain how to categorize the data so generated. The data were later inserted into Statistical Package for the Social Sciences (SPSS) software version 20.

6.3. Sampling

The study used a non-probability sampling method in selecting the respondents by employing a purposive sampling technique. This technique is effective, as it enables a deliberate choice of informants or respondents owing to their qualities (Tongco, Citation2007). This strategy gives the researcher the ability to decide on the information needed and to choose people who can and are able to provide the information based on their expertise or experience. Owing to privacy issues, the researcher did not acquire a sampling frame from the banking sector. The sample size for this study is 500 respondents. Purposive sampling was used to select 50 respondents from 10 commercial banks, namely Access Bank, Eco Bank, First Bank, First City Monument Bank, Guaranty Trust Bank, Jaiz Bank, Polaris Bank, Union Bank, United Bank of Africa, and Zenith Bank.

The 10 commercial banks were chosen using 4 criteria, in conformity with global trends toward the modernization of financial institutions. First, because of the customers’ demand for better banking products and services, these banks introduced various types of electronic banking, such as automated teller machines (ATMs), the Internet, telephone, and mobile banking apps. Second, this group of banks have between two to four ATMs around or in the vicinity of their banks. These factors qualify these banks as having the highest number of ATMs. This has minimized congestion and queues in banking halls. Third, this group of banks has also introduced customer-oriented rules and regulations, which were welcomed by the Basle II Plus Compliance Committee that supervised Nigerian banks (Mbah et al., Citation2014). Fourth, the 10 banks have at least 2 branches within Sokoto metropolis and this has significantly positioned them as capable of serving customers better and seamlessly offering products and services.

6.4. Data collection

The recruitment of the participants occurred outside the banking halls. This offered the researcher room to engage in open conversations with each individual to identify whether they had an active bank account. It also helped identify individuals who interacted or were still interacting with the banks under study. The participants were given information on what the study was about. Before they answered the questionnaire, details on the study were provided and their informed consent was taken. They were told that this study was voluntary, and that the questionnaire was designed to conceal their identities and maintain their anonymity. When they agreed to participate, they were asked to sign a consent form. Then, they were asked to fill up a self-administered questionnaire that was collected immediately after they finished. The data collection took place over six months, between February and July 2019. A response rate of 100% was obtained, as purposive sampling allows a researcher to solicit respondents until the expected sample is achieved.

6.5. Ethical consideration

The Jawatankuasa Etika Penyelidikan (Manusia)—JEPeM of Universiti Sains Malaysia granted ethical clearance for the study with clearance code: USM/JEPeM/18080377. The researcher observed ethical requirements, which included confidentiality, anonymity and the right to withdraw from the study at any stage.

6.6. Instrument development

The questionnaire used in this analysis comprised three different sections. Section A focused on the demographic characteristics of the respondents. Section B comprised statements that measured the dimensions related to the research questions. Section C contained statements measuring the frequency of customer interaction in the banking sector. Section B was divided into three dimensions of trust: dispositional, institutional, and interpersonal. This study focuses solely on the interpersonal dimension of trust (benevolence, cognitive, and affective trust) as the researcher could not combine the three multi-dimensional trust axes (dispositional, institutional, and interpersonal) in one research article.

To gather data on the impact of the interpersonal dimension of trust (benevolence, cognitive, and affective trust) on customer interaction in the banking sector, customers were asked to complete five benevolence trust items adapted from Colquitt et al. (Citation2007), five cognitive trust items adapted from Erdem and Ozen (Citation2003), five affective trust items adapted from Dadzie et al. (Citation2018), and seven customer interaction items formulated based on Schaarschmidt et al. (Citation2018) and Matthing et al. (Citation2004). All items were assessed on a 5-point Likert scale (strongly disagree to strongly agree) response format. The items were reduced to 15 after the pilot study because of the ambiguity in some items that required an explanation before they could be answered.

6.7. Pilot study

Data were collected from 200 bank customers over two months during the pilot. The 20 items measuring the “interpersonal dimension of trust” were subject to principal component analysis (PCA) using SPSS version 20. Before performing PCA, the suitability of data for factor analysis was assessed. The inspection of the correlation matrix revealed the presence of many coefficients of.3 and above. The KMO value was .893, exceeding the recommended value of .6 (Kaiser, Citation1970; Citation1974), and Bartlett’s Test of Sphericity was .000 (where p < .05). This reached statistical significance and supported the factorability of the correlation matrix. The two components solution explained a total of 56.3% of the variance, with Component 1 contributing 12% and Component 2 contributing 9%. To support the interpretation of these two components, Oblimin rotation was performed. The rotated solution revealed the presence of a simple structure (Thurstone, Citation1947), with both components showing a number of strong loadings and all variables loading substantially only on one component. Component extraction values ranged between .868 and .498 for Component 1 and .591 and −.305 for Component 2, showing a high concentration of values above .3 in all clusters. All extracted components had high values that are concentrated in two clusters and were thus retained. All commonalities were above .4, ranging from .872 to .477, and were thus retained. There was a positive correlation (r = 472) between the factors. The results supported the use of the items for data collection.

6.8. Data analysis

This study used the Partial Least Square (PLS) approach using SmartPLS version 3.2 to analyze the data. It also used the bootstrapping method (10000 resamples) to evaluate the level of significance for loadings and path coefficients.

7. Results

7.1. Demographic characteristics of participants

From the 500 respondents, a total of 309 (61.8 percent) were male, while 191 (38.2 percent) were female. The age group of 18 to 25 years (37.6 percent) and 26 to 33 years (32.1 percent) constituted the biggest portion of the sample, followed by the age group of 34 to 41 years (14.9 percent). About 44.4 percent possessed bachelor’s degrees, 15.7 percent possessed ordinary national diplomas, and 14.7 percent had secondary school certificates. Only 6.8 percent had a master’s degree and higher diploma.

7.2. Reflective measurement model evaluation

The guidelines proposed by Hair et al. (Citation2019) were followed to assess the model in this study. The result of the assessment of the reflective measurement model in Table shows that factor loadings exceeded 0.7, which represent acceptable values for factor loading reliability. The internal consistency reliability in Table reveals that Cronbach’s Alpha, rho_A, and composite reliability were above 0.7, which indicates that the items used to represent the constructs have satisfactory internal consistency reliability. The average variance extracted (AVE) was greater than 0.5, which shows that all constructs exceed the recommended values. Discriminant validity of the model was assessed based on the HeteroTrait-MonoTrait (HTMT) ratio as a newly proposed criterion to assess discriminant validity in Variance-Based Structural Equation Modeling (VB-SEM) Figure (Henseler et al., Citation2015). Table presents the HTMT values of the constructs based on the original sample and 95% confidence intervals (one-tailed), implying the establishment of discriminant validity based on HTMT0.9 and HTMTinference criteria as all HTMT values were smaller than 0.9 and the upper level of the Bias-Corrected and Accelerated (BCa) bootstrap confidence intervals were below the value of 1.

Table 1. Factor loadings

Table 2. Alpha, rho_A, composite reliability, and convergent validity of the constructs

Table 3. Discriminant validity of the constructs based on HTMT0.9 and HTMTinference Criteria

7.3. Structural model evaluation

The structural model was evaluated based on guidelines suggested by Hair et al. (Citation2019). The standard assessment criteria considered are the assessment of collinearity, statistical significance, and relevance of the path coefficients, the blindfolding-based cross-validated redundancy measure Q2, the coefficient of determination (R2), and the model’s out-of-sample predictive power using the PLSpredict procedure.

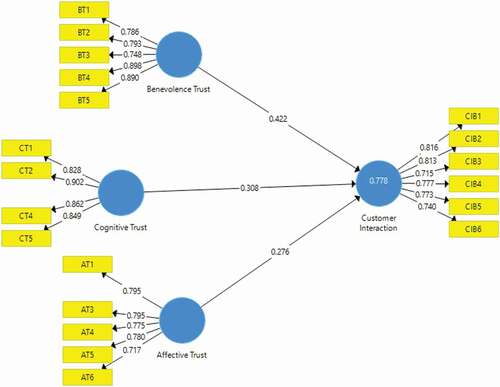

First, collinearity assessment was tested. Table shows that all the Inner VIF values for the independent variables (affective, benevolence, and cognitive trust) that were examined for lateral collinearity are less than 5, indicating that lateral multicollinearity is not a concern in the study. Second, the path coefficient was analyzed. Based on the assessment of the path coefficient, as shown in Table , all three relationships are found to have t-value > 1.645 and were thus significant at the 0.05 level. Specifically, the predictors of affective (β = 0.276 p < 0.01), benevolence (β = 0.422 p < 0.01), and cognitive (β = 0.308 p < 0.01) trust are positively related to customer interaction. Thus, H1, H2, and H3 are supported. Third, effect sizes of the exogenous constructs on the model’s predictive accuracy and relevance were tested. Table reveals the predictive relevance of the model that the Q2 value is larger than 0. The model has predictive relevance for certain endogenous constructs. The one Q2 value for customer interaction (Q2 = 0.453) is more than 0, indicating that the model has sufficient predictive relevance. Next, f2 was examined. Benevolence trust (0.424) has a substantial effect in producing R2 for customer interaction. Affective (0.165) and cognitive (0.186) trust have a medium effect in producing R2 for customer interaction. Fourth, the model out-of-sample predictive power was assessed. Table explains 77.8% of the variance. Meanwhile, R2 value of 0.778, which is above the 0.26 value, as suggested by Cohen (Citation1988), indicates a substantial model. Table also shows that most dependent construct indicators in the PLS-SEM analysis produced higher prediction errors of the root mean squared error (RMSE) when compared to the naïve linear regression model (LM) benchmark. This indicates that the model has no predictive power.

Figure 1. Results of the structural equation model analysis

Table 4. Collinearity assessment among the constructs

Table 5. Final path coefficients

Table 6. Effect sizes of the exogenous constructs on the model’s predictive accuracy and relevance

Table 7. Model out-of-sample predictive power

8. Discussion

This study explored the influence of the interpersonal dimension of trust on customer interaction in the banking sector. It employed benevolence, cognitive, and affective trust as sub-constructs of the interpersonal dimension of trust in the banking sector.

The results show that benevolence trust has a positive influence on customer interaction in the banking sector. This corresponds with the previous literature which has showed that benevolence trust reduces uncertainties and feelings of anxiety in individuals during their interactions with another party (Svare et al., Citation2019; Wu et al., Citation2017). This study emphasizes that the care shown to customers by the staff of the banking sector can influence their financial interactions. Customers are delighted with the level of care they receive from the bank staff because it reduces their perceived risk during their financial interactions. The honesty of employees, including the level of care given to customers, positively influences their understanding of the risk associated with their financial interactions with the bank. Krot and Rudawska (Citation2016) found that customers benefited from face-to-face interactions with the organization’s employees. This study also corroborates the fact that face-to-face interactions between customers and bank staff can induce confidence in their financial interactions. The respondents were confident that their financial information will not be revealed to anyone by the bank staff. They also said that they had never experienced fraudulent activities on their account. This made them believe that their personal information was protected by the bank staff. The banking sector appointed account managers for each bank account to ensure that the customers’ account information was secure. This inspired confidence among customers and encouraged them to engage in financial interactions with their banks.

This study also provides empirical evidence that cognitive trust has a positive influence on customer interaction in the banking sector. This has also been supported in the literature, wherein it has been shown that cognitive trust is based on concrete connections established as a result of shared backgrounds and experiences that have removed uncertainty and nervousness from the relationship (Hite, Citation2005; Yang et al., Citation2009; Ziegler & Golbeck, Citation2007). This study shows that the competency of bank employees influences customers’ financial interactions. Customers who availed services offered by the banking sector assessed the competency of the bank staff. They were delighted with the reactions they received from the bank staff in response to their problems. Daniele and Geys (Citation2015) posited that interpersonal connections prevent parties from engaging in distrustful behavior during their interactions. This aligns with the findings of this study, which show that interpersonal interactions between customers and bank staff can build reputations based on experience. Parayitam and Papenhausen (Citation2016) and Morrow et al. (Citation2004) highlighted that cognitive trust can influence one’s decision to commit to another party in a situation. This study shows that the commitment of bank staff to customers’ goals can influence their financial interactions. Bank staff are always ready to ensure that customers achieve their goals whenever they visit the bank for financial interactions. This makes customers calm and more open to resolving their challenges, knowing that the bank staff are committed to addressing their problems.

Affective trust influences customer interaction in the banking sector positively. This is also supported by the literature, where affective trust is about depending solely on a specific partner based on emotional characteristics (Chen et al., Citation2014; Fard, Citation2012). This study emphasizes that the emotional connection between the customer and the bank staff has an impact on the customer’s financial interactions. The personal bond between the customer and the bank staff creates comfort and ease in conducting financial interactions. The emotional connection between the customer and the staff is a personal bond that is difficult to break. This connection is necessary to reassure customers that the employees of the banking sector are worthy of protecting and helping customers during financial interactions. Accordingly, Wasti et al. (Citation2011) described that affective trust grows over time as the parties involved in an interaction continue to engage in a social exchange by showing reciprocated, genuine care, and by developing relational bonds. This study shows that customers are happy with the concern they are shown during their financial interactions with the bank staff. Customers are likely to exhibit unstable behavior when they face an issue concerning their means of livelihood. Thus, the bank’s ability to show concern for issues affecting its customers can influence the financial interactions between the bank and its customers. These results show that the level of sympathy exhibited to customers by the bank staff can influence the financial interactions between the customer and the bank.

The educational qualification of respondents directly and indirectly supports the result of the study that interpersonal dimension of trust influences customer interaction in the banking sector in Sokoto State, Nigeria. The data on educational qualifications reveal that most respondents had acquired some level of western education. This may not be unconnected with the fact that, in Sokoto State, indigent students in public schools receive scholarships for their primary to tertiary levels of education. Scholarship recipients in tertiary institutions also receive stipends. Therefore, most people who are willing to acquire some level of education have the opportunity to acquire their first degrees or at least, an ordinary national diploma (OND) certificate. Thus, the level of educational exposure of the respondents (degree or OND), in one way or another, can influence their understanding of the interpersonal dimension of trust (benevolence, cognitive, and affective trust), and how they respond to questions on those concepts. As most respondents had a bachelor’s degree and OND certificates, it may have influenced their ability to understand and appreciate the behavior of the bank staff during their financial interactions in their banks.

Theoretically, the results of this study contribute to the concept of trust in the literature on organizational behavior by providing an understanding of how the interpersonal dimension of trust can influence customer interaction in the bank. This corresponds with Giddens (Citation1990) assumption on facework commitment to trust in the organization. Giddens argued that modernization and globalization have increased the extent of risk and uncertainty in organizations, which can be minimized through the introduction of the concept of trust during their interactions. Giddens (Citation1990) asserted that face-to-face (interpersonal) interactions can help reduce tensions and nervousness during their interactions. This study supports the assertion that the interpersonal dimension of trust can influence customer interaction in the banking sector. It reveals that the interpersonal dimension of trust, namely benevolence, cognitive, and affective trust does influence customer interaction in a bank. The ability of the bank staff to show care, prevent harm, and protect customer information through face-to-face interactions influence customer interaction in a bank. The reliability, reputation, competence, and commitment of bank staff influence customer interaction in the bank. The ability of the bank staff to show attention and empathy to their customers also influences their interaction in a bank.

9. Implications and limitations

The ability of the bank staff to care for customers and protect their information during their financial interactions is imperative. Bank employees should remind customers of their roles in the banking sector, including how much they care for their patronage and enjoy it. This can go a long way in inspiring clients to engage in more frequent financial interactions in their banks. Customers become satisfied with the efforts of the bank staff toward preventing harm against them despite having access to their account information in the course of their financial transactions. The efforts put in by the bank staff to protect their customers from fraudsters and scammers can also influence the extent of their financial interactions with the bank.

The commitment, competence, and reputation of bank staff during their financial interactions with their customers are important. The commitment demonstrated by bank workers toward tackling customer-related problems is crucial. It gives them a sense of optimism and belonging, and this may affect their financial contact with the bank. The competence of the bank staff may affect customers’ financial interactions with the bank. Customers are worried about their money and rely on employees with whom they believe they have built their own excellent credibility in the course of previous financial interactions. The more successful the financial interaction becomes; the more relationships bank employees build with their clients. This can, in turn, affect their financial interactions.

The emotional connection and empathy shown by bank staff is critical for customers during their financial interactions. The emotional bond created between bank employees and customers can reduce the chance of bank fraud. This incentive provided by emotional connection can influence customer interaction in a bank. The empathy that the bank staff show toward customers facing financial problems is critical. Showing empathy by the bank staff can give customers a sense of relief that the banking sector understands their feelings. This can positively impact their financial interactions. These factors, if maintained, can lead to growth and development in the banking sector.

This study has several limitations. First, the inability to obtain a sampling framework from the banking sector affects the generalizability of its findings. Second, the study focused only on Sokoto metropolis, which comprises only 3 out of 23 local government areas in Sokoto State.

10. Recommendations

Benevolence trust influences customer interaction in the banking sector in Sokoto State, Nigeria. It is imperative for policymakers and executives of the banking sector to arrange workshops and seminars for their staff on how to show care to their customers whenever they visit for financial interactions. It is also important for the banking sector to train its staff on using computers, including how to protect customers’ accounts in the course of their financial interactions.

Cognitive trust can influence customer interaction in the banking sector in Sokoto State, Nigeria. To ensure that workers retain a high degree of reliability, commitment, reputation, and competence during their financial interactions with their customers, it is necessary for policymakers and executives to enforce checks and balances on the staff. This can be done regularly through customer feedback and staff evaluation. It will help evaluate employee efficiency to ensure growth and development in the banking sector.

Affective trust influences customer interaction in the banking sector in Sokoto State, Nigeria. The banking sector should rely on expert support to educate and train its staff on how to build and sustain their emotional connections with their customers because of its importance in face-to-face financial interactions. Policymakers and executives should strategize on inspiring the staff to show empathy and sympathy toward their customers. This is a grassroots-led approach to encourage workers to support their customers by going above and beyond during their financial interactions.

The study that benevolence, cognitive, and affective trust positively influence customer interaction also shows the importance of the banking sector in Sokoto State, Nigeria, as well. It demonstrates that, because of the positive experience that can be gained from it, customers prefer using the banking hall for financial interaction. This is important to Sokoto State bank customers and therefore the banking sector should continue to sustain financial interactions in the banking hall, including enhancing interactions based on feedback from their esteem customers.

11. Conclusion

This study explored the influence of the interpersonal dimension of trust on customer interaction in the banking sector. The interpersonal dimension of trust is an individual’s confidence in another party based on face-to-face interactions with them. The results revealed a positive relationship among benevolence, cognitive, and affective trust in customer interaction in banks in Sokoto State. The interpersonal dimension of trust is indispensable to the banking sector as it shows how benevolence, cognitive, and affective trust influence customer decisions to interact with banks and avail their services. We recommend that the banking sector maximize the influence of the interpersonal dimension of trust in customer interaction with the banking sector in order to retain and attract customers and to enable growth and development in the system.

Additional information

Funding

Notes on contributors

Abdulrahman Bello Bada

Mr. Abdulrahman Bello Bada currently teaches at the Department of Sociology, Faculty of Social Sciences, Usmanu Danfodiyo University Sokoto, Nigeria. He has a bachelor’s degree in Sociology from the same institution, Master of Social Sciences (Anthropology and Sociology) from Universiti Sains Malaysia, Penang, Malaysia, where he is currently pursuing a PhD in Sociology with a specialization in the Sociology of Organizational and Consumer Behavior.

Premalatha Karupiah

Dr. Premalatha Karupiah is an Associate Professor of Sociology at the School of Social Sciences, Universiti Sains Malaysia, Penang, Malaysia. She teaches research methodology and statistics. Her research interests include beauty culture, femininity, educational and occupational choices, and issues related to the Indian diaspora. Her articles have been published in leading journals.

References

- Adiele, K. C., Nnamseh, M., & Omunakwe, P. O. (2018). Workplace interpersonal relationship and customer satisfaction in deposit money banks in Port- Harcourt. Paper presented at the proceedings of the 12th Annual National Conference of the Academy of Management Nigeria, Abuja, Nigeria, Nile University of Nigeria.

- Alam, I. (2011). Process of customer interaction during new service development in an emerging country. The Service Industries Journal, 31(16), 2741–18. https://doi.org/10.1080/02642069.2010.512660

- AlHarbi, A., Heavin, C., & Carton, F. (2016). Improving customer oriented decision making through the customer interaction approach. Journal of Decision Systems, 25(sup1), 50–63. https://doi.org/10.1080/12460125.2016.1187417

- Andersen, P. H., & Kumar, R. (2006). Emotions, trust and relationship development in business relationships: A conceptual model for buyer–seller dyads. Industrial Marketing Management, 35(4), 522–535. https://doi.org/10.1016/j.indmarman.2004.10.010

- Brush, T. H., Dangol, R., & O’Brien, J. P. (2012). Customer capabilities, switching costs, and bank performance. Strategic Management Journal, 33(13), 1499–1515. https://doi.org/10.1002/smj.1990

- Cameron, M. P., Richardson, M., & Siameja, S. (2016). Customer dissatisfaction among older consumers: A mixed-methods approach. Ageing and Society, 36(2), 420–441. https://doi.org/10.1017/S0144686X14001354

- Chen, X., Eberly, M. B., Chiang, T., Farh, J., & Cheng, B. (2014). Affective trust in Chinese leaders: Linking paternalistic leadership to employee performance. Journal of Management, 40(3), 796–819. https://doi.org/10.1177/0149206311410604

- Chhetri, P. (2014). The role of cognitive and affective trust in the relationship between organizational justice and organizational citizenship behavior: A conceptual framework. Business: Theory and Practice, 15(2), 170–178. https://doi.org/10.3846/btp.2014.17

- Chua, R. Y. J., Ingram, P., & Morris, M. W. (2008). From the head and the heart: Locating cognition-and affect-based trust in managers’ professional networks. Academy of Management Journal, 51(3), 436–452. https://doi.org/10.5465/amj.2008.32625956

- Cohen, J. (1988). Statistical power analysis for the behavioral science (2nd ed.). Lawrence Erlbaum Associates.

- Colquitt, A. J., Brent, A. S., & Jeffery, A. L. (2007). Trust, trustworthiness, and trust propensity: A meta-analytic test of their unique relationships with risk taking and job performance. Journal of Applied Psychology, 92(4), 909–927. https://doi.org/10.1037/0021-9010.92.4.909

- Colquitt, J. A., & Salam, S. C. (2009). Foster trust through ability, benevolence, and integrity. In A. L. Edwin (Ed.), Handbook of principles of organizational behavior: Indispensable knowledge for evidence-based management (pp. 389). A John Wiley and Sons, Ltd, Publication.

- Creswell, J. W. (2013). Research design: Qualitative, quantitative, and mixed methods approaches. Sage publications.

- Dadzie, K. Q., Dadzie, C. A., & Williams, A. J. (2018). Trust and duration of buyer-seller relationship in emerging markets. Journal of Business and Industrial Marketing, 33(1), 134–144. https://doi.org/10.1108/JBIM-04-2017-0090

- Daniele, G., & Geys, B. (2015). Interpersonal trust and welfare state support. European Journal of Political Economy, 39, 1–12. https://doi.org/10.1016/j.ejpoleco.2015.03.005

- Danneels, E. (2003). Tight–loose coupling with customers: The enactment of customer orientation. Strategic Management Journal, 24(6), 559–576. https://doi.org/10.1002/smj.319

- Delgado-márquez, B., Hurtado-torres, L., & Aragón-correa, J. A. (2013). On the measurement of interpersonal trust transfer: Proposal of indexes. Social Indicators Research, 113(1), 433–449. https://doi.org/10.1007/s11205-012-0103-z

- Drake, J., & Mehta, N. (2006). Benevolent competence and integrity-based trust in knowledge transfer: A look at software reuse. Paper presented at the proceedings of the twelfth Americas Conference on Information Systems, August 04th-06th, Acapulco, Mexico.

- Eastlick, M. A., & Lotz, S. (2011). Cognitive and institutional predictors of initial trust toward an online retailer. International Journal of Retail and Distribution Management, 39(4), 234–255. https://doi.org/10.1108/09590551111117527

- Erdem, F., & Ozen, J. (2003). Cognitive and affective dimensions of trust in developing team performance. Team Performance Management: An International Journal, 9(5/6), 131–135. https://doi.org/10.1108/13527590310493846

- Evans, A. M., & Krueger, J. I. (2009). The psychology (and economics) of trust. Social and Personality Psychology Compass, 3(6), 1003–1017. https://doi.org/10.1111/j.1751-9004.2009.00232.x

- Fard, D. S. (2012). Gender, trust, and interpersonal relationships [Master’s thesis]. University of Gothenburg.

- Foss, J. N., Laursen, K., & Pedersen, T. (2011). Linking customer interaction and innovation: The mediating role of new organizational practices. Organization Science, 22(4), 980–999. https://doi.org/10.1287/orsc.1100.0584

- Giddens, A. (1990). The consequences of modernity. Polity Press.

- Ha, B., Park, Y., & Cho, S. (2011). Suppliers’ affective trust and trust in competency in buyers its effect on collaboration and logistics efficiency. International Journal of Operations and Production Management, 31(1), 56–77. https://doi.org/10.1108/01443571111098744

- Habibov, N., & Afandi, E. (2015). Pre- and post-crisis life-satisfaction and social trust in transitional countries: An initial assessment. Social Indicators Research, 121(2), 503–524. https://doi.org/10.1007/s11205-014-0640-8

- Hair, F. J., Risher, J. J., Sarstedt, M., & Ringle, M. C. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Hanzaee, K. H., & Norouzi, A. (2012). The role of cognitive and affective trust in service marketing: Antecedents and consequence. Research Journal of Applied Sciences, Engineering and Technology, 4(23), 4996–5002.

- Henseler, J., Ringle, M. C., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hite, J. (2005). Evolutionary processes and paths of relationally embedded network ties in emerging entrepreneurial firms. Entrepreneurship Theory and Practice, 29(1), 113–144. https://doi.org/10.1111/j.1540-6520.2005.00072.x

- Jalava, J. (2006). Trust as a decision: The problems and functions of trust in Luhmannian Systems Theory. University of Helsinki. Printed by Yliopistopaino.

- Johnson, D., & Grayson, K. (2005). Cognitive and effective trust in service relationships. Journal of Business Research, 58(4), 500–507. https://doi.org/10.1016/S0148-2963(03)00140-1

- Kaiser, F. H. (1970). A second generation little jiffy. Psychometrika, 35(4), 401–415. https://doi.org/10.1007/BF02291817

- Kaiser, F. H. (1974). An index of factorial simplicity. Psychometrika, 39(1), 31–36. https://doi.org/10.1007/BF02291575

- Krot, K., & Rudawska, I. (2016). The role of trust in doctor-patient relationship: Qualitative evaluation of online feedback from Polish patients. Economics and Sociology, 9(3), 76–88. https://doi.org/10.14254/2071-789X.2016/9-3/7

- Laursen, K., & Salter, A. (2006). Open for innovation: The role of openness in explaining innovative performance among UK manufacturing firms. Strategic Management Journal, 27(2), 131–150. https://doi.org/10.1002/smj.507

- Letki, N. (2006). Investigating the roots of civic morality: Trust, social capital, and institutional performance. Political Behaviour, 28(4), 305–325. https://doi.org/10.1007/s11109-006-9013-6

- Lewicki, R. J., Tomlinson, E. C., & Gillespie, N. (2006). Models of interpersonal trust development: Theoretical approaches, empirical evidence, and future directions. Journal of Management, 32(6), 991–1022. https://doi.org/10.1177/0149206306294405

- Lewis, J. D., & Weigert, A. (1985). Trust as a social reality. Social Forces, 63(4), 967–985. https://doi.org/10.1093/sf/63.4.967

- Matthing, J., Sandén, B., & Edvardsson, B. (2004). New service development: Learning from and with customers. International Journal of Service Industry Management, 15(5), 479–498. https://doi.org/10.1108/09564230410564948

- Mbah, C. C., Francis, A. C., & Oseloka, I. C. (2014). Marketing banks’ products in Nigeria for improved customers’ satisfaction and loyalty. Interdisciplinary Journal of Contemporary Research in Business, 6(3), 310–320.

- McKnight, D. H., & Chervany, N. L. (2001). Conceptualizing trust: A typology and e-commerce customer relationships model. Paper presented at the proceedings of the 34th Annual Hawaii International Conference on System Sciences, Maui, HI, USA.

- Meyer, S., Ward, P., Coveney, J., & Rogers, W. (2008). Trust in the health system: An analysis and extension of the social theories of Giddens and Luhmann. Health Sociology Review, 17(2), 177–186. https://doi.org/10.5172/hesr.451.17.2.177

- Meyer, S. B., & Ward, P. R. (2008). Do your patients trust you? A sociological understanding of the implications of patient mistrust in healthcare professionals. Australasian Medical Journal, 1(1), 1–12. https://doi.org/10.4066/amj.2008.7

- Morrow, J., Jr, Hansen, L., & Pearson, A. W. (2004). The cognitive and affective antecedents of general trust within cooperative organizations. Journal of Managerial Issues, 16(1) 48–64. https://www.jstor.org/stable/40601183

- Mosch, R., & Prast, H. (2008). Confidence and trust: Empirical investigation for the Netherland and the Financial Sector. Ocational Studeies, 6(2), 1–63. http://hdl.handle.net/10419/37384

- Muhammad, A. H., Shahzad, B. K., & Iqbal, A. (2011). Service quality and customer satisfaction in the banking sector: A comparative study of conventional and Islamic banks in Pakistan. Journal of Islamic Marketing, 2(3), 203–224. https://doi.org/10.1108/17590831111164750

- Nejad, M. G., Tran, H. T. T., & Corner, J. (2016). The impact of communication channels on mobile banking adoption. International Journal of Bank Marketing, 34(1), 78–109. https://doi.org/10.1108/IJBM-06-2014-0073

- Nguyen, N. (2016). Reinforcing customer loyalty through service employees’ competence and benevolence. The Service Industries Journal, 36(13–14), 721–738. https://doi.org/10.1080/02642069.2016.1272595

- Ozdemir, S., Trott, P., & Hoecht, A. (2007). New service development: Insights from an explorative study into the Turkish retail banking sector. Innovation, 9(3–4), 276–291. https://doi.org/10.5172/impp.2007.9.3–4.276

- Parayitam, S., & Papenhausen, C. (2016). Agreement-seeking behavior, trust, and cognitive diversity in strategic decision making teams: Process conflict as a moderator. Journal of Advances in Management Research, 13(3), 292–315. https://doi.org/10.1108/JAMR-10-2015-0072

- Peng, L. S., & Moghavvemi, S. (2015). The dimension of service quality and its impact on customer satisfaction, trust, and loyalty: A case of Malaysian banks. Asian Journal of Business and Accounting, 8(2), 91–121. https://ssrn.com/abstract=2762052

- Poon, P., Albaum, G., & Yin, C. (2017). Exploring risks, advantages and interpersonal trust in buyer-salesperson relationships in direct selling in a non-western country. International Journal of Retail and Distribution Management, 45(3), 328–342. https://doi.org/10.1108/IJRDM-08-2016-0124

- Russell, S. (2005). Treatment-seeking behaviour in urban Sri Lanka: Trusting the state, trusting private providers. Social Science & Medicine, 61(7), 1396–1407. https://doi.org/10.1016/j.socscimed.2004.11.077

- Schaarschmidt, M., Walsh, G., & Evanschitzky, H. (2018). Customer interaction and innovation in hybrid offerings: Investigating moderation and mediation effects for goods and services innovation. Journal of Service Research, 21(1), 119–134. https://doi.org/10.1177/1094670517711586

- Schlichter, B. R. (2010). Dynamic trust in implementation of large information systems: Conceptualized by features from Giddens’ theory of modernity. Systems, Signs and Actions: An International Journal on Communication, Information Technology and Work, 4(1), 1–22.

- Svare, H., Gausdal, A. H., & Möllering, G. (2019). The function of ability, benevolence, and integrity-based trust in innovation networks. Industry and Innovation, 27(6) 1–20. https://doi.org/10.1080/13662716.2019.1632695

- Tan, F. B., & Sutherland, P. (2004). Online consumer trust: A multi-dimensional model. Journal of Electronic Commerce in Organization, 2(3), 40–58. https://doi.org/10.4018/jeco.2004070103

- Thurstone, L. L. (1947). Multiple factor analysis. University of Chicago Press.

- Tongco, M. D. C. (2007). Purposive sampling as a tool for informant selection. Ethnobotany Research and Application, 5, 147–158. https://doi.org/10.17348/era.5.0.147-158

- Udechukwu, I., Redmond, D. M., & Mujtaba, B. G. (2012). Spinning the wheels of trust and culture in organizations: A conceptual and mathematical model using social exchange theory. International Journal of Arts and Commerce, 1(4), 11–28.

- Uzkurt, C., Kumar, R., Semih, K. H., & Eminoğlu, G. (2013). Role of innovation in the relationship between organizational culture and firm performance: A study of the banking sector in Turkey. European Journal of Innovation Management, 16(1), 92–117. https://doi.org/10.1108/14601061311292878

- Vinokurova, N. (2019). Re‐shaping demand landscapes: How firms change customer preferences to better fit their products. Strategic Management Journal, 40(13), 2107–2137. https://doi.org/10.1002/smj.3074

- Von Hippel, E. (2005). Democratizing innovation. MIT Press.

- Wang, S., Tomlinson, E. C., & Noe, R. A. (2010). The role of mentor trust and protégé internal locus of control in formal mentoring relationships. Journal of Applied Psychology, 95(2), 358–367. https://doi.org/10.1037/a0017663

- Ward, P. R., & Meyer, S. B. (2009). Trust, social quality and wellbeing: A sociological exegesis. Development and Society, 38(2), 339–363. https://doi.org/https://www.jstor.org/stable/10.2307/deveandsoci.38.2.339

- Wasti, S. A., Tan, H. H., & Erdil, S. E. (2011). Antecedents of trust across foci: A comparative study of Turkey and China. Management and Organization Review, 7(2), 279–302. https://doi.org/10.1111/j.1740-8784.2010.00186.x

- Webber, S. S. (2008). Development of cognitive and affective trust in teams: A longitudinal study. Small Group Research, 39(6), 746–769. https://doi.org/10.1177/1046496408323569

- Wu, C., Lin, Y., & Chen, T. Y. (2017). Moderating price sensitivity of low-uncertainty daily eco-friendly products: Creating benevolence trust and reducing uncertainties. Journal of Relationship Marketing, 16(4), 286–301. https://doi.org/10.1080/15332667.2017.1349558

- Xu, F., Evans, A. D., Li, C., Li, Q., Heyman, G., & Lee, K. (2013). The role of honesty and benevolence in children’s judgments of trustworthiness. International Journal of Behavioral Development, 37(3), 257–265. https://doi.org/10.1177/0165025413479861

- Yang, J., Mossholder, K., & Peng, T. K. (2009). Supervisory procedural justice effect: The mediating roles of cognitive and affective trust. Leadership Quarterly, 20(2), 143–154. https://doi.org/10.1016/j.leaqua.2009.01.009

- Ziegler, C. N., & Golbeck, J. (2007). Investigating interactions of trust and interest similarity. Decision Support Systems, 43(2), 460–494. https://doi.org/10.1016/j.dss.2006.11.003

- Zur, A., Leckie, C., & Webster, C. M. (2012). Cognitive and affective trust between Australian exporters and their overseas buyers. Australasian Marketing Journal (AMJ), 20(1), 73–79. https://doi.org/10.1016/j.ausmj.2011.08.001