?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We focus on firms’ risk-taking for customers and investigate how this type of risk-taking is influenced by “performance relative to aspiration” (PRA). Specifically, we examine the PRA and project-financing (PF) loan activities of all 79 savings banks in South Korea from 2013 to 2021. Contrary to the prevalent prediction that risk-taking increases with negative PRA, we demonstrate that banks with a more positive PRA take higher risk through PF loans. This suggests that a more positive PRA has given banks the freedom of action to pursue a social-based goal of small business support, which has been neglected by management as less important than their most important goal of pursuing their own profit. Furthermore, unlike the dominant idea that family firms are more risk-averse than non-family firms, we find that when PRA is positive, family firms engage in risky actions more actively for their customers than non-family counterparts. In other words, banks with better PRA take more risk to provide financial opportunities to their customers and this type of risk-taking is more pronounced for family firms. Implications and future research are discussed.

1. Introduction

Scholars in the strategic management have been interested in whether and how firms take varying degrees of risks in response to “performance relative to aspiration” (PRA) (P. Bromiley et al., Citation2001; P. H. I. L. I. P. Bromiley & Rau, Citation2010; Schumacher et al., Citation2020; Smulowitz et al., Citation2020). Specifically, prior studies argue that, when performance is above aspirations (positive PRA), firms place more emphasis on proven strategic actions that lead to such good performance, while when performance is below aspirations (negative PRA), they explore new strategic ones to improve poor performance (Cyert & March, Citation1963; Dong, Citation2021; Eggers & Suh, Citation2019; Gaba et al., Citation2022; Greve & Gaba, Citation2017; March & Simon, Citation1958; Xie et al., Citation2019). As a result, scholars predict that when performance is below aspirations, firms’ risk-taking becomes generally greater, whereas when performance is above aspirations, firms’ risk-taking decreases (Lim & Mccann, Citation2013; P. Bromiley, Citation1991; Palmer & Wiseman, Citation1999; Singh, Citation1986; Smulowitz et al., Citation2020; Wiseman & Bromiley, Citation1996).

However, while existing studies provide an excellent insight into how firms’ risk-taking will be in response to PRA, they have analyzed the behavior of risk-taking primarily with the logic of profit maximization. In other words, the existing prediction that risk-taking increases when performance is below aspirations is heavily based on the idea that firms take risks to pursue their own profit through the improvement of performance (Hoskisson et al., Citation2017). Accordingly, there is a lack of sufficient recognition among existing literature that firms take risks for the benefits of customers and, more importantly, that firms will then respond differently to PRA by changing their willingness to take risks.

This study focuses on the firms’ risk-taking for their customers, which has been overlooked in prior studies. Specifically, if firms’ motivation for risk-taking is closer to benefitting their customers rather than themselves, how is this type of risk-taking related to PRA? Furthermore, does the relationship between risk-taking and PRA vary by the type of corporate ownership? In particular, how will the unique strategic characteristics of family firms, compared to non-family firms, affect the relationship between risk-taking for customers and PRA?

We argue that firms’ risk-taking increases when PRA is positive, contrary to existing predictions. To empirically test this argument, we investigated the PRA and project-financing (PF) loan activities of entire 79 savings banks in South Korea from 2013 to 2021. PF loans are business loans that savings banks provide to small and medium-sized enterprises (SMEs) with high future potential, despite their current weak performance. PF loan is one of the most dangerous loans managed by savings banks because while several types of collateral are possible in PF loans in certain countries, such as Spain (Bros & Vivas, Citation2019), PF loans in South Korea are made only with business potential, that is, future cash-flows, without collateral. Thus, if a borrower construction company declares bankruptcy, it is impossible for savings banks in South Korea to recover the loan, resulting in enormous financial losses. Thus, by lending money without collateral, banks take a substantial risk in order to provide their customers with financial opportunities for future growth. Due to the nature of PF loans, banks that put their own interests first do not actively participate in PF loans by rejecting most PF loan requests from SME customers.

Under these circumstances, our results show that the greater the positive PRA, the more active the banks’ participation in PF loans. In other words, contrary to the prevalent prediction that risk-taking increase when PRA is negative, banks with a greater positive PRA take rather higher risks through more engagement in dangerous PF loans. This suggests that a greater positive PRA has given banks the freedom (or leeway) of action to pursue a social-based goal of small business support, which has been neglected by management as less important than their most important goal of pursuing their own profit. And the freedom resulting from positive PRA make banks more willing to take risks to provide financial opportunities to their SME customers. Furthermore, contrary to the dominant idea that family firms are more risk-averse than non-family firms, the results demonstrate that the positive relationship between positive PRA and PF loans becomes more pronounced for family-owned savings banks. This suggests that when performance is above aspirations, family firms’ unique strategic characteristics makes family firms take more risks for their customers than non-family firms to enhance their long-term non-financial value such as social reputation, honor and customer loyalty.

In this respect, this study makes several important contributions to relevant literatures. First, this study contributes to the literature on behavioral theory of the firm (BTOF) by suggesting that the relationship between risk-taking and PRA may vary depending on the strategic value a firm pursues through risk-taking. Specifically, this study suggests that we need to study various motive of risk-taking other than the pursuit of own profit and whether and how these different types of risk-taking exhibit diverse relationships with PRA. Second, this study contributes to the literature on family business by suggesting that if family firms perceive that they can enhance their long-term non-financial value by undertaking risks, they engage in risky actions more actively than their non-family counterparts do.

2. Theory and hypotheses

2.1. Positive PRA and firms’ risk-taking for the benefit of customers

In general, strategic management scholars have analyzed firms’ risk-taking mainly through the lens of maximization of economic interest (Hoskisson et al., Citation2017). In particular, when performance is lower than aspirations, firms engage in risky activities with uncertain outcomes to turn around unacceptable financial performance or improve their economic position relative to other firms (P. Bromiley, Citation1991; Singh, Citation1986; Smulowitz et al., Citation2020). On the other hands, when performance is higher than aspirations, firms seek stability by adhering to proven strategic actions that lead to such good performance, thereby lowering their risk-taking (Lim & Mccann, Citation2013; Palmer & Wiseman, Citation1999). However, while the pursuit of profit is admittedly the most important goal of firms, the extant literature has not paid sufficient attention to the various potential motives of firms’ risk-taking and, more importantly, to the possibility that firms respond differently to PRA depending on the strategic value they pursue through risk taking.

Nowadays, an increasing number of companies are increasing their business activities not only for themselves but also for other stakeholders such as customers, local suppliers, and employees (Wickert & Risi, Citation2019). For example, firms seek to support local community by forming partnerships with local businesses in which they are located, instead of maximizing their individual profits by working with the most competitive outside partners (Govindan et al., Citation2018). In addition, many firms make substantial social investments (e.g., building local libraries, donating to schools, and protecting the environment), which are less directly related to immediate financial profit (Carroll & Brown, Citation2018). Considering the increasing number of altruistic behaviors of firms, under what circumstances will firms’ risk-taking stand out the most when such actions are more for their customers’ benefit than themselves?

Regarding this, contrary to existing arguments, we argue that firms will increase their risk-taking, especially when performance is above aspirations (that is, positive PRA). First of all, firms have no choice but to allocate their valuable resources and capabilities to different goals based on their strategic importance (Hutchison-Krupat & Kavadias, Citation2015). In a situation where there are severe competitions in the markets and strategic resources are limited, firms must use their scarce resources and capabilities in achieving more strategically important goals. The most strategically important objective for a company is the pursuit of its own profit above all else. The pursuit of profit is the fundamental reason that a company was born and is the only way to make it sustainable. Of course, firms’ strategic decisions to pursue the benefit of customers or local communities can also greatly enhance their competitiveness in the long run. Prior studies empirically demonstrate that firms’ active pursuit of customer value can increase their long-term market performance by improving their reputation and customer loyalty (e.g., Reimann et al., Citation2010). However, while firms’ decision to pursue customer benefits can be conducive to their long-term competitiveness, pursuing customer value is not a high strategic priority from a firm’s viewpoint because it has no direct relevance to its immediate profits.

Thus, firms first spend their scarce resources and capabilities on the goals they deem most important among their strategic priorities; once they achieve these goals to some extent, they can then increase efforts towards their next important strategic goals (Greve & Gaba, Citation2017; Greve, Citation2008). When actual performance is higher than aspirations, management can interpret this as a sign that they have substantially achieved their most important goal of pursuing profits. Therefore, when PRA is positive, firms then tend to increase efforts towards achieving strategic objectives that have lower strategic priority, such as pursuing consumer value. In other words, exceeding a primary financial goal allows firms to marginally increase their devotion to secondary objectives (Cyert & March, Citation1963; Greve, Citation2008). Hence, a positive PRA gives companies the freedom to pursue a less important objective in their strategic priorities; in our case, this means accommodates the demands of customers. Essentially, compared to firms without a positive PRA, those with a positive PRA have more freedom and are more likely to be willing to take risks for customers’ benefit.

The positive relationship between positive PRA and risk-taking for customers can also be explained in terms of corporate social legitimacy rather than strategic priority logic. If firms today ignore the expectations of the business community and act only in their own interests (i.e., based solely on their own financial consideration), they are condemned by many social stakeholders as vicious companies (Fernando & Lawrence, Citation2014; Jeong & Kim, Citation2019). Or they may even lose legitimacy and be expelled from the community. Thus, an increasing number of firms are trying to maintain their legitimacy by taking social responsibility and accommodating the demands of various stakeholders. However, if the firm is too faithful to the needs of its stakeholders to be recognized for its legitimacy, such as being too obedient to social demands, the efficiency of the firm will be ignored and the viability of the firm may be threatened. Indeed, if a company is too engrossed in meeting social demands, the capital and resources required for research and development (R&D) investment decrease, reducing the firm’s competitiveness (Merkelsen, Citation2011).

Then, the most effective way to pursue economic efficiency and gain legitimacy from stakeholders (e.g., consumers) is to actively respond to social demands when the firm has financial leeway. When a firm is struggling financially, its legitimacy will not be greatly undermined by its stakeholders, even if the firm pays less attention to social demands because stakeholders are well aware that the survival of a firm comes first. However, if firms only pursue their own profits, not social value, even in a financially viable situation, their legitimacy will be greatly undermined by stakeholders. This is especially true for customers because firms generate most profits from them. Therefore, when PRA is positive, firms try to protect their legitimacy by more actively accommodating social demands. Consequently, this increases firms’ willingness to take risks for customer benefits.

From the above discussion, we propose our first hypothesis as follows.

Hypothesis 1:

There is a positive relationship between positive PRA and firms’ risk-taking for the benefits of customers.

2.2. The moderating role of familiness on the relationship between positive PRA and firms’ risk-taking for customers

In the second hypothesis, we predict that the positive relationship between positive PRA and firms’ risk-taking for customer will vary according to the type of corporate ownership. Strategic management scholars have long argued that corporate ownership can affect not only how firms operate but also the value they ultimately pursue, thereby affecting their strategic choices (e.g., Baysinger et al., Citation1991; Denis et al., Citation1999). The decision to take risks to accommodate customer demands is clearly an important strategic choice for management. This study argues that such an important strategic choice by firms, risk-taking for the benefit of customers, can be greatly influenced by the type of corporate ownership. In other words, we strongly believe that unique strategic characteristics of family firms compared to non-family counterparts make family firms choose different strategic action, thereby affecting firms’ risk-taking for their customers.

Family business research has demonstrated that there are notable differences in strategic decisions between family and non-family firms (Berrone et al., Citation2012; Gibb Dyer, Citation2006) and, as a result, family firms exhibit different strategic behaviors than their non-family counterparts (Gomez‐mejia et al., Citation2010). The essence of family business literature is the socioemotional wealth (SEW) perspective that either financial consideration or profit maximization is not the foremost reference point in family firms’ principles for making strategic choices. Rather, “family firms are typically motivated by, and committed to, the preservation of their SEW”; that is, the emotional and non-financial value attached by family members to their firm (Berrone et al., Citation2012, p. 259). Thus, family firms are perceived as placing more strategic importance on the preservation of non-financial value such as tradition, honor and reputation rather than the maximization of pure financial profits when making strategic choices (Berrone et al., Citation2012; Gomez-Mejia et al., Citation2011).

Of course, family firms’ unique strategic choices can sometimes undermine the economic value of their business. Gómez-Mejía et al. (Citation2007) show that to preserve their historical way of doing business, Spanish family-owned olive mills usually prefer to remain independent rather than join a cooperative; this inhibits performance and greatly increases subsequent financial uncertainty. Nevertheless, regardless of the potential negative impact on economic value due to the unique strategic nature of family firms, many empirical studies reported that family firms are more responsible and reliable to their employees, suppliers, and customers in order to preserve the honor of the family in their local community (Berrone et al., Citation2010) and to succeed this long-standing honor to the next generation (Bennedsen et al., Citation2007; Pérez-González, Citation2006). Indeed, compared to non-family firms, family firms continue relationships with long-time buyers and reduce customer benefit to a lesser extent to preserve their long-standing honor in the community (Block, Citation2010; Stavrou et al., Citation2007). The greater responsible and altruistic posture of family firms toward their stakeholders can increase their willingness to take risks for customer benefits, if necessary.

Notably, family firms are perceived to be more risk-averse than non-family firms to avoid the loss of their current SEW (Leitterstorf & Rau, Citation2014; Singla et al., Citation2014). However, recent studies suggest that family firms are more likely than non-family firms to bear the cost and uncertainty of pursuing certain actions, driven by the belief that the risks that such actions entail are offset by the non-economic values in the long-term (Gomez-Mejia et al., Citation2019; Gómez-Mejia et al., Citation2021). That is, if family firms anticipate that they can further enhance their long-term SEW by undertaking risks, this will reduce their inherent aversion toward current SEW loss due to risk-taking. Firms’ risk-taking to accommodate the demands of desperate customers can clearly increase long-term SEW. For example, firms’ active risk-taking for their customers can lead to social recognition, which provides a strong foundation for non-financial values, such as firm reputation, honor, and customer loyalty. In summary, when PRA is positive, family firms can be more active than non-family firms in taking risks for customers because they believe this type of risk-taking can further strengthen their long-term SEW.

Thus, the second hypothesis is proposed as follows.

Hypothesis 2:

A positive relationship between positive PRA and risk-taking for customers will be stronger for family firms

3. Methods

3.1. Sample

We investigate the PF loan activities of all 79 savings banks in South Korea from 2013 to 2021. There are two main reasons for choosing Korean savings banks to test our hypotheses. First, unlike commercial banks, savings banks are financial companies whose purpose is to support local small businesses and households. Therefore, besides the primary goal of pursuing profits, the goal of supporting the local community and small businesses is more important for the management of savings banks than commercial banks. Second, in South Korea, numerous savings banks are still owned by families, and the number of family- and non-family-owned savings banks is similar. Therefore, it is a very good setting for analyzing the differences in strategic actions according to a bank’s ownership structure. Our main data sources are the periodic disclosure data released on each savings bank’s website, proxy statements filed with the Korean Financial Supervisory Service, and data on annual savings bank loan status provided by the Korean Savings Banks Federation.

To give important information about our sample, first, Korean savings banks have a short history compared to commercial banks in Korea, as well as American and European banks. The average age of the 79 savings banks is only 31 years, and the oldest savings bank is still less than 50 years old. Second, the average asset size of Korean savings banks is only USD 1.5 billion, which is very small compared to USD 300 billion of Korean commercial banks. Third, 40 savings banks out of 79 were owned by families, and unlike typical commercial banks, these family-owned savings banks do not frequently change their CEOs. The average tenure of a CEO at a family-owned savings bank is 16 years. Fourth, when comparing family savings banks and non-family savings banks, non-family savings banks are generally larger than family savings banks, but family savings banks have a longer history.

3.2. Measurement

3.2.1. Independent variable

The independent variable (IV) is a positive PRA. PRA is usually calculated as the actual performance minus aspirations. Researchers construct aspirations using a firm’s past performance (e.g., P. Bromiley & Harris, Citation2014; Smulowitz et al., Citation2020). Thus, we measure aspirations as the previous year’s return on assets (ROA) and calculate PRA as the difference between the current and prior year’s performance. Since we lag these variables, PRA equals the difference between firm ROA at t-1 and t-2.

Following previous research (e.g., Desai, Citation2016; Lim & Mccann, Citation2013), we measure positive PRA as zero if the PRA is negative and equal to PRA if it is positive. Accordingly, our measure captures not only whether the firm exceeds aspiration levels but also by how much. To address potential outliers, we follow P. Bromiley and Harris (Citation2014) and winsorize this independent variable at the 2% level. Our results are also robust to non-winsorizing and winsorizing at both the 1% and 5% levels.

3.2.2. Dependent variable

The dependent variable (DV) is PF loan engagement which is calculated as follows.

DV in our study is the extent to which firm take risks for their customers. The most common case in which savings banks are willing to take risks for customers is to accept loan requests from financially-weak customers who lack solid collateral and/or cash-flows. PF loans are among the most dangerous loans managed by savings banks. PF loans are business loans, mainly extended to small- and medium-sized construction companies, and the bank lends money based on the potential of their business instead of collateral, such as buildings or land. While, in true PF, banks relinquish the right to recover the loans in the event of default because loan securitization is based solely on the future cash-flows of the project (Müllner, Citation2017), several types of collateral are possible in PF loans in certain countries, such as Spain (Bros & Vivas, Citation2019). (For international comparison of PF, see Hainz & Kleimeier, Citation2006) However, in South Korea, PF loans are made only with business potential, that is, future cash-flows, without collateral. Thus, if a borrower construction company declares bankruptcy, it is impossible for savings banks in South Korea to recover the loan, resulting in enormous financial losses. Furthermore, because there is no collateral and the loan period for a construction project is usually more than 10 years, banks face challenges in selling PF loans to other financial companies. Owing to the nature of PF loans, most savings banks seeking stable and certain profits have lower preference for PF lending. That is, banks which prioritize their own interests reject most PF loan requests from SME customers and do not actively participate in PF loans.

Note that as our measurement is novel and context-dependent, it may lead to a lack of validity. Thus, we interviewed five experts (two financial analysts, two bankers, and one journalist) to check whether our method actually measures what it intends to measure. All experts agreed that our measurement was a good measure of banks’ willingness to take risks for their customers. In particular, they opined that it is appropriate to consider only PF loans as a dependent variable, and not all small business and low-income household loans in which savings banks participate. This is because for other small business and low-income household loans, banks do get collateral; hence, they do not bear the default risk, unlike the case of PF loans. The significant factors for this collateralized lending are more likely to be bank profitability, borrower credit rating, or collateral, rather than the banks’ willingness to take risks for customers. Through our interviews, the validity of measuring only the PF loan as dependent variable, not the entire small business and low-income household loan, was verified.

3.2.3. Moderating variable

A moderating variable is binary, which equals 1 if the company is a family firm, and 0 otherwise. Following prior studies on family businesses (e.g., Anderson & Reeb, Citation2003; Feldman et al., Citation2016), we defined family firms as those in which the founder or at least one founding family member by blood or marriage is (a) a CEO or president or (b) the largest shareholder or has at least 20% of the shares, either individually or as a group. The savings bank’s equity status and information on the executives and directors were manually obtained through regular disclosure data on the bank’s respective website.

3.2.4. Control variable

To reduce the confounding effect, we consider numerous firm- and CEO-level control variables that may influence our dependent variable. The first one is corporate loan ratio. This variable is a proxy for the extent of banks’ resource constraints. Banks with constrained internal resources are more likely to engage in simple household loans rather than complex PF loans (Paravisini, Citation2008). The second one is PF ratio, which is the ratio of actual amount of PF loans to the bank’s maximum limit on PF. Since PF loans are risky, financial authorities set a limit on the proportion of PF loans for each bank. A high PF ratio signals substantial risk; then, banks are less likely to provide new PF loans to other customers. Third, banks with greater financial soundness tend to operate conservatively (Michalak & Uhde, Citation2012). Bank soundness was measured using the BIS ratio. We also control for bank size using the number of bank employees. Bank age can also impact the degree of participation in PF loans because firms tend to avoid risk as they age (Sørensen & Stuart, Citation2000). CEO-level control variables may also affect banks’ willingness toward PF lending. CEO replacement can suddenly change a firm’s strategy (Barron et al., Citation2011). Here, this variable equals 1 if CEO replacement occurs and 0 otherwise. CEO’s tenure and age were also controlled for. Typically, the older the CEO and the longer the CEO’s tenure, the greater the rejection of risky operations (Musteen et al., Citation2010).

3.3. Model

We used a panel dataset. Scholars have advocated the use of panel samples for empirical research because they control for unobserved heterogeneity, and deal with both dynamic effects across the entire samples and average effects across individual units (Guerras-Martín et al., Citation2014). The generalized least squares (GLS) method has been suggested to be the most suitable for statistically examining panel data sets because it can effectively handle the problem of cross-sectional heteroskedasticity and within-unit serial correlation (Dielman, Citation1983). Hence, we adopted the GLS to test our hypotheses. The GLS regression model can be implemented using either a random- or fixed-effects model. A random-effects model assumes that the firm-specific residual has a distribution with a variance of . Meanwhile, a fixed-effect model assumes that the variance of the firm-specific residuals is zero, and thus, has no distribution. To decide between the two effects, we used the Hausman test with the null hypothesis that a random-effect model is recommended. The resulting p-value was 0.76, and thus, we adopted the random-effects GLS regression. However, we also tested our hypotheses employing a fixed-effects model, and obtained results broadly consistent with our main analyses employing a random-effects model. The analysis was performed in Stata with the program’s xt family commands, specifically designed to deal with panel dataset. All independent, moderating, and control variables were lagged by 1 year to increase causality. Table provides a brief description of the definitions and differences between model 1 and model 8 in our analysis.

Table 1. The definitions and differences from model 1 to model 8

Table 2. Descriptive statistics and correlation matrix

Table 3. Results of random-effect GLS regression

4. Results

Table presents the descriptive statistics and Pearson product-moment correlations of the variables. All variables were tested for normality and those found to be not normal were Box-Cox transformed. To test for multicollinearity, we calculated the variance inflation factors (VIF). The VIFs for all variables were significantly lower than the cut-off of 10 recommended in studies (Kutner et al., Citation2004).

We now turn to the results of hypotheses tests. Table presents the results of GLS regression for both main and moderated effects. Model 1 is a baseline model with only control variables. Corporate loan ratio, bank size and CEO replacement are negatively associated with bank’s engagement in PF loans with significant p-value. Model 2 adds the variable of interest to test our main effects. In Hypothesis 1, we predict that firms’ risk-taking for the benefit of customers is positively related to PRA because positive PRA will provide freedom of action, and firms will use that freedom to take a risk for the benefit of customers. In model 2, we can check that the estimated coefficient of PRA is statistically significant and positive (coefficient 18.361, p-value 0.003). This result provides support for Hypothesis 1.

In Hypothesis 2, we argue that the positive relationship between PRA and firms’ risk-taking for customers will be stronger for family firms. To test Hypothesis 2, we add to Model 4 a multiplicative interaction term between PRA and family firm. In model 4, we find support for the moderating effect of family firm for the relationship between risk-taking and PRA. In particular, we find the interaction between PRA and family firms is significant and positive (coefficient 15.022, p-value 0.002), supporting Hypothesis 2.

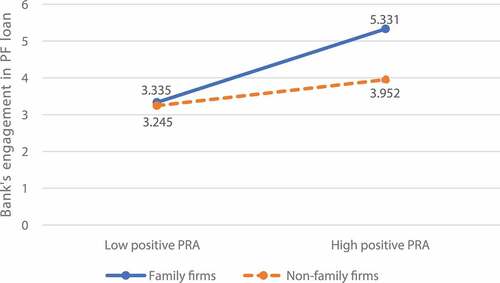

To visualized this interaction effect, we plotted the predicted value of firms’ risk-taking for family firms and non-family firms at the two levels of PRA. To do so, we relied on the procedure reported in Lee and Park (Citation2008). First, for each of the two companies (i.e., family and non-family), we divided our sample into two groups in terms of the PRA variable (i.e., lower mean and higher mean groups). Second, for each group, the mean values for the lower and higher groups were calculated, respectively. Lastly, we utilized the estimated coefficients in Table to create plots for firms’ different risk-taking according to corporate ownership. As shown in Figure , the interaction graph further support Hypothesis 2.

Figure 1. Steeper slope of family firm’s risk-taking for customers with respect to positive PRA.

4.1. Robustness test

To further support our results, we conducted an alternative test using a different approach to measure PRA. While we originally adopted the firm’s past performance (historical aspirations) as a proxy for aspirations, the performance of comparable organizations (social aspirations) is also widely used (P. Bromiley & Harris, Citation2014). Industry median ROA was used to measure social aspirations. Thus, in an alternative test, PRA is calculated as the difference between the firm’s performance and the industry median ROA in the prior year (t-1). Table shows that both hypotheses are still supported by an alternative approach. In other words, banks with better performance relative to others take more risk to provide financial opportunities to customers and this type of risk-taking is more pronounced for family firms.

Table 4. Alternative test with different measure of PRA (social aspirations)

5. Discussion

This study focuses on the firms’ risk-taking for the benefit of customers and investigates how this type of risk-taking is associated with PRA. To this end, we investigated the PF loan activities and PRA of all 79 savings banks in South Korea from 2013 to 2021. Contrary to the prevalent prediction that firms’ risk-taking increase when performance is below aspirations, our results demonstrate that banks with greater positive PRA are taking higher risk through active engagement in dangerous PF loans. This suggests that, when investigating how firms’ risk-taking will be in response to PRA, it is necessary for us to consider what kinds of strategic value firms pursue through risk-taking. Also, unlike the dominant perception that family firms are more risk-averse than non-family firms, the results show that, when PRA is positive, family-owned savings banks take rather greater risks than non-family counterparts by engaging more actively in PF loans. This suggests that the unique characteristics of family firms in their strategic choices enables family firms to take more risks for customers than non-family firms to enhance their non-financial value.

5.1. Theoretical contribution

The outcomes of the present study provide important contributions to the relevant literature. First, this study contributes to the literature on BTOF by suggesting that the relationship between risk-taking and PRA may vary depending on the strategic value a company pursues through risk-taking. BTOF studies examine how PRA influences firms’ risk-taking (e.g., P. Bromiley et al., Citation2001; P. H. I. L. I. P. Bromiley & Rau, Citation2010), generally predicting that when performance falls below aspiration levels, firms’ risk-taking should increases, and when performance exceeds aspiration levels, firms’ risk-taking should decrease (e.g., Lim & Mccann, Citation2013; Palmer & Wiseman, Citation1999). However, these predictions focus primarily on the aspect of the firms’ pursuit of own profit in analyzing their risk-taking behavior according to PRA. As a result, a sufficient attention has not been paid to the possibility that firms can take risks for the benefits of customers and, more importantly, that firms, in this case, respond differently to PRA by changing their willingness to take risks. In this study, contrary to the existing prediction, we demonstrated that banks’ engagement in risky PF loans was rather greater when performance is above aspirations. In other words, when PRA is positive, savings banks take higher risks to provide economically-weak SME customers with financial opportunities (benefits) for future growth. Thus, this study allows us to reinforce theory building by exploring the boundary conditions where BTOF predictions may need further refinement. In addition, this study suggests that BTOF research also needs to study various motive of risk-taking other than the pursuit of own profit and whether and how these different types of risk-taking are associated with PRA.

In fact, our results are similar to those of Smulowitz et al. (Citation2020), who showed that positive PRA lets banks pursue the social goal of community support, such as supporting economically weak customers. Thus, our study is in line with previous research, which suggests that banks make more social investment for financially-weak customers when PRA is positive. However, by theoretically associating a social goal (e.g., supporting SMEs) with firms’ risk-taking, our study further suggests that positive PRA increases banks’ willingness to take risks for social value. Specifically, our results suggest that a positive PRA provides savings banks with the freedom to pursue customer benefits, which were typically prioritized less by banks’ management compared to the primary goal of pursuing profits. And the freedom obtained from a positive PRA allows banks to take more risk than usual in providing financial opportunities to their SME customers.

Second, this study contributes to the literature on family business by suggesting that if family firms perceive that they can enhance their long-term SEW by undertaking risks, family firms conduct risky actions more actively than non-family counterparts. Research has documented that family firms engage in risky actions less than non-family firms, such as corporate acquisition (Gomez-Mejia et al., Citation2018), collaboration (Gómez-Mejía et al., Citation2007), internationalization (Singla et al., Citation2014), diversification (Munoz-Bullon et al., Citation2018) and going public (Leitterstorf & Rau, Citation2014), because these actions may decrease their current SEW. However, by ignoring the potential long-term SEW gains that such risky actions can bring, scholars have paid less attention to the idea that family firms may take more risks than non-family firms if these actions help them increase their long-term SEW. In this study, we show that the positive relationship between positive PRA and banks’ engagement in risky PF loan becomes stronger for family-owned savings banks. This suggests that when PRA is positive, family-owned savings banks are more willing to take risks for customers for long-term SEW gain than their non-family counterparts. Indeed, a decision to take substantial risks to provide financial benefits to their financially weak SME customers can strengthen their long-term non-financial value, such as social reputation, honor, and customer loyalty, which are pursued by family members.

5.2. Managerial implication

Our research also provides important managerial implication for family business owners who are strategically considering risk-taking for social value (e.g., supporting customers). Our study shows that, when PRA is positive, family-owned savings banks are more active in PF lending than non-family savings banks. That is, contrary to the predominant view that family firms are more risk-averse than non-family firms (Gomez-Mejia et al., Citation2018; Muñoz-Bullon et al., 2018; Leitterstorf & Rau, Citation2014), family businesses are more likely than non-family counterparts to take risks for the benefit of customers when performance is above aspiration. Therefore, family business managers need to strategically inform external stakeholders that, contrary to common sense, family firms are more willing to take risks than non-family firms if risk-taking is for the benefit of their customers, not their own profit. Considering that companies want more outcomes with less investment, actively informing external stakeholders of this fact will further increase the long-term return of family firms’ social investment. For example, news that a company is willing to take risks for its customers strengthens the company’s reputation and ultimately raises its legitimacy. Indeed, active promotion of social activities is especially important for most family businesses today, which operate with a small local customer base, such as Korean Savings Bank, a sample of our study.

5.3. Limitation and future research

This study has some limitations, which also provides opportunities for future research. First, our sample comprises of only Korean firms. While we sought to remove sampling bias by including all 79 savings banks in South Korea, our findings may not be generalizable to other countries. For example, the policies and regulations imposed by financial authorities differ from country to country, and thus, each bank’s risk-taking for customers can be significantly influenced by the institutional environments. In addition, our sample consisted of only banks and did not include firms from other business sectors. Future research should investigate the applicability of findings by country, industry, and business type. This can have high theoretical value. For example, it is theoretically valuable to identify the countries, industries, and circumstances under which firms’ risk-taking behavior for customers exhibit different pattern from that with PRA. Further, future research should consider a contingency approach to the study of risk-taking for customers to establish a more refined understanding of the relationship between PRA and risk-taking for customers. By incorporating diversified circumstances and characteristics, we can comprehensively refine the boundary conditions under which a positive PRA promotes a firm’s willingness take to risks for customers.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data that support the findings of this study are available on request from the corresponding author. Part of the data used in the research cannot be disclosed to the outside due to the protection of banks’ customer information.

References

- Anderson, R. C., & Reeb, D. M. (2003). Founding‐family ownership and firm performance: Evidence from the S&P 500. The Journal of Finance, 58(3), 1301–19. https://doi.org/10.1111/1540-6261.00567

- Barron, J. M., Chulkov, D. V., & Waddell, G. R. (2011). Top management team turnover, CEO succession type, and strategic change. Journal of Business Research, 64(8), 904–910. https://doi.org/10.1016/j.jbusres.2010.09.004

- Baysinger, B. D., Kosnik, R. D., & Turk, T. A. (1991). Effects of board and ownership structure on corporate R&D strategy. Academy of Management Journal, 34(1), 205–214. https://doi.org/10.2307/256308

- Bennedsen, M., Nielsen, K. M., Pérez-González, F., & Wolfenzon, D. (2007). Inside the family firm: The role of families in succession decisions and performance. The Quarterly Journal of Economics, 122(2), 647–691. https://doi.org/10.1162/qjec.122.2.647

- Berrone, P., Cruz, C., & Gomez-Mejia, L. R. (2012). Socioemotional wealth in family firms: Theoretical dimensions, assessment approaches, and agenda for future research. Family Business Review, 25(3), 258–279. https://doi.org/10.1177/0894486511435355

- Berrone, P., Cruz, C., Gomez-Mejia, L. R., & Larraza-Kintana, M. (2010). Socioemotional wealth and corporate responses to institutional pressures: Do family-controlled firms pollute less? Administrative Science Quarterly, 55(1), 82–113. https://doi.org/10.2189/asqu.2010.55.1.82

- Block, J. (2010). Family management, family ownership, and downsizing: Evidence from S&P 500 firms. Family Business Review, 23(2), 109–130. https://doi.org/10.1177/089448651002300202

- Bromiley, P. (1991). Testing a causal model of corporate risk taking and performance. Academy of Management Journal, 34(1), 37–59. https://doi.org/10.2307/256301

- Bromiley, P., & Harris, J. D. (2014). A comparison of alternative measures of organizational aspirations. Strategic Management Journal, 35(3), 338–357. https://doi.org/10.1002/smj.2191

- Bromiley, P., Miller, K. D., & Rau, D. (2001). Risk in strategic management research. The Blackwell Handbook of Strategic Management, 259–288.

- Bromiley, P. H. I. L. I. P., & Rau, D. (2010). Risk taking and strategic decision making. Handbook of Decision Making, 307–326.

- Bros, H., & Vivas, J. (2019). Project finance 2019 Spain. Layout 1, Cuatrecases. https://www.cuatrecasas.com/resources/project-finance-2019-spain-4137-9131-1154-v.1-617abd9ab4f4e180715735.pdf?v1.22.0.202205251146

- Carroll, A. B., & Brown, J. A. (2018). Corporate social responsibility: A review of current concepts, research, and issues. Corporate Social Responsibility. https://doi.org/10.1108/S2514-175920180000002002

- Cyert, R. M., & March, J. G. (1963). A behavioral theory of the firm. Behavioral Science, 4(2), 169–187. https://doi.org/10.1002/bs.3830040202

- Denis, D. J., Denis, D. K., & Sarin, A. (1999). Agency theory and the influence of equity ownership structure on corporate diversification strategies. Strategic Management Journal, 20(11), 1071–1076.

- Desai, V. M. (2016). The behavioral theory of the (governed) firm: Corporate board influences on organizations’ responses to performance shortfalls. Academy of Management Journal, 59(3), 860–879. https://doi.org/10.5465/amj.2013.0948

- Dielman, T. E. (1983). Pooled cross-sectional and time series data: A survey of current statistical methodology. The American Statistician, 37(2), 111–122. https://doi.org/10.1080/00031305.1983.10482722

- Dong, J. Q. (2021). Technological choices under uncertainty: Does organizational aspiration matter? Strategic Management Journal, 42(5), 898–916. https://doi.org/10.1002/smj.3253

- Eggers, J. P., & Suh, J. H. (2019). Experience and behavior: How negative feedback in new versus experienced domains affects firm action and subsequent performance. Academy of Management Journal, 62(2), 309–334. https://doi.org/10.5465/amj.2017.0046

- Feldman, E. R., Amit, R., & Villalonga, B. (2016). Corporate divestitures and family control. Strategic Management Journal, 37(3), 429–446. https://doi.org/10.1002/smj.2329

- Fernando, S., & Lawrence, S. (2014). A theoretical framework for CSR practices: Integrating legitimacy theory, stakeholder theory and institutional theory. Journal of Theoretical Accounting Research, 10(1), 149–178.

- Gaba, V., Lee, S., Meyer-Doyle, P., & Zhao Ding, A. (2022). Prior experience of managers and maladaptive responses to performance feedback: Evidence from mutual funds. Organization Science. https://doi.org/10.1287/orsc.2022.1605

- Gibb Dyer, W., Jr. (2006). Examining the “family effect” on firm performance. Family Business Review, 19(4), 253–273. https://doi.org/10.1111/j.1741-6248.2006.00074.x

- Gomez‐mejia, L. R., Makri, M., & Kintana, M. L. (2010). Diversification decisions in family‐controlled firms. Journal of Management Studies, 47(2), 223–252. https://doi.org/10.1111/j.1467-6486.2009.00889.x

- Gómez-Mejia, L. R., Chirico, F., Martin, G., & Baù, M. (2021). Best among the worst or worst among the best? Socioemotional wealth and risk-performance returns for family and non-family firms under financial distress. Entrepreneurship Theory & Practice, 10422587211057420. https://doi.org/10.2139/ssrn.3945256

- Gomez-Mejia, L. R., Cruz, C., Berrone, P., & De Castro, J. (2011). The bind that ties: Socioemotional wealth preservation in family firms. The Academy of Management Annals, 5(1), 653–707. https://doi.org/10.5465/19416520.2011.593320

- Gómez-Mejía, L. R., Haynes, K. T., Núñez-Nickel, M., Jacobson, K. J., & Moyano-Fuentes, J. (2007). Socioemotional wealth and business risks in family-controlled firms: Evidence from Spanish olive oil mills. Administrative Science Quarterly, 52(1), 106–137. https://doi.org/10.2189/asqu.52.1.106

- Gomez-Mejia, L. R., Neacsu, I., & Martin, G. (2019). CEO risk-taking and socioemotional wealth: The behavioral agency model, family control, and CEO option wealth. Journal of Management, 45(4), 1713–1738. https://doi.org/10.1177/0149206317723711

- Gomez-Mejia, L. R., Patel, P. C., & Zellweger, T. M. (2018). In the horns of the dilemma: Socioemotional wealth, financial wealth, and acquisitions in family firms. Journal of Management, 44(4), 1369–1397. https://doi.org/10.1177/0149206315614375

- Govindan, K., Shankar, M., & Kannan, D. (2018). Supplier selection based on corporate social responsibility practices. International Journal of Production Economics, 200, 353–379. https://doi.org/10.1016/j.ijpe.2016.09.003

- Greve, H. R. (2008). A behavioral theory of firm growth: Sequential attention to size and performance goals. Academy of Management Journal, 51(3), 476–494. https://doi.org/10.5465/amj.2008.32625975

- Greve, H. R., & Gaba, V. (2017). Performance feedback in organizations and groups: Common themes. The Oxford Handbook of Group and Organizational Learning, 1–45.

- Guerras-Martín, L. Á., Madhok, A., & Montoro-Sánchez, Á. (2014). The evolution of strategic management research: Recent trends and current directions. BRQ Business Research Quarterly, 17(2), 69–76. https://doi.org/10.1016/j.brq.2014.03.001

- Hainz, C., & Kleimeier, S. (2006). Project finance as a risk-management tool in international syndicated lending. Governance and the Efficiency of Economic Systems (GESY). SFB/TR, 15. https://doi.org/10.2139/ssrn.567112

- Hoskisson, R. E., Chirico, F., Zyung, J., & Gambeta, E. (2017). Managerial risk taking: A multitheoretical review and future research agenda. Journal of Management, 43(1), 137–169. https://doi.org/10.1177/0149206316671583

- Hutchison-Krupat, J., & Kavadias, S. (2015). Strategic resource allocation: Top-down, bottom-up, and the value of strategic buckets. Management Science, 61(2), 391–412. https://doi.org/10.1287/mnsc.2013.1861

- Jeong, Y. C., & Kim, T. Y. (2019). Between legitimacy and efficiency: An institutional theory of corporate giving. Academy of Management Journal, 62(5), 1583–1608. https://doi.org/10.5465/amj.2016.0575

- Kutner, M. H., Nachtsheim, C. J., Neter, J., & Wasserman, W. (2004). Applied linear regression models (Vol. 4). McGraw-HillIrwin.

- Lee, H. U., & Park, J. H. (2008). The influence of top management team international exposure on international alliance formation. Journal of Management Studies, 45(5), 961–981. https://doi.org/10.1111/j.1467-6486.2008.00772.x

- Leitterstorf, M. P., & Rau, S. B. (2014). Socioemotional wealth and IPO underpricing of family firms. Strategic Management Journal, 35(5), 751–760. https://doi.org/10.1002/smj.2236

- Lim, E. N., & Mccann, B. T. (2013). The influence of relative values of outside director stock options on firm strategic risk from a multiagent perspective. Strategic Management Journal, 34(13), 1568–1590. https://doi.org/10.1002/smj.2088

- March, J. G., & Simon, H. A. (1958). Organizations. John wiley & sons.

- Merkelsen, H. (2011). The double‐edged sword of legitimacy in public relations. Journal of Communication Management, 15(2), 125–143. https://doi.org/10.1108/13632541111126355

- Michalak, T. C., & Uhde, A. (2012). Credit risk securitization and bank soundness in Europe. The Quarterly Review of Economics and Finance, 52(3), 272–285. https://doi.org/10.1016/j.qref.2012.04.008

- Müllner, J. (2017). International project finance: Review and implications for international finance and international business. Management Review Quarterly, 67(2), 97–133. https://doi.org/10.1007/s11301-017-0125-3

- Munoz-Bullon, F., Sanchez-Bueno, M. J., & Suárez-González, I. (2018). Diversification decisions among family firms: The role of family involvement and generational stage. BRQ Business Research Quarterly, 21(1), 39–52. https://doi.org/10.1016/j.brq.2017.11.001

- Musteen, M., Barker, V. L., III, & Baeten, V. L. (2010). The influence of CEO tenure and attitude toward change on organizational approaches to innovation. The Journal of Applied Behavioral Science, 46(3), 360–387. https://doi.org/10.1177/0021886310361870

- Palmer, T. B., & Wiseman, R. M. (1999). Decoupling risk taking from income stream uncertainty: A holistic model of risk. Strategic Management Journal, 20(11), 1037–1062.

- Paravisini, D. (2008). Local bank financial constraints and firm access to external finance. The Journal of Finance, 63(5), 2161–2193. https://doi.org/10.1111/j.1540-6261.2008.01393.x

- Pérez-González, F. (2006). Inherited control and firm performance. The American Economic Review, 96(5), 1559–1588. https://doi.org/10.1257/aer.96.5.1559

- Reimann, M., Schilke, O., & Thomas, J. S. (2010). Customer relationship management and firm performance: The mediating role of business strategy. Journal of the Academy of Marketing Science, 38(3), 326–346. https://doi.org/10.1007/s11747-009-0164-y

- Schumacher, C., Keck, S., & Tang, W. (2020). Biased interpretation of performance feedback: The role of CEO overconfidence. Strategic Management Journal, 41(6), 1139–1165. https://doi.org/10.1002/smj.3138

- Singh, J. V. (1986). Performance, slack, and risk taking in organizational decision making. Academy of Management Journal, 29(3), 562–585. https://doi.org/10.2307/256224

- Singla, C., Veliyath, R., & George, R. (2014). Family firms and internationalization‐governance relationships: Evidence of secondary agency issues. Strategic Management Journal, 35(4), 606–616. https://doi.org/10.1002/smj.2111

- Smulowitz, S. J., Rousseau, H. E., & Bromiley, P. (2020). The behavioral theory of the (community‐oriented) firm: The differing response of community‐oriented firms to performance relative to aspirations. Strategic Management Journal, 41(6), 1023–1053. https://doi.org/10.1002/smj.3123

- Sørensen, J. B., & Stuart, T. E. (2000). Aging, obsolescence, and organizational innovation. Administrative Science Quarterly, 45(1), 81–112. https://doi.org/10.2307/2666980

- Stavrou, E., Kassinis, G., & Filotheou, A. (2007). Downsizing and stakeholder orientation among the Fortune 500: Does family ownership matter? Journal of Business Ethics, 72(2), 149–162. https://doi.org/10.1007/s10551-006-9162-x

- Wickert, C., & Risi, D. (2019). Corporate social responsibility. Cambridge University Press.

- Wiseman, R. M., & Bromiley, P. (1996). Toward a model of risk in declining organizations: An empirical examination of risk, performance and decline. Organization Science, 7(5), 524–543. https://doi.org/10.1287/orsc.7.5.524

- Xie, E., Huang, Y., Stevens, C. E., & Lebedev, S. (2019). Performance feedback and outward foreign direct investment by emerging economy firms. Journal of World Business, 54(6), 101014. https://doi.org/10.1016/j.jwb.2019.101014