Abstract

Customer satisfaction is at the heart of any successful business entity. The influence of service quality on the role of customer orientation in achieving greater customer satisfaction in the banking industry from the perspective of customers has not received the required attention in the marketing literature. This study sought to respond to the question of whether service quality could influence the effect of customer orientation on customer satisfaction. The study adopts a quantitative research approach with a descriptive survey design. With the aid of PLS-SEM, data from 391 commercial bank customers was analysed. It was identified that, within the banking industry, customer orientation is a key predictor of customer satisfaction. Customer satisfaction would improve when service quality improves, and service quality plays a partial role in the relationship between customer orientation and service quality. The study recommends that policymakers develop comprehensive policies and also direct the management of commercial banks to develop customer orientation programmes.

1. Introduction

Customer orientation is a key focus for any firm’s relationships with its market (Kohli & Jaworski, Citation1990; Lee et al., Citation2021). As the central component of market orientation, customer orientation is also an important driver of firm performance (Nurfarida et al., Citation2021). The highly competitive nature of today’s markets is forcing organisations to be more sensitive to customers’ needs in order to retain their customers and acquire new ones. As a result, customer satisfaction has been the major concern of all organizations, including banks (Dam & Dam, Citation2021). In order to satisfy the customers and maintain their loyalty, the banks must focus on building customer orientation skills in their staff so as to build a strong relationship with customers. Nevertheless, banks’ being customer-oriented does not necessarily guarantee customer satisfaction unless a quality service is delivered to satisfy the bank customer (Bamfo et al., Citation2018).

The banking sector of Ghana, which is the focus of this study, has remained a very strategic sector for the nation’s quest for development and prosperity for its’ citizens. The liberalisation of the financial sector in conjunction with the economic reforms in the late 1980s and early 1990s has created room for more banks, including foreign banks, to patronise in the commercial banking sector (Aryeetey, Citation2008). It has also increased the supply of financial services and given customers the impetus to demand quality service. Currently, there are a good number of foreign and local banks in Ghana. They continue to roll out innovative products and services and use branch networking, automated services, and personalization of services as their major strategies to enrich the customer experience and improve the satisfaction level of customers in order to retain them (Boateng et al., Citation2021). The sector was deemed appropriate for this study because, over the years, there have been complaints regarding the attitude and behaviour of banks. Also, commercial banks in Africa and Ghana are facing low levels of customer satisfaction and loyalty due to high levels of customer demands with regards to technological changes and innovation (Nwanji et al., Citation2020).

It must be acknowledged that a number of studies (e.g., Li et al., Citation2019; Wibawa & Sukaatmadja, Citation2018) have been conducted on customer orientation in other sectors, like the public sector. However, these studies did not pay particular attention to measuring customer orientation from the perspective of customers. This notwithstanding, Li et al.’s (Citation2019) study only focused on customer orientation, satisfaction, and service quality with a focus on the electricity sector, which is a public utility service provider. This study is worth considering in a critical sector like the bank, where competition is very keen, which makes customer orientation a service quality and an important service marketing concept. Previous studies found a positive effect of customer orientation on customer satisfaction (Ang et al., Citation2011; Homburg et al., Citation2011), and found a positive relation between service quality and customer satisfaction (Segoro & Elvira, Citation2021).

Although scholars (see, Dam & Dam, Citation2021; Li et al., Citation2019) have recognised the importance of customer satisfaction, prior research was insufficient in several respects. First, customer orientation was evaluated by the employees of banks rather than the customers. Farrell et al. (Citation2001) argue that assessment of service quality should occur on two fronts: from employee and customer perspectives. Second, there is a need for more rigorous quantitative methodology and analysis, which can smooth the way of building integration models to set out the antecedents of customer satisfaction, such as customer orientation and service quality. Hence, the study seeks to effectively determine the effect of customer orientation on customer satisfaction and service quality among customers of commercial banks. Additionally, to assess the effect of service quality on customer satisfaction and investigate the influence of service quality on the relationship between customer orientation and customer satisfaction among customers of commercial banks. The role of service quality in this relationship is novel, especially in emerging markets. It adds to the bank’s marketing literature because, unlike most earlier studies, it assesses quality from the customer’s perspective. The study is important for marketing managers and relationship managers. It provides further strategies to influence bank customers’ behaviour.

The study contributes to market orientation, service quality, and customer satisfaction literature. Measuring customer orientation, one of the three variables of market orientation theory, from the perspective of customers has been made clear. This adds to the many areas where the theory of market orientation has been tested in recent times. The literature on the essence of customer orientation, customer satisfaction, and service quality in the banking sector has been established. For instance, it is established that service quality influences the effect of customer orientation on customer satisfaction.

Subsequent sections of the paper examine the literature on the subject matter, the research methods adopted for the study, the results and discussion, and the study’s implications. First, a literature review and hypothesis development are given.

2. Literature review and hypotheses development

This section reviews literature related to the study’s key concepts: customer orientation, customer satisfaction, and service quality. The study’s hypotheses are further developed.

2.1. The concept of customer orientation, service quality and customer satisfaction

2.1.1. Customer orientation

Customer orientation can be understood as an extension of relationship marketing, as both concepts emphasise the creation of sustainable competitive advantages through excellence in customer service (Steinman et al., Citation2000; Wibawa & Sukaatmadja, Citation2018). Similar to marketing relationships, customer orientation is aimed at enhancing and sustaining the profitability of a company by creating long-term relationships with customers and maximising their satisfaction (Yavas et al., Citation2011). According to Slater and Narver (Citation1998), customer orientation is one of the main principles of market orientation. Good awareness and understanding of the needs of customers not only help the business to generate superior value for the enterprise itself but also for its customers. Racela (Citation2014) describes customer orientation as “a provider’s ability to continuously test customers’ latent needs and discover potential needs.” A set of task-oriented behaviours such as customer support services is referred to as “consumer orientation.” Since it is limited to behaviours that consumers are likely to anticipate from a salesperson in the position of a businessperson, it has been dubbed “functional customer orientation” (Homburg et al., Citation2011).

Customer orientation also involves an employee’s propensity to develop a personal relationship with customers. Herhausen (Citation2011) suggested that customer orientation consists of behavioural and cultural characteristics. Whereas the behavioural perspective defines customer orientation as associated with the production and distribution of market information and its responsiveness (Dhingra et al., Citation2020), the cultural perspective is connected to the more fundamental characteristics of the company. From the behavioural perspective, Slater and Narver (Citation1998, p. 23) describe market orientation as an “organizational culture … that produces the most successful and efficient behaviours necessary for the development of superior value for the purchaser and, therefore, continuous superior performance for the company.” Therefore, activities to influence the organization’s customer orientation fall into two categories (Homburg et al., Citation2011). Customer orientation is often conceptualised to cover customer need recognition, customer engagement, customer concerns, and resolution channels (Taleghani et al., Citation2011).

Similarly, Majava et al. (Citation2014) referred to “customer involvement” as the extent to which the customer takes part in the production and distribution of the service. This is further supported by Jiang et al. (Citation2019), who suggest that the involvement of the customer is about exchanging knowledge, taking responsible actions, and maintaining personal contact between the company and the customer.

Likewise, Latyshova et al. (Citation2015) and Anabila et al. (Citation2020) also argued that customer orientation as a strategic decision is to focus all company resources to support and satisfy profit-making customers. Similarly, Fader (Citation2020) argues that customer orientation implies the analysis of customer value and the immediate concentration of marketing activities on the actual consumer segment with high added costs in order to maximise profits. Customer orientation is also conceptualised as a company’s ability to produce solid market results by meeting profitable customer requirements through a customer-centric company structure.

The study adopted a modified dimension of customer orientation, namely: customer needs identification, customer involvement, customer complaints, and customer channel resolution, as suggested (Jiang et al., Citation2019). Researchers such as Al Samman and Mohammed (Citation2020) and Choi and Joung (Citation2017) have used this framework. As such, this study adopted the framework to identify current practices, define future practices, and define key words and key issues in the commercial banking sector in Ghana.

2.1.2. Service quality

Quality of service can be defined as the perceived decisions arising from an appraisal process in which consumers equate their perceptions with what they believe they have received (Meesala & Paul, Citation2018). Abror et al. (Citation2019) further argue that the quality of the service is determined by its compliance with the customer’s requirements and expectations, and the better the fit, the higher the satisfaction. Following this, Zamry and Nayan (Citation2020) established three-dimensional approaches to service quality in terms of physical quality, interactive quality, and company quality. Physical quality refers to the quality of the resources and facilities used to provide services. It focuses on the physical settings that promote perceived quality. Interactive quality is the outcome of interactions between the consumer and interactive components such as contests, games, and ATMs. Interactive components are used to promote the quality of services given to customers. For instance, the use of ATMs, games, contests, and quizzes allows organisations to test the knowledge capacities of their customers or clients. The corporate quality of a company refers to the perception of quality by its customers over a long period of time. Previous studies such as Ali et al.’s (Citation2022) perceived corporate quality as the only quality dimension that consumers could determine before buying a service. It could be deduced that these three components of service quality are interrelated and combine to promote the quality of services given to customers in any organisational setting (Gong & Yi, Citation2018; Khan et al., Citation2019).

Service quality is often conceptualised as a multi-faceted construct of five dimensions: responsiveness, which includes Responsiveness, Assurance, Tangibility, Empathy and Reliability (RATER; Cronin & Taylor, Citation1992; Parasuraman et al., Citation1988). Tangibility applies to physical services, staff, and equipment used by the service provider (Naik et al., Citation2010). Reliability represents the consistency of the service provider and accuracy of performance, while responsiveness means the willingness of employees to react quickly and to be able to support customers (Parasuraman et al., Citation1988). Assurance refers to the expertise, courtesy, and trust of staff, while empathy is the capacity to provide customer service and individual attention (Robledo, Citation2001). In addition, B. Zeithaml et al. (Citation2006) defined perceived service quality as a general attitude of judgment in relation to the overall excellence of service superiority. It is the degree of difference between the expectations of the customer and the perception of the service rendered. On the other hand, Sultan and Wong (Citation2010) consider service quality an attitude arising from customers’ long-term evaluations of the services they receive. However, the current study adopted three dimensions of service quality, namely responsiveness, tangibility, and reliability, as suggested by Parasuraman et al. (Citation1988). This is basically due to their direct relevance to the study’s objectives. A modified version of SERVQUAL postulated by Parasuraman et al. (Citation1988) was adopted in this research as Hapsari et al. (Citation2016); Meesala and Paul (Citation2018) postulate that they are the best predictors of service quality. Service quality can be best described by consumers because they are the beneficiaries and eventual users of services offered by banks.

2.1.3. Customer satisfaction

Satisfaction as a term can be defined as a post-consumption or evaluative approach that differs from the hedonic spectrum and focuses on the product (Glowa, Citation2014). Customer satisfaction or dissatisfaction is a cognitive or affective reaction that surfaces in the form of a response to a single or prolonged series of service experiences. Murad (Citation2021) assumed that there were three key components of customer satisfaction, namely: cognitive, affective, or conative; the topic to which the response was directed; and the length of the assessment. In the literature, however, there are two main interpretations of satisfaction: satisfaction as a process and satisfaction as a result (Gustafsson et al., Citation2015).Satisfaction can therefore be characterised as an appraisal judgment of preference relating to a particular purchase decision.

In this study, customer satisfaction means that customers are pleased with the actions of banks, with goods and services, and that banks have succeeded in attracting and retaining them. To the degree that consumers invest time and money in banks, they demand high-value services. In other words, customer satisfaction is the popularity that the customer obtains from the different features of the product. In addition, it is a source of profit and an incentive for banks to carry out their activities (Khadka & Maharjan, Citation2017).

In the corporate world, customer satisfaction is understood as an overall customer attitude towards the services and products of a bank or service provider. Customer satisfaction has also been held accountable for customer loyalty over the last few years, which is referred to as a continuous positive customer purchasing behaviour towards a specific company or brand. Customer satisfaction is the most important factor contributing to customer loyalty, and customer satisfaction as a variable can influence customer loyalty and potential purchasing intentions (Machirori & Fatoki, Citation2014).

Kotler (Citation2007) was among the first to suggest that satisfaction is correlated with performance that meets expectations, whereas disappointment arises when performance falls below expectations. It is widely accepted that satisfaction is the feeling of enjoyment or dissatisfaction of an individual arising from a comparison of the perceived output of a product in relation to his or her expectations (Körner et al., Citation2015). This shows that if the perceived output is lower than anticipated, consumers will be disappointed. Otherwise, if the perceived expectations are met with results, consumers would be at an indifferent or neutral level. Customer satisfaction can also be seen as a customer’s overall assessment of the success of an offer made to date by banks (Machirori & Fatoki, Citation2014). Items measuring customer satisfaction may include reliability of bank services, product or service information, product or service accessibility, value for money, customer responsiveness, and a short waiting time.

2.2. Hypotheses development

2.2.1. Customer orientation and customer satisfaction

Before customers patronise a bank service, they often have some kind of expectation of service delivery that they desire or wish to be met after purchase and consumption. To meet these expectations, banks are expected to put customers at the heart of quality service delivery. Banks that put customers first are said to be customer-centric. One characteristic of a service is inseparability, which means most service offers have concurrent production and consumption. This remains a highly relevant context for service providers and customers. The bank’s practises have an influence on customer satisfaction. In the context of bank service delivery, customer orientation is about understanding the needs of customers not only to help the bank generate superior value but also for the satisfaction of their customers (Racela, Citation2014). On the other hand, customer satisfaction is understood as an overall customer attitude towards the product or service of a bank or service provider (Machirori & Fatoki, Citation2014). Those two variables (Customer Orientation and Customer Satisfaction) have enjoyed much attention in the service marketing literature and among some scholars (Henni-Tharau, 2004). Wali et al. (Citation2015) discovered a significant direct and indirect relationship between customer orientation and customer satisfaction. The study therefore hypothesises that

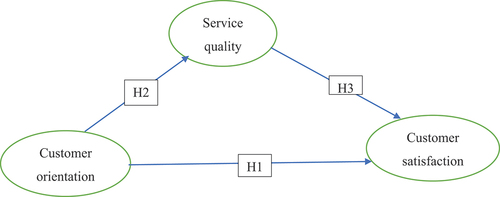

H1: Customer orientation has a significant positive effect on customer satisfaction among customers of commercial banks.

2.2.2. Customer orientation and service quality

Customer Orientation can be understood as an extension of relationship marketing, as both concepts emphasise the creation of sustainable competitive advantage through excellence in customer service (Steinman et al., Citation2000). Similarly, Khan et al. (Citation2019) posit that for service firms to enhance sustainable profitability, the key is customer orientation, as it further helps banks understand customers’ needs and provides essential information to organisations so they can meet customers’ needs with the right products and services. Thus, a highly customer-oriented organization, especially a bank, is important for quality service delivery, customer satisfaction, and survival. Furthermore, the role of customer orientation is a strong variable in quality service delivery in the service sector (Latyshova, Syablova, & Oyner, Citation2015). Scholars (e.g., Li et al., Citation2019) report that when service firms are customer-oriented, they tend to provide quality service to satisfy their customers. It can be concluded that customer orientation is critical in building the service quality of a service firm. The study therefore hypothesises that

H2: Customer orientation has a positive effect on service quality among customers of commercial banks.

2.2.3. Service quality and customer satisfaction

The service quality concept has been extensively discussed in marketing literature. Perceived service quality is a customer’s overall assessment of the service’s performance (V. A. Zeithaml et al., Citation1996). Similarly, customer satisfaction, which is about customers’ assessment of the supposed incongruity between their expectations and the actual service delivered, has also enjoyed massive review in the marketing literature (Tse & Wilton, Citation1988). Currently, these two constructs (service quality and customer satisfaction) have and will continue to receive much consideration in academia (Bamfo et al., Citation2018). Thus, the provision of a high-quality bank service is important for any bank, as it is part of the rational consideration for a customer to be satisfied with the bank. Furthermore, the role of perceived service quality is a strong variable with other marketing variables such as customer orientation and customer satisfaction in banking (Bakar et al., Citation2012). Scholars (e.g., see Kadir et al., Citation2017) report that when some customers perceive high service quality, they tend to be more satisfied. Finally, past empirical studies (e.g., Bakar et al., Citation2012) conclude that service quality is critical in building customer satisfaction. Thus, the hypothesis related to service quality in commercial banks is stated as follows:

H3: Service Quality has a positive effect on Customer Satisfaction.

2.2.4. Mediation role of service quality in customer orientation and customer satisfaction

Research has proven that customer orientation (CO) can directly affect customer satisfaction (CS; Machirori & Fatoki, Citation2014; Racela, Citation2014; Wali et al., Citation2015). However, it remains unclear whether this relationship can be mediated by service quality (SQ). Service quality focuses on a firm’s ability to deliver expected services to their customers; in view of this, some studies have concluded that it plays a role in promoting CO, which in turn leads to better customer satisfaction. However, the extent (partial, full, or none) to which SQ mediates this relationship remains inconsistent. For instance, Li et al. (Citation2019) revealed that SQ fully mediates the relationship between CO and CS in Ghana’s public utility sector. It was concluded that the presence of SQ improves CO and, subsequently, CS. According to Khen et al. (Citation2010), customers, in recent times, are increasingly becoming mindful of their rights and needs, therefore pushing businesses to constantly improve their service quality in order to keep them satisfied. Rai and Medha (Citation2013) also contend that CS is dependent on CO; however, it can be improved through SQ. These are clear indications that even though CO leads to CS, this effect can be strengthened through SQ. In contrast, Aburayya et al. (Citation2020) found that CO had an insignificant indirect effect on CO through SQ, concluding that SQ does not significantly moderate the linkage between CO and SQ. The finding implies that CO can directly affect CS without passing through SQ. Despite these inconsistencies in previous findings, the study hypothesised that:

H4: Service quality mediates the relationship between customer orientation and customer satisfaction.

2.5. Hypothezed conceptual framework

Figure demonstrates the hypothesed relationship between the constructs of the study as discussed above in section 2.2 of the study.

Figure 1. Study model.

3. Research methods

The nature of the study objectives is quantitatively inclined, hence its adoption of the positivist philosophy, quantitative research approach with a descriptive survey design. The study adopts a survey approach by studying commercial banks in the Greater Accra region of Ghana. Six commercial banks in the Greater Accra region therefore represent the population for this study. The exact number of customers of commercial banks could not be ascertained, and that was a key limitation in determining the sample size. Hair et al. (Citation2006) estimate that a population of 2,005,895 bank account holders of these banks, with a 95% confidence level and a 5% margin of error, will give a sample size of 384 (Hair et al., Citation2006). However, a few additions were made to make the sample size 420 tonnes to cater for non-responders. However, 381 customers fully completed the research instrument within the period of data collection. This gave a response rate of 91%, which the researcher deemed reliable for the study (Creswell & Plano-Clark, Citation2018).

In relation to sampling procedures, multi-stage sampling was used. First, the purposive sampling technique was used to select six (6) commercial banks in Greater Accra based on the following: large nature of branches; customer base; high asset base; and high market share (BOG, Citation2017). The study further employed a statistical random sampling technique by putting the banks and customers into various strata of local and foreign banks. Customers were randomly selected from a sample of their banks. The data collection was done through the administration of structural questionnaires by the researchers.

Items measuring the various variables were adapted from existing studies. Customer orientation was adopted and modified from measurements developed by Garrido-Moreno and Padilla-Melendez (Citation2011). Service quality measurements were adopted and modified from Karatepe et al. (Citation2005). Customer satisfaction measurements were adopted and modified from Leninkumar (Citation2017). Details of the items measuring each of the constructs are shown in Appendix . The data collection commenced on 5 October 2021 and ended on 13 January 2022.

4. Analysis, results and discussion

The partial least square structural equation modelling (PLS-SEM) technique was used to test the study’s hypotheses. This method covers violations of normality (multivariate normality) without requiring any hard assumptions about the distributional characteristics of the input data (Hair et al., Citation2014). It uses a confirmatory (hypothesis-testing) approach to investigate the structural theory of a problem (Babin, Hair, & Boles, Citation2008). Furthermore, because the PLS-SEM method can handle normality violations and missing data, no significant assumptions about the distributional properties of the raw data are necessary (Hair et al., Citation2012). This statistical tool employs both regression and factor analysis in its measurement models (Ullman & Bentler, Citation2012). As a result, it is useful for determining causal linkages between and among components, utilising a range of evaluation items. In this research, the PLS-SEM provides a thorough examination of the causal relationships among customer orientation (CO), service quality (SQ), and customer satisfaction (CS).

The results of the demographic characteristics of the study are shown in Appendix .

4.1. Regression model assessment

The regression model in the PLS-SEM was initially tested for quality purposes prior to the actual hypothesis testing. According to Hair et al. (Citation2014), the regression model is primarily evaluated to ensure that its constructs and associated indicators are of high quality and relevance and that the model’s output may be used to impact policies and practices. As a result, the researchers used item loadings to assess the quality of the indicators first. This is done to verify that the indicators allocated to each construction are accurate and high-quality indicators.

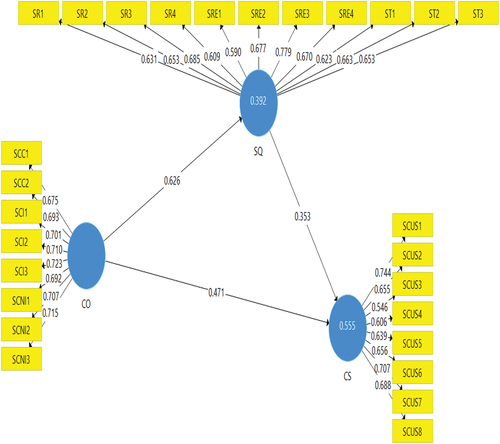

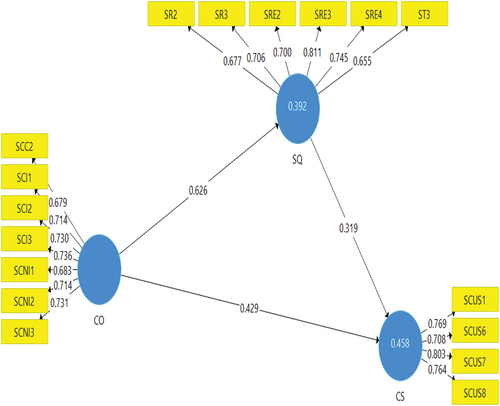

To achieve this, the rule suggests that indicator loadings should be ≥ 0.70 (Hair et al., Citation2017; Memon et al., Citation2021). The rule also proposes that item loadings greater than 0.70 could be deleted from the model, but with high precaution. Hair and Sarstedt (Citation2021), emphasise that instead of automatically removing items with loadings below 0.70, researchers should carefully evaluate the indicator’s impact or relevance to the other validity and reliability measures. Hence, items greater than 0.70, especially those between 0.40 and 0.70, could be maintained if they have positive impacts on the model’s validity and reliability. Figure depicts the regression model with all of the indicators’ item loadings and constructs, whereas Figure depicts the final regression model after all of the irrelevant items have been eliminated from the initial model.

Figure 2. Initial model.

Figure 3. Final model.

Preliminary analysis was undertaken to assess the study constructs after confirming the quality of each construct’s indicators. The researchers used PLS-SEM for reflective latent variables and a multicollinearity test for formative latent variables in confirmatory factor analysis (Hair et al., Citation2016). Convergence validity (CV) and discriminant validity (DV) are required for a scale to pass the confirmatory factor analysis test. Using the Fornell and Larcker criterion to check for DV, the square root of the minimum average variance extracted (AVE) must be greater than the maximum inter-construct correlations (Fornell & Larcker, Citation1981; Hair et al., Citation2016). According to Hensler et al. (Citation2015), the heterotrait-monotrait ratio (HTMT) of the correlations should also be determined before concluding on discriminant validity. All of the constructs (latent variables) in Table exhibited HTMT correlations of less than 0.85, demonstrating DV (Hair et al., Citation2017).

Table 1. Reliability and Validity

Furthermore, the rho A (to check for indicator reliability) and composite reliability (CR) tests in Table show that the results are greater than 0.70, as proposed by Hair et al. (Citation2017) and Henseler et al. (Citation2015). As such, the constructs utilised in this investigation met the composite reliability criteria. In terms of the AVE, all the values were greater than 0.5 (Hair et al., Citation2017), indicating convergent validity. Deductively, all the reliability and validity tests passed, paving the way for an assessment of the model’s predictive accuracy and relevance.

The predictive accuracy (R2) effect size (f2) and predictive relevance (Q2) were also used to evaluate the structural model in terms of predictive relevance and accuracy. For example, the R2 described the sum of the contributions of the predictor variables to the outcome construct (CS).

Table revealed that, about 45.8 percent of change in customer satisfaction (CS) is directly contributed by customer orientation (CO). This is because, the model produced an R2 of 45.8 percent in the link between CO and CS. This result demonstrates a good fit for the model, as CO accounts for roughly half of the total variation in CS; thus, to improve CS by about 45 percent, the commercial banks need to focus on CO. Also, CO was found to statistically contribute 39.2 percent of any change in SQ; thus, to improve SQ by over 30 percent, commercial banks need to pay attention to CO. In terms of Q2, the rule suggests that each construct’s values must be greater than zero (0); thus, Q2 < 0 suggests the absence of predictive relevance. From Table , all the Q2 values were above 0; signalling that the predictor variables can relevantly predict any change in the exogenous variable (CS). However, SQ (0.224) is a better predictor of CS than CO (0.194); implying that, when both CO and SQ are implemented, the latter predicts any variation in SQ better than the former. Finally, the f2 was also assessed to determine the actual contribution of each exogenous construct (CO and SQ) to the endogenous construct (CS). The rule for assessing f2 suggests that 0.02–0.15 (weak), 0.15–0.35 (medium) and ≥ 0.35 indicates strong (Benitez et al., Citation2020). From Table , both CO (0.207) and SQ (0.114) had medium effects on CS; however, CO had a higher impact on CS than SQ. Simply put, when both CO and SQ are implemented, CO will have a higher effect on CS than SQ.

Table 2. Predictive accuracy, predictive relevance and effect size

5. Estimation of path coefficients

After meeting the quality criteria of the PLS-SEM, the path coefficients were finally estimated to determine whether the hypotheses were supported or rejected. Table presented five columns: structural path, t-stats, p-values, β-values and decision rule. These outcomes were used to discuss three direct effects: (i) CO and CS (ii) CO and SQ (iii) SQ and CS and one mediation effect. In testing for hypotheses using the PLS-SEM, previous studies (Hair et al., Citation2017, Hair & Sarstedt, Citation2021; Sarstedt et al., Citation2021; Wong, et al., Citation2019) have preferred t-stats to p-values; ruling that the t-stat should be > 1.96 (i.e., p < 0.05). Simply put, a directional hypothesis is supported if the t-stat is > 1.96 and vice versa.

Table 3. Structural equation model output and decision rule

The study first hypothesised that: “Customer orientation (CO) has a significant positive effect on Customer Satisfaction (CS) among customers of commercial banks”. From Table , the following outcomes were obtained: t = 7.291, p = 0.00; β = 0.429; thus, with t-stat > 1.96, H1 was supported. This result means that CO has a significant positive effect on CS; thereby, any change in CO will cause a change in CS by 42.9 percent. Also, H2 proposed that, “Customer orientation (CO) has a significant positive effect on service quality (SQ) commercial banks” which was also supported. This is because, the model revealed a T of 18.031 with p of 0.000 and β of 0.626. This result indicates that SQ is significantly and positively affected by CO; with CO contributing about 62.6 percent to any change in SQ. Simply put, SQ can improve by 62.6 percent if commercial banks improve CO. In terms of H3 that SQ significantly and positively improves CS, the following results were obtained: t = 5–688, p = 0.00; β = 0.319. This result shows that SQ directly affect CS; indicating support for H3. Also, Table revealed that any unit change in SQ will lead to a unit change in CS by 0.319. Thus, about 31.9 percent of change in CS is significantly caused by SQ. given these direct effects, it could be argued that, CO has a moderate significant effect on SQ (0.626) and medium effect on CS (0.429); while, SQ also has a medium significant effect on CS (0.319). Deductively, improving CO will lead to significant improvements in SQ by 62.6 percent and CS by 42.9 percent and SQ will subsequently improve CS by 31.9 percent.

5.1. Mediation effect

Table also presented the outcome of the indirect effect to determine whether SQ significantly mediates the relationship between CO and CS (H4). The mediation analysis explains the degree to which the indirect effect (SQ) affects the hypothesised direct paths (CO and CS). As Zhao et al. (Citation2010) recommended, the mediation effect is determined by comparing the significant values of the indirect path directions with their direct paths. From Table , the specific indirect effect results were: t-stat (5.111), p (0.000), and β (0.200) and the direct effect results were: t (7.291) and p (0.000). After comparing these effects, the study found SQ to partially mediate the association between CO and CS. This is because, previous studies (Hair & Sarstedt, Citation2021; Lee et al., Citation2021; Wong, Citation2019) have revealed that a partial mediation effect exists when the t-stats of both the direct and specific indirect effects are significant. Therefore, service quality plays a partial role in the linkage between customer orientation and customer satisfaction.

5.2. Discussion

With respect to the results presented in the previous section, both CO and SQ had significant and positive effects on CS, whereas CO also had a direct and positive effect on SQ. The result for H1, for instance, shows that CO plays a significant role in causing a change in CS, implying that commercial banks in Ghana will experience higher CS if they promote CO. More precisely, if these banks continue to remain customer-oriented by focusing on addressing the needs of their customers, they are highly likely to witness improved customer satisfaction. Previous studies have proven that customers whose needs are met by their banks are highly likely to become satisfied and, invariably, exhibit positive attitudes (Glowa, Citation2014; Gustafsson et al., Citation2015; Murad, Citation2021). Karatepe (Citation2011) rightly pointed out that customer orientation is synonymous with relationship marketing, where businesses focus on developing long-lasting relationships with their clients or customers in order to attain sustainable business outcomes, including customer satisfaction. With Ghana’s banking industry facing customer satisfaction issues since the banking crisis in 2017, the study’s outcome suggests that this challenge could be addressed if commercial banks became more customer-oriented. Customer orientation, according to Fader (2011), entails analysing customer value and immediately focusing marketing actions on the actual consumer segment with high added costs in order to optimise customer attitudes and performance outcomes. This study’s finding has, therefore, been supported by Racela (Citation2014), Machirori and Fatoki (Citation2014), and Wali et al. (Citation2015), who all found CO to significantly improve CS. Wali et al. (Citation2015) specifically concluded that the presence of CO leads to higher CS and invariably improved overall performance.

In terms of H2, the study’s results also revealed that CO significantly affected SQ. This result implies that the services offered by Ghana’s commercial banks could improve if much emphasis is placed on customer orientation. In the service industry, like the banking sector, for instance, the term “quality” is subjective and primarily dependent on the recipients’ (customers’) perceptions or experiences. As such, customers would perceive the services delivered by commercial banks as being of high quality if they addressed their needs or met their expectations. As such, with customer orientation directly focusing on identifying, analyzing, and addressing customers’ needs, it is not surprising to find that it has a positive effect on service quality within the context of Ghana’s banking industry. More precisely, commercial banks that continue to remain customer-focused are highly likely to witness improved service quality. For instance, Zamry and Nayan (Citation2020) proposed three approaches to service quality and concluded that they should be developed in line with customers’ needs and expectations through direct customer involvement. Likewise, Khan et al. (Citation2019) argue that customer orientation is critical for service firms to achieve long-term profitability because it helps banks understand customers’ needs and provides critical information to organisations so they can meet those needs with the right products and services. In like manner, Li et al. (Citation2019) suggested that they tend to provide quality services when they are customer-oriented, with Li et al. (Citation2019) concluding that customer orientation is key to developing service quality in any service organisation. These are clear indications that, when commercial banks in Ghana advance customer orientation, they are highly likely to offer quality services.

Moreover, the study also found service quality (SQ) to directly influence customer satisfaction (CS) at commercial banks in Ghana. This result implies that customers’ levels of satisfaction can improve if more emphasis is placed on service quality. Clearly, customers or clients in Ghana’s banking sector crave quality services; thus, commercial banks that provide them are highly likely to promote customer satisfaction. This result is a clear indication that customer satisfaction will remain low in the absence of service quality; thus, delivering services that meet customers’ expectations is among the steps to winning their hearts, exhibited through satisfaction. Simply put, delivering quality services in areas of tangibility, assurance, reliability, responsiveness, and empathy plays a crucial role in attaining customer satisfaction. For instance, according to Abror et al. (Citation2019), service quality describes a service’s conformity with the customer’s requirements and expectations, and the better the fit, the higher the satisfaction. Similarly, according to Kadir et al. (Citation2017), clients who perceive great service quality are happier and more satisfied. Other studies have buttressed this finding by concluding that service quality plays a phenomenal role in building strong customer satisfaction in the service industry (Bakar et al., Citation2012). Although the study’s findings are not any different from previous outcomes, one can argue that re-echoing the relevance of SQ within the scope of Ghana’s commercial banks would be key to overcoming the recent customer satisfaction challenges, which came about as a result of the banking crisis coupled with the COVID pandemic.

Finally, the study found service quality to partially mediate the relationship between customer orientation and customer satisfaction in the banking sector of Ghana. This result implies that the effect of customer orientation on customer satisfaction still exists, but in a smaller proportion, and that service quality partially mediates this relationship. The result also implies that commercial banks in Ghana can promote customer satisfaction among their customers if they embrace customer orientation and service quality. Simply put, better service quality is needed to strengthen customer orientation in order to increase customer satisfaction levels by 20 percent. This result clearly indicates that commercial banks can improve the satisfaction levels of their customers by 20 percent if they invest in service quality and better customer orientation. The study’s findings are in line with assertions by Khen et al. (Citation2010), Li et al. (Citation2019), and Rai and Medha (Citation2013). It is noted that, although Li et al.’s (Citation2019) findings are similar to those of this study, some differences exist. This is because Li et al. (Citation2019) found a full mediation effect, while this present study found a partial mediation effect. Arguably, this difference in findings could arise from differences in the geographical settings of these two studies. Regardless, these studies revealed that SQ plays a significant mediating role in the correlation between CO and CS. However, the study’s finding was contrasted by Aburayya et al. (Citation2020), who found SQ to have no indirect role in the link between CO and CS. The authors concluded that only a direct relationship can be found between CO and CS without necessarily passing through SQ. In this light, the study suggested that commercial banks can strengthen the relationship between CO and CS through SQ.

The study demonstrates that customer orientation is a critical factor in predicting customer satisfaction and that rising service standards in the banking industry would result in higher customer satisfaction. Particularly in emerging areas, the significance of service quality in this connection is unique. Because it evaluates quality from the standpoint of the consumer, it adds to the body of research on bank marketing. Relationship managers and marketing managers will benefit from the study. It offers methods for influencing the behaviour of bank clients.

The study demonstrates that customer orientation is a critical factor in predicting customer satisfaction and that rising service standards in the banking industry would result in higher customer satisfaction. Particularly in emerging areas, the significance of service quality in this connection is unique. Because it evaluates quality from the standpoint of the consumer, it adds to the body of research on bank marketing. Relationship managers and marketing managers will benefit from the study. It offers methods for influencing the behaviour of bank clients.

6. Conclusions

The study investigated the effects of CO on CS, with SQ playing a mediating role within the context of Ghana’s banking industry. It specifically tested four hypotheses, which were largely achieved. In terms of H1, for instance, the study found CS to be significantly influenced by CO, implying that CO plays a crucial role in improving CS. In view of this, the study concluded that CO is a key predictor of CS within the Ghanaian banking industry. With respect to H3, the study revealed that SQ directly affects CS, implying that CS would improve if SQ improved and vice versa. It was concluded that commercial banks that emphasise service quality in areas of responsiveness, empathy, and tangibility are likely to achieve higher satisfaction levels among their customers.

Finally, after testing H4, it was revealed that SQ partially mediates the relationship between CO and CS. It was concluded that SQ plays a partial role in the relationship between CO and CS within the banking sector of Ghana. More precisely, SQ is responsible for part of the linkage between CO and CS.

7. Practical implications

Policymakers should develop comprehensive policies and also direct the management of commercial banks to develop customer orientation programmes in order to improve the current customer satisfaction levels in the banking industry. Also, management should continue to adopt new ways of improving customer orientation in order to attain higher customer satisfaction. For instance, more accessible platforms could be provided to customers to help them channel their grievances and opinions to management, which should in turn provide timely and appropriate feedback to the customers. Management should also provide customer-designed products and services that directly meet customers’ expectations and needs. Furthermore, the PLS-SEM output found CO to significantly and positively affect SQ, implying that CO is a valuable contributor to SQ. It was specifically concluded that commercial banks in Ghana can improve their current services by embracing CO. Simply put, understanding customers’ needs is critical for Ghana’s commercial banks, as it allows them to identify a market niche and fill that niche with the proper items to achieve perceived service quality. The study recommends that more customer-oriented policies, practices, and packages should be implemented in order to meet the perceived service quality of customers in the banking industry. In terms of practice, for instance, commercial banks should engage customers in knowledge, information, and other resource sharing. They should also establish clear contact with customers through proper communication channels in order to build long-lasting relationships and subsequently promote service quality.

In addition, the study recommended that the management of the commercial banks should continue to invest in activities that directly improve the quality of the services they currently deliver. More precisely, investing in sophisticated technologies would improve the overall quality of services (responsiveness, tangibility) rendered by these banks, thereby promoting customer satisfaction. Also, management should ensure that the services being delivered in the banking industry are perceived as high quality and customer-friendly, thus meeting customers’ expectations and, invariably, satisfaction levels.

Finally, the study suggests that commercial banks in Ghana can improve the satisfaction levels of their customers by emphasising customer orientation and service quality. This can be achieved by ensuring that the services delivered by the commercial banks are streamlined to meet customers’ needs. By doing so, customers would tend to exhibit positive attitudes such as satisfaction, commitment, and, invariably, loyalty. More practically, the management of these banks should ensure that their products and services are customer-oriented, that is, directly aimed at meeting customers’ expectations in order to improve satisfaction. For instance, service quality can be improved by providing quality customer complaint management, identifying customer needs, developing staff skills, investing in technology, and ensuring continuous service improvement. The study, therefore, concludes that customer satisfaction in the banking industry of developing economies like Ghana can be improved if commercial banks emphasise customer orientation through service quality.

8. Suggestions for further research

Although the study’s purpose was largely achieved, a little more can be done to boost the overall literature on the subject matter. In terms of geographical limitation, the study focused on some selected commercial banks in Ghana; thus, generalising findings across all commercial banks in the country and other developing economies should be done with caution. Given this, future research could take a more broad-based approach to their studies, incorporating other commercial banks in Ghana and/or other emerging economies. Also, further research could employ the mixed methods approach in order to obtain both qualitative and quantitative data to improve current findings.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Eric Gonu

Eric Gonu is a lecturer in the department of marketing and supply chain management, University of Cape Coast, Ghana. He holds a Doctor of Philosophy in Business Administration. His area of specialisation is Marketing. His research interests are in the areas of service quality management, customer relationship management, customer service, service marketing and relationship marketing.

References

- Abror, A., Patrisia, D., Engriani, Y., Evanita, S., Yasri, Y., & Dastgir, S. (2019). Service quality, religiosity, customer satisfaction, customer engagement and Islamic bank’s customer loyalty. Journal of Islamic Marketing, 11(6), 1691–20. https://doi.org/10.1108/JIMA-03-2019-0044

- Aburayya, A., Marzouqi, A., Alawadhi, D., Abdouli, F., & Taryam, M. (2020). An empirical investigation of the effect of employees’ customer orientation on customer loyalty through the mediating role of customer satisfaction and service quality. Management Science Letters, 10(10), 2147–2158. https://doi.org/10.5267/j.msl.2020.3.022

- Ali, B. J., Saleh, P. F., Akoi, S., Abdulrahman, A. A., Muhamed, A. S., Noori, H. N., & Anwar, G. (2021). Impact of service quality on the customer satisfaction: Case study at online meeting platforms. International Journal of Engineering, Business and Management, 5(2), 65–77. https://doi.org/10.22161/ijebm.5.2.6

- Ali, R., Wahyu, F. R. M., Darmawan, D., Retnowati, E., & Lestari, U. P. (2022). Effect of Electronic Word of Mouth, Perceived Service Quality and Perceived Usefulness on Alibaba's Customer Commitment. Journal of Business and Economics Research (JBE), 3(2), 232–237. https://doi.org/10.47065/jbe.v3i2.1763

- Al Samman, A. M., & Mohammed, A. T. I. (2020). The mediating role of job satisfaction and affective commitment in the relationship between internal marketing practices and customer orientation. International Journal of Organizational Analysis. https://doi.org/10.1108/IJOA-06-2020-2254

- Anabila, P., Kastner, A. N. A., Bulley, C. A., & Allan, M. M. (2020). Market orientation: A key to survival and competitive advantage in Ghana’s private universities. Journal of Marketing for Higher Education, 30(1), 125–144. https://doi.org/10.1080/08841241.2019.1693474

- Ang, Y. S., Lee, V. H., Tan, B. I., & Chong, A. Y. L. (2011). The impact of TQM practices on learning organisation and customer orientation: A survey of small service organisations in Malaysia. International Journal of Services, Economics and Management, 3(1), 62–77. https://doi.org/10.1504/IJSEM.2011.037178

- Aryeetey, E. (2008). From informal finance to formal finance in Sub-Saharan Africa: Lessons from linkage efforts. AERC/IMF African Finance for the 21st Century Unpublished Manuscript. https://www.researchgate.net/profile/Ernest-Aryeetey/publication/254264799_From_Informal_Finance_to_Formal_Finance_in_Sub-Saharan_Africa_Lessons_from_Linkage_Efforts/links/54427fae0cf2a6a049a8991d/From-Informal-Finance-to-Formal-Finance-in-Sub-Saharan-Africa-Lessons-from-Linkage-Efforts.pdf

- Babin, B. J., Hair, J. F., & Boles, J. S. (2008). Publishing research in marketing journals using structural equation modeling. Journal of Marketing Theory and Practice, 16(4), 279–286. https://doi.org/10.2753/MTP1069-6679160401

- Bakar, A. H. A., Tabassi, A. A., Razak, A. A., & Yusof, M. N. (2012). Key factors contributing to growth of construction companies: A Malaysian experience. World Applied Sciences Journal, 19(9), 1295–1304. https://doi.org/10.5829/idosi.wasj.2012.19.09.1454

- Bamfo, B. A., Dogbe, C. S. K., Osei-Wusu, C., & Wright, L. T. (2018). The effects of corporate rebranding on customer satisfaction and loyalty: Empirical evidence from the Ghanaian banking industry. Cogent Business & Management, 5(1), 1413970. https://doi.org/10.1080/23311975.2017.1413970

- Bank of Ghana [BoG] (2017). Annual report. Accra, Ghana: BoG.

- Benitez, J., Henseler, J., Castillo, A., & Schuberth, F. (2020). How to perform and report an impactful analysis using partial least squares: Guidelines for confirmatory and explanatory is research. Information & Management, 57(2), 103168. https://doi.org/10.1016/j.im.2019.05.003

- Boateng, F., Adesi, M., Yeboah, E., Oduro, L. M., & Sackey, M. M. (2021). Customer satisfaction and customer loyalty in the post-crisis banking sector of Ghana. Journal of Marketing and Consumer Research, 76, 04–76. https://www.researchgate.net/profile/Frank-Boateng-2/publication/349735116_Customer_Satisfaction_and_Customer_Loyalty_in_the_Post-Crisis_Banking_Sector_of_Ghana/links/603fb0ce299bf1e07854194a/Customer-Satisfaction-and-Customer-Loyalty-in-the-Post-Crisis-Banking-Sector-of-Ghana.pdf

- Choi, E. K., & Joung, H. W. (2017). Employee job satisfaction and customer-oriented behavior: A study of frontline employees in the foodservice industry. Journal of Human Resources in Hospitality & Tourism, 16(3), 235–251. https://doi.org/10.1080/15332845.2017.1253428

- Creswell, J. W., & Plano-Clark, V. (2018). Designing and conducting mixed methods research. Sage Publication. 3ed.

- Cronin, J. J., Jr, & Taylor, S. A. (1992). Measuring service quality: A re-examination and extension. Journal of Marketing, 56(3), 55–68. https://doi.org/10.1177/002224299205600304

- Dam, S. M., & Dam, T. C. (2021). Relationships between service quality, brand image, customer satisfaction, and customer loyalty. The Journal of Asian Finance, Economics and Business, 8(3), 585–593. https://doi.org/10.13106/jafeb.2021.vol8.no3.0585

- Dhingra, S., Gupta, S., & Bhatt, R. (2020). A study of relationship among service quality of E-commerce websites, customer satisfaction, and purchase intention. International Journal of E-Business Research (IJEBR), 16(3), 42–59. https://doi.org/10.4018/IJEBR.2020070103

- Fader, P. (2020). Customer centricity: Focus on the right customers for strategic advantage. Wharton digital press.

- Farrell, A. M., Souchon, A. L., & Durden, G. R. (2001). Service encounter conceptualisation: Employees’ service behaviours and customers’ service quality perceptions. Journal of Marketing Management, 17(5–6), 577–593. https://doi.org/10.1362/026725701323366944

- F. Hair, J., Jr., Sarstedt, M., Hopkins, L., Kuppelwieser, G., & V. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review, 26(2), 106–121. https://doi.org/10.1108/EBR-10-2013-0128

- Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. John Wiley and Sons.

- Garrido-Moreno, A., & Padilla-Meléndez, A. (2011). Analyzing the impact of knowledge management on CRM success: The mediating effects of organizational factors. International Journal of Information Management, 31(5), 437–444. https://doi.org/10.1016/j.ijinfomgt.2011.01.002

- Glowa, T. (2014). Measuring customer satisfaction: Exploring customer satisfaction’s relationship with purchase behaviour. BookBaby.

- Gong, T., & Yi, Y. (2018). The effect of service quality on customer satisfaction, loyalty, and happiness in five Asian countries. Psychology & Marketing, 35(6), 427–442. https://doi.org/10.1002/mar.21096

- Gustafsson, A., Johnson, M. D., & Inger, R. (2015). The effects of customer satisfaction, relationship commitment dimensions, and triggers on customer retention. American Marketing Association, 13(2), 12–29. https://doi.org/10.1509/jmkg.2005.69.4.210

- Hair, E., Halle, T., Terry-Humen, E., Lavelle, B., & Calkins, J. (2006). Children's school readiness in the ECLS-K: Predictions to academic, health, and social outcomes in first grade. Early Childhood Research Quarterly, 21(4), 431–454. https://doi.org/10.1016/j.ecresq.2006.09.005

- Hair, J. F., Hult, G. T. M., Ringle, C. M., Sarstedt, M., & Thiele, K. O. (2017). Mirror, mirror on the wall: A comparative evaluation of composite-based structural equation modeling methods. Journal of the Academy of Marketing Science, 45(5), 616–632. https://doi.org/10.1007/s11747-017-0517-x

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2012). Partial least squares: The better approach to structural equation modeling? Long Range Planning, 45(5–6), 312–319.Hair. et al., 2014. https://doi.org/10.1016/j.lrp.2012.09.011.

- Hair, J. F., Jr, & Sarstedt, M. (2021). Data, measurement, and causal inferences in machine learning: Opportunities and challenges for marketing. Journal of Marketing Theory and Practice, 29(1), 65–77. https://doi.org/10.1080/10696679.2020.1860683

- Hair, J. F., Jr, Sarstedt, M., Matthews, L. M., & Ringle, C. M. (2016). Identifying and treating unobserved heterogeneity with FIMIX-PLS: Part I–method. European Business Review, 28(1), 63–76. https://doi.org/10.1108/EBR-09-2015-0094

- Hapsari, R., Clemes, M., & Dean, D. (2016). The mediating role of perceived value on the relationship between service quality and customer satisfaction: Evidence from Indonesian airline passengers. Procedia Economics and Finance, 35, 388–395. https://doi.org/10.1016/S2212-5671(16)00048-4

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hensler, J., Ringle, M. C., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Herhausen, D. (2011). Understanding proactive customer orientation: Construct development and managerial implications. Springer Science & Business Media.

- Homburg, C., Müller, M., & Klarmann, M. (2011). When does salespeople’s customer orientation lead to customer loyalty? The differential effects of relational and functional customer orientation. Journal of the Academy of Marketing Science, 39(6), 795–812. https://doi.org/10.1007/s11747-010-0220-7

- Jiang, W., Li, J., Yan, H., Li, H., & Chen, M. (2019). Customer orientation and success in introduction of new products: An empirical study in an emerging economy. Journal of Business & Industrial Marketing, 35(2), 306–317. https://doi.org/10.1108/JBIM-11-2018-0361

- Kadir, A. R., Kamariah, N., & Saleh, A. (2017). The effect of role stress, job satisfaction, self-efficacy and nurses’ adaptability on service quality in public hospitals of Wajo. International Journal of Quality and Service Sciences. https://doi.org/10.1108/IJQSS-10-2016-0074

- Karatepe, O. M. (2011). Service quality, customer satisfaction and loyalty: The moderating role of gender. Journal of Business Economics & Management, 12(2), 278–300. https://doi.org/10.3846/16111699.2011.573308

- Karatepe, O. M. (2011). Service quality, customer satisfaction and loyalty: The moderating role of gender. Journal of Business Economics & Management, 12(2), 278–300. https://www.ceeol.com/search/article-detail?id=330255

- Khadka, K., & Maharjan, S. (2017). Customer satisfaction and customer loyalty. Unpublished master’s thesis, Department of Business Management, Centria University of Applied Sciences.

- Khan, M. A., Zubair, S. S., & Malik, M. (2019). An assessment of e-service quality, e-satisfaction and e-loyalty. South Asian Journal of Business Studies, 8(3), 283–302. https://doi.org/10.1108/SAJBS-01-2019-0016

- Kheng, L. L., Mahamad, O., & Ramayah, T. (2010). The impact of service quality on customer loyalty: A study of banks in Penang, Malaysia. International Journal of Marketing Studies, 2(2), 57. www.shorturl.at/nxBWX

- Kohli, A. K., & Jaworski, B. J. (1990). Market orientation: The construct, research propositions, and managerial implications. Journal of Marketing, 54(2), 1–18. https://doi.org/10.1177/002224299005400201

- Körner, M., Wirtz, M. A., Bengel, J., & Göritz, A. S. (2015). Relationship of organisational culture, teamwork and job satisfaction in interprofessional teams. BMC Health Services Research, 15(1), 243. https://doi.org/10.1186/s12913-015-0888-y

- Kotler, P. R. (2007). Principles of Marketing. 12. Publisher: Prentice Hall.

- Latyshova, L. S., Syaglova, Y. V., & Oyner, O. K. (2015, October). The customer–oriented approach: The concept and key indicators of the customer driven company. DIEM: Dubrovnik International Economic Meeting, 2(1), 637–645. https://hrcak.srce.hr/161648

- Latyshova, L. S., Syaglova, Y. V., & Oyner, O. K. (2015, October). The customer–oriented approach: The concept and key indicators of the customer driven company. DIEM: Dubrovnik International Economic Meeting, 2(1), 637–645.

- Lee, C. M. J., Che-Ha, N., & Alwi, S. F. S. (2021). Service customer orientation and social sustainability: The case of small medium enterprises. Journal of Business Research, 122, 751–760. https://doi.org/10.1016/j.jbusres.2019.12.048

- Leninkumar, V. (2017). An n investigation on the relationship between service quality and customer loyalty: A mediating role of Customer satisfaction. Archives of Business Research, 5(5), 1–23. https://doi.org/10.14738/abr.55.3152

- Li, W., Pomegbe, W. W. K., Dogbe, C. S. K., & Novixoxo, J. D. (2019). Employees’ customer orientation and customer satisfaction in the public utility sector: The mediating role of service quality. African Journal of Economic and Management Studies, 10(4), 408–423. https://doi.org/10.1108/AJEMS-10-2018-0314

- Machirori, T., & Fatoki, O. (2014). An empirical investigation into the extent of customer satisfaction and customer loyalty at big retail stores in King William’s Town, South Africa (Electronic version). African Journal of Business Management, 8(4), 7665–7673. https://doi.org/10.5897/AJBM11.1491

- Majava, J., Nuottila, J., Haapasalo, H., & Law, K. M. (2014). Customer needs in market-driven product development: Product management and R&D standpoints. Technology and Investment, 2(2), 45–61. https://doi.org/10.4236/ti.2014.51003

- Meesala, A., & Paul, J. (2018). Service quality, consumer satisfaction and loyalty in hospitals: Thinking for the future. Journal of Retailing and Consumer Services, 40, 261–269. https://doi.org/10.1016/j.jretconser.2016.10.011

- Memon, M. A., Ramayah, T., Cheah, J. H., Ting, H., Chuah, F., & Cham, T. H. (2021). PLS-SEM statistical programs: A review. Journal of Applied Structural Equation Modeling, 5(1), 1–14. https://doi.org/10.47263/JASEM.5(1)06

- Murad, S. (2021). The effect of E-Retail on customer satisfaction: case study from Jordan. Turkish Journal of Computer and Mathematics Education (TURCOMAT), 12(5), 989–999. https://doi.org/10.17762/turcomat.v12i5.1743

- Naik, C. K., Gantasala, S. B., & Prabhakar, G. V. (2010). Service quality (SERVQUAL) and its effect on customer satisfaction in retailing. European Journal of Social Sciences, 16(2), 231–243. https://d1wqtxts1xzle7.cloudfront.net/33058318/chat_luong_dich_vu_va_su_hai_long_cua_dv_ban_le-libre.pdf?1393951193=&response-content-disposition=inline%3B+filename%3DService_Quality_Servqual_and_its_Effect.pdf&Expires=1672695744&Signature=WKIdkieXQEly2naX3yX9JcjyNEWRzhcPKJxfy4e9OPT9k-~CyPeW2CJgpkiURQfbe1pzPA1uPGjYf-RA507eHirWefr99PuDtUGujvKwBPIJzlY6tYKUQa~etnimvG4qkztEBu5Prx-fANNCmeBq~7UGL3dpbEc1DLFLc18CSua1dJhKvVhOJw3iSTuQbbc1g0MvBGJLh3IuhL0JApsLusEgu4obeTcfU9SnPFe5c19WqAp0xGo6sfKJRd9i~kICAa~l7ARa2ZrDZ5tlKpJ8QINWnmiEBQRBgPAyq7pLl4m38eGUr5~8rOSSdjg2I8Flow2gx4KO5SJ-MXB4PPf8eQ__&Key-Pair-Id=APKAJLOHF5GGSLRBV4ZA

- Nurfarida, I. N., Sarwoko, E., & Arief, M. (2021). The impact of social media adoption on customer orientation and SME performance: An empirical study in Indonesia. The Journal of Asian Finance, Economics and Business, 8(6), 357–365. https://doi.org/10.13106/jafeb.2021.vol8.no6.0357

- Nwanji, T. I., Howell, K. E., Faye, S., Otekunrin, A. O., Eluyela, D. F., Lawal, A. I., & Eze, S. C. (2020). Impact of foreign direct investment on the financial performance of listed deposit banks in Nigeria. International Journal of Financial Research, 11(2), 323. https://doi.org/10.5430/ijfr.v11n2p323

- Parasuraman, A., Zeithaml, V. A., & Berry, L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 60(1), 12–40. file:///C:/Users/HP%20ELITE%20X2/Downloads/Escala%20Servqual%20-%20Journal%20of%20Retailing.pdf

- Racela, O. C. (2014). Customer orientation, innovation competencies, and firm performance: A proposed conceptual model. Procedia-Social and Behavioral Sciences, 148, 16–23. https://doi.org/10.1016/j.sbspro.2014.07.010

- Rai, A. K., & Medha, S. (2013). The antecedents of customer loyalty: An empirical investigation in life insurance context. Journal of Competitiveness, 5(2), 139–163. https://doi.org/10.7441/joc.2013.02.10

- Robledo, M. A. (2001). Measuring and managing service quality: Integrating customer expectations. Managing Service Quality: An International Journal, 11(1), 22–31. https://doi.org/10.1108/09604520110379472

- Sarstedt, M., Ringle, C. M., & Hair, J. F. (2021). Partial least squares structural equation modeling. In Handbook of market research (pp. 587–632). Cham: Springer International Publishing. https://doi.org/10.1007/978-3-319-57413-4_15

- Segoro, W., & Elvira, L. (2021). The effect of marketing strategy and service quality on customer satisfaction and its impact on customer loyalty of BJB bank in bekasi. In 5th Global Conference on Business, Management and Entrepreneurship (GCBME 2020) (pp. 560–564). Atlantis Press.

- Slater, S. F., & Narver, J. C. (1998). Customer‐led and market‐oriented: Let’s not confuse the two. Strategic Management Journal, 19(10), 1001–1006. https://doi.org/10.1002/(SICI)1097-0266(199810)19:10<1001::AID-SMJ996>3.0.CO;2-4

- Steinman, C., Rohit, D., & John, U. F. (2000). Beyond market orientation: When customers and suppliers disagree. Journal of the Academy of Marketing Science, 28(1), 109–119. https://doi.org/10.1177/0092070300281010

- Sultan, P., & Wong, H. Y. (2010). Service quality in higher education–a review and research agenda. International Journal of Quality and Service Sciences, 2(2), 259–272. https://doi.org/10.1108/17566691011057393

- Taleghani, M., Gilaninia, S., & Mousavian, S. J. (2011). The role of relationship marketing in customer orientation process in the banking industry with focus on loyalty (case study: Banking industry of Iran). International Journal of Business and Social Science, 2(19), 1–16. file:///C:/Users/HP%20ELITE%20X2/Downloads/5y1.org_263f4ba0513c892551cfbb72d30bccb4.pdf

- Tse, D. K., & Wilton, P. C. (1988). Models of consumer satisfaction formation: An extension. Journal of Marketing Research, 25(2), 204–212. https://doi.org/10.1177/002224378802500209

- Ullman, J. B., & Bentler, P. M. (2012). Structural equation modeling. Handbook of Psychology, Second Edition, 2. https://doi.org/10.1002/9781118133880.hop202023

- Wali, F., Wright, T., Nwokah, G., & Reynolds, L. (2015). Customer relationship management and service quality: Aqualitative study.European Academy of Management (EURAM) Conference, 17th - 20th June, 2015, Kozminski University, Warsaw Poland. Retrieved July 21, 2018, from http://eprints.hud.ac.uk/25053

- Wibawa, I. G. N. R. S., & Sukaatmadja, I. P. G. (2018). The effect of customer orientation of service employee in building customer retention in X Company Bali. IOSR Journal of Business and Management, 20(2), 1–21. https://doi.org/10.9790/487X-2007022127

- Wong, S. C., Lim, J. Y., Lim, C. S., & Hong, K. T. (2019). An Empirical Study on Career Choices Among Undergraduates: A PLS-SEM Hierarchical Component Model (HCM) Approach. International Journal of Human Resource Studies, 9I(2), 276–298. https://doi.org/10.5296/ijhrs.v9i2.14841

- Yavas, U., Karatepe, O. M., & Babakus, E. (2011). Do customer orientation and job resourcefulness moderate the impact of interrole conflicts on frontline employees’ performance? Tourism and Hospitality Research, 11(2), 148–159. https://doi.org/10.1057/thr.2010.25

- Zamry, A. D., & Nayan, S. M. (2020). What is the relationship between trust and customer satisfaction? Journal of Undergraduate Social Science and Technology, 2(2), 1–16. https://abrn.asia/ojs/index.php/JUSST/article/view/76

- Zeithaml, V. A., Berry, L. L., & Parasuraman, A. (1996). The behavioral consequences of service quality. Journal of Marketing, 60(2), 31–46. https://doi.org/10.1177/002224299606000203

- Zeithaml, B., Bitner, M. J., & Gremler, J. (2006). . Service Marketing: Integrating Customer Focus across the Firm (Vol. 4, pp.56–87). Boston, MA: McGraw-Hill/Irwin. https://library.wur.nl/WebQuery/clc/1809666

- Zhao, X., Lynch, J. G., Jr., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and truths about mediation analysis. The Journal of Consumer Research, 37(2), 197–206. https://doi.org/10.1086/651257