Abstract

Students of the millennial generation have several characteristics, including being wasteful in their management of money and being highly dependent on information and communication technology. These phenomena mean financial literacy is important for them, in order that they become capable, wise, and efficient individuals who are future-oriented in managing their personal finances. This study aims to create a model for developing the financial management behavior of students. It covers five variables, namely financial behavior, financial attitude, financial knowledge, social media exposure, and peer influence. By using purposive sampling and a five-point Likert scale questionnaire, this study collected data from 327 students spread across several universities in Indonesia. The results of the descriptive analysis show that the students’ financial management behavior (FMB), financial attitude, and financial knowledge are classified as good. Structural equation modeling (SEM) analysis using the single-composite indicator technique shows that 58% of FMB is influenced by financial exposure from social media, financial attitude, and peer influence. Social media exposure and peer influence take on a strategic nature. Financial knowledge, financial attitude, and financial behavior are internal variables related to financial literacy. Further research would need to identify the external variables that have a potential influence on the internal variables of financial literacy.

PUBLIC INTEREST STATEMENT

Millennial generation has several characteristics, including a high dependence on technology and wasteful use of money. Therefore, the millennial generation, including students, need to be equipped with financial literacy education so that they can manage finances prudently in the future. Financial literacy consists of three components, namely financial knowledge, financial attitude, and financial behavior. Financial knowledge affects financial attitude and financial attitude, in turn, affects financial behavior. Social media as a platform for making social contact has important roles in developing students’ financial literacy. Likewise, peer also has significant influence on students’ financial knowledge and behavior. Indirect influence of Peers on the students’ financial attitude was also statistically significant. Educators need to consider the use of social media and peer influence in developing financial literacy among the millennial generation.

1. Introduction

Students’ financial behavior receives a lot of attention from researchers in Indonesia such as Herawati (Citation2015), Laily (Citation2016), and Upadana and Herawati (Citation2020). This is motivated by the fact that students today are members of the millennial generation who have very particular characteristics. The terms “millennial generation” or “Generation Y” refer to the generation born between 1980 and 2000 (DeVaney, Citation2015) or the generation born in 1980 or later (Ng et al., Citation2010). This generation has different characteristics from previous generations (Farrell & Hurt, Citation2014), because the millennial generation was raised in an environment that was beginning to globalize and experience the massive use of information and communication technology (internet). Currently, members of the millennial generation in Indonesia number over 63 million, which is a very significant proportion of the population.

Millennials have unique characteristics, including wastefulness (Nurhadi, Citation2020; Yuwono & Juniani, Citation2020) and they depend on internet technology a lot (Kurnia, Citation2020). The wasteful nature of the millennial generation, regarding their money management skills, is mostly influenced by their life-style which is exemplified by their use of online media (Nurhadi, Citation2020). Besides this, the number of social media users in Indonesia has reached 150 million people, where Facebook and Instagram are the most widely used platforms (Pertiwi, Citation2019). The millennial generation’s information technology literacy and the ease of shopping online are also important factors that cause their consumptive lifestyle. Previous study found that the use of internet is significantly correlated with consumption behavior (Pabedinskaitė & Šliažaitė, Citation2012). Therefore, control is needed so that the millennial generation does not fall into economic difficulties in the future, because they are not clever at managing their finances. Previous research has found that self-control does not have a significant effect on saving behavior (Yuwono & Juniani, Citation2020), which means that the millennial generation is less able to control its saving behavior. Students need to be equipped with knowledge and attitudes so that they are more prudent at managing their finances. Navickas et al. (Citation2014) contended that financial literacy has an important role for young households in managing their personal finances. Therefore, universities need to provide a learning environment that allows students to improve their ability to manage their personal finances.

Studies focusing on the financial behavior among Indonesian students have been conducted by some academics. Herdjiono and Damanik (Citation2016) examined the effect of financial knowledge, financial attitude, and parents’ income on students’ financial behavior. Laily (Citation2016) examined the effect of students’ characteristics on financial behavior with financial literacy as a mediating variable. Dewi et al. (Citation2020) focused their study on the determinants of finacial literacy among Indonesian academics. Lastly, Alexandro (Citation2019) examined the effect of economic literacy and economic education on students’ economic behavior. Research on the role of social media and peers’ influence on financial knowledge, financial attitude, and financial behavior among Indonesian students seems to be non-existent.

Previous studies found that social media has negative impacts on social life. For example, social media has an unfavorable impacts on the health of youth (Rambaree et al., Citation2020) and the social life of citizens (Mugari & Cheng, Citation2020). However, there are many positive impacts of social media on social life as contended by De Las Heras-Pedrosa et al. (Citation2020) that social media can be a promising health communication tool between hospitals and their patients. Therefore, there is a possibility that social media can also be used as a platform to develop financial literacy among millennial generation.

This research is based on an understanding that financial literacy’s factors—knowledge, attitude, and behavior—do not appear simultaneously, but there is a causal relationship between them. Fessler et al. (Citation2019) have attempted to treat the three factors of financial literacy as independent variables. Financial behavior is individual behavior in making decisions regarding managing personal finances that are efficient and productive for long-term needs. This behavior is needed by the millennial generation, especially students, so that they can become a generation that is more prudent in managing their personal finances. Research conducted by Van Rooij et al. (Citation2011) found that financial literacy plays a very important role in the financial decision-making of individuals. The purpose of this study is to identify a model for developing financial behavior among college students, who are members of the millennial generation, by taking into account several variables that have the potential to be influences. This model will be useful for universities in providing more effective learning about personal financial management so that graduates have sufficient abilities to manage their personal finances in the present and in the future.

2. Literature review and hypothesis development

2.1. Financial knowledge, attitude, and behavior

Currently, information and communication technology and globalization have changed individual behavior in terms of consumption behavior (Sima et al., Citation2020) and personal financial management (Servon & Kaestner, Citation2008). Individuals who use information and communication technology find it easier to obtain various types of information about goods, services and finance. Millennials use this technology very intensively (Kurnia, Citation2020), so they tend to be more wasteful when spending their money (Nurhadi, Citation2020; Yuwono & Juniani, Citation2020). Students, as members of the millennial generation, need to adopt smarter financial behavior so that they can manage their finances better.

Research conducted by the OECD-INFE (Citation2011) finds that financial literacy is based on three factors, namely knowledge, attitude, and behavior. The measurement of financial literacy is also based on these factors. Subsequent researchers such as Potrich et al. (Citation2016), Fessler et al. (Citation2019), and Yahaya et al. (Citation2019) treat these three factors separately. Therefore, this study also treats the three factors—knowledge, attitude, and behavior—as internal variables of financial literacy.

As previously stated, financial literacy consists of knowledge, attitude, and behavior (Potrich et al., Citation2016). However, measuring financial literacy by adding the three factors as suggested by the OECD-INFE (Citation2011) may be misleading (Fessler et al. (Citation2019). In other words, knowledge, attitide, and behavior are different variables which may have a causality relationship. Furthermore, Fessler et al. (Citation2019) and Yahaya et al. (Citation2019) state that knowledge affects attitude, and attitude, in turn, affects behavior. Meanwhile, knowledge does not have a significant effect on financial behavior (Yahaya et al., Citation2019). In other words, attitude is a mediating variable between knowledge and behavior.

Financial management behavior (FMB) is rational individual behavior for planning, implementing, and evaluating personal financial decisions. These decisions include how individuals spend money, make investments, and evaluate their personal financial position. The previously developed behavioral theory explains that attitude is an important variable in determining behavior through intention as an intervening variable (Ajzen, Citation1991). However, research conducted by Herdjiono and Damanik (Citation2016) finds that attitude has a direct influence on students’ personal financial management behavior. Furthermore, Ibrahim and Alqaydi (Citation2013) also find that individuals with a strong financial attitude tend to be more careful in using credit cards. Other studies have also found that attitude is a determinant of financial management behavior (Yap et al., Citation2018). According to research conducted in Austria, financial attitude has a causal relationship with financial behavior (Fessler et al., Citation2019).

2.2. Social media, financial knowledge, attitude, and behavior

Members of the millennial generation who were born and raised in the era of information and communication technology have turned social media into an important medium for various purposes. As stated by Kurnia (Citation2020), the millennial generation has a high dependence on internet technology. Yusop and Sumari (Citation2013) also find that the millennial generation, especially students, uses social media for communication, socialization, financial information retrieval, and for research purposes in order to complete college assignments. Social media is a promising tool for communication between hospitals and their patients (De Las Heras-Pedrosa et al., Citation2020). Social media is increasingly important because, in Indonesia, the number of users is very high (Pertiwi, Citation2019) which allows social media to be used for various purposes, including improving students’ financial literacy. Meanwhile, researchers are more concerned with the influence of social media on consumer behavior. Kumar et al. (Citation2016), Godey et al. (Citation2016), and Pabedinskaitė and Šliažaitė (Citation2012) find that social media is able to influence consumer behavior. It is likely that the use of social media also affects students’ financial behavior.

Besides influencing students’ financial behavior, social media is likely to have an influence on their financial attitude. Research with student respondents conducted by Herdjiono and Damanik (Citation2016) concludes that financial attitude is usually influenced by social interactions. This proposition is based on the results of research into whether social media can influence brand attitude (Khair & Ma’ruf, Citation2020). Other studies have found that customer attitude is a strong mediator between social media and the intention to purchase (Lim et al., Citation2017). The results from these two studies can be used as the basis for making the proposition that social media also possibly plays an important role in shaping the financial attitude of students.

As stated by Yusop and Sumari (Citation2013), one of the functions of social media for students is for research purposes when completing university assignments. By using the meta analysis Ahmed et al. (Citation2019), concluded that social media is becoming more important for the purposes of sharing knowledge. Likewise, Eid and Al-Jabri (Citation2016) have also found that students use social media for knowledge sharing purposes. Besides being a medium for sharing knowledge, social media also has a role in increasing students’ engagement and information exchanges (Evans, Citation2014) and improving the teaching and learning process (Rasiah, Citation2014). In other words, social media has a more important role in the education process in higher education. Most likely, social media also has an important role in developing students’ financial literacy.

2.3. Peer influence, social media and financial knowledge

Peers is one of references for an individual to think, perceive and behave. In the learning process peers play an important role for an individual engaged. One of the important roles of peers is to help friends solve learning problems (Wentzel, Citation2017). Because of its strategic influence lecturers, as facilitators of the learning process, often use collaborative learning where students can work together. In the era of information and communication technology, millennials mostly use social media to socialize with their peers. Research conducted in America and China shows that communication with peers has a positive and significant effect on shopping behavior using social media (Muralidharan & Men, Citation2015). Subjective norms are a kind of pressure that peers or other parties bring to bear upon individuals to do something, for example, to use technology. Subjective norms play an important role in increasing individuals’ intention to make purchases using social media (Sin et al., Citation2012). Furthermore, Isomidinova et al. (Citation2017) find that the agent of socialization has a significant impact on financial literacy, even though the money attitude variable does not have a significant effect. The insignificant effect of money attitude on financial literacy in the study of Isomidinova et al. (Citation2017) may be caused by multicolonierity problems—there is a significant correlation between the independent variables—causing the variable of money attitude to have no significant effect on financial literacy. The findings of this study can serve as the basis for the idea that peers play a significant role in individuals using social media, and are also able to change an individual’s behavior.

Individuals who enjoy positive relationships with their peers will reap the benefits, namely increased academic accomplishments (Wentzel, Citation2017). Relationships with peers serve as a forum for joint learning (Fahraeus, Citation2004) by exchanging various types of information including knowledge exchanges. Previous studies found that social networks can be used as a means of exchanging relevant content (Yang & Chen, Citation2008) and sharing knowledge (Ahmed et al., Citation2019; Eid & Al-Jabri, Citation2016; Evans, Citation2014). The strong role of peers in providing information and knowledge to individuals is used as the basis for collaborative learning. Research conducted by Erkens and Bodemer (Citation2019) finds that collaborative learning is a feasible method for sharing knowledge. It is possible that peers will play an important role in increasing financial knowledge.

2.4. Hypothesis

The characteristics of the millennial generation include their high dependence on information technology (Kurnia, Citation2020) and their wasteful nature in financial management (Nurhadi, Citation2020; Yuwono & Juniani, Citation2020). Therefore, the millennial generation needs financial literacy education so that they are better able manage personal finances. Financial literacy has an important role for individuals in making personal financial decisions (Van Rooij et al., Citation2011) and in managing personal finances in the household (Navickas et al., Citation2014). Financial literacy consists of three factors, namely financial knowledge, financial attitude, and financial behavior (Fessler et al., Citation2019; OECD-INFE, Citation2011; Potrich et al., Citation2016; Yahaya et al., Citation2019). Financial knowledge has an influence on financial attitude and in turn financial attitude has an influence on financial behavior (Fessler et al., Citation2019; Herdjiono & Damanik, Citation2016; Yahaya et al., Citation2019; Yap et al., Citation2018).

Millennials use social media for various purposes, such as communication, socializing, and for seeking information in order to complete school assignments (Yusop & Sumari, Citation2013) and for knowledge sharing (Ahmed et al., Citation2019; Eid & Al-Jabri, Citation2016). Social interaction is an important determinant of financial attitude (Herdjiono & Damanik, Citation2016). In addition, social media has a significant influence on customer attitude (Lim et al., Citation2017). Information technology also has a significant influence on individual consumption behavior (Sima et al., Citation2020). It is likely that social media also affects the millennial generation’s financial knowledge, financial attitude and financial behavior.

In the learning process, peers play an important role in helping solve problems (Wentzel, Citation2017), exchanging relevant content (Yang & Chen, Citation2008), and sharing knowledge (Ahmed et al., Citation2019; Eid & Al-Jabri, Citation2016; Evans, Citation2014). In addition, peers play a role in influencing shopping events using social media (Muralidharan & Men, Citation2015; Sin et al., Citation2012). It is likely that social media exposure has a positive influence on financial knowledge, financial behavior, and the use of social media for the millennial generation.

Financial behavior is jointly determined by financial attitude, peer influence, and social media exposure. In turn, financial attitude is influenced by knowledge and at the same time financial attitude serves as an intervening variable between knowledge and financial behavior. Moreover, social media exposure also has an influence on financial attitude and financial knowledge. Finally, peer influence also affects the use of social media and student knowledge. This hypothesis model will be tested with data and analysis to obtain a fit and parsimonious empirical model. The study posits eight hypotheses as follows:

H1: Financial attitude has a significant influence on the financial management behavior of students.

H2: Knowledge has a significant influence on financial attitude.

H3: Students’ exposure to social media affects their financial behavior.

H4: Social media plays a positive role in shaping students’ financial attitudes.

H5: Social media plays an important role in increasing students’ financial knowledge.

H6: Peers have an influence on the financial behavior of students.

H7: Peers have an influence on students’ exposure to social media.

H8: Peers have an influence on students’ financial knowledge.

3. Research methods

The population of this study comprises students from the economics faculties of Indonesian universities in 2020. Data were collected using purposive sampling by distributing a Google Form questionnaire link to all the public and private universities. With this online survey method, and being voluntary in nature, this study has succeeded in collecting data from 327 submissions from respondents in several regions of Indonesia. This number of respondents is sufficient for the purposes of structural equation modeling analysis, as presented by Kline (Citation2016, p. 16), who states that the amount of data required for SEM analysis is at least 200 responses.

This study covers five latent variables, namely financial behavior, financial attitude, financial knowledge, exposure to social media, and peer influence. The financial behavior variable measures the individual’s financial behavior in making decisions, so that his/her finances can be used efficiently and productively for long-term needs. Dew and Xiao (Citation2011) state that financial management behavior has four main factors, namely consumption, cash flow management, saving and investment, and credit management. Financial attitude is used to measure students’ attitudes towards the importance of acting prudently in personal financial. Financial attitude is a value held by individuals when applying financial principles to decision making, in order to properly utilize resources (Rajna et al., Citation2011). The knowledge variable is the personal financial knowledge that the students possess. According to Potrich et al. (Citation2016), financial knowledge is classified into basic knowledge and advanced knowledge. The social media exposure variable measures how students behave in using social media to gain financial information, investment information, and knowledge, as well as to expand their networks. Peer influence measures the impact of social contact with peers to exchange knowledge, and engage in financial planning, spending money, and investing.

4. Results

4.1. Research instrument’s test

In developing the research instruments, this study adapts the scale of measurement for knowledge, attitude, and financial behavior that was previously developed by Potrich et al. (Citation2016) and Dew and Xiao (Citation2011), which are then tested in Indonesian cultural settings. Furthermore, this research develops social media and peer influence instruments. After designing the instruments, they were then tested and analyzed to ensure they were valid and reliable instruments.

This study has conducted validity and reliability tests using the corrected-item total correlation (CITC) and Cronbach’s alpha. The results of the validity and reliability analysis show that all the statement items used to collect data have met the validity and reliability requirements. De Vaus (Citation2013) states that CITC is considered valid if it has a coefficient of above 0.3 and an instrument is considered reliable if it has a Cronbach’s alpha coefficient above 0.7. shows that the lowest CITC value is 0.349. Initially, knowledge was classified into two parts, namely “Basic Knowledge” with seven statement items, and “Advanced Knowledge” with nine statement items. These two variables are put together because there is a high correlation between basic knowledge and advanced knowledge. The combined results show better results, having a Cronbach’s alpha coefficient of 0.914, with the lowest CITC value being 0.405. above provides more complete information about the validity and reliability of the instrument.

Table 1. Validity and reliability test

This study uses descriptive analysis to determine the extent of each variable. The mean, min, max, and standard deviation values are used to describe the variables. The next analysis is structural equation modeling using the single-composite indicator (SIC) technique. This technique is used to obtain a parsimonious SEM model, making it easy to achieve a fit model (Ghozali, Citation2007). In addition, this SIC technique avoids the disposal of variable indicators to obtain a fit model. This analysis technique begins with manually calculating the composite loading factor and the composite variance error of all the latent variables. The results of this calculation are included in the factor loading parameter and the error variance of each latent variable in the AMOS model. In addition, the data from the indicators are also calculated using the factor score weight to obtain composite data.

To provide information of model’s goodness of fit, the study calculated several indices, as suggested by Yanto et al. (Citation2017). The expected value of chi-squared is not significant with a p value > 0.05. This means that the covariance matrix of the sample and population is not different. Value of CMIN/d.f. is expected to be less than 3.00 (Ferdinand, Citation2005), while the RMSEA value should be below 0.08 (Ferdinand, Citation2005; Ghozali, Citation2007). Other indices used are GFI, AGFI, NFI, CFI and TLI with a minimum threshold value of 0.9 each (Ghozali, Citation2007). Besides this, a multivariate nomality test has also been conducted. The value of the multivariate normality should be below 2.58. If this value is above 2.58, this study will perform bootstrapping using the Bollen-Stine technique. The SEM analysis can be continued if the Bollen-Stine p coefficient is above 0.05 (Whidiarso, Citation2012).

4.2. Descriptive analysis

The results of the descriptive analysis show that financial behavior has an average score of 47.99 (80%), with the lowest score being 23 and the highest score being 60, with a standard deviation of 7.196. If the average value is divided by the number of question items, it produces the number 3.99, which means that the students perceive that their financial behavior can be categorized as good. Financial attitude has an average value of 44.70 (89%) with ten statement items which means that financial attitude is in the good category (4.44). Students’ knowledge of finance can be classified as good with the average score being 58.07 (73%), the lowest score being 26.00 with a standard deviation of 5.366. Social media exposure can be categorized as good with an average of 38.1 and the number of items being nine, while peer influence has an average value of 24.49 (70%) and a standard deviation of 5.79, gained from seven items, can be classified as sufficient. provides more complete information regarding this descriptive analysis.

Table 2. Descriptive analysis

4.3. Structural equation modelling (SEM) analysis

This study has five latent variables with 54 question items (), which means that the model developed using structural equation modeling will have at least 54 parameters. If all the parameters into the model were entered, this research would experience many difficulties in fulfilling the goodness of fit test. Besides this, the model that has been built will also be difficult and complex. In other words, the model that has been developed will not be parsimonious. To obtain a model that is parsimonious and fit, researchers usually reduce the number of indicators, reduce the amount of data, or use other techniques. To avoid a complicated model or the omission of indicators, this study uses SEM analysis with a single composite indicator (SCI) technique. This technique combines all the indicators into a single composite indicator with a manual calculation procedure.

Table 3. Single composite indicator

The results of calculations using spread sheet find the composite loading factor for the knowledge variable to be 0.546483017 and the composite variance error to be 0.017878996. These two coefficients have been entered into the parameters of the AMOS model and analyzed using the original data that had been adjusted for the factor score weight. The results of the analysis show that the factor loading rate for a single composite is 0.961 from the knowledge variable. The financial behavior variable has a composite loading factor of 0.46863132 and a composite variance error of 0.03043463. After these two numbers are included in the factor loading and error parameters of the AMOS model, it has been found that the factor loading of a single composite is 0.934 for the financial behavior variable. provides information that the factor loading of a single composite has good performance with all the coefficient values exceeding 0.9. With a factor loading value for a single composite above 0.9, it is expected to be able to present all the indicators for each latent variable. By using one indicator for each variable, the model developed for this study will be simpler, and it will be easier to obtain a satisfactory goodness of fit. below provides more complete information about the composite factor loading parameters, composite error parameters of the variance, and the factor loading for a single composite for each latent variable.

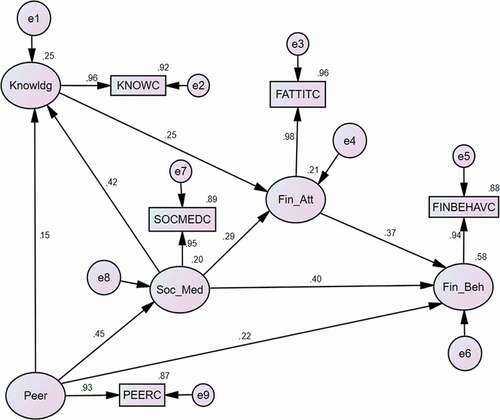

The results of the SEM analysis using the SCI technique show that financial behavior is significantly influenced by three variables, namely financial attitude with an estimated value of 0.368 (p < 0.05), social media exposure with an estimated value of 0.401 (p < 0.05), and the peer influence variable has an estiamated value of 0.223 (p < 0.05). The results of the squared multiple correlation calculation show that these three variables have a coefficient of 0.581 or the effect of these three variables reaches 58%. This also means that 58% of the variations in financial behavior are influenced by variations in financial attitude, social media exposure, and peer influence. Financial attitude, as an intervening variable, is influenced by students’ financial knowledge (0.246, p < 0.05) and students’ exposure to social media (0.285, p < 0.05). The squared multiple correlation value for the two variables is 0.211 or (21%). In other words, 21% of the variation in financial attitude is influenced by variations in financial knowledge and social media. Further analysis also shows that Peer has significant indirect on financial attitude with beta of 0.212.

Exposure to social media has a significant influence on students’ financial knowledge with an estimate value of 0.419 (p < 0.05). Peer influence also has a significant impact on students’ financial knowledge (0.149, p < 0.05), and affects students’ exposure to the use of social media (0.452, p < 0.05). The squared multiple correlation value is 0.254 or 25%, meaning that students’ financial knowledge is influenced by peer influence and exposure to social media. Thus, the eight hypotheses proposed by this study are all accepted. below is a summary of the results of the hypotheses’ testing.

Table 4. Summary of hypothesis testing

is a summary of the results of the hypotheses’ testing in visual form. This model is an empirical model that has fulfilled several indices for goodness of fit. The result of the analysis shows that the chi-squared value is 3.503 (p = 0.174), which means that the p value exceeds 0.05. The CMIN/d.f value obtained is 1.751 with a threshold value below 3.0. The next test is GFI and AGFI with a value of 0.996 and 0.968, respectively, with a minimum limit requirement of 0.9 for these two indices. Meanwhile, the baseline comparisons of NFI, TLI, and CFI have respective values of 0.992, 0.982, and 0.996 with a value of 0.9 being the lowest value. The RMSEA index value is 0.048 which also meets the requirement, which is that it is below 0.08. Thus, the results of the goodness of fit test using the eight indices provide evidence that the model is a good fit.

Figure 1. Improving financial literacy among the millennial generation

The results of the analysis show that the multivariate normality is 27.962 which means that the data’s distribution is not normal. This abnormality is mostly caused by the distribution of data from the financial attitude variable, with a c.r. kurtosis value amounting to 21.648. Therefore, this study has carried out bootstrapping with a sample size of 2,000. The results of this bootstrapping analysis using the Bollen-Stine technique showed a p-value of 0.212 (p > 0.05) which means that the SEM analysis can be continued.

5. Discussion

Financial literacy, which has been measured by adding up the scores of three factors, namely financial knowledge, attitude and financial behavior, needs to be separated, because financial behavior is significantly influenced by financial attitude, while financial attitude is influenced by financial knowledge. This study has found that financial knowledge has an influence on financial attitude. In turn, financial attitude has an influence on financial behavior. These results support the findings of Fessler et al. (Citation2019), and Yahaya et al. (Citation2019). The influence of financial attitude on financial behavior has also been demonstrated by previous researchers such as Herdjiono and Damanik (Citation2016), Ibrahim and Alqaydi (Citation2013), and Yap et al. (Citation2018). Future research could treat financial knowledge, financial attitude, and financial behavior, as stated by OECD-INFE (Citation2011), as internal variables of financial literacy.

As previously stated, students are members of the millennial generation which relies heavily on internet technology. It turns out that the results of this study have found that the students’ exposure to social media has positive benefits for learning financial literacy. Social media has a significant influence on financial behavior. This findings are in line with previous studies that the use of social media (Godey et al., Citation2016; Kumar et al., Citation2016) and internet (Pabedinskaitė & Šliažaitė, Citation2012) can change consumer behavior. Social media also has a positive role in developing students’ financial attitudes, because social media serves as a tool for virtual social interaction. According to Herdjiono and Damanik (Citation2016), attitude is influenced by the social interactions engaged in by students. The findings of studies in the marketing field that social media can influence brand attitude (Khair & Ma’ruf, Citation2020) and customers’ attitudes (Lim et al., Citation2017) are in line with the finding of this study. This study found that social media exposure can influence students’ financial attitude. Another function of social media is as a tool for sharing knowledge and the completion of college assignments. These findings are supported by the results of this study, which show that social media can increase students’ financial knowledge. In other words, students use social media not only for communication purposes, but also as a means to seek and exchange financial knowledge.

This study has also found that peers play an important role in the learning process of financial literacy. Their role in improving students’ financial knowledge is quite significant. Peers assist with solving common problems students encounter in learning (Wentzel, Citation2017) and they share knowledge materials. Therefore, educators should always carry out collaborative learning with the aim of providing a place for students to study together. Lecturers have an important role in facilitating students to learn from each other and share knowledge based on the perspective of each student.

This study has found that peers play a strong role in changing financial behavior. This finding is in line with the results of research in the field of marketing showing that communication with peers can change individual behavior. Individual word of mouth between peers has the potential to change individual behavior. This finding is in line with the results of research conducted in community settings in America and China, showing that communication with peers can change individual behavior. This finding is also consistent with the technology acceptance model (TAM) in which subjective norms—pressure from outside the individual, including peers—have a significant effect on the intention to purchase products. This study has found that peers have a significant influence on students’ exposure to social media. This finding also means that subjective norms (peer pressure) have an influence on the use of social media by students.

The results of descriptive analysis show that the students’ financial behavior can be classified as good. Financial behavior is formed by an educational process based on both a curriculum and extracurricula activities. To improve the quality of students’ financial behavior, lecturers need to consider the use of social media for learning financial literacy, as suggested by Rasiah Rasiah (Citation2014) and Evans (Citation2014). The role of social media in learning financial literacy occupies a strategic place, because social media is able to influence all the variables of financial literacy, namely financial knowledge, financial attitude, and financial behavior. The role of social media will be even more important in financial literacy education, because the number of social media users is very significant (Pertiwi, Citation2019), so the use of social media will be able to reach many targets. Besides paying attention to social media, financial literacy learning also needs to pay attention to peer influence. Peer influence also plays an important role in developing financial behavior, financial knowledge, and exposure to social media.

The success in improving the quality of students’ financial behavior is largely influenced by social media, their financial attitude and peer influence. The problems with the millennial generation are that they are wasteful (Nurhadi, Citation2020; Yuwono & Juniani, Citation2020). On the other hand, the millennial generation’s number of members is very significant, so developing rational financial behavior is seen as important for their future. Since financial literacy is pivotal for young generation for managing personal finances, universities needs to carry out financial literacy education intensively, with various modes of learning including learning using social media and making maximum use of the role of peers. The use of collaborative learning is increasingly important for learning financial literacy, according to the recommendations of Erkens and Bodemer (Citation2019). Therefore, this education must equip students with sufficient financial literacy so that individuals are able to make better financial decisions. Regardless of the unfavorable impact of social media on personal and social life, this research found the bright side that social media has pivotal roles in building financial literacy among millennial generation.

6. Conclusion

Students at the faculties of economics of several universities in Indonesia have good financial literacy. More specifically, the students’ performance in terms of financial knowledge, financial attitude, and financial behavior can also be classified as good. Students’ exposure to social media is also classified as good, while peer influence is still classified as sufficient. Financial attitude is an interverning variable between the financial knowledge and financial behavior variables. These three variables can be treated as the internal variables of financial literacy where financial behavior is influenced by financial attitude, and financial attutude is influenced by both basic and advanced financial knowledge.

With a very significant number of users, social media provides benfits for building financial literacy, which consists of financial knowledge, financial attitude, and financial behavior. The society must give a positive effect in social media, which has the greatest influence on financial knowledge, followed by financial behavior and financial attitude. When studying financial literacy, it should be possible to take advantage of social media considering that students, as members of the millennial generation, are highly dependent on information and communication technology. Peer influence has a strategic role in developing financial literacy. Peers have a significant influence on social media exposure, financial behavior and financial knowledge. Peer influence also indirectly affect financial attitude. Collaborative learning is one of the promising strategies for students to use when learning financial literacy.

Educators need to take advantage of social media, not only for social purposes, but for teaching the students who are learning financial management. Financial management content needs to be posted on social media as study materials for students. Given the important role of peers, educators need to continue to take advantage of the influence of peers in designing models for learning financial literacy.

Limitation of this research is this study uses purposive sampling which means inaccuracies in our sampling is possible. Future research would need to be conducted using multi-stage sampling to ensure that the samples analyzed are truly representative. In addition, this study only collected data from economics and business students. Collecting data form other major students may provide different conclusion. This research also just collect data from Indonesian students who have a same culture each others. Subsequent research would also need to identify external variables that have the potential to affect the internal variables of financial literacy i.e. financial knowledge, financial attitude, and financial behavior. Future research also needs to collect data from non-economics and business students and students from other country to compare and provide more complete information about financial literacy among millennial generation.

Additional information

Funding

Notes on contributors

Heri Yanto

Heri Yanto is an associate professor at the Department of Accounting, Universitas Negeri Semarang, Indonesia. His research interests are accounting education, environmental accounting, and behavioural accounting and finance.

Norashikin Ismail

Norashikin Ismail is an associate professor of accounting and finance, Universiti Teknologi MARA, Shah Alam Selangor, Malaysia. Her research interest are corporate governance and sustainability, behavioral finance and accounting.

Kiswanto Kiswanto

Kiswanto Kiswanto is an associate professor in accounting at the Universitas negeri Semarang. His research interests are taxation, behavioral finance and accounting, environmental accounting.

Nurhazrina Mat Rahim

Nurhazrina Mat Rahim is a lecturer of accounting and finance. Her research interests are behavioral finance and accounting, accounting education, and financial accounting.

Niswah Baroroh

Niswah Baroroh an assistant professor at the Department of Accounting, Universitas Negeri Semarang. Her research interests are sustainability reports, intellectual capital, enterprise risk management and SMEs.

References

- Ahmed, Y. A., Ahmad, M. N., Ahmad, N., & Zakaria, N. H. (2019). Social media for knowledge-sharing: A systematic literature review. Telematics and Informatics, 37, 72–15. https://doi.org/10.1016/j.tele.2018.01.015

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/10.1016/0749-5978(91)90020-T

- Alexandro, R. (2019). Factors affecting student financial behavior in Indonesia. Humanities, 4(2), 380–391. https://doi.org/10.20448/801.42.380.391

- De Las Heras-Pedrosa, C., Rando-Cueto, D., Jambrino-Maldonado, C., Paniagua-Rojano, F. J., & Feng, G. C.. (2020). Analysis and study of hospital communication via social media from the patient perspective. Cogent Social Sciences, 6(1), 1718578. https://doi.org/10.1080/23311886.2020.1718578

- De Vaus, D. (2013). Surveys in social research. Routledge.

- DeVaney, S. A. (2015). Understanding the millennial generation. Journal of Financial Service Professionals, 69(6), 11–14.

- Dew, J., & Xiao, J. J. (2011). The financial management behavior scale: Development and validation. Journal of Financial Counseling and Planning, 22(1), 43–59.

- Dewi, V. I., Febrian, E., Effendi, N., Anwar, M., & Nidar, S. R. (2020). Financial literacy and its variables: The evidence from Indonesia. Economics & Sociology, 13(3), 133–154. https://doi.org/10.14254/2071-789X.2020/13-3/9

- Eid, M. I. M., & Al-Jabri, I. M. (2016). Social networking, knowledge sharing, and student learning: The case of university students. Computers & Education, 99, 14–27. https://doi.org/10.1016/j.compedu.2016.04.007

- Erkens, M., & Bodemer, D. (2019). Improving collaborative learning: Guiding knowledge exchange through the provision of information about learning partners and learning contents. Computers & Education, 128, 452–472. https://doi.org/10.1016/j.compedu.2018.10.009

- Evans, C. (2014). Twitter for teaching: Can social media be used to enhance the process of learning? British Journal of Educational Technology, 45(5), 902–915. https://doi.org/10.1111/bjet.12099

- Fahraeus, E. R. (2004). Distance education students moving towards collaborative learning-A field study of Australian distance education students and systems. Journal of Educational Technology and Society, 7(2), 129–140.

- Farrell, L., & Hurt, A. C. (2014). Training the millennial generation: Implications for organizational climate. E Journal of Organizational Learning & Leadership, 12(1), 47–60.

- Ferdinand, A. (2005). Structural equation modeling dalam Penelitian Manajemen edisi 3. Badan Penerbit Universitas Diponegoro.

- Fessler, P., Silgoner, M., & Weber, R. (2019). Financial knowledge, attitude and behavior: Evidence from the Austrian survey of financial literacy. Empirica, 47, 1–19. https://doi.org/10.1007/s10663-019-09465-2

- Ghozali, I. (2007). Structural equation modelling: Konsep dan aplikasi dengan AMOS. Badan Penerbit Universitas Diponegoro.

- Godey, B., Manthiou, A., Pederzoli, D., Rokka, J., Aiello, G., Donvito, R., & Singh, R. (2016). Social media marketing efforts of luxury brands: Influence on brand equity and consumer behavior. Journal of Business Research, 69(12), 5833–5841. https://doi.org/10.1016/j.jbusres.2016.04.181

- Herawati, N. T. (2015). Kontribusi pembelajaran di perguruan tinggi dan literasi keuangan terhadap perilaku keuangan mahasiswa. Jurnal Pendidikan Dan Pengajaran, 48(3), 60–70. https://doi.org/10.23887/jppundiksha.v48i1-3.6919

- Herdjiono, I., & Damanik, L. A. (2016). Pengaruh financial attitude, financial knowledge, parental income terhadap financial management behavior. Jurnal Manajemen Teori Dan Terapan| Journal of Theory and Applied Management, 9(3), 226–241. http://dx.doi.org/10.20473/jmtt.v9i3.3077

- Ibrahim, M. E., & Alqaydi, F. R. (2013). Financial literacy, personal financial attitude, and forms of personal debt among residents of the UAE. International Journal of Economics and Finance, 5(7), 126–138. http://dx.doi.org/10.5539/ijef.v5n7p126

- Isomidinova, G., Singh, J. S. K., & Singh, K. (2017). Determinants of financial literacy: A quantitative study among young students in Tashkent, Uzbekistan. Electronic Journal of Business & Management, 2(1), 61–75.

- Khair, T., & Ma’ruf, M.. (2020). Pengaruh strategi komunikasi media sosial instagram terhadap brand equity, brand attitude, dan purchase intention. Jurnal Manajemen Komunikasi, 4(2), 1–18. https://doi.org/10.24198/jmk.v4i2.25948

- Kline, R. B. (2016). Principles and practice of structural equation modeling (4th ed.). Guilford Press.

- Kumar, A., Bezawada, R., Rishika, R., Janakiraman, R., & Kannan, P. (2016). From social to sale: The effects of firm-generated content in social media on customer behavior. Journal of Marketing, 80(1), 7–25. https://doi.org/10.1509/jm.14.0249

- Kurnia, S. (2020). Hubungan antara Kontrol Diri dengan Perilaku Phubbing pada Remaja di Jakarta. Jurnal Psikologi: Media Ilmiah Psikologi, 18(1), 58–67.

- Laily, N. (2016). Pengaruh literasi keuangan terhadap perilaku mahasiswa dalam mengelola keuangan. Journal of Accounting and Business Education, 1(4), 1–17. http://dx.doi.org/10.26675/jabe.v1i4.6042

- Lim, X. J., Radzol, A. M., Cheah, J., & Wong, M. (2017). The impact of social media influencers on purchase intention and the mediation effect of customer attitude. Asian Journal of Business Research, 7(2), 19–36. https://doi.org/10.14707/ajbr.170035

- Mugari, I., & Cheng, K.. (2020). The dark side of social media in Zimbabwe: Unpacking the legal framework conundrum. Cogent Social Sciences, 6(1), 1825058. https://doi.org/10.1080/23311886.2020.1825058

- Muralidharan, S., & Men, L. R. (2015). How peer communication and engagement motivations influence social media shopping behavior: Evidence from China and the United States. Cyberpsychology, Behavior, and Social Networking, 18(10), 595–601. https://doi.org/10.1089/cyber.2015.0190

- Navickas, M., Gudaitis, T., & Krajnakova, E. (2014). Influence of financial literacy on management of personal finances in a young household. Business: Theory and Practice, 15(1), 32–40. https://doi.org/10.3846/btp.2014.04

- Ng, E. S., Schweitzer, L., & Lyons, S. T. (2010). New generation, great expectations: A field study of the millennial generation. Journal of Business and Psychology, 25(2), 281–292. https://doi.org/10.1007/s10869-010-9159-4

- Nurhadi, Z. F. (2020). Youtube sebagai media Informasi Kecantikan Generasi Millenial. Commed: Jurnal Komunikasi Dan Media, 4(2), 170–190. https://doi.org/10.33884/commed.v4i2.1585

- OECD-INFE. (2011). Measuring financial literacy: Core Questionnaire in measuring financial literacy: Questionnaire and Guidance notes for conducting an internationally comparable survey of financial literacy.

- Pabedinskaitė, A., & Šliažaitė, V. (2012). Consumers behaviour in e-commerce. Business: Theory and Practice, 13(4), 352–364. https://doi.org/10.3846/btp.2012.37

- Pertiwi, W. K. (2019). Facebook Jadi Medsos Paling Digemari di Indonesia. https://tekno.kompas.com/read/2019/02/05/11080097/facebook-jadi-medsos-paling-digemari-di-indonesia?page=all.

- Potrich, A. C. G., Vieira, K. M., & Mendes-Da-Silva, W. (2016). Development of a financial literacy model for university students. Management Research Review, 39(3), 356–376. https://doi.org/10.1108/MRR-06-2014-0143

- Rajna, A., Ezat, W. S., Al Junid, S., & Moshiri, H. (2011). Financial management attitude and practice among the medical practitioners in public and private medical service in Malaysia. International Journal of Business and Management, 6(8), 105–113. https://doi.org/10.5539/ijbm.v6n8p105

- Rambaree, K., Mousavi, F., Magnusson, P., Willmer, M., & Serpa, S.. (2020). Youth health, gender, and social media: Mauritius as a glocal place. Cogent Social Sciences, 6(1), 1774140. https://doi.org/10.1080/23311886.2020.1774140

- Rasiah, R. R. V. (2014). Transformative higher education teaching and learning: Using social media in a team-based learning environment. Procedia-Social and Behavioral Sciences, 123, 369–379. https://doi.org/10.1016/j.sbspro.2014.01.1435

- Servon, L. J., & Kaestner, R. (2008). Consumer financial literacy and the impact of online banking on the financial behavior of lower‐income bank customers. Journal of Consumer Affairs, 42(2), 271–305. https://doi.org/10.1111/j.1745-6606.2008.00108.x

- Sima, V., Gheorghe, I. G., Subić, J., & Nancu, D. (2020). Influences of the Industry 4.0 revolution on the human capital development and consumer behavior: A systematic review. Sustainability, 12(10), 4035. https://doi.org/10.3390/su12104035

- Sin, S. S., Nor, K. M., & Al-Agaga, A. M. (2012). Factors affecting Malaysian young consumers’ online purchase intention in social media websites. Procedia - Social and Behavioral Sciences, 40, 326–333. https://doi.org/10.1016/j.sbspro.2012.03.195

- Upadana, I. W. Y. A., & Herawati, N. T. (2020). Pengaruh Literasi Keuangan dan Perilaku Keuangan terhadap Keputusan Investasi Mahasiswa. Jurnal Ilmiah Akuntansi Dan Humanika, 10(2), 126–135. http://dx.doi.org/10.23887/jiah.v10i2.25574

- van Rooij, M., Lusardi, A., & Alessie, R. (2011). Financial literacy and stock market participation. Journal of Financial Economics, 101(2), 449–472. https://doi.org/10.1016/j.jfineco.2011.03.006

- Wentzel, K. R. (2017). Peer relationships, motivation, and academic performance at school. In Handbook of competence and motivation: Theory and application (2nd ed., pp. 586–603). The Guilford Press.

- Whidiarso, W. (2012). Pemodelan Persamaan Struktural (SEM) pada Data yang Tidak Normal. http://widhiarso.staff.ugm.ac.id

- Yahaya, R., Zainol, Z., Osman, J. H., Abidin, Z., & Ismail, R. (2019). The effect of financial knowledge and financial attitudes on financial behavior among university students. International Journal of Academic Research in Business and Social Sciences, 9(8), 22–32. http://dx.doi.org/10.6007/IJARBSS/v9-i8/6205

- Yang, S. J. H., & Chen, I. Y. L. (2008). A social network-based system for supporting interactive collaboration in knowledge sharing over peer-to-peer network. International Journal of Human-Computer Studies, 66(1), 36–50. https://doi.org/10.1016/j.ijhcs.2007.08.005

- Yanto, H., Yulianto, A., Sebayang, L. K. B., & Mulyaga, F. (2017). Improving the compliance with accounting standards without public accountability (SAK ETAP) by developing organizational culture: A case of Indonesian SMEs. Journal of Applied Business Research (JABR), 33(5), 929–940. https://doi.org/10.19030/jabr.v33i5.10016

- Yap, R. J. C., Komalasari, F., & Hadiansah, I. (2018). The effect of financial literacy and attitude on financial management behavior and satisfaction. Bisnis & Birokrasi Journal, 23(3), 140–146.

- Yusop, F. D., & Sumari, M. (2013). The use of social media technologies among Malaysian youth. Procedia - Social and Behavioral Sciences, 103, 1204–1209. https://doi.org/10.1016/j.sbspro.2013.10.448

- Yuwono, W., & Juniani, J. (2020). Studi Empiris Manajemen Pengelolaan Tabungan pada Generasi Milenial di Kota Batam. Strategic: Jurnal Pendidikan Manajemen Bisnis, 20(1), 25–32. https://doi.org/10.17509/strategic.v20i1.25396