?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Online service quality acts as a lever that service providers use to drive e-customer retention in most affluent economies globally. Given the exponential growth in the adoption of internet banking during the COVID-19 pandemic, the purpose of this study was to evaluate the antecedents of e-customer retention among banks in Zimbabwe post the pandemic. Grounded in the expectancy-disconfirmation theory, the study adopts an explanatory research design and a quantitative research approach. Data was collected using convenience sampling and hand-administered questionnaires. Covariance based Structural Equation Modelling (SEM) in SPSS AMOS examined 261 valid responses. The findings of the study revealed the positive impact of e-banking service quality on e-customer satisfaction and e-word of mouth. E-customer satisfaction also positively influenced e-word of mouth and e-customer retention. The results were also confirmatory of the positive effect of e-customer satisfaction and e-word of mouth on e-customer retention. The paper reveals that although significant e-banking adoption was enforced through COVID-19 regulations, banks were responsive enough to install the requisite e-banking infrastructure. Thus, post pandemic banking experiences have induced confirmation of e-banking service quality and consequentially e-customer satisfaction, e-WOM and e-retention. The study therefore flags the important antecedent role of e-banking service quality to e-customer satisfaction, e-word of mouth and e-customer retention. To promote the e-customer retention in the post COVID-19 era in Zimbabwe, banks need to maximize perceived internet banking service quality.

REVIEWING EDITOR:

1. Introduction

The adoption of internet-based services has now penetrated most industries across developed, emerging and pre-emerging economies (Khan & Alhumoudi, Citation2022; Naeem & Ozuem, Citation2021). Internet banking (e-banking) is defined as the provision, delivery and consumption of financial services using the internet and web-based applications (Al-Hawari, Citation2014; Shankar & Jebarajakirthy, Citation2019). Building competitive advantage by enhancing customer relationships through digital servicescapes has been recently popularized due to rapid developments in electronic commerce and globalisation (Amin, Citation2016; Ezechirinum et al., Citation2020). Further, the eruption of the COVID-19 pandemic also reinforced e-banking adoption especially in developing economies such as Zimbabwe (Chowdhury et al., Citation2022; Dangaiso et al., Citation2022). Most banks have since made concerted efforts to revamp their digital banking capabilities globally (Bala et al., Citation2021; Chavda, Citation2021; Sudarsono et al., Citation2020).

Electronic banking has seen exponential growth in the recent decades marking a significant transformation in the delivery of financial services (Indrasari et al., Citation2022). According to the World Bank (Citation2021), 51% of adults in developing countries owned e-bank accounts, rising to 68% in 2017 and 76% in 2021. The Global Findex 2021 database shows that 71% of all people in developing countries had bank accounts with digital services (World Bank, Citation2021). More so, digital payments saw the biggest growth in developing countries as two 2/3 (66.6%) make or receive digital payment (World Bank, Citation2021). According to the Institute of Bankers in Zimbabwe (IOBZ, Citation2022), e-banking has serendipitously expanded economic performance as 88.4% of the banking population made or received a digital remittance between 2021 and 2022. Mobile money services also saw a 75% usage from 42% in 2012 (CBZ, Citation2021; IOBZ, Citation2022). The COVID-19 pandemic has spurred financial inclusion in developing countries such as Zimbabwe through digital banking.

Notwithstanding the rapid adoption of internet banking during the COVID-19 pandemic, most Zimbabwean banks still face overwhelming queues in their banking malls (CBZ, Citation2021; Mavaza, Citation2019). More so, customer retention in online servicescapes has been a contentious subject in Zimbabwe. Studies by Manyanga et al. (Citation2022) and Mavaza (Citation2019) reveal that Zimbabwean banks’ customers own multiple bank accounts stemming from low perceived service quality, past bank failures, lack of trust and high perceived risk. These pertinent issues present important research questions on the current status of service quality, customer satisfaction and customer retention in the banking sector in Zimbabwe given the emergency e-banking adoption at the hands of COVID-19.

Further, although research in the domain of internet banking service quality, customer satisfaction and retention has since developed rapidly, the World Bank (Citation2021) reports that 1.4 billion people are still unbanked. The low customer response rate has been attributed to poor service quality, poor technology infrastructure, lack of trust, high perceived risk, poor task-technology fit, constrained access to internet services, online customer disappointments, negative attitudes, low skill set, customer phobias and lack of financial resources (Chavda, Citation2021; Khan & Alhumoudi, Citation2022; Madziro & Ncube, Citation2021). This suggests that more context focused empirical research is still imperative to gain a deeper understanding of consumer perceptions and motivations of their banking behaviors in both physical and online services capes.

Cognizant of the inherent challenges of implementing internet banking in developing economies such as Zimbabwe, the merits of digital banking cannot be undermined. Internet banking has huge potential to support economic growth, service delivery, e-commerce, better consumer welfare, expanded regional trade, Gross Domestic Product (GDP) and lower average operational costs (Manohar et al., Citation2020; Manyanga et al., Citation2022). Implemented on a customer-centric design, internet banking has huge potential to enhance customer experience, satisfaction, customer retention, market share, brand equity and long-term competitive advantage (Manohar et al., Citation2020). Although empirical developments in the domain of service quality, customer satisfaction and customer loyalty have spurred in the financial services industry, there is still lack of plausible data in developing countries such as Zimbabwe on how consumers who adopted COVID-19 induced e-banking are responding to the phasing out of the pandemic.

It is evident that e-banking has been impulsively adopted hence customers have had no choice due to the closure of physical servicescapes (Dangaiso et al., Citation2022; Madziro & Ncube, Citation2021). Whether or not e-banking service quality sufficed to achieve e-customer satisfaction, e-word of mouth and e-customer retention, it is still a question yet to have an empirical response. COVID-19 induced e-banking meant that the key antecedent role of e-service quality on e-customer retention was made redundant. However, long-term e-customer retention in the post COVID-19 era is uncertainty in Zimbabwe given that COVID-19 is phasing out, internet infrastructure is still unstable and customers are queueing for operationalizing financial transactions (IOBZ, Citation2022; Mavaza, Citation2019). The relationship between the Zimbabwean banking system and its customers is a peculiar case given the prior collapse of the monetary system pre 2009 (Manyanga et al., Citation2022; Roux & Abel, Citation2017); and this presents a unique context through which the future viability of digital banking post the COVID-19 era can be envisaged.

The determination of this study was to investigate the nexus between e-banking service quality, e-customer satisfaction, e-word of mouth and e-customer retention post the COVID-19 period in the context of Zimbabwean banks. This research has the potential to understand key consumer perceptions of internet banking without the intervention of push variables such as COVID-19. This could be key in informing a customer centric strategy that addresses customer preferences in the absence of any restraining factors. The research can be of note to banks as they attempt to design a more customer centric strategy for long-term customer relationship management as COVID-19 can ‘no longer support digital banking’ anymore. The findings of this research may inform key stakeholders such as the government, monetary authorities, investors, financial service providers, financial services marketers and managers on customer perceptions of e-banking and their future behavioral intentions. The results may also facilitate the development of an inclusive monetary system and policy, e-banking infrastructure as catalysts for effective marketing of customer-centric banking products and services. The subsequent sections of this paper cover the research questions, literature review, material and methods, findings, implications, limitations and future research prospects.

1.1. Research questions

The study sought to provide answers to the following research questions;

Does internet banking service quality positively influence customer satisfaction during the post COVID-19 period in Zimbabwe?

Does internet banking service quality positively influence electronic word of mouth during the post COVID-19 period in Zimbabwe?

Does customer satisfaction positively influence electronic word of mouth during the post COVID-19 period in Zimbabwe?

Does electronic word of mouth positively influence customer retention during the post COVID-19 period in Zimbabwe?

Does customer satisfaction positively influence customer retention during the post COVID-19 period in Zimbabwe?

2. Literature review

2.1. Overview of the Zimbabwean banking industry

To have a better understanding of the customer experience from the Zimbabwean financial sector, a concise historical review of the banking industry and as well as an account of current issues in the banking industry are imperative. The inherent lack of trust in the Zimbabwean monetary system, tracked to the collapse of the banking system between 2000 and 2009, presents huge barriers for bank relationship marketing (Dlamini & Mbira, Citation2017; Manyanga et al., Citation2022; Roux & Abel, Citation2017). In their typology of phases in the evolution of the financial system in the post-independence era, Roux and Abel (Citation2017) labelled the period in question; ‘the crisis period,’ to sufficiently posit the demise of the Zimbabwean banking system into perspective.

The banking system has been unstable over the past two decades given hyperinflation, abrupt currency changes, bank closures, rife corporate governance scandals, low industry capacity utilization and supply side shocks (Nyamutowa & Masunda, Citation2013; Nyoka, Citation2022). These problems culminated in the loss of customer savings, pension funds and depositor funds (Manyanga et al., Citation2022; Roux & Abel, Citation2017). The restoration of the Zimbabwean RTGS dollar in 2019 further thickened customer skepticism on the integrity of the monetary authorities and the financial services sector (Reserve Bank of Zimbabwe, Citation2019). The Zimbabwean RTGS dollar struggled to find widespread acceptance, with inflation that peaked at 837% in July 2020 helping to erode its value (International Monetary Fund, Citation2022).

The Banking Amendment Act (Act 12 of 2015) extended the regulatory role of the Reserve Bank of Zimbabwe to critically monitor the accountability of directors, shareholders and management as key custodians of depositors funds (Manyanga et al., Citation2022). Although the government has made concerted efforts to sanitise the financial service sector in the past few years, the banking system still struggles to attract desired service usage and customer patronage (Manyanga et al., Citation2022; Nyoka, Citation2022). The compounded effects of an unstable monetary system, low investor confidence, economic volatility, hyperinflationary tendencies and unpredictable policies has brewed protracted customer mistrust in the financial system which acts as a major deterrent on the successful marketing of banking products in Zimbabwe (Dlamini & Mbira, Citation2017; Nyoka, Citation2022).

2.2. COVID-19 pandemic and developments in the banking industry in Zimbabwe

A steady rise in the adoption of internet banking has been evident in Zimbabwe during the pre COVID-19 era (CBZ, Citation2021; IOBZ, Citation2022). This was encouraged by rapid changes in banking technology, mass adoption of mobile phones and changes in customer preferences globally (Leung, Citation2020; Manyanga et al., Citation2022). However, the eruption of the COVID-19 pandemic forced all service providers to revamp internet banking servicescapes as the regulations enforced the decongestion of public spaces. According to the World Bank (Citation2021), 51% of adults in developing countries owned e-bank accounts, rising to 68% in 2017 and 76% in 2021. More so, the Institute of Bankers Zimbabwe IOBZ (Citation2022) reported that 96% of domestic transactions were facilitated by internet banking between 2019 and 2022.

Although exponential growth in digital banking services has been evident, the IOBZ Citation2022 report notes the disproportionate effect that COVID-19 has had on enabling the banks to migrate from brick and mortar systems. Paradoxically, COVID-19 has had significant strides in the adoption of banking but banks have been subject to overwhelming customer queues for face-to-face financial services post the COVID-19 era (CBZ, Citation2021; IOBZ, Citation2022). During the peak COVID-19 era, banking was one of the essential services that was exempted under the COVID-19 restrictions and a sizeable customer population still took huge risks to revert to physical banking (CBZ, Citation2021). This raises key questions on the nexus between e-banking service quality, customer satisfaction and retention potential in the Zimbabwean context. Further, the differential effect of e-banking service quality thus presents important connotations on long-term customer loyalty in the banking industry in Zimbabwe post the COVID-19 pandemic.

2.3. Theoretical background

This study examines the impact of internet banking service quality on e-customer satisfaction, e-word of mouth and customer retention in Zimbabwe. It is theoretically grounded in the expectancy-disconfirmation theory (Oliver, Citation1980). According to the theory, consumers make post consumption evaluation by comparing the perceived performance against their expectations of the service. According to Oliver, positive disconfirmation means that the expectations have been surpassed by the performance, hence the customer is delighted. When expectations are matched by performance (confirmation), a customer is satisfied. Only negative disconfirmation causes dissatisfaction, where the perceptions of performance are below the expected standards. The expectancy-disconfirmation theory also enlightens that post use evaluation forms the basis for post consumption behavioral intentions and hence the behaviors. Satisfaction is expected to lead to repurchase intent, positive word of mouth and customer retention. Dissatisfaction is expected to yield customer complaints, negative word of mouth and customer defection.

This study borrows its theoretical lens from this framework because of its ability to connect the focal constructs; internet banking service quality (perceived performance) to future customer behaviors resulting from the evaluation of service (e-customer satisfaction, e-word of mouth and customer retention). The research evaluates relationships between consumer perceived internet banking quality and post consumption attitudes and behavior, hence the theory fully supports this study. Theories such as the Technology Adoption Model (Davies, Citation1989) and its extensions eg the Unified Theory of Acceptance and Use of Technology (UTAUT) (Venkatesh et al., Citation2003) were inappropriate because they are silent on post usage outcomes. Technology adoption theories propose the determinants of adoption behavior whereas the disconfirmation paradigm predicts the antecedents and outcomes of customer satisfaction upon consuming a service; therefore, the expectancy-disconfirmation theory was selected to provide theoretical parameters for this research.

2.4. Conceptual framework

2.4.1. Internet banking service quality

E-service quality is the consumer’s subjective assessment on the quality of services they received via the internet (Parasuraman et al., Citation2005; Zeithaml et al., Citation2002). There is a consensus that substantive research has resulted in diverse conceptualisations and measurements of e-service quality (Amin, Citation2016). Zeithaml et al.(Citation2002) operationalised an e-service quality framework (E-SQUAL) comprising of ease of use, privacy, graphic design, information availability, reliability compensation and contact. Parasuraman et al. (Citation2005) also developed an instrument for e-shopping websites around four dimensions of fulfilment, efficiency, availability and privacy. Herington and Weaven (Citation2009) developed e-banking service quality measurement scales built on four dimensions of personal needs, site organisation, user friendliness and efficiency. Amin (Citation2016) also measured internet banking as a multi-dimensional scale consisting of personal need, user friendliness, site organization and efficiency. Ui Haq and Awan (Citation2020) used an instrument based on reliability, private and security, web design and customer service and support in e-banking service quality during the COVID-19 pandemic.

Although there are variations in the different models of measuring e-service quality, similarities are evident. Ease of use, reliability, responsiveness, assurance, privacy, responsiveness overlap in many studies (Amin, Citation2016; Herington & Weaven, Citation2009; Jayawardhena, Citation2004; Sathiyavany & Shivany, Citation2018; Ui Haq & Awan, Citation2020). Given the need to device ways of reinforcing the adoption of e-banking in pre-emerging economies, extensive research in e-banking service quality is still imperative.

2.4.2. E-customer satisfaction

Customer satisfaction has been extensively studied in literature because of its strong bearing on future consumer behavioral intentions (Kotler & Armstrong, Citation2018). In the disconfirmation theory, Oliver (Citation1980) defines customer satisfaction convergence of customers’ expectations and performance on the delivered products and services. When the perceived performance matches or surpasses the customer’s expectations of the service, the customer is satisfied. Kotler and Armstrong (Citation2018) claims that when the business meets its customer’s expectations, the customer is satisfied and when the perceived performance exceeds the customer’s expectations, the customer is delighted. On the contrary, if perceived performance falls short of customer expectations, the customer is dissatisfied (Dangaiso & Makudza, Citation2022; Fullerton & Taylor, Citation2015). According to Khan et al. (Citation2023), e-satisfaction is the contentment of the customer with respect to prior purchasing experience with an identified e-commerce firm.

2.4.3. E-word of mouth

Word of mouth (WOM) has been defined as a post consumption propensity or action by a customer to spread their product or service experiences with their acquaintances (Gvili & Levy, Citation2018; Naeem, Citation2019; Torabi & Bélanger, Citation2021). Positive word of mouth refers to a post purchase behavior by a satisfied customer to share their pleasant experiences with service to other people (van Tonder et al., Citation2018; Yen & Tang, Citation2019). WOM helps to reduce perceived risk associated with product or service purchases (Chowdhury et al., Citation2022; Hajli, Citation2014; Sudarsono et al., Citation2020). In an e-banking context, positive e-word of mouth has been defined as the spreading of delightful customer experiences with an e-banking service (Sathiyavany & Shivany, Citation2018). In digital servicescapes, customers rely on peer reviews, recommendations and online chatrooms on websites, official social media blogs, personal blogs and other web 2.0 and 3.0 applications where user generated content allows customers to make recommendations and share experiences (Gvili & Levy, Citation2018; Makudza et al., Citation2022; Timoshenko & Hauser, Citation2019).

2.4.4. E-customer retention

Confronted with e-banking options just a click away, less switching costs plus the exponential growth of mobile money services, customers seem to have more power in their relationships with e-banking service providers (Benjarongrat & Neal, Citation2017; Manyanga et al., Citation2022; Suganya et al., Citation2018). Extant marketing literature identifies loyal customers as critical to business growth and long-term sustainability (Dangaiso et al., Citation2022; Makudza, Citation2021) due to their relationship with profitability and market share (Gronroos, Citation2002; Kotler & Armstrong, Citation2018). E-customer retention has been defined as the number of customers who do business with an e-service provider and remain with them over a given period of time (Ezechirinum et al., Citation2020; Khan & Alhumoudi, Citation2022). Thus, this definition views customer retention as the customers who repatronise with an e-service provider over a known or specific period time. The literature identifies e-customer retention as a proxy and driver of long-term e-customer loyalty (Jairus, Citation2016).

2.5. Development of hypotheses

2.5.1. Internet banking service quality and e-customer satisfaction

A causal relationship between service quality and customer satisfaction has been subject to debate in marketing literature and no consensus has yet been found (Amin, Citation2016; Khan et al., Citation2023). Some scholars refer to customer satisfaction as an antecedent of service quality whilst other scholars authors argue that service quality is an antecedent of customer satisfaction (Cronin et al., Citation2000; Cronin & Taylor, Citation1992; Dangaiso et al., Citation2022). These debates have dominated services marketing literature and Gronroos (Citation2002), a prominent marketing scholar, even proposed to refer those two definitions to the customers themselves.

In the e-banking context, Jairus (Citation2016) found that if internet banking service quality is perceived to be high, customers are most likely to be satisfied with their service. Furthermore, Anderson and Srinivasan (Citation2003), Jairus (Citation2016), Khan and Alhumoudi (Citation2022) and Sudarsono et al. (Citation2020) suggest that e-customer satisfaction is highly influenced by website interface characteristics and this can result in positive emotions and ultimately satisfaction. In the context of COVID-19 mediated e-banking, banks invested in state of the art technology infrastructure to improve service quality and customer satisfaction. Further, e-banking studies in the context of COVID-19 eg Bala et al. (Citation2021) and Khan et al. (Citation2023) also found that internet banking service quality led to customer satisfaction. Given this support, the study proposed that;

H1: E-banking service quality positively and significantly influences e-customer satisfaction.

2.5.2. Internet banking service quality and e-word of mouth

Although significant marketing literature acknowledges the importance of word of mouth in the customer markets, it has received relatively less empirical attention (Naeem & Ozuem, Citation2021; Timoshenko & Hauser, Citation2019). Within the context of internet banking, word of mouth is very important as it significantly reduces consumer perceived risk with online transactions (Gvili & Levy, Citation2018). Most peer to peer relationships have now been popularized as information seeking customers connect, give each other advice, recommendations and share their online experiences across a broad spectrum of services (Kavitha & Gopinath, Citation2020; Suganya et al., Citation2018; van Tonder et al., Citation2018; Yen & Tang, Citation2019).

Internet banking can be enhanced by e-word of mouth as customers talk about their banking experiences to their friends, families and colleagues (Chowdhury et al., Citation2022; Naeem & Ozuem, Citation2021). The advent of web technologies has created serendipitous avenues that allow customers to share reviews, comments and service experiences (Makudza et al., Citation2021; Rachbini et al., Citation2021). Customers share both positive and negative word of mouth depending of their individual perceptions of the service experience (Suganya et al., Citation2018). Literature supports that lack of trust with paperless transactions is the most significant barrier to e-business; however, substantial literature suggests that customers trust peer to peer recommendations than they rely on firms’ marketing communications (Chowdhury et al., Citation2022; Naeem & Ozuem, Citation2021; van Tonder et al., Citation2018). Further, with the recent growth of social media use in Zimbabwe, it is imperative that internet banking service quality evaluations are shared by consumers online. Internet banking during the COVID-19 pandemic have shown that it led to positive recommendations on websites and social media platforms (Indrasari et al., Citation2022; Manohar et al., Citation2020). Given that, the study also predicted that;

H2: E-banking service quality positively and significantly influences positive e-word of mouth.

2.5.3. E-customer satisfaction and e-word of mouth

Post consumption evaluation plays an important role in the customer’s future behavioral intentions (Kotler & Armstrong, Citation2018). Using the disconfirmation theory (Oliver, Citation1980), customers evaluate their service experiences based on prior expectations versus their perceived performance. The subjective outcome forms the basis for their future behavioral intentions towards the service provider (Anderson & Srinivasan, Citation2003; Kavitha & Gopinath, Citation2020; Manyanga et al., Citation2022; Ui Haq & Awan, Citation2020). In the internet-banking context, customers also compare their expectations of service with the perceived performance (Bala et al., Citation2021; Makudza, Citation2021). Satisfied customers have a disposition to share their positive service journey or experience with their acquaintances (Timoshenko & Hauser, Citation2019; Yen & Tang, Citation2019). Positive word of mouth has the power to reinforce a provider’s products and services because customers trust recommendations from other customers, especially in digital servicescapes (Chowdhury et al., Citation2022; van Tonder et al., Citation2018).

Nowadays, the power of word of mouth has been enhanced by convenience of e-customer communities, chatrooms, social media blogs, recommendations and reviews on bank websites (Manohar et al., Citation2020; Naeem & Ozuem, Citation2021; Suganya et al., Citation2018). E-customer satisfaction has been identified in literature as the key antecedent to e-word of mouth communication and customers are inclined to share their positive e-experiences that evoke positive emotions (Kavitha & Gopinath, Citation2020; Rachbini et al., Citation2021; Samosir et al., Citation2023; Torabi & Bélanger, Citation2021). The positive influence of e-customer satisfaction on e-word of mouth communication has been reported in a number of COVID-19 mediated studies eg Kavitha and Gopinath (Citation2020), Manyanga et al. (Citation2022) and Torabi and Bélanger (Citation2021). In the light of these findings, the study also predicted that;

H3: E-customer satisfaction positively and significantly influences e-word of mouth.

2.5.4. E-word of mouth and e-customer retention

Customer experience management has been found to be fundamental in the service industry (Makudza, Citation2021; Manyanga et al., Citation2022). Consumption of financial services involves a lot of inherent risks and potentially huge losses (Nyoka, Citation2022; Roux & Abel, Citation2017), thus trust, commitment and assurance (Chowdhury et al., Citation2022; Hajli, Citation2014; Morgan & Hunt, Citation1994) are necessary in digital servicescapes. E-recommendations, reviews and shared social experiences reinforce customers’ staying intentions with digital financial service providers (Gvili & Levy, Citation2018; Naeem & Ozuem, Citation2021; Suganya et al., Citation2018). As information-seeking customers find P2P recommendations from other customers, they are inclined to consider staying intentions. Customers seek grouping, approval and feelings of security that accompany group choices (Ajzen, Citation1991), thus subjective norms influence behavioral intentions when customers listen to peer recommendations about their digital banking experiences.

Amid, customer mistrust in the Zimbabwean banking system (Manyanga et al., Citation2022; Roux & Abel, Citation2017), the role of e-word of mouth can award e-banks an important lifeline through e-customer retention. Given that the banking industry had declined in the recent decade (Dlamini & Mbira, Citation2017; Roux & Abel, Citation2017), e-word of mouth can be used as a lever to attain e-customer trust and confidence in internet banking. More so, the COVID-19 pandemic got customers actively seeking digital financial services providers to enable them to transact away from brick and mortar facilities (Bala et al., Citation2021; Madziro & Ncube, Citation2021; Sudarsono et al., Citation2020). Although affluent service providers have been earmarked to reap huge returns from word of mouth, it has been largely ignored in empirical research in most pre-emerging economies. Positive word of mouth for e-banking services is likely to yield customer retention in Zimbabwe post the COVID-19 pandemic. Notwithstanding, a positive relationship between e-word of mouth and customer retention during the COVID-19 era eg Manyanga et al. (Citation2022) and Rachbini et al. (Citation2021). Based on this support, the study also proposed that;

H4: E-word of mouth positively and significantly influences e-customer retention.

2.5.5. E-customer satisfaction and e-customer retention

Customer satisfaction has been extensively cited as one of the significant antecedents of business success in literature (Anderson & Srinivasan, Citation2003; Indrasari et al., Citation2022; Khan et al., Citation2023; Kotler & Armstrong, Citation2018; Manyanga et al., Citation2022). Extensive research has been conducted in different service industries to examine the relationship between customer satisfaction and customer loyalty in the traditional context (Anderson & Srinivasan, Citation2003; Sathiyavany & Shivany, Citation2018). Similarly, studies in internet banking also cite the positive effect of e-customer satisfaction on e-customer retention (Khan & Alhumoudi, Citation2022; Manyanga et al., Citation2022; Mbama & Ezepue, Citation2018; Ui Haq & Awan, Citation2020).

Research evidence to substantiate the positive relationship between the two constructs has been evident eg (Amin, Citation2016; Anderson & Srinivasan, Citation2003; Indrasari et al., Citation2022; Khan & Alhumoudi, Citation2022; Rachbini et al., Citation2021). In the post COVID-19 era alike, e-banks meeting or exceeding customer expectations are most likely to have repatronising online customers and long-term exchange relationships. Satisfied e-banking customers have a high propensity to improve e-customer retention even when the COVID-19 factors have subsided. As a result, this study also hypothesised that;

H5: E-customer satisfaction positively and significantly influences e-customer retention.

3. Materials and methods

3.1. Design, population and sampling

The study aimed to evaluate causal relationships between e-banking service quality, e-customer satisfaction, e-WOM and e-customer retention. An explanatory research design was hence adopted. Consistent with positivism, the study employed a quantitative research approach that involved the examination of priori hypothesized relationships using Structural Equation Modelling (SEM). Bindura is the provincial capital of Mashonaland Central province (Zimbabwe) with a total of 10 banks. With all these banks providing internet banking, e-banking customers from these 10 banks were the target population for the research.

A convenience sampling technique was used to select 315 respondents who visited banking and shopping malls at different times of the day. The study was conducted based on customers who confirmed their recent use of internet banking services. To ensure sufficient representation of the local banks clientele, the proportionate distribution method was adopted. Sample size determination was based on sizes used in similar studies, data analysis methods, completion rates, and resource constraints (Malhotra, Citation2011). The sample was based on a selected Zimbabwean province which was accessible and with a bank count capable of producing generalizable findings.

The survey was conducted in the month of July 2023. Although COVID-19 restrictions have been relaxed in Zimbabwe following the flattening of the epidemic curve, the study adhered to social distancing guidelines, the use of hand sanitisers and strict hygiene practices as a precaution. The adoption of an online survey was disregarded on grounds of low response rates inherent in virtual studies (Amin, Citation2016).

3.2. Estimation model

Structural models are built on the regression coefficient between exogenous latent variables and endogenous latent variables (gamma or γ), the regression coefficient between endogenous latent variables and endogenous latent variables (beta or β). All endogenous latent variables must have an error or residual term zeta (ζ). The estimation model in illustrates the proposed structural relationships.

Figure 1. Estimation model.

Endogenous variable = Exogenous variable + Endogenous variable + error. Based on this, the structural equation model for this study is;

E-customer satisfaction = γ1.2Internet banking service quality + ζ1/res1

E-Word of mouth = γ1.1Internet banking service quality + β3.1E-customer satisfaction +ζ2/res2

E-customer retention = β2.1E-Word of mouth + β3.1E-customer satisfaction + ζ3/res3

Measurement model outer model

The researcher specifies which variables measure which constructs. The equation in this case is as follows;

Exogenous equation measurement model Exogenous concept

Measurement model for Endogenous latent variable is as follows;

3.3. Operational definitions of research constructs

provides the operational definitions of research constructs.

Table 1. Operational definitions of research constructs.

3.3. Measures

The research instrument used in this study was adopted from extant literature. Al-Hawari (Citation2014) observes the high multi-collinearity problems evident on studies that measured internet banking as a multidimensional construct. Following Al-Hawari’s methodology, an integrated ten item scale was adopted by using two items from each of the 5 dimensions of e-banking SQUAL; reliability, efficiency, e-responsiveness, privacy and contact (Al-Hawari, Citation2014). E-customer satisfaction and e-customer retention were measured using scales from Amin (Citation2016) and Herington and Weaven (Citation2009). E-word of mouth was measured using items adopted from Timoshenko and Hauser (Citation2019) and Yen and Tang (Citation2019). In addition to the categorical data for the demographic data of the respondents, ordinal-scaled data for the research constructs was collected using a 7-point Likert scale from strongly disagree (1) to strongly agree (7). A pilot study was conducted based on 16 finalist students from a local university who had prior usage experience of e-banking services.

3.4. Procedures and ethical compliance

The study was conducted with adherence to ethical research standards. Compliant with the ethics of consumer surveys, the requirement to have informed consent was satisfied. Furthermore, participation was voluntary and assurances of the privacy and confidentiality of behavioral data were given. The respondents were also informed not to indicate their names and bank account information on the questionnaires. To mitigate Common Methods Bias (CMB) (Podsakoff et al., Citation2003), participants were informed that there were no right or wrong responses.

3.5. Data analysis methods

Assessment of the measurement model employed Confirmatory Factor Analysis in order to enable relationships between latent constructs and their observed items (unidimensionality) to be statistically examined. Unidimensionality measures how well a factor (latent or unobserved construct) is represented by its measured items (Hair et al., Citation2019). A factor loading represents the correlation between a factor and its observed variables. Factor loadings of 0.5 were used as the cut off point for all the retained items (Hair et al., Citation2019). The indices used to check the suitability of the models belong to a group of absolute and relative or incremental model fit indices. These were the normed Chi square (x2/df), Goodness of Fit Index (GFI), Root Mean Residual (RMR), Root Mean Square Error of Approximation (RMSEA), Comparative Fit Index (CFI), Normed Fit Index (NFI) and Tucker Lewis Index (TLI). The detailed evaluation criterion are provided in .

Table 2. Fit evaluation for the structural model.

Convergent validity was examined using the Average Variance Explained (AVE < 0.5). AVE is the mean of the sum of squared factor loadings measuring a latent factor (Hair et al., Citation2019). An AVE of 0.5 indicates that each observed variable or item explains at least 50% of the variance in the latent factor. Discriminant validity was examined using the Fornell & Larcker (Citation1981) criterion. Based on the measure, the square root of the AVE should be greater than any correlations between a construct and any other in the model. The Maximum Shared Variance (MSV) was also compared with the AVE. MSV should be smaller than AVE to establish discriminant validity (Hair et al., Citation2019). Internal consistency was examined using Cronbach Alpha and Composite Reliability. A threshold of 0.7 has been a rule of thumb for both measures in extant literature. Common Methods Variance was examined using Harman’s single factor test through an unrotated factor solution in Exploratory Factor Analysis (EFA) (Hair et al., Citation2010; Podsakoff et al., Citation2003).

Covariance Based Structural Equation Modelling (CB-SEM) in AMOS (21) was employed to enable model estimation and examination of structural relations in the proposed model. SEM is an advanced, parametric examination method employing regression analysis, path analysis and Confirmatory Factor Analysis to predict model parameters and test hypotheses (Kline, Citation2023). The objectives of the study were to test causal relationships in a hypothesized model therefore SEM was employed. Further, SEM provides researchers with the ability to concurrently estimate relationships between exogenous and all endogenous variables, producing detailed and reliable parameters than methods such as regression analysis. A maximum likelihood method was employed and at 95% Confidence Interval, t-values greater than +1.96 and p-values less than 0.05 were used to denote positive and statistically significant relationships.

4. Results and discussion

4.1. Sample characterisation

The questionnaires that were hand delivered to respondents were 315 and 282 were returned, a response rate of 89.52%. There were 21 multivariate outliers that were discarded in preliminary analysis and 261 valid responses were retained for further analyses. The main demographic highlights were that 56.7% were females, 61.3% were aged between 18 and 35 years, 51.7% were formally employed and 64.8% had bachelor’s degree education. shows the socio-demographic profile for the study.

Table 3. Demographic profile.

4.2. Assessment of the measurement model

The purpose of Confirmatory Factor Analysis (CFA) was to evaluate whether the hypothesised factor structure well represented the latent constructs or not (Kline, Citation2023). Confirmatory Factor Analysis examines a priori hypothesised measurement model of the relationships between the indicator observed variables and the latent constructs (Kline, Citation2023; Schumacker & Lomax, Citation2010). The 4 latent constructs were developed in a CFA model, with 10 observed items for internet banking service quality, 6 for e-customer satisfaction, 5 for e-word of mouth and 4 for e-customer retention. Using maximum likelihood estimation, all observed variables produced good and significant loadings above 0.5 (Hair et al., Citation2019). This indicates that the correlation between the latent constructs and their indicators was at least 0.5 (at least 50% shared variance).

After satisfying unidimensionality, the model fit was examined to check the discrepancy of the hypothesized factor structure from the sample data. The CFA model obtained a very good fit (x2/df = 1.856; GFI = 0.916; RMR = 0.04; RMSEA = 0.05; TLI = 0.955; CFI = 0.963; NFI = 0.924. According to Schumacker and Lomax (Citation2010), x2/df should range between 1 and 5 (smaller means better fit), GFI should be at least 0.9 (0.95 indicates perfect fit), CFI should be at least 0.9 (0.95 indicates perfect fit), TLI should be at least 0.9 (0.95 confirms perfect fit), NFI should be at least 0.9 (0.95 indicates perfect fit). Further, RMSEA should be below 0.08 where 0.05 is a good fit and 0.01 indicates perfect fit. RMR as well should be below 0.08 and the closer to 0, the better fit (Kline, Citation2023). There were no theoretically supported suggestions from the modification indices nor the standardized residual covariance matrix to respecify the measurement model.

To examine Common Methods Variance, the unrotated factor solution through an EFA procedure was used (Hair et al., Citation2019). The results indicated that no factor accounted for 50% of the total variance (Podsakoff et al., Citation2003). Construct validity was examined using the Average Variance Extracted (AVE) and scores ranged from 0.591 to 0.753. By the recommendations of Hair et al. (Hair et al., Citation2019), AVEs should be at least 0.5 and Composite Reliability (CR) should be greater than AVE to confirm convergent validity. These requirements were satisfied. The Squared Multiple Correlations (SMC) were also greater than 0.25 (Hair et al., Citation2019), thus convergent validity was present.

Discriminant validity was examined using the comparison between the Maximum Shared Variance (MSV) and AVE. The MSV is the square of the highest correlation of a construct and any other in the model. According to Hair et al. (Citation2019), MSV < AVE to confirm discriminant validity, this condition was satisfied as shown in . More so, the Fornell & Larcker (Citation1981) criteria was also used. The square root of the AVEs of latent constructs in the model were greater than any inter-correlations between the constructs (Fornell & Larcker, Citation1981) as shown in .

Table 4. Discriminant validity: the Fornell-Larcker criterion.

Reliability (internal consistency) was examined using Cronbach alpha (CA) and Composite Reliability (CR). The lowest alpha value was 0.919 (E-word of mouth) and the highest was 0.940 (Internet banking service quality). Composite reliability also ranged between 0.923 (E-word of mouth) to 0.935 (Internet banking service quality). Thus, guided by Hair et al. (Citation2019), the minimum requirement of 0.7 for both measures was satisfied. The psychometric properties of the measurement model are shown in .

Table 5. Psychometric properties of the measurement model.

4.3. Structural equation modelling and hypothesis testing

Prior to SEM, normality was examined using skewness and kurtosis. Skewness and Kurtosis values were in the range of c1.96 to +1.96 and –7 to +7, respectively (Hair et al., Citation2019; Kline, Citation2023), hence the assumption was not violated. Using Maximum likelihood estimation, SEM was used to examine the structural relationships in the hypothesized model. The results of the model fit for the structural model are shown in . According to Hair et al. (Citation2019) and Schumacker and Lomax (Citation2010) the model attained a very good fit.

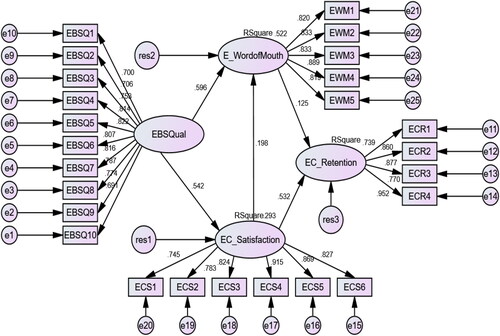

The structural model examined the proposed relationships between e-banking service quality, e-customer satisfaction, e-word of mouth and e-customer retention. shows the structural model.

Figure 2. The structural model. The path diagram shows standardized estimates. Source: Survey data.

The path estimate between e-banking service quality and e-customer satisfaction was positive and statistically significant (β = 0.542, t-value= 8.032, p < .001). The estimate between e-banking service quality and e-word of mouth was also positive and significant (β = 0.596, C.R/t = 8.260, p < .001). More so, we examined the causal link between e-customer satisfaction and e-word of mouth and the result was positive and statistically significant (β = 0.198 C.R/t = 3.263, p = .001). These relationships were statistically significant, hence hypotheses H1, H2 and H3 were supported. The study also proposed that e-word of mouth positively influences e-customer retention in internet banking. This relationship gained empirical support. Lastly, the path between e-customer satisfaction and e-customer retention was positive and statistically significant (β = 0.532, C.R/t = 7.732, p < .001). Thus, given these findings, hypotheses H4 and H5 were also supported. shows the outcomes of hypothesis testing.

Table 6. Results of hypothesis testing.

4.4. Discussion of findings

The study examined the relationships between internet banking service quality, e-customer satisfaction, e-word of mouth and e-customer retention in the context of e-banking in Bindura, Zimbabwe. In H1, the study had proposed that e-banking service quality has a positive and significant effect on e-customer satisfaction. Results from SEM (β = 0.542, t = 8.032, p < .001) supported this relationship and H1 was accepted. This confirms the importance of efficiency, site organization, security and contact, service reliability and e-responsiveness in internet banking (R2 = 0.293). These results support those of Al-Hawari (Citation2014), Amin (Citation2016), Bala et al. (Citation2021), and Ui Haq and Awan (Citation2020). Contrastingly, key scholars argue that the relationship between service quality and customer satisfaction is contextual and often spurious hence it is difficult to delineate the antecedent and outcome variables eg Cronin and Taylor (Citation1992), Cronin et al. (Citation2000) and Gronroos (Citation2002). Their arguments have influenced major departures in the conceptualization and operationalization of service quality over the years.

The findings of this study also support the influence of e-banking service quality on e-word of mouth (β = 0.596, t = 8.260, p < .001), hence we accepted H2. This supports the view that customers who experience online e-banking quality that meets their performance expectations have a high propensity to share their delightful experiences with their friends, relatives and even on peer to peer (P2P) chatrooms, website reviews and social media recommendations. This is consistent with previous research studies (Chowdhury et al., Citation2022; Timoshenko & Hauser, Citation2019; Yen & Tang, Citation2019). More so, they support the expectancy-disconfirmation theory (Oliver, Citation1980) to confirm that high perceived service quality leads to positive future behavioral intent.

The results also confirm that e-customer satisfaction has a positive and significant effect e-word of mouth (β = 0.198, t = 3.263, p = .001), thus H3 was accepted. Satisfied customers share voluntary and positive e-word of mouth recommendations with customers seeking product recommendations. The current study augment the findings of Gvili and Levy (Citation2018), Hajli (Citation2014), Naeem (Citation2019) and Naeem and Ozuem (Citation2021). The importance on e-banking service quality and e-customer satisfaction on e-word of mouth was confirmed (R2 = 0.522). However, the relationship between e-customer satisfaction and e-word of mouth is also confounded by loyalty intent (Dangaiso et al., Citation2022; Manyanga et al., Citation2022).

This study also predicted that word of mouth via online platforms such as bank websites, personal blogs and official bank social networks positively influences e-customer retention (H4). Outcomes of SEM (β = 0.125, t = 2.102, p = .04) influenced the support for H4. In support of the disconfirmation theory (Oliver, Citation1980), the study shows that positive disconfirmation brings positive post experience behaviors such as sharing reviews, positive service ratings, testimonials and loyalty intent. Further, concurrent with Manyanga et al. (Citation2022), Naeem and Ozuem (Citation2021) and Suganya et al. (Citation2018), these findings add to the literature the interesting role of e-word of mouth in internet banking from a pre-emerging economy. However, Naeem (Citation2019) warns that customers have privacy reservations for giving out e-word of mouth on their financial information and banking experiences, limiting its application in e-banking.

In H5, the study proposed that e-customer satisfaction has a positive and significant influence on e-customer retention. The results confirm that this relationship was confirmed (β = 0.532, t = 7.732, p < .001), hence H5 was accepted. The key proposition in the expectancy-disconfirmation theory (Oliver, Citation1980) was supported. Prior research has shown that customer satisfaction is a key antecedent to customer loyalty behaviors eg Amin (Citation2016), Al-Hawari (Citation2014), Chowdhury et al. (Citation2022), Khan and Alhumoudi (Citation2022) and Ui Haq and Awan (Citation2020). However, Dahlstrom et al. (Citation2014) reiterate that the effect of customer satisfaction on retention is weak if there is a high perceived risk. Given this, the delicate relationship of Zimbabwean banks and their customers cannot be overlooked. Effective relationship marketing imperatives are key to nuetralise their effect of perceived risk and augment e-customer satisfaction in building sustainable customer retention.

These findings have important connotations to the future of e-banking in Zimbabwe in the post COVID-19 era. Although Zimbabwean banks gained significant adoption leverage through COVID-19, it is important to note that the post pandemic customer experience with e-banking will be only determined by the perceived internet banking service quality. This implies that banks should maintain and continuously improve the way they interact with customers online so that they attain e-customer satisfaction, e-word of mouth and customer retention. Of note to Zimbabwean banks is how their customers still use brick and mortar banking, perhaps it provides further insight into the different levels of customer experience between physical and online servicescapes. The future of banking lies with digital services, thus, Zimbabwean banks should foster service reliability, availability, security, site organization, efficiency and responsiveness across their online service platforms.

5. Conclusions, implications and future research

5.1. Conclusions

The aim of the study was to determine the influence of internet banking service quality on e-customer satisfaction, e-word of mouth and customer retention in the post COVID-19 pandemic era in Zimbabwe. Based on 261 valid samples, the study concluded that although the adoption of e-banking leveraged on COVID-19 social decongestion regulations, banks maintained adequate levels of service quality as evidenced by the positive outcomes of our structural model. E-customer retention was positively influenced by internet banking service quality, e-customer satisfaction and e-word of mouth in the post pandemic period in Zimbabwe.

5.2. Managerial implications and recommendations

The study brings important implications to the financial services industry in Zimbabwe post the COVID-19 pandemic. In light of the above findings, banks need to continuously support internet-banking services with a seamless technology infrastructure that comes with high-speed processing, availability, reliability, e-security and privacy, customer support and site organization. If banks heavily invest in high-end e-banking applications, software programs and Information Communication Technologies (ICT) to automate customer support, this has huge potential to enhance customer experience and service quality. Banks should utilize internet-banking servicescapes to improve e-customer satisfaction, e-customer experience and build strong value laden e-customer relationships.

The study also recommends that banks should educate their e-customers on the internet banking journey. Most consumers in pre-emerging markets encounter service failure because they do not fully know how to use the service. Further, banks should simplify the product design and make transacting easy to follow. The design should be user friendly and feature rich. Internet banking platforms should have easy to follow guides on how to navigate the customer journey from; 1. Website/Application home screen, 2. Money transfer list, 3. Transfer information, 4. Transaction confirmation, 5. Password, 6. OTP Authentication, 7. Transaction notification. This a typical customer journey mapping with e-transactions and to enhance customer experience and satisfaction, easy to follow training manual guides should be employed.

Banks should also utilize big data and analytics to effectively study their segments and individual behaviors online. Big data analytics provides the bank with an opportunity to make a virtual 360° tour of their internet banking services users. This enables detailed development of customer profiles based on their transaction history, personal habits, incomes and expenses, lifestyles and other demographic traits that inform their online behaviors. Big data analytics also allows banks to segment and target its offerings which are tailor made to suit personal needs. This strategy utilizes customer information to improve banking experience and customer satisfaction.

Banks should leverage their social media strategy to expedite customer engagement on social media platforms. Further, internet-banking websites should encourage customer to give feedback through reviews. This provides an online channel for customers to convey feedback about their internet banking experiences. Delighted customers spread positive e-word of mouth to bank prospects. Social media should also be used to augment customer support. Engagement with customers provides assurance and motivation to new customers and skeptical segments into using e-services. Banks should use customer feedback from social media as a springboard for improving internet banking service quality and hence customer satisfaction and retention.

Banks should also prioritize an integrated omnichannel experience that connects operational synergies in both online and offline platforms eg websites, mobile apps, call centres, branches and USSD platforms. A sizeable proportion of customers in developing countries like Zimbabwe are still enduring a cultural transition from physical banking to e-banking services. To effectively manage this customer transition in the post COVID-19 era, banks should seek to achieve customer satisfaction by fostering continuous improvement in both online and offline servicescapes. This would improve overall customer satisfaction and customer retention over a wide spectrum of banking products and services.

The study also recommends that banks should automate digital customer support. To effectively develop online relationships with customers, bank should move from traditional customer support to chatbots and Customer Relationship Management (CRM) tools and automation that can effectively handle customer queries. As customer queries expand, manual work can be difficult, repetitive, time and resource consuming. Automating customer service adds an additional layer of competitive advantage for internet banking.

5.3. Limitations and future research

This paper examined a proposed model that accounted for 73.9% of the variability in e-customer retention in internet banking services. Future studies may incorporate variables such as perceived value, e-trust and perceived risk to improve the explanatory power of the model. More so, this research evaluated causal relationships between e-banking service quality, e-customer satisfaction, e-word of mouth and e-customer retention. Future studies may focus on an integrated services framework, in both online and offline servicescapes, so that a holistic approach can be adopted to enhance customer retention, profitability and growth across all service domains.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The materials and data used in this research will be availed by the authors upon a reasonable request.

Additional information

Funding

Notes on contributors

Phillip Dangaiso

Phillip Dangaiso is a full-time Marketing lecturer and published author at Chinhoyi University of Technology, Zimbabwe.

Paul Mukucha

Paul Mukucha (PhD) is a senior Marketing lecturer and accomplished researcher at Bindura University of Science Education (BUSE), Zimbabwe.

Forbes Makudza

Forbes Makudza is a seasoned author and senior Marketing lecturer at University of Zimbabwe (UZ). Group research interests include service quality, management of servicecapes, digital banking, marketing of financial services and digital marketing.

Tendai Towo

Tendai Towo is a full-time Banking and Finance lecturer and published author at BUSE.

Knowledge Jonasi

Knowledge Jonasi is a full-time Banking and Finance lecturer and published author at BUSE.

Divaries Cosmas Jaravaza

Divaries C. Jaravaza (PhD) is a senior Marketing lecturer and accomplished researcher at Bindura University of Science Education (BUSE), Zimbabwe.

References

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 1–19. https://doi.org/10.1016/0749-5978(91)90020-T

- Al-Hawari, M. (2014). Does customer sociability matter? Differences in e-quality, e-satisfaction, and e-loyalty between introvert and extravert online banking users. Journal of Services Marketing, 28(7), 538–546.

- Amin, M. (2016). Internet banking service quality and its implication on e-customer satisfaction and e-customer loyalty. International Journal of Bank Marketing, 34(3), 280–306. https://doi.org/10.1108/IJBM-10-2014-0139

- Anderson, R. E., & Srinivasan, S. S. (2003). E-satisfaction and e-loyalty: a contingency framework. Psychology & Marketing, 20(2), 123–138. https://doi.org/10.1002/mar.10063

- Bala, T., Jahan, I., Amin, M. A., Tanin, M. H., Islam, M. F., Rahman, M. M., & Khatun, T. (2021). Service quality and customer satisfaction of Mobile banking during COVID-19 lockdown: evidence from rural area of Bangladesh. Open Journal of Business and Management, 09(05), 2329–2357. https://doi.org/10.4236/ojbm.2021.95126

- Benjarongrat, P., & Neal, M. (2017). Exploring the service profit chain in a Thai bank. Asia Pacific Journal of Marketing and Logistics, 29(2), 432–452. https://doi.org/10.1108/APJML-03-2016-0061

- CBZ. (2021). COVID-19’S impact on the banking sector in Zimbabwe. https://www.finance-monthly.com/2021/08/covid-19s-impact-on-the-banking-sector-in-zimbabwe-from-an-hr-perspective/

- Chavda, V. (2021). Effectiveness of e-banking during the COVID-19 pandemic. IJARCCE, 10(10), October 2021. https://doi.org/10.17148/IJARCCE.2021.101001

- Chowdhury, S. A., Islam, S., Haque, S., Chowdhury, M. S. R., & Hossain, M. E. (2022). Customer trust in e-banking during COVID-19 in Bangladesh. Indian Journal of Finance and Banking, 10(1), 45–53. https://doi.org/10.46281/ijfb.v10i1.1772

- Cronin, J. J. J., Brady, M. K., & Hult, G. T. M. (2000). Assessing the effects of quality, value, and customer satisfaction on consumer behavioral intentions in service environments. Journal of Retailing, 76(2), 193–218. https://doi.org/10.1016/S0022-4359(00)00028-2

- Cronin, J. J. J., & Taylor, S. A. (1992). Measuring service quality: a reexamination and extension. Journal of Marketing, 56(3), 55–68. https://doi.org/10.1177/002224299205600304

- Dahlstrom, R., Nygaard, A., Kimasheva, M., & Ulvnes, A. M. (2014). How to recover trust in the banking industry? A game theory approach to empirical analyses of bank and corporate customer relationships. International Journal of Bank Marketing, 32(4), 268–278. https://doi.org/10.1108/IJBM-03-2014-0042

- Dangaiso, P., & Makudza, F. (2022). The influence of electronic learning service quality on student satisfaction: evidence from Zimbabwean public universities. Social Sciences and Education Research Review, 9(2), 148–158. https://doi.org/10.5281/zenodo.7474398

- Dangaiso, P., Makudza, F., & Hogo, H. (2022). Modelling perceived e-learning service quality, student satisfaction and loyalty. A higher education perspective. Cogent Education, 9(1), 2145805. https://doi.org/10.1080/2331186X.20222145805

- Davies, F. D. (1989). Perceived usefulness, perceived ease of use and user acceptance of information technology. MIS Quarterly, 13(4), 313–339. https://doi.org/10.2307/249008

- Dlamini, B., & Mbira, L. (2017). View metadata, citation and similar papers at core.ac.uk. Journal of Economics and Behavioral Studies, 9(3(J), 212–219. https://doi.org/10.22610/jebs.v9i3.1760

- Ezechirinum, A., Anucha, V. C., & Leslie, B. O. (2020). Internet banking service quality and customer retention in deposit money banks in Rivers Sate Nigeria. British Journal of Marketing Studies, 8(3), 29–53.

- Fornell, C., & Larcker, D. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.2307/3150980

- Fullerton, G., & Taylor, S. (2015). Dissatisfaction and violation: two distinct consequences of the wait experience. Journal of Service Theory and Practice, 25(1), 31–50. https://doi.org/10.1108/JSTP-10-2013-0237

- Gronroos, C. (2002). Service management and marketing. John Wiley & Sons.

- Gvili, Y., & Levy, S. (2018). Consumer engagement with eWOM on social Media: the role of social capital. Online Information Review, 42(4), 482–505. https://doi.org/10.1108/OIR-05-2017-0158

- Hair, J. F., Black, W. C., Babin, B., & Anderson, R. E. (2010). Multivariate data analysis (7th ed.). Prentice Hall Upper Saddle River.

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2019). Multivariate data analysis (8th ed.). Cengage.

- Hajli, M. N. (2014). A study of the impact of social network on consumers. International Journal of Market Research, 56(3), 387–404. https://doi.org/10.2501/IJMR-2014-025

- Herington, C., & Weaven, S. (2009). E-retailing by banks: e-service quality and its importance to customer satisfaction. European Journal of Marketing, 43(9/10), 1220–1231. https://doi.org/10.1108/03090560910976456

- Indrasari, A., Nadjmie, N., & Endri, E. (2022). Determinants of satisfaction and loyalty of e-banking users during the COVID-19 pandemic. International Journal of Data and Network Science, 6(2), 497–508. https://doi.org/10.5267/j.ijdns.2021.12.004

- International Monetary Fund. (2022). Staff Country Reports: Zimbabwe: 2022. https://www.imf.org/en/Publications/CR/Issues/2022/04/08/Zimbabwe-2022-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-by-the-516378

- IOBZ. (2022). Digital transaction banking security in Zimbabwe. https://www.iobz.co.zw/

- Jairus, M. N. (2016). Effect of Electronic Banking on Customer Retention in Commercial Banks in Nakuru Town. International Journal of Science Research, 7(5), 1354–1358. https://doi.org/10.21275/ART20182454

- Jayawardhena, C. (2004). Measurement of service quality in internet banking: the development of an instrument. Journal of Marketing Management, 20(1-2), 185–207. https://doi.org/10.1362/026725704773041177

- Kavitha, D. H., & Gopinath, D. R. (2020). Effect of service quality on satisfaction and word-of-mouth: small scale industries and their commercial banks in Tamil Nadu. International Journal of Management, 11(11), 3034–3043. https://doi.org/10.34218/IJM.11.11.2020.288

- Khan, F. N., Arshad, M. U., & Munir, M. (2023). Impact of e-service quality on e-loyalty of online banking customers in Pakistan during the Covid-19 pandemic: mediating role of e-satisfaction. Future Business Journal, 9(1), 23. https://doi.org/10.1186/s43093-023-00201-8

- Khan, M. A., & Alhumoudi, H. A. (2022). Performance of E-banking and the mediating effect of customer satisfaction: A structural equation model approach. Sustainability, 14(12), 7224.

- Kline, R. B. (2023). Principles and practice of structural equation modelling (5th ed.). The Guilford Press.

- Kotler, P., & Armstrong, G. (2018). Principles of marketing. (17th ed.). Pearson.

- Leung, L. S. K. (2020). The impact of diurnal preferences on customer satisfaction, word of mouth and repurchasing: A study in Indian college online shoppers. Asia-Pacific Journal of Management Research and Innovation, 16(1), 21–30. https://doi.org/10.1177/2319510X19897455

- Madziro, N., & Ncube, H. (2021). Evaluating adoption of electronic banking (e-banking) during the COVID-19 era: a discourse of barriers facing banking clients in the Zimbabwean context. Global Scientific Journals, 9(3). www.globalscientificjournal.com

- Makudza, F. (2021). Augmenting customer loyalty through customer experience management in the banking industry. Journal of Asian Business and Economic Studies, 28(3), 191–203. https://doi.org/10.1108/JABES-01-2020-0007

- Makudza, F., Sandada, M., & Madzikanda, D. (2021). Augmenting social commerce acceptance through an all-inclusive approach to social commerce drivers. evidence from the hotel industry. Malaysian E Commerce Journal, 5(2), 55–63. https://doi.org/10.26480/mecj.02.2021.55.63

- Makudza, F., Sandada, M., & Madzikanda, D. D. (2022). Modelling social commerce buying behaviour: an adaption of the sequential consumer decision making model. Management Research and Practice, 14(1), 17–19.

- Malhotra, N. K. (2011). Marketing research: An applied approach. Pearson Education.

- Manohar, S., Mittal, A., & Marwah, S. (2020). Service innovation, corporate reputation and word-of-mouth in the banking sector: A test on multigroup-moderated mediation effect. Benchmarking, 27(1), 406–429. https://doi.org/10.1108/BIJ-05-2019-0217

- Manyanga, W., Makanyeza, C., & Muranda, Z. (2022). The effect of customer experience, customer satisfaction and word of mouth intention on customer loyalty: The moderating role of consumer demographics. Cogent Business & Management, 9(1), 2082015. https://doi.org/10.1080/23311975.2022.2082015

- Mavaza, T. (2019). E-banking adoption by Zimbabwean banks: an exploratory study. PM World Journal, 8(11), 1–10.

- Mbama, C. I., & Ezepue, P. O. (2018). Digital banking, customer experience and bank financial performance: UK customers’ perceptions. International Journal of Bank Marketing, 36(2), 230–255. https://doi.org/10.1108/IJBM-11-2016-0181

- Morgan, R., & Hunt, S. (1994). The commitment-trust theory of relationship marketing. Journal of Marketing, 58(3), 20–38. https://doi.org/10.2307/1252308

- Naeem, M. (2019). Do social networking platforms promote service quality and purchase intention of customers of service-providing organizations? Journal of Management Development, 38(7), 561–581. https://doi.org/10.1108/JMD-11-2018-0327

- Naeem, M., & Ozuem, W. (2021). The role of social media in internet banking transition during COVID-19 pandemic: Using multiple methods and sources in qualitative research. Journal of Retailing and Consumer Services, 60, 102483. https://doi.org/10.1016/j.jretconser.2021.102483

- Nyamutowa, C., & Masunda, S. (2013). An analysis of credit risk a management practises in commercial banking institutions in Zimbabwe. International Journal of Economics Research, 4(1), 31–46. www.ijeronline.com

- Nyoka, C. (2022). Banks and the fallacy of supervision: the case for Zimbabwe. Banks and Bank Systems, 10(3), 8–17.

- Oliver, R. L. (1980). A cognitive model of the antecedents and consequences of satisfaction decisions. Journal of Marketing Research, 17(4), 460–469. https://doi.org/10.2307/3150499

- Parasuraman, A., Zeithaml, V. A., & Malhotra, A. (2005). ES-QUAL a multiple-item scale for assessing electronic service quality. Journal of Service Research, 7(3), 213–233. https://doi.org/10.1177/1094670504271156

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioural research: A critical review of literature and recommended remedies. The Journal of Applied Psychology, 88(5), 879–903. https://doi.org/10.1037/0021-9010.88.5.879

- Rachbini, W., Anggraeni, D., & Wulanjani, H. (2021). The influence of electronic service quality and electronic word of mouth (eWOM) toward repurchase intention (study on e-commerce in Indonesia). Jurnal Komunikasi, 37(1), 42–58. https://doi.org/10.17576/JKMJC-2021-3701-03

- Reserve Bank of Zimbabwe. (2019). 2019 annual report. https://www.rbz.co.zw/index.php/publications-notices/publications/annual-reports/743-2019-annual-report

- Roux, P. L., & Abel, S. (2017). An evaluation of the efficiency of the banking sector in Zimbabwe. African Review of Economics and Finance, 9(2), 285–307.

- Samosir, J., Purba, O. R., Ricardianto, P., Dinda, M., Rafi, S., Sinta, A. K., Wardhana, A., Anggara, D. C., Trisanto, F., & Endri, E. (2023). The role of social media marketing and brand equity on e-WOM: Evidence from Indonesia. International Journal of Data and Network Science, 7(2), 609–626. https://doi.org/10.5267/j.ijdns.2023.3.010

- Sathiyavany, N., & Shivany, S. (2018). E-banking service qualities, E-customer satisfaction, and e-loyalty: A conceptual model. International Journal of Social Sciences and Humanities Invention, 5(6), 4808–4819. https://doi.org/10.18535/ijsshi/v5i6.08

- Schumacker, R. E., & Lomax, R. G. (2010). A Begginner’s guide to structural equation modeling. Routledge.

- Shankar, A., & Jebarajakirthy, C. (2019). The influence of e-banking service quality on customer loyalty: A moderated mediation approach. International Journal of Bank Marketing, 37(5), 1119–1142. https://doi.org/10.1108/IJBM-03-2018-0063

- Sudarsono, H., Nugrohowati, R. N. I., & Tumewang, Y. K. (2020). The effect of COVID-19 pandemic on the adoption of internet banking in Indonesia: Islamic bank and conventional bank. The Journal of Asian Finance, Economics and Business, 7(11), 789–800. https://doi.org/10.13106/jafeb.2020.vol7.no11.789

- Suganya, A., Theresha, M., Figurado, Q., Fernando, G., Lathursha, S., Sinduja, K., & Shivany, S. (2018). The electronic word of mouth and customer retention t retail stores in Jaffna Market. International Conference on Advanced Marketing.

- Timoshenko, A., & Hauser, J. R. (2019). Identifying customer needs from user-generated content. Marketing Science, 38(1), 1–20. https://doi.org/10.1287/mksc.2018.1123

- Torabi, M., & Bélanger, C. H. (2021). Influence of online reviews on student satisfaction seen through a service quality model. Journal of Theoretical and Applied Electronic Commerce Research, 16(7), 3063–3077. https://doi.org/10.3390/jtaer16070167

- Ui Haq, I., & Awan, T. M. (2020). Impact of e-banking service quality on e-loyalty in pandemic times through the interplay of satisfaction. Journal of Management Development, 17(1/2), 39–55. https://doi.org/10.1108/XJM-07-2020-0039

- van Tonder, E., Petzer, D. J., van Vuuren, N., & De Beer, L. T. (2018). Perceived value, relationship quality and positive WOM intention in banking. International Journal of Bank Marketing, 36(7), 1347–1366. https://doi.org/10.1108/IJBM-08-2017-0171

- Venkatesh, V., Morris, M. G., Davis, G. B., Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27(3), 425. https://doi.org/10.2307/30036540

- World Bank. (2021). Monitoring COVID-19 impact on households in Zimbabwe, Report No. 2: results from a high-frequency telephone survey of households. World Bank.

- Yen, C. A., & Tang, C. H. (2019). The effects of hotel attribute performance on electronic word-of- mouth (eWOM) behaviors. International Journal of Hospitality Management, 76(1), 9–18. https://doi.org/10.1016/j.ijhm.2018.03.006

- Zeithaml, V. A., Parasuraman, A., & Malhotra, A. (2002). Service quality delivery through web sites: a critical review of extant knowledge. Journal of the Academy of Marketing Science, 30(4), 362–375. https://doi.org/10.1177/009207002236911