Abstract

Throughout the history of the development of the economy, financial intermediation has performed the functions of reducing transaction costs, having a stimulating effect on the economic system. However, at certain stages, when replacing the real sector of the economy, could cause economic crises, inflating the money supply. The period after the collapse of the USSR became a pivotal experience for all former republics. The destruction of existing economic ties, the reorientation of the economic system from a centrally controlled to a market system, and other unfavorable factors did not promote the dynamic growth of the economy and affected the well-being of the population. This study attempts to determine the impact of financial intermediation institutes on the welfare of the population in the post-Soviet countries. We use the methodology of chrono-discrete monogeographic comparative analysis proposed by Demichev (2019) for legal institutions. In our study, we discuss the change from a planned economy to a market economy. The development of financial intermediation institutions can accelerate the way out of the crisis and stimulate the growth of the population’s well-being, but a balance is needed between the financial and real sectors of the economy.

1. Introduction

Financial intermediation is an economic tool and a sphere of economic activity, the purpose of which is to meet the needs of the population. In this case, needs are the primary factors, and the activity itself is secondary. The effectiveness of economic growth can be assessed in terms of the dynamics of gross income and per capita income; however, a more global assessment is social efficiency, expressed as the degree of satisfaction of the population in terms of their needs, which can be assessed from the standpoint of the welfare of the population. The well-being of the population is the most important factor in ensuring a decent quality of life for citizens.

Some researchers have defined well-being as the level of satisfaction with vital goods. Smith (Citation1776) considered financial intermediation as a means of providing wealth, reduce poverty through the interaction of personal and public interests. This definition illustrates the relationship between financial intermediation and the level of wealth, as it has already been justified that financial intermediaries bring together the interests of actors; that is, the consumer receives a greater degree of satisfaction when using financial services that provide the population with an increased level of income and acceptable investment risk. The definition by Campanella (Citation2009) and Morelli (Citation1953) associates well-being with an equable distribution of goods in society, as it provides for the overflow of resources from excess to scarce areas, emphasizing the contribution of financial intermediation in increasing well-being.

The UN assesses the well-being of a population through a comprehensive diagnosis in various areas, including employment, health, nutrition, demographic conditions, education, and human freedom. Among the factors that affect people’s well-being, the UN also highlights socioeconomic sustainability, which depends on financial market development.

Financial intermediation improves the well-being of people both materially and spiritually:

In material terms, financial intermediaries help to increase the capital of the segment of the population that acts as savers, save transaction costs, and secure more income with less risk via investments, which makes it possible to meet future needs, maintain the standard of living for the elderly, and people with disability;

For those participants in the financial market who are borrowers, financial intermediaries expand the possibilities of meeting the needs of the moment, provide quality medical treatment, assist in acquiring real estate, and aid in receiving education on a paid basis; in the absence of financial intermediaries, the current consumption level of borrowers would be lower;

In terms of morality, financial intermediaries, by increasing the reliability of investments, provide confidence in the future and better health, with the time that is saved when using the services of intermediaries used to meet other needs such as recreation;

Empowerment through borrowing allows people to feel more comfortable in the current period.

Financial intermediaries are organizations that participate in the generation of added value, thereby increasing GDP and ensuring the economic growth of the country’s economic system as a whole. Financial institutions are generally taxpayers, expanding the state budget revenue and increasing the state’s ability to meet the needs of the population. Financial institutions make it possible to finance innovations from a country’s internal reserves, which provides opportunities for future economic development.

At the same time, it should be noted that certain risks are associated with financial intermediation. Reassessment of one’s own capabilities when using borrowed funds can lead to a situation in which a person is unable to fulfill obligations, and the person’s financial situation deteriorates noticeably. Such a situation is possible in the case of dishonest behavior of financial intermediaries, aggressive imposition of services, and citizens lacking information on the cost of credit products. To eliminate this phenomenon, state regulations and the development of financial literacy among populations are necessary.

The relationship between the activities of financial intermediaries and economic growth is a debatable topic in the scientific community, as there are both supporters and opponents of the idea of a correlation between the rates of economic growth and the development of financial institutions. Thus, Bagehot (Citation1920) and Hicks (Citation2003) consider the importance of capital markets for stimulating economic growth, citing as an example the situation in Great Britain in the 18th and 19th centuries, when the agrarian economic system was being transformed into an industrial, capital-intensive one. Capital markets provided resources for investors who were ready to innovate. At the same time, Robinson (Citation2000) points to the inverse relationship between economic growth and the development of financial institutions as its consequences. In our opinion, the relationship between financial intermediation and economic growth is clear. The growth rate of financial intermediation and its development should be assessed not only in quantitative terms, but also in qualitative ones, understanding the latter as the degree of customer satisfaction, building of a reputation, and competing in the global financial market.

Financial intermediation depends on global economic trends, as it is associated with the international movement of funds. Therefore, for the development of financial institutions, it is necessary to develop a system for reducing risks and dependence on international counterparties, which is especially true for the Russian Federation.

In addition, economists note the dependence of financial intermediation on inflationary trends. In the context of rising inflation, the activity of financial intermediaries is reduced, and the number of so-called “refusals from a financial intermediary” (“financial disintermediation”) increases when investors and savers enter into transactions between themselves on their own, without using the services of an intermediary. Thus, to develop financial intermediaries, it is necessary to control the inflation rate.

To study the general development trends in post-Soviet countries, it is necessary to clarify the objective of the analysis. We should agree with the authoritative opinion of Demichev (Citation2021) that the category “post-Soviet countries” should include all the republics of the former Soviet Union. In addition to other factors, the dynamics of socioeconomic processes in post-Soviet countries are determined by the existence of the union state (USSR).

This study determines the impact of a financial intermediation institute on the welfare of the post-Soviet population.

Our tasks are the following:

Conduct a comparative analysis of economic development indicators in post-Soviet countries

Perform a comparative analysis of the well-being of the population

Trace the relationship between the level of development of financial intermediation and the well-being of the population in post-Soviet countries.

The methodological basis of the study is institutional theory and system analysis.

The theoretical basis of the study was the works of specialists in the field of the theory of financial intermediation Zemlyachev and Zemlyacheva (Citation2019), Darbinyan and Sandoyan (Citation2010), Kostrovets (Citation2020), Pisarenko (Citation2017).

The problems of economic development and the structure of the financial system of the post-Soviet countries are revealed in the works of Donetskova (Citation2018), Lukyanovich (Citation2021), Muratova (Citation2021), Pishchik (Citation2016).

The problems of developing the activities of financial intermediaries in the post-Soviet countries are considered in the works of Tashirov (Citation2016).

Currently, the post-Soviet countries’ economy is developing under conditions of serious external pressure; there are crisis phenomena in the development of the economic systems of the countries. The development of financial intermediation institutions can accelerate the way out of the crisis and stimulate the growth of the population’s well-being. Financial intermediation can act as a catalyst for the development of the financial market, provided that the right tools are chosen to support this industry. At the current stage of economic development, it is important to formulate universal principles and algorithms for the development of financial intermediary institutions that can be used in emerging markets and will serve to strengthen the economic security of the post-Soviet countries.

Highly appreciates the role of financial intermediaries in countries with developing economies Tikhomirova (Citation2013), considering financial intermediation as an incentive for the development of the service sector and the most important factor influencing the innovation processes of the tertiary sector.

Currently, there are several theories defining the essence of financial intermediation and assessing the relationship between the structure of the financial market and the well-being of the population in different ways. The publication of a series of reports by the Central Bank of the Russian Federation (Citation2017) was devoted to this problem, where researchers studied the experience of countries with economies in transition in the field of formation of financial markets and came to conclusions about the need to develop non-banking institutions, such as mutual investment funds, private pension funds, insurance companies, etc.

The question of the ratio of the banking and non-banking sector in the financial intermediation market remains debatable. Bakaykina (Citation2017) emphasizes the role of development banks in the lending market for small and medium-sized businesses in Russia.

At the same time, the relationship between the development of financial instruments and the growth in the welfare of the population is emphasized by most researchers (Glotova et al. (Citation2019), Soldatenkova (Citation2019):

The importance of the role of the Central Bank’s in the development of financial intermediation is accepted by most researchers (Uglitskikh et al., Citation2017). The issues of interaction of financial intermediaries of various types are widely considered: banks and insurance companies; banks and pension funds. We can agree with the opinion of Donetskova (Citation2016) that for the development of the financial market it is necessary to intensify competition in the financial services market.

We support the point of view of Pishchulov (Citation2021) that the type and specifics of the specialization of financial intermediaries, by accelerating the movement of funds from the lender to the borrower, can affect the speed of transactions in the economy, which, in turn, affects economic growth and the level of well-being of the population.

Financial and insurance intermediaries play an important role in strengthening economic security. The possibilities of these institutions to reduce the risks of the regional financial system are considered in the work of Kozminykh (Citation2020).

In our opinion, financial intermediaries in the transforming economies should perform somewhat different functions than in developed financial systems. Financial intermediation in emerging financial markets should create incentives for active economic growth, here it is necessary to use innovative tools, to use the mechanisms of public-private partnership.

Pishchik (Citation2016) believes that in order to develop the financial market of the post-Soviet countries, it is worth focusing more on the insurance market and the securities market. Pisarenko (Citation2017) emphasizes the role of special universal financial intermediaries—financial conglomerates. We believe that a comprehensive development of financial intermediation institutions is necessary, including investment funds, financial cooperatives, pension funds, etc.

The empirical material of the study was the statistical data of international organizations, open data posted on the official websites of intermediary organizations (banks, insurance companies, investment funds, etc.).

The rest of this paper is organized as follows. Section 2 describes the method used in this study. Section 3 describes our results, while Section 4 provides an analysis. Section 5 concludes the study.

2. Materials and methods

We propose using the methodology of chrono-discrete monogeographic comparative (CdMC) analysis proposed by Demichev (Citation2019) for legal institutions, enabling the study of the dynamics of socioeconomic processes. Adapted to economic objects, such a methodology involves the use of different methods, approaches, and theoretical concepts for the analysis of various economic phenomena that occurred in the same territory with changes in economic formation over time. In our case, we discuss the change from a planned economy to a market economy. In post-Soviet countries, a transitional or mixed economic model has emerged during the transition to a market economy.

Let’s figure out what is behind this concept.

In traditional comparative analyses the comparison is done for similar type of institutions, ideas, and so on for different countries that existed in the same historical period, or, in the case of a chronological discrepancy, it is done between similar constructs of reality, at the same stages of historical development.

“Monogeographic” (from “mono” - one) means that comparison is done among the state institutions, ideas, concepts, etc., that existed not in different countries, but in one country.

“Chrono-discrete” (from “chronos” - time and “discreteness” - separation, division, non-continuity) refers to the institutions that are compared, have had a time gap in their existence because of different reasons, so their existence is discrete. Moreover, in the history of such institutions there should be not just a break, but a certain break in tradition. In fact, it is not the same institution that has evolved over a long period of time that is compared, but similar institutions that emerged under similar conditions in different historical periods in the absence of direct continuity between them.

The author of the civilizational approach, the English historian Toynbee (Citation1939), speaking about the development of civilizations, formulated the law of “challenge—and - response.” Its essence is that sooner or later every civilization faces certain natural, social or other external and internal challenges. If an adequate response is not found to the challenge, then civilization perishes. In the event of successful resolution of the challenge, the nation continues to develop.

The CdMCA methodology (CdMCA -methodology) is a set of scientific approaches, principles, and methods for studying institutions, ideas, concepts, phenomena, etc. that existed at different times in one country, and in the history of which there was an interruption of the legal tradition.

The subject of the CdMCA is the elements of historical and modern reality, studied with the help of the CdMCA methodology. At present, the subject of CdMCA includes state and legal institutions, ideas and concepts, principles, and phenomena.

Chrono-discrete institutions are state, legal, and other institutions that existed in the same country in different historical periods and in the existence of which there was a time gap (chrono-discrete pause), which led to the interruption of the legal tradition.

Chrono-discrete ideas and concepts are those ones that existed in the same country in different historical periods and in the existence of which there was a time gap (chrono-discrete pause), which led to the interruption of the legal tradition.

A chrono-discrete phenomenon is a collection of fragments of historical and modern objective reality that have certain autonomy and integrity, as well as similar characteristics, properties, features, elements, between which there was a chrono-discrete pause.

A chrono-discrete pause is a time of non-existence, an interruption of the historical tradition of a chrono-discrete institution, an idea, a concept, a phenomenon between its abolition and revival in the same country in different historical periods.

3. Results

3.1. Dynamics of the main economic development indicators

3.1.1. GDP comparative analysis

Here, we consider the dynamics of the main indicator of economic growth—GDP. Our findings support the opinion of Golovnin and Grinberg (Citation2021) who stated that GDP remains the most important indicator of economic development, allowing for the comparison of cross-country economic growth dynamics. Based on statistical data, a comparative analysis was carried out (Table ) to compare the positions of countries; the range of 1995–2019 was chosen because only for this period relevant data for all countries exist. In 1990, data were not provided for the Baltic States or the Republic of Moldova, and for 2020–2021, no information for Turkmenistan was available.

Table 1. Rating of post-Soviet countries in terms of GDP in billions of US dollars at current prices

During the period under review, some changes in the ranking occurred. Kazakhstan moved from third place to second, overtaking Ukraine; Azerbaijan sharply increased the volume of its GDP, moving from the 11th position immediately to 7th; Turkmenistan and Armenia moved up two positions; Latvia, Estonia, and Georgia dropped two positions at once; and Moldova and Kyrgyzstan lowered their places by one rank.

Russia steadfastly retained first position with a noticeable margin over all other states.

It can be clearly seen that the volume of GDP in Kazakhstan and Ukraine has changed dramatically: In 1995, Ukraine’s GDP was more than twice that of Kazakhstan’s, but in 2019, Kazakhstan was well ahead in this indicator. Among the Baltic countries, Lithuania was ahead of Latvia and Estonia in both 1995 and 2019. A sizable leap occurred for Armenia.

A comparison of the volumes by share of the total GDP is illustrated in Table . Russia occupied the largest share in the structure of the GDP; however, over the past period (1995–2019), its contribution decreased by 5.8%. A substantial reduction of 2.9% occurred in the share for Ukraine. Uzbekistan’s share reduced by 0.1%. Simultaneously, the shares of the following countries increased: Kazakhstan (3.6%), Azerbaijan (1.5%), Turkmenistan (1.4%), Lithuania (0.8%), Estonia (0.4%), Latvia and Armenia (0.3% each), and Georgia and Moldova (0.2% each). The increase in the shares of Tajikistan and Kyrgyzstan was very modest at 0.1% each.

Table 2. Share of total GDP of post-Soviet countries, %

In general, the contribution of post-Soviet countries for the period 1995–2019 increased by 1.08% but still amounted to a very small amount of world GDP (2.77%).

The Soviet Union was the world’s second-largest economy, with a GDP (GNP) of $2,660Footnote1 billion in 1990, more than double the combined GDP of all post-Soviet countries in 1995. It took these countries approximately eight years to reach the Soviet level of production. An analysis of the growth dynamics allows us to conclude that the most difficult period was 1990–1995. During this period, a sharp decline occurred in all post-Soviet countries. The largest drops in GDP in 1995 were noted in Tajikistan (12.42%), Ukraine (12.2%), Azerbaijan (11.8%), Belarus (10.4%), and Kazakhstan (8.2%). GDP growth was noted in only two countries: Armenia (6.9%) and Georgia (2.6%). However, in Georgia, the GDP decline reached 14.79% in 1990.

Considering GDP growth in post-Soviet countries from 1995 to 2019 at current prices, it can be noted that the greatest increases are for Azerbaijan (18.9 times) and Turkmenistan (17.2 times), and the smallest increases were observed in Ukraine (2.2 times) and Russia (3.3 times) (Table ).

Table 3. GDP growth rates from 1995 to 2019 at current prices in post-Soviet countries (according to the WB methodology)

In the recent period from 2015 to 2021, all countries recorded an increase in GDP from 2015 to 2019 (calculated based on a constant local currency), with the following exceptions of a decrease: Ukraine by 9.77% in 2015; Belarus by 3.83% and 2.53% in 2015 and 2016, respectively; the Republic of Moldova by 0.34% in 2015; Russia by 1.97 in 2015; and Azerbaijan by 3.1% in 2016.

In 2020, there was a reduction in the GDP of all post-Soviet countries, except for Tajikistan (growth by 4.4%) and Uzbekistan (growth by 1.89%). The decline in GDP was caused by the COVID-19 pandemic and related global trends (Table ).

Table 4. Post-Soviet countries’ GDP growth (annual, %) (according to the WB methodology)

3.1.2. Dynamics of GDP per capita

We now estimate the dynamics of GDP per capita using PPP. For the 24 years from 1995 to 2019, the indicator increased to a maximum in Armenia (by 748.46%) followed by Georgia (729.94%), and the smallest growth rates were in Ukraine (222.65%), Uzbekistan (249.57%), and Tajikistan (268.57%), in that order (Table ).

Table 5. Ranking of GDP per capita growth rates by PPP in post-Soviet countries

The following changes took place in the ranking of countries. Kazakhstan moved from 3rd to 5th place, while at the end of 2019, the highest GDP per capita indicators were noted in the Baltic countries (Lithuania − 39911.3 US dollars, Estonia − 38961.5 US dollars, Latvia − 32893.9 US dollars). Lithuania increased its place in the ranking by one position and became the leader in the post-Soviet space in terms of GDP per capita, overtaking Estonia; Latvia’s position increased from 5th place to 3rd place; Russia retained the 4th position; Kyrgyzstan remained at the 14th position; Tajikistan also remained at the 15th position; the place in the rating of Ukraine sharply decreased (from position 6 in 1995 to position 12 in 2019); Belarus rose from 7th place in 1995 to 6th place in 2019; the rating of Turkmenistan increased from 8th place in 1995 to 7th in 2019; Moldova moved from 9th position in 1995 to 11th position in 2019; Azerbaijan’s position rose from 10th place in 1995 to 9th place in 2019; Uzbekistan’s place shifted from 11th position in 1995 to 13th place; Georgia’s place rose from 12th in 1995 to 8th in 2019; and Armenia improved its ranking from 13th place in 1995 to 10th place in 2019.

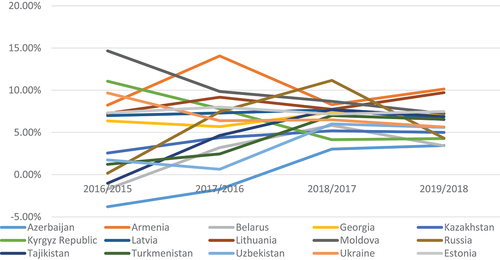

The growth rates of per capita GDP in 2015 differed significantly across countries; however, by 2019, the figures had flattened (Figure ).

Figure 1. GDP per capita growth rate from 2015 to 2019.

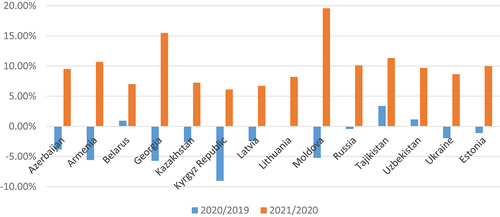

In 2020, most countries showed a drop in the indicator; the maximum was in Kyrgyzstan (9.04%) followed by Georgia (5.7%), and Armenia (5.58%). In 2021, the dynamics became sharply corrected; in all post-Soviet countries, the indicator increased by at least 6% (Figure ).

Figure 2. GDP per capita growth rate in 2020 and 2021.

3.1.3. Dynamics of external borrowings

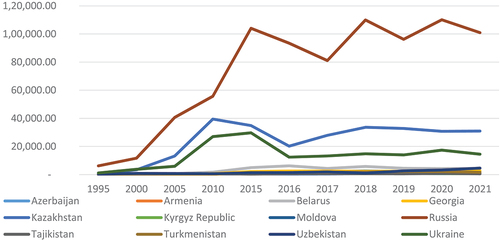

The GDP growth in the countries under consideration was accompanied by an increase in external borrowings. In general, for all countries in this time period, the dynamics of external debt are unstable, with a growth trend (Figure ).

Figure 3. Dynamics of external debt service in the post-Soviet countries from 1995–2021, in millions of US dollars at current prices.

In general, over this period, external debt increased in all post-Soviet states (excluding the Baltic countries and Tajikistan) (Table ). The growth rate of external debt servicing differs markedly by country: the increase was almost 200 times in Azerbaijan (195.4 times) and Armenia (181.8 times), while external debt increased more than 130 times in Georgia and Kazakhstan. In other countries, the increase in external debt was much less: from 24 times in Belarus to 9.5 times in Kyrgyzstan.

Table 6. Dynamics of external debt in the post-Soviet countries, in millions of US dollars

Considering the volume of external debt as a share of the GNI, we note significant changes in most countries, except for Russia (Table ).

Table 7. Dynamics of external debt in post-Soviet countries, % of GNI

In Russia, the volume of debt in the GNI structure decreased by 3.3%, amounting to 27.8% of the GNI, which is close to the indicator of Azerbaijan (27.5%). In other countries, external debt is more than 50% of the GNI structure, from 56.2% in Uzbekistan to 124.8% in Georgia. A level of external debt relative to GDP of more than 60% poses a danger to the stability of the state’s economic system (Senchagov & Mityakov, Citation2011).

3.2. Dynamics of financial intermediation development

3.2.1. Number of deposits in commercial banks

The development of financial intermediation in post-Soviet countries can be analyzed by studying the dynamics of the number of depositors. In general, from 2004 to 2021, the number of deposits in commercial banks (per 1,000 adults) increased: in Tajikistan, it increased by more than eight times from 172 in 2004 to 1,385 in 2021; in Georgia, the indicator increased almost five times from 207 in 2004 to 1,026 in 2021; in Uzbekistan, the growth was 2.8 times, from 245 in 2004 to 688 in 2021; and in Latvia, the number of deposits increased by 36%, from 944 in 2004 to 1282 in 2021 (Table ).

Table 8. Dynamics of number of depositors in commercial banks (per 1000 adults)

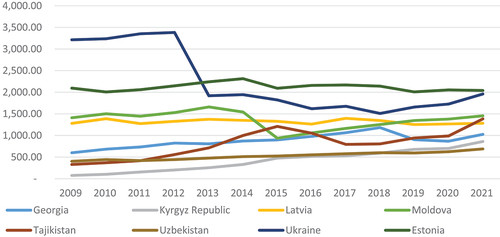

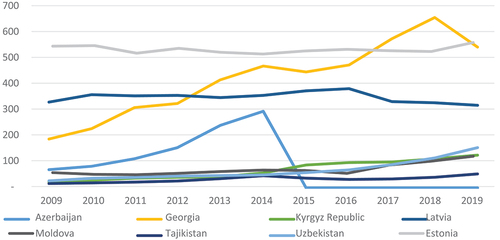

Visually, the dynamics since 2009 is shown in Figure .

Figure 4. Depositors in commercial banks (per 1000 adults).

The largest number of deposits as of 2021 was in Estonia at 2,041; it was somewhat less in Ukraine at 1,960. The group of more than 1,000 contributions includes countries such as Moldova (1,454), Tajikistan (1,385), Latvia (1,282), and Georgia (1,026); Kyrgyzstan’s figure did not exceed 1,000 (860).

Considering the dynamics of the number of borrowers, the following trends can be noted: in Georgia, the number of borrowers increased by 188% from 186 in 2009 to 535 in 2021; in Uzbekistan, the growth rate was 7.8 times, from 27 in 2009 to 211 in 2021; in Latvia, the number of borrowers decreased by 9.5% from 326 in 2009 to 295 in 2021; Tajikistan experienced an increase from 16 in 2004 to 53 in 2019 (3.3 times); in Estonia, there was a decrease in borrowers by 17.5% from 544 in 2009 to 449 in 2021; in Moldova, the indicator increased by 3.4 times from 54 in 2004 to 182 in 2021; and in Kyrgyzstan, the increase was 5.5 times from 23 in 2009 to 127 in 2021.

The dynamics of the number of borrowers is shown in Figure .

Figure 5. Borrowers in commercial banks in post-Soviet countries, number per 1000 people.

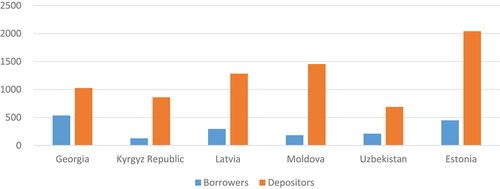

It is interesting to compare the number of depositors and borrowers (data for 2021) (Figure ).

Figure 6. Number of borrowers and depositors in commercial banks in post-Soviet countries, number per 1000 people.

As can be seen from the figure, the number of savers significantly outpaces the number of borrowers in all countries for which data are available for the period.

3.2.2. Dynamics of arrears

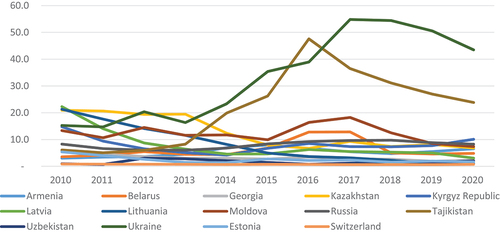

Next, we estimate the overdue debt, which shows the effectiveness of lending. We consider Switzerland as a benchmark indicator. The dynamics are shown in Figure .

Figure 7. Share (%) of overdue debt in total lending.

For the period from 2010 to 2020, the following changes took place:

The share of overdue debt increased in Ukraine by 28.2% from 15.3% in 2010 to 43.5% in 2020; in Tajikistan, by 17.7% from 6.1% in 2010 to 23.8% in 2020; in Armenia, by 3.6% from 3% in 2010 to 6.6% in 2020; in Belarus, by 1.3% from 3.5% in 2010 to 4.8% in 2020; and in Uzbekistan, by 1.1% from 1% in 2010 to 2.1% in 2020.

The share of overdue debt decreased in Lithuania by 20.3% from 21.3% in 2010 to 1.0% in 2020; in Latvia, by 19.2% from 22.3% in 2010 to 3.1% in 2020; in Kazakhstan, by 14% from 20.9% in 2010 to 6.9% in 2020; in Kyrgyzstan, by 4.7% from 14.8% in 2010 to 10.1% in 2020; in Moldova, by 5.9% from 13.3% in 2010 to 7.4% in 2020; in Estonia, by 3.8% from 5.4% in 2010 to 1.6% in 2020; and in Georgia, by 3.6% from 5.9% in 2010 to 2.3% in 2020.

The share of overdue debt has not changed in Russia and amounted to 8.3% as of 2020.

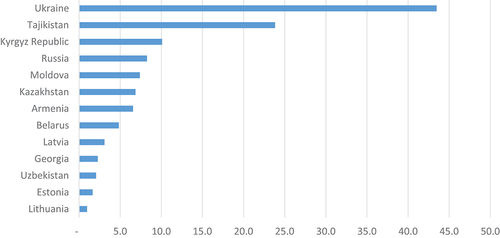

The ranking of countries by the level of overdue debt in 2020 is presented in Figure .

Figure 8. Ranking of countries by the level of overdue debt as of 2020, % of total debt.

As can be seen from the figure, Ukraine has the largest share of overdue debt, namely 43.5%; Tajikistan also has a large share at 23.8%. Countries with an average debt level include Kyrgyzstan, Russia, Moldova, Kazakhstan, Armenia, and Belarus. Decreased arrear levels were observed in Latvia, Georgia, Uzbekistan, Estonia, and Lithuania.

3.3. Assessing the dynamics of well-being

3.3.1. Human capital index

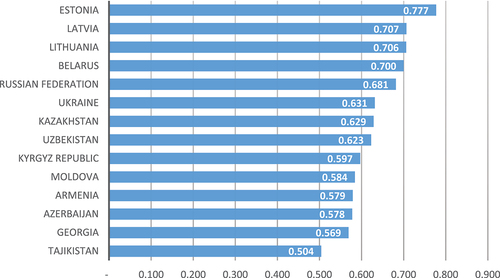

Let us consider the main indicators of the well-being of the population in post-Soviet countries and conduct a comparative analysis of these indicators. An integral indicator of human development is the human capital index (HCI), which reflects life expectancy, an educational component, and health status. The ratings of post-Soviet countries, calculated according to the level of the human capital index, are illustrated in Figure .

Figure 9. Human capital index in the post-Soviet countries, as of 2020.

As shown in the figure, Estonia occupies a pronounced leadership position, with an HCI of 0.777. Further, with a noticeable difference, there is a group of countries with approximately the same values: Latvia (0.707), Lithuania (0.706), and Belarus (0.700). Russia has a slightly lower value (0.681). There is a group of countries with indicators ranging from 0.631 to 0.623 (Ukraine, Kazakhstan, and Uzbekistan). Next, a group of five countries with HCI values ranging from 0.597 to 0.569 (Kyrgyzstan, Moldova, Armenia, Azerbaijan, and Georgia) exists. Rounding out the grouping of 14 countries was Tajikistan, with a value of 0.504. Turkmenistan did not provide any such data.

Table lists the dynamics according to WB data.

Table 9. Dynamics of changes in the human capital index

Considering the dynamics for 10 years from 2010 to 2020, it can be noted that in eight countries, there was an increase in the HCI: in Azerbaijan, the maximum increase in the index was recorded as 16.1%; in Russia, the increase in HCI was 13.3%; in Estonia, the increase in the index was 7%; in Kazakhstan, the increase was 5.8%; in Georgia, the increase in the index was 5.1%; in Moldova, the index increased by 5.1%; in Latvia, the index increased by 4.5%; and the minimum growth of the index was noted in Lithuania at 2.6%.

The HCI decreased by 0.2% over the period 2010–2020 only in Ukraine. Data for this period are available for only nine countries.

The positive dynamics of the index for all countries were noted in 2017 compared with 2010. The growth of the index was noted in all countries (there are data for nine of them); the maximum increase was in Kazakhstan (25.6 %) and the minimum in Ukraine (2.3%).

In 2018, compared with 2017, a negative trend was observed in two states: Ukraine and Georgia, where the index decreased by 0.7 and 0.8, respectively.

In 2020, compared with 2018, there were negative dynamics in nine countries: the index decreased from 0.5% in Armenia to 19.1% in Kazakhstan. An increase in HCI was observed only in Moldova (0.4%), Estonia (0.4%), and Kyrgyzstan (0.5%).

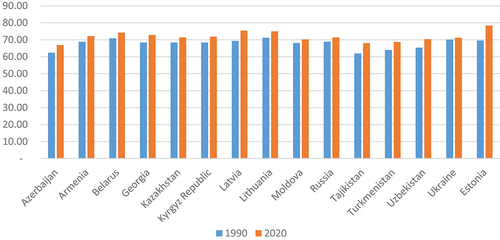

3.3.2. Life expectancy at birth

Let us consider the individual components of welfare assessment by estimating the life expectancy at birth. Table presents an analysis of dynamics over the past 30 years. The places in the table are arranged in descending order of the indicator.

Table 10. Dynamics of change in life expectancy at birth, years

At the end of 2020, in terms of life expectancy at birth, the clear leaders are the Baltic countries, where the indicator varies from 78.35 years to 74.93 years:

Estonia ranks first with an indicator of 78.35 years. Since 1990, this indicator has grown by 12.8%, and the country has risen from 4th place to 1st in the ranking of post-Soviet countries.

Latvia holds second place, with an indicator of 75.39 years. Over 30 years, there has been an increase of 8.8%, and the country has risen by three positions.

Lithuania is in third place with an indicator of 74.93 years. During the period under review, there was an increase of 5.3%, and the country dropped by two positions in the ranking; in 1990, it was the leader in life expectancy in the post-Soviet space.

Belarus is slightly behind the Baltic countries. At the end of 2020, it was in 4th place with an indicator of 74.23 years, there was an increase of 4.8% over the period, and the country lost two positions in the ranking (Figure ).

Figure 10. Dynamics of life expectancy at birth, years.

The largest increases in life expectancy at birth were observed in Estonia (12.8%), Tajikistan (9.9%), and Latvia (8.8%).

The smallest growth was noted in Ukraine (1.6%).

4. Discussion

At present, the post-Soviet economy is developing under conditions of serious external pressure; there is crisis phenomena in the development of the economic systems of countries included in the integration group. The development of financial intermediation institutions can accelerate the way out of the crisis and stimulate the growth of the population’s well-being. Financial intermediation can act as a catalyst for the development of the financial market, provided that the right tools are chosen to support this industry. At the current stage of economic development, it is important to formulate universal principles and algorithms for the development of financial intermediary institutions that can be used in emerging markets and will serve to strengthen economic security.

Tikhomirova (Citation2013) highly appreciates the role of financial intermediaries in countries with developing economies, considering financial intermediation as an incentive for the development and the innovation processes of the service sector.

Currently, there are enough different theories of financial intermediation, which define its essence in different ways and assess the relationship between the structure of the financial market and the well-being of the population in different ways. The publication of a series of reports by the Central Bank of the Russian Federation (2017) was devoted to this problem, where researchers studied the financial markets’ formation experience in the countries with transition economics and came to conclusion of the need to develop non-banking institutions, such as mutual investment funds, private pension funds, insurance companies, etc.

A discussion on the banking and non-banking sector ratio in the financial intermediation market remains debatable. Bakaykina (Citation2017) emphasizes the role of the banks in the development of SME lending market in Russia.

At the same time, the relationship between the development of financial instruments and the growth in the welfare of the population is emphasized by most researchers (Glotova et al., Citation2019; Soldatenkova, Citation2019).

The importance of the role of the Central Bank in the development of financial intermediation is acknowledged by most researchers (Uglitskikh et al., Citation2017). The interaction of different financial intermediaries are widely considered: banks and insurance companies; banks and pension funds. We can agree with the opinion of Donetskova (Citation2016) that for the development of the financial market it is necessary to intensify competition in the financial services’ market.

We support the point of view of Pishchulov (Citation2021) that the type and specifics of the specialization of financial intermediaries, by accelerating the movement of funds from the lender to the borrower, can affect the speed of transactions in the economy, which, in turn, affects economic growth and the level of well-being of the population.

Financial and insurance intermediaries play an important role in strengthening economic security by reducing the degree of operations’ risks especially in regional financial markets (Kozminykh, Citation2020).

In our opinion, financial intermediaries in transition economies should perform fairly different functions than in developed financial systems. Financial intermediation in emerging financial markets should create incentives for active economic growth, here it is necessary to use innovative tools, and the mechanisms of public-private partnership.

Pishchik (Citation2016) believes that to develop the financial market of the EAEU, it is worth focusing more on the insurance and the securities’ market. Pisarenko (Citation2017) emphasizes the role of special universal financial intermediaries—financial conglomerates.

We believe that a comprehensive development of financial intermediation institutions is necessary, including investment funds, financial cooperatives, pension funds, etc.

Based on the results of the study, it can be noted that countries with high indicators of economic development and well-being of the population (the Baltic states, Russia, and Kazakhstan) also demonstrate a high degree of financial instrument use. These countries are experiencing dynamic growth in GDP per capita. Kyrgyzstan, Tajikistan, and Uzbekistan were the least developed countries according to this indicator. Over the post-Soviet period, Armenia significantly improved its performance, while Uzbekistan fell.

The Human Development Index underlines the identified trends; the Baltic countries, Belarus, and Russia show the highest indicators, while the lowest were recorded in Tajikistan, Georgia, and Azerbaijan.

In the dynamics of overdue debt, there is no direct relationship with development indicators, but there are similar trends with other indicators; the most favorable situation is observed in the Baltic countries, as well as in Uzbekistan and Georgia. In the latter two countries, this situation developed because of restrictions in the banking sector.

5. Conclusions

Financial intermediation stimulates economic development and expands the well-being of the population through the better satisfaction of needs and increased national income. Financial intermediaries are an integral part of the modern financial system and contribute to the growth of efficiency in the financial market by ensuring the implementation of investment and innovation projects. Financial intermediation balances economic development and the alignment of intersectoral disproportions because financial resources are transferred from less profitable to more profitable areas. Financial intermediaries allow to earn income from resources that would otherwise be simply set aside and withdrawn from circulation. This demonstrates the relationship between financial intermediation, economic growth, and the well-being of the population.

It is necessary to note some limitations associated with the short period of existence of the post-Soviet countries, as well as the high rate of changes that have in the economies under consideration. The “special military operation” conducted by the Russian Federation, the imposed sanctions and restrictions on financial flows and trade of goods and services by the developed economies introduce new inputs and change the vector of the regional development. The consequence is the increased uncertainty, geopolitical risks, and a reduction in the planning period of economic agents and the population. There are also significant risks of statehood and possible changes in the model of economic development of the region under consideration. This imposed restrictions, have a strong influence on the choice of ways to develop the financial system of the post-Soviet countries as a superstructure of the real sector of the economy, and require further socio-economic research on the response of the countries’ economies to ongoing changes.

The development of financial intermediation is associated with the digital economy, qualitative changes in the process of providing financial services, and transitions to online services and ecosystems. Alternative types of financial transactions that exclude intermediation, such as peer-to-peer lending, are also developing.

To improve financial institutions’ efficiency, it is necessary to ensure that state regulations are in accordance with changes in economic practices. Particular attention should be paid to the development of financial intermediation in developing countries, as financial institutions push the economy toward rapid development.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Karen Vladimirovich Turyan

Karen Vladimirovich Turyan holds a Bachelor of Engineering and a Master of Economics from National Polytechnic University of Armenia, and a PhD in Economics from Institute of Economics of National Academy of Science, Armenia. He is a charter holder of CFA Institute, USA since 2018. He has more than 20 years of experience in Investment banking, as well as teaching in the universities.

Notes

1. The 1991 CIA World Factbook, URL: https://ia800501.us.archive.org/35/items/theciaworldfactb00025gut/25.txt

References

- Bagehot, W. (1920). Lombard street: A description of the money market. John Murray.

- Bakaykina, A. V. (2017) Competition of development banks in the market of financial intermediaries in lending to small and medium-sized businesses in Russia [ PhD dissertation of Economic Sciences]. Place of defense: FGAOUVO National Research University Higher School Economics. 195, (in Russian).

- Campanella, T. (2009). The city of sun. A poetical dialogue between a grandmaster of the knights hospitallers and a Genoese Sea-captain, his guest. First published in 1623., The floating press, ISBN: 978-1-775410-51-5, 74 p.

- Comparison of the model of the Russian financial sector with models of the financial sectors of other countries. (2017). Series of reports on economic research. (in Russian). (Date of the application: 11.06.2023). https://cbr.ru/Content/Document/File/16716/wp_23.pdf

- Darbinyan, A. R., & Sandoyan, E. M. (2010). Institutions of financial intermediation in the modern economy. Bulletin of the International Nobel Economic Forum, 1(3), 89–22. .

- Demichev, A. A. (2019). About the conceptual apparatus of chrono-discrete monogeographical comparative law. In A. A. Demicheva & K. A. Demichev Ed., Actual problems and prospects for the development of the scientific school of Chronodiscrete monogeographical comparative law: A collection of scientific papers based on the materials of the Second All-Russian Scientific Conference. (pp. 9–19). NRU RANEPA. in Russian.

- Demichev, A. A. (2021). Problems and prospects of using the chronodiscrete methodology monogeographic comparative law in the countries of the post-Soviet space. Actual problems and prospects for the development of the scientific school of Chronodiscrete monogeographical comparative law: Collection of scientific papers based on the materials of the Fourth All-Russian Scientific Conference, November 17, 2021. Nizhny Novgorod: NRU RANEPA, Pp. 9–18 EDN IQTTWF, (in Russian).

- Donetskova, O. Y. (2016). Modern features of the interaction of financial intermediaries in Russia. Architecture of finance: anti-crisis financial strategies in the context of global changes: collection of materials of the VII International scientific and practical conference, St. Petersburg, April 21–22, 2016 of the year. St. Petersburg: St. Petersburg State University of Economics. 402–405 EDN YRBATX, (in Russian).

- Donetskova, O. Y. (2018) Formation of a single financial market of the EAEU. Cooperation of the Republic of Belarus and the Orenburg region in innovative activities: Proceedings of the international scientific and practical conference November 20, 2018. Orenburg OOO IPK “Universitet”. 174–177, (in Russian).

- Glotova, I. I., Tomilina, E. P., & Doronin, B. A. (2019). Interaction parameters of financial intermediaries as a key factor in achieving financial market stability. Economics and Management: Problems, Solutions, 2(3), 99–104. in Russian.

- Golovnin, M. Y., & Grinberg, R. S. (2021). Outcomes of 30 years of economic transformation in the post-Soviet space: Light and shadows. Outlines of Global Transformations: Politics, Economics, Law, 14(5), 6–29. in Russian. https://doi.org/10.23932/2542-0240-2021-14-5-1

- Hicks, J. R. (2003). A theory of economic history. Translated from English/Common ed. And intro. Art. PM Nureeva – M. NP. Journal of Economic Issues, 224. in Russian.

- Kostrovets, L. B. (2020). Influence of the development of the banking system on investment activity. Collection of Scientific Works of the Series Finance, Accounting, Audit, 3(19), 190–201. -EDN DETRPZ, (in Russian).

- Kozminykh, O. V. (2020). Minimization of the economic risks of the insurer associated with the activities of financial and insurance intermediaries [ PhD dissertation of Economic Sciences]. Place of defense: FGBOU VO “St. Petersburg State University”, 195, (in Russian).

- Lukyanovich, N. V. (2021). Prospects for Eurasian economic Integration in the context of rising global challenges and threats. Problemy Natsional’noi Strategii, 1(1), 78–96. (in Russian). https://doi.org/10.52311/2079-3359_2021_1_78

- Morelli, É. G. (1953). Code of nature or the true spirit of its laws. Editions Sociales. (in French).

- Muratova, D. B. (2021). Main aspects of investment activity in the Republic of Kazakhstan. Forum Series: Humanitarian and Economic Sciences, 3(23), 99–102. in Russian.

- Pisarenko, Z. V. (2017). Financial convergence as a special mechanism for modifying the pension and insurance sectors of the world financial services market [ Doctor of Economic Sciences]. Place of protection: St. Petersburg State University. (in Russian).

- Pishchik, V. Y. (2016). Formation of the union of capital markets in the euro area: A projection on the EAEU with the participation of Russia. Economics Taxes Right, 9(2), 60–66. in Russian.

- Pishchulov, V. M. (2021). Connecting primary investors and end borrowers is one of the most important functions of financial intermediaries. Economics: Yesterday, Today, Tomorrow, 11(1), 167–175. https://doi.org/10.34670/AR.2021.99.42.020

- Robinson, J. (2000). Euler’s theorem and the problem of distribution. In V. M. Galperin Ed., Milestones of economic thought. Volume 3. Markets for factors of production. (pp. 59–81). School of Economics. in Russian.

- Senchagov, V. K. and Mityakov, S. N. (2011). Using the index method to assess the level of economic security//Vestnik ekonomicheskoi bezopasnosti. No. 5, (in Russian)

- Smith, A. (1776). An inquiry into the nature and causes of the wealth of nations. In The Glasgow Edition of the works and correspondence of Adam Smith, Vol. 2: An inquiry into the nature and causes of the wealth of nations, Vol. 1 (pp. 426–437). Oxford University Press. https://doi.org/10.1093/oseo/instance.00043218

- Soldatenkova, I. V. (2019). Development of financial supervision of the Bank of Russia as a mega-regulator of the financial market. Hypothesis, 1(6), 93–98. in Russian.

- Tashirov, A. (2016). Patterns of development of small and medium-sized businesses and the banking sector of the Kyrgyz Republic as a financial intermediary. Proceedings of the Issyk-Kul Forum of Accountants and Auditors of Central Asian Countries, 1-2(13), 340–345. EDN WMQTEV, (in Russian).

- Tikhomirova, O. B. (2013). Formation of strategic directions for the development of financial intermediation as a factor in increasing the efficiency of the service sector [ PhD dissertation]. Place of defense: FGOUVPO “St. Petersburg State University of Cinema and Television”, 153, (in Russian).

- Toynbee, A. J. (1939). A study of history. Identifier: in.ernet.dli.2015.148449, Identifier-ark: ark:/13960/t2993pg98, https://archive.org/details/in.ernet.dli.2015.148449/page/n7/mode/2up

- Uglitskikh, O. N., Klishina, Y. E., & Gladilin, A. A. (2017). The role of financial intermediaries in the financial market. Economics and Management: Problems, Solutions, 4(4), 49–53. EDN YSPFVB, (in Russian).

- World Bank, Statistics of Key Economic Development Indicators https://databank.worldbank.org/source/world-development-indicators

- Zemlyachev, S. V., & Zemlyacheva, O. A. (2019). The essence of financial intermediation and its participants. Veles, 5-1(71), 33–44. in Russian.