Abstract

Based mainly on agency theory, this research examines the impacts of tax enforcement and independent audit on the internal control effectiveness and financial reporting quality in Vietnam enterprises. The data analysis is applied to PLS-SEM. The survey method was carried out on a sample of 341 enterprises with headquarters mainly in the three largest cities of Vietnam (Hanoi, Hochiminh and Danang cities) from April to June 2021. The result findings showed that all three factors: independent audit, tax enforcement, and internal control effectiveness, have significant impacts on the financial reporting quality; particularly, tax enforcement has a negative effect while the other two factors have a positive impact. This research’s main contribution is the negative relationship between tax enforcement and financial reporting quality. This result shows the contractionary view with other existing research. The difference in this research’s findings compared to other existing research was explained in theoretical and practical perspectives. In addition, the mediating role of internal control in the relationship between tax enforcement, independent audit and financial reporting quality was confirmed through results. The findings of this research are very important in proposing regulations and policies related to implementing the monitoring mechanism from both inside (internal control system) and outside the enterprise (independent audit, tax enforcement) to increase the quality of financial reports.

PUBLIC INTEREST STATEMENT

Financial reporting is a fundamental source of information in explaining the functioning of the market and has traditionally been associated with the communication carried out by companies to stakeholders and the public on their financial activities. Firms with a higher quality financial reporting will ensure a more comprehensive and practical economic analysis, stock trading volume, and higher equity returns. This study examines the role of monitoring mechanism from both inside and outside the enterprise in assuring the financial reporting quality in enterprises. The results stated that independent audit, tax enforcement, and internal control effectiveness have significant impacts on the financial reporting quality; particularly, tax enforcement has a negative effect while the other two factors have a positive impact. We have proposed regulations and policies related to implementing the monitoring mechanism to increase the quality of financial reports.

1. Introduction

The primary role of financial reporting (FR) is to serve interested parties by providing helpful information for making economic decisions, thus providing reliable and high-quality information about a company’s operations to stakeholders are one of the most important objectives of financial statements (Ikbal Tawfik et al., Citation2022). Besides, FR information also improves the performance of the entity’s activities (Tran et al., Citation2021), and increases investment and decision-making efficiency (Ikbal Tawfik et al., Citation2022). Trombetta (Citation2021) investigates that FR is a fundamental source of information in explaining the functioning of the market and has traditionally been associated with the communication carried out by companies to stakeholders and the public on their financial activities. Therefore, providing the reliable, timely and relevant information is necessary for efficient markets (Mardessi, Citation2022). According to Gelinas et al. (Citation2017), accounting information helps users make beneficial decisions; therefore, investors need to create an efficient market. Qualified FR also reduces the information-gathering costs that financial analysts can face. In other words, firms with a higher quality FR will ensure a more comprehensive and practical economic analysis, stock trading volume, and higher equity returns (Iatridis, Citation2011).

Practically, the public has been paying more attention to FR quality since a plethora of financial scandals (Pucheta‐Martínez et al., Citation2016). Several influential scandals can be mentioned: Ahold in the Netherlands; Parmalat in Italy; Enron, Worldcom, Xerox, Lehman Brothers and Madoff in the US; and Gescartera, Bankia and Pescanova in Spain. Those scandals and their severe consequences have led to a wide range of regulations and recommendations on corporate governance at international and domestic levels to increase information quality to keep the public secure from potential risks in capital markets. FR quality has become a central issue drawing attention to both accounting practitioners and academic research (El-Bannany, Citation2018; Trombetta & Imperatore, Citation2014).

Research into FR quality is usually accompanied by exploring the factors impacting them. Much research on FR quality is accompanied by exploring the factors impacting them and using Agency theory as an important foundation (Pham et al., Citation2021). The Agency theory focuses on addressing the relationship between the principal and the agent (Eisenhardt, Citation1989). The agent is considered to have private information that is not accessible to the principal and this information forms the basis for the agent’s choice of actions. To meet the contractual obligations between the agent and the principal, accounting is considered an appropriate tool for managers (representatives) to use. However, the exploitation of accounting tools for the self-interested behaviors of managers will be limited by implementing an effective monitoring mechanism. Based on the above arguments, research on the relationship between monitoring mechanism implementation and FR quality has always attracted the attention of researchers.

For monitoring from outside the enterprise, the role of the independent audit (IAU) in FR quality has been specifically examined by many studies. Patterson et al. (Citation2019); Zandi et al. (Citation2019); Almaqtari et al. (Citation2020), Hasan et al. (Citation2020), and Mardessi (Citation2022) confirmed that the IAU plays an important role in monitoring, managing and improving FR quality. In contrast, studies by Davidson et al. (Citation2005), Almaqtari et al. (Citation2017), Hashed and Almaqtari (Citation2021) stated that there were no differences in FR quality between enterprises audited by Big 4 (Big 5) and Non-Big. It can be explained that the inconsistency in the role of the IAU on FR quality comes from many reasons, including that previous studies often divided the study sample into two groups: the group of FR audited by Big 4 (Big 5) and the group of FR audited by Non-big 4. Very few studies have been conducted comparing the quality of audited FR with the quality of unaudited FR. So that problem leads to the interesting question is whether there is a quality difference between audited FR and unaudited FR.

Research from Hanlon et al. (Citation2014) examined the monitoring of FR quality from outside the enterprise through tax enforcement (TAE) in the US context. That result showed a positive relationship between TAE and FR quality. However, evidence obtained in a voluntary-tax-compliance country like the US is probably inappropriate for Vietnam, which applies enforced tax compliance. In the enforced tax-compliance mechanism, the relationship between tax authorities and taxpayers is coercive and compulsory. Moreover, the law grants tax authorities considerable power enabling them to implement tax investigations and examine the accounting operation of enterprises. This situation results in compliance with accounting regulations and may not be an optimal solution for handling accounting activities. In several countries that applied enforced tax compliance, such as Vietnam, it is interesting to examine whether the relationship between TAE and FR is significantly positive and similar to other research in the same field.

For monitoring FR quality from inside the enterprise, several studies have particularly focused on the role of the internal control effectiveness (INC) in ensuring FR quality. Recent studies by Ji et al. (Citation2017), Agbenyo et al. (Citation2018), Krishnan et al. (Citation2020), and Ud Din et al. (Citation2021), agreed that establishing an effective internal control system is an important factor in ensuring the quality of FR. However, the above studies only studied the direct impact of INC on FR quality, and there is a lack of examining the mediating role of INC on the relationship between TAE, IAU, and FR quality.

Based on a foundation overview of previous studies, this research argued that although the impact of the monitoring mechanism on FR quality has been mentioned in previous studies through agency theory, research on this relationship is still limited. First, the approach to monitoring factors is often individual; limited studies examine the chain from IAU, TAE, INC, and FR quality. Secondly, the role of the IAU in the FR quality remains controversial; thirdly, there is a lack of studies investigating the mediating role of INC in the relationship between IAU, TAE, and FR quality.

There are three main objectives in this study. The first is to examine the relationship between IAU, TAE, INC, and FR quality. Secondly, this study will investigate the mediating roles of INC in the relationship between IAU, TAE and FR quality. The audit’s impact on FR quality is evaluated by comparing FR quality in audited firms and unaudited enterprises. The survey method was carried out on a sample of 341 enterprises with headquarters mainly in the three largest cities of Vietnam (Hanoi, Hochiminh city, and Danang city). This research contributes to the extant literature on the FR quality in several ways. First, to our best knowledge, this study is the first to examine the chain from TAE, IAU, INC and FR quality. Second, this paper explains INC’s mediating role in the relationship between the IAU, TAE, and FR quality. Third, it explains the different relationships between TAE and FR quality on tax compliance mechanisms. Fourth, this research proposes tax and IAU policies and internal control as mechanisms for improving FR quality in an Asian transition market.

2. Literature review

2.1. FR quality

Until now, there is no globally agreed concept providing a comprehensive definition of the quality of FR is an established requirement (Herath & Albarqi, Citation2017). The FR quality is the accuracy at which the FR provides information regarding an entity’s operation, primarily cash flow, to inform its investors (Biddle et al., Citation2009). Koo et al. (Citation2017) believe that FR quality is defined as the informativeness of the FR about the basic economic situation of the company, which can affect the dividend policy of the entity. FR quality is also conceptualized through its characteristics. IASB (Citation2010), IASB (Citation2018) determined that the quality of FR was understood as the attribute that makes the information presented in the financial statements applicable to the users of the information. Accordingly, two fundamental qualitative characteristics are identified: relevance and faithful representation. The enhancing characteristics are comparability, verifiability, timeliness, and understandability. Thus, FR quality is a high-order construct including three second-order constructs: relevance, faithful representation, and enhancing qualitative.

The qualitative characteristics published by FASB and IASB are considered as the primary premise for FR quality direct measurement. Jonas and Blanchet (Citation2000) developed an FR quality scale consisting of five components (relevance, reliability, comparability, consistency, and clarity) by following the qualitative characteristics of FASB. Relevance includes three second-order constructs (predictive value, feedback value, and timeliness). Reliability comprises four first-order constructs (verifiability, completeness, substance, neutrality). Comparability, consistency, and clarity are first-order constructs. Although Jonas and Blanchet (Citation2000) stopped at scale construction, it is considered one of the seminal studies on setting up the FR quality scale based on qualitative characteristics and inherited by later studies. Adapted from Jonas & Blanchet’s study, Van Beest et al. (Citation2009) developed an FR quality scale composed of five components: relevance, faithful representation, understandability, comparability, and timeliness. Based on the existing literature on assessing the usefulness of FR quality by Jonas and Blanchet (Citation2000), Van Beest et al. (Citation2009), and experienced Bulgarian experts’ opinions, Tsoncheva (Citation2014) has proposed an FR scale that includes four components: relevance, faithful representation, understandability, and comparability. Pham et al. (Citation2021) measured FR quality in enterprises in Vietnam. Based on the reference of the FR quality scale from Van Beest et al. (Citation2009) and consultation with experts, the proposed FR quality scale is a third-order construct, including three second-order constructs (relevance, faithful representation, and enhancing quality) measured by 28 items.

Based on previous studies, we concluded that measuring FR quality based on qualitative characteristics required by FASB, IASB was the research direction that attracted interest in recent years with pioneering studies of Jonas and Blanchet (Citation2000) and Van Beest et al. (Citation2009).

2.2. INC

The internal control structure and effectiveness are presented in the COSO framework. In 2013, the COSO Framework was designed to assess the effectiveness of the internal control system in achieving objectives as determined by management. It also lists three categories of objectives: Operations Objectives, Reporting Objectives, Compliance Objectives. Judging INC through the degree of internal control required to meet the three above objectives of COSO is one of the critical foundations for the concept of INC. Based on the COSO framework, Myllymäki and Jokipii (Citation2011) defined INC as providing a reasonable guarantee that a company was using its resources effectively and complying with the rules and regulations that the financial information on it was accurate and reliable. Mulyani and Arum (Citation2016) believe that the INC is the ability of the Board of Managers to achieve company goals, understand the company’s business operations, and comply with laws and regulations.

Previous literature shows that INC measurements are often conducted through examining determinants of weaknesses in internal control for companies that disclosed material liabilities in internal control over FR under Sections 302 and 404 of the Sarbanes-Oxley Act (SOX; Altamuro & Beatty, Citation2010; Morris, Citation2011; Rubino & Vitolla, Citation2014). Besides, INC measurement is based on the awareness of business management about the achieving levels of internal control goals following COSO’s view is more and more focused with researches of Myllymäki and Jokipii (Citation2011), Länsiluoto et al. (Citation2016), and Thuần and Cường (Citation2020). Based on these points of view, the INC scale of their research is the second-order construct including three first-order constructs: effectiveness and efficiency of operations; reliability of FR; compliance with applicable laws and regulations.

2.3. TAE

TAE is defined as the utilization or application of all those relevant laws that will aid and assist the taxman in performing the duties; laws not necessarily relating to taxation but apply to the enforcement of tax laws (Tanko, Citation2015). The measure of tax authority enforcement is not easily obtained (Desai et al., Citation2007). Hanlon et al. (Citation2014) highlighted that TAE is the managers’ perception of the probability of an internal revenue service audit (IRS audit).

2.4. INC and FR quality

Based on the regulations of internal control influence on financial information and the foundation of agency theory, previous studies have suggested that ensuring the effective operation of internal control at the firm will establish a monitoring mechanism within firms, reducing the problem of asymmetric information and thereby contributing to the increase of FR quality. Methods to determine the relationship between INC and FR quality from previous studies are diversified, such as analysis of the connection between internal control weakness disclosure and FR quality, comparison of FR quality between the group of firms that are regulated and not regulated by internal control; analysis the direct impact of INC on FR quality

For the analysis of the connection between internal control weakness disclosure and FR quality, several studies have shown that firms that do not guarantee the effectiveness of internal control have more significant information uncertainty (Beneish et al., Citation2008), provide low-quality FR (Doyle et al., Citation2007; Lari Dashtbayaz et al., Citation2019), and the entity’s FR could not achieve confidence in its accuracy (Elbannan, Citation2009). Clinton et al. (Citation2014) consistently investigated the effects of ineffective internal control and required reporting of material weaknesses in internal control on financial forecasting. That research found that analysts’ forecast accuracy lacks correctness, and forecast dispersion is more significant for companies with less effective internal controls than companies with efficient internal controls. For the comparison of FR quality, Oh et al. (Citation2014) investigated the relationship between internal control over FR regulation in Korean Listed Companies Association and showed that the strictness of IC regulation deters the managers’ opportunistic behaviors and limits discretionary accruals, thereby helping to ensure high-quality FR; Krishnan et al. (Citation2020) studied the impact of applying internal control regulations introduced by SOX on the FR quality of companies in the United States. That research showed that compared to the PRESOX period, the quality of FR of firms is significantly improved when using SOX Sections 302 and 404a.

For the analysis the direct impact of INC on FR quality, many studies believed that INC is an important factor in determining the FR quality (Phornlaphatrachakorn, Citation2019); poor quality of internal control is associated with an increased incidence of fraud (Ud Din et al., Citation2021; Donelson et al., Citation2017; Ji et al., Citation2017). Therefore, understanding the determinants of INC is significant in improving FR quality. Moreover, Agbenyo et al. (Citation2018) argues that internal control plays an important role and positively impacts FR quality, especially when all stakeholders comply with the objectives and mandates of the firms. To sum up, this research recommends that compliance with the objectives of the internal control policy must set the goal of ensuring the FR quality. A review of previous studies shows that the positive impact of INC on FR quality has always been confirmed through many research directions. From the above literature review, we proposed the research hypothesis:

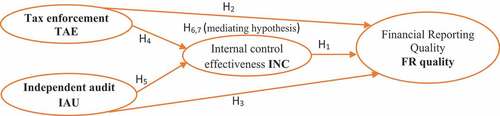

H1: INC has a positive effect on FR quality

2.5. TAE and FR quality

Ewert and Wagenhofer (Citation2019) showed that a common assumption in policymaking and empirical research is that greater enforcement is always expected because it improves the quality of FR. Enforcement is an important element of the institutional framework to ensure the quality of FR of companies. The relationship between TAE and FR quality has also received the attention of some FR quality-related studies. Studies from Desai and Dharmapala (Citation2009) suggested that tax avoidance behavior will increase earnings management. In addition, an increase in TAE by tax authority will reduce tax avoidance behavior and contribute to an increase in FR quality. Research by Hanlon et al. (Citation2014) examined the relationship between TAE and FR quality. The authors argued that when collecting taxes on corporate profits, the government is considered the largest minority shareholder in most businesses. Therefore, like other shareholders, the government is interested in accurately reporting (taxable) income and preventing insiders from extracting money from the company for their self-interest. Hanlon et al. (Citation2014) found evidence that the higher the TAE, the more warranted the FR quality.

Previous research has studied the relationship between TAE and FR quality in the context of voluntary tax compliance in countries like the United States. Meanwhile, in several countries that follow the enforced tax compliance model, like Vietnam, the relationship between tax authority and taxpayers is often inequitable. Therefore, the question of whether there is a positive relationship between TAE and FR in the countries following the enforced tax compliance model is worth considering. More importantly, research to examine the effect of TAE to FR quality in an enforced tax compliance model country like Vietnam, would provide compelling evidence for this question. Therefore, we proposed the research hypothesis:

H2: TAE has a positive effect on FR quality

2.6. IAU and FR quality

Based on the agency theory, many previous studies have suggested that the enforcement of the monitoring mechanism from firms’ external, in which the role of the IAU is particularly focused, is considered as an effective control mechanism for the organization. Monitoring the behavior of regulators as well as ensuring the honesty and reliability of FR, enhances investor protection and improves their confidence (Hasan et al., Citation2020). When considering the impact of IAU on FR quality, most of the previous studies were done on the basis of dividing the sample into two groups (group of FR audited by Big 5, Big 4 and group of FR audited by Non big) and compare the quality of FR between the two groups. Bell and Carcello (Citation2000) indicated that auditors play a crucial role in FR fraud detection and audit is a vital controller that monitors firms’ managers with the separation between ownership and management rights. IAU reduces the benefit conflicts between managers and owners (Jensen & Meckling, Citation1976; Xiao et al., Citation2004). Archambault and Archambault (Citation2003) found that disclosure in firms audited by the Big 6 is higher than those audited by Non big 6. Research from Hạnh (Citation2015) showed that the information transparency of Big 4 audited FR was greater than that in FR audited by Non big 4, and IAU positively impacted FR transparency. Zandi et al. (Citation2019) concluded that Big 4 auditors negatively impact firms’ profit management behavior due to their less involved in profit management activities than those audited by Non big 4. More briefly, the FR audited by Big 4 have better quality compare to Non big 4. Nevertheless, Patterson et al. (Citation2019); Hasan et al. (Citation2020) argued that the FR audited by the Big 4 reflects the company’s concerted efforts to create an FR that ensures higher quality and thus reduces errors in the presentation of accounting information; independent audit plays an important role in monitoring the management and enhancement of the FR quality (Almaqtari et al., Citation2020; Citation2021); the Big 4 allows companies to detect losses earlier and thus reduce the level of earnings manipulation (Mardessi, Citation2022); the FR creditability is improved by external auditors—who perform audits of financial statements by applicable ethical and auditing standards. In order to achieve these objectives, external auditors need to have particular schemes and adhere to professionalism, independence, and objectivity (Khalil, Citation2022).

However, some studies show that IAU’s role in FR quality has unclear results. Research by Davidson et al. (Citation2005) showed no difference between the quality of FR audited by the Big 5 and Non-big 5. Consistently, Almaqtari et al. (Citation2017) research showed no difference in quality between FR audited by the Big 4 and Non-big 4. Based on the above results, the authors have recommended that corporate governance’s role be revised to increase the role of FR quality and limit earnings management. Research of Hashed and Almaqtari (Citation2021) also showed no difference in FR quality between companies audited by the Big 4 and Non-Big 4. Hence, this research also believes that to increase FR quality, it is necessary to apply more regulations and information disclosure requirements and to establish a FR supervisory board.

A review of previous studies shows that the impact of IAU on FR quality has not been consistent. Besides, the prior literature on the link between IAU and FR quality is primarily conducted in listed firms where audited FR is required. Hence, FR quality is compared between firms audited by Big-4 and those with the non-Big-4 audits. Few works compare the FR quality of audited firms and that of non-audited firms. From the above literature review, we proposed the research hypothesis:

H3: IAU has a positive effect on FR quality

2.7. TAE and INC

Hanlon et al. (Citation2014) suggested that TAE is the probability of an IRS audit by enterprise tax authorities. Although the tax authorities are not responsible for detecting weaknesses in internal control at the unit, tax authorities also assess the unit’s tax law enforcement through the implementation of tax inspection; help detect errors related to compliance with tax regulations and tax accounting; propose recommendations to help the unit make timely adjustments to these errors to ensure good tax law enforcement. This allows businesses to discover internal control weaknesses. Vanchukhina et al. (Citation2020) suggested that the relationship between tax inspections and INC is explained by the concept of tax administration based on enhanced information interaction between tax authorities and taxpayers. Accordingly, taxpayers must provide more detailed information about accounting and tax-related operations to tax authorities. This has highlighted the role of internal control, which is considered an effective support tool for taxing monitoring from tax authorities. Specifically, suppose the entity’s INC is secured. In that case, the tax authority will reduce the administrative burden on the taxpayer and may decide not to conduct some form of a complex and expensive tax audit. This shows that tax supervision from tax authorities has required businesses to focus on improving the effectiveness of the internal control system at their units to provide quality assurance information. Based on the above, we believe that the higher the frequency of tax inspection, the more secure the INC at the unit. On that basis, we propose H4:

H4: TAE has a positive effect on INC

2.8. IAU and INC

When performing the audit, the auditor must understand the client is in control to plan and determine the tests’ nature, timing, and extent. Although it is not the auditor’s responsibility to detect all internal control weaknesses, the approach based on the internal control system helps the auditor detect quite a few internal control deficiencies. International Standard 265 required the auditor to notify management of these deficiencies to help the entity improve the quality of internal control. Notifying internal control deficiencies to the Board of Directors is not a new topic; since August 1977, AICPA has made this requirement for Auditing firms in the United States.

Quite a few previous studies have demonstrated that IAU improves the effectiveness and quality of internal control (Chalmers et al., Citation2019). With the independent and objective assessment of the auditors, the weaknesses of the internal control will be detected and communicated to the Board of Directors so that they can make adjustments to improve the effectiveness and quality of internal control (Chen et al., Citation2016; Haislip et al., Citation2016). Chen et al. (Citation2016) found that auditing firms with many years of cooperation with clients will have a lot of knowledge about the client’s activities. This will help the IAU evaluate internal control in detail, thereby helping the client reduce internal control weaknesses. Haislip et al. (Citation2016) concluded that auditors’ in-depth IT knowledge helps clients minimize internal control weaknesses in the information technology environment. From the above literature review, we proposed the research hypothesis:

H5: IAU has a positive effect on INC

2.9. The mediating role of INC

The INC role for FR has drawn substantial attention from lawmakers, legislators, and regulators since a series of financial affairs such as Enron and Worldcom. Most recent legal regulations have emphasized the link between the INC and reducing the risk of information on the FR. Section 404 SOX requires US-listed firms to evaluate and disclose the effect of internal control on FR (at the fiscal year-end) associated with IAU reports regarding the influence of internal control performance on FR. In Europe, Directive 2006/46/EC requires annual disclosure of corporate governance, including the description of critical attributes of the systems of risk management and IC concerning the financial information establishment process from listed companies. Vietnam Accounting Law 2015 stipulates that an accounting entity must establish an internal control system to ensure its assets are protected from improper and inefficient use. Transactions are approved according to authority and are fully documented as the basis for the establishment and presentation of FR honestly and reasonably. That law also requires transactions to be approved according to source and are fully recorded as the basis for the establishment and presentation of FR faithfully and fairly. The abovementioned regulations indicate that organizing and operating an effective internal control system is a concern for most countries today. Internal controls are seen as effective tools for minimizing the risk of fraud, ensuring compliance with all laws and regulations, and maintaining the integrity of information. Internal control systems help organizations to achieve their objectives by providing reasonable assurance regarding the reliability of FR and the effectiveness and efficiency of operations. Studies on the role of IAU to FRQ have shown that independent audit plays a significant role in detecting financial fraud (Bell & Carcello, Citation2000) and identifying errors in the presentation of accounting information (Almaqtari et al., Citation2020; Citation2021). Auditors will report fraud, errors and weaknesses in internal controls of audited firms to ensure qualified internal control performance, aiming to increase FR quality. However, these recommendations are only effective when the Board of Directors (the oversight factor of the internal control system) absorbs these recommendations to improve the internal control system, especially the internal control in preparing and presenting financial statements. Therefore, when considering the positive impact of IAU on INC (hypothesis H5) and INC on FR quality (H1), this research expects that an effective internal control system will help increase the positive role of IAU on FRQ. Similarly, when considering the positive impact of TAE on INC (hypothesis H4) and of INC on FR quality (H1), this research also expects that an effective internal control system will help increase the role of TAE on FRQ. On that basis, hypotheses H6 and H7 are proposed:

H6: INC mediates the relationship between TAE and FR quality

H7: INC mediates the relationship between IAU and FR quality

The research proposal is presented in Figure .

Figure 1. Research model.

3. Research methods

3.1. Sampling and data collection

The unit of analysis for this research is based on the firm level. This research used convenience sampling for two main reasons: first, even though convenience sampling lacks generalization in results but this sampling method is considered useful in this research because respondents can be reached based on proximity or ease of accessibility (J. F. J. F. Hair et al., Citation2014); Secondly, because of the sensitively of the accounting information, this sampling method helps us to reach firms that willing to provide information. The survey method was conducted through a directly distributed questionnaire (face-to-face) and via email survey. The survey respondents in this research are carefully selected and have top management levels in organizations. They are CFOs, chief accountants, and senior accountants with three years of experience working in the enterprise. A representative respondent was selected in each firm to answer the survey questionnaire. Those respondents are considered to have in-depth knowledge of FR quality. The data collection tool was a questionnaire with a 5 points Likert scale (except for two directly measured variables, listed as timeliness quality characteristics and TAE; and one Dummy variable, IAU).

The survey period was from April to June 2021. We sent a total of 650 questionnaires and received 425 responses with a response rate of 65.4%. The response rate was high because we selected the survey respondents attending professional accounting seminars to update their accounting, tax, and finance knowledge. We have also participated in these seminars as a lecturer or reporters. The received questionnaires were screened based on comparing the respondents’ job positions and working experience to meet the research objectives. After the screening process, we had 341 qualified surveys considered eligible for the analysis. This sample size is considered adequate for the partial least squares—structural equation modeling method (PLS-SEM). The rejected samples were mainly because of lacking experience in accounting industries or not meeting the job position’s research requirements.

Based on the 341 qualified samples, the research figured out general sampling statistics as listed in Table . The number of enterprises based in Hochiminh City accounts for 47.21%, Hanoi City is 36.6%, and Danang City is 16.13%. These sampling characteristics reflected the reality of the dispersion of enterprises by provinces and cities in Vietnam. Accordingly, Hochiminh City (Southern) is considered the most important economic center, where most businesses operate. Next is Hanoi city (Northern region), the political center, where the number of companies is ranked after Hochiminh city. Danang city (Central area) is the 4th largest city in Vietnam.

Table 1. Sampling characteristics

Among 341 samples, 50.15% of enterprises have performed FR audits by IAU. This data also reflects the reality in Vietnam when the State regulation only mandates FR audited by IAU for particular objects (foreign-invested enterprises; public companies, state-owned enterprises, …). Survey respondents’ percentages listed as Chief accountants (53.08%), CFO (14.96%), and accountants (31.96%), and all have three or more years of experience working in the accounting area.

3.2. The research scales

The control self-assessment method invited respondents’ opinions on a numerical scale with a Likert scale anchored by strongly disagree (1) and strongly agree (5). The survey questionnaire was set up to collect data to measure research model factors.

FR quality: Base on the IASB (Citation2018) Conceptual Framework, FR quality is conceptualized as the qualitative characteristics that make the information presented in the FR useful to the users for making decisions (Pham et al., Citation2021). According to IASB (Citation2018), two fundamental qualitative characteristics are relevance (includes predictive value and confirmatory value) and faithful representation (includes complete, neutral and Free from error), the enhancing characteristics are comparability, verifiability, timeliness, and understandability. This research adapted the FR quality scale from (Pham et al. (Citation2021). The FR quality variable is a third-order construct, measured by 28 items. The scale structure and measurement method are illustrated in Table .

Table 2. Scale structure and scale measurement in FR quality

INC scale: Based on the COSO framework, INC is conceptualized as the level of internal control required to meet three objectives, including efficiency and effectiveness of activities, reliability of FR, and compliance with laws and regulations (Länsiluoto et al., Citation2016). In this research, this scale is adapted from research by Länsiluoto et al. (Citation2016), and labeled as INC, including three components: efficiency and effectiveness of activities (EFF1 ➔ EFF4), reliability of FR (REI1 ➔ REI4), and compliance with laws and regulations (LAW1 ➔ LAW4). Länsiluoto et al. (Citation2016) surveyed CFO respondents, so we slightly modified the title to suit the research objectives, CFO, Chief accountant, and accountant.

TAE scale: TAE is defined as using or applying all relevant laws to guide and assist taxpayers in carrying out their duties (Tanko, Citation2015). This scale was developed based on the initiatives of Hanlon et al. (Citation2014) and the measurements via the probability of an IRS audit and labeled as TAE. However, it is different from Hanlon et al. (Citation2014), which is based on the managers’ perception of the probability of an audit; this study is mainly about the actual occurrence of a tax audit. The survey defined the times of implementing basic tax audits in 5 years (2016–2020). The probability of a tax audit will be recognized by the times of implementing tax audit in this period divided into 5. Hence, the value of TAE is from 0 to 1.

IAU scale: IAU is conceptualized as FR is audited by audit firms (Pham et al., Citation2021) and labeled as IAU. Adapted from the research from Pham et al. (Citation2021), a dummy variable takes the value one if FR is audited; otherwise, its value is 0.

Table presents the sources of the scales used for this research.

Table 3. Sources of the scales

4. The research’s findings

4.1. Examining the quality of the outer loading and testing methods

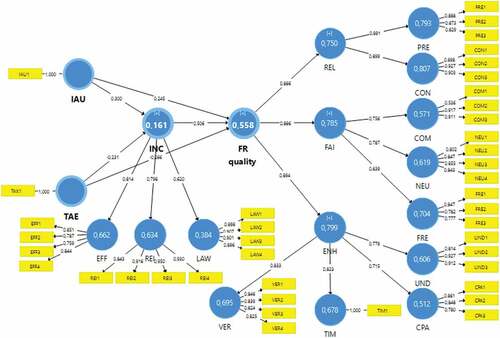

The quality of the observed variables is considered by the external loading coefficient of the observed variables. Hulland (Citation1999) suggested that the value of this coefficient should be greater than the minimum threshold of 0.5 to ensure quality. On that basis, we removed the observable COM4 (outer loading equals 0.282). After removing COM4, the external loadings of the remaining observed variables were all greater than 0.5, and all are statistically significant (corresponding P values are equal to 0), as listed in Table . Besides, this study’s FR quality variable concept is quadratic (including nine first-order components), and INC is a quadratic concept (including three first-order parts). Therefore, the author implements the first-order components when performing the testing steps, according to Hair et al. (Citation2018).

Table 4. Scale items and latent variable evaluation

4.2. Scale reliability

The research evaluated the scale’s reliability on SMART—PLS through three indicators: Cronbach’s Alpha, RhoA and Composite Reliability (CR). Thọ (Citation2011) said that the scale ensures reliability when Cronbach’s Alpha ranges from 0.6 to 0.95. J. Hair et al. (Citation2010) believed that CR needs to be at the threshold of 0.7 or higher. The evaluation results in Table showed that all scales’ Cronbach’s Alpha values are exceptional, ranging from 0.727 to 0.931. Likewise, the RhoA value ranges from 0.738 to 0.931, and the CR price also varies from 0.844 to 0.945. In addition, because the concepts of timeliness (TIM), TAE and IAU are directly measured by 1 item, the values of all three indicators are equal to 1. The results showed that the scales are all ensured in high reliability.

4.3. Convergent validity

Hair et al. (Citation2010) suggested that the scale ensures convergent validity when the scale’s Average Variance Extracted (AVE) reaches a value of 0.5 or more. Table shows the AVE ranging from 0.644 to 0.829. The result showed that the scales ensure Convergent validity.

4.4. Discriminant validity

The HTMT index and the square root index of the AVE were used. Henseler et al. (Citation2015) said the scale is guaranteed when the HTMT index is below 0.9. Fornell and Larcker (Citation1981) recommend that discriminability is insured when the square root of the AVE for each latent variable is higher than all correlations between the latent variables. Table showed the HTMT coefficient has the highest value of 0.832. Table showed that the square root of the AVE of each latent variable (the number on the diagonal) was more significant than its correlation coefficient with any other research concept in the model. In addition, the highest value of the correlation coefficients between latent variables (the number below the diagonal) is 0.542 and lower than the lowest value of CR (equal to 0.843). The result showed that the research model’s scale ensures discriminant validity.

Table 5. Heterotrait-monotrait ratio (HTMT)

Table 6. Fornell-larcker criterion

The CFA figure is presented in Figure .

Figure 2. The CFA figure.

4.5. Multicollinearity in the structural model

The research used the VIF value to check this phenomenon. Thọ (Citation2011) suggested that if VIF was more significant than 2, the study needed to interpret the regression weights. Table showed that the VIF value of each relationship arising between latent variables in the model has the highest value of 1.192 and is much lower than the threshold value suggested by Thọ (Citation2011). This result shows that there is no multicollinearity in this study.

Table 7. Inner VIF Values

4.6. Results

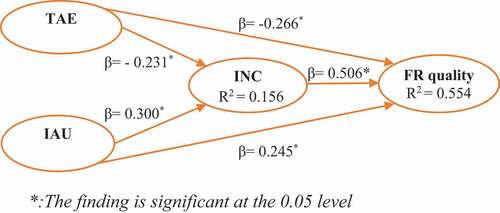

The hypotheses were tested using Smart- PLS3 software. To provide evidence for testing the research hypotheses, the author has evaluated the standardized impact coefficient and the level of statistical significance corresponding to each research hypothesis. Besides, to assess the model’s fit, the research also evaluates adjusted R2 values for two dependent variables of the research model, FR quality and INC. Basic bootstrapping was used with 500 bootstrap subsamples. The test results are presented in Table and Figure , including t-values for PLS paths in the model; adjusted R2 values of the two dependent variables: INC and FR quality. The results of data analysis in Table showed that the adjusted R2 coefficient of all dependent variables was above the minimum threshold of 0.1 (specifically INC = 0.156 and FR quality = 0.554). The results show that the proposed research model has met the requirements of the structural and measurement model. Based on the above results, we conclude that three factors INC, TAE and IAU explain 55.4% of the variation of FR quality and two factors TAE and IAU explain 15.6% of the interpretation of INC.

Figure 3. Presents the simple structural modeling for the results.

Table 8. Partial least squares results

5. Discussion and conclusion

5.1. H1 and H3

According to hypotheses H1 and H3, INC and IAU have a significant positive effect on FR quality with a statistical significance level of 0.05 (INC: β = 0.506, p-value = 0; IAU: β = 0.245, p-value = 0), hence, H1 and H3 are supported. The positive impact of INC on FR quality is considered similar to previous studies of Doyle et al. (Citation2007), Beneish et al. (Citation2008), Elbannan (Citation2009), Oh et al. (Citation2014), Donelson et al. (Citation2017), Ji et al. (Citation2017), and Phornlaphatrachakorn (Citation2019), and Lari Dashtbayaz et al. (Citation2019), and Krishnan et al. (Citation2020), and Ud Din et al. (Citation2021). Therefore, internal control with effectiveness will contribute to the control of management’s activities, help prevent and detect mistakes, and help the organization achieve the operational, reporting and compliance objectives. Similarly, regarding the positive impact of the IAU on FR quality, along with previous research by Zandi et al. (Citation2019), Patterson et al. (Citation2019), and Hasan et al. (Citation2020); Almaqtari et al. (Citation2020); Almaqtari et al. (Citation2021), Hashed and Almaqtari (Citation2021), Mardessi (Citation2022), and Khalil (Citation2022), this research contributes to the confirmation of the IAU’s monitoring role for the quality assurance of FR at the enterprises. Based on the results of the research, it is recommended that government agencies need to complete the regulations to ensure quality from the audit firms; namely: they need to continue to review, amend, and stronger handling policies to prohibit violations that affect the quality of the audit of both the audit firms as well as the firms being audited.

The important role of the INC and IAU in ensuring FR quality is explained by agency theory. Lari Dashtbayaz et al. (Citation2019) suggested that one of the most important factors in enhancing FR quality is to reduce information asymmetry through increasing audit quality and effectiveness of internal control. Besides, the decision to increase monitoring costs from the principal, including monitoring from the outside (IAU) and inside the enterprise (INC), will help reduce the behavior of earnings management and increase FR quality (Ud Din et al., Citation2021).

5.2. H5

IAU have a significant positive effect on INC with a statistical significance level of 0.05 (β = 0.300, p-value = 0), hence, H5 is supported. This finding is aligned with Chen et al. (Citation2016), Haislip et al. (Citation2016), and Chalmers et al. (Citation2019). This result implies that with the evaluation and understanding of the activities as well as the management characteristics of the stakeholders, with the experience and ability, the auditors are able to detect the weaknesses internal control of the audited firms. Accordingly, IAU plays an important role in detecting shortcomings, thereby contributing to the improvement and ensuring the effectiveness of internal control.

5.3. H2 and H4

Differences from hypothesis development proposed that TAE has a positive significant effect on FR quality (H2) and INC (H4); the hypotheses H2 and H4 are rejected because β equals −0.226 and −0.231, respectively. The research results show that TAE has a negative effect on FR quality (with β equal to −0.266); similarly, TAE has a negative effect on INC (with β similar to −0.231). This result is completely different from previous studies by Desai and Dharmapala (Citation2009), Hanlon et al. (Citation2014), and Vanchukhina et al. (Citation2020). The negative effect of TAE on FR quality and INC is considered the main contribution of this study and can be explained by many reasons, namely:

Considering the practical perspectives on the relationship between tax authorities and businesses in Vietnam: the current tax law empowers tax authorities to inspect and judge compliance with accounting regulations on the accuracy and truthfulness of accounting data when conducting tax examinations at businesses. In addition, tax is still considered the primary user of FR in Vietnam in terms of practices and enterprises’ perceptions. Although the income tax accounting standard was issued by the Ministry of Finance of Vietnam in 2006, from the accounting perspective, firms should follow the accounting standards and regimes instead of relying on tax regulations in practice in Vietnam (MOF, Citation2005). Most businesses still need a long time to adapt and become familiar with the Accounting Standard and this is explained for many reasons: first, the concept of tax and accounting homogeneity has existed for a long time in the process of establishment and development of accounting in Vietnam. Secondly, the firms will take longer to explain to the tax authorities the deviations between tax and accounting, including the recognition of Deferred Income Tax. Besides, when performing tax audits, some tax officials often interfere in the accounting records and presentation of information on the FR of enterprises to monitor tax avoidance. Tax authorities often apply tax regulations rather than asking enterprises to comply with standards and policies of accounting when they implement accounting inspections at enterprises. Consequently, pressure from tax authorities can be considered one of the biggest obstacles preventing accounting from adequately adapting to accounting standards and regulations. Therefore, to avoid inconvenience, some businesses have chosen to make accounting under the tax regulations depreciation, provisioning, recording expenses, revenue, …) instead of according to the accounting standards and policies. This phenomenon seriously affected the FR quality.

Considering the aspect of the main users of FR in Vietnam: tax authorities are considered one of the main users of FR in Vietnam. Depending on the type of business, the current Vietnamese accounting system requires businesses to submit FR to the tax authorities annually or quarterly and annually (MOF, Citation2014). Due to the close relationship between accounting and tax for a long time (from the formation of Vietnamese accounting until the deferred income tax Vietnamese accounting standard in 2006), most businesses still consider tax authority as an FR “s main user. The receiving and absorbing tax authorities” contributions, the enterprise’s internal control system, considered to include activities, measures, plans, views, rules, policies, and efforts of the unit, is often aimed at facilitating tax declarations. Therefore, the operation of internal control at the firms’ level is also partly influenced by the recommendations of the tax authorities after-tax inspection. This action is also the cause of the negative impact of TAE on INC.

Considering based on contextual differences between studies: Desai and Dharmapala (Citation2009), Hanlon et al. (Citation2014) studied the relationship between TAE and FR quality in countries that apply the voluntary tax compliance model like the United States. However, this study was conducted for businesses in Vietnam, a country that follows the enforced tax compliance model, where the tax authority is considered a powerful authority over businesses. In order to avoid confrontation with tax authorities and reduce hassles in explaining the differences between tax and accounting, some businesses often choose to follow the recommendations of the tax authorities, including correcting their accounting books and FR. The results of this study are essential evidence for the negative relationship between TAE and FR quality in countries that follow the enforced tax compliance model like Vietnam.

Beside, the negative impact of TAE on FR quality and INC can be explained by theory of planned behavior (TPB). TPB is an extension of the theory of reasoned action from Madden et al. (Citation1992). Several studies in the accounting literature adapted the Theory of Planned Behavior to explain the tendency of business managers to commit fraud in FR choices (Carpenter & Reimers, Citation2005). Carpenter and Reimers (Citation2005) demonstrated that the TPB predicts whether managers’ choices regarding corporate governance are ethical or immoral. According to the TPB, intentions are the key to understanding behavior. Three dimensions are: (1) attitudes toward the activity, (2) societal norms, and (3) perceived control over the conduct influences intentions. TPB is founded on the central idea that humans make systematic use of information to make rational behavioral decisions, and it connects people’s behavioral intents to perform with their actual conduct (Thoradeniya et al., Citation2015). According to Thoradeniya et al. (Citation2015), firm accountants face increasing pressure from various stakeholder groups, including shareholders, investors, employees, and the government. In response to that pressure, firms might choose to report accounting statements based on Vietnam accounting standards. However, in the process of working with the Vietnam tax authority, firms might have pressure to adjust the accounting data in the direction of referring to the tax regulations (accounting according to the provisions of the tax law). There are several reasons for adjusting accounting data: avoid quarrels with tax authorities because this will be detrimental to the firms when making tax finalization for the next time; the firms can save time to resolve the program with the tax authority when recognizing the withheld tax (especially in the case where the accounting profit is higher than the taxable profit), which might help firms less exposed to risks in tax declaration aspect. Hence, accountants need to be rational (by comparing the benefits and consequences of financial accounting reports) and make decisions that meet social responsibility and accountability.

5.4. H6 and H7

The existence of a mediating effect in this research model is explained by Hair Jr et al. (Citation2021). Accordingly, the necessary condition for confirming mediating results was that the direct relevant impact must be statistically significant. For the hypothesis that INC acted as a mediating variable between TAE and FR quality, the condition was that the immediate effect of TAE on INC and the direct impact of INC on FR quality must be statistically significant. Based on the above results, the study concludes that INC acts as a mediator and positively influences the relationship between IAU and FR quality with a statistical significance of 5% and β of 0.152. Similarly, INC also acts as an intermediate variable between TAE and FR quality with a statistical significance of 0.05. However, the negative value of β (equal to −0.117) indicates that INC plays a negative role in the relationship between TAE and FR quality. In other words, although TAE has a negative impact on INC, ensuring the effectiveness of internal control at the unit will minimize the negative impact of TAE on FR quality. The mediating role of the INC is considered one of the key findings of this study and is explained by the following reasons:

When considering the relationship between audit and FR quality, enterprises should take advantage of the provision of an effective internal control system to achieve short- and long-term goals, maintain good financial standing and profits, deal with unprecedented incidents, and respond properly to shareholders (Lari Dashtbayaz et al., Citation2019; Root, Citation2000). Therefore, effective internal control will increase the positive impact of audit on FR quality.

Based on agency theory, recent studies by Lari Dashtbayaz et al. (Citation2019), Ud Din et al. (Citation2021), Ikbal Tawfik et al. (Citation2022), and Alsmady (Citation2022) all advocate the establishment of a monitoring mechanism in enterprises with special emphasis on the role of internal control. These activities will help to strengthen the supervision of the agent’s activities, ensure proper observance of laws and regulations, helping to increase FR quality. Internal control to ensure effectiveness will require enterprises to perform accounting works based on compliance with regulations and accounting standards rather than on tax laws due to side effects of TAE. In other words, effective internal control will reduce the negative impact of TAE on FR quality.

6. Implications

This research contributes knowledge on both theory and practical perspectives, in confirming the role of the monitoring mechanism from inside and outside the firms to ensure FR quality. First, the study’s most important finding was shown in the evidence of a negative relationship between TAE and FR quality. One possible explanation for the results differs from previous studies depending on the research context. Specifically, the previous research of Desai and Dharmapala (Citation2009); Hanlon et al. (Citation2014) was conducted in the US—which has significant shifts in the tax administration model, from the enforced tax compliance model to the voluntary tax compliance model, showing the affects how handling and behavior of tax officers when performing tax inspection work at enterprises. In countries that implement the voluntary tax compliance model, there is mutual respect between tax authorities and taxpayers; Tax authorities act as service providers and have a duty to satisfy taxpayers’ customers. The primary goal of the tax authority is to reduce tax avoidance so the taxpayer’s professional accounting expertise is respected. This resulted in the tax code being enforced, decreasing management obfuscation and diversion, and boosting FR quality (Hanlon et al., Citation2014). In countries with an enforced tax compliance model like Vietnam, tax authorities and taxpayers are often based on power and coercion. Tax authorities often interfere with the accounting area in businesses, and businesses often spend a lot of time and effort explaining the difference between tax declaration data and accounting data. To deal with these tax authority requirements, instead of according to accounting standards and regimes, many firms applied their accounting work based on tax regulations (depreciation, provision, revenue recognition, cost of production, …), which has seriously affected the FR quality. The above arguments were also the basis for explaining the negative relationship between TAE and INC. When receiving and absorbing tax authorities’ contributions, the enterprise’s internal control system, considered to include activities, measures, plans, views, rules, policies, and efforts of the unit, is often aimed at facilitating tax declarations. Therefore, instead of encouraging the business to comply with accounting regulations when preparing and presenting FR, internal control promotes tax regulations, mainly related to recognizing revenue and expenses under the corporate income tax law. Based on the above facts, this study highly recommended that tax administrators change their working perspectives and avoid putting pressure on businesses in processing and presenting their financial statements. In addition, tax administrators also need to have a good understanding of accounting and should be aware that the primary basis for performing accounting work at the unit is accounting standards; The provisions of tax (which are the main provisions of the Law on Corporate Income Tax) are only used to recognize revenues and expenses when declaring tax, not as a basis for identifying revenues and expenses in FR. In addition, tax officers should not directly or indirectly provide accounting services for businesses to ensure independence in work and ensure the quality of FR. Second, with the survey sample divided into two groups (a group of enterprises that have not performed FR audits, and a group of enterprises that have performed FR audits), the study has also contributed to affirming the role of IAU for FR quality. The test results show that the audited FR has higher quality than the unaudited FR. Along with the positive impact of INC on FR quality, this study has contributed to confirming the monitoring mechanism’s role from inside (INC) and outside the enterprise (IAU) to FR quality. In Vietnam, the current Accounting Law requires accounting units to set up internal control systems in their units to secure assets. The entity’s safety is ensured to avoid misuse and inefficiency; the transactions are approved by the proper authority and are fully recorded as the basis for preparing and presenting the secured financial statements. However, the implementation is still facing difficulties due to the lack of legal documents specifying the organization, inspection, and supervision to ensure the INC. In order to contribute to improving the quality of FR, we recommend that the State management agencies in Vietnam consider the regulation on the implementation of internal control, and issue implementation guidelines. Information on internal control specifically for each type of accounting unit. In terms of the IAU perspectives, this research recommends that the government public sector issue regulations to limit competition based on the current reduction of audit fees; It is necessary to have regulations on reasonable sanctions for audit firms and auditors who have made mistakes in the quality of audit services. Third, this study also confirms the mediating role of INC on the relationship between TAE, IAU and FR quality. This research suggests that the strict regulation of internal control helps limit the opportunistic behavior of managers, and limit the arbitrariness in using the discretionary accruals, thereby helping to minimize the negative impact of TAE on FR quality and increase the positive impact of IAU on FR quality.

7. Limitations and future research

This study aims to measure TAE based on the actual occurrence of a tax audit. The actual occurrence of a tax audit is primarily determined based on the number of times the tax audit was performed over five consecutive years before the survey (from 2016 to 2020) divided by 5. Measuring TAE through the probability of a tax audit may not be the most optimal method because of the difficulty in measuring TAE (Desai et al., Citation2007). Therefore, future studies need to pay attention to supplementing and improving the method of measuring TAE.

The research model has R2 adj = 0.554. That means INC, IAU and TAE can explain 55.4% of the variation of FR quality, so the following study should find out more potential factors affecting the FR quality. Moreover, future research needs to explore the interpretation of INC variability in addition to the IAU and TAE factors.

Acknowledgements

This research is funded by University of Economics and Law, Vietnam National University Ho Chi Minh City, Vietnam and University of Economics Ho Chi Minh City (UEH), Ho Chi Minh City, Vietnam.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Quoc Thuan Pham

Quoc Thuan Pham is a lecturer at the Faculty of Accounting and Audit, University of Economics and Law, VNU HCMC, Vietnam with around 24 year teaching and researching in Accounting and Auditing. His research interest could be found in accounting, audit, policy and finance.

Thi Giang Tan Tran

Thi Giang Tan Tran is a associate professor of School of Accounting at UEH University in Vietnam with around 40 year teaching and researching in Accounting and Auditing. Her research interest could be found in accounting, audit and internal control.

Thi Thao Hien Bui

Thi Thao Hien Bui is a lecturer at International University, VNU HCMC, Vietnam. She is also a Ph.D. student at Taylor’s Business School, Taylor’s University, Selangor, Malaysia. Her research interests are in the areas of the firm internal control & financial report quality, firm performance.

Anh Thanh Bui is a lecturer at University of Economics and Law, VNU HCMC, Vietnam. His preferred research areas are corporate governance, accounting conservatism and fraudulent financial reporting.

Thi Phuong Loan Nguyen

Thi Phuong Loan Nguyen is a lecturer at University of Economics and Law, VNU HCMC, Vietnam. She is also a Ph.D. student at Victoria University of Wellington, Wellington, New Zealand. Her research covers a variety of topics related to accounting and audit.

Anh Thanh Bui

Thi Thao Hien Bui is a lecturer at International University, VNU HCMC, Vietnam. She is also a Ph.D. student at Taylor’s Business School, Taylor’s University, Selangor, Malaysia. Her research interests are in the areas of the firm internal control & financial report quality, firm performance.

Anh Thanh Bui is a lecturer at University of Economics and Law, VNU HCMC, Vietnam. His preferred research areas are corporate governance, accounting conservatism and fraudulent financial reporting.

References

- Agbenyo, W., Jiang, Y., & Cobblah, P. K. (2018). Assessment of government internal control systems on financial reporting quality in Ghana: A case study of Ghana revenue authority. International Journal of Economics and Finance, 10(11), 40–27. https://doi.org/10.5539/ijef.v10n11p40

- Almaqtari, M. F. A., Al-Homaidi, M. E. A., & Ahmad, A. 2017. Impact of corporate governance mechanisms on financial reporting quality: Evidence from India. Emerging Issues in Finance, 2017, 144. https://www.researchgate.net/profile/Eissa-Al-Homaidi/publication/348339810_Impact_of_corporate_governance_mechanisms_on_financial_reporting_quality_Evidence_from_India/links/5ff8e49045851553a02e7690/Impact-of-corporate-governance-mechanisms-on-financial-reporting-quality-Evidence-from-India.pdf.

- Almaqtari, F. A., Farhan, N. H., Al-Homaidi, E. A., & Mishra, N. (2020). An empirical evaluation of financial reporting quality of the Indian GAAP and Indian accounting standards. International Journal of Accounting, Auditing and Performance Evaluation, 16(2–3), 200–229. https://doi.org/10.1504/IJAAPE.2020.112717

- Almaqtari, F. A., Hashed, A. A., Shamim, M., & Al-ahdal, W. M. (2021). Impact of corporate governance mechanisms on financial reporting quality: A study of Indian GAAP and Indian Accounting Standards. Problems and Perspectives in Management, 18(4), 1. http://dx.doi.org/10.21511/ppm.18(4).2020.01

- Alsmady, A. A. (2022). Quality of financial reporting, external audit, earnings power and companies performance: The case of Gulf Corporate Council Countries. Research in Globalization, 5, 100093. https://doi.org/10.1016/j.resglo.2022.100093

- Altamuro, J., & Beatty, A. (2010). How does internal control regulation affect financial reporting? Journal of Accounting and Economics, 49(1–2), 58–74. https://doi.org/10.1016/j.jacceco.2009.07.002

- Archambault, J. J., & Archambault, M. E. (2003). A multinational test of determinants of corporate disclosure. The International Journal of Accounting, 38(2), 173–194. https://doi.org/10.1016/S0020-7063(03

- Bell, T. B., & Carcello, J. V. (2000). A decision aid for assessing the likelihood of fraudulent financial reporting. Auditing: A Journal of Practice & Theory, 19(1), 169–184. https://doi.org/10.2308/aud.2000.19.1.169

- Beneish, M. D., Billings, M. B., & Hodder, L. D. (2008). Internal control weaknesses and information uncertainty. The Accounting Review, 83(3), 665–703. https://doi.org/10.2308/accr.2008.83.3.665

- Biddle, G. C., Hilary, G., & Verdi, R. S. (2009). How does financial reporting quality relate to investment efficiency? Journal of Accounting and Economics, 48(2), 112–131. https://doi.org/10.1016/j.jacceco.2009.09.001

- Carpenter, T. D., & Reimers, J. L. (2005). Unethical and fraudulent financial reporting: Applying the theory of planned behavior. Journal of Business Ethics, 60, 115–129. https://doi.org/10.1007/s10551-004-7370-9

- Chalmers, K., Hay, D., & Khlif, H. (2019). Internal control in accounting research: A review. Journal of Accounting Literature, 42, 80–103. https://doi.org/10.1016/j.acclit.2018.03.002

- Chen, Y., Gul, F. A., Truong, C., & Veeraraghavan, M. (2016). Auditor client specific knowledge and internal control weakness: Some evidence on the role of auditor tenure and geographic distance. Journal of Contemporary Accounting & Economics, 12(2), 121–140. https://doi.org/10.1016/j.jcae.2016.03.001

- Clinton, S. B., Pinello, A. S., & Skaife, H. A. (2014). The implications of ineffective internal control and SOX 404 reporting for financial analysts. Journal of Accounting and Public Policy, 33(4), 303–327. https://doi.org/10.1016/j.jaccpubpol.2014.04.005

- Davidson, R., Goodwin‐Stewart, J., & Kent, P. (2005). Internal governance structures and earnings management. Accounting & Finance, 45(2), 241–267. https://doi.org/10.1111/j.1467-629x.2004.00132.x

- Desai, M. A., & Dharmapala, D. (2009). Earnings management, corporate tax shelters, and book-tax alignment. National Tax Journal, 62(1), 169–186. https://dx.doi.org/10.2139/ssrn.884812

- Desai, M. A., Dyck, A., & Zingales, L. (2007). Theft and taxes. Journal of Financial Economics, 84(3), 591–623. https://doi.org/10.1016/j.jfineco.2006.05.005

- Donelson, D. C., Ege, M. S., & McInnis, J. M. (2017). Internal control weaknesses and financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), 45–69. https://doi.org/10.2308/ajpt-51608

- Doyle, J., Ge, W., & McVay, S. (2007). Determinants of weaknesses in internal control over financial reporting. Journal of Accounting and Economics, 44(1), 193–223. https://doi.org/10.1016/j.jacceco.2006.10.003

- Eisenhardt, K. M. (1989). Agency theory: An assessment and review. Academy of Management Review, 14(1), 57–74. https://doi.org/10.5465/amr.1989.4279003

- Elbannan, M. A. (2009). Quality of internal control over financial reporting, corporate governance and credit ratings. International Journal of Disclosure and Governance, 6(2), 127–149. https://doi.org/10.1057/jdg.2008.32

- El-Bannany, M. (2018). Financial reporting quality for banks in Egypt and the UAE. Corporate Ownership & Control, 15(2), 116–131. http://doi.org/10.22495/cocv15i2art10

- Ewert, R., & Wagenhofer, A. (2019). Effects of increasing enforcement on financial reporting quality and audit quality. Journal of Accounting Research, 57(1), 121–168. https://doi.org/10.1111/1475-679X.12251

- Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Sage Publications Sage CA.

- Gelinas, U. J., Dull, R. B., Wheeler, P., & Hill, M. C. (2017). Accounting Information Systems. Cengage Learning.

- Hair, J., Black, B., Babin, B., & Anderson, R. (2010). Multivariate data analysis 7th Pearson prentice hall. Upper Saddle River.

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. (2014). Exploratory factor analysis multivariate data analysis (7th Pearson New International edition). Harlow: Pearson.

- Hair, J. F., Jr., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modeling (PLS-SEM) (Third ed.). Sage publications.

- Hair, J., Sarstedt, M., Ringle, C. M., & Gudergan, S. P. (2018). Advanced issues in partial least squares structural equation modeling (PLS-SEM). Sage publications.

- Haislip, J. Z., Peters, G. F., & Richardson, V. J. (2016). The effect of auditor IT expertise on internal controls. International Journal of Accounting Information Systems, 20(2016), 1–15. https://doi.org/10.1016/j.accinf.2016.01.001

- Hạnh, L. T. M. (2015). Financial information transparency in listed companies on Vietnam’s stock market. (PhD). University of Economic of Hochiminh City, Hochiminh City. http://digital.lib.ueh.edu.vn/handle/UEH/42459

- Hanlon, M., Hoopes, J. L., & Shroff, N. (2014). The effect of tax authority monitoring and enforcement on financial reporting quality. The Journal of the American Taxation Association, 36(2), 137–170. https://doi.org/10.2308/atax-50820

- Hasan, S., Kassim, A. A. M., & Hamid, M. A. A. (2020). The impact of audit quality, audit committee and financial reporting quality: Evidence from Malaysia. International Journal of Economics and Financial Issues, 10(5), 272. https://doi.org/10.32479/ijefi.10136

- Hashed, A., & Almaqtari, F. (2021). The impact of corporate governance mechanisms and IFRS on earning management in Saudi Arabia. Accounting, 7(1), 207–224. http://dx.doi.org/10.5267/j.ac.2020.9.015

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Herath, S. K., & Albarqi, N. (2017). Financial reporting quality: A literature review. Int. J. Bus. Manag. Commer, 2(2), 1–14. https://www.researchgate.net/profile/Siriyama-Herath/publication/314236476_Financial_Reporting_Quality_A_Literature_Review/links/58bc692d92851c471d563950/Financial-Reporting-Quality-A-Literature-Review.pdf.

- Hulland, J. S. (1999). The Effects of Country-of-Brand and Brand Name on Product Evaluation and Consideration. Journal of International Consumer Marketing, 11(1), 23–40. https://doi.org/10.1300/J046v11n01_03

- IASB. (2010). Conceptual framework for financial reporting. https://www.ifrs.org/projects/2010/conceptual-framework-2010/#published-documents (Accessed: 15 March 2018)

- IASB. (2018). Conceptual framework for financial reporting. https://www.ifrs.org/projects/2018/conceptual-framework/#published-documents (Accessed: 17 June 2019)

- Iatridis, G. E. (2011). Accounting disclosures, accounting quality and conditional and unconditional conservatism. International Review of Financial Analysis, 20(2), 88–102. https://doi.org/10.1016/j.irfa.2011.02.013

- Ikbal Tawfik, O., Almaqtari, F. A., Al-ahdal, W. M., Abdul Rahman, A. A., & Farhan, N. H. (2022). The impact of board diversity on financial reporting quality in the GCC listed firms: The role of family and royal directors. Economic Research-Ekonomska Istraživanja, 1–33. https://doi.org/10.1080/1331677X.2022.2120042

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Ji, X.-D., Lu, W., & Qu, W. (2017). Voluntary Disclosure of Internal Control Weakness and Earnings Quality: Evidence From China. The International Journal of Accounting, 52(1), 27–44. https://doi.org/10.1016/j.intacc.2017.01.007

- Jonas, G. J., & Blanchet, J. (2000). Assessing quality of financial reporting. Accounting Horizons, 14(3), 353–363. https://doi.org/10.2308/acch.2000.14.3.353

- Khalil, U. F. (2022). Auditor choice and its impact on financial reporting quality: A case of banking industry of Pakistan. Asia Pacific Management Review. https://doi.org/10.1016/j.apmrv.2021.12.001

- Koo, D. S., Ramalingegowda, S., & Yu, Y. (2017). The effect of financial reporting quality on corporate dividend policy. Review of Accounting Studies, 22(2), 753–790. https://doi.org/10.1007/s11142-017-9393-3

- Krishnan, J., Krishnan, J., & Liang, S. (2020). Internal control and financial reporting quality of small firms. Review of Accounting and Finance, 19(2), 221–246. https://doi.org/10.1108/RAF-05-2018-0107

- Länsiluoto, A., Jokipii, A., & Eklund, T. (2016). Internal control effectiveness – A clustering approach. Managerial Auditing Journal, 31(1), 5–34. https://doi.org/10.1108/MAJ-08-2013-0910

- Lari Dashtbayaz, M., Salehi, M., & Safdel, T. (2019). The effect of internal controls on financial reporting quality in Iranian family firms. Journal of Family Business Management, 9(3), 254–270. https://doi.org/10.1108/JFBM-09-2018-0047

- Madden, T. J., Ellen, P. S., & Ajzen, I. (1992). A Comparison of the Theory of Planned Behavior and the Theory of Reasoned Action. Personality and Social Psychology Bulletin, 18(1), 3–9. https://doi.org/10.1177/0146167292181001

- Mardessi, S. (2022). Audit committee and financial reporting quality: The moderating effect of audit quality. Journal of Financial Crime, 29(1), 368–388. https://doi.org/10.1108/JFC-01–2021-0010

- MOF. (2005). VAS 17 - Income Taxes - Issued in pursuance of the Minister of Finance Decision No. 12/2005/QD-BTC (Vietnam). http://russellbedford.vn/index.php?option=com_content&view=article&id=77&catid=18 (Accessed: 2 April 2021)

- MOF. (2014). Guidelines For Accounting Policies For Enterprises - Issued in pursuance of the Minister of Finance Circular No. 200/2014/QD-BTC (Vietnam). http://danketoan.com/attachments/circular-200-2014-tt-btc-pdf.962677885/ (Accessed: 12 April 2021)

- Morris, J. J. (2011). The impact of enterprise resource planning (ERP) systems on the effectiveness of internal controls over financial reporting. Journal of Information Systems, 25(1), 129–157. https://doi.org/10.2308/jis.2011.25.1.129

- Mulyani, S., & Arum, E. D. P. (2016). The influence of manager competency and internal control effectiveness toward accounting information quality. International Journal of Applied Business and Economic Research, 14(1), 181–190. https://repository.unja.ac.id/668/3/1459747480.pdf.

- Myllymäki, E.-R., & Jokipii, A. (2011). The relationship between internal control effectiveness and operating performance. Contributions to Accounting, Auditing and Internal Control, 131–148. Acta Wasaensia. https://www.researchgate.net/profile/Barbro_Back/publication/227191297_The_Self-Organizing_Map_in_Selecting_Companies_for_Tax_Audit/links/00b7d51813ed8a4857000000.pdf#page=147

- Oh, K., Choi, W., Jeong, S. W., & Pae, J. (2014). The effect of different levels of internal control over financial reporting regulation on the quality of accounting information: Evidence from Korea. Asia-pacific Journal of Accounting & Economics, 21(4), 412–442. https://doi.org/10.1080/16081625.2014.880203

- Patterson, E. R., Smith, J. R., & Tiras, S. L. (2019). The interrelation between audit quality and managerial reporting choices and its effects on financial reporting quality. Contemporary Accounting Research, 36(3), 1861–1882. https://doi.org/10.1111/1911-3846.12487

- Pham, Q. T., Ho, X. T., Nguyen, T. P. L., Pham, T. H. Q., & Bui, A. T. (2021). Financial reporting quality in pandemic era: Case analysis of Vietnamese enterprises. Journal of Sustainable Finance & Investment, 1–23. https://doi.org/10.1080/20430795.2021.1905411

- Phornlaphatrachakorn, K. (2019). Internal control quality, accounting information usefulness, regulation compliance, and decision-making success: Evidence from canned and processed foods businesses in Thailand. International Journal of Business, 24(2), 198–215. https://ijb.cyut.edu.tw/var/file/10/1010/img/865/V24N2-5.pdf.

- Pucheta‐Martínez, M. C., Bel‐Oms, I., & Olcina‐Sempere, G. (2016). Corporate governance, female directors and quality of financial information. Business Ethics: A European Review, 25(4), 363–385. https://doi.org/10.1111/beer.12123

- Root, S. J. (2000). Beyond COSO: Internal control to enhance corporate governance. John Wiley & Sons.

- Rubino, M., & Vitolla, F. (2014). Internal control over financial reporting: Opportunities using the COBIT framework. Managerial Auditing Journal, 29(8), 736–771. https://doi.org/10.1108/MAJ-03-2014-1016

- Tanko, M. B. (2015). Tax law enforcement: Practice and procedure. Research Journal of Finance and Accounting, 6(7), 143–147. https://core.ac.uk/download/pdf/234630660.pdf.

- Thọ, N. Đ. (2011). Phương pháp nghiên cứu khoa học trong kinh doanh. TP. Nhà xuất bản Lao động-Xã hội.

- Thoradeniya, P., Lee, J., Tan, R., & Ferreira, A. (2015). Sustainability reporting and the theory of planned behaviour. Accounting, Auditing & Accountability Journal, 28(7), 1099–1137. https://doi.org/10.1108/AAAJ-08-2013-1449