Abstract

The emergence of the Sustainable Development Goal; Agenda 2030, has led to the development and growth of knowledge in various fields of learning. One among several is water management accounting; this field of study becomes necessary in addressing water use, water stress, and a tool for water advocacy which is an integral part of SDG goal 6; clean water and sanitation. Water management accounting (WMA) is a burgeoning field of research within the management accounting research cluster. This research area aims at providing information to improve the use of water resources, a resource being utilized by businesses as an essential raw material component; which facilitates production. The objective of this article is to make evident the insufficient body of literature in this evolving field of knowledge, thus providing research insight to researchers in management sciences. In achieving this objective, this study employs explicitly a bibliometric approach to analyse the volume of publications in the WMA research cluster from 2000 to 2018 using the Scopus database. Furthermore, a critique of the literature that emerged from the bibliometric approach was carried out in a tabular form to establish more research gaps. The study observed that water management accounting research cluster is currently plagued with stunted growth and low publication output. The authors recommended that scholars, researchers and managers should contribute to the development and research intensity in this budding field of knowledge.

PUBLIC INTEREST STATEMENT

This study provides an outlook on understanding the status of water management accounting research. It establishes a pathway into this field of study by critiquing the few articles written in this field and suggesting research gaps, opportunities, methods and material issues in this research domain. Hence, contributing to the establishment of research agendas in the water management accounting research cluster.

1. Introduction

The threat to the sustainable supply of freshwater is consistently increasing over the years. It has been attributed to factors such as population growth, economic development, industrial and nuclear activities, and the effects of global warming (Daniel & Sojamo, Citation2012; Christ & Burritt, Citation2017). These developments have intensified concerns about the need to account for freshwater globally (Pacific Institute, Citation2009; Signori & Bodino, Citation2013). Thus, it led to an academic field of study termed water management accounting. The visibility of water management accounting can be attributed to the emergence and vigorous drive of the Sustainable Development Goal; Agenda 2030. This has led to the development of knowledge in various fields of learning, chief among which is water management accounting, a field of study geared towards addressing issues related to water use and stress, sustainable use of water in production, and sustainable management of water which is an integral part of SDG goal 6, clean water and sanitation. Water management accounting can be described as the sub-discipline of environmental management accounting within the management accounting discipline. Its aim is to systematically and quantitatively assess the water situation and implications on water supply and demand, circulation, availability and use in definite domains, thereby making available information that enlightens water science, management and governance to aid sustainable outcomes for the society (Food and Agriculture Organisation, 2012).

The research term “Water Management” is not exclusively attributable to researchers and academics in the management sciences, but has a multidisciplinary connotation and spread. Thus, due to the multidisciplinary nature of water management research, it is influenced by several scholarly contributions from diverse research disciplines such as hydrology, environmental science, water science, civil engineering, chemical engineering, biological science, and chemistry among others (Emenike et al., Citation2017; Imtiaz Ferdous et al., Citation2019; Omole et al., Citation2019; Omole & n.d.ambuki, Citation2015; Torres López et al., Citation2019; Zhan-Ming & Chen, Citation2013). However, minimal contributions to the water management literature have been observed from management accounting research discipline. Hence, the need for this article; which used the bibliometric approach to analyze the volume of contribution and impact to the water management literature from the management sciences, especially the accounting discipline. The study also seeks to identify some research gaps that can further be explored as a means of contributing to literature in this budding field of water management by critiquing the articles that emerged from the Scopus database. The essence of this study is to provide clarity on the current position of water management accounting research from a global perspective using the Scopus database as a reference point. In addition, the study will be critical for academics and researchers in the management sciences in setting a research agenda.

Water stewardship has become critical due to the recklessness engaged by corporate businesses in the use of water. A case in point is the lawsuit levelled against Coca-Cola by the village council of Kerela, India. Water can no longer be seen as just a free gift of nature, rather as an economic and ecological asset used for the manufacture of goods and services. The economic use of water has gifted us a concept in management sciences termed water management accounting; which can be used as an internal means of assessing the sustainable use of water before, during and after production among corporate users.

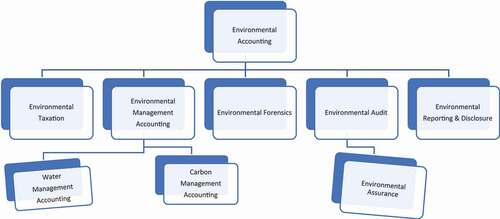

According to Morrison et al. (Citation2010), water accounting is described as the study and practice of providing information to improve water management by businesses. Water accounting can also be described as a procedure for analyzing the uses, depletion, and productivity of water within the context of a water basin (Molden, Citation1997). Corporate water management accounting can be described as the provision and analysis of both financial and non-financial information to support management on water management decisions. The discussion on water management accounting bears its root in the environmental accounting research domain, which focuses on employing activities, methods and systems in recording, analyzing and reporting environmentally induced financial impacts on organizations (Schaltegger et al., Citation2000). Furthermore, environmental accounting is about harmonizing the connection between environmental and financial performance by embedding environmental sustainability within an organization’s operational protocols, value system, and communicating information to decision-makers that can help reduce water cost and business risk. The association between environmental accounting and water accounting, as deduced from literature is depicted in (Burritt et al., Citation2002; Mudge, Citation2008; Steinbach et al., Citation2009; Christ & Burritt, Citation2017).

Figure 1. Framework illustrating the relationship between environmental accounting and water management accounting. Source: Author (2019)

Bibliometric analysis is a discipline in the information and library sciences that evaluates bibliographic material by using quantifiable methods (Merediz-Solà & Bariviera, Citation2019). It is also described as the use of statistical methods to analyze books, articles, and other publications. Recently, there is an increase in the use of bibliometric analysis in evaluating scientific output among scholars from various disciplines (Amin et al., Citation2019; Amirbagheri et al., Citation2018; Asmi et al., Citation2019; Bouzembrak et al., Citation2019; Ezenwoke et al., Citation2019; Rialp et al., Citation2019; Rodríguez-Ruiz et al., Citation2019; Yang et al., Citation2019). The first condition necessary for the use of bibliometric analysis is the existence of a robust database which serves as a repository for bibliographic materials. This study engaged the Scopus database for the purpose of analyzing literature in the water management accounting research field. The Scopus database was heralded in November 2004. It is the biggest abstract and citation database in peer-reviewed literature, introducing smart tools to trail, analyze and visualize research. The database has over five thousand (5000) publishers and more than 22800 titles (Scopus, Citation2017). This study's choice of the Scopus database is based on the global reach and the comprehensive outlook of the database in the field of science, technology, medicine, social science, arts and humanities.

2. Methods and materials

The method used to achieve the objective stated in this study is the bibliometric approach; the data were obtained from the Scopus database, which was heralded in November 2004. In obtaining the required data for analysis, specific keyword query “{Water Management Accounting}” was formulated for this study. The search term would be used to scan through the article titles, abstracts and keywords in the Scopus database in other to retrieve relevant documents for the study.

In order to ensure that the search query is limited to the time frame of the study, there is a need to specify the publication year (PUBYEAR) under consideration. For the purpose of this study, the PUBYEAR specified was “PUBYEAR > 1999 AND PUBYEAR < 2019”. The years, “>1999” and “<2019”, were specified so as to retrieve all relevant materials published between the year 2000–2018.

The search query was conducted (11 October 2018, 11:22 AM). The date is specified so as to ensure clarity in the way and manner the output was obtained. Second, to delimit the study to items captured at the date and time stated since the Scopus database is continuously updated with more current and recent literature hourly, daily, monthly and yearly. The braces {} used together with the search query {Water Management Accounting}is a well-defined collection of distinct objects. Hence, it will only feature results that contain these words as specified by the search query in any of its Title, Abstract and Keyword.

Three (3) documents met the specified criteria; this served as the Scopus data used for the analysis performed in this study. The data were downloaded from the Scopus database using the CSV export. This report was opened by the MS Excel application, and it contained the following columnar headings, beginning from column A—K: access type, year, author name, subject area, document type, source title, keyword, affiliation, funding-sponsor, country, source-type, respectively. These data were used for the purpose of analysis, with the aid of applications such as Google sheet, and MS Excel for visualization. To further establish a research agenda, the articles were critiqued to identify areas in which further scholarly research and studies could be undertaken in the water management accounting research domain,

3. Results

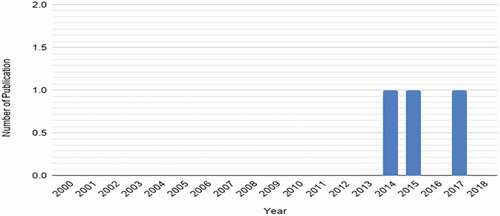

3.1. Yearly publication distribution

The graph in , reveals that only one article in the field of water management accounting was published in 2014, 2015 and 2017, in contrast, the year 2000–2013, 2016 and 2018 were drought years. Therefore, it is evident that accounting research has lost over a decade of academic contribution to this novel and noble research agenda (SDG 6). Hence, more needs to be done to improve on the global research output in this area, as one article per year (2014, 2015, 2017) will be considered below par.

Figure 2. Yearly distribution of WMA research since 2000

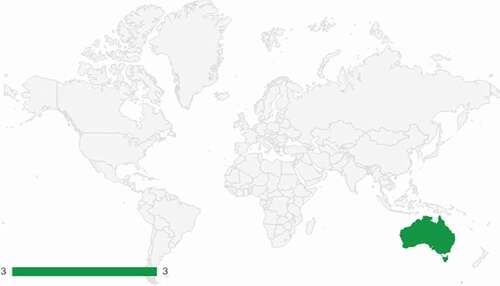

3.2. Country distribution

The geographical map depicted in reveals the country by country contribution to WMA research based on the number of publications emanating from each country of the world. From the analysis of the map, only Australia, contributed the three (3) articles obtained from the Scopus database.

Figure 3. Global distribution of WMA research outputs

3.3. Authorship analysis

Currently, about four (4) authors have contributed to the current state of WMA research, based on the data retrieved from the Scopus database for the period covered. A further look at the authorship pattern gives us an insight into the publication frequency and authors collaborative effort per article. From , only one author has two articles/publication attributable to his/her research effort while the remaining two authors each have one article/publication traceable to them.

Table 1. Publication frequency

Second, the collaborative pattern of the authors of the three documents that formed the base of this study was also evaluated. The data shows that the author’s collaborative pattern ranged from a single authorship to two authors per article. It is observed from the data analyzed that two articles/publication were authored by an individual, i.e. single authors. In contrast, only one article/publication was collaboratively published by two individuals, i.e. two authors. Thus, single authors produced two scholarly documents, while only one scholarly document was authored by two individuals. This is captured in .

Table 2. Collaborative pattern of authors

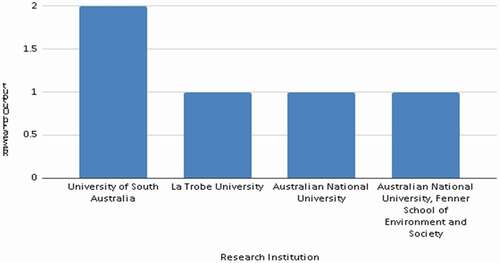

3.4. Contributing/productive institutions

The bar chart in reveals the analysis of research institutions from which WMA articles were published, and the frequency of the research output is also captured. From the analysis, the University of South Australia is currently the leading institution on the subject with a total of two publications over a period of focus. Other institutions are La Trobe University, Australian National University and Australian National University, Fenner School of Environment and Society, which each have one publication, respectively.

Figure 4. Institutional contributors to WMA research

3.5. Source outlets

The result of reveals the publishing outlets where WMA research has been published. It is observed that three journals, namely, British Accounting Review, and Journal of Cleaner Production published by Elsevier; Social and Environmental Accountability Journal published by Taylor & Francis were responsible for the dissemination of knowledge in WMA research.

Table 3. Outlet of WMA research (2000–2018)

3.6. Document type

The pie chart depicted in reveals the various document types that have been published from 2000 to 2018. Only two document types have been published thus far, articles have been the highest with 66.7% and review papers have been the lowest with 33.3%. This shows that other means of publishing scholarly works such as Conference Paper, Book chapters, Conference Review, Editorial, Note, Book, and Monograph are yet to be explored by authors in the WMA research cluster.

Figure 5. Variety of documents in AIS research

4. Discussion

Sustainability issues have become an issue of global debate since the introduction of sustainable development goals (SDGs) in 2000. Critical among these discussions are issues bordering on water (SDG 6), water use, water, sanitation and hygiene, and water for business among others. More specifically, when you type the word “water” into the Scopus database and limit your search to the year 2000–2018, it will return two million, four hundred and thirty-one thousand, nine hundred and seven (2,431,907) document results consisting of academic articles, books, book chapters, conference papers, reviews, notes, short survey, letter, conference review, editorial, business articles, abstract report, data paper and reports from diverse subject areas and one hundred and fifty-eight (158) countries of the world. Despite the volume of literature on water, these have not translated to a productive output in the water management accounting research cluster, as evidenced in the results obtained from the yearly publication distribution. The results revealed that the years 2000–2013, 2016, and 2018 were characterized with no scholarly output in management sciences on water management accounting. Thus, losing more than a decade of scholarly contribution to this novel field. Furthermore, issues such as water pollution, water stress, water scarcity, and water for business among others are concerns most countries of the world are faced with. Although these issues have research implications on water management accounting, it was observed from the result of that the only country currently contributing to this discussion through the lens of water management accounting is Australia. This realization turned our attention to Australia, only to understand that they are faced with water woes, crisis and shortages as a result of drought. Hence, these publications could be attributable to the undersupply of freshwater suffered in Australia. This raises some critical questions. Is Australia the only country faced with an undersupply of freshwater? Why are there no publications from countries with similar challenges? Hence, this fulfils the essence of this study, which is to serve as a wake-up call to scholars, and researchers in management sciences, particularly those in environmental management accounting and related fields to intensify research efforts in this field of knowledge.

A cursory look into the authorship pattern revealed that the three articles were authored by three individuals, namely Roger Burritt of the Australian National University, Canberra, Katherine Christ of the University of South Australia and Nicolas Pawsey of La Trobe University. Roger and Katherine were co-authors of Water Management Accounting: A framework for corporate practice, published in 2017 with Journal of Cleaner Production; Katherine, published Water management accounting and the wine supply chain: Empirical evidence from Australia in 2014, with The British Accounting Review as a single author and Nicolas, in 2015 published, Water management accounting and the wine supply chain: Empirical evidence from Australia with Social and environmental accountability journal as a single author. Christ and Burritt (Citation2017) in their study explored the challenges of improving business decisions on water scarcity, water surpluses and water management opportunities due to the lack of data. The study introduced the Corporate Water Management Accounting as a recently proposed extension to Environmental Management Accounting designed to support corporate management decisions and improve both economic and environmental water-related business outcomes. The study was very insightful and expository. However, it could have gone beyond just proposing an extension to giving insights on what business researches could focus on. Therefore, other studies may seek to focus on water treatment costing and reporting, tax incentives to businesses with sustainable water management and practices, impact of business factors on water management accounting practices, water recycling infrastructural incentives, corporate water governance, corporate water responsibility, corporate-community water stewardship nexus, determinants of sustainable water practices, technological factors influencing the practices of water management accounting among others. Christ (Citation2014) examined the influence of organizational size, regulatory pressure, and corporate environmental strategy as drivers of water management accounting using contingency and new institutional sociology theories. This study was the first empirical work of its kind in the water management accounting research cluster. However, the study limited its scope to the wine industry alone. Therefore, other studies may seek to examine other sectors of the economy that depend on water for their operations such as beverages, chemicals and paint, hoteliers, and pharmaceuticals, among others.

5. Conclusion and recommendation

The authors have employed the use of bibliometric analysis in discussing three publications that emerged from the Scopus database based on specified search criteria, as discussed earlier in this paper. The bibliometric discuss was themed around yearly publication distribution, country distribution, authorship analysis, contributing/productive institution, source outlet and document types. The study went further to critique the papers obtained from the query with the intention of suggesting areas for further studies and research gaps observed. From the observation of the authors, water management accounting research is still at an infantile stage despite the massive attention on Sustainable Development Goals (SDGs) and sustainability at the global and corporate levels, respectively. This was evidenced by the stunted growth in the publication output of this research cluster. It was observed that Australia is the only country contributing to the development of research in water management accounting cluster. Furthermore, the contribution to scholarly output was traced to only three individuals, namely Roger Burritt, Katherine Christ and Nicolas Pawsey from different institutions in Australia. The implication of the observed results reveals that there is an urgent need for scholars, researchers and managers to contribute to the development and intensity of research in the water accounting research cluster thereby enhancing the fulfilment of the sustainable development goals, improving the engagement of corporate organization in the use of water for business and the development of literature for this budding field of knowledge.

Acknowledgements

The authors appreciate and acknowledge Covenant University, Nigeria for bearing the financial obligation of publishing this paper.

Disclosure statement

There is no conflict of interest to declare in this manuscript.

Additional information

Funding

Notes on contributors

Olamide A. Olusanmi

Olamide Olusanmi a faculty member from Covenant University, Nigeria and associate of The Institute of Chartered Accountants of Nigeria (ICAN). His research interest is in the field of Environmental Accounting, Management Accounting, Corporate Governance, Taxation and Entrepreneurship.

Francis K. Emeni

Francis-Kehinde Emeni a Professor of Accounting at the University of Benin, Nigeria. He is a fellow at The Institute of Chartered Accountants of Nigeria (ICAN) and also a research fellow to the same Institute. He has supervised several postgraduate students at Masters and Doctoral levels.

Uwalomwa Uwuigbe

Uwalomwa Uwuigbe a Professor of Accounting and currently the Dean, College of Business and Social Sciences, Covenant University, Nigeria. He has supervised over 100 students at B.Sc, M.Sc. and Ph.D levels. He is a Member of the Nigeria Institute of Management (NIM), Chartered Global Management Accountant United Kingdom (CGMA) among others.

Oyewole S. Oyedayo

Oyewole Oyedayo a faculty member from Covenant University, Nigeria. Her research interest is in the field of Sustainability Accounting, Accounting Information System and Cost Accounting.

References

- Amin, M., Khan, F., & Zuo, M. (2019). A bibliometric analysis of process system failure and reliability literature. Engineering Failure Analysis, 106, 1. https://doi.org/10.1016/j.engfailanal.2019.104152

- Amirbagheri, K., Merigó, J., & Yang, J.-B. (2018). A bibliometric analysis of leading countries in supply chain management research. In Advances in Intelligent Systems and Computing (pp. 182–10). International Conference of Modelling and Simulation in Engineering, Economics, and Management.

- Asmi, F., Anwar, M., Zhou, R., Wang, D., & Sajjad, A. (2019). Social aspects of ‘climate change communication’ in the 21st century: A bibliometric. Journal of Environmental Planning and Management, 62(14), 2393–2417. https://doi.org/10.1080/09640568.2018.1541171

- Bouzembrak, Y., Klüche, M., Gavai, A., & Marvin, H. (2019). Internet of Things in food safety: Literature review and a bibliometric analysis. Trends in Food Science and Technology, 94, 54–64. https://doi.org/10.1016/j.tifs.2019.11.002

- Burritt, R., Hahn, T., & Schaltegger, S. (2002). Towards a comprehensive framework for environmental management accounting – links between business actors and EMA tools. Australian Accounting Review, 12(27), 39–50. https://doi.org/10.1111/j.1835-2561.2002.tb00202.x

- Christ, K. (2014). Water management accounting and the wine supply chain: Empirical evidence from Australia. The British Accounting Review, 46(4), 379–396. https://doi.org/10.1016/j.bar.2014.10.003

- Christ, K., & Burritt, R. (2017). Water management accounting: A framework for corporate practice. Journal of Cleaner Production, 152, 379–386. https://doi.org/10.1016/j.jclepro.2017.03.147

- Christ, K. L., & Burritt, R. L. (2017). What constitutes contemporary corporate water accounting? A review from a management perspective. Sustainable Development, 25(2), 138–149. https://doi.org/10.1002/sd.1668

- Daniel, M. A., & Sojamo, S. (2012). From risks to shared value? Corporate strategies in building a global water accounting and disclosure regime. Water Alternatives, 5(3), 636–657.

- Emenike, C., Tenebe, I., Omole, D., Ngene, B., Oniemayin, B., Maxwell, O., & Onoka, B. (2017). Accessing safe drinking water in sub-Saharan Africa: Issues and challenges in South–West Nigeria. Sustainable Cities and Society, 30, 263–272. https://doi.org/10.1016/j.scs.2017.01.005

- Ezenwoke, O., Ezenwoke, A., Eluyela, D., & Olusanmi, O. (2019). A bibliometric study of accounting information systems research from 1975-2017. Asian Journal of Scientific Research, 12(2), 167–178. https://doi.org/10.3923/ajsr.2019.167.178

- Imtiaz Ferdous, M., Adams, C., & Boyce, G. (2019). Institutional drivers of environmental management accounting adoption in public sector water organisations. Accounting, Auditing and Accountability Journal, 32(4), 984–1012. https://doi.org/10.1108/AAAJ-09-2017-3145

- Merediz-Solà, I., & Bariviera, A. F. (2019). A bibliometric analysis of bitcoin scientific production. Research in International Business and Finance, 50, 294–305. https://doi.org/10.1016/j.ribaf.2019.06.008

- Molden, D. (1997). Accounting for water use and productivity. International Irrigation Management Institute.

- Morrison, J., Schulte, P., & Schenek, R. (2010). Corporate water accounting: An analysis of methods and tools for measuring water use and its impacts. Pacific Institute.

- Mudge, S. (2008). Environmental forensics and the importance of source identification. Issues in Environmental Science and Technology, 26, 1–17. https://doi.org/10.1039/9781847558343-00001

- Omole, D., Jim-George, T., & Akpan, V. (2019). Economic analysis of wastewater reuse in Covenant University. Journal of Physiscs; Conference Series, 1–10. DOI: 10.1088/1742-6596/1299/1/012125

- Omole, D., & Ndambuki, J. (2015). Nigeria’s legal instruments for land and water use: Implications for national development. In E. Osabuohien (Ed.), Handbook of research on in-country determinants and implications of foreign land Acquisitions (pp. 354–373). IGI Global.

- Pacific Institute. (2009). Climate change and the global water crisis: What businesses need to know and do.

- Pawsey, N. (2015). Water management accounting and the wine supply chain: Empirical evidence from Australia. Social and Environmental Accountability Journal, 35(3), 195. https://doi.org/10.1080/0969160X.2015.1093770

- Rialp, A., Merigó, J., Cancino, C., & Urbano, D. (2019). Twenty-five years (1992–2016) of the international business review: A bibliometric overview. International Business Review, 28(6), 51. https://doi.org/10.1016/j.ibusrev.2019.101587

- Rodríguez-Ruiz, F., Almodóvar, P., & Nguyen, Q. (2019). Intellectual structure of international new venture research: A bibliometric analysis and suggestions for a future research agenda. Multinational Business Review, 27(4), 285–316. https://doi.org/10.1108/MBR-01-2018-0003

- Schaltegger, S., Hahn, T., & Burritt, R. (2000). Environmental management accounting: Overview and main approaches. Center for Sustainability, 1.

- Scopus. (2017) . Content coverage guide. Elsevier.

- Signori, S., & Bodino, G. (2013). Water management and accounting: Remarks and new insights from an accountability perspective. Studies in Managerial and Financial Accounting, 26, 115–161. DOI: 10.1108/S1479-3512(2013)0000026004

- Steinbach, N., Palm, V., Cederlund, M., Georgescu, A., & Hass, J. (2009). Environmental taxes. Statistics Sweden. https://unstats.un.org/unsd/envaccounting/londongroup/meeting14/LG14_18a.pdf

- Torres López, S., Barrionuevo, M., & Rodríguez-Labajos, B. (2019). Water accounts in decision-making processes of urban water management: Benefits, limitations and implications in a real implementation. Sustainable Cities and Society, 50, 101676. https://doi.org/10.1016/j.scs.2019.101676

- Yang, Y., Reniers, G., Chen, G., & Goerlandt, F. (2019). A bibliometric review of laboratory safety in universities. Safety Science, 27, 60–62. https://doi.org/10.1016/j.ssci.2019.06.022

- Zhan-Ming, C., & Chen, G. (2013). Virtual water accounting for the globalized world economy: National water footprint and international virtual water trade. Ecological Indicators, 28(1), 142–149. https://doi.org/10.1016/j.ecolind.2012.07.024